United States Blueberry Market Analysis by Mordor Intelligence

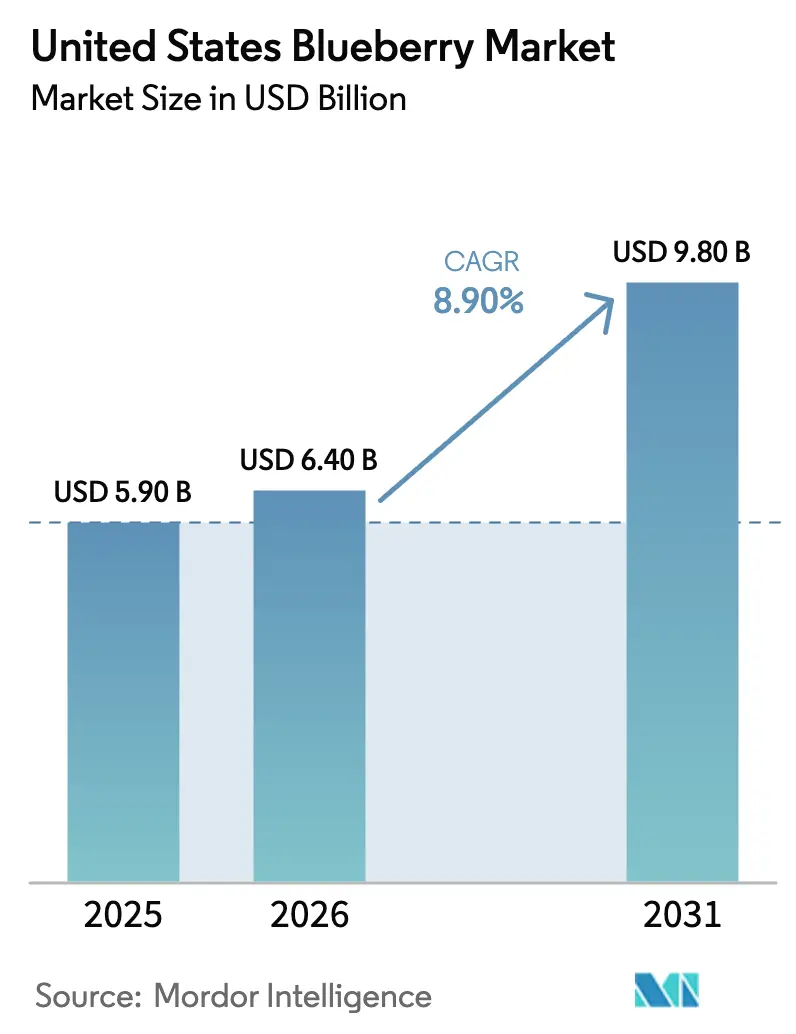

The United States blueberry market size was valued at USD 5.90 billion in 2025 and is estimated to reach USD 6.40 billion in 2026, further projected to grow to USD 9.80 billion by 2031, advancing at a compound annual growth rate (CAGR) of 8.90% during the forecast period (2026–2031). Momentum stems from a nine-fold increase in per-capita intake since 2000, steady retail adoption of premium clamshells at nearly USD 6, and the blending of domestic harvests with counter-seasonal imports to secure year-round shelf presence. Peruvian supply filled roughly 57% of its export volume to the United States in 2024, but a 10% tariff introduced in 2025 is redirecting metric-ton flows toward China[1]Source: Marco Aquino, “Peru Turns to China as United States Tariffs Squeeze Blueberry Exports,” Reuters, reuters.com, thereby tightening United States inventories during the period from September to April. On the domestic front, cultivated acreage reached 104,800 acres in 2024, accounting for 40% of all berry plantings[2]Source: USDA National Agricultural Statistics Service, “Noncitrus Fruits and Nuts 2024 Summary (May 2025),” nass.usda.gov.. However, labor scarcity, pest losses exceeding USD 718 million annually, and California water costs of up to USD 2,000 per acre-foot are constraining yield gains, despite the emergence of high-tunnel and container systems that can potentially double open-field output. Competitive pressure is intensifying as Driscoll’s and Agroberries expand their proprietary genetics and vertically integrated supply chains, while mechanization reduces Oregon harvest costs from USD 1,323 to USD 331 per metric ton, delivering close to USD 10 million in annual statewide savings. Finally, the launches of functional beverages and the dietary habits of glucagon-like peptide-1 (GLP-1) medication users are opening ancillary demand channels that blur the lines between produce and wellness categories, lifting elasticity for premium fruit.

Key Report Takeaways

By source, counter-seasonal imports accounted for 62.0% of the United States blueberry market share in 2025, while the domestic supply is projected to grow at an 8.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Blueberry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on antioxidant-rich foods | +1.2% | National and strongest in urban coastal markets | Medium term (2-4 years) |

| Growth in controlled-environment agriculture acreage | +1.5% | Pacific Northwest, Southeast, and Midwest tunnel clusters | Long term (≥ 4 years) |

| Inclusion of blueberries in functional beverage launches | +0.8% | National, led by wholesale clubs and natural-food chains | Short term (≤ 2 years) |

| Expansion of domestic high-yield highbush cultivars | +1.3% | Florida, Georgia, and California early adopters | Medium term (2-4 years) |

| Retailer private-label promotion and price locks | +0.9% | National, concentrated in Walmart, Costco, and Kroger | Short term (≤ 2 years) |

| Genomic-assisted breeding cutting time-to-market for new varieties | +0.8% | Research hubs in Florida, Michigan, and United States Department of Agriculture - Agricultural Research Service sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Controlled-Environment Agriculture Acreage

Controlled-environment setups, such as high tunnels and substrate containers, are helping growers extend their harvest calendars and secure premiums when supply is tight. These structures can move the picking window up by four to five weeks compared with open-field rows, putting domestic fruit on shelves before Peruvian arrivals swell the September-April market. USDA data counted 104,800 cultivated blueberry acres in 2024, a 2% increase over 2023, with a rising share of that gain attributed to protected systems across the Southeast and Pacific Northwest. Container production that relies on five- to seven-gallon pots filled with coconut coir or peat moss maintains a pH between 4.5 and 5.5 and an electrical conductivity of less than 2.0 deciSiemens per meter, benchmarks that are challenging to achieve in the alkaline soils of many Midwestern sites. Densities can reach 10,976 plants per hectare, yet outlays often exceed USD 120,000 per hectare, limiting uptake to operations with strong capital access or channels that reward premium fruit. Rising wages and the increasing availability of soft-catch harvesters will enhance the appeal of controlled environments; however, smaller farms may remain in open fields due to upfront costs and the need for cultivar matching.

Expansion of domestic high-yield highbush cultivars

Marker-assisted breeding from university partnerships is rolling out Farthing, Chickadee, and Meadowlark lines that deliver firmer berries and longer shelf life. Southern highbush cultivars thrive in low-chill regions, with Florida’s FasTrack program cutting the juvenile phase to under one year. Yield improvements close the historical gap where Peruvian fields produced nearly double per-hectare volumes. Replanting costs of nearly USD 120,000 per hectare constrain rapid turnover. However, payback periods shorten as price stability improves and input costs level off.

Retailer Private-Label Promotion and Price Locks

Private-label blueberries, priced 15-25% below branded clamshells, held a combined 55% share at Walmart, Costco, and Kroger in 2025. Price commitments shield shoppers from seasonal swings but move margin pressure to packers. Retailers that locked in multi-year supply during the 2025 Peruvian tariff maintained facings, while competitors scrambled. As penetration increases, smaller growers without scale must pivot toward direct-to-consumer models or niche organic markets.

Genomic-assisted breeding cutting time-to-market for new varieties

CRISPR-Cas9 edits achieved efficiencies of up to 23% in USDA trials, and the USD 6.4 million VacciniumCAP consortium aligns genomic selection pipelines to predict seedling performance. Pangenome assemblies pinpoint loci for firmness and acidity, enabling breeders to release cultivars that withstand mechanical harvest[3]Source: USDA Agricultural Research Service, “Blueberry Genomics and Breeding Research,” ars.usda.gov. State-level labeling rules and import regulations may fragment early adoption, but growers in permissive jurisdictions can secure a lead on premium genetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages during peak harvest windows | -0.7% | Pacific Northwest, Southeast, and California | Short term (≤ 2 years) |

| Spotted-wing drosophila and emerging fungal pathogens | -0.6% | Pacific Northwest, Great Lakes, and national | Medium term (2-4 years) |

| Rising competition from Peru-origin counter-seasonal berries | -0.5% | Import-dependent regions nationwide | Medium term (2-4 years) |

| Water-use restrictions in California growing regions | -0.2% | Central Valley and southern coastal districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor shortages during peak harvest windows

Soft-catch machines reduced Oregon picking costs around USD 0.33 per kg, saving USD 10 million annually, yet installations run above USD 200,000, and many legacy blocks lack uniform ripening traits. Immigration policy uncertainty and competition from higher-paying crops reduce crew availability, leading to rushed picking that compromises berry size and firmness. Robotics remains in its prototype stage, leaving growers vulnerable to wage inflation and unharvested fruit.

Spotted-wing drosophila and emerging fungal pathogens

Economic losses top USD 718 million yearly as the insect lays eggs in ripening fruit. Exclusion netting costs roughly USD 6,100 per acre and is prohibitive for conventional operations. Fungicide rotations are facing rising resistance, and climate change is extending the range of pests northward. Growers without rigorous monitoring can lose up to 30% of their crop, discouraging new plantings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Regional production is anchored in Washington, Oregon, Michigan, Georgia, and Florida, with each region tailoring cultivar choices to its local chill-hour profiles. Pacific Northwest farms enjoy temperate summers and access to irrigation, enabling both fresh and processed streams. Southeast orchards capitalize on mild winters to enter the market ahead of Peruvian arrivals, commanding premiums for early fruit. Michigan channels substantial output into frozen supply for food service and bakery clients, while California’s acreage remains limited by water constraints and competition from higher-margin strawberries. The 18% acreage growth since 2017 is slowing as pest pressure, labor scarcity, and groundwater caps emerge.

Urban coastal markets exhibit the highest per-capita consumption, driven by health-conscious demographics and the dominance of chains that offer private-label programs. Fruitist distributes into 12,500 North American locations, illustrating how vertically integrated suppliers meet the volume and quality requirements of national retailers. Food-service demand is concentrated in metropolitan areas where smoothies, salads, and baked goods featuring blueberries are available year-round. Income and education levels correlate with higher blueberry consumption, indicating potential for improvement in rural and lower-income areas.

Import reliance is most pronounced in the Northeast and Midwestern states during the September–April off-season, when domestic harvests decline. Ports at Los Angeles, Miami, and Newark handle the bulk of arrivals, and cold-chain integrity at these nodes governs retail shelf life. If Peruvian shipments retreat because of continued tariffs, regions with limited local production risk price spikes and potential shortages, whereas Southeast and Pacific Northwest growers may lengthen their seasons under tunnels to capture new demand.

Competitive Landscape

The United States blueberry market is increasingly characterized by vertical integration, with major players managing breeding, production, packing, and distribution to ensure consistent quality and a year-round supply. Prominent marketers, such as Driscoll's Inc. and Naturipe Farms LLC, utilize extensive grower networks and counter-seasonal sourcing to stabilize supply volumes and meet retailer demands, creating significant competitive barriers for smaller market participants.

Competition in the market revolves around proprietary genetics, control over cold-chain and packing infrastructure, and direct alignment with retailers. Breeding programs focus on traits such as firmness, shelf life, sweetness, and compatibility with mechanical harvesting, which help reduce shrinkage and enhance product consistency. These capabilities increasingly set large, vertically integrated suppliers apart from independent growers and regional packers.

Automation and digitalization are transforming cost structures and operational efficiencies in the market. Soft-catch harvesting systems and post-harvest automation reduce reliance on labor, while traceability and logistics platforms enhance supply chain transparency. Although controlled-environment production presents opportunities for new entrants, the high capital investment required continues to favor well-capitalized, vertically integrated operators.

Recent Industry Developments

- October 2025: Fruitist raised USD 150 million led by J.P. Morgan to expand jumbo-blueberry acreage, cold storage, and post-harvest automation across its United States farms, bolstering supply for 12,500 North American retail outlets.

- October 2025: AMFRESH bought TERRAMARA FRESH, adding 600 hectares of next gen blueberries to its Pacific Rim network and strengthening year round deliveries to United States retailers through patented, high-antioxidant cultivars.

- September 2024: Agroberries acquired BerryWorld, creating the second-largest berry marketer with major blueberry acreage in Washington, Oregon, California, and Florida, supported by United States-based cooling hubs that shorten harvest-to-shelf time.

United States Blueberry Market Report Scope

A blueberry is a small, round, blue-purple berry from the Vaccinium genus, valued for its sweet-tart flavor, high antioxidant content, and use in fresh consumption and processed foods.

The United States Blueberry Market Report is segmented by production (in terms of volume), consumption (in terms of value and volume), imports (in terms of value and volume), exports (in terms of value and volume), wholesale price trend analysis and forecasts, as well as a competitive landscape. Market forecasts are provided in terms of value (USD) and volume (metric tons).

United States

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistic and Infrastructure | ||

| Seasonality Analysis | ||

| United States | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large is the United States blueberry market in 2026?

The United States blueberry market is estimated to reach USD 6.40 billion in 2026 and is forecast to expand to USD 9.80 billion by 2031.

What is the projected growth rate of the United States blueberry market through 2031?

The market is projected to increase at an 8.90% CAGR during the 2026–2031 period.

What are the main production challenges for United States growers?

Key hurdles include labor shortages, spotted-wing drosophila and fungal diseases, high water costs in California, and capital requirements for high-tunnel systems and mechanical harvesters.

How are retailers influencing blueberry pricing?

Large chains use private-label programs and multiyear price locks that shift margin risk to growers but stabilize consumer prices, especially during off-season import fluctuations.

Page last updated on: