Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

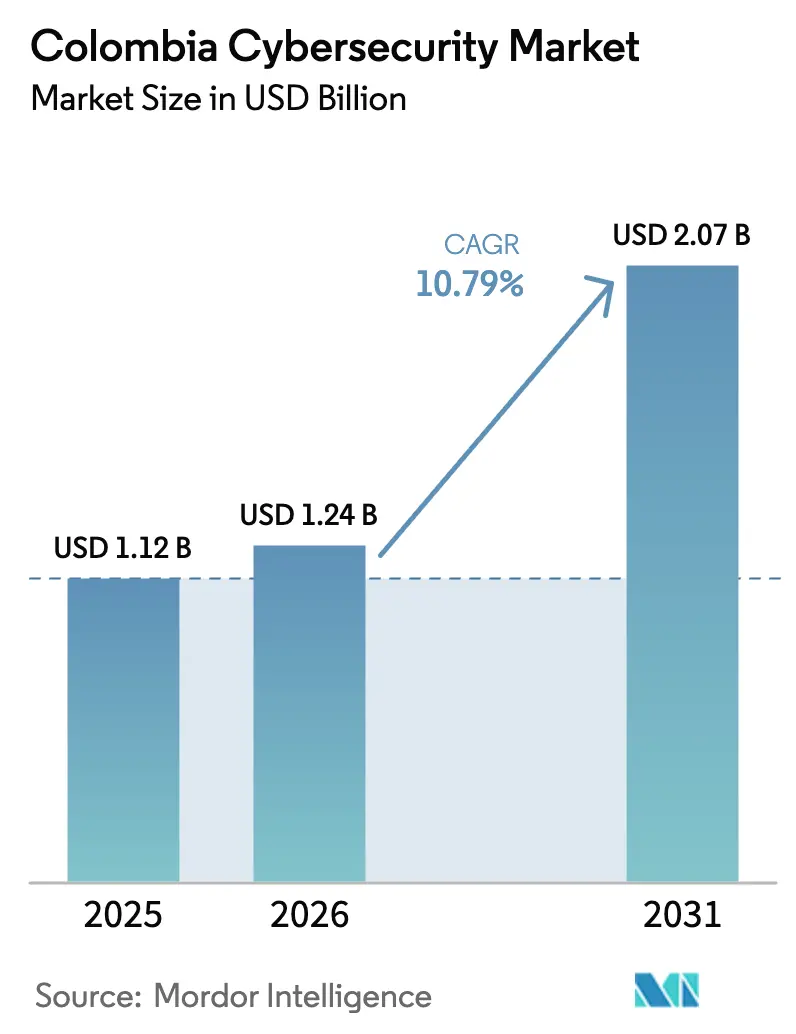

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 10.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Cybersecurity Market Analysis by Mordor Intelligence

The Colombia cybersecurity market size is projected to be USD 1.12 billion in 2025, USD 1.24 billion in 2026, and reach USD 2.07 billion by 2031, growing at a CAGR of 10.79% from 2026 to 2031. Threat volume remains the primary growth catalyst, with the country absorbing 36 billion malicious events in 2024 that accounted for 25% of Latin American incidents. A national Security Operations Center, launched in January 2025, is resetting public-sector security baselines and encouraging private firms to align controls with government playbooks. Instant-payment adoption after the October 2025 launch of Bre-B is expanding real-time fraud vectors and accelerating demand for behavioral analytics in financial services. Parallel enforcement of Law 1581 and External Circular 001 is pushing enterprises to adopt privacy-by-design frameworks, thereby elevating investment priorities for data governance tools. Finally, recurring supply-chain outages, such as the July 2024 CrowdStrike disruption, are reinforcing multi-vendor strategies that favor open, interoperable detection and response stacks.

Key Report Takeaways

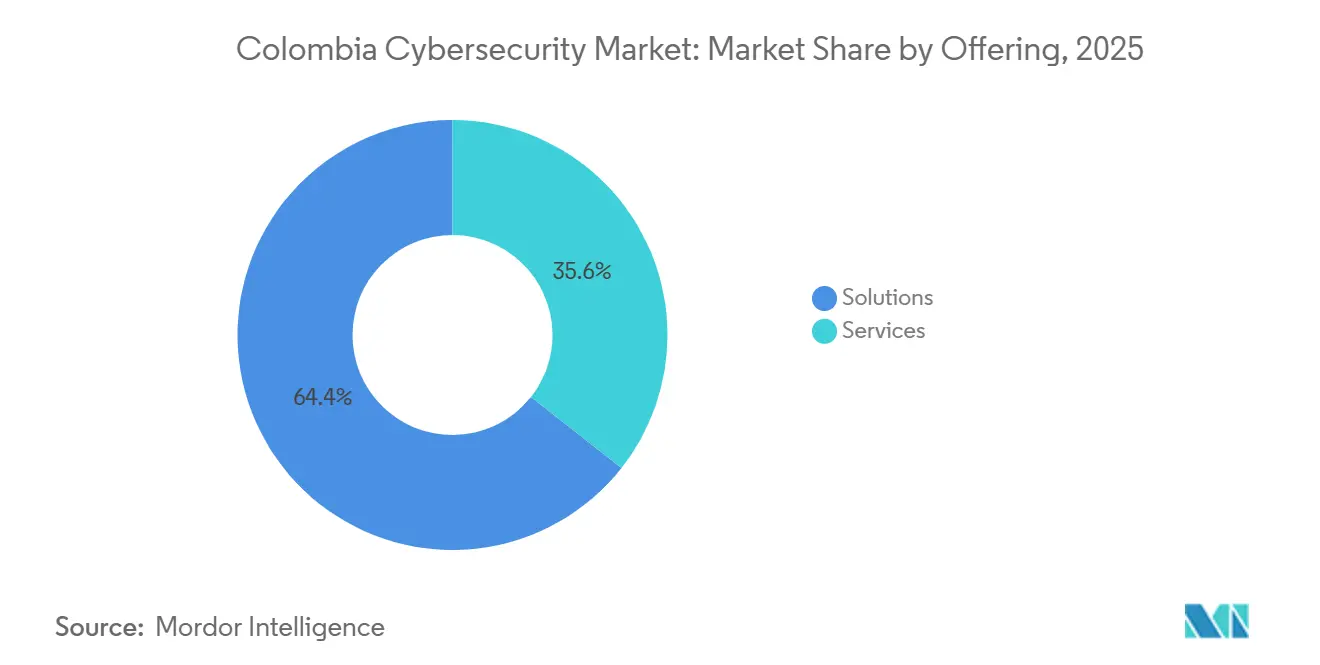

- By offering, solutions led with 64.38% Colombia cybersecurity market share in 2025, while services are advancing at an 11.23% CAGR through 2031.

- By deployment mode, cloud platforms commanded 62.36% of the 2025 Colombia cybersecurity market size and are expanding at an 11.04% CAGR on the back of SME migrations.

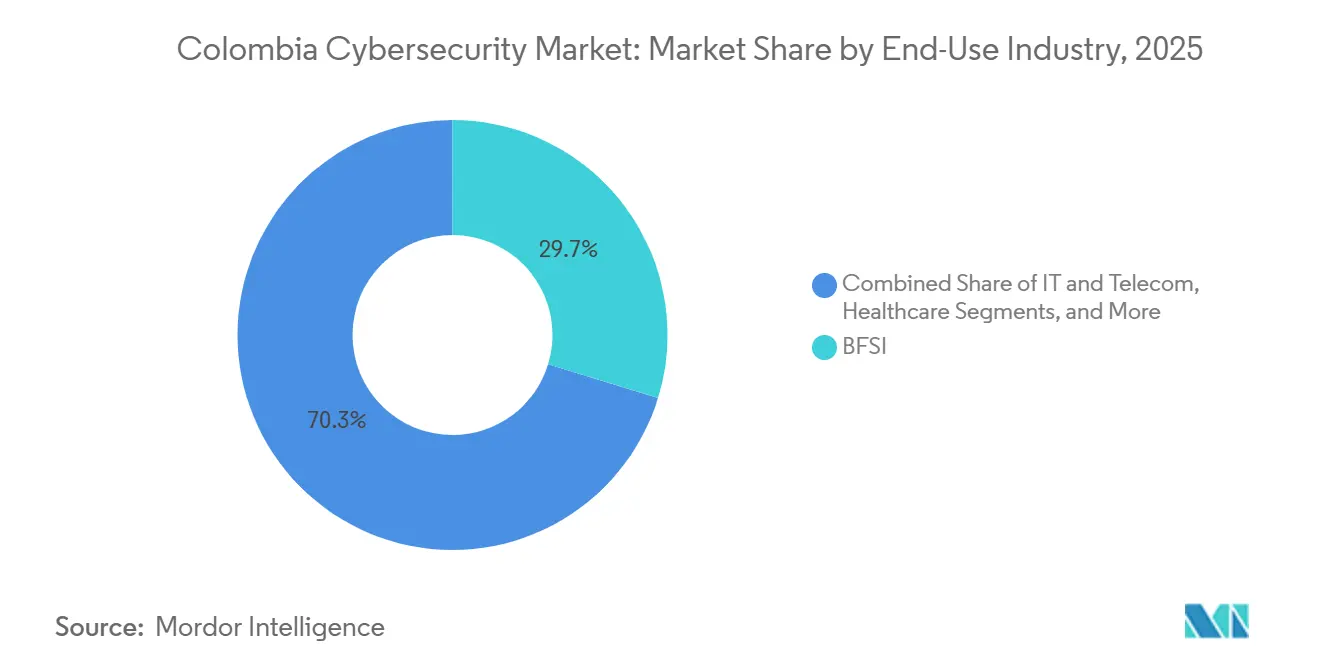

- By end-use industry, banking, financial services, and insurance captured 29.73% of 2025 spending, whereas healthcare is projected to grow at a 12.16% CAGR to 2031.

- By enterprise size, large organizations accounted for 61.83% of 2025 revenue, but SMEs are forecast to rise at an 11.84% CAGR under tighter data-protection enforcement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cyber Attacks on Critical Infrastructure | +2.3% | National, led by Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Accelerated Government Digital Services | +1.9% | National, early gains in Bogotá, Barranquilla, Cartagena | Medium term (2-4 years) |

| Enforcement of Data-Protection Regulation | +1.6% | National | Medium term (2-4 years) |

| Surge in Cloud Adoption among SMEs | +1.8% | National, higher urban penetration | Medium term (2-4 years) |

| Fintech Sandbox Expansion Driving API Security | +1.4% | Bogotá fintech corridor | Short term (≤ 2 years) |

| Nearshore Outsourcing Boosting Compliance Demand | +1.5% | Bogotá, Medellín, Barranquilla | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber Attacks on Critical Infrastructure

Colombia ranked second in Latin America for attempted intrusions in 2024, with utilities, telecom backbones, and energy grids enduring persistent ransomware and living-off-the-land tactics. The 2023 IFX Networks breach impaired 762 corporate clients, demonstrating cascading risk in shared hosting environments. Decree 338 now compels critical operators to disclose incidents within 24 hours, compressing response cycles and driving adoption of managed detection and deception tooling.[1]Ministerio de Tecnologías de la Información y las Comunicaciones, “Estrategia Nacional de Ciberseguridad 2025,” mintic.gov.co Refresh intervals for perimeter devices have fallen from five years to 18 months as boards demand resilience metrics. In parallel, behavioral analytics and automated playbooks are moving from pilot to production to counter evasion techniques that bypass signature engines.

Accelerated Government Digital Services

The national Security Operations Center aggregates telemetry across ministries, enabling real-time threat sharing that shortens dwell time for public portals. Digital identity issuance surpassed 5 million credentials by July 2024, expanding authentication attack vectors. Phishing campaigns now replicate tax and subsidy portals, forcing adoption of multi-factor authentication and continuous authorization guards. The CONPES 3995 policy further obliges agencies to conduct annual risk reviews, channeling budget toward identity governance and zero-trust pilots. Collectively, these measures embed cybersecurity in public-sector modernization roadmaps and create a replicable control blueprint for private firms.

Enforcement of Data-Protection Regulation

Sanctions under Law 1581 climbed 22% in 2024 as the Superintendencia de Industria y Comercio moved from guidance to penalties. External Circular 001 of 2025 introduced biometric governance rules that require algorithmic transparency for credit-scoring engines, stimulating demand for privacy-enhancing technologies. Law 2502 classified misuse of artificial intelligence as an aggravating factor in identity theft, extending liability to firms deploying untested models. Enterprises are now integrating differential privacy into analytics pipelines and automating compliance reports to avoid fines of up to 2% of annual revenue. Board oversight is tightening, and budgets for privacy impact assessments are increasing accordingly.

Surge in Cloud Adoption among SMEs

Consumption-based SaaS bundles are lowering capital barriers for SMEs, which historically deferred security upgrades due to cost. The International Chamber of Commerce found cloud uptake rising fastest among urban micro-enterprises that value predictable monthly fees. Public cloud providers now offer Colombian data-center regions and customer-managed encryption keys to satisfy residency concerns. Nevertheless, misconfigured storage buckets and permissive identity roles caused a noticeable share of breaches in 2025, prompting Superintendencia Financiera guidance on baseline controls for outsourced workloads. As a result, posture-management and container-security tools are gaining traction within SME budgets.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Sensitivity among SMEs | -1.2% | Secondary cities nationwide | Medium term (2-4 years) |

| Acute Cybersecurity Talent Shortage | -1.5% | Bogotá and Medellín | Long term (≥ 4 years) |

| Limited Cyber Insurance Penetration | -0.7% | National | Medium term (2-4 years) |

| Fragmented Rural Connectivity | -0.6% | Remote and rural locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Cybersecurity Talent Shortage

Colombia needs an additional 5,000 practitioners, with deficits most acute in cloud architecture and incident response. University curricula trail industry requirements, prompting firms to outsource tier-one tasks to managed service providers. Automation is filling part of the gap, yet vendor concentration risks linger as a handful of MSSPs dominate outsourcing awards. Premium salary pressure is lifting total cost of ownership for in-house security functions, motivating demand for low-code orchestration platforms that compress manual workloads.

High Upfront Cost Sensitivity among SMEs

An ICC survey showed delivery cost and financing hurdles as primary blockers to ICT investment for 617 Colombian MSMEs.[2]International Chamber of Commerce, “ICT Adoption Survey Colombian MSMEs 2024,” iccwbo.org While pay-per-user options shift spending to operating budgets, small firms face bill-shock risk when usage outpaces forecasts. Integration complexity mounts as point solutions proliferate without native interoperability. Absent subsidies or tax incentives, laggards cling to legacy antivirus, widening the maturity gap between security-forward and resource-constrained SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Share as Talent Deficit Persists

Solutions accounted for 64.38% Colombia cybersecurity market share in 2025, while services are expanding at an 11.23% CAGR as firms outsource threat hunting and incident response to offset local skills shortages. Professional services are surging among enterprises pursuing ISO 27001 or SOC 2 Type II attestations, whereas managed detection and response is penetrating mid-market manufacturers that lack in-house security operations centers. Within solutions, cloud security and identity governance posted the highest budget gains, driven by workload migration and zero-trust mandates. Application security spend is accelerating in fintechs that must protect open-banking endpoints specified by the Superintendencia Financiera. Network and endpoint controls remain foundational but are commoditizing as vendors fold them into unified appliances.

Service growth is also underpinned by vendor diversification strategies triggered by the July 2024 CrowdStrike outage, which renewed interest in multi-vendor extended detection and response architectures that reduce monoculture risk. Integrated risk-management platforms are gaining popularity among boards that demand dashboards translating vulnerability data into financial exposure. Overall, the services uptrend reflects a structural shift from product acquisition to outcome-based contracting across the Colombia cybersecurity market.

By Deployment Mode: Cloud Dominates as Consumption Models Lower Barriers

Cloud platforms captured 62.36% of the 2025 Colombia cybersecurity market size and are set to expand at an 11.04% CAGR through 2031. Financial-sector clarity under External Circular 005, which allows non-core workloads in public cloud subject to compensating controls, is catalyzing lift-and-shift projects.[3]Superintendencia Financiera de Colombia, “Circular Externa 005 de 2019,” superfinanciera.gov.co Cloud-native vendors embed policy guardrails in infrastructure-as-code templates, enabling DevSecOps teams to enforce compliance on first deployment. Misconfiguration remains a leading breach vector, spurring rapid uptake of posture-management tools.

Latency-sensitive utilities and telecom operators still favor on-premises monitoring to meet 24-hour incident reporting mandated by Decree 338. As a result, hybrid architectures that split sensitive workloads on-site while pushing analytics to the cloud are emerging as pragmatic middle ground. The outcome is a deployment spectrum where cloud retains the growth edge, but localized control planes remain integral to critical infrastructure resilience within the Colombia cybersecurity market.

By End-Use Industry: Healthcare Accelerates as Telemedicine Expands Attack Surface

Banking, financial services, and insurance led 2025 spending, owning 29.73% of the Colombia cybersecurity market, a position reinforced by Bre-B instant payments that drove new volumes across application programming interfaces. Banks are layering behavioral biometrics and graph analytics to combat account takeover and money-laundering schemes. Healthcare is projected to grow at a 12.16% CAGR, the fastest among verticals, as electronic health-record mandates and telemedicine expand ransomware exposure. Enforcement actions under Law 1581 are compelling hospitals to encrypt data in transit and restrict role-based access, elevating security maturity.

Retail, industrial manufacturing, energy, and government follow, each confronting sector-specific risks. Manufacturers are hardening supervisory control and data-acquisition environments, while energy operators implement segmentation and intrusion detection systems to satisfy Decree 338. Collectively, divergent risk profiles are driving tailored control frameworks, but healthcare’s rapid digitalization positions it as the breakout growth engine inside the broader Colombia cybersecurity market.

By End-User Enterprise Size: SMEs Accelerate under Regulatory Pressure

Large enterprises generated 61.83% of 2025 revenue, leveraging mature security operations centers and multi-vendor stacks to avoid single-point failure. These firms are piloting extended detection and response that unifies endpoint, network, and cloud telemetry to speed investigation cycles. SMEs, however, are forecast to rise at an 11.84% CAGR as regulatory fines climb. Per-user bundles like Microsoft 365 E5 are popular for turning capex into opex and delivering preset security policies.

Operationalizing these suites remains challenging without dedicated staff, prompting SMEs to contract turnkey monitoring from managed security providers. Cost sensitivity persists, but enforcement momentum suggests continued SME uplift as compliance graduates from advisory to punitive across the Colombia cybersecurity market.

Geography Analysis

Bogotá dominates spending, propelled by dense financial and governmental footprints that face strict oversight under Law 1581 and Decree 338. Medellín’s fintech corridor hosts 394 sandbox startups that prioritize API security and fraud analytics to meet External Circular specifications. Cali and Barranquilla follow as industrial and logistics hubs investing in operational technology protection. Rural regions remain constrained by patchy connectivity that limits cloud-delivered security enforcement.

National initiatives, including the Security Operations Center and refreshed cybersecurity strategy, aim to widen defensive parity, but execution risk tied to budgets and skills could slow rural rollout. Nearshore outsourcing clients are imposing ISO 27001 and SOC 2 Type II requirements, elevating baseline practices in Bogotá and Medellín service providers.

Geography therefore acts as a demand differentiator, with urban centers capturing the bulk of incremental Colombia cybersecurity market growth until infrastructure gaps close.

Competitive Landscape

Global incumbents Cisco, Palo Alto Networks, Fortinet, Microsoft, and IBM command enterprise contracts via local integrators, yet cloud-native challengers such as Zscaler, CrowdStrike, and SentinelOne are winning mid-market deals with consumption-based licenses. The 2024 CrowdStrike outage spotlighted monoculture risk and triggered board-level mandates for multi-vendor extended detection architectures, benefiting API-centric platforms.[4]Microsoft Threat Intelligence Center, “Analysis of the July 2024 Endpoint Outage,” microsoft.com Vertical specialization is intensifying, with vendors tailoring modules for banking fraud, healthcare compliance, and manufacturing operational technology controls.

White-space persists in managed detection for mid-tier manufacturers and API security for fintechs. Regional MSSPs differentiate with in-country data residency and Spanish-language support that align with Superintendencia compliance demands.

Certification holdings, especially ISO 27001 and SOC 2 Type II, increasingly tilt contract awards, embedding governance expectations into product roadmaps. Overall, functional breadth, automation depth, and compliance alignment define the competitive battleground inside the Colombia cybersecurity market.

Colombia Cybersecurity Industry Leaders

Cisco Systems Inc.

Palo Alto Networks Inc.

Fortinet Inc.

IBM Corporation

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft Copilot for Security added Spanish language support for incident summaries, enhancing analyst productivity in Colombian MSSPs.

- January 2026: MinTIC initiated a pilot to extend the national threat-intelligence feed to 10 rural municipalities, targeting full coverage by 2028.

- October 2025: Bre-B instant payments launched, onboarding 30 million users within weeks and catalyzing real-time fraud detection investments.

- June 2025: Colombia published an updated national cybersecurity strategy, prioritizing workforce development and public-private threat exchange.

Colombia Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Colombia Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the projected value of the Colombia cybersecurity market by 2031?

It is forecast to reach USD 2.07 billion, reflecting a 10.79% CAGR from 2026 to 2031.

Which deployment mode is growing fastest in Colombia?

Cloud-based security, which held 62.36% share in 2025 and is advancing at an 11.04% CAGR through 2031.

Why is healthcare spending on cybersecurity accelerating?

Telemedicine expansion and electronic health-record mandates are increasing ransomware exposure, driving a 12.16% forecast CAGR for the sector.

How severe is Colombia’s cybersecurity talent gap?

The country needs roughly 5,000 additional professionals, particularly in cloud architecture and incident response.

What regulatory changes are shaping security investment?

Stricter enforcement of Law 1581, External Circular 001 of 2025, and Law 2502 are shifting budgets toward privacy-by-design and AI governance controls.

Which segments are most attractive for new entrants?

Managed detection and response for mid-market manufacturers and API security solutions for fintech startups present significant growth opportunities.

Page last updated on: