Cybersecurity Mesh Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.98 Billion |

| Market Size (2031) | USD 16.63 Billion |

| Growth Rate (2026 - 2031) | 18.97% CAGR |

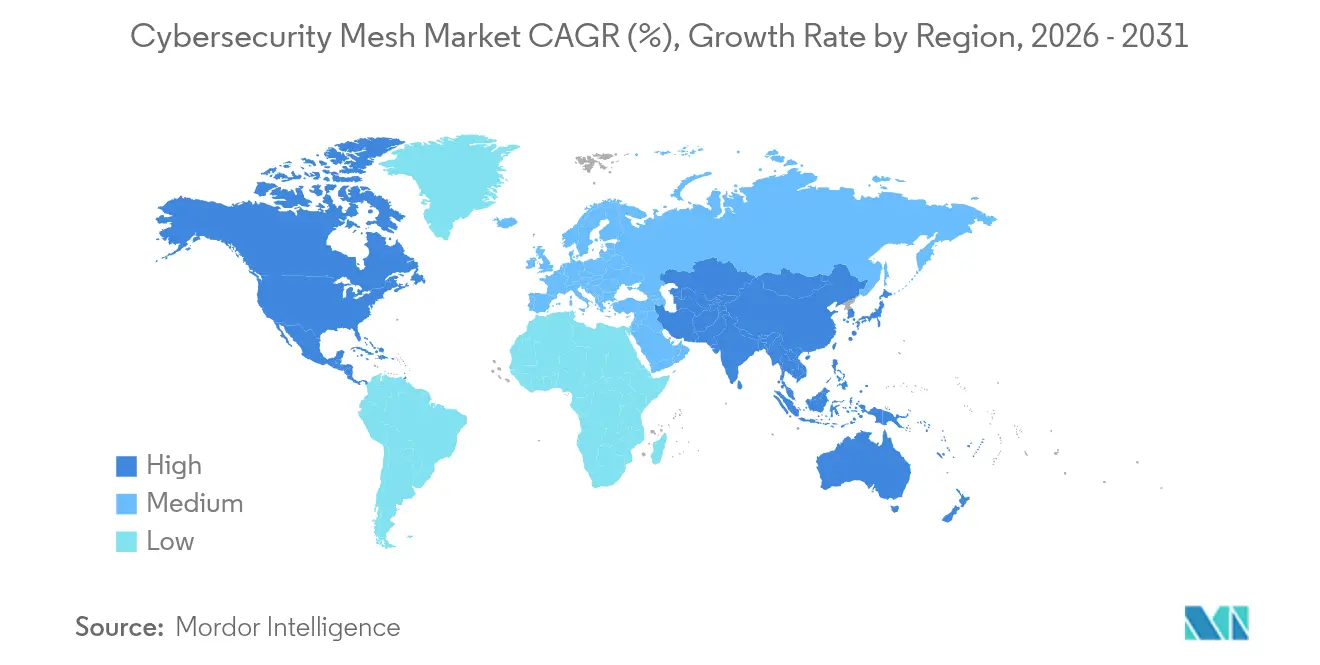

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

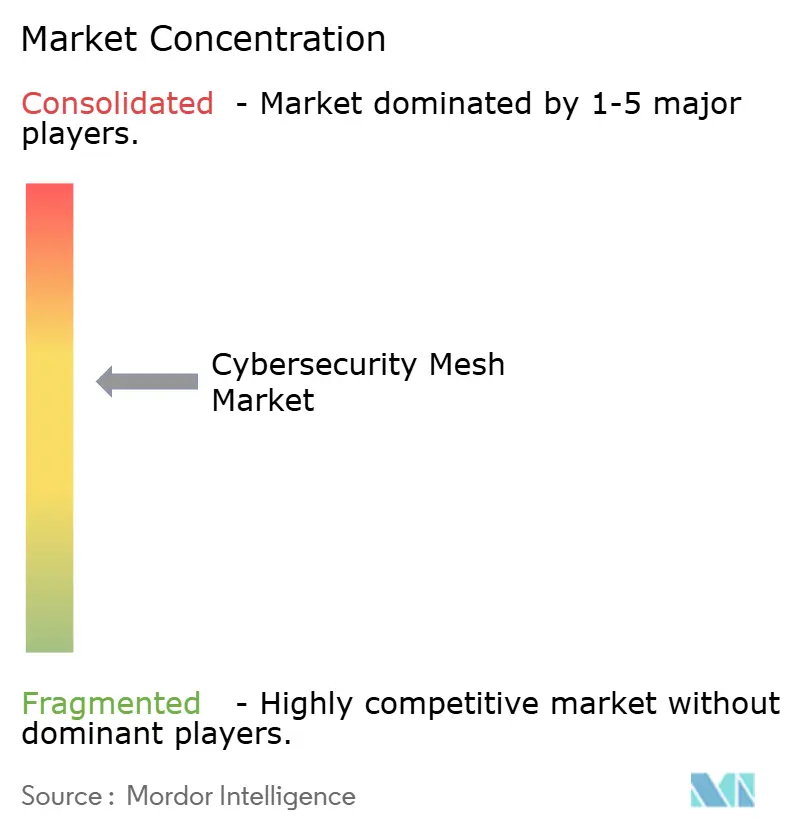

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Mesh Market Analysis by Mordor Intelligence

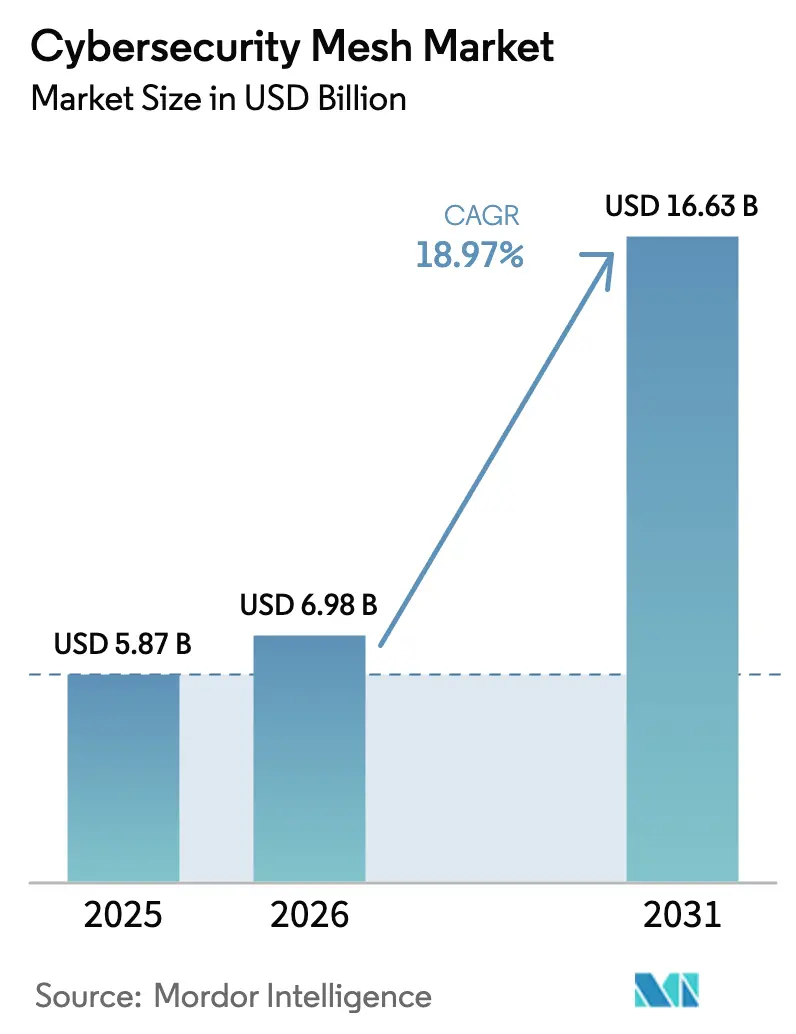

The cybersecurity mesh market size was valued at USD 5.87 billion in 2025 and estimated to grow from USD 6.98 billion in 2026 to reach USD 16.63 billion by 2031, at a CAGR of 18.97% during the forecast period (2026-2031). Surging attack sophistication, stricter Zero Trust mandates, and the rapid fusion of AI with policy engines underpin this double-digit trajectory. Demand concentrates in sectors that operate distributed infrastructures—IT-telecom, healthcare, and government—because mesh architectures remove single-point vulnerabilities, streamline compliance, and shrink incident response windows. Vendors accelerate platform consolidation, enabling buyers to replace fragmented point tools with unified policy fabrics that support hybrid work and cloud-native workloads. Capital allocation toward 5G, quantum-safe crypto, and AI-assisted orchestration further widens addressable use cases, ensuring sustained investment momentum.

Key Report Takeaways

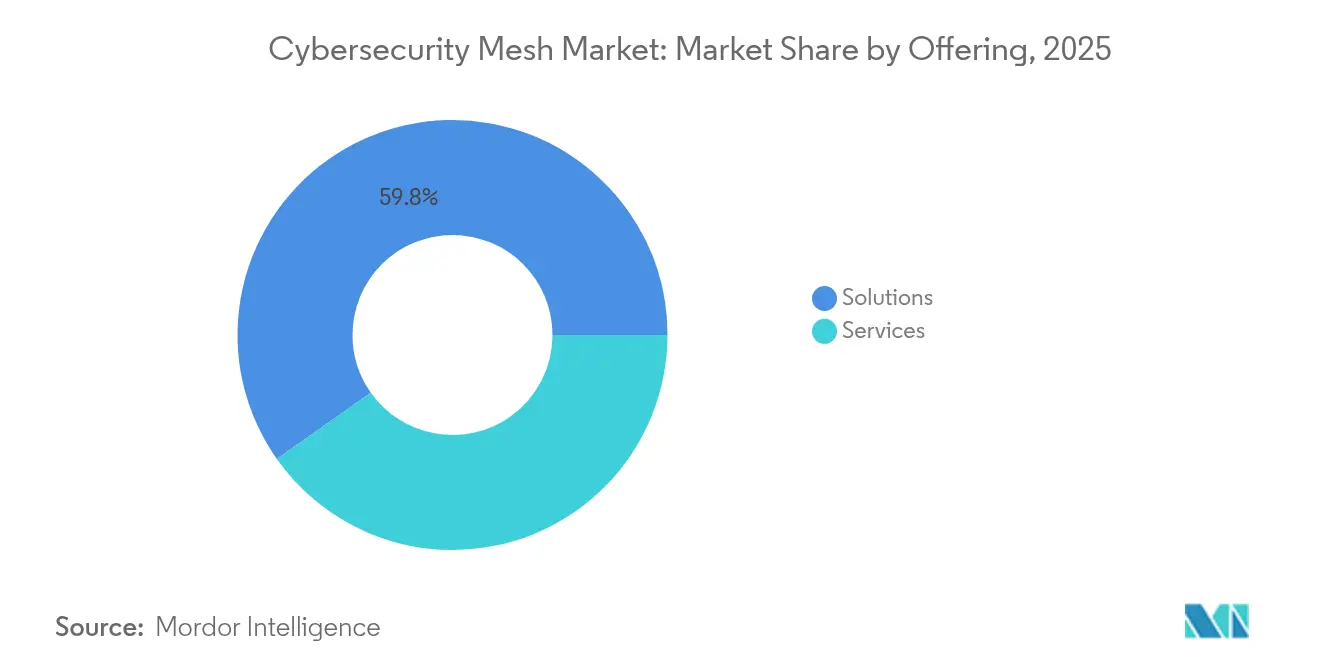

- By offering, solutions captured 59.78% revenue share in 2025; services are forecast to expand at a 14.2% CAGR to 2031.

- By deployment mode, the cloud segment commanded 70.45% of the cybersecurity mesh market share in 2025, while hybrid-cloud implementations are projected to grow at 12.2% CAGR through 2031.

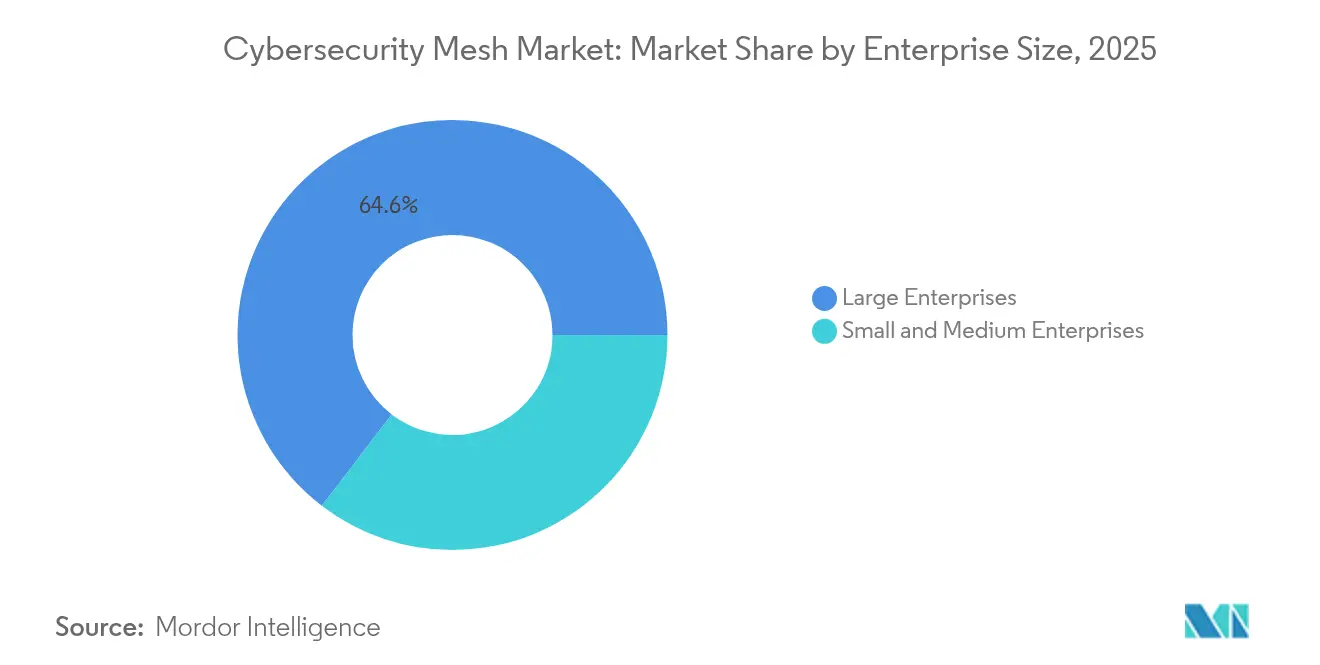

- By enterprise size, large enterprises held 64.60% of adoption in 2025, whereas SMEs are expected to grow at 15.1% CAGR.

- By end-user industry, IT-telecom led with 31.12% share of the cybersecurity mesh market size in 2025; healthcare is advancing at a 14.1% CAGR through 2031.

- By geography, North America accounted for 38.45% revenue share in 2025, while Asia-Pacific is set to expand at 12.6% CAGR on the back of government-funded digital-trust programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cybersecurity Mesh Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and sophistication of cyber-attacks | +4.2% | Global | Short term (≤ 2 years) |

| Expansion of hybrid and remote workforce models | +3.8% | North America and Europe | Medium term (2-4 years) |

| Regulatory push toward Zero Trust architectures | +3.5% | North America, Europe, APAC | Medium term (2-4 years) |

| Growing cloud-native application footprints | +3.1% | Global | Long term (≥ 4 years) |

| AI-driven adaptive policy orchestration | +2.7% | North America, Europe | Long term (≥ 4 years) |

| Micro-segmentation demand in 5G network slicing | +2.2% | APAC, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency and Sophistication of Cyber-Attacks

State-sponsored groups such as Volt Typhoon intensified advanced persistent threat campaigns in 2024, lifting global ransomware incidents by 22% and breaching critical infrastructure through AI-enabled tactics. Mesh frameworks cut lateral-movement risk by embedding distributed controls near every asset, which helped early adopters cut breach exposure by 68% relative to perimeter-centric designs.

Expansion of Hybrid and Remote Workforce Models

Permanent hybrid workforces forced a pivot away from VPN concentration points toward identity-centric access fabrics. Homestead Financial, for instance, eliminated VPN backhaul by adopting a mesh-based Zero Trust Exchange, driving a 35% IT-operations cost drop and a marked uptick in user satisfaction.

Regulatory Push Toward Zero-Trust Architectures

Executive Order 14144 (Jan 2025) obliges U.S. federal agencies to operationalize Zero Trust with explicit milestones, while NIS2 sets EUR 10 million penalty ceilings for non-compliance in Europe. These edicts turn compliance into a budget-protected line item, directly translating into cybersecurity mesh market demand.

AI-Driven Adaptive Policy Orchestration

Platforms such as Prisma SASE now harness machine learning to rewrite access policies in real time, cutting false positives by 60% and letting analysts process 10× more events. AI also mitigates workforce shortages by automating triage and containment tasks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation complexity and integration cost | -2.8% | Global | Short term (≤ 2 years) |

| Shortage of mesh-literate cybersecurity talent | -2.3% | North America, Europe | Medium term (2-4 years) |

| Interoperability gaps with legacy on-prem tools | -1.9% | North America, Europe | Medium term (2-4 years) |

| Vendor lock-in risks in multi-vendor meshes | -1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Implementation Complexity and Integration Cost

Projects often span 6-12 months and demand USD 2–5 million upfront, placing pressure on capex-sensitive buyers. Phoenix Children’s Hospital staged its rollout over three quarters to avoid clinical-care disruption, underlining the planning burden tied to mesh transitions.

Shortage of Mesh-Literate Cybersecurity Talent

A 4 million-person global skills gap means only 72% of U.S. openings are filled, inflating salaries 25–40% above conventional roles[1]ISC², “2025 Cybersecurity Workforce Study,” isc2.org. SMEs feel this pinch most acutely and often postpone projects or outsource operations to managed service providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Drive Market Foundation

Solutions secured 59.78% of 2025 revenue as enterprises prioritized purchasing core platforms before layering in services. Demand centered on integrated policy engines and distributed enforcement points that form the backbone of a scalable cybersecurity mesh market. Vendor earnings reinforce this tilt: Palo Alto Networks reported USD 2.29 billion Q3 2025 revenue, up 15% on brisk Prisma SASE uptake, while Fortinet logged USD 1.54 billion Q1 2025 revenue, a 14% jump attributable to its Security Fabric portfolio.

Service revenues accelerate at a 14.2% CAGR as organizations shift from piloting to optimization. Managed detection and response, consulting, and integration work underpin this rise, giving mid-market buyers mesh access without steep learning curves. CrowdStrike’s USD 4.3 billion annual recurring revenue, growing 23%, exemplifies the traction of bundled service-plus-platform propositions.

By Deployment Mode: Cloud Dominance Reflects Architectural Alignment

Cloud deployments held 70.45% share in 2025, confirming architectural affinity between mesh principles and elastic cloud fabrics. Continuous feature release, shared threat intelligence, and consumption-based pricing help enterprises trim 30–40% of operating cost versus equivalent on-prem stacks while shrinking update windows to hours rather than quarters. Hybrid architectures bridge sovereignty gaps for regulated workloads, guided by NIST SP 800-207A’s Zero Trust blueprint.

On-prem approaches persist in defense and critical infrastructure, where air-gap mandates persist, but growth remains muted. Even those buyers often adopt cloud-provisioned management planes to simplify policy orchestration, suggesting a gradual shift rather than a binary divide.

By Enterprise Size: SME Growth Accelerates Through Managed Services

Large enterprises owned 64.60% revenue in 2025 as they commandeered sizable budgets for bespoke mesh rollouts extending across multi-cloud estates. The U.S. Department of Defense’s aim for full Zero Trust by 2030 showcases the scale and rigor applied at the upper end of the market.

SMEs expand faster, posting a 15.1% CAGR through 2031 by capitalizing on SaaS-delivered mesh stacks. Southern Cross Hospitals secured 14 facilities through Prisma Access delivered as a managed service, validating that smaller IT teams can reach an enterprise-grade posture without hiring large internal staff.

By End-User Industry: Healthcare Drives Fastest Growth

IT-telecom contributed 31.12% of 2025 spend, using mesh architectures to secure multi-tenant cores and 5G slices critical for low-latency applications. High device density and strict SLA requirements make granular segmentation indispensable.

Healthcare leads growth at a 14.1% CAGR. Apollo Hospitals adopted distributed identity controls to protect patient data across telemedicine and in-facility care, proving mesh effectiveness in high-sensitivity environments. Regulatory frameworks such as HIPAA and the EU NIS2 revise compliance baselines upward, reinforcing adoption urgency.

BFSI, retail, and public-sector entities form the next tier of opportunity. All three verticals combine stringent compliance rules with transaction-heavy workloads, conditions well-suited to the deterministic access principles inherent in the cybersecurity mesh market.

Geography Analysis

North America retained 38.45% of 2025 revenue, reflecting Executive Order 14028’s mandate that all federal agencies adopt Zero Trust and pour funding into supporting architectures. Both public and private operators benefited from a deep vendor ecosystem that speeds integrations and cuts deployment cycles. Canada’s national cybersecurity strategy and Mexico’s financial-sector cloud guidelines further widen regional demand, though the United States remains the epicenter.

The Asia-Pacific cybersecurity mesh market gains speed at 12.6% CAGR. South Korea boosted cybersecurity funding to KRW 2.45 trillion (USD 1.84 billion), a 15.7% uplift that fuels nationwide Zero Trust pilots, while the PRC’s Eastern Data Western Compute project elevates demand for distributed policy frameworks that manage data flows across regions. Japan’s Beyond 5G road-map channels investment into AI-defined network defenses, and Australia’s International Cyber Engagement Strategy positions Canberra as a regional services hub.

Europe’s push centers on GDPR and NIS2, elevating baseline expectations for incident reporting, encryption, and access controls. Mesh architecture provides the granular audit trails and continuous authentication needed to satisfy both data-sovereignty and operational-continuity requirements. The Middle East and Africa pursue mesh adoption in tandem with national digital-economy programs, but skill shortages and legacy constraints temper near-term momentum.

Competitive Landscape

Market concentration is moderate as platform leaders consolidate share yet face pressure from niche innovators. Palo Alto Networks, Fortinet, and Zscaler deliver unified policy engines, endpoint agents, and service-edge gateways—components that together underpin the cybersecurity mesh market. Their RandD agendas increasingly focus on AI-assisted policy tuning, quantum-safe crypto, and automated incident response.

MandA remains a core route to capability expansion. Sophos’s February 2025 acquisition of Secureworks enhances managed detection reach, while CyberArk’s USD 1.54 billion Venafi deal extends into certificate lifecycle management, a linchpin for machine-to-machine trust. Intel pursues patents for network-associated object allocation, hinting at hardware-level acceleration for distributed security.

Disruptors differentiate on autonomous segmentation, privacy-preserving analytics, and post-quantum algorithms. Cisco’s Hypershield exemplifies AI-driven micro-segmentation that tracks intent rather than static attributes, providing a blueprint for next-wave contenders.

Cybersecurity Mesh Industry Leaders

IBM Corporation

Palo Alto Networks, Inc.

Check Point Software Technologies Ltd.

Zscaler, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sophos acquired Secureworks, merging MDR expertise with endpoint and network controls to deliver a consolidated platform.

- February 2025: DigiCert announced plans to acquire Vercara, expanding its digital-trust stack into DNS and DDoS protection.

- January 2025: SentinelOne completed the USD 155 million purchase of PingSafe to deepen cloud-posture management.

- March 2024: Zscaler bought Avalor, enriching its Zero Trust Exchange with advanced analytics.

Global Cybersecurity Mesh Market Report Scope

Cybersecurity mesh is a cyber defense strategy that independently secures each device with its own perimeter, such as firewalls and network protection tools. Many security practices use a single perimeter to secure an entire IT environment, but a cybersecurity mesh uses a holistic approach.

The cybersecurity mesh market is segmented by type (solution, services), by deployment (cloud, on-premises), by enterprise size (SMEs, large enterprises), by end-user (BFSI, it and telecom, retail, healthcare, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| Cloud |

| On-Premises |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Retail |

| Healthcare |

| Government |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Solutions | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Retail | |||

| Healthcare | |||

| Government | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the cybersecurity mesh market?

The cybersecurity mesh market stands at USD 6.98 billion in 2026 and is projected to reach USD 16.63 billion by 2031.

Which segment dominates the cybersecurity mesh market?

Solutions contribute 59.78% of 2025 revenue, highlighting buyer emphasis on core platforms before services.

Why is Asia-Pacific the fastest-growing region?

Heavy government funding, 5G rollouts, and national data strategies push the region toward a 12.6% CAGR.

How does AI influence cybersecurity mesh adoption?

AI enhances threat detection accuracy by 60% and automates policy adjustments, which eases analyst workload and accelerates response.

Page last updated on: