Roofing Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 111.65 Billion |

| Market Size (2031) | USD 139.32 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

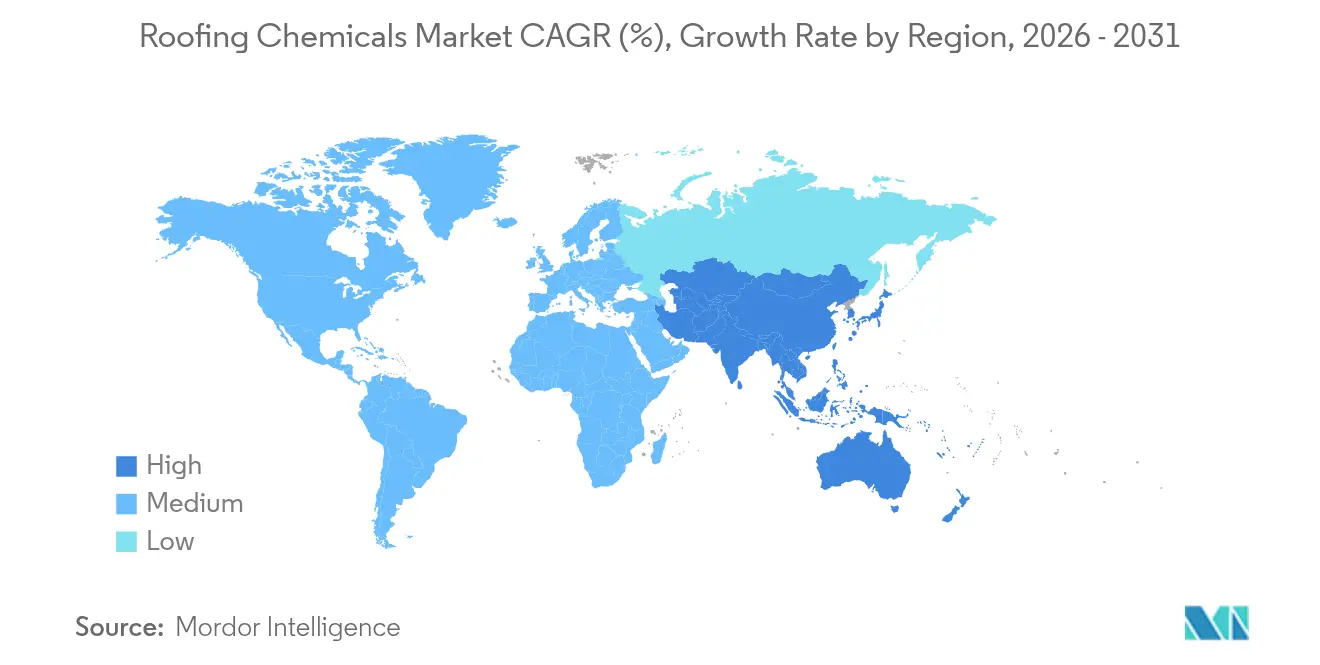

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Roofing Chemicals Market Analysis by Mordor Intelligence

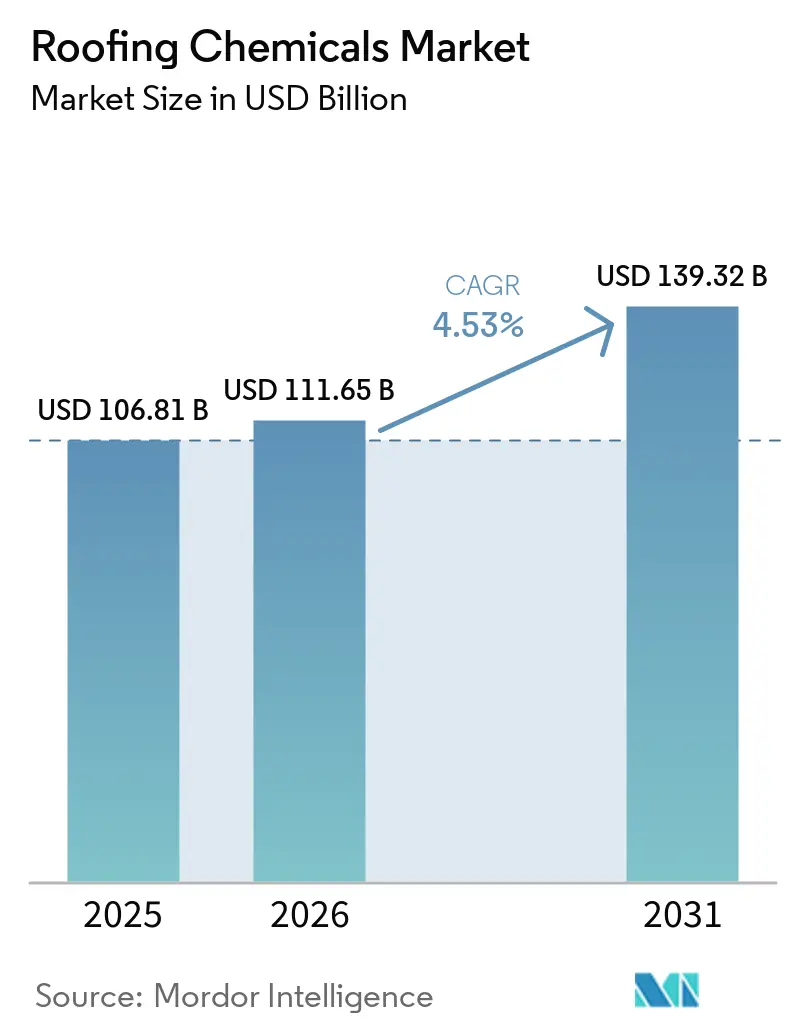

The Roofing Chemicals market size is expected to grow from USD 106.81 billion in 2025 to USD 111.65 billion in 2026 and is forecast to reach USD 139.32 billion by 2031 at 4.53% CAGR over 2026-2031. A steady replacement cycle in mature economies combines with rising new-build activity in Asia-Pacific to keep demand on an upward trajectory. Construction stimulus programs, intensifying weather-related roof failures and stricter energy codes are widening the application scope of polymer-modified, low-VOC and reflective chemistries. Bituminous systems still dominate project specifications, yet polyurethane, acrylic and silicone alternatives are scaling quickly as building owners prioritize lifecycle value and regulatory compliance. Market fragmentation remains high, but consolidation momentum is accelerating as suppliers seek cost leverage, geographic reach and technology depth.

Key Report Takeaways

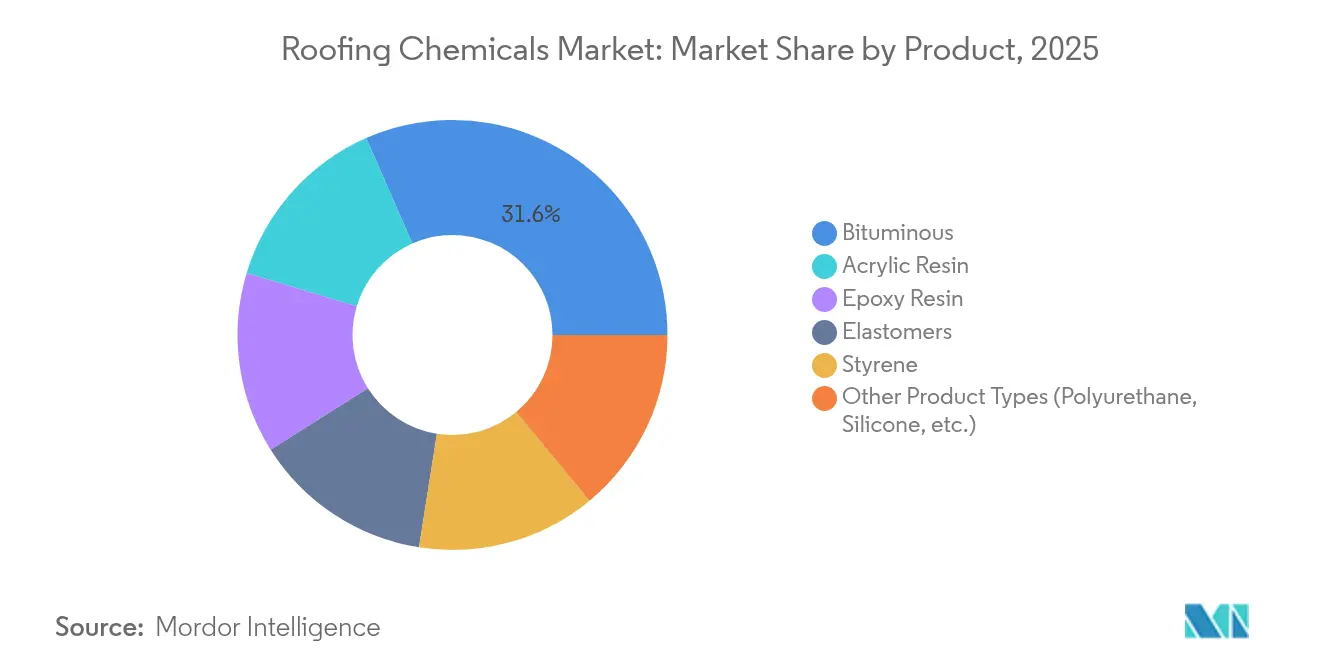

- By product type, bituminous products led with 31.58% of the roofing chemicals market share in 2025, while other product types such as polyurethane- and silicone-based systems are projected to expand at 5.44% CAGR through 2031.

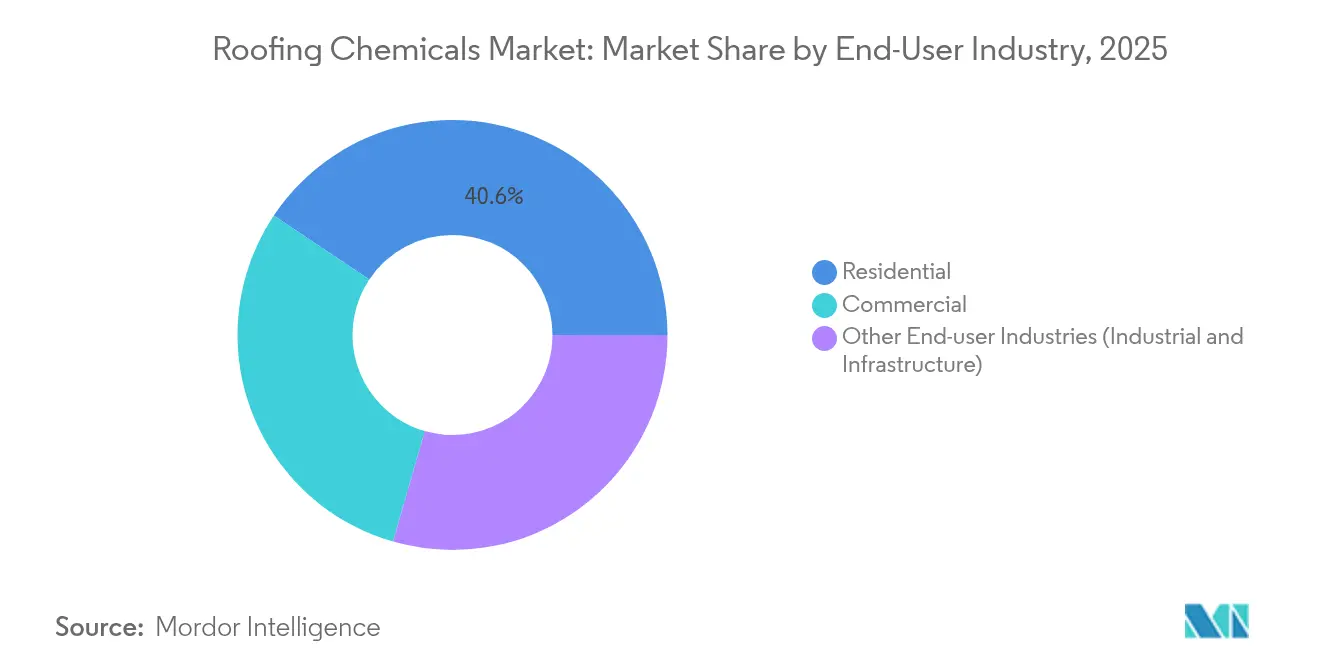

- By end-user industry, the residential sector accounted for 40.62% of the roofing chemicals market size in 2025, whereas industrial and infrastructure applications are advancing at 5.15% CAGR between 2026-2031.

- By geography, Asia-Pacific captured 44.02% revenue in 2025; the same region is forecast to grow at a 5.04% CAGR, the fastest worldwide to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Roofing Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Construction and Infrastructure Sector | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Aging Building Stock and Roof Replacement Projects | +1.8% | North America & Europe, spill-over to developed APAC markets | Long term (≥ 4 years) |

| Growing Demand for Energy-Efficient and Cool Roofs | +0.9% | Global, with early adoption in California, EU, and urban heat island zones | Medium term (2-4 years) |

| Increasing Climate Resilience and Waterproofing Needs | +1.3% | Global, with highest impact in hurricane/hail-prone regions | Short term (≤ 2 years) |

| Insurance-Led Push for Class-A Fire-rated Chemistries | +0.7% | North America, Australia, and wildfire-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Construction and Infrastructure Sector

Global construction outlays are climbing on the back of large-scale stimulus and urbanization projects. In the United States, the Infrastructure Investment and Jobs Act is driving USD 126 billion in public highway and street work, a 16% year-on-year uplift that spills over into demand for protective roofing coatings on bridges, transit hubs and maintenance depots. Elevated cement, lumber and labor costs continue to squeeze contractor margins, amplifying the appeal of durable yet price-competitive bituminous membranes. Project backlogs remain healthy, but workforce shortages are prompting applicators to shift toward pre-formulated, spray-applied systems that reduce on-site labor hours.

Aging Building Stock and Roof Replacement Projects

Non-discretionary re-roofing now outweighs new-build demand in North America and Europe. Commercial facilities erected during the late-1980s boom are reaching end-of-service life, creating a predictable stream of retrofit work anchored in premium chemical upgrades. The U.S. roofing services sector generated USD 27.5 billion in 2023, buoyed by owners opting for high-performance membranes that extend service intervals and meet rising energy-efficiency targets. Stable replacement-cycle visibility shields the roofing chemicals market from cyclical dips in new construction.

Growing Demand for Energy-Efficient and Cool Roofs

Energy codes are turning reflective coatings from niche to norm. California’s Title 24 now requires low-slope roofs to achieve aged solar reflectance of 0.63 and thermal emittance of 0.75, sharply boosting uptake of bright-white acrylic and elastomeric systems. The U.S. Department of Energy calculates that cool roofs cut annual air-conditioning use by up to 15% in warm climates[1]U.S. Department of Energy, “Cool Roofs,” energy.gov. These economics, combined with urban-heat-island concerns, are propelling acrylic dispersions and silicone topcoats into mainstream specifications worldwide.

Increasing Climate Resilience and Waterproofing Needs

Hailstorms, hurricanes and convective wind events are intensifying, pushing property insurers to insist on higher-grade roof assemblies. U.S. roof repair and replacement outlays reached USD 31 billion in 2024, a 30% rise versus 2022, with wind and hail losses accounting for more than one-quarter of residential claim values. Polymer-modified bitumen and elastomeric membranes that retain flexibility under extreme thermal cycling are gaining share as building codes embed resilience metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil Price Volatility | -0.8% | Global, with highest impact on bituminous product segments | Short term (≤ 2 years) |

| Stringent VOC/REACH Caps on Bitumen | -0.6% | Europe, North America, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Skilled-Labour Shortage for Spray-Applied Systems | -0.4% | North America, Europe, developed APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility

Bituminous product lines face sustained margin pressures due to instability in raw material costs. Studies indicate that a 1% increase in crude oil prices results in a 0.58% rise in asphalt prices, with a lag of three months. In 2024, the Producer Price Index for Asphalt Shingle and Coating Materials Manufacturing decreased by 2.19% to 293.79, reflecting the recent moderation in crude oil prices[2]Bureau of Labor Statistics, “Producer Price Index by Industry: Asphalt Shingle and Coating Materials,” bls.gov. Nevertheless, the persistent volatility remains a critical strategic concern. Manufacturers are addressing this challenge by developing hybrid formulations aimed at reducing petroleum dependency while preserving performance standards. This volatility significantly impacts price-sensitive market segments and creates opportunities for bio-based alternatives that offer more stable input costs.

Stringent VOC/REACH Caps on Bitumen

Environmental regulations are reshaping the landscape of traditional bituminous formulations. These regulations not only compel costly reformulations but also carve out market share opportunities for compliant alternatives. For instance, the South Coast Air Quality Management District's Amended Rule 1168, citing toxicity concerns, bans para-Chlorobenzotrifluoride and tertiary-Butyl Acetate in roofing products. The rule also sets VOC limits across 59 categories of adhesives and sealants. Meanwhile, Europe's REACH regulations require registration dossiers for chemicals produced in quantities exceeding 1 ton annually. This could result in certain chemicals being withdrawn from the market, subsequently driving up product costs. Such regulatory pressures are hastening the shift towards waterborne and low-VOC formulations. This shift notably favors acrylic and polyurethane systems, which not only align with environmental standards but also uphold application performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bituminous Dominance Faces Innovation Pressure

Bituminous membranes retained a 31.58% leadership position in 2025 on the strength of contractor familiarity and attractive upfront economics. Polymer-enhanced variants such as SBS-modified sheets are improving cold-flex and fatigue resistance, ensuring relevance despite the advance of high-performing alternatives. Yet polyurethane, silicone and acrylic coatings are expanding at a 5.44% CAGR as the roofing chemicals market shifts toward low-VOC, cool-roof and rapid-cure requirements. Dow’s bio-based NORDEL REN EPDM illustrates the pivot to renewable feedstocks while matching legacy performance.

R&D focus is trained on hybrid systems that marry the toughness of bitumen with the reflectance or elasticity of polymers. Waterborne polyurethane dispersions now offer tensile strengths above 20 MPa with VOC levels below 50 g/L, positioning them for specification in municipal retrofit programs. Modified acrylics dominate the cool-roof niche, while silicone topcoats win on ponding-water resistance in low-slope assemblies. This cascade of innovation keeps the roofing chemicals market competitive and opens white-space opportunities for suppliers with formulation agility.

By End-user Industry: Residential Stability Meets Industrial Growth

Residential reroofing delivers predictable volume, supplying 40.62% of 2025 revenue as homeowners replace aging shingles and upgrade to energy-saving coatings. The segment enjoys tailwinds from favorable mortgage rates and government housing incentives, yet faces contractor shortages that can prolong project timelines. Industrial facilities and infrastructure, however, constitute the fastest-growing customer group, expanding at 5.15% CAGR through 2031 as operators overhaul legacy roofs to meet stricter safety, insulation and emissions norms.

Transportation authorities now specify chemically resistant membranes for tunnels and bridge decks, leveraging the roofing chemicals market size captured under civil engineering budgets. In the commercial arena, 68% of roofing contractors anticipate higher coating sales in 2025, reflecting owner preference for extend-in-place liquid overlays that minimize business disruption. Suppliers able to tailor formulations to niche industrial pain points—acids, solvents, temperature spikes—stand to secure premium margins.

Geography Analysis

Asia-Pacific accounted for 44.02% of global revenue in 2025 and is projected to record a 5.04% CAGR to 2031, making it both the largest and fastest-advancing arena for the roofing chemicals market. China’s real-estate and infrastructure push keeps SBS-modified bitumen at the forefront, while India’s pipeline of transport corridors and industrial parks accelerates adoption of polymer-enhanced, reflective coatings. Sika’s recent plant investments in China and Singapore demonstrate supplier commitment to localized production of mortars and roof systems.

North America remains a replacement-driven arena. Title 24 and similar city codes are steering the roofing chemicals market toward high-reflectance, low-VOC products, while USD 31 billion in 2024 storm-damage payouts underscore the urgency for impact-resistant chemistries. The region’s roofing chemicals market size is further supported by public-sector retrofits of schools, airports and federal facilities funded under infrastructure legislation.

Europe advances on a sustainability mandate. REACH obligations and circular-economy targets are prompting formulators to remove hazardous solvents and embrace recycling pathways. Saint-Gobain’s acquisition of asphalt-shingle recycling technology signals mainstream acceptance of closed-loop concepts within the roofing chemicals market. Market growth concentrates in Germany, France and the Nordics, where subsidy programs reward energy-positive refurbishment.

Competitive Landscape

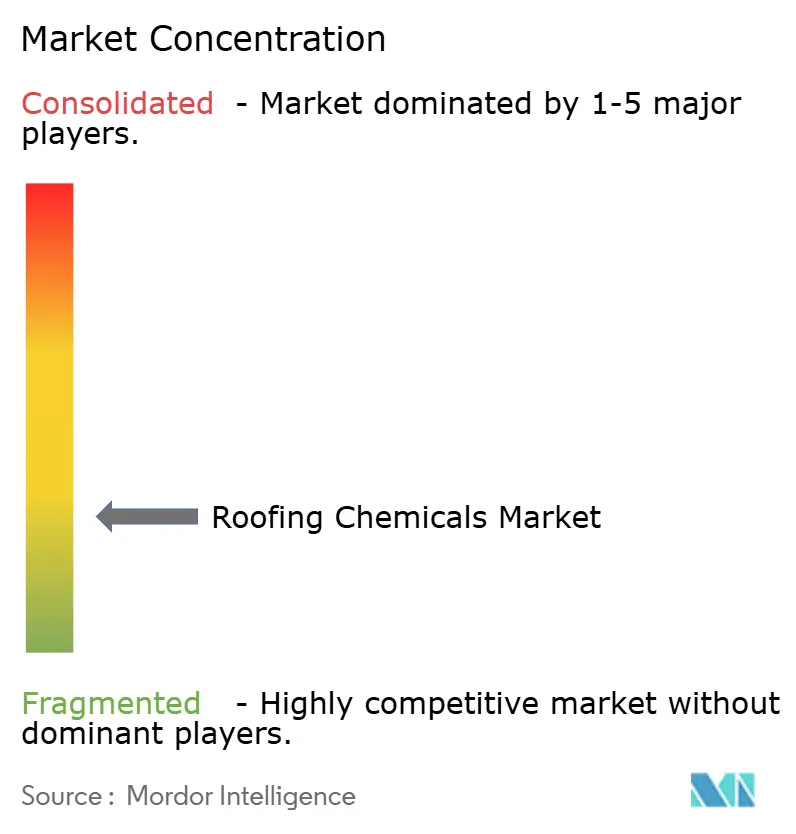

The roofing chemicals market remains highly fragmented despite ongoing consolidation. GAF’s USD 1.1 billion purchase of Icopal exemplifies the roll-up logic aimed at pool-ing technology and distribution scale. Players pursue vertical integration—backward into polymer synthesis or forward into installation services—to lock in margins as crude volatility and labor costs rise.

Technology leadership is a central wedge. Sika’s moisture-curing, one-part polyurethane patent streamlines job-site logistics by eliminating mix-ratio errors, cutting labor hours and VOC emissions. Dow and other chemical majors channel resources into bio-based elastomers and waterborne dispersions, aligning with end-market decarbonization goals. Digital tools—from AI-driven demand forecasting to mobile technical-support apps—differentiate suppliers on contractor service.

Emerging disruptors target gaps in sustainability. Start-ups piloting algae-based resins and PET-recycled polyols attract venture funding, while roofing-system OEMs form alliances with waste-handlers to harvest post-consumer shingles. Established brands counter by scaling pilot projects: Owens Corning has validated recycled-asphalt shingles that could divert 2 million tons of waste annually. As M&A activity intensifies, sellers with proprietary eco-formulations or regional market access command valuation premiums.

Roofing Chemicals Industry Leaders

Owens Corning

BASF

Sika AG

Carlisle Companies Inc.

GAF Materials LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sika completed the acquisition of Cromar Building Products, a supplier of roofing systems in the United Kingdom, primarily serving customers through distribution channels. This acquisition presents significant cross-selling opportunities and supports Sika's strategic expansion within the UK's roofing market.

- March 2025: H.B. Fuller introduced an innovative technology designed to transform commercial roofing installations while promoting environmental sustainability. The H.B. Fuller Millennium PG-1 EF ECO2 is a high-performance roofing adhesive that eliminates the use of chemical blowing agents by utilizing naturally occurring atmospheric gases.

Global Roofing Chemicals Market Report Scope

The roofing chemicals market report includes:

| Bituminous |

| Acrylic Resin |

| Epoxy Resin |

| Elastomers |

| Styrene |

| Other Product Types (Polyurethane, Silicone, etc.) |

| Residential |

| Commercial |

| Other End-user Industries (Industrial and Infrastructure) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Bituminous | |

| Acrylic Resin | ||

| Epoxy Resin | ||

| Elastomers | ||

| Styrene | ||

| Other Product Types (Polyurethane, Silicone, etc.) | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Other End-user Industries (Industrial and Infrastructure) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Roofing Chemicals Market size?

The roofing chemicals market size is USD 111.65 billion in 2026.

What is the forecast CAGR for the roofing chemicals market to 2031?

Market revenue is projected to expand at a 4.53% CAGR between 2026 and 2031.

Which product segment leads the roofing chemicals market?

Bituminous membranes hold the leading 31.58% share, thanks to cost-performance balance and contractor familiarity.

Which region offers the fastest growth opportunity?

Asia-Pacific delivers the highest growth, posting a 5.04% CAGR as infrastructure and urbanization accelerate.

Page last updated on: