Healthcare Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 42.31 Billion |

| Market Size (2031) | USD 97.79 Billion |

| Growth Rate (2026 - 2031) | 18.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Healthcare Cybersecurity Market Analysis by Mordor Intelligence

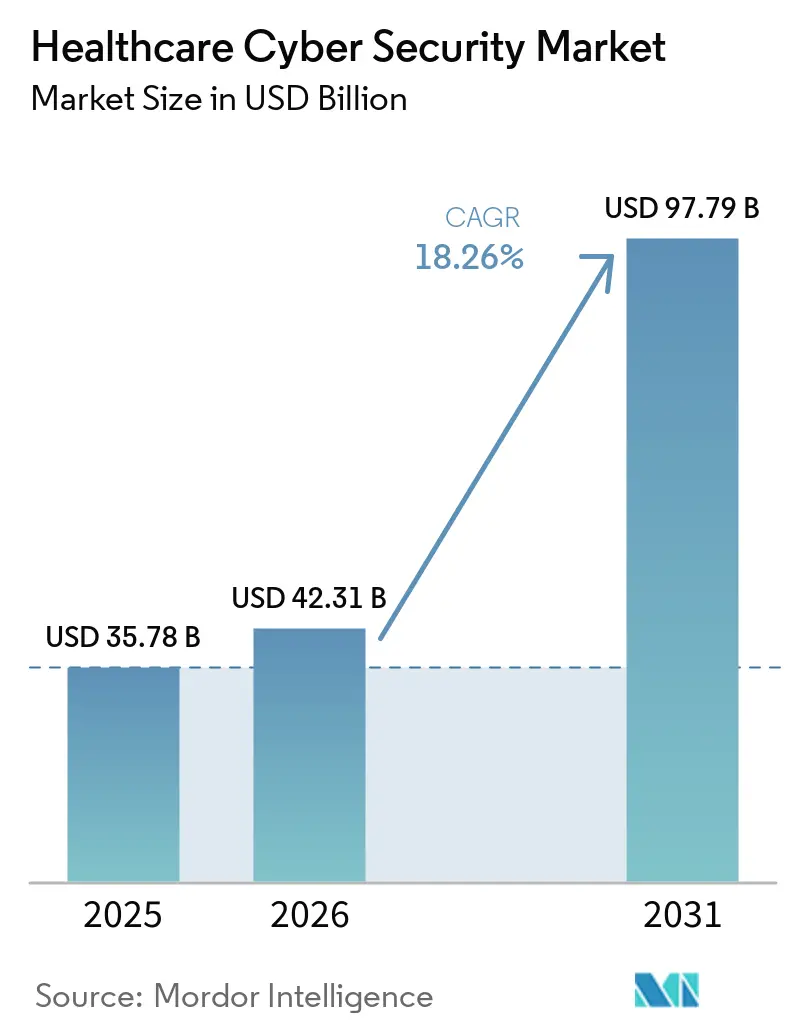

The healthcare cybersecurity market size was valued at USD 35.78 billion in 2025 and estimated to grow from USD 42.31 billion in 2026 to reach USD 97.79 billion by 2031, at a CAGR of 18.26% during the forecast period (2026-2031). The spending surge reflects an industry-wide scramble to defend electronic protected health information against a record wave of intrusions. Healthcare providers reported 677 major breaches in 2024 that exposed 182.4 million patient records, underscoring the sector’s high-value data and persistent threat landscape. Heightened federal oversight, notably the Food and Drug Administration’s Section 524B requirements for all new connected medical devices, obliges manufacturers and providers to budget for life-cycle security programs. Parallel to device rules, the Office for Civil Rights’ stiffer HIPAA enforcement and the Department of Health and Human Services’ voluntary cybersecurity performance goals have pushed boards to elevate cyber risk to a top-three enterprise issue. Government funding amplifies the momentum: Washington’s 2025 consolidated cyber budget earmarks USD 13 billion for civilian agencies, a portion of which flows to hospitals modernizing legacy systems. Simultaneously, the American Hospital Association’s alert that nation-state actors targeted United States facilities in 2024 catalyzes the uptake of zero-trust frameworks and real-time monitoring solutions.

Key Report Takeaways

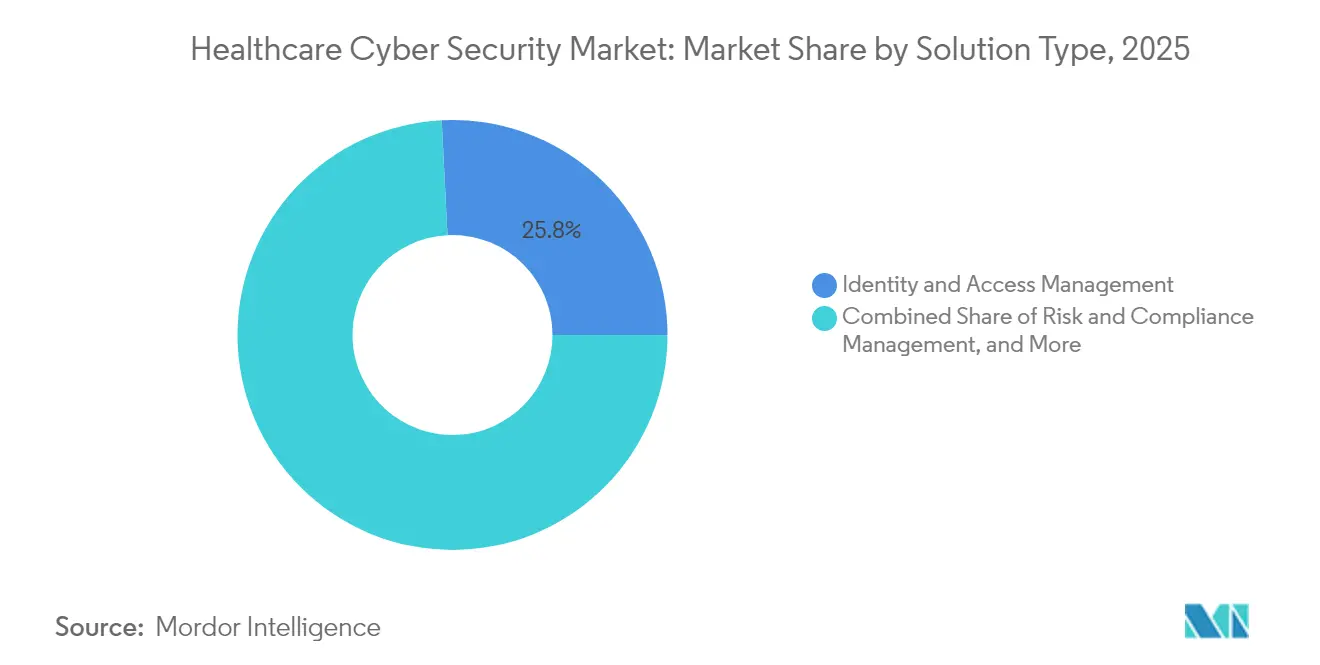

- By solution type, Identity and Access Management held 25.80% of the healthcare cyber security market share in 2025; Security Information and Event Management is projected to grow at 18.72% CAGR through 2031.

- By security type, network security accounted for 33.95% of the healthcare cyber security market size in 2025, while cloud security is advancing at an 18.58% CAGR to 2031.

- By deployment mode, on-premise models dominated with 55.62% revenue share in 2025, yet cloud deployment is forecast to post an 18.95% CAGR between 2026-2031 in the healthcare cybersecurity market.

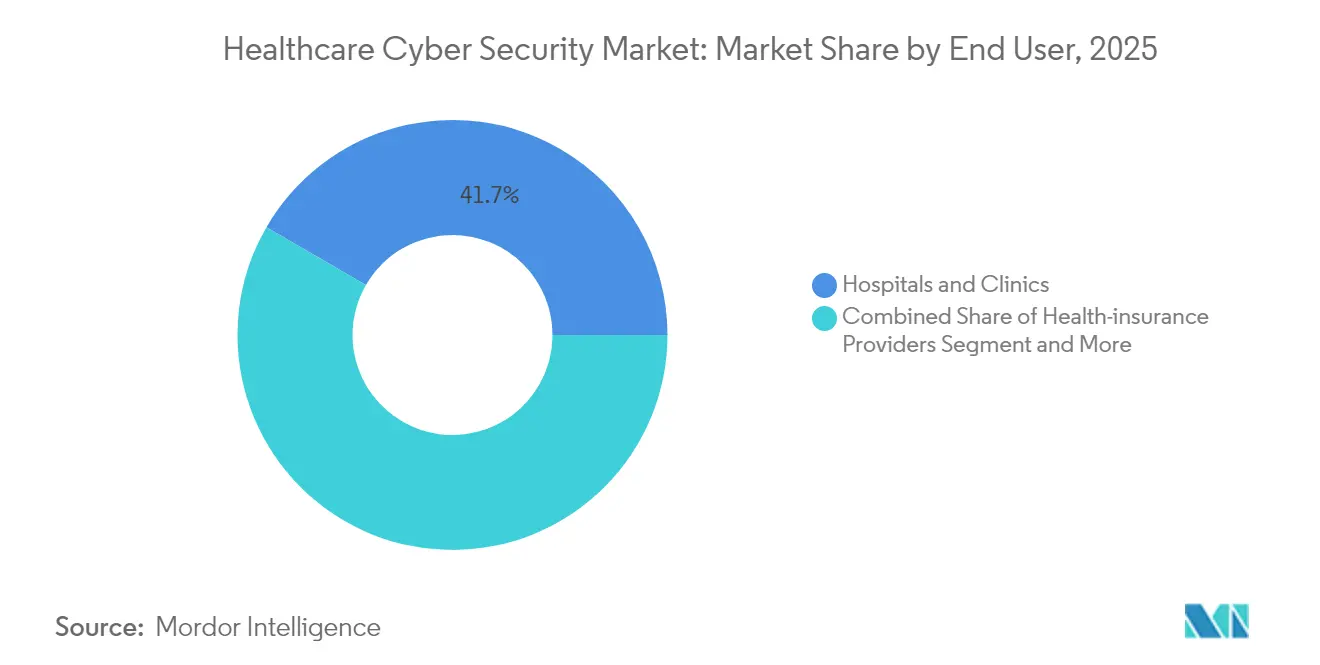

- By end user, hospitals and clinics captured 41.65% of the healthcare cyber security market share in 2025; health-insurance providers represent the fastest-expanding end-user segment at 18.44% CAGR.

- By geography, North America led with 34.12% revenue share in 2025, while Asia-Pacific is on track for a 19.12% CAGR through 2031 in the healthcare cybersecurity market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating frequency and sophistication of cyber-attacks | +4.2% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Regulatory mandates and compliance burden | +3.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid cloud-based EHR and tele-health adoption | +3.1% | Global, led by developed markets | Medium term (2-4 years) |

| Low security penetration among smaller providers | +2.7% | Global, particularly rural and developing regions | Long term (≥ 4 years) |

| Medical-device security tied to value-based care models | +2.3% | North America, expanding to Europe | Long term (≥ 4 years) |

| Zero-trust frameworks for IoMT environments | +1.8% | Global, early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Frequency and Sophistication of Cyber-Attacks

Security researchers confirmed that adversaries linked to Russia, China, North Korea, and Iran probed hospital infrastructure daily in 2024, culminating in breaches that touched an estimated 259 million medical records.[1]American Hospital Association, “Hospitals and Health Systems Face Rising Cyber Threats,” aha.org Health records command a premium on illicit markets because they enable insurance fraud, blackmail, and espionage. This dual utility fuels relentless reconnaissance, ransomware, and supply-chain attacks. Artificial-intelligence tooling now automates spear-phishing and voice deep-fake scams, eroding user-based defenses. Providers respond by prioritizing continuous monitoring, multi-factor authentication, and least-privilege policies across cloud workloads and connected devices in the healthcare cybersecurity market.

Regulatory Mandates and Compliance Burden

Section 524B requires every new medical device submitted to the FDA after March 2023 to include a Software Bill of Materials, secure development attestations, and a plan for coordinated vulnerability disclosure.[2]Food and Drug Administration, “Cybersecurity in Medical Devices: Refuse-to-Accept Guidance,” fda.gov Beyond pre-market clearance, manufacturers must patch flaws for the product’s commercial life. Hospitals integrating these devices, therefore, budget for integrated risk management platforms able to track firmware, security advisories, and patch status in real time. Simultaneously, the HHS Cybersecurity Performance Goals outline baseline safeguards—such as immutable backups and privileged access controls—that many boards treat as de facto standards. Identity, Credential, and Access Management frameworks endorsed by the Cybersecurity and Infrastructure Security Agency replace password-centric models with risk-based, certificate-driven authentication.

Rapid Cloud-Based EHR and Tele-Health Adoption

The pandemic accelerated migration of electronic health record instances, imaging archives, and virtual-care platforms to public and hybrid clouds. As workloads sprawl, security teams must enforce HIPAA and global privacy statutes in multi-tenant environments. Pharmaceutical sponsors running decentralized trials store genomic data and intellectual property in cloud research platforms, requiring end-to-end encryption, anomaly detection, and secure DevOps pipelines. Tele-health endpoints—ranging from video kiosks to smartphone apps—extend attack surfaces to patient homes, intensifying demand for zero-trust access brokers, zero-trust network access and continuous device posture checks.

Low Security Penetration Among Smaller Providers

Financial distress afflicts 46% of rural U.S. hospitals, leaving limited capital for cyber defense initiatives. Voluntary surveys by Microsoft’s Rural Hospital Security Program found widespread gaps in email filtering, multi-factor authentication, and network segmentation. Because regional referral networks share claims data, a compromise in a small clinic can propagate laterally into tertiary centers. Public-private grants and managed security services are emerging to close this resilience divide, yet adoption remains slow due to staffing shortages and competing infrastructure needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints in small providers | -2.1% | Global, particularly rural and developing regions | Short term (≤ 2 years) |

| Shortage of specialised cyber-security talent | -1.8% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Legacy system interoperability challenges | -1.4% | Global, particularly acute in developed markets | Medium term (2-4 years) |

| Vendor-liability ambiguity for FDA-regulated devices | -1.2% | North America, expanding to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints in Small Providers

Smaller hospitals often run on operating margins below 2%, leaving inadequate reserves for layered security tooling and 24×7 monitoring. Investigations into recent closures show cyber incidents can trigger permanent shutdowns when ransom demands and downtime erode liquidity. The Healthcare Sector Coordinating Council recommends classifying cybersecurity as an allowable Medicare expense, yet reimbursement policy remains under review. Until sustainable funding emerges, adoption of subscription-based managed detection and response services is the primary avenue for risk reduction.

Shortage of Specialized Cyber-Security Talent

Healthcare requires defenders who understand clinical workflows, regulatory frameworks, and operational technology. Competitive pressure from finance and tech industries raises compensation beyond what many non-profit systems can match. As a stop-gap, providers outsource tier-one monitoring, invest in low-code security orchestration, and adopt AI-driven analytics that triage alerts with minimal human input. The emergence of AI-driven cybersecurity tools offers potential solutions to talent constraints, but successful implementation requires specialized knowledge that many healthcare organizations currently lack.[3]Healthcare Information and Management Systems Society, Inc. (HIMSS), "Health System Cybersecurity Budgets Increasing, But Lack of AI Governance Threatens Security," himss.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: IAM Dominance Faces SIEM Disruption

Identity and Access Management tools accounted for 25.80% of the healthcare cybersecurity market size in 2025 as organizations focused on controlling privileged credentials inside sprawling clinical ecosystems. However, demand is shifting toward Security Information and Event Management platforms, which are forecast to grow at 18.72% CAGR to 2031. The change reflects a consensus that continuous log correlation and behavioral analytics offer faster breach containment than perimeter controls alone. Over the forecast period, cybersecurity roadmaps show budget reallocation from stand-alone antivirus toward converged detection stacks that integrate SIEM, SOAR, and user-entity analytics.

Risk and compliance suites remain steady because they streamline documentation for HIPAA, GDPR, and device post-market surveillance audits. Encryption and data-loss-prevention modules gain traction within zero-trust architectures, especially where providers must share radiology images and lab data across multiple cloud tenants. Emerging behavioral analytics solutions built with machine learning sit in the “other solutions” bucket and are frequently piloted in research institutes experimenting with precision medicine workloads.

By Security Type: Network Security Leads Cloud Transformation

Network security retained 33.95% of the healthcare cybersecurity market share in 2025 because hospitals continue to segment VLANs connecting operating rooms, pharmaceutical automation, and picture-archiving systems. The pivot to cloud workloads is nonetheless reshaping priorities: cloud security tools are poised for an 18.58% CAGR, propelled by migrations of EHR instances to hyperscale providers.

Endpoint protection confronts proliferating device heterogeneity, from bedside infusion pumps to clinician smartphones. Application security rises as in-house development teams build patient-facing portals that integrate third-party APIs, necessitating runtime protection and software composition analysis. Medical-device and IoMT security, once an afterthought, is now a board-level issue because more than 14,000 healthcare IP addresses expose device telemetry to the public internet—a statistic that rallies funding for agentless network detection and regulated device patch orchestration.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premises Dominance

On-premises environments captured 55.62% of 2025 revenue, as many providers keep radiology archives and financial records within their data centers to satisfy data residency clauses. Yet the shift is unmistakable: cloud deployments are tracking a 18.95% CAGR to 2031 as CIOs seek subscription models, automatic scaling, and resilient disaster-recovery zones. Hybrid architectures prevail, mixing local compute for latency-sensitive imaging with cloud-native analytics engines used for population health studies.

Healthcare cybersecurity industry observers note that edge computing, where portable AI diagnostic tools run in ambulances or rural clinics, blurs conventional deployment definitions. New procurement doctrines emphasize API-level integration and cross-plane identity propagation, enabling unified security policies across hospital campuses, cloud clusters, and edge endpoints.

By End User: Hospitals Drive Growth While Insurance Providers Emerge

Hospitals and clinics represented 41.65% of 2025 demand because they store the largest troves of patient data and must sustain life-critical services round the clock. Insurers, although historically lite IT spenders, now register an 18.44% CAGR as payers invest in fraud analytics and secure data exchanges that underpin value-based care contracts. The February 2024 Change Healthcare ransomware event, which froze claims processing nationwide, validated insurer exposure and accelerated procurement of third-party risk-management platforms.

Pharmaceutical and biotechnology companies allocate larger shares of R&D budgets to secure cloud research environments that protect molecular IP and trial subject data. Diagnostic laboratories modernize laboratory information systems, driving investment in ransomware containment for high-throughput sequencing equipment. Tele-health providers and digital-health start-ups, grouped under “other end users,” adopt managed security services to offset staffing gaps and speed regulatory clearances.

By Organization Size: SMEs Drive Growth Despite Resource Constraints

Large enterprises controlled 63.58% revenue in 2025 of the healthcare cybersecurity market, yet small and medium-size entities are forecast to advance at 19.86% CAGR to 2031 as threat awareness climbs. The Microsoft rural-hospital program and similar initiatives from insurers and device vendors lower entry barriers by subsidizing multi-factor authentication, EDR, and immutable backup deployments.

Nonetheless, SMEs still struggle with vendor selection and incident-response planning. Many rely on state health-information exchanges for shared security operations and threat-intelligence feeds. Policy proposals to make cyber investments reimbursable under Medicare could further unlock SME spending, but until codified, most rely on flexible, usage-based subscription contracts rather than capital purchases.

Geography Analysis

North America maintained 34.12% healthcare cyber security market share in 2025, backed by the world’s strictest PHI regulations, a mature insurance system, and high per-capita health IT budgets. Federal funding, including the 2025 civilian cyber allocation, underwrites modernization of electronic health records and cloud adoption. The United States also endured the largest known breach the 2024 Change Healthcare incident affecting 100 million individuals which solidified zero-trust roadmaps and third-party risk audits. Canada’s Pan-Canadian Artificial Intelligence Strategy and Mexico’s social-security digitization initiatives further enlarge regional demand for SIEM and endpoint detection tools.

Asia-Pacific is the fastest-growing territory at 19.12% CAGR in the global healthcare cybersecurity market. National e-health mandates in Japan, South Korea, and India integrate cloud-hosted patient registries with secure identity platforms, spurring local demand for data-masking and encryption-as-a-service offerings. China’s Healthy China 2030 blueprint designates cybersecurity one of six enabling pillars for smart hospitals, boosting orders for domestic firewall and vulnerability-management vendors that meet cross-border data flow restrictions. Australia’s federal budget anchors subsidies for rural tele-health, leading to a 92% jump in digital-health solicitation requests from 2022-2024.

Europe’s privacy-centric regime ensures steady growth as GDPR fines crystallize board-level accountability. Germany allocates EUR 3 billion to hospital digitization with at least 15% reserved for IT security enhancements, stimulating procurement of identity orchestration and secure email gateways. France implements its “MaSanté 2025” e-health strategy with a cybersecurity annex that mandates threat-intelligence sharing among regional health agencies. The United Kingdom’s NHS “Data Saves Lives” program directs funds to modernize legacy paging and imaging platforms, contingent upon ISO 27001 certification.

The Middle East and Africa exhibit accelerating adoption as Gulf Cooperation Council states build smart-city hospitals and seek compliance with the National Cybersecurity Authority’s Healthcare Sector Controls. South Africa and Kenya pilot cloud-based immunization registries accompanied by tokenization schemes that de-identify patient data. South America registers steady expansion led by Brazil’s open-health initiatives and Argentina’s electronic prescription rollout, both of which require encryption key management and secure API gateways.

Competitive Landscape

The healthcare cyber security market remains moderately fragmented. Roughly 15 vendors account for half of global revenue, leaving room for niche specialists in IoMT segmentation and managed detection. Consolidation is accelerating: Palo Alto Networks integrated IBM’s QRadar cloud analytics into its Cortex platform in 2024, and Google’s USD 32 billion purchase of Wiz bolstered its Chronicle security stack. Such deals illustrate a race to offer full-stack platforms that span network, endpoint, and cloud defense with built-in HIPAA templates.

Domain expertise now differentiates winners in the healthcare cybersecurity space. Vendors with dedicated healthcare business units provide pre-configured threat-intelligence feeds that flag device recalls and FDA advisories. The FDA’s 2024 warning letter to Becton Dickinson over Pyxis vulnerabilities signaled punitive consequences for suppliers lacking structured secure-design programs. Consequently, device manufacturers partner with cybersecurity firms to embed SBOM tracking and over-the-air patch channels prior to 510(k) submissions.

White-space opportunities persist in rural hospital protection, medical-device micro-segmentation, and AI governance. Meanwhile, start-ups leveraging federated learning defend imaging-diagnostic AI models without centralizing patient data, addressing privacy concerns under GDPR and state privacy laws. Incumbents counter by investing in extended detection and response suites optimized for HL7 and DICOM traffic.

Healthcare Cybersecurity Industry Leaders

-

IBM Corporation

-

Cisco Systems Inc.

-

AO Kaspersky Lab

-

Broadcom Inc. (Symantec)

-

McAfee LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft expanded its Cybersecurity Program for Rural Hospitals to include AI-driven risk scoring, enrolling 550 hospitals for no-cost assessments.

- March 2024: The FDA issued draft guidance that tightens pre-market cyber requirements, emphasizing continuous patch support and SBOM transparency.

- May 2024: Palo Alto Networks finalized the purchase of IBM’s QRadar cloud assets, training 1,000 IBM consultants on Palo Alto’s healthcare rule-sets.

- June 2024: The White House announced alliances with leading cloud vendors to provide subsidized security services to up to 2,100 rural hospitals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the healthcare cybersecurity market as all software, hardware, and managed services that protect clinical information systems, connected medical devices, and patient data repositories against unauthorized access, disruption, or exfiltration across provider, payer, life sciences, and public health environments.

Scope exclusion: non-clinical enterprise security tools sold to healthcare conglomerates solely for office IT needs are not covered.

Segmentation Overview

-

By Solution Type

- Identity and Access Management

- Risk and Compliance Management

- Antivirus and Antimalware

- Security Information and Event Management (SIEM)

- Intrusion Detection / Prevention (IDS/IPS)

- Encryption and Data-Loss Prevention

- Other Solutions

-

By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Medical-Device / IoMT Security

-

By Deployment Mode

- On-premise

- Cloud

-

By End User

- Hospitals and Clinics

- Pharmaceuticals and Biotechnology Firms

- Health-insurance Providers

- Diagnostic Laboratories

- Other End Users

-

By Organisation Size

- Large Enterprises

- Small and Medium Enterprises

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Chile

- Rest of South America

-

Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with CISOs of IDNs, regional payers, cloud-hosted telehealth platforms, and cybersecurity solution integrators across North America, Europe, and Asia Pacific helped validate spending ratios, average selling prices, and deployment pain points, while clarifying regional regulatory nuances that desk research left ambiguous.

Desk Research

Analysts began with open data sets from bodies such as the US HHS Office for Civil Rights, the European Union Agency for Cybersecurity, and the Australian Cyber Security Centre, which quantify breach counts, record exposure volumes, and penalty trends. We matched those signals with procurement filings on sites like SAM.gov, annual 10-K disclosures from major EHR and med-tech vendors, and customs shipment records collated through D&B Hoovers and Volza to size cross-border device flows. Trade associations, for example, the College of Healthcare Information Management Executives and the IoT Security Foundation, supplied adoption benchmarks for zero-trust architectures and IoMT inventories. These publicly available sources are illustrative only; many others were consulted to round out secondary insights.

Market-Sizing & Forecasting

We reconstructed global revenue using a top-down spend pool build that starts with healthcare IT outlays by region, subtracts non-security categories, and then applies breach-driven security penetration rates. Supplier roll-ups of sampled ASP × installed base data served as a selective bottom-up check. Key variables include: annual count of disclosed healthcare data breaches (>500 records), average cost per breach (IBM-Ponemon index), installed stock of networked medical devices (FDA Unique Device Identifier registry), proportion of cloud-hosted EHR deployments, and mandatory audit frequency under HIPAA, GDPR, and NIS2. A multivariate regression links those drivers to historical revenue, while scenario analysis captures regulatory tightening and ransomware escalation. Gaps in country-level spend were bridged by applying per-bed security outlays derived from primary interviews.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, anomaly checks against independent breach and capex datasets, and variance reconciliation with fresh expert feedback. Mordor refreshes the model every twelve months and reruns critical assumptions when material cyber events trigger market repricing.

Why Our Healthcare Cybersecurity Baseline Commands Reliability

Published estimates often diverge because firms differ on what counts as healthcare spend, the aggressiveness of their threat escalation scenarios, and how frequently they refresh numbers.

Key gap drivers include: competitors bundling general corporate security spend into healthcare totals, using static ASP assumptions that ignore post-Change Healthcare hikes, and relying on one-off surveys without reconciling them with breach statistics or device shipment data that Mordor's team tracks quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.78 B (2025) | Mordor Intelligence | - |

| USD 22.52 B (2025) | Global Consultancy A | Excludes managed detection & response and third-party risk services |

| USD 20.40 B (2024) | Industry Association B | Uses hospital IT budgets only, omits payer and pharma spend |

| USD 18.20 B (2023) | Regional Consultancy C | Older base year, ASPs not adjusted for 2024 ransomware premium |

In sum, by tethering revenue to transparent breach metrics and device counts, and by updating assumptions after every major incident, Mordor Intelligence delivers a balanced, traceable baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

Why is the Healthcare Cybersecurity Market growing faster than other critical-infrastructure sectors?

The sector’s high-value data, strict new device regulations, and the record 677 breaches logged in 2024 are pushing annual spending up 18.26% during 2026-2031.

Which segment of the Healthcare Cybersecurity Market will grow the fastest to 2031?

Cloud-security solutions are projected to post an 18.58% CAGR as hospitals migrate EHRs and imaging archives to public and hybrid clouds.

How large is the North American Healthcare Cybersecurity Market in 2025?

North America represents 34.12% of global revenue, buoyed by HIPAA enforcement and federal cyber spending programs.

What is Section 524B and why does it matter

Section 524B of the FD&C Act obliges every new connected medical device to include a cybersecurity plan and SBOM, forcing manufacturers and providers to invest in life-cycle security management

How are small and rural hospitals addressing cybersecurity with limited budgets?

Many leverage federal grants and managed detection-and-response subscriptions, such as Microsoft’s Rural Hospital Program, which offers AI-aided risk assessments at no cost.

Page last updated on: