Cranberries Market Size and Share

Cranberries Market Analysis by Mordor Intelligence

The cranberries market size is projected to expand from USD 9.2 billion in 2025 and USD 9.8 billion in 2026 to USD 13.6 billion by 2031, registering a CAGR of 6.77% between 2026 to 2031. The increasing demand for clean-label ingredients in nutraceuticals, beverages, and snacks is expanding the consumer base for cranberries. North America held a significant share of the global consumption value in 2025, led by the United States, which combines the largest global harvest with strong domestic demand. The Asia-Pacific region is the fastest-growing consumer market, driven by China's simplified regulations for importing frozen fruit and enhanced cold-chain infrastructure. Challenges such as limited pollination resources and regional fertilizer constraints are increasing production costs. Nevertheless, advancements in precision irrigation, drone scouting, and carbon credit programs are improving farm profitability. Additionally, the growing awareness of the health benefits associated with cranberries, including their antioxidant properties and their role in maintaining urinary tract health, is further driving demand. The increasing incorporation of cranberries in functional foods and beverages is also contributing to market growth, as consumers seek products that offer both nutritional value and convenience.

Key Report Takeaways

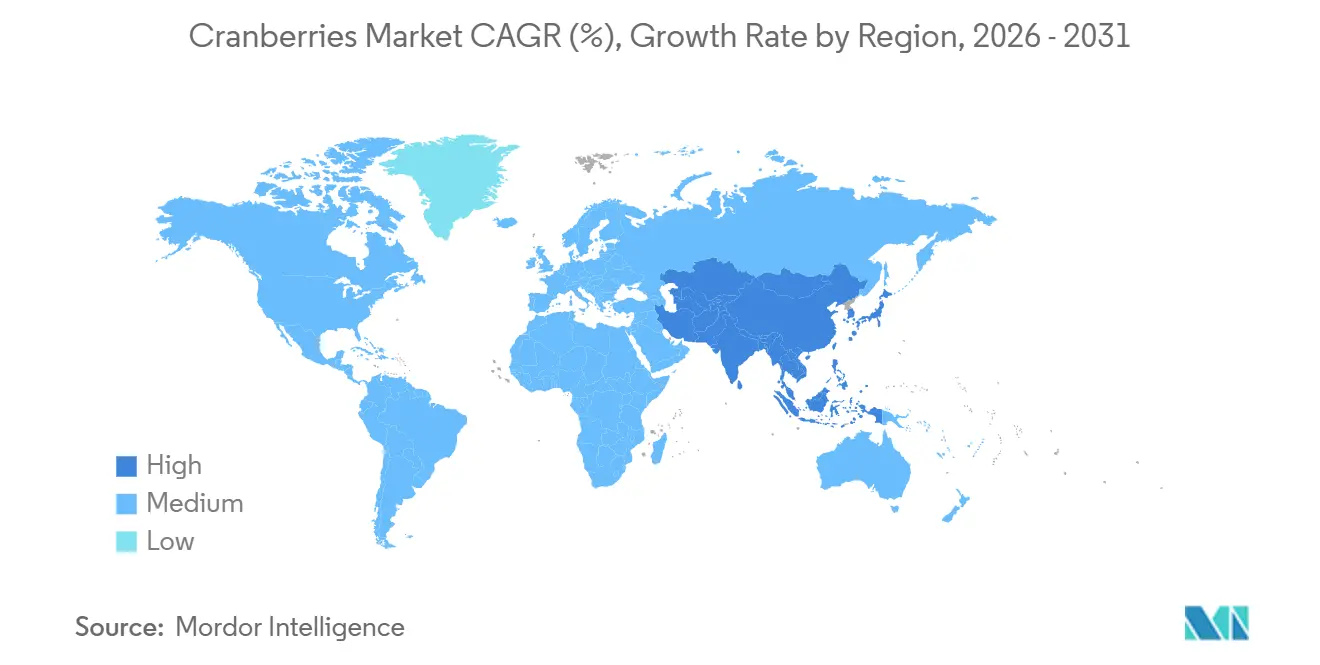

By geography, North America accounted for 46% of the cranberries market size in 2025, whereas the Asia-Pacific region is poised for the fastest 11.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Cranberries Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating demand from nutraceutical and functional beverage formulators | +1.8% | North America and Europe | Medium term (2-4 years) |

| Growing popularity of dried‐cranberry substitutes driving fresh brand visibility | +1.2% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising adoption of cranberries as natural antioxidants and colorants | +1.5% | Europe and North America | Medium term (2-4 years) |

| Expansion of direct-to-consumer e-commerce for bulk produce | +0.9% | Asia-Pacific spillover to North America | Short term (≤ 2 years) |

| Precision-flood harvesting boosting yields in colder latitudes | +0.7% | United States, Canada, Netherlands, and Russia | Long term (≥ 4 years) |

| Wetland carbon-credit programs increasing bog profitability | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand from Nutraceutical and Functional Beverage Formulators

Manufacturers are incorporating cranberry extracts rich in A-type proanthocyanidins into supplement capsules, ready-to-drink beverages, and protein powders to address consumer demand for clinically supported urinary tract health benefits. Clinical studies validate the effectiveness of proanthocyanidins (PACs) in reducing the recurrence of urinary tract infections. The European Food Safety Authority declined to approve a health claim for Pacran in prior evaluations, citing insufficient mechanistic data [1]Source: European Food Safety Authority, “Scientific Opinions on Health Claims,” EFSA.EUROPA.EU. This regulatory caution has not dampened commercial interest. Beverage companies are reformulating products with cranberry juice concentrate as a substitute for synthetic ascorbic acid, aiming to capitalize on clean-label preferences. Fresh cranberries provide anthocyanin and flavonol profiles, which are extracted by processors for these applications, creating a competing demand channel alongside juice-processing allocations. This trend is particularly evident in North America and Europe, where supplement usage exceeds 50% of adults, and functional beverage launches experienced double-digit growth in 2024 and 2025.

Precision-Flood Harvesting Boosting Yields in Colder Latitudes

Growers in regions such as Wisconsin, Quebec, and the Netherlands are utilizing soil moisture sensors, weather station networks, and automated flood control gates to optimize water application during frost protection and flood irrigation during harvest. These precision techniques reduce water waste by 20% to 30% and enhance berry quality by preventing over-saturation, which can dilute anthocyanin content. The United States Department of Agriculture (USDA), through projects running from 2020 to 2025, has validated frost-protection models that growers now integrate into decision-support software. Quebec achieved record yields of 26,000 pounds per acre in 2024, partly due to the adoption of these systems, which enable growers to align flood timing with varietal phenology. In Massachusetts, a 25% tax credit, capped at USD 100,000, is available for bog renovation and irrigation automation, encouraging capital investment. This technology has limited applicability in Chile and other warmer regions where frost risk is negligible, restricting its geographic adoption.

Wetland Carbon-Credit Programs Increasing Bog Profitability

Cranberry bogs are recognized as wetland ecosystems under voluntary carbon-certification frameworks, including the European Union Carbon Certification Framework established by Regulation 2024/3012. This framework requires five-year project commitments, verification of additionality, and third-party monitoring[2]Source: European Commission, “Agricultural Statistics,” EC.EUROPA.EU . Growers in regions such as Massachusetts and Quebec are participating in carbon-offset programs that provide payments ranging from USD 15 to USD 30 per metric ton of CO2-equivalent sequestered annually. These payments serve as a supplementary income source, enhancing the financial viability of maintaining cranberry bogs rather than converting them into solar installations or residential developments. The European Union framework emphasizes soil emission reductions and biodiversity co-benefits, which align well with the low-tillage and perennial characteristics of cranberry production. Program participation remains limited, with less than 10% of total acreage enrolled. This is primarily due to the administrative burden of documentation and uncertainties surrounding credit pricing. As corporate net-zero commitments increase, the demand for high-quality agricultural carbon credits is projected to grow, potentially doubling offset prices by 2028.

Growing Popularity of Dried-Cranberry Substitutes Driving Fresh Brand Visibility

The retail expansion of dried cranberries in trail mixes, granola bars, and snack packs has familiarized consumers with cranberry flavor profiles, thereby lowering barriers to fresh-fruit trial. Grocers report that shoppers who purchase dried cranberries exhibit 30% higher conversion rates for fresh berries during harvest season, as they seek whole-fruit alternatives to sugar-infused dried variants. This cross-category halo effect is particularly strong in the Asia-Pacific region, where cranberries were historically a niche product. E-commerce platforms in China now feature fresh cranberries in premium gift boxes during the Lunar New Year, capitalizing on the berry's red color and health associations. The August 2024 removal of quarantine requirements for frozen cranberries in China further accelerated this trend, enabling year-round availability and reducing logistics friction.

Restraints Impact Analysis of Cranberries Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs of commercial bog cultivation | −1.1% | North America and Europe | Long term (≥ 4 years) |

| Low consumer awareness in developing economies | −0.8% | Africa, Middle East, and South America | Medium term (2-4 years) |

| Declining native-bee populations raising pollination costs | −0.6% | Global, acute in North America | Short term (≤ 2 years) |

| Fertilizer-sulfate restrictions disrupting yield optimization | −0.4% | Massachusetts, Cape Cod, and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Consumer Awareness in Developing Economies

Cranberries lack a culinary tradition in Africa, the Middle East, and much of South America, where local berries and tropical fruits are more prevalent in diets. Retail penetration remains below 5% in these regions, and fresh cranberries are often absent from supermarket produce sections, except in expatriate-focused stores. Consumer education campaigns are costly and require sustained investment, which small exporters cannot afford. Chile, despite being the third-largest producer, exports over 90% of its crop to North America and Europe, reflecting weak domestic demand. In Kenya and South Africa, imported cranberries face tariff and logistics costs that price them above local alternatives, such as Cape gooseberries. The Middle East exhibits modest growth potential, with Turkey and Azerbaijan experimenting with domestic cultivation, but production remains negligible. Without government-led nutrition programs or retailer-funded sampling initiatives, awareness will remain a binding constraint on demand growth in these geographies through 2031.

Fertilizer-Sulfate Restrictions Disrupting Yield Optimization

Cranberries thrive in acidic soils with a pH between 4.0 and 5.5, which is typically maintained through the application of elemental sulfur or ammonium sulfate. Massachusetts Department of Environmental Protection regulations limit sulfate loading near Cape Cod aquifers, where elevated sulfate levels pose a threat to drinking-water quality. Growers must adopt alternative acidification methods, such as sulfuric acid injection or organic amendments like peat moss, which are more expensive and labor-intensive. Nitrogen application is also restricted within setback zones of 3 meters from watercourses, which reduces fertilizer efficiency and forces growers to rely on precision application technologies. These constraints are most binding in Massachusetts, where 40% of bogs lie within regulated watersheds. Europe's Farm to Fork Strategy targets a 20% reduction in fertilizer use by 2030, adding pressure on Dutch and German growers to adopt nutrient-recycling systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

North America Cranberries Market

North America accounted for 46% of the cranberries market size in 2025, with the United States and Canada collectively dominating the majority. The region exhibits mature market dynamics, characterized by growth driven by premiumization, organic expansion, and export diversification. Quebec's 2024 production surge to 154,288 metric tons, driven by record yields of 26,000 pounds per acre, positions Canada to capture incremental export share in Europe and Asia [3]Source: Statistics Canada, “Fruit Production Statistics 2024,” STATCAN.GC.CA. The United States' 2025 production totaled 8.13 million barrels, reflecting a 9% decrease from 2024. This decline highlights the impact of weather volatility and emphasizes the importance of developing climate-resilient cultivars.

APAC Cranberries Market

The Asia-Pacific region is expanding at 11% CAGR through 2031, driven by China's August 2024 removal of quarantine requirements for frozen fruit, which has unlocked a year-round supply. This has enabled e-commerce platforms like Alibaba's Freshippo to feature cranberries in premium gift assortments. Japan and South Korea are experiencing growth, with cranberries being positioned as functional ingredients in supplements and beverages that target urinary-tract health and antioxidant benefits. SF Express and JD Logistics are investing in cold-chain infrastructure, including the construction of new refrigerated warehouses, upgrading existing facilities, and expanding fleets of temperature-controlled vehicles. These investments aim to increase refrigerated capacity by 25% annually from 2024 to 2026. These efforts are reducing spoilage and facilitating direct-to-consumer deliveries within 24 hours in major cities.

EMEA, South America and Turkey Cranberries Market

Europe's cranberry market is influenced by Germany, the United Kingdom, and the Netherlands, which act as key re-export hubs. While the region experiences slower population growth and high baseline consumption, the European Union's Farm to Fork Strategy, aiming for a 50% reduction in pesticide use by 2030, is boosting demand for organic cranberries. These organic products typically command price premiums ranging from 30% to 50%. In South America, Chile plays a significant role in meeting counter-seasonal demand for organic cranberries in North America and Europe. In Africa and the Middle East, the market faces challenges due to low consumer awareness and limited retail penetration. However, Turkey's experimental cultivation efforts in the Rize and Artvin provinces could establish a regional supply by 2028.

Regulatory Landscape

Regulation affecting cranberries covers crop production practices, environmental compliance, food safety, and cross-border phytosanitary rules. In the United States, USDA Agricultural Marketing Service terminated Federal Marketing Order No. 929 effective July 31, 2024, removing federal handler-level requirements tied to collective administration and shifting more promotional and reporting burdens to firms, state programs, and industry groups.

At the state level, production guidance and compliance frameworks remain active, including the Michigan Department of Agriculture and Rural Development 2026 Generally Accepted Agricultural and Management Practices (GAAMPs) for cranberry production and ongoing extension guidance from the UMass Amherst Cranberry Station. In Europe, sustainability-linked frameworks such as the European Union Carbon Certification Framework (Regulation 2024/3012) provide a structure for monitoring and verification in carbon-credit projects, intersecting with cranberry bog management where growers participate in voluntary carbon programs.

Value Chain Analysis

The cranberry value chain begins with specialized input procurement, including vines, sand for bog management, fertilizers, and crop protection, followed by cultivation and harvesting (wet and dry harvest), and then handling and primary processing. In North America, cooperatives and handlers play an outsized role in aggregation, storage, and channel allocation across fresh pack, juice concentrate, dried fruit, and ingredient streams. Ocean Spray coordinates supply from member growers, while independent processors such as Decas Cranberry Products route fruit to higher-spec ingredient and specialty applications.

After post-harvest handling, the chain splits into retail-oriented fresh and sweetened dried formats and B2B ingredient pathways that supply nutraceutical, functional beverage, and natural colorant customers using concentrates and extracts. Public and extension infrastructure also supports productivity and compliance upgrades, including Massachusetts' Cranberry Renovation and Enhancement Program for bog improvements and technical guides from institutions such as the UMass Cranberry Station, which help growers manage water, pest pressure, and regulatory requirements that affect yield, quality, and cost-to-serve.

Competitive Landscape

The cranberries market encompasses producers, importers, exporters, and other stakeholders. Ocean Spray Cranberries Inc. leads the market through its cooperative structure, which includes 700 family farmers across North America. This model ensures a consistent supply and facilitates product distribution to over 70 countries. While the cooperative structure shields Ocean Spray from spot-price volatility, it restricts flexibility in shifting toward high-margin fresh-market channels, as member growers prioritize volume contracts for juice and dried-fruit processing. Decas Cranberry Products Inc., a key market player, operates as an independent processor, enabling it to allocate fresh cranberries for applications such as natural colorant extraction and functional ingredient production, capitalizing on the clean-label segment. Cliffstar LLC, a subsidiary of Refresco, holds a significant share by sourcing fresh cranberries for contract beverage manufacturing. Additionally, Cape Cod Select LLC and Patience Fruit and Co. focus on premium fresh-pack retail and organic market niches, respectively.

The termination of the United States Department of Agriculture's Marketing Order No. 929 in July 2024 has decentralized collective promotional efforts, shifting export-market development costs to individual firms and state specialty crop block grants. Opportunities in the market include direct-to-consumer e-commerce, organic certification, and carbon credit monetization. Growers implementing precision irrigation and drone-based pest monitoring have reduced input costs by 15% to 20% while enhancing berry quality, providing a competitive edge in fresh-market channels. The European Union Carbon Certification Framework, effective as of 2024, enables cranberry bogs to generate offset credits. Early adopters in Massachusetts and Quebec have enrolled acreage, earning USD 15 to USD 30 per metric ton of CO2-equivalent, further strengthening their market position.

Smaller players, such as Fruit d'Or Inc. in Quebec and Cran Chile SA, are expanding organic production to meet the demand from European processors, who are replacing synthetic colorants with cranberry anthocyanins. Technology adoption across the industry remains uneven. Larger cooperatives are investing in automated harvesting equipment and upgrading their cold storage facilities, while smaller growers often rely on manual labor and third-party logistics. This reliance limits their ability to meet retailer quality standards for fresh berries, presenting challenges in the competitive market landscape.

Market Opportunities and Future Outlook

Export-market development and demand diversification beyond traditional juice channels remain key whitespace areas, supported by funded programs and changing import pathways. The Cranberry Institute has used USDA funding to expand outreach in multiple destinations, including a USD 1 million Regional Agricultural Promotion Program (RAPP) award and a USD 1.2 million Market Access Program grant focused on markets such as India, parts of South America (Brazil and Colombia), and Southeast Asia. In September 2025, it also engaged Orissa International to support a US cranberry marketing program in Malaysia, Singapore, Thailand, and Vietnam.

Opportunities are also tied to higher-value ingredient uses where cranberries serve as clean-label antioxidants, colorants, and bioactive-rich extracts for supplements and fortified foods. Asia-Pacific demand has a practical access catalyst in China, where the August 2024 removal of quarantine requirements for frozen fruit imports simplifies phytosanitary handling for frozen cranberries and supports year-round supply to e-commerce-led channels. Alongside trade friction, including 30% to 34% tariffs applied by China on North American cranberry products noted by industry sources, suppliers have needed to expand destination and product-format mixes, including frozen, dried, concentrates, and extracts, to match different buyer requirements and regulatory regimes.

Recent Industry Developments in Cranberries Market

- July 2026: Quebec Cranberry Growers - The region entered the bloom period with crop development progressing in line with seasonal expectations despite pollination running approximately 3-4 days behind normal levels. The pace supports near-term supply visibility for processors and can influence pricing dynamics in the short term.

- May 2026: Ocean Spray Cranberries, Inc. launched new Craisins Dried Cranberry flavors (Strawberry and Raspberry Lemonade) in single-serve 1 oz pouches and Sour Watermelon in 6 oz pouches. The initiative expands the product assortment in the dried cranberries segment and strengthens brand relevance in snacking channels and supports premium and value SKUs.

- May 2026: Ocean Spray Cranberries, Inc. appointed Brandgenuity as exclusive licensing agency to manage consumer product category expansion. The partnership accelerates go-to-market and supports licensing driven portfolio growth.

Cranberries Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the cranberries market is defined as the value of cranberries sold as fresh fruit and as cranberry-based products made from real fruit solids, including frozen berries, sweetened dried cranberries, juices, concentrates, sauces, powders, and standardized extracts, across major consuming regions.

Scope exclusions: Products that only use synthetic cranberry flavoring and do not contain cranberry fruit solids are excluded from the market value.

Segments Covered in This Report

- By Geography

- North America

- United States

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Canada

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Mexico

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Germany

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United Kingdom

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Spain

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Netherlands

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Russia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Germany

- Asia-Pacific

- China

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Japan

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- China

- South America

- Chile

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Peru

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Brazil

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Chile

- Middle East

- Turkey

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Azerbaijan

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Turkey

- Africa

- South Africa

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- South Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping supply, trade, and consumption signals that are publicly trackable for cranberries and processed cranberry formats. We lean on official agriculture and trade statistics and price references, such as USDA data releases, FAOSTAT series, UN Comtrade trade tables, Statistics Canada agriculture publications, and Eurostat trade and production indicators, which help us anchor direction and scale.

After that, company filings, investor materials, and association websites are used to understand product mix shifts between fresh, dried, and juice forms, plus channel movement into ingredients and nutraceutical use. Where needed, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records are used to verify large moves and reduce missing-company bias. The sources listed here are illustrative only, and many other public documents and datasets are also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the desk model with reality checks from growers, processors, ingredient sellers, distributors, and buyers in food, beverage, and supplements. We also validate price realization and mix changes by speaking with respondents across the main producing and importing regions, so the final totals reflect how cranberry products are actually traded and consumed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | APAC: 49% |

| Mid tier: 54% | Functional/Unit leaders: 38% | EMEA: 33% |

| Smaller Players: 20% | Managers: 45% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using top-down reconstruction from production, import and export flows, and consumption value signals, then translated into market value using observed wholesale and realized pricing. Once the demand pool is formed, selective bottom-up checks are run using sampled price times volume for key formats, along with channel checks on processed products, to make sure totals do not drift from what suppliers and buyers recognize.

For cranberries, the main inputs include planted area and yield movements, harvest volumes by major producing countries, processed share split between fresh, dried, and juice or concentrate, wholesale price trend direction, trade balances for key HS-coded berry and fruit preparation lines, and seasonality patterns that drive shipments around holiday demand. When direct public splits are missing for a format, we rely on interview-based mix ranges, then apply conservative bounds and re-check against trade values and pricing, so gaps do not inflate the market.

For forecasting, we use scenario analysis supported by simple multivariate relationships between demand growth and variables like per capita fruit intake trends, functional food and supplement adoption, processing capacity additions, and price sensitivity seen in retail promotions. Assumptions are adjusted only after they are confirmed in primary discussions and after they remain consistent with the historical time series behavior.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as production-to-export ratios, price and volume consistency, and import value per ton trends that would indicate unrealistic pricing. If a region shows an unusual jump, we re-review the underlying drivers and trigger follow-up calls to confirm whether it is a real shift or a data timing issue.

Before sign-off, the model goes through multi-step analyst review where assumptions, conversions, and currency treatments are tested for variance and logic. Reports are refreshed annually, and interim updates are made when material events occur, such as a major crop disruption, policy change affecting imports, or a sharp price move. Right before delivery, we recheck the latest public releases so clients receive an updated view.

Mordor Intelligence's Cranberries Market Size Compared With Other Published Estimates

Published cranberry market values often look different because each publisher chooses its own product boundary, year mapping, and price basis, then updates assumptions at different times. Some studies also mix "cranberry flavored" items into the total, which can change the number even if cranberry supply did not move much.

Trade values, production volumes, and wholesale price trend checks are the evidence that keep Mordor Intelligence's 2025 estimate tied to real cranberry fruit solids across fresh and processed formats, instead of counting adjacent flavored products or double-counting concentrate flows. Differences also come from whether a source reports only fresh fruit revenue, uses retail shelf prices rather than traded or realized prices, or applies aggressive ASP increases without validating them through import value per ton and channel feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.20 B (2025) | |

| Trade Journal A | USD 2.35 B (2024) | This estimate appears to focus on fresh cranberries only, which omits dried pieces, juice, concentrate, sauces, powders, and standardized extracts that carry meaningful value outside fresh retail. |

| Industry Blog B | USD 2.30 B (2025) | The scope is presented as a broad cranberries market, but the underlying segmentation leans toward a functional-ingredient view, which can undercount mainstream food and beverage consumption and can be sensitive to assumed extract penetration and ASP growth. |

The spread in the table mostly comes from product boundary and the price level used to convert volume into value. When the market is anchored to observable supply, trade, and price signals and then checked with buyer and seller feedback, the result is a practical estimate that can be repeated and updated as new crop and trade data arrives.

Key Questions Answered in the Report

What is the projected market size of cranberries in 2026?

The cranberries market size reached USD 9.8 billion in 2026 and is set to grow at a 6.77% CAGR through 2031.

Which region is expanding fastest in cranberry demand?

Asia-Pacific is growing at 11% CAGR through 2031, with China driving double-digit gains after import rules eased.

Who is the leading player in the global cranberries market?

Ocean Spray Cranberries Inc. led with significant revenue in 2025, supported by a cooperative of 700 farms.

What technological shifts are boosting cranberry yields?

Precision-flood harvesting and drone-based pest monitoring are cutting water use and pesticides while elevating berry quality.

Page last updated on: