Copper Clad Laminate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.82 Billion |

| Market Size (2031) | USD 24.02 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

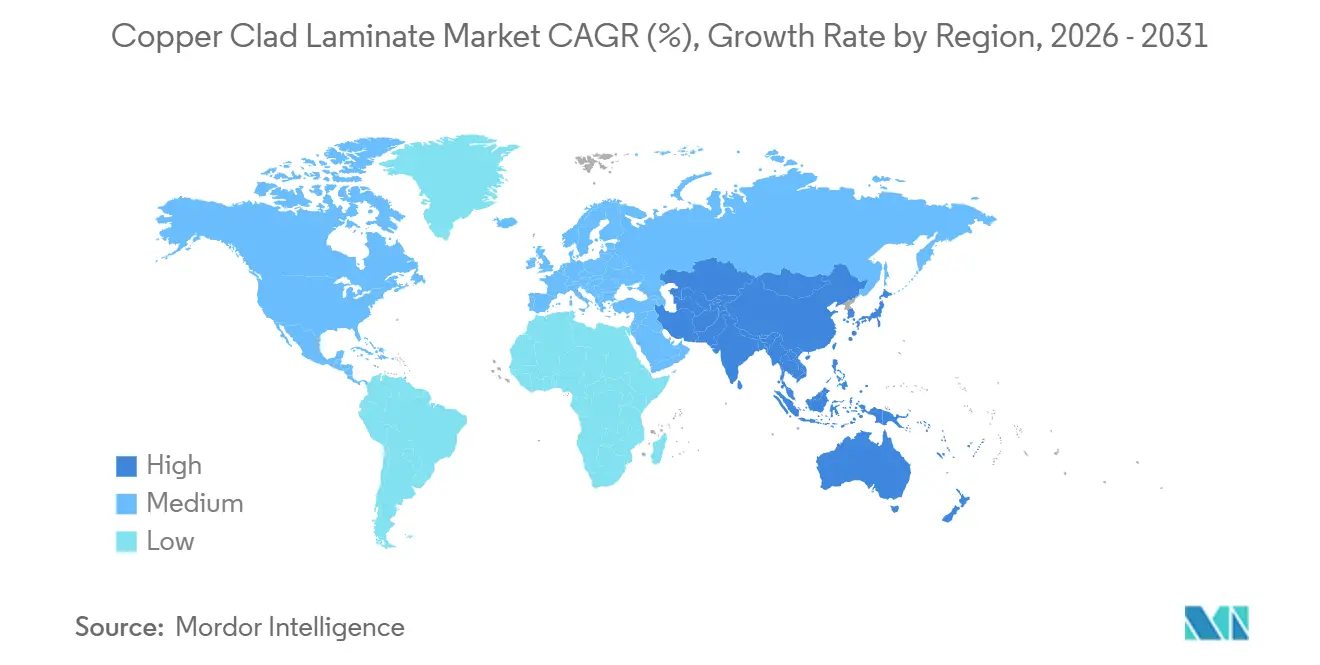

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Copper Clad Laminate Market Analysis by Mordor Intelligence

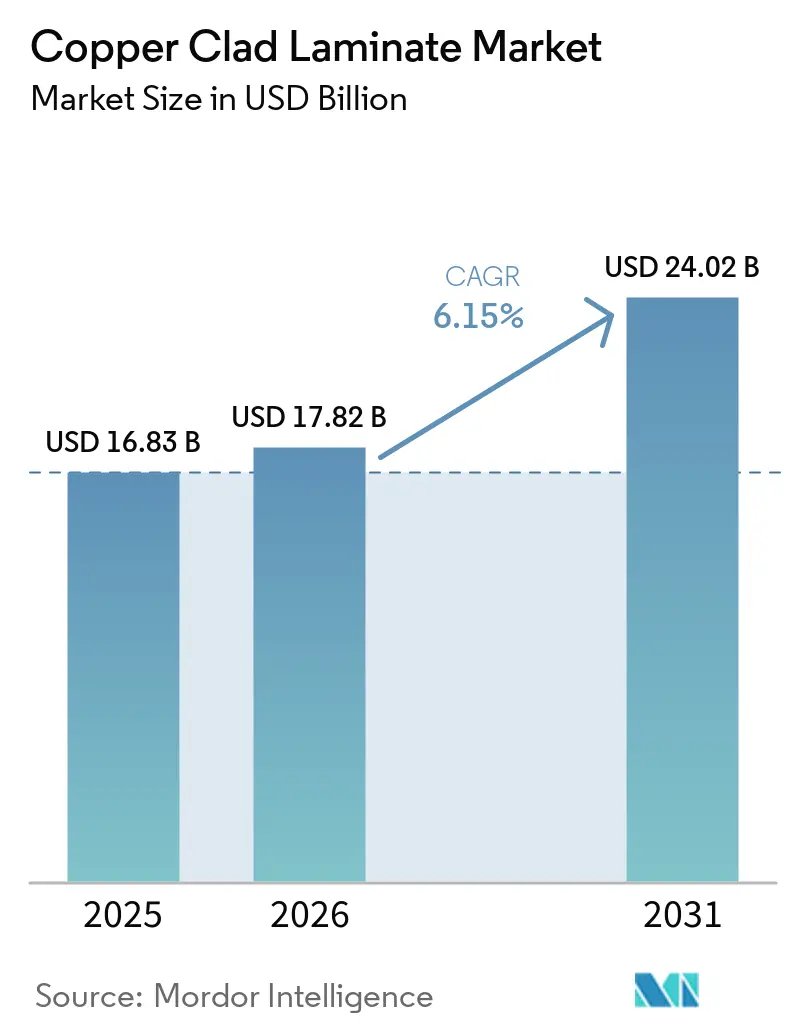

The Copper Clad Laminate Market size was valued at USD 16.83 billion in 2025 and is estimated to grow from USD 17.82 billion in 2026 to reach USD 24.02 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031). Specialty grades that serve AI-server boards and automotive radar command 30-50% price premiums, shifting revenue mix away from commodity FR-4. Certification cycles led by hyperscalers now shape production plans; Nvidia’s M10 qualification with Shengyi Technology and Taiwan Union Technology illustrates how a single program can redirect capacity and margins. Automotive electrification, the roll-out of 5G and emerging 6G networks, and demand for GaN/SiC power modules are reinforcing value migration toward high-thermal and ultra-low-loss materials. Lower raw-material costs projected for 2026 offer a temporary margin reprieve, yet compliance with stricter global EHS rules is lifting capital spending on halogen-free, low-carbon production lines.

Key Report Takeaways

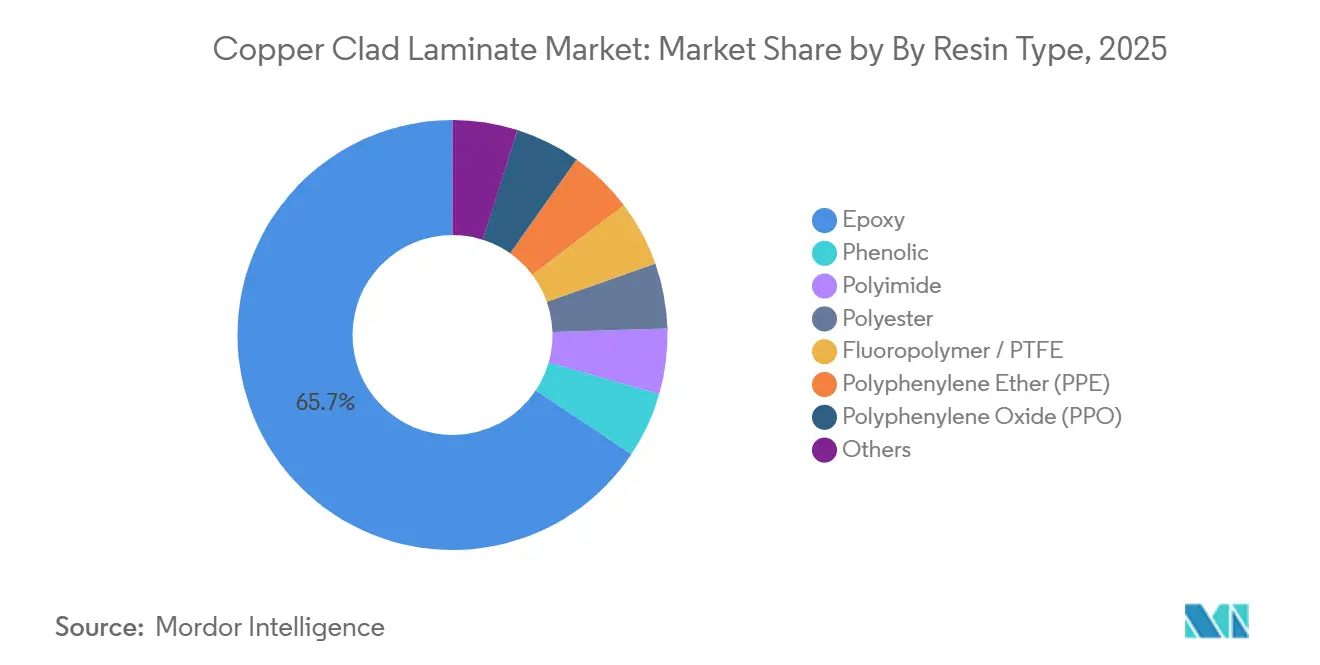

- By resin type, epoxy held 65.66% of the Copper Clad Laminate market share in 2025, while polyimide is expected to post the highest 7.12% CAGR between 2026 and 2031.

- By form factor, rigid boards accounted for 78.21% of the Copper Clad Laminate market size in 2025, while flexible laminates are projected to grow at a 7.34% CAGR through 2031.

- By Reinforcement material, fiberglass accounted for 72.19% of the Copper Clad Laminate market size in 2025, while composites are projected to grow at a 7.56% CAGR through 2031.

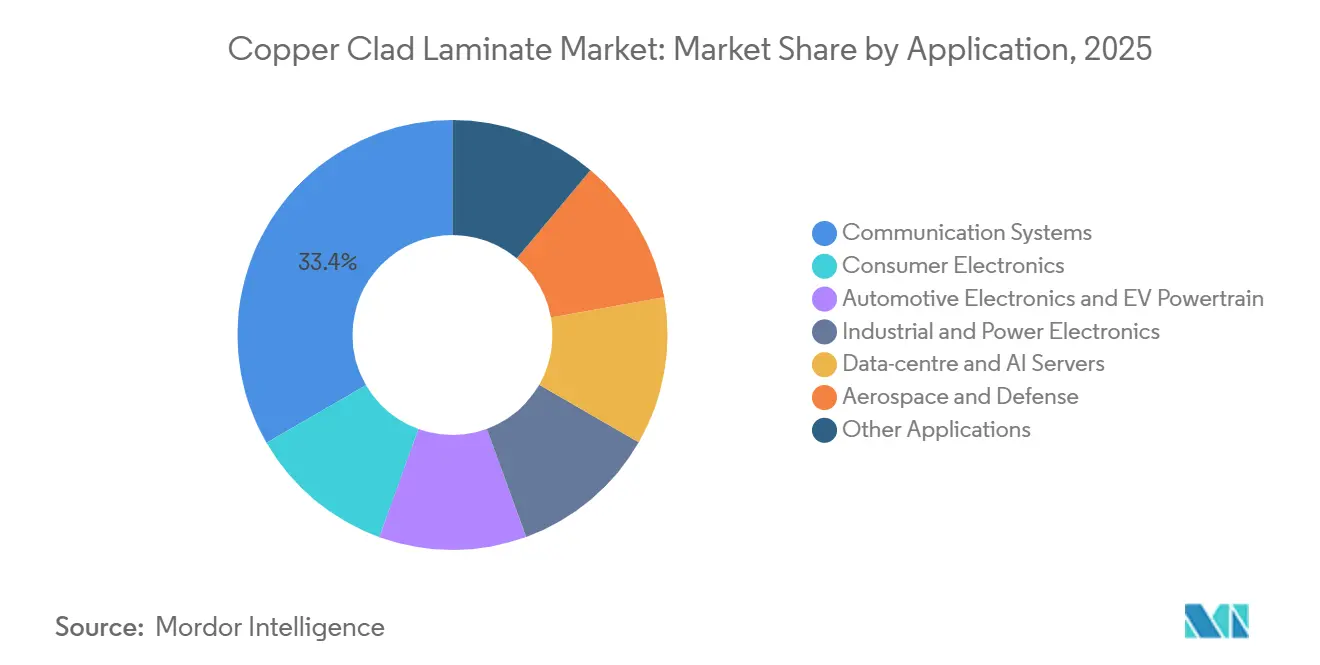

- By application, communication systems contributed 33.36% revenue in 2025; automotive electronics delivered the fastest 7.67% CAGR to 2031.

- By Geography, Asia-Pacific commanded 35.38% of global revenue in 2025 and is forecast to rise at 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Copper Clad Laminate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand for electronics and PCB | +1.2% | Global, led by APAC (>50% of growth) | Medium term (2-4 years) |

| Acceleration of 5G network infrastructure | +1.0% | North America, Europe, China, South Korea, Japan | Short term (≤2 years) |

| Automotive electrification and ADAS uptake | +1.5% | China, EU, North America; spillover to India, Thailand | Long term (≥4 years) |

| AI-server boards need embedded-capacitance | +1.3% | North America hyperscalers, Taiwan/China clusters | Medium term (2-4 years) |

| Rise of GaN/SiC power modules | +0.9% | Global, concentrated in EV and industrial power segments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Robust Demand for Electronics and PCB Drives Baseline Growth

India’s electronics output climbed from INR 1.90 lakh crore (USD 29.6 billion) in FY 2015 to INR 9.52 lakh crore (USD 113 billion) in FY 2024, raising local PCB requirements and boosting the Copper Clad Laminate market. Twenty-two projects cleared under the Electronics Component Manufacturing Scheme in January 2026 unlocked INR 41,863 crore (USD 4.438 billion) of investment aimed at domestic laminate and PCB (Printed Circuit Board) plants. Suppliers integrating into high-layer HDI (High-Density Interconnect) boards capture stronger margins even as low-cost FR-4 faces price pressure.

Acceleration of 5G Network Infrastructure Rollout Fuels High-Frequency CCL Adoption

5G base-station builds require laminates with dielectric loss below 0.005 across 24-77 GHz, a niche addressed by RO3003 and RO4830 Plus families[1]J. Smith, “Energy-Efficient 5G Material Requirements,” agcmmm.com. Taiwan Union Technology’s R&D for halogen-free, carbon-neutral materials underscores how carriers seek both performance and sustainability. Early 6G research is already prompting prototypes of polyimide films operating in the sub-THz band, though readiness sits at TRL 3-6.

Automotive Electrification and ADAS Penetration Reshape Material Specifications

Electric drivetrains boost PCB content per car from roughly USD 70 to USD 250, demanding laminates that endure more than 200°C and stable dielectric constants at 77 GHz. Rogers launched RO4830 Plus in February 2025 to meet these requirements. Panasonic committed JPY 17 billion (USD 108.8 million) to double MEGTRON capacity in Thailand by 2028, aligning with automakers’ moves to high-thermal substrates.

AI-Server Boards Demand Ultra-Thin Embedded-Capacitance CCL

Data-center boards for Nvidia Blackwell and Rubin GPUs need dielectric layers as thin as 25 μm. Doosan won exclusive supply for Rubin after Elite Material failed GB300 tests in 2025, signaling winner-take-most dynamics. Qualification success raises entry barriers and locks in multi-year revenue streams for compliant suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and petroleum-based resin volatility | -0.8% | Global, acute in China and Taiwan | Short term (≤2 years) |

| Stricter global EHS and carbon rules | -0.5% | EU, North America, China, ASEAN | Medium term (2-4 years) |

| CAPEX inflation for next-gen production | -0.4% | Thailand, India, Vietnam, global capacity additions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper and Petroleum-Based Resin Price Volatility Compresses Margins

Copper prices on the London Metal Exchange peaked near USD 13,842 per tonne in 2024 before moderating, and epoxy resin feedstock costs rose 7-10% annually through 2025, driven by petroleum price swings and supply-chain disruptions in Asia-Pacific[2]Land and Houses Bank PLC, “Metals and Resin Price Outlook,” landandhouses.co.th. Resonac Holdings implemented a 30% price increase effective March 2026, and Kingboard Laminates and Nan Ya Plastics executed multiple price adjustments in 2025, yet these actions lag raw-material cost spikes by 3-6 months, compressing gross margins during the interim. Smaller CCL manufacturers without vertical integration into copper foil or resin production face acute vulnerability: they lack the scale to negotiate fixed-price contracts and cannot absorb cost inflation without passing it downstream, which risks losing share to larger competitors who can offer price stability.

Stricter Global EHS and Carbon-Footprint Regulations Elevate Compliance Costs

REACH, RoHS, and carbon border fees force investments in halogen-free chemistries and renewable power. Taiwan Union Technology saved 1,820 MWh over three years, avoiding 925.9 ton CO₂, signaling the scale of efficiency programs now expected by OEMs. Suppliers outside these programs risk disqualification from hyperscaler tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Volume Leadership Versus Polyimide Value Growth

Epoxy held 65.66% of 2025 volume, anchoring commodity boards for consumer devices, yet polyimide captured faster growth with a 7.12% CAGR through 2031 as aerospace and flexible electronics seek durability to 250°C. Specialty fluoropolymer grades, though small, earn 3-5 times epoxy prices by meeting mmWave and radar requirements. Suppliers such as Shengyi integrate PTFE capability to secure embedded-capacitance server wins, highlighting how resin choice determines margin bands.

High-performance blends now pair epoxy with PPO to reduce CTE mismatch, supporting multi-layer server boards. Phenolic and paper-based products are declining as single-sided applications fade. Composite resin launches, including Arlon’s 85N and Panasonic’s HIPER series, capture aerospace and EV inverter niches and help suppliers defend pricing power during raw-material swings.

By Form Type: Rigid Dominance Meets Flexible Momentum

Rigid products contributed 78.21% of 2025 revenue, yet flexible laminates are pacing at a 7.34% CAGR to 2031, owing to foldable phones and wearables. Doosan’s FCCL demonstrates durability over 1 million folds, while Taiflex’s USD 35 million Thailand plant will support automotive interiors and display modules.

Rigid-flex hybrids are spreading into medical devices and robotics, commanding a 2-3 times cost premium. Suppliers that master ultra-thin copper handling and adhesive-less lamination secure design-win stickiness. Meanwhile, large rigid producers defend scale economies through in-house glass fabric and copper foil, allowing aggressive pricing in commodity FR-4 to protect share.

By Reinforcement Material: Fiberglass Scale Against Composite Performance

Fiberglass owned 72.19% of the 2025 volume, offering low cost and mature logistics. Composite reinforcements of aramid, LCP, or ceramic fibers are forecast at a 7.56% CAGR as radar, EV powertrain, and satellite payloads need lower Coefficient of Thermal Expansion (CTE) and lighter weight. Fulltech’s Thailand investment aims to supply next-gen fiberglass for high-layer server boards.

Composite materials command 2-10 times the price of glass fabric, but address smaller, high-margin orders. Liquid crystal polymer layers enable antenna modules in smartphones and autonomous vehicles requiring dielectric constants below 3.0. Paper reinforcement is in structural decline as multilayer demand dominates.

By Application: Communication Leads, Automotive Accelerates

Communication systems took 33.36% of 2025 demand, anchored by 5G base stations and data-center switches. Automotive electronics are projected to expand at a 7.67% CAGR, lifting the Copper Clad Laminate market size for vehicles from USD 2.8 billion in 2025 to USD 4.3 billion by 2031. Battery management, onboard chargers, and radar modules are key drivers.

Consumer electronics remain large but low-margin as shipment growth cools. Industrial power and renewable energy inverters boost the need for high-thermal laminates with more than 2 W/mK conductivity. Aerospace and defense, despite small volume, pay USD 50-200 per m² for polyimide/PTFE materials, providing outsized profit pools for qualified suppliers.

Geography Analysis

Asia-Pacific generated 35.38% of 2025 revenue and is projected to rise at a 7.78% CAGR through 2031. Thailand and India alone have announced incentive-led investments, catalyzing local laminate demand. China maintains the largest consumption base, yet geopolitical shifts are steering Taiwanese and mainland firms to Southeast Asia, with Thailand’s PCB share expected to top 5% globally in 2026.

North America and Europe together accounted for about half of global revenue, owing to aerospace, defense, and hyperscale data centers. AGC Multi Material America expanded distribution through Tritek to fortify UnitedStates supply security. EU carbon policies elevate compliance hurdles, favoring large incumbents that can fund halogen-free and renewable power upgrades.

South America and the Middle East & Africa held the lowest share in 2025. Brazil’s vehicle rebound and Gulf-state telecom projects offer white-space growth, but infrastructure gaps and limited upstream feedstocks temper near-term penetration. Early movers that provide local technical support may capture loyalty as regional manufacturing ecosystems mature.

Competitive Landscape

The Copper Clad Laminate market is moderately fragmented. Technology leadership remains the decisive lever. Panasonic’s MEGTRON expansions, Rogers’ RO4830 Plus, and Isola’s IS550H show how resin and reinforcement innovation underpins long-term contracts. IPC-4101 and UL 94 V-0 compliance gatekeep entry, concentrating share among suppliers that can deliver traceability, reliability, and low-carbon footprints.

Copper Clad Laminate Industry Leaders

Kingboard Laminates Holdings Ltd.

SHENGYI TECHNOLOGY CO., LTD.

NAN YA PLASTICS CORPORATION

Taiwan Union Technology Corporation

Panasonic Industry Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Chennai-based electronics manufacturing services firm Syrma SGS Technology is planned to invest INR 1,800 crore (USD 208.8 million) to set up India’s largest multi-layer printed circuit board (PCB) and copper clad laminate (CCL) manufacturing unit in Andhra Pradesh. The integrated manufacturing facility is likely to be commissioned by 2026-27.

- February 2025: Resonac Corporation has developed low thermal expansion copper-clad laminates designated for use in next-generation semiconductor packages that suppress warpage, one of the challenges associated with the increasing size of semiconductor packages. Resonac aims to start mass production of this product in 2026.

- January 2025: DuPont announced participation in DesignCon 2025 Expo, showcasing Pyralux flex circuit laminates and Kapton polyimide films designed for AI printed circuit boards, 5G networks, and electric vehicle applications, emphasizing signal integrity and thermal performance under extreme conditions.

Global Copper Clad Laminate Market Report Scope

Copper Clad Laminate (CCL) is the foundational material for manufacturing printed circuit boards (PCBs), consisting of an insulating substrate (typically epoxy resin and fiberglass) laminated with copper foil on one or both sides. It provides the conductive paths, structural integrity, and insulation for electronics, widely used in consumer electronics, automotive, and 5G infrastructure.

The Copper Clad Laminate market is segmented by resin type, form type, reinforcement material, application, and geography. By resin type, the market is segmented into epoxy, phenolic, polyimide, polyester, fluoropolymer/PTFE, polyphenylene ether (PPE), polyphenylene oxide (PPO), and others. By form type, the market is segmented into rigid and flexible. By reinforcement material, the market is segmented into fiberglass fabric, paper-based, composite/aramid/LCP, and other materials. By application, the market is segmented into communication systems, consumer electronics, automotive electronics, and ev powertrain, industrial and power electronics, data-centre and AI servers, aerospace and defense, and other applications. The report also covers the market size and forecasts for copper-clad laminate in 15 countries across major regions in value (USD).

| Epoxy |

| Phenolic |

| Polyimide |

| Polyester |

| Fluoropolymer / PTFE |

| Polyphenylene Ether (PPE) |

| Polyphenylene Oxide (PPO) |

| Others |

| Rigid |

| Flexible |

| Fiberglass Fabric |

| Paper-based |

| Composite / Aramid / LCP |

| Other Materials |

| Communication Systems |

| Consumer Electronics |

| Automotive Electronics and EV Powertrain |

| Industrial and Power Electronics |

| Data-centre and AI Servers |

| Aerospace and Defense |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Epoxy | |

| Phenolic | ||

| Polyimide | ||

| Polyester | ||

| Fluoropolymer / PTFE | ||

| Polyphenylene Ether (PPE) | ||

| Polyphenylene Oxide (PPO) | ||

| Others | ||

| By Form Type | Rigid | |

| Flexible | ||

| By Reinforcement Material | Fiberglass Fabric | |

| Paper-based | ||

| Composite / Aramid / LCP | ||

| Other Materials | ||

| By Application | Communication Systems | |

| Consumer Electronics | ||

| Automotive Electronics and EV Powertrain | ||

| Industrial and Power Electronics | ||

| Data-centre and AI Servers | ||

| Aerospace and Defense | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for copper clad laminate growing?

The Copper Clad Laminate Market size was valued at USD 16.83 billion in 2025 and is estimated to grow from USD 17.82 billion in 2026 to reach USD 24.02 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

Which resin type is gaining the most value share?

Polyimide grades are advancing at a 7.12% CAGR through 2031 due to aerospace, flexible electronics and high-temperature automotive needs.

Why are hyperscalers important customers for laminate suppliers?

Programs such as Nvidia’s Rubin AI board require ultra-thin, embedded-capacitance laminates and grant multi-year contracts to qualified suppliers, rapidly shifting market share.

What is driving flexible laminate demand?

Foldable smartphones, wearables and automotive interior displays need substrates that survive over 1 million bends, pushing flexible CCL to a 7.34% CAGR.

How are sustainability rules affecting producers?

REACH, RoHS and carbon border measures force investments in halogen-free chemistries and renewable power, raising compliance costs but offering a competitive edge to early movers.

Page last updated on: