Liquid Roofing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

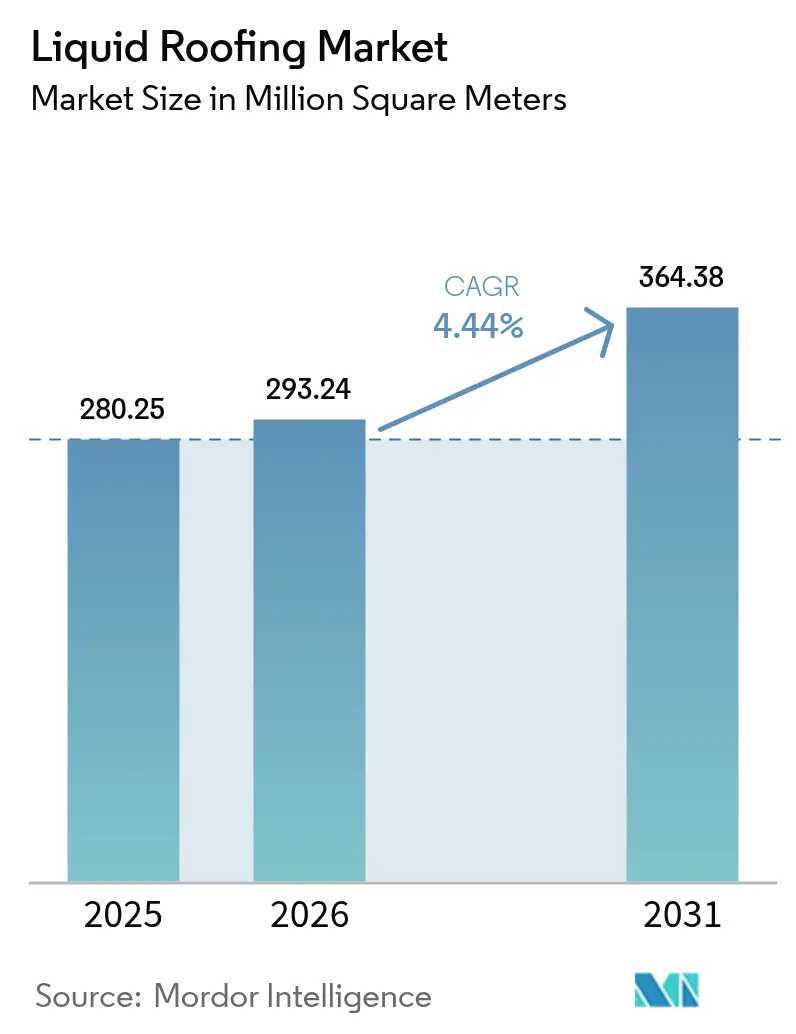

| Market Volume (2026) | 293.24 Million square meters |

| Market Volume (2031) | 364.38 Million square meters |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Roofing Market Analysis by Mordor Intelligence

The Liquid Roofing Market size is expected to grow from 280.25 million square meters in 2025 to 293.24 million square meters in 2026 and is forecast to reach 364.38 million square meters by 2031 at a 4.44% CAGR over 2026-2031. Intensifying climate risk, insurer-driven roof-condition scoring, and rapid gains in digital diagnostics are reshaping demand away from reactive patching toward preventive, data-ready liquid systems. Acrylic chemistry still accounts for more than half of global volume, yet silicone, polyurea, and hybrid technologies are winning share wherever long-term UV stability, fast return-to-service, or embodied-carbon limits dominate specification decisions. Flat-roof construction linked to data centers and logistics hubs accelerates segment growth, while residential re-roofing mandates in hurricane and hail corridors create a dependable baseline of recurring demand. Competitive intensity remains moderate because the top five suppliers control only about two-fifths of worldwide shipments, leaving room for regional specialists to monetize labor-saving equipment, green-roof substrates, and photovoltaic underlayments.

Key Report Takeaways

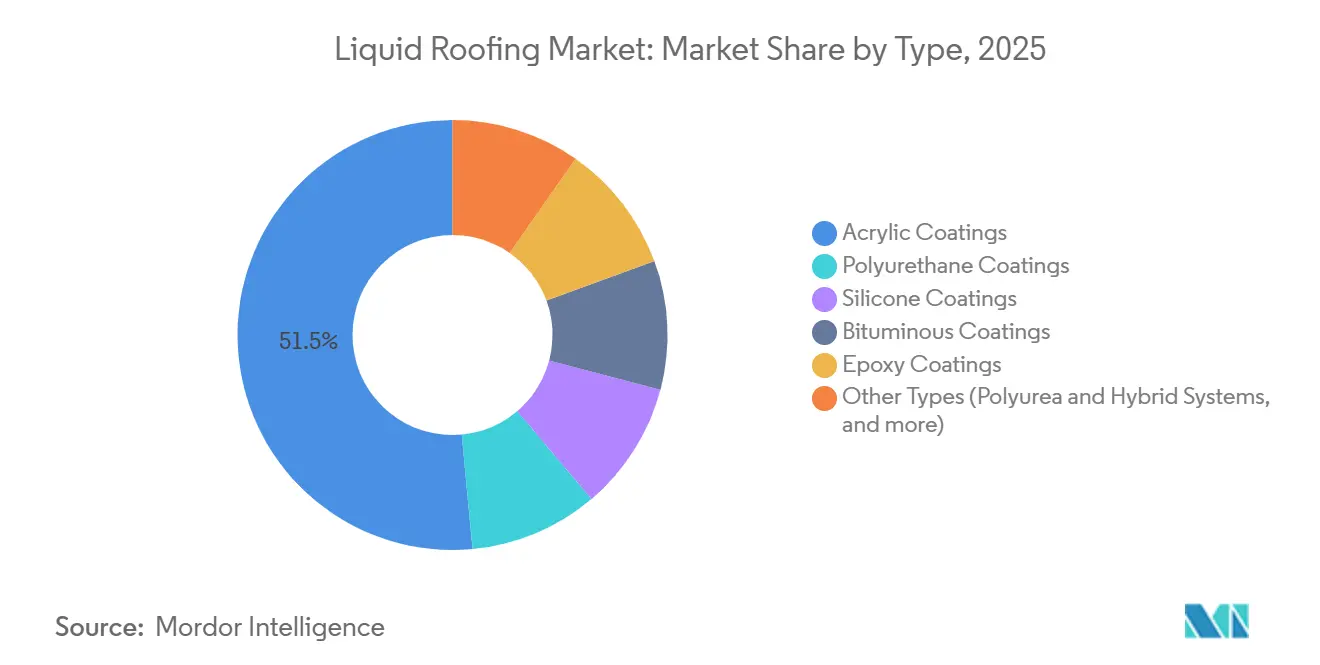

- By type, acrylic coatings led with 51.49% share in 2025, and silicon type is set to expand at the fastest CAGR of 5.04% to 2031.

- By application, flat roofs commanded 61.64% of the liquid roofing market share in 2025 and are forecast to grow at a 5.96% CAGR through 2031, driven by ponding resistance needs in commercial buildings.

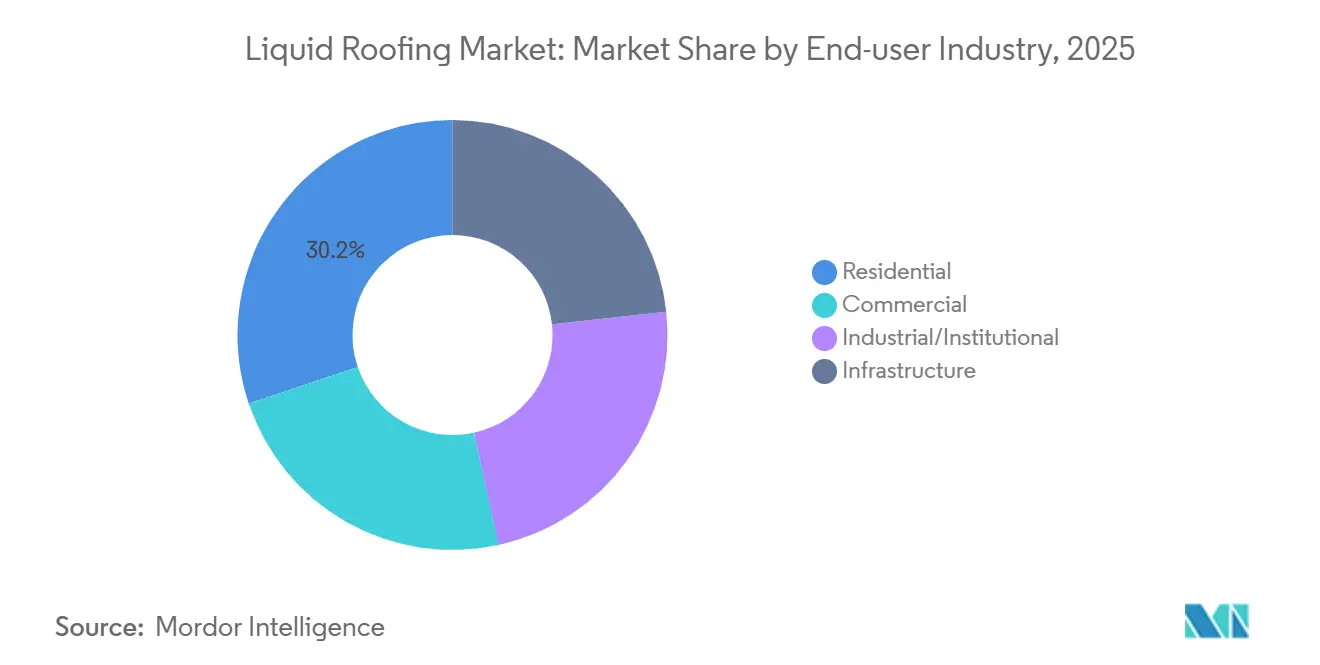

- By end user, the residential segment captured a 30.18% share in 2025 while advancing at the fastest 4.89% CAGR, as single-family and multifamily owners shift from tear-off reroofing to re-coat cycles.

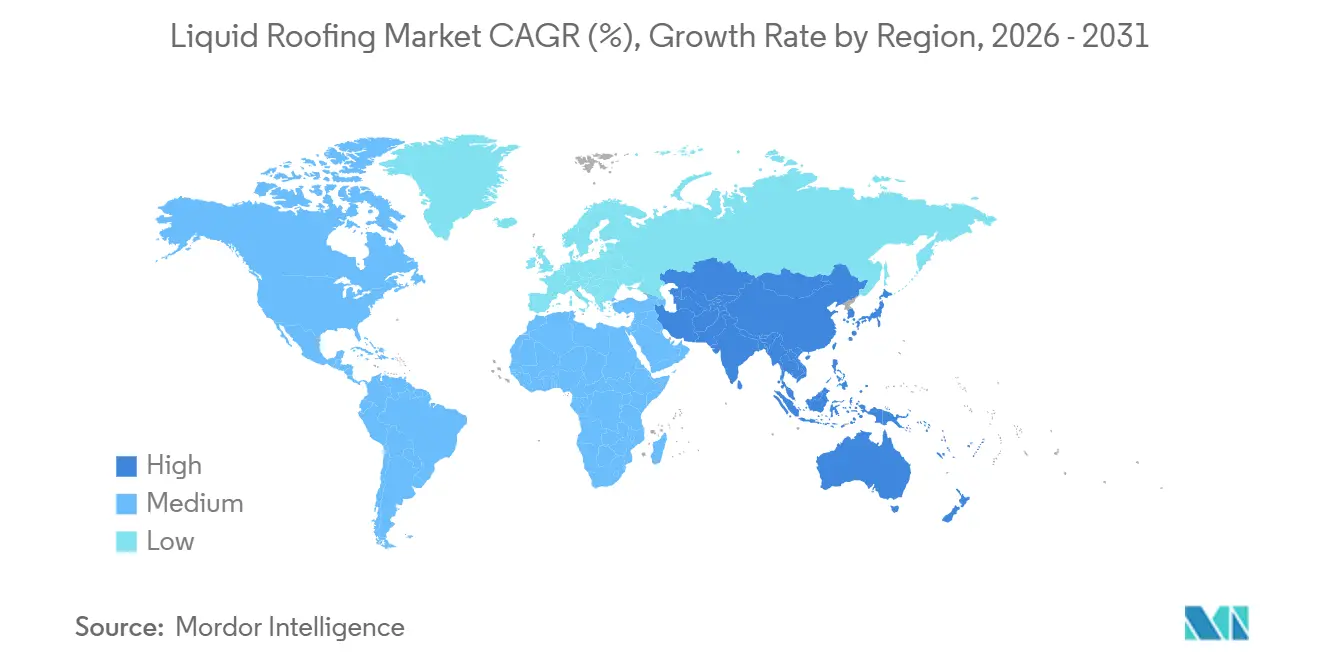

- By geography, Asia-Pacific dominated with a 41.20% share in 2025 and is poised for a 4.80% CAGR to 2031 on the back of megacity infrastructure programs that favor field-applied waterproofing.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Roofing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging re-roofing demand amid climate-related extreme weather | +0.8% | Global, with acute intensity in North America Gulf Coast, APAC typhoon corridors, Europe Central hailstorm zones | Medium term (2-4 years) |

| Fast-curing polyurea & hybrid systems cut site downtime | +0.6% | North America, Europe, APAC urban centers (data centers, logistics hubs) | Short term (≤ 2 years) |

| Infrastructure stimulus across Asia-Pacific megacities | +0.9% | APAC core (China, India, Indonesia, Vietnam), spill-over to Middle East | Medium term (2-4 years) |

| Insurance premium discounts for resilient liquid membranes | +0.4% | North America, Europe (Germany, France, UK), Australia | Long term (≥ 4 years) |

| AI-based moisture mapping accelerates preventive maintenance | +0.5% | North America, Europe, APAC Tier-1 cities (commercial/institutional segments) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Re-Roofing Demand Amid Climate-Related Extreme Weather

Insurance payouts for roof damage have surged worldwide, pushing owners to upgrade from granular shingles to elastomeric coatings that dissipate hail energy without cracking[1]Verisk, “U.S. 2024 Roof-Related Claims Report,” verisk.com. US hail and wind claims alone reached USD 31 billion in 2024, a 22% jump in one year, and European hailstorms inflicted EUR 4.2 billion in insured losses the same season. In response, carriers increasingly require impact-resistant Class 4 membranes as a condition of policy renewal, converting what used to be discretionary maintenance into a risk-mitigation imperative. Liquid roofs also reduce landfill waste because crews apply new layers over intact decks instead of executing full tear-offs. The combined economics of lower disposal costs and premium discounts firmly embed the liquid roofing market in climate-adaptation budgets.

Fast-Curing Polyurea & Hybrid Systems Cut Site Downtime

Pure polyurea membranes cure within seconds, allowing contractors to reopen data-center or hospital rooftops the same day the job starts. Hybrid polyurea-polyurethane blends add superior adhesion to metal and concrete, addressing delamination that occasionally plagues 100% polyurea. Sikalastic-625 BMS delivers a 2-hour rain-ready window and 35% lower embodied carbon than earlier products, demonstrating that speed need not compromise sustainability[2]Sika, “Sikalastic-625 BMS Technical Data Sheet,” sika.com. Johns Manville’s SeamFree PMMA, launched in 2025, walks on in 30 minutes, providing a spray-gun-free alternative for crews short on specialized equipment. Because 92% of U.S. roofers report difficulty recruiting skilled labor, every minute shaved from cure or setup time translates directly into lower payroll outlays and higher project throughput.

Infrastructure Stimulus Across Asia-Pacific Megacities

Developing Asia needs USD 1.7 trillion in annual infrastructure spending through 2030, according to the Asian Development Bank, and that pipeline is overwhelmingly dominated by flat-roof transit hubs, logistics parks, and industrial estates. China’s 2025 budget earmarks CNY 3.8 trillion (USD 523 billion) for railways, airports, and manufacturing clusters that specify low-slope liquid roofs accommodating HVAC and solar arrays. India’s construction gross value added expanded 7.4% in FY-2026 as cement consumption climbed 8–11%, a forward indicator of rising coating demand. ASEAN projects, from Indonesia’s Batang Industrial Park to Vietnam’s Long Thanh Airport, embed reflective waterproofing layers into energy-efficiency criteria, assuring long-run volume for the liquid roofing market. Contractors favor monolithic liquids over rolled sheets to minimize seam liability on the vast deck areas typical of these megaprojects.

Insurance Premium Discounts for Resilient Liquid Membranes

US underwriters now cut premiums 10–15% on properties protected by UL 2218 Class 4 or FM 4473-approved elastomeric roofs. In Europe, several German and French insurers added drone-based roof-scoring to renewal protocols during 2025, rewarding facilities that maintain intact liquid membranes and penalizing cracked bituminous felts. Economic payback models show that a USD 15,000 coating can return USD 1,200 per year in premium savings, achieving breakeven in less than 13 years, well inside the 20-year design life of today’s silicone systems. Australian carriers apply similar logic in cyclone-prone Queensland, where liquid roofs outperform mechanically fastened sheets on uplift resistance, again reinforcing a favorable risk–reward calculus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate & bitumen prices squeeze margins | -0.7% | Global, acute in Europe and North America where feedstock imports dominate | Short term (≤ 2 years) |

| Tightening regional bans on high-VOC products | -0.5% | Europe (EU Directive 2004/42/EC), California SCAQMD, select APAC cities | Medium term (2-4 years) |

| Skilled-applicator shortage in emerging economies | -0.6% | APAC (India, Indonesia, Vietnam), Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate & Bitumen Prices Squeeze Margins

MDI price swings exceeded 30% during 2024-2025 after unplanned outages at several European plants, while Brent crude fluctuations sent bitumen benchmarks gyrating 18–25% quarter-to-quarter. Contracting firms often bid on projects six to twelve months ahead, leaving producers exposed when feedstock spikes arrive mid-execution. Multinationals hedge, but smaller regional formulators lack low-cost finance or futures market access, forcing them either to absorb shocks or exit polyurethane-heavy lines. Reformulation toward water-based acrylics and high-solids silicones reduces isocyanate dependence, yet slower cure or temperature-sensitivity limits those options on fast-track or winter jobs. The resulting margin compression tempers otherwise healthy headline growth for the liquid roofing market.

Tightening Regional Bans on High-VOC Products

EU Directive 2004/42/EC caps solvent-borne roof coatings at 500 g/L VOC, and member states such as Germany now enforce sub-100 g/L limits in urban air zones. California’s SCAQMD Rule 1113 restricts architectural coatings to 50 g/L, while China’s top-tier cities launched their own VOC fee structures in 2024. The patchwork compels global brands to run duplicate SKUs and invest in water-borne manufacturing lines, driving unit costs 15–25% higher than traditional solvent products. Meanwhile, ASEAN countries with lax rules still welcome cheaper, high-VOC bituminous mastics, forcing suppliers into dual portfolios that complicate inventory while diluting scale economies. Compliance overhead thus slows penetration, especially for startups that cannot amortize reformulation across a broad base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silicone Momentum Builds on Superior UV Durability

Acrylics accounted for 51.49% of 2025 volume, anchoring the cost-sensitive core of the liquid roofing market. Their water-borne chemistry offers respectable reflectivity and substrate versatility at installation prices 20–30% below silicone. However, silicone coatings are advancing at a 5.04% CAGR because their dirt resistance and color stability halve recoating frequency in high-irradiance regions, lowering lifecycle cost despite higher purchase price. Polyurethane sits between the two, prized for chemical and abrasion resistance on industrial decks, yet prone to UV chalking unless top-coated, a drawback increasingly cited in bid specifications. Polyurea and hybrid systems, though still niche, unlock unique value, second-level cure, and year-round application, which contractors select for critical facilities despite premium pricing. EU rules now require Environmental Product Declarations, a mandate that amplifies the appeal of low-carbon acrylic and silicone recipes and could further tilt the liquid roofing market share mix during the forecast window.

Across all chemistries, the push toward bio-based polyols and recycled fillers accelerates, driven by public procurement scoring. Sika’s 2024 introduction of a bio-content hybrid with 35% lower embodied carbon exemplifies competitive positioning through sustainability credentials. Meanwhile, pure polyurea adoption spreads from oil-sand work camps and freezer warehouses into municipal transit platforms once deemed too cost-sensitive; here, minimal shutdowns outweigh material premiums. Suppliers that bundle coatings with cloud-connected quality-assurance sensors deepen loyalty because the data stream proves compliance long after installation. Over the next five years, type-level differentiation will pivot less on standalone chemistry and more on total-system packages, primer, membrane, finish, and analytics, that blend speed, durability, and verified carbon metrics for increasingly sophisticated buyers in the liquid roofing market.

By Application: Flat Roofs Capture Solar and HVAC Upside

Flat roofs seized 61.64% of 2025 demand and are forecast to grow 5.96% a year, outstripping every other application category. Data-center investment alone is projected to jump from USD 28 billion in 2024 to USD 45 billion by 2028, and those facilities universally favor low-slope decks for rooftop chillers and photovoltaic arrays. France’s 2024 code requiring at least 30% of commercial rooftop area to host solar panels or green roofs further institutionalizes flat-roof dominance in Europe. Liquid membranes excel here because they create monolithic barriers free of seams, a critical advantage when penetrations for inverters, conduits, and HVAC curbs number in the hundreds. In terms of the liquid roofing market size, the flat-roof subsegment is on track to surpass 230 million square meters by 2031 if present trajectories hold.

Pitched roofs, linked mostly to single-family homes, advance more slowly but remain meaningful due to storm-driven re-roofing in the US Sunbelt and European countryside. Liquids enter these steep slopes mainly as restorative top coats, extending asphalt life by up to ten years and qualifying for insurer rebates tied to impact resistance. Domed and complex-geometry roofs, while niche, rely almost exclusively on spray liquids because rolled goods are labor-prohibitive on curved surfaces. High-profile sports venues now specify polyurea under ETFE skylights to guard against condensation, illustrating application diversity. Even within the fast-growing flat cohort, specification patterns diverge: warehouses pick budget acrylics, data centers pay for silicone or hybrid polyurea, and public transit opts for low-VOC water-bornes to satisfy procurement rules. Such complexity reinforces why application-centric marketing outperforms one-size-fits-all tactics in the liquid roofing market.

By End-User Industry: Residential Baseline, Industrial Upside

Residential buyers absorbed 30.18% of global volume in 2025 and are forecast to expand 4.89% yearly as aging shingle roofs reach end-of-life across North America and Europe. US building codes in hurricane alley now encourage elastomeric retrofits that earn homeowners double-digit insurance discounts, catalyzing a steady replacement cadence even when macro housing starts fluctuate. Price sensitivity dominates, so acrylic remains the default, but silicone’s lifecycle gap is narrowing as homeowners factor in fewer recoats and cooler attic temperatures that trim utility bills.

Commercial end-users, offices, retail, hospitality, select reflective membranes that shave cooling loads and unlock LEED points, putting silicone and hybrid PMMA in pole position. Industrial plants and institutional campuses, comprising roughly 35–40% of the liquid roofing market size, readily absorb premium polyurea because avoiding production downtime eclipses first-cost math. Hospitals value seamless waterproofing under helipads, while schools bid fast-cure systems during limited summer breaks. Infrastructure, bridges, train stations, parking decks, leans toward high-build polyurea that pairs abrasion resistance with chemical durability. The segmentation shows a bifurcated demand structure: residential growth supplies predictable volume; industrial and infrastructure projects deliver high-margin upside, together sustaining the broader liquid roofing market.

Geography Analysis

Asia-Pacific controlled 41.20% of 2025 volume and is projected to maintain a 4.80% CAGR to 2031 on the back of megacity infrastructure and manufacturing build-outs. China’s 2025 plan allocates CNY 3.8 trillion to rail and industrial hubs, and liquid membranes feature prominently in waterproofing specifications due to speed and low-slope compatibility. India’s cement output, an early indicator of slab and roof demand, rose 8–11% year-on-year through mid-2026, aligning with accelerating consumption of acrylic and silicone coatings. Southeast Asia’s export-processing zones, from Vietnam’s Phu My 3 to Indonesia’s Batang Industrial Park, increasingly require reflective roofs to meet investor carbon protocols, ensuring strong uptake across the liquid roofing market.

North America represents a majority of the worldwide shipments, with US data-center construction alone climbing 26% in 2026. Canadian wildfire rebuilds and Mexican hurricane repairs further lift regional re-roofing. Insurers have started algorithmic roof scoring that penalizes cracked felts, thereby steering owners toward elastomeric liquids, a policy dynamic unique to the mature but opportunity-rich North American slice of the liquid roofing market.

In Europe, macro construction shrank 0.5% month-to-month in early 2025 as housing starts stalled in Germany and France. Nonetheless, EU climate plans and ultra-low-VOC mandates deliver a quality over quantity story; high-solids silicone and water-based acrylic now dominate specifications, commanding premiums that offset flat regional volume. Southern Europe, led by Spain’s 11.2% surge in December 2024 construction tied to tourism projects, bucked the slowdown, illustrating intra-regional divergence. Strict CPR and diisocyanate-training rules raise entry barriers, consolidating share with incumbents able to finance compliance while shrinking the addressable pool for budget imports.

Competitive Landscape

The liquid roofing market exhibits moderate fragmentation. Technology remains the principal battleground. Johns Manville’s SeamFree PMMA competes head-to-head with polyurea on cure speed but needs no plural-component guns, appealing to labor-short contractors. Sika counters with bio-content hybrids that not only cure fast but also slash embodied carbon, a feature prized in EU public tenders. Digitalization forms the third vector: vendors bundle cloud-linked moisture sensors and QA dashboards to lock in specifiers for the next maintenance cycle, turning membranes into data platforms.

Liquid Roofing Industry Leaders

Sika AG

RPM INTERNATIONAL INC.

Carlisle Companies Incorporated

Akzo Nobel N.V.

Standard Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain completed the acquisition of FOSROC, broadening its construction-chemicals portfolio and adding liquid roofing lines to its global network.

- February 2024: Mapei SpA acquired Bitumat in Saudi Arabia, enhancing market access for liquid waterproofing systems across the Gulf Cooperation Council region.

Global Liquid Roofing Market Report Scope

Liquid roofing is a liquid material applied to a roof or top surface of a construction to create a watertight layer or membrane. It is highly used for flat roofs, pitched roofs, and, in some cases, domed roofs. Liquid roofing is mainly made from acrylics, polyurethane, bitumen, silicone, and epoxy materials and is used for roofs and top surfaces of residential, commercial, industrial, and institutional buildings and infrastructure.

The liquid roofing Market is segmented into type, application, end-user industry, and geography. By type, the market is segmented into polyurethane coatings, acrylic coatings, bituminous coatings, silicone coatings, epoxy coatings, and other types (modified silane polymers, liquid butyl rubber, elastomeric liquid coatings, and cementitious liquid membranes). By application, the market is segmented into domed roofs, pitched roofs, and flat roofs. By end-user industry, the market is segmented into residential, commercial, industrial/institutional, and infrastructure. The report also covers the market size and forecasts for the Liquid Roofing Market in 17 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts were made on the basis of volume (square meters).

| Polyurethane Coatings |

| Acrylic Coatings |

| Silicone Coatings |

| Bituminous Coatings |

| Epoxy Coatings |

| Other Types (Polyurea & Hybrid Systems, etc.) |

| Flat Roofs |

| Pitched Roofs |

| Domed Roofs |

| Residential |

| Commercial |

| Industrial/Institutional |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Polyurethane Coatings | |

| Acrylic Coatings | ||

| Silicone Coatings | ||

| Bituminous Coatings | ||

| Epoxy Coatings | ||

| Other Types (Polyurea & Hybrid Systems, etc.) | ||

| By Application | Flat Roofs | |

| Pitched Roofs | ||

| Domed Roofs | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial/Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What will the global liquid roofing market reach by 2031?

It is forecast to reach 364.38 million square meters by 2031 at a 4.44% CAGR.

Which coating type currently dominates worldwide liquid roofs?

Water-based acrylic coatings led with 51.49% of 2025 volume.

Why are flat roofs the fastest-growing application?

Data-center, warehouse, and logistics construction favors low-slope decks that effortlessly integrate HVAC and solar equipment.

How do insurers influence liquid roof adoption?

Carriers in the US and Europe now grant 10–15% premium discounts for UL 2218 Class 4 or equivalent elastomeric membranes

Which region supplies the highest volume growth through 2031?

Asia-Pacific, propelled by infrastructure megaprojects in China, India, and ASEAN markets, expands at 4.80% a year.

Page last updated on: