Cycling Helmet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

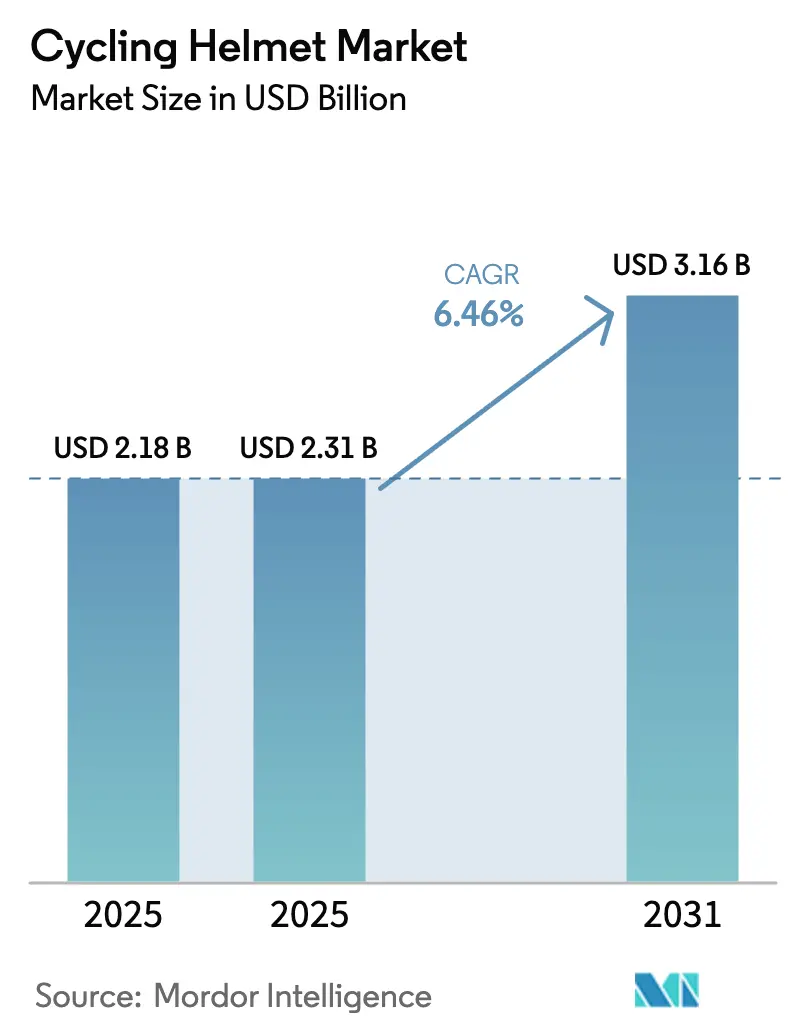

| Market Size (2025) | USD 2.31 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

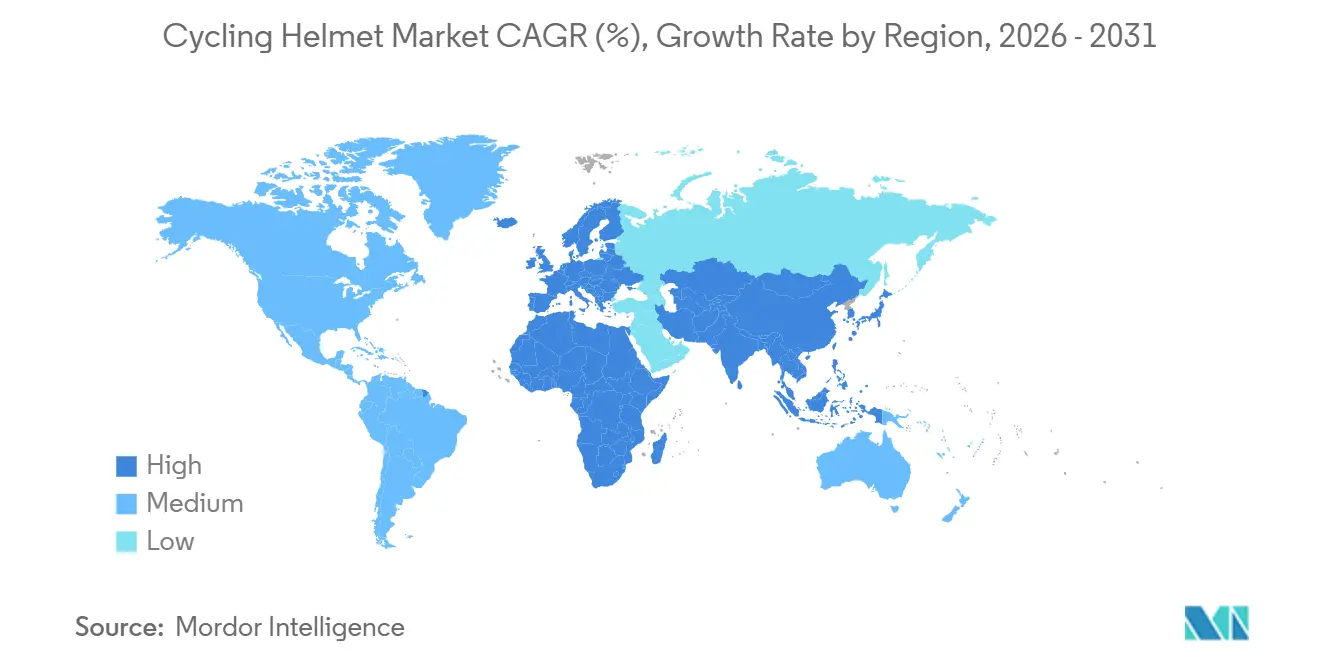

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cycling Helmet Market Analysis by Mordor Intelligence

The cycling helmet market size is projected to expand from USD 2.18 billion in 2025 and USD 2.31 billion in 2026 to USD 3.16 billion by 2031, registering a CAGR of 6.46% between 2026 to 2031. Increasing regulatory requirements, the growth of electric bike (e-bike) fleets, and significant municipal investments in dedicated cycle lanes are driving demand among both commuter and recreational rider segments. This shift is transforming head protection from a fashion-oriented discretionary purchase into an essential element of urban mobility infrastructure. Post-pandemic supply chain adjustments have optimized inventory management, while direct-to-consumer (DTC) brands have enhanced digital customer acquisition efforts, leading to greater price transparency. Efforts to combat counterfeit products and the introduction of rotational-impact technology into mid-tier price ranges are influencing consumer expectations regarding safety certifications and perceived value. The competitive landscape remains moderate, with legacy conglomerates, specialist innovators, and direct-to-consumer (DTC) entrants competing for market share, without any single company dominating the market.

Key Report Takeaways

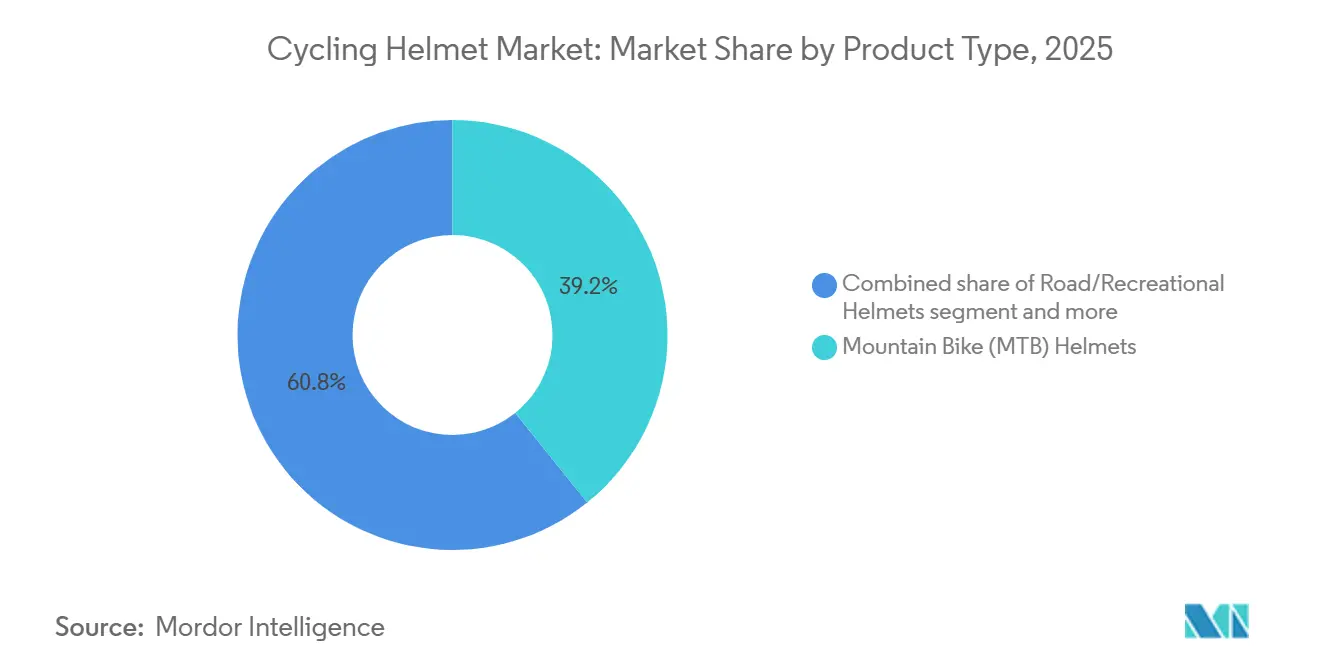

- By product type, mountain bike helmets led with 39.21% of cycling helmet market share in 2025, while road and recreational models are projected to expand at a 7.91% CAGR through 2031.

- By end user, adults accounted for 78.71% of 2025 revenue, yet the kids segment is forecast to post the fastest 7.81% CAGR through 2031.

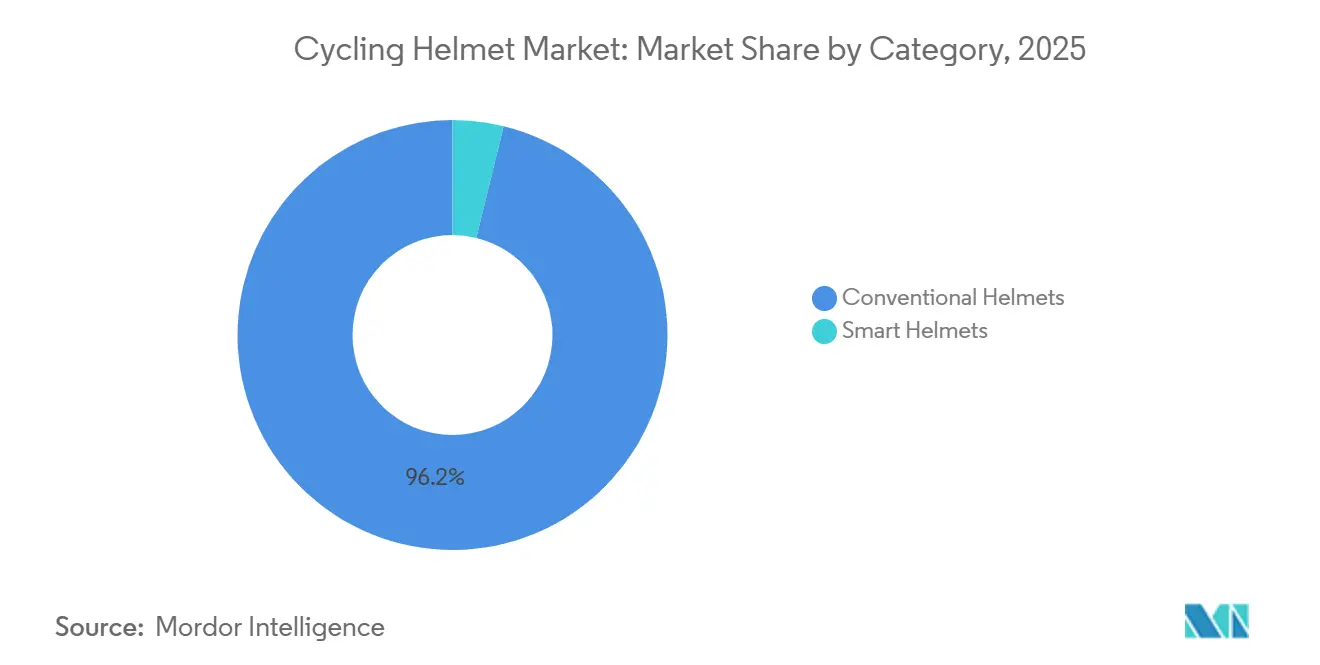

- By category, conventional models dominated with 96.17% volume in 2025; however smart variants are advancing at an 8.01% CAGR to 2031.

- By distribution channel, offline retail maintained 57.91% of 2025 sales, while online platforms are expanding at a 7.25% CAGR on the back of DTC momentum.

- By geography, Europe captured 37.21% of 2025 revenue, yet Asia-Pacific is poised to record the highest 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cycling Helmet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising safety awareness about head injury risks | +0.8% | Global, with stronger uptake in Europe and North America | Medium term (2-4 years) |

| Government regulations mandating helmet use | +1.2% | Asia-Pacific (India, China), Europe (Netherlands, select EU states), North America (state-level mandates) | Short term (≤ 2 years) |

| Public campaigns promoting cycling safety | +0.5% | Europe, North America, Australia | Medium term (2-4 years) |

| Growth in cycling for fitness and recreation | +0.9% | Global, with emphasis on North America and Europe | Long term (≥ 4 years) |

| Urban mobility trends favoring sustainable transport | +1.0% | Europe, Asia-Pacific urban corridors, select North American cities | Medium term (2-4 years) |

| E-bike adoption requiring enhanced protection | +1.3% | Asia-Pacific (China, India, Southeast Asia), Europe (Germany, Netherlands, France), North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising safety awareness about head injury risks

Epidemiological data linking cycling head injuries to long-term cognitive impairment is shaping consumer perceptions. Research shows that helmets significantly reduce the risk of head injuries, depending on the nature of the impact. Furthermore, Swedish electric bike (e-bike) riders using helmets with Release Layer Systems face a notably lower risk of head injuries compared to those who do not wear helmets. According to the World Health Organization (WHO), millions of road deaths occur annually, with pedestrians and cyclists comprising a significant proportion [1]Source: World Health Organization, “Road safety takes centre stage at world’s leading transport forum,” who.int. Public health agencies are using this data to promote helmet adoption as a public health intervention rather than merely an individual choice. Virginia Tech's helmet-safety ratings, which assess hundreds of models and assign scores, have become a recognized industry standard. These ratings influence retail placement and consumer purchasing decisions by providing a performance benchmark that translates laboratory findings into practical criteria for buyers. The American Academy of Pediatrics (AAP) has reported that millions of children ride bicycles in the United States, with a substantial number of non-fatal injuries recorded in recent years. However, helmet usage remains inadequate in the absence of mandatory laws, highlighting that awareness alone is insufficient without regulatory measures. In Sweden and the Netherlands, insurance companies are testing premium discounts for certified-helmet users. This financial incentive promotes safety awareness by linking it to economic behavior changes. Additionally, it generates actuarial data that could guide future underwriting models.

Government regulations mandating helmet use

Regulatory mandates are increasingly shifting helmet adoption from voluntary to mandatory in key growth markets. For example, India has introduced a regulation effective January 2026, requiring the sale of two Bureau of Indian Standards (BIS)-certified helmets with every new two-wheeler [2]Source: Press Information Bureau (PIB), “Centre Urges Consumers to Use Only Bureau of Indian Standards (BIS) Certified Helmets for Safety,” pib.gov.in. This policy is anticipated to drive significant demand for certified helmets and generate substantial manufacturing employment opportunities. Additionally, it aims to combat the counterfeit helmet market, where non-compliant helmets, offering inadequate protection, are produced at low costs and sold at inflated prices through dealerships. In the United States, helmet laws differ by state, with several states enforcing regulations primarily for riders under specific age thresholds. California's Assembly Bill 1774, effective in 2024, mandates helmet use for electric bike (e-bike) riders under the age of 17, reflecting a fragmented regulatory approach that creates enforcement gaps. Similarly, Australia updated its Consumer Goods Safety Standard in 2024 to enhance compliance thresholds [3]Source: Australian Competition and Consumer Commission (ACCC), “Improving mandatory product safety standards,” productsafety.gov.au. In the Netherlands, efforts are underway to promote the adoption of the NTA-8776 standard for electric bike helmets, which imposes stricter drop-test requirements compared to the conventional EN 1078 certification. These diverse regulatory frameworks pose compliance challenges for multinational brands but also create opportunities for regional specialists who can navigate local certification processes more effectively than global competitors. In India, the Ministry of Road Transport and Highways (MoRTH) conducted multiple helmet-sample tests and search and seizure operations during the previous financial year. One such operation in Delhi resulted in the seizure of a significant number of non-compliant helmets, highlighting increased regulatory enforcement efforts.

Public campaigns promoting cycling safety

Municipal and non-governmental organizations are integrating helmet promotion into broader cycling safety initiatives. For example, Copenhagen's cycling budget for 2025 includes funding for infrastructure as well as visibility campaigns aimed at normalizing helmet use through peer influence. In the Netherlands, cycling safety campaigns leverage social proof by showcasing helmet adoption among professional cyclists and commuters, addressing the perception that helmets are unnecessary in low-speed urban settings. Similarly, Manchester's five-year cycling plan for the period 2026 to 2031 and the United Kingdom's Cycling and Walking Investment Strategy 3 for the years 2025 to 2030 incorporate helmet promotion within active travel frameworks, linking public health outcomes to modal shift objectives. In the United States, North Carolina's Department of Transportation (DOT) funds its Bicycle Helmet Initiative through revenue generated from "Share the Road" license plates, illustrating how dedicated funding streams can support long-term programs beyond annual budget cycles. Additionally, Dell Children's Medical Center in Austin and the University of Michigan's Pop-up Safety Town distributed free helmets in 2024, coupled with hands-on fitting education. This approach addresses behavioral barriers to helmet adoption by integrating product training into community health initiatives. Research conducted by the Safe Transportation Research and Education Center (SafeTREC) indicates that free helmet distribution alone is insufficient without proper education on fit and maintenance. This insight has led to campaigns incorporating sizing tools and post-purchase support into distribution protocols.

Growth in cycling for fitness and recreation

The American Academy of Pediatrics reported that millions of children in the United States ride bicycles, with a significant number of non-fatal injuries recorded in 2020. However, free helmet-distribution programs alone have been insufficient to ensure sustained adoption without accompanying education on proper fit and maintenance. Research conducted by the Safe Transportation Research and Education Center (SafeTREC) found that a notable percentage of helmet returns are due to sizing and fit issues, underscoring the gap between distribution and effective usage. In 2024, Dell Children's Medical Center in Austin and the University of Michigan's Pop-up Safety Town addressed this challenge by distributing free helmets alongside hands-on fitting education. This model integrates product training into community health initiatives, addressing behavioral factors influencing helmet adoption. The North Carolina Department of Transportation funds its Bicycle Helmet Initiative through revenue generated by "Share the Road" license plates. This funding model demonstrates how earmarked revenue streams can support long-term programs independent of annual budget cycles. Additionally, the increase in youth sports participation is driving incremental demand for helmets. Brands that incorporate sizing tools, virtual try-on features, and post-purchase support into their direct-to-consumer channels are reducing return rates and building trust with safety-conscious parents, thereby increasing customer lifetime value. In developing markets, bike ownership among children is growing at a rapid annual rate. This trend presents a significant opportunity for brands that can navigate local certification requirements and offer product ranges that balance affordability with compliance standards, such as those set by the Bureau of Indian Standards or equivalent certifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced helmets | -0.9% | Global, with acute pressure in price-sensitive Asia-Pacific and South America markets | Medium term (2-4 years) |

| Comfort and fit issues for users | -0.4% | Global, particularly hot and humid climates in Asia-Pacific, Middle East, and South America | Long term (≥ 4 years) |

| Poor ventilation in hot climate | -0.3% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Counterfeit products undermining trust | -0.7% | Asia-Pacific (India, China, Southeast Asia), Middle East and Africa, select South America markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced helmets

Rotational-impact technologies, including the Multi-directional Impact Protection System (MIPS), WaveCel, and Release Layer System, contribute to higher bill-of-materials costs, leading to retail price premiums. Flagship models such as the ABUS GAMECHANGER 2.0 MIPS and MET's Trenta 3K Carbon exemplify this trend. This pricing structure has resulted in a two-tier market. Affluent consumers in Europe and North America tend to prefer helmets with advanced safety features, while price-sensitive buyers in Asia-Pacific and South America often choose basic expanded polystyrene shells that meet minimum certification standards but lack rotational protection. In India, the two-helmet mandate, which requires Bureau of Indian Standards (BIS) certification, is anticipated to slightly increase entry-level helmet prices. This is due to manufacturers needing to retool for anti-lock braking system (ABS) compatibility and front-disc upgrades. Canyon's Deflectr, which holds Virginia Tech's top safety rating, demonstrates how proprietary intellectual property can deliver premium performance at mid-market price points. However, such offerings remain exceptions rather than the norm in the category. Proposals by Indian industry stakeholders to reduce the goods and services tax (GST) on helmets could potentially accelerate the adoption of certified helmets. However, fiscal constraints in emerging markets limit the political feasibility of implementing such measures. Additionally, smart helmets face adoption challenges as consumers often weigh the benefits of connectivity against concerns over battery life and higher replacement costs.

Comfort and fit issues for users

Helmet returns are often linked to sizing and fit issues, highlighting a gap between product distribution and effective usage. This challenge is particularly evident in the youth helmet market, where significant variations in children's head shapes make standardized sizing charts inadequate. To address this, brands are adopting augmented-reality try-on tools, detailed sizing charts based on head circumference, and flexible return policies to ease purchase concerns. However, these measures lead to increased operational costs and added complexity. The American Academy of Pediatrics has noted that improper helmet fit can significantly reduce effectiveness. Loose retention systems allow helmets to shift during impacts, while overly tight straps cause discomfort, discouraging consistent use. Initiatives such as those by Dell Children's Medical Center in Austin and the University of Michigan's Pop-up Safety Town have distributed free helmets along with hands-on fitting education. These programs integrate product training into community health efforts, addressing behavioral barriers to helmet adoption. Technological advancements, including the multi-directional impact protection system and WaveCel technology, have increased helmet weight, which can be perceived as uncomfortable during prolonged use. This discomfort is particularly noticeable in hot climates, where added insulation worsens heat retention. To improve fit across diverse head shapes, manufacturers are exploring modular retention systems, adjustable padding, and gender-specific designs. However, these innovations introduce production complexities and create inventory management challenges for retailers managing multiple sizes and configurations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Trail Dominance Meets Road Acceleration

Road and recreational helmets are projected to grow at an annual rate of 7.91% through 2031, surpassing the growth of mountain bike helmets, despite the latter accounting for 39.21% of 2025 revenue. This trend is driven by urban commuters prioritizing features such as aerodynamics, weight reduction, and integrated connectivity over trail-specific impact protection. POC's Cytal Lite, launched during the 2025 Tour de France, exemplifies the premium road segment's focus on incremental performance improvements. Similarly, Giant's 2026 Pursuit Multi-directional Impact Protection System (MIPS) and Rev Pro Multi-directional Impact Protection System helmets emphasize drag reduction at high speeds and have earned Virginia Tech's 5-star safety rating. While mountain bike helmets are growing at a slower pace than the overall category, they are incorporating modular innovations. For example, Leatt's Enduro 3.0 helmet offers a three-in-one design, functioning as a full-face helmet with a removable chin bar, a half-shell, or an open-face helmet with ear covers. This design addresses the need for a balance between downhill protection and trail ventilation. Adventure helmets, positioned between road and mountain bike designs, cater to gravel riders and bikepacking enthusiasts with features such as visor compatibility, extended rear coverage, and mounting points for action cameras and lighting systems.

Canyon's December 2025 release of the Deflectr helmet introduces a patented Release Layer System, which utilizes polycarbonate bearings to significantly reduce rotational velocity compared to helmets without this system. This innovation highlights how bicycle original equipment manufacturers are leveraging vertical integration to develop proprietary safety technologies, competing with licensed solutions such as the Multi-directional Impact Protection System.

By End User: Adult Volume Versus Kids Velocity

Adults accounted for 78.71% of the revenue in 2025, while the kids' segment is projected to grow at an annual rate of 7.81% through 2031. School-based distribution programs, increased parental willingness to invest in rotational-impact technologies, and rising youth sports participation have driven initiatives such as Charlottesville's helmet distribution in June 2024. In North Carolina, the Department of Transportation funds its Bicycle Helmet Initiative through revenue generated from "Share the Road" license plates. Similarly, the University of Michigan's Pop-up Safety Town integrates free helmet distribution with hands-on fitting education, highlighting how community health programs are combining product training with distribution to address behavioral adoption challenges. Research from the Safe Transportation Research and Education Center (SafeTREC) emphasizes that free distribution alone is insufficient without proper education on fit and maintenance. This has led brands to incorporate features like sizing tools, virtual try-on options, and post-purchase support into their direct-to-consumer strategies.

Adult helmets are available across a wide price range, from basic expanded polystyrene models to premium carbon-composite designs with integrated electronics. This segmentation reflects varying use cases, budgets, and safety features. According to the American Academy of Pediatrics, millions of children in the United States ride bicycles, with a significant number of non-fatal injuries reported in 2020. However, helmet usage remains low in the absence of mandatory laws. In developing markets, bike ownership among children is increasing at a notable rate, creating opportunities for brands that can navigate local certification requirements and offer products balancing affordability with compliance to standards such as the Bureau of Indian Standards.

By Category: Conventional Scale Versus Smart Innovation

Conventional helmets accounted for 96.17% of the projected 2025 volume, while smart helmet designs are growing at an annual rate of 8.01% through 2031. Smart helmets, featuring advancements such as fall-detection algorithms, rear LED (Light Emitting Diode) arrays, and Bluetooth mesh intercoms, are transitioning from premium niches to mid-tier product lines. For example, LIVALL's L23 model integrates features like fall detection, SOS (Save Our Souls) alerts, brake warnings, and turn signals. Similarly, the EVO21 offers patented SOS fall-detection and GPS (Global Positioning System) location alerts, making connectivity features more accessible to commuter segments. Lumos Nyxel combines integrated LEDs, a Multi-directional Impact Protection System (MIPS), and Quin crash detection. Sena's S helmet, equipped with Mesh Intercom and Bluetooth version 5.2, caters to group riders prioritizing communication, contrasting with solo commuters who focus on visibility. Despite the significant growth rate of smart helmets, their small market base and higher return rates due to battery life concerns and connectivity issues are limiting broader adoption.

Conventional helmets have benefited from decades of material science advancements, incorporating expanded polystyrene foam, polycarbonate shells, and rotational-impact liners to achieve high safety ratings, such as Virginia Tech's five-star certification. For instance, Canyon's Deflectr helmet exemplifies this standard. The Multi-directional Impact Protection System (MIPS), while adding cost and weight, is integrated into millions of helmets annually as of 2025. This technology has demonstrated measurable improvements in reducing rotational acceleration during laboratory tests, though its effectiveness diminishes under certain conditions, such as when the head is neck-constrained or when a realistic scalp layer is included in testing protocols. Alternatives to MIPS, such as WaveCel (Bontrager/Trek), which claims a significant reduction in concussion risk but adds weight, and KinetiCore (Lazer), which incorporates crumple zones into the expanded polystyrene liner, are diversifying the landscape of rotational protection. However, this growing variety is causing consumer confusion, which brands must address through education and third-party validation. Additionally, the NTA-8776 Dutch standard for e-bike helmets, which mandates higher-velocity drop tests, is gaining traction beyond the Netherlands. Municipalities are increasingly linking infrastructure subsidies to compliance with this certification, providing a regulatory advantage for conventional helmets that meet or exceed the standard.

By Distribution Channel: Offline Incumbency Versus Online Momentum

Offline retail stores accounted for 57.91% of transactions in 2025, driven by specialty cycling shops that provide fitting services, product education, and immediate product availability. However, online platforms are expanding at an annual growth rate of 7.25% through 2031. Direct-to-consumer brands, such as Canyon and Thousand, are bypassing traditional distribution channels to retain profit margins and collect customer data. Electronic commerce (e-commerce) is projected to grow at a compound annual growth rate (CAGR), with Amazon leading in transaction volume through third-party sellers and marketplace operations. Additionally, Shopify-enabled direct-to-consumer brands achieve higher profit margins by controlling the customer experience and avoiding wholesale discounts.

Smart helmets are witnessing significant year-on-year growth in online sales, underscoring the effectiveness of the online channel for technology-oriented products that require detailed specifications and customer reviews to address consumer concerns. Seasonality trends reveal that motorcycle helmet sales peak in late summer, while bicycle helmet sales peak in late autumn. These trends create inventory management challenges for omnichannel retailers, who must balance stock levels across both physical and digital platforms. Offline channels remain critical for providing tactile validation, which is essential for safety products where fit and comfort play a significant role in customer satisfaction. However, the high return rate for youth helmets, primarily due to sizing issues, highlights the limitations of in-store fitting when parents purchase without the child being present.

Geography Analysis

Europe is set to lead the global cycling market, contributing 37.21% of the projected revenue in 2025. This leadership is supported by factors such as mandatory helmet regulations in the Netherlands, advanced cycling infrastructure in Germany and France, and the European Union's funding commitment through 2027 for developing thousands of kilometers of new cycle paths. However, the region faces challenges, including a contraction in Germany's bicycle market in 2024 due to inventory corrections following pandemic-era oversupply. In 2024, Germany recorded significant bicycle sales in the millions, with e-bikes accounting for a substantial share. Similarly, the Netherlands sold hundreds of thousands of bicycles, with e-bikes capturing nearly half of the market share, while France generated considerable revenue from millions of units sold, including hundreds of thousands of e-bikes. Investments in cycling infrastructure, such as the Netherlands' funding commitment in November 2025 and Copenhagen's budget allocation for similar initiatives, continue to drive market growth. These investments also promote helmet use through peer influence and visibility campaigns. Additionally, the adoption of the NTA-8776 standard for e-bike helmets, which requires higher drop-test thresholds compared to the EN 1078 standard, is expanding beyond the Netherlands. This reflects the growing need for enhanced protection due to higher e-bike speeds, offering a compliance advantage to brands that proactively meet the stricter standard.

The Asia-Pacific region is anticipated to be the fastest-growing segment, with an annual growth rate of 7.71% through 2031. This growth is driven by India's upcoming two-helmet mandate in January 2026, increasing e-bike adoption in China, and higher middle-class spending on safety-certified gear. India's policy mandates two Bureau of Indian Standards-certified helmets with every new two-wheeler purchase, which is expected to significantly boost annual demand for certified helmets, create substantial manufacturing jobs, and reduce counterfeit products that have eroded consumer trust. The Ministry of Road Transport and Highways conducted extensive helmet-sample tests and multiple search-and-seizure operations in the previous financial year, including a Delhi operation that confiscated a large number of non-compliant helmets, signaling stricter regulatory enforcement. As of June 2025, numerous manufacturers held valid Bureau of Indian Standards licenses for protective helmets, a number expected to rise as the two-helmet rule drives demand. Additionally, bike ownership among children in developing markets is steadily increasing, creating opportunities for brands to offer products that comply with Indian Standard 4151:2015 certification requirements. These standards cover impact absorption, penetration resistance, retention-system integrity, flame resistance, weight limits, peripheral vision, and visor clarity.

North America, South America, and the Middle East and Africa collectively account for the remaining global revenue. North America benefits from state-level helmet mandates and investments in urban cycling infrastructure, such as funding from New York City's Department of Transportation and California's Active Transportation Program Cycle 8. In the United States, helmet laws in several states, primarily targeting riders under a certain age, create a fragmented regulatory framework that limits uniform nationwide adoption. However, California's Assembly Bill 1774 for 2024, which mandates helmets for e-bike riders under a specific age, demonstrates how state-level policies can drive incremental demand. In South America and the Middle East and Africa, helmet adoption remains low due to affordability issues, weak enforcement, and cultural norms that prioritize convenience over safety. Despite these challenges, urbanization and rising two-wheeler ownership are generating latent demand. Brands can address this demand through affordable designs, local manufacturing, and partnerships with municipal safety programs. According to the World Health Organization, approximately 1.2 million road deaths occur annually, with pedestrians and cyclists accounting for over a quarter. This highlights the public health need for protective equipment in emerging markets, where road safety infrastructure has not kept pace with vehicle growth.

Competitive Landscape

The cycling helmet market shows moderate competitive intensity, with established sports-equipment companies, specialized helmet manufacturers, and direct-to-consumer brands coexisting without a single dominant player. Vista Outdoor's divestiture of Bell, Giro, and Fox Racing to Strategic Value Partners highlights private equity interest in acquiring helmet portfolios from diversified outdoor-recreation companies. This transaction underscores a focus on operational efficiency and potential future consolidations. Similarly, Canyon's introduction of the Deflectr helmet, which ranked first in Virginia Tech's safety ratings due to its patented Release Layer System licensed from a London-based innovation firm, demonstrates how bicycle original-equipment manufacturers are integrating protective gear into their product lines. This approach aims to capture accessory margins, leverage proprietary intellectual property, and bypass traditional wholesale channels. Additionally, Trek's WaveCel technology, exclusive to Bontrager helmets and claiming a significant reduction in concussion risk, along with POC's extended sponsorship of professional cycling teams, highlights how brands are utilizing proprietary safety systems and athlete endorsements to command premium pricing and shape consumer perceptions.

Market growth opportunities are concentrated in three key areas: affordable rotational-impact protection for emerging markets, modular helmet designs, and integrated connectivity features. In emerging markets, the cost premium associated with the Multi-Directional Impact Protection System (MIPS) limits adoption, creating a demand for more affordable solutions. Modular helmet designs, such as Leatt's 3-in-1 Enduro helmet, cater to multiple use cases, offering versatility to consumers. Integrated connectivity features, including fall detection, navigation, and communication, are gaining traction, provided they do not compromise weight or ventilation.

Specialized's anti-counterfeit operation, which resulted in the seizure of counterfeit products and several arrests, highlights the challenges established brands face in protecting intellectual property and maintaining consumer trust. This issue benefits vertically integrated companies with direct-to-consumer distribution and blockchain-enabled authentication systems. Emerging players like Thousand Helmets and Lumen Labs are targeting urban commuters with aesthetically appealing designs, integrated lighting, and competitive direct-to-consumer pricing. However, their scalability is hindered by a limited product range and developing brand recognition. Virginia Tech's helmet-safety ratings, which evaluate hundreds of models and assign scores, have become an industry benchmark influencing retail placement and consumer preferences. Smaller players often face difficulties meeting these standards due to limited access to advanced testing facilities and materials-science expertise.

Cycling Helmet Industry Leaders

POC Sports

KASK S.p.A.

Vista Outdoor Inc.

Trek Bicycle Corp.

MET Helmets

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: 6D has introduced the ATB-3 full-face helmet, tested by downhill racer Reece Wilson on the DH circuit. The helmet features a reduced shell size to improve the field of view, enhanced rear protection extending close to the neck, and improved ventilation. Designed specifically for mountain biking, it emphasizes safety to address the demands of increasing speeds.

- December 2025: Canyon introduced its first mountain bike (MTB) helmet, the Deflectr, which received a top 5-star safety rating from Virginia Tech upon its launch. Equipped with patented RLS technology, the helmet features dual shells and polycarbonate bearings to minimize rotational forces and reduce the risk of concussions. Specifically designed for trail riders, it provides enhanced ventilation, a precise fit, and weighs 396 grams.

- July 2025: POC introduced the ultra-lightweight Cytal Lite helmet, weighing less than 200 grams, during the 2025 Tour de France. Designed for enhanced heat management and ventilation during climbs, it was launched in collaboration with EF Pro Cycling riders.

Global Cycling Helmet Market Report Scope

The cycling helmet market focuses on protective headgear designed for cyclists to reduce the risk of impact injuries during activities such as road cycling, mountain biking, urban commuting, and recreational riding. The market is segmented by product type, including road or recreational helmets, mountain bike (MTB) helmets, and sports or adventure helmets. It is also categorized by end user, covering kids and adults, and by category, which includes conventional helmets and smart helmets. Distribution channels are divided into offline retail stores and online retail stores. Geographically, the market spans North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Road/Recreational Helmets |

| Mountain Bike (MTB) Helmets |

| Sports/Adventure Helmets |

| Kids |

| Adult |

| Conventional Helmets |

| Smart Helmets |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Road/Recreational Helmets | |

| Mountain Bike (MTB) Helmets | ||

| Sports/Adventure Helmets | ||

| By End User | Kids | |

| Adult | ||

| By Category | Conventional Helmets | |

| Smart Helmets | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the cycling helmet market be by 2031?

The cycling helmet market size is projected to reach USD 3.16 billion by 2031, expanding at a 6.46% CAGR from 2026 to 2031.

Which helmet type is growing fastest?

Road and recreational helmets are forecast to grow at 7.91% annually through 2031, the highest among product categories.

What drives helmet demand in Asia-Pacific?

India’s two-helmet mandate, China’s rapid e-bike uptake, and rising disposable income are propelling the region at a 7.71% CAGR.

How big is the smart-helmet opportunity?

Smart models represent only 3.83% of 2025 volume but are advancing at an 8.01% CAGR, potentially surpassing USD 320 million in revenue by 2031.

Are counterfeits still a major issue?

Yes, regulators seized over 21,000 non-compliant units in the United States in 2025, and leading brands continue large-scale enforcement actions.

Page last updated on: