Adherence Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

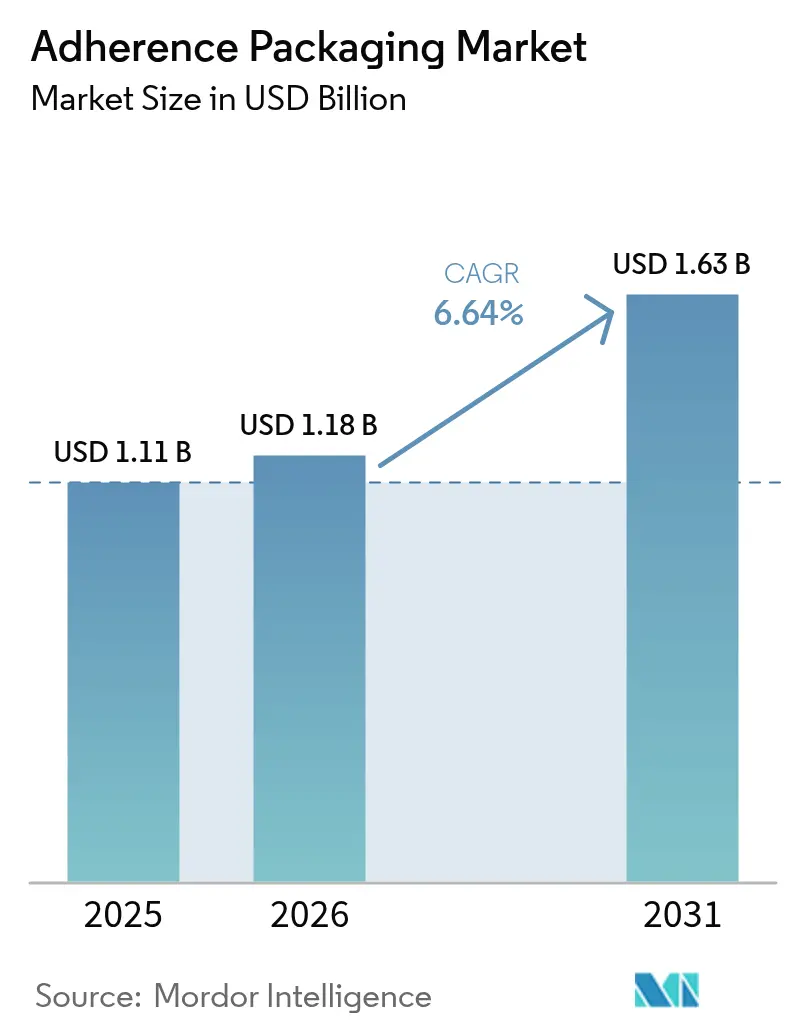

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adherence Packaging Market Analysis by Mordor Intelligence

The adherence packaging market size is expected to grow from USD 1.11 billion in 2025 to USD 1.18 billion in 2026 and is forecast to reach USD 1.63 billion by 2031 at 6.64% CAGR over 2026-2031. Growth accelerates as chronic disease prevalence heightens the need for medication compliance, centralized pharmacy automation scales adherence formats, and payer incentives make packaging‐enabled adherence a reimbursable outcome. North America leads current demand thanks to Medicare Advantage bonus payments tied to CMS Star Ratings, while Asia-Pacific exhibits the most rapid expansion on the back of widening healthcare access and regulatory convergence. Material innovation, especially in recyclable composites, aligns with global sustainability mandates, and mounting geriatric polypharmacy pushes providers toward user-friendly dose organization. Competitive intensity rises as automation vendors, material scientists, and data-driven start-ups converge on integrated adherence solutions that generate measurable health and cost benefits.

Key Report Takeaways

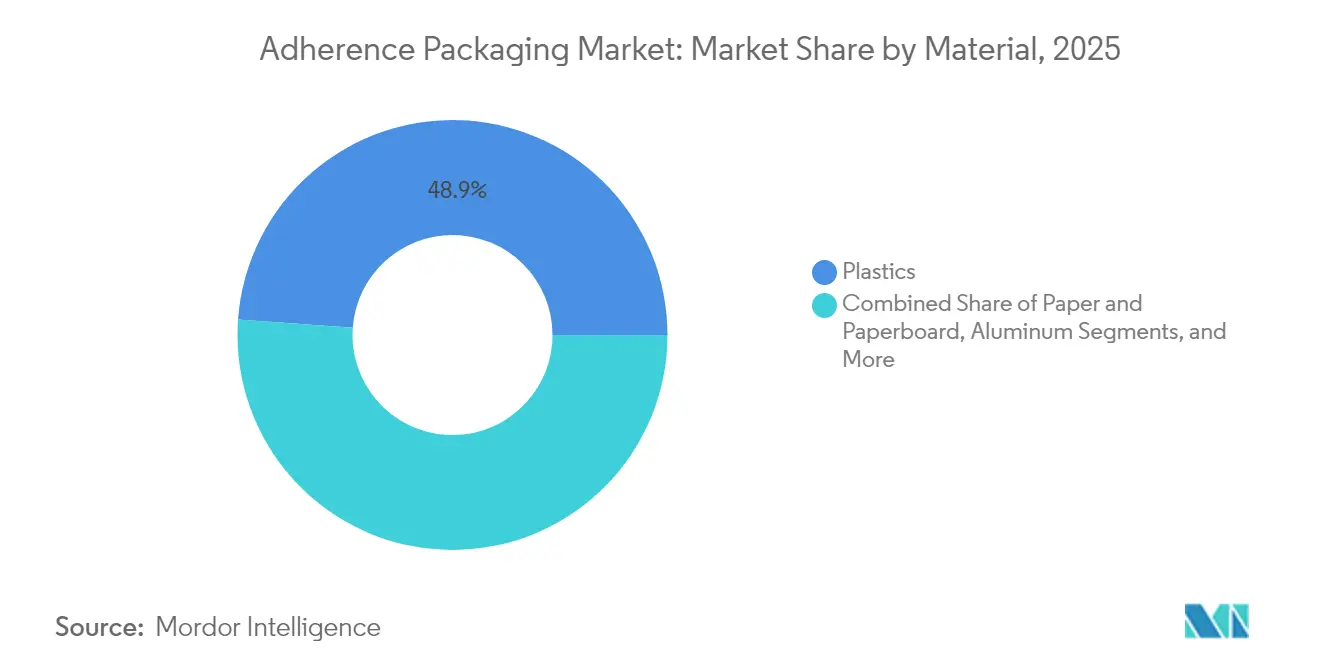

- By material, plastics retained 48.86% of the adherence packaging market share in 2025, yet composite alternatives are advancing at an 7.90% CAGR through 2031.

- By system, multi-dose formats held 61.74% share of the adherence packaging market size in 2025, while unit-dose products are projected to expand at a 7.05% CAGR to 2031.

- By end user, retail pharmacies commanded 45.48% of the adherence packaging market size in 2025, whereas mail-order channels record the highest projected CAGR at 6.98% through 2031.

- By geography, North America led with 38.92% of adherence packaging market share in 2025; Asia-Pacific is forecast to post the fastest 8.31% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adherence Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Need to Minimize Medication Wastage | +1.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| High Prevalence of Medication Non-adherence | +1.8% | Global, particularly acute in North America | Short term (≤ 2 years) |

| Geriatric-Driven Polypharmacy Surge | +1.5% | Global, spill-over into Asia-Pacific and Europe | Long term (≥ 4 years) |

| Centralized Pharmacy Automation Scaling | +1.1% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Payer Incentives Linked to Adherence Metrics | +0.9% | North America core, selective EU adoption | Short term (≤ 2 years) |

| ESG Push for Recyclable Paper-based Blisters | +0.7% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Need to Minimize Medication Wastage

Serialization requirements under the U.S. Drug Supply Chain Security Act highlight dose-level traceability, making adherence packaging instrumental in cutting redundant stock and expired returns. Dose-specific dispensing curtails over-prescription while improving compliance, lowering pharmaceutical waste across retail, mail-order, and institutional channels. Health agencies estimate that better adherence could prevent 125,000 U.S. deaths annually and save USD 100-289 billion in direct costs. [1] U.S. Department of Health and Human Services, “Medication Adherence Report 2024,” hhs.gov Parallel cost pressure from an 18% polyethylene price jump during 2024 encourages sustainable formats that reduce virgin resin dependency while matching pharmaceutical barrier needs.

High Prevalence of Medication Non-adherence and Cost Burden

Roughly one in two chronic-condition patients worldwide fails to take therapy as prescribed, prompting urgent demand for packaging that makes regimens simpler to follow. Poor compliance contributes to 125,000 U.S. deaths and more than USD 100 billion in avoidable spending each year. [2]Centers for Disease Control and Prevention, “Medication Adherence Study 2024,” cdc.gov Programs such as Kaiser Permanente’s diabetes blister initiative raised adherence 23% and cut emergency visits 15%, showing tangible clinical and economic upside. Connected packs layer sensors and mobile alerts onto traditional formats, giving providers real-time visibility and enabling early outreach before complications escalate.

Geriatric-Driven Polypharmacy Surge

Four in ten adults aged 65+ now manage five or more daily medications, magnifying confusion, drug interactions, and dosing errors. Updated 2024 Beers Criteria list packaging aids among essential geriatric tools. Color-coded reminders, time-stamped pockets, and easy-open seals help older adults and caregivers coordinate complex regimens. Aluminum price swings of 22% during 2024 encourage research into alternative barriers that keep tablets stable while holding costs steady for fixed-income seniors.

Centralized Pharmacy Automation Scaling Adherence Formats

Large chains and health systems funneled record capital into robotic dispensing during 2024, with 78% of U.S. chains implementing automation that favors machine-compatible packs. Automated fill-and-seal units lift throughput, trim labor, and raise accuracy. CVS Health documented a 35% accuracy gain and 28% cycle-time reduction after installing integrated adherence lines. When packaging suppliers align tooling with robotics vendors, pharmacies unlock end-to-end workflow efficiency from inventory management to last-mile delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Installation and Maintenance Costs | −0.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Limited Awareness Among Physicians and Caregivers | −0.6% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Data-Privacy Regulations Hindering Smart Packs | −0.5% | EU leading, global expansion | Short term (≤ 2 years) |

| Recycling Mandates Raising Multi-material Costs | −0.4% | EU core, North America following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Maintenance Costs of Automated Systems

Independent pharmacies face average robotics outlays of USD 500,000-750,000, or roughly one-fifth of annual revenue. [3]U.S. Small Business Administration, “Healthcare Technology Investment Report 2024,” sba.gov Additional building upgrades inflate capital demands, while consumables add a recurring 12-18% to operating expenses. Emerging-market providers grapple with currency swings and lower prescription volumes that lengthen payback periods beyond five years, slowing widespread automation uptake.

Limited Awareness Among Physicians and Caregivers in Emerging Markets

Six in ten clinicians in low- and middle-income regions receive minimal training on medication delivery innovations. Without clear understanding of clinical gains, prescribers stay with basic bottles, dampening patient pull and manufacturer investment. Education pilots in Southeast Asia show adoption climbs from 8% to 35% when structured physician programs run for six months, highlighting the value of targeted outreach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Composite Innovation Drives Sustainability

Plastic substrates kept 48.86% of adherence packaging market share in 2025 due to established converting lines, robust moisture barriers, and competitive economics. Yet composites post the swiftest 7.90% CAGR as regulators valorize recyclability and brand owners chase ESG commitments. The adherence packaging industry now sees bio-polymer-paper hybrids advancing from pilot to scale, supported by IPEC guidelines that codify sustainable excipient compatibility. Paper-based formats gain in low-humidity therapies, while aluminum maintains niche leadership in ultra-barrier indications. Pfizer’s 2024 transition of eight products to composite films trimmed packaging carbon 25% without jeopardizing drug stability. Although bio-based resins carry 20-30% premiums, Medicare bonus payments and EU EPR avoidance often offset incremental spend, encouraging broader adoption. Ongoing resin price volatility further underlines the appeal of diversified, less petroleum-dependent material portfolios.

Composites also prove compatible with digital features, embedding near-field communication tags between paper and polymer layers without compromising barrier strength. That integration supports future smart-pack roll-outs in sustainability-sensitive geographies. Suppliers continue optimizing heat-seal windows, printable surfaces, and high-clarity windows to match patient information needs, positioning composites for outsized share capture over the forecast horizon.

By System: Unit-Dose Automation Accelerates

Multi-dose cards dominate retail workflows and therefore retain 61.74% of adherence packaging market size in 2025. Pharmacies favor the format for its week-at-a-glance simplicity across chronic regimens. Even so, unit-dose blister expansion at 7.05% CAGR signals a shift toward hospital and mail-order models that prioritize individual pill tracking. Hospitals deploying unit-dose saw medication errors fall 45% and nursing workflows improve by nearly one-third. Though unit dosing consumes 15-20% more wrap per pill, reduced waste and error mitigation justify the material uptick, especially where payer penalties for adverse events loom large.

Automation spurs further momentum. Robotic loaders accurately place single tablets into color-coded cavities, seal with serialized lidding, and feed data to electronic health records. Closed-loop integration appeals to institutional buyers tasked with audit readiness and controlled substance stewardship. As centralized fill centers scale, economies spread, narrowing the cost delta with multi-dose approaches and helping unit-dose offerings cross into retail and home delivery segments.

By Packaging Format: Pouches Gain Automation Advantage

Traditional blisters remained the largest format with 41.55% share in 2025, supported by decades of tooling optimization, proven tamper evidence, and clear product view. Yet pouches and strips rise 7.26% each year, buoyed by flexible films that require 30-40% less material per dose. Direct-to-print surfaces let pharmacies personalize patient details without secondary labels, cutting changeover time and scrap. Walgreens’ pouch pilot reduced material use 28% and raised fill accuracy 22%, clearly demonstrating operational upside.

Rigid bottles stay relevant for bulk generics, but their share inches lower as payers demand proof of dose-level compliance. Flexible substrates also facilitate ambient, refrigerated, and cold-chain applications by allowing film selection tailored to the molecule, avoiding over-specification and keeping total costs down. Sustainability targets further lift pouches because they traverse recycling streams more readily than multi-layer blisters, especially when paired with mono-material caps and zippers.

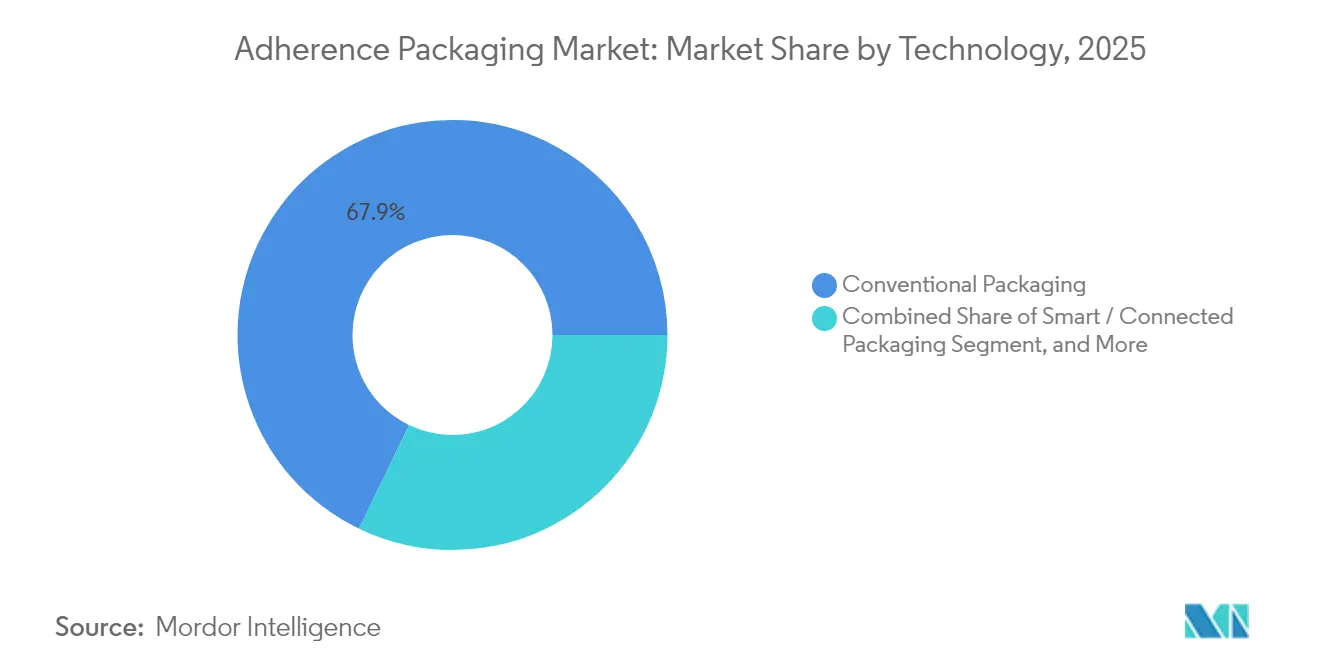

By Technology: Smart Packaging Disrupts Traditional Models

Conventional designs still account for 67.85% of 2025 shipments, but smart and connected solutions log an 7.72% CAGR as IoT platforms mature. IEEE standards now frame interoperability and cybersecurity, enabling scalable rollouts endorsed by health insurers. Novartis observed 38% adherence gains and fewer interventions after piloting sensor-equipped packs that ping patients when doses lapse. Connectivity extends beyond reminders. Aggregated real-world data helps pharma validate value-based contracts and supports regulators in pharmacovigilance, further cementing strategic relevance.

Regulatory headwinds exist, yet suppliers pivot to on-device analytics that store only de-identified metadata, easing GDPR friction. Component miniaturization drops sensor costs, and printable batteries open the door to low-profile layouts that fit existing dispensing equipment. As reimbursement pathways reward documented outcomes, smart packaging becomes less of a novelty and more of a competitive imperative.

By End User: Mail-Order Automation Drives Growth

Retail pharmacies remain the primary channel, reflecting 45.48% of adherence packaging market size in 2025. Face-to-face counseling and local presence keep foot traffic healthy, though high labor overhead pushes chains toward in-store robotics or hub-and-spoke fulfillment. Mail-order providers outpace at 6.98% CAGR by marrying centralized automation with nationwide delivery. The U.S. Postal Service logged 13.2% prescription shipment growth during 2024. Amazon Pharmacy’s integrated packs boosted satisfaction 31% while curbing synchronization issues 24%, underlining convenience gains.

Hospitals and long-term care facilities demand sophisticated, often unit-dose, systems that mesh with electronic med-administration records. Joint Commission guidelines and CMS quality metrics tie reimbursements to safe drug handling, sustaining institutional investment. Scale favors packagers that tailor configurations to each end user’s workflow, regulatory setting, and payer mix, reinforcing the need for modular, automation-ready equipment lines.

Geography Analysis

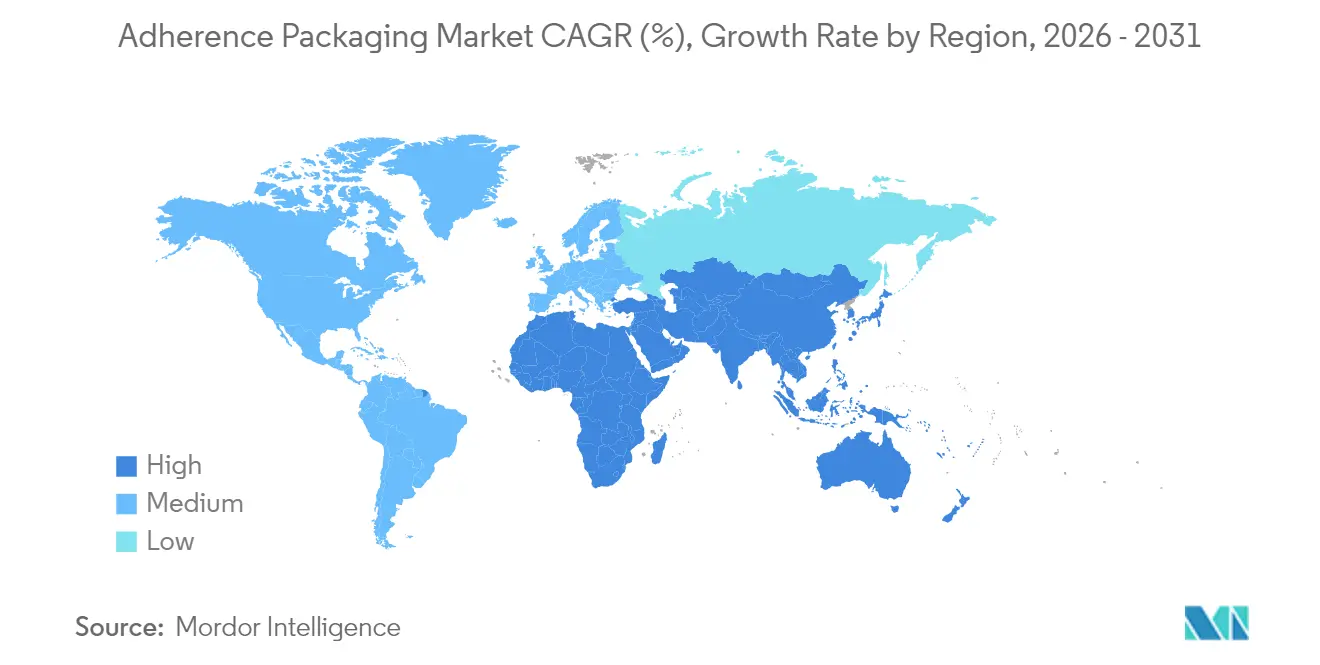

North America captured 38.92% of adherence packaging market share in 2025 thanks to advanced automation ecosystems and payer programs that reward documented compliance. U.S. adoption is anchored by Medicare Advantage bonus structures, the Drug Supply Chain Security Act’s serialization rules, and widespread mail-order penetration. Canada’s single-payer approach emphasizes cost-effective formats and steady composite uptake, while Mexico’s budding private insurance sector introduces new growth pockets as regulations converge with international standards.

Asia-Pacific posts the most robust 8.31% CAGR, driven by expanding access, aging demographics, and chronic disease escalation. China upgrades hospital pharmacies and local packaging capacity under NMPA rules aligned with global norms, unlocking substantial volume for both conventional and smart packs. Japan, South Korea, and Australia, with mature infrastructure, deploy automation and sensor-enabled solutions to address elderly care challenges, yielding measurable reductions in medication-related hospitalizations. India’s trajectory hinges on regulatory harmonization and investment in cold-chain and e-pharmacy logistics, which are progressing alongside digital-health initiatives.

Europe balances sustainability leadership with privacy protection. The PPWR mandates full recyclability by 2030, fast-tracking composite and paper-based innovation. Germany anchors regional volume through reimbursement policies that privilege adherence-enhancing interventions, while France, Italy, Spain, and the United Kingdom advance pilot programs marrying recyclable substrates with data-light smart features compatible with GDPR. Cross-border regulatory divergence following Brexit adds complexity but also fosters solution specialization tailored to national compliance nuances.

Regulatory Landscape

Adherence packaging suppliers operate across medicines packaging controls and packaging sustainability rules. In the European Union, safety-feature requirements under Commission Delegated Regulation (EU) 2016/161 (unique identifier via 2D barcode plus an anti-tampering device) reinforce unit-level traceability for many prescription medicines, which influences lidding design, print quality, and verification workflows across blisters, pouches, and cartons.

Sustainability compliance is tightening in parallel. The EU Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, applies from 12 August 2026 and introduces new requirements around recyclability, labeling, and conformity documentation, with limited exceptions relevant to certain primary pharmaceutical packaging. In addition, ISO 15378:2017/Amd 1:2024 updates GMP-oriented expectations for primary packaging materials (approved in December 2024), strengthening the role of audited quality systems and documented controls across converters and component suppliers.

Value Chain Analysis

The adherence packaging value chain starts with resin, paperboard, aluminum foil, adhesives, coatings, and electronics or identification components (NFC, printed sensors, 2D data matrix coding), followed by film extrusion, thermoforming or cold-form foil conversion, printing, and lamination. Packaging converters then manufacture blisters, pouches or strips, cards, and cartons, while equipment providers supply sealing, vision inspection, and pharmacy automation that must run these formats at high uptime. Downstream, distributors and medication management intermediaries deliver materials and equipment into retail and mail-order pharmacies, hospitals, and long-term care facilities, where adherence packs are filled, verified, and dispensed alongside counseling, reimbursement documentation, and, for smart formats, data capture.

Integration across packaging and data workflows is becoming a defining feature of the chain. Examples include Centor (a Gerresheimer company) co-developing a smart weekly pill organizer with RxCap (April 2025), and Keystone Folding Box Co. partnering with Med-Con Technologies to combine Key-Pak blister cards with digital prompting using 2D matrix barcodes and cloud logging (July 2025). Bottlenecks concentrate in specialized barrier inputs and machine capacity, because high-spec films or foils and validated converting lines require long qualification cycles, and centralized pharmacy automation pushes demand toward machine-compatible materials, print fidelity, and consistent cavity and seal performance.

Competitive Landscape

The adherence packaging market shows moderate fragmentation as established converters, automation houses, and data-driven entrants vie for end-to-end platform leadership. The USPTO recorded 342 packaging patents in 2024, two-thirds focused on smart or sustainable designs, underscoring rapid innovation. Market leaders invest in robotics alliances and vertical integration to lock in pharmacy networks and ensure seamless hardware-consumable interoperability. Omnicell’s 2025 purchase of Medication Management Partners enhances its long-term care reach, while Gerresheimer’s USD 54 million U.S. expansion adds composite capability targeted at North American unit-dose demand.

Start-ups leverage AI analytics and direct-to-consumer channels to disrupt traditional distribution, offering cloud dashboards that link patient, provider, and payer in real time. Meanwhile, material suppliers like Amcor and West advance high-barrier recyclable films and IoT syringe platforms, illustrating how barrier science and electronics converge. Buyers increasingly weigh ESG credentials and data generation potential, not just unit cost, when awarding multi-year supply agreements.

Adherence Packaging Industry Leaders

Amcor plc

Smurfit WestRock

Omnicell Inc.

Becton, Dickinson and Company

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability-compliant adherence formats represent a clear whitespace because many traditional adherence packs rely on mixed materials that are difficult to recycle, while Europe is moving toward stricter packaging sustainability requirements under Regulation (EU) 2025/40 applying from 12 August 2026. Commercial traction for recyclable adherence designs is visible in Jones Healthcare Group, whose Qube Eco (launched in 2025) received Platinum Best of Show at the PAC Global Awards in April 2026 and has been positioned for expansion across North America, the UK, and Europe. This suggests growing buyer readiness to qualify alternatives to legacy multi-material structures.

Another opportunity area sits in the convergence of adherence packaging with automation and connectivity, especially where proof of adherence supports payer programs and clinical follow-up. BD expanded its advanced robotics offering with Sinteco (March 2026) to streamline hospital pharmacy operations, including automated unit-dose packaging from bulk medications, reinforcing demand for unit-dose, machine-readable formats compatible with pharmacy robotics. On the innovation side, PillSafe secured seed investment in March 2026 to commercialize a wirelessly connected adherence system designed to integrate into pharmacy automated fill systems, indicating continued development of adherence packs that generate usable adherence data without major workflow disruption.

Recent Industry Developments

- June 2026: Amcor announced a multi-million-dollar investment to expand its healthcare packaging facility in Sira, Karnataka, India, increasing capacity for high-performance and patient-centric drug-delivery packaging. The investment strengthens local supply for regulated pharma packaging and supports shorter lead times for adherence formats used by fast-scaling pharmacy and hospital channels.

- March 2026: BD and Sinteco expanded their collaboration to advance pharmacy automation, including automated unit-dose packaging systems that convert bulk medications into individually packaged doses for hospital workflows. This supports adoption of unit-dose, traceable adherence formats and tightens the linkage between dispensing robotics and packaging consumables.

- November 2025: Smurfit Westrock opened a dedicated adherence and clinical packaging facility near Dublin Airport, positioned to serve clinical trials and regulated pharmaceutical packaging needs. The facility adds specialized capacity close to major logistics corridors, improving responsiveness for trial kits and compliance-driven packaging programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the adherence packaging market covers packaging formats and related components used to organize and dispense oral solid and similar medications by dose and schedule, which supports patients taking medicines as directed in retail and institutional settings.

Scope exclusions: We exclude drug content value, standalone mobile reminder apps, and general pharmaceutical packs that are not designed for dose organization and adherence support.

Segmentation Overview

- By Material

- Plastics

- Polyethylene

- Polyethylene Terephthalate

- Polyvinyl Chloride

- Other Plastics

- Paper and Paperboard

- Aluminum

- Composite Materials

- Plastics

- By System

- Unit-dose Packaging

- Multi-dose Packaging

- By Packaging Format

- Blisters

- Pouches / Strips

- Bottles

- Other Packging Formats

- By Technology

- Conventional Packaging

- Smart / Connected Packaging

- Sustainable / Eco-friendly Packaging

- By End User

- Retail Pharmacies

- Hospitals

- Long-term Care Facilities

- Mail-order Pharmacies

- Others End User

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning the definition and demand pool with public and non-paywalled sources such as US FDA packaging and labeling guidance pages, US Census Bureau trade and manufacturing statistics, UN Comtrade import and export series for packaging materials, and OECD health statistics that help frame medicine use patterns. We also reviewed sources such as CDC and WHO aging and chronic disease indicators, since adherence-packaging demand tends to track polypharmacy and refill frequency.

To convert this foundation into market math, we screened annual reports, 10-K style filings, investor presentations, and press releases to map product coverage and regional exposure. Patent databases were checked to see where innovation is concentrated, and an import and export shipment-level database was used selectively to sanity-check cross-border movement for key packaging substrates. These sources are illustrative, and additional public references were used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary inputs came from interviews and structured surveys with packaging converters, contract packagers, pharmacy operations teams, and hospital and long-term care stakeholders across major regions. We used these discussions to confirm adoption rates by care setting, typical order sizes, pricing movement by format, and where manual versus automated adherence solutions are being preferred in practice.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 39% |

| Mid tier: 46% | Functional/Unit leaders: 43% | EMEA: 36% |

| Smaller Players: 17% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where healthcare dispensing volumes and patient cohorts are reconstructed by region, then filtered through adherence-packaging penetration by care setting before value is calculated. Because pricing varies by format and automation level, average selling prices are modeled separately for common solutions and then applied to implied unit demand.

To keep the model grounded, we used inputs such as aging population growth, chronic disease prevalence, prescription refill frequency, long-term care bed counts, and pharmacy automation adoption signals as practical indicators that move demand year to year. In markets where public data is thin, gaps were handled by using proxy indicators (for example, refill volumes and institutional capacity) and then adjusting with interview feedback on local adoption.

For forecasting, scenario analysis was used to reflect differences in policy support for adherence programs, the pace of pharmacy workflow modernization, and material cost pass-through. The forward view was also checked with selective bottom-up approximations, such as sampled volume-by-format with realistic price bands from channel checks, which helped correct totals when early runs drifted from what buyers and suppliers see in the field.

Data Validation & Update Cycle

Outputs are validated by triangulating the model against independent signals, such as regional prescription activity proxies, packaging substrate trade patterns, and stated capacity or expansion announcements, then reviewing where the math does not line up. When unusual jumps appear, assumptions on penetration, pricing, or care-setting mix are revisited and follow-up calls are triggered with relevant respondents to confirm what changed.

Before sign-off, the estimates go through multi-step analyst reviews that include variance checks across regions and cross-checks against prior-year patterns. Reports are refreshed annually, and interim updates are made when material events occur, such as policy shifts, major capacity additions, or sharp input cost swings. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Adherence Packaging Market Size Measured Against Other Published Estimates

Published market values for adherence packaging can vary even when they cover the same broad theme, since the market boundary and the conversion from demand to value are not handled the same way. Differences most often come from what is counted as adherence packaging, which care settings are emphasized, and how pricing is treated over time.

By tracking dosing-format mix and refreshing price bands each year using primary checks, Mordor Intelligence keeps the 2026 market total tied to actual pharmacy and institutional usage signals, rather than stretching scope into adjacent pharma packaging or applying a single flat price curve across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.18 B (2026) | |

| Global Consultancy A | USD 1.27 B (2026) | Uses a broader packaging boundary that can pull in general medication packaging adjacent to adherence formats, and assumes faster adoption in institutional channels with less explicit care-setting validation. |

| Industry Publisher B | USD 1.09 B (2024) | Anchors the market on a shorter historical window and applies uniform pricing and penetration assumptions, which can understate value where automated adherence solutions and higher spec materials are growing. |

The comparison shows that the spread is mainly explained by what gets included as adherence packaging and how adoption and pricing are refreshed over the study period. When scope is kept specific to adherence-led formats and the inputs are tied back to measurable dispensing and care-setting indicators, the resulting market size stays easier to trace and repeat from one update to the next.

Key Questions Answered in the Report

What is the current size of the adherence packaging market?

The adherence packaging market size is USD 1.18 billion in 2026 and is projected to reach USD 1.63 billion by 2031.

Which region is growing fastest for adherence packaging solutions?

Asia-Pacific records the highest 8.31% CAGR through 2031, supported by broader healthcare access and regulatory alignment.

Why are composite materials important in adherence packs?

Composites combine pharmaceutical-grade barriers with recyclability, enabling compliance with regulations that require all packaging to be recyclable by 2030.

How do payer incentives affect adoption?

Programs such as CMS Star Ratings reward high adherence scores, encouraging pharmacies to adopt packaging that demonstrably raises patient compliance.

What role do smart packs play in medication management?

Smart packs embed sensors and connectivity that remind patients, track dosing, and feed adherence data back to providers, often lifting compliance by double-digit percentages.

Page last updated on: