Immunofluorescence Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

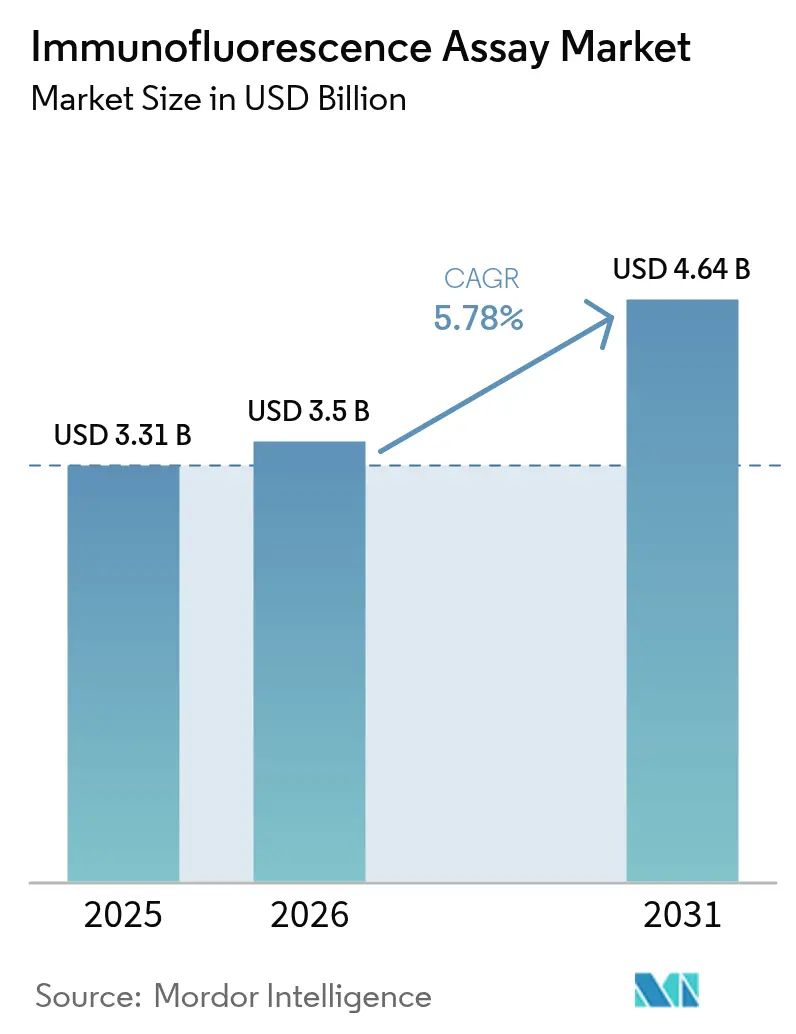

| Market Size (2026) | USD 3.5 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

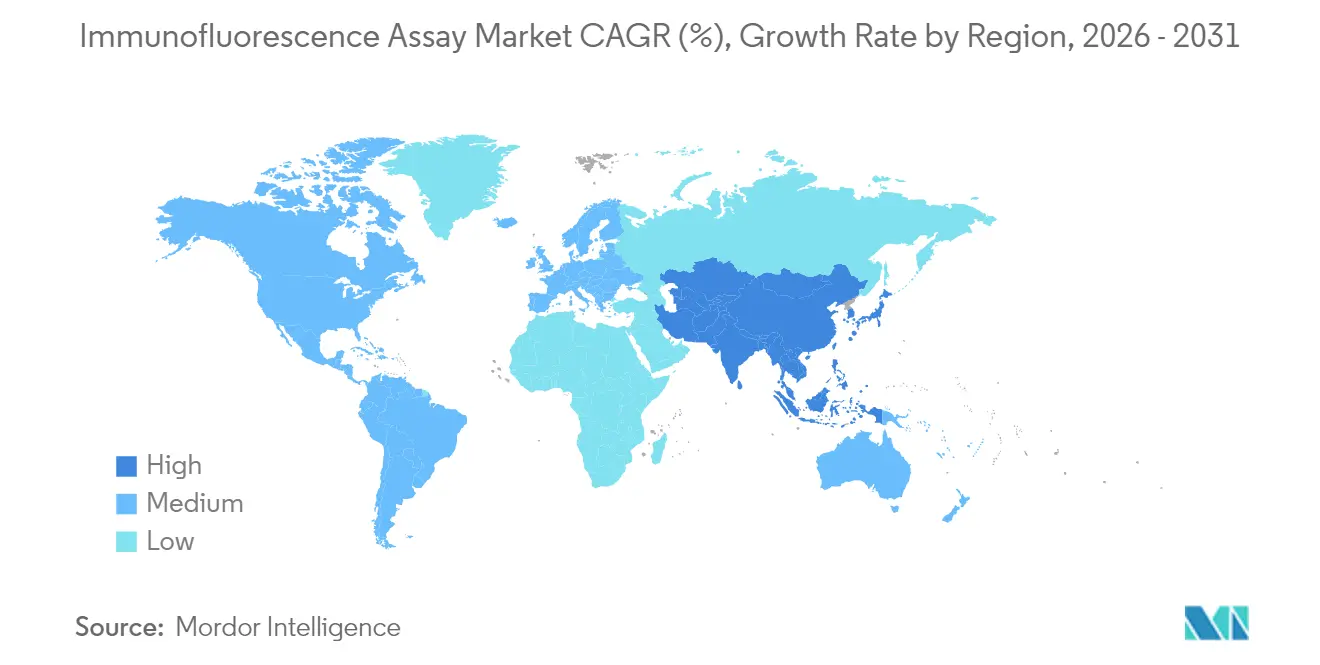

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immunofluorescence Assay Market Analysis by Mordor Intelligence

The Immunofluorescence Assay market size is expected to grow from USD 3.31 billion in 2025 to USD 3.5 billion in 2026 and is forecast to reach USD 4.64 billion by 2031 at 5.78% CAGR over 2026-2031. Growth reflects the migration from manual fluorescence microscopy to AI-enabled digital pathology systems that streamline image analysis and raise diagnostic precision.[1]Source: FDA, “Laboratory Developed Tests Regulatory Impact Analysis,” fda.gov Expansion is reinforced by the wider use of companion diagnostics in precision medicine, continued infectious-disease surveillance, and investment in microfluidic point-of-care platforms suited to resource-limited settings. Capital equipment upgrades toward automated instruments, together with large hospital groups adopting standardized laboratory-developed test protocols, further propel the immunofluorescence assay market. However, cost pressure from advanced microscopes and tightened disposal rules on PFAS-based fluorophores temper near-term adoption.

Key Report Takeaways

- By product, reagents and kits led with 61.45% revenue share in 2025, while instruments are projected to post the fastest 6.84% CAGR through 2031.

- By immunofluorescence type, indirect methods accounted for 64.90% of the immunofluorescence assay market share in 2025; direct methods are poised to expand at a 6.12% CAGR.

- By application, infectious-disease testing captured 45.10% of immunofluorescence assay market size in 2025; cancer diagnostics and research show the highest 6.62% CAGR to 2031.

- By end user, pharmaceutical and biotechnology companies held 42.90% share in 2025, whereas academic and research institutes record the quickest 6.98% CAGR.

- By geography, North America commanded 39.65% of immunofluorescence assay market share in 2025; Asia-Pacific is forecast to rise at a 7.14% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immunofluorescence Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Cancer and Infectious Diseases | +1.2% | Global | Medium term (2-4 years) |

| Expanding Governmental and NGO Funding | +0.8% | North America & EU, APAC emerging | Short term (≤ 2 years) |

| Growing Use of Companion Diagnostics and Precision Medicine | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Multiplex Spatial-Omics IF Platforms in Drug Discovery | +0.9% | North America & EU | Medium term (2-4 years) |

| AI-Enabled Digital Pathology Driving Decentralized IF Adoption | +1.1% | Global | Long term (≥ 4 years) |

| Microfluidic Point-Of-Care IF Kits in Emerging Markets | +0.7% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cancer and Infectious Diseases

Cancer prevalence and lingering infectious-disease burdens elevate demand for multiplex immunofluorescence platforms that detect tumor markers and pathogens in the same run. Multi-cancer early-detection tests demonstrating 95.4% accuracy showcase the value of high-sensitivity fluorescence imaging in population screening. Parallel advances in tuberculosis point-of-care assays adapted from COVID-19 workflows highlight how existing test infrastructure can be repurposed to serve broader disease-monitoring programs.[2]Source: Lydia M. L. Holtgrewe et al., “Innovative COVID-19 Point-of-Care Diagnostics,” Journal of Clinical Medicine, mdpi.com This dual-utility profile underpins the growth momentum observed across the immunofluorescence assay market.

Expanding Governmental and NGO Funding

Targeted grants and health-system modernization schemes accelerate platform rollouts, notably portable fluorescence readers that function in decentralized settings. The European Medicines Agency’s backing of novel tuberculosis diagnostics underscores a public-sector push for rapid, high-specificity tests. In the United States, the FDA estimates USD 3.51 billion annualized benefits tied to standardized laboratory-developed test oversight, encouraging labs to adopt compliant automated instruments. Such funding channels directly influence purchase decisions in the immunofluorescence assay market.

Growing Use of Companion Diagnostics and Precision Medicine

Regulators now frequently require biomarker-led patient stratification for drug approvals. Roche’s HER2 assay for biliary-tract cancer shows how fluorescence-based companion diagnostics reduce therapeutic uncertainty. AI-integrated image-analysis modules further narrow inter-reader variability, positioning digital immunofluorescence as the analytical backbone of precision oncology.

Multiplex Spatial-Omics IF Platforms in Drug Discovery

Drug developers rely on spatial-omics panels that quantify up to 8 biomarkers in preserved tissue, saving scarce samples and accelerating target validation. Workflow automation cuts manual scoring time to 7.7% of legacy whole-slide studies, freeing personnel for high-value analytical tasks. Partnerships linking flow cytometry with mutation-detection chemistry further expand the toolset available to oncology researchers. These platforms are particularly valuable for cell and gene therapy development, where understanding spatial relationships between therapeutic targets and surrounding cellular environments is essential for optimizing treatment efficacy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability Of Alternative High-Throughput Assay Formats | -0.6% | Global | Medium term (2-4 years) |

| High Capital Cost of Advanced Fluorescence Microscopes | -0.4% | Emerging markets, smaller laboratories | Short term (≤ 2 years) |

| Photobleaching & Inter-Lab Variability Hurting Trial Reproducibility | -0.3% | Global, particularly clinical trials | Long term (≥ 4 years) |

| Environmental Rules on Fluorophore/PFAS Waste | -0.2% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative High-Throughput Assay Formats

Next-generation sequencing and label-free multiphoton imaging now deliver higher multiplexing and quantitative rigor, siphoning projects that would traditionally rely on immunofluorescence. Microfluidic biosensors that work directly with body fluids further tighten competition by trimming sample volume and turnaround time.[3]Source: Abdul Rehman Haris et al., “Alternative Assay Technologies,” biomarkerresearch.net Single-cell analysis technologies are providing unprecedented insights into cellular heterogeneity and disease mechanisms, offering research capabilities that complement but may eventually supersede certain immunofluorescence applications. The integration of artificial intelligence with these alternative platforms is accelerating their adoption by reducing technical complexity and improving diagnostic accuracy, creating sustained competitive pressure on immunofluorescence market growth.

High Capital Cost of Advanced Fluorescence Microscopes

Complete AI-enabled platforms exceed USD 500,000, a level many smaller labs cannot absorb without external financing. Modularity—such as add-on spectral detectors—mitigates but does not erase the barrier, explaining slower uptake in lower-income regions. The economic impact is particularly pronounced in academic and research institutions where funding cycles and budget approval processes can delay equipment purchases for multiple years, limiting market growth potential in key customer segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Instruments Drive Technology Modernization

In 2025, reagents and kits generated 61.45% of revenue, yet instrument sales are rising fastest at 6.84% CAGR as labs pivot to automation. Platform providers couple hardware with image-analysis software in subscription bundles, smoothing cash-flow hurdles and nurturing multi-year service contracts. Upgradable spectral-flow cytometers and remote-monitored slide stainers exemplify how modular designs stretch asset lifecycles and speed return on investment.

Accessory purchases scale proportionally, covering slide loaders, calibration beads, and barcode scanners. As AI modules demand consistent illumination and precise stage control, buyers increasingly treat high-resolution objectives and environmental enclosures as integral parts of platform modernization. This ecosystem view anchors long-range procurement plans across the immunofluorescence assay market.

By Immunofluorescence Type: Direct Methods Gain Precision Medicine Traction

Indirect techniques kept 64.90% share in 2025 thanks to established autoimmune protocols, yet direct immunofluorescence exhibits stronger appetite from oncology programs requiring rapid single-step staining. Adoption climbs as pathologists value shorter assay cycles when guiding intraoperative decisions. Rising HER2-low breast-cancer testing illustrates how direct conjugates support quantitative thresholding without amplification artifacts.

Indirect methods retain importance for broad screens such as antinuclear antibody panels, leveraging HEp-2 substrates to visualize multiple autoantibody classes concurrently. Their cost-effectiveness and existing reimbursement codes ensure continued dominance in routine labs. Still, the immunofluorescence assay market anticipates incremental share migration to direct formats where turnaround and specificity trump batch economy.

By Application: Cancer Diagnostics Accelerate Through Precision Medicine

Infectious-disease testing commanded 45.10% of the immunofluorescence assay market share in 2025, built on sustained respiratory-virus surveillance networks. Yet cancer diagnostics and research, expanding at 6.62% CAGR, outpaces all other uses as targeted therapies multiply. AI-scored CD8 immunophenotyping now informs immunotherapy selection, spotlighting the central role of multiplex fluorescence in tumor-microenvironment profiling.

Autoimmune testing remains a stable pillar, bolstered by enhanced biomarker panels that detect serologically inactive lupus cases earlier. Together, these verticals maintain steady overall demand, but the incremental growth engine for the immunofluorescence assay market lies firmly in precision oncology workflows.

By End User: Academic Institutes Lead Research Innovation

Pharmaceutical and biotechnology companies represented 42.90% of revenue in 2025 and continue to drive high-value instrument demand for companion-diagnostic development. Academic and research institutes, however, post the quickest 6.98% CAGR as grant cycles prioritize multi-omics projects dependent on advanced fluorescence imaging. Their open-science ethos accelerates assay innovation, seeding future commercial applications for the immunofluorescence assay market.

Hospital and reference laboratories form the workhorse segment, focusing on throughput and lab-information-system compatibility. Contract research organizations round out demand, offering outsourced biomarker studies that absorb installed-base instruments nearing end-of-life in corporate labs.

Geography Analysis

North America held 39.65% of global revenue in 2025, benefiting from large installed bases of automated slide scanners and a supportive FDA pathway that clarifies quality-system expectations. High per-capita healthcare spending enables faster replacement cycles, and tax incentives for capital investment reduce adoption risk for mid-sized hospitals. Corporate activity, such as Thermo Fisher Scientific’s USD 3.1 billion purchase of Olink, consolidates platform portfolios and widens menu offerings, reinforcing regional leadership.

Europe follows closely, aided by stringent but predictable IVDR frameworks that encourage harmonized performance claims. The immunofluorescence assay market size for the region benefits from cross-border reimbursement pacts and Horizon Europe research funding that underwrites large biomarker consortia. Extended IVDR transition deadlines give SMEs breathing room to complete conformity assessments without halting product availability.

Asia-Pacific is the fastest-growing territory at 7.14% CAGR through 2031. China’s domestic champions, such as Autobio Diagnostics, scale high-volume analyzer production, lowering cost-per-test and expanding access in county-level hospitals. India sees indigenous firms like Meril Diagnostics tailoring microfluidic fluorescence cartridges for endemic infections, supporting double-digit rural market growth. Government-sponsored health-insurance schemes further unlock demand for decentralized diagnostics, propelling the immunofluorescence assay market across Southeast Asia.

Competitive Landscape

The market is moderately concentrated. Integrated solution plays dominate strategy: Danaher’s Leica Microsystems provides microscopes, slide scanners, and image-analysis software, while Thermo Fisher unites antibodies, fluorophores, and cloud analytics. M&A remains an essential lever; Bio-Rad’s pipeline includes validated rare-cell antibodies to complement its droplet-digital PCR instruments, strengthening multimodal assay suites.

Strategic alliances shape product roadmaps. Leica Biosystems’ 2025 investment in Indica Labs links scanner hardware with AI decision-support tools, presenting a turnkey digital pathology platform for mid-sized hospitals. BD’s collaboration with Biosero automates sample loading for flow cytometers, shrinking hands-on time and boosting throughput.

Emerging competitors concentrate on niche innovations such as PFAS-free fluorophore chemistries and AI-native software modules that retrofit onto existing microscopes. Their agility challenges incumbents’ slower release cycles and keeps the immunofluorescence assay market dynamic.

Immunofluorescence Assay Industry Leaders

Abcam

PerkinElmer Inc.

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories

Danaher (Leica Biosystems & Molecular Devices)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: A case series confirms serum anti-MOG antibodies detectable via indirect immunofluorescence but absent in cerebrospinal fluid, reinforcing the assay’s clinical utility in neuromyelitis optica spectrum disorder.

- April 2024: Creative Diagnostics launches immunofluorescence assay testing services aimed at virology research laboratories.

- June 2023: Revvity’s EUROIMMUN arm debuts the UNIQO 160 automated indirect immunofluorescence system for autoimmune disease diagnostics.

Global Immunofluorescence Assay Market Report Scope

As per the scope of the report, immunofluorescence is the specific antigen and antibody reaction where the antibodies are labeled with a fluorescent dye, and the antigen-antibody complex is visualized using a fluorescent microscope. This immunochemical technique allows the detection and localization of a wide variety of antigens in different types of tissues of various cell preparations. The immunofluorescence assay market is segmented by product (reagents and kits, instruments, consumables & accessories), type (indirect immunofluorescence, and direct immunofluorescence), application (cancer, infectious diseases, autoimmune diseases, and others), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across the major regions globally. The report offers the values (USD million) for the above segments.

| Reagents and Kits |

| Instruments |

| Accessories |

| Indirect Immunofluorescence |

| Direct Immunofluorescence |

| Cancer Diagnostics and Research |

| Infectious Disease Testing |

| Autoimmune Disease Testing |

| Others |

| Hospital and Reference Laboratories |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Reagents and Kits | |

| Instruments | ||

| Accessories | ||

| By Immunofluorescence Type | Indirect Immunofluorescence | |

| Direct Immunofluorescence | ||

| By Application | Cancer Diagnostics and Research | |

| Infectious Disease Testing | ||

| Autoimmune Disease Testing | ||

| Others | ||

| By End User | Hospital and Reference Laboratories | |

| Pharmaceutical and Biotechnology Companies | ||

| Academic and Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the immunofluorescence assay market in 2026?

Immunofluorescence assay market size stands at USD 3.5 billion in 2026, rising to USD 4.64 billion by 2031 at a 5.78% CAGR over 2026-2031.

Which product segment is growing fastest?

Instrument sales grow the quickest at a 6.84% CAGR as laboratories upgrade to AI-enabled automated platforms.

What drives Asia-Pacific growth?

Government investment in diagnostic infrastructure, expansion of point-of-care testing, and cost-efficient local manufacturing push Asia-Pacific to a 7.14% CAGR.

How do companion diagnostics influence demand?

Regulatory emphasis on biomarker-guided therapy selection boosts uptake of high-specificity immunofluorescence assays integrated into precision-medicine workflows.

What is the key restraint for smaller laboratories?

Up-front capital outlays for advanced fluorescence microscopes can exceed USD 500,000, delaying adoption among budget-constrained facilities.

Page last updated on: