Recycled Materials Packaging Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

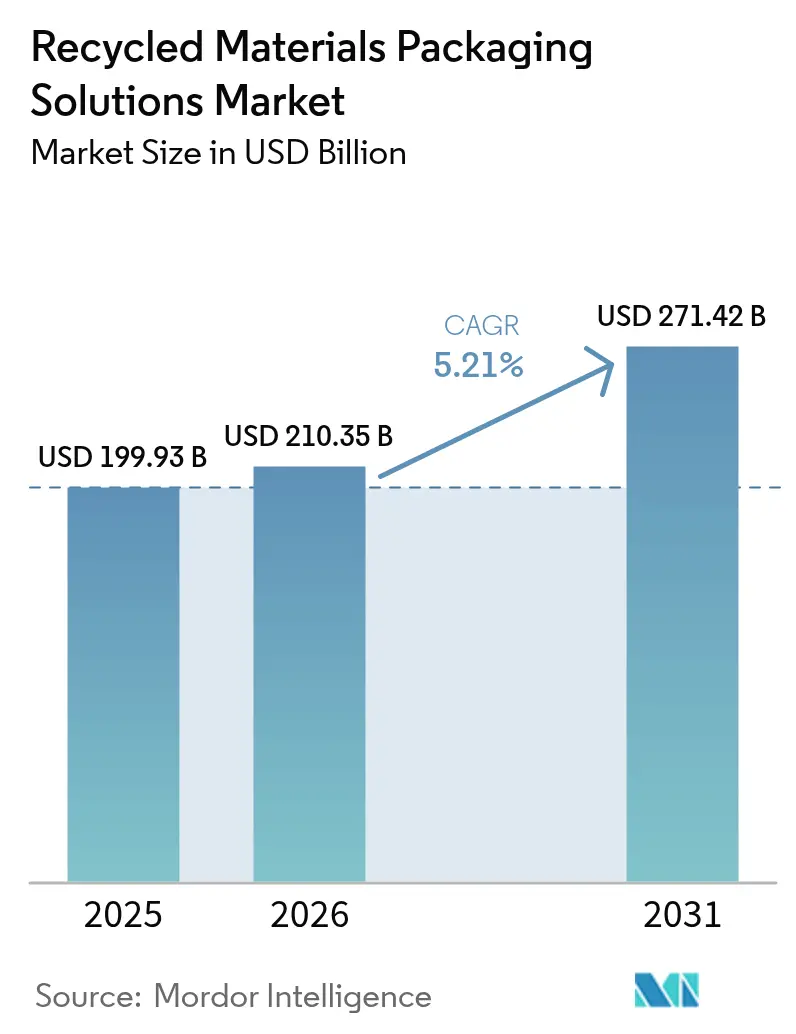

| Market Size (2026) | USD 210.35 Billion |

| Market Size (2031) | USD 271.42 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

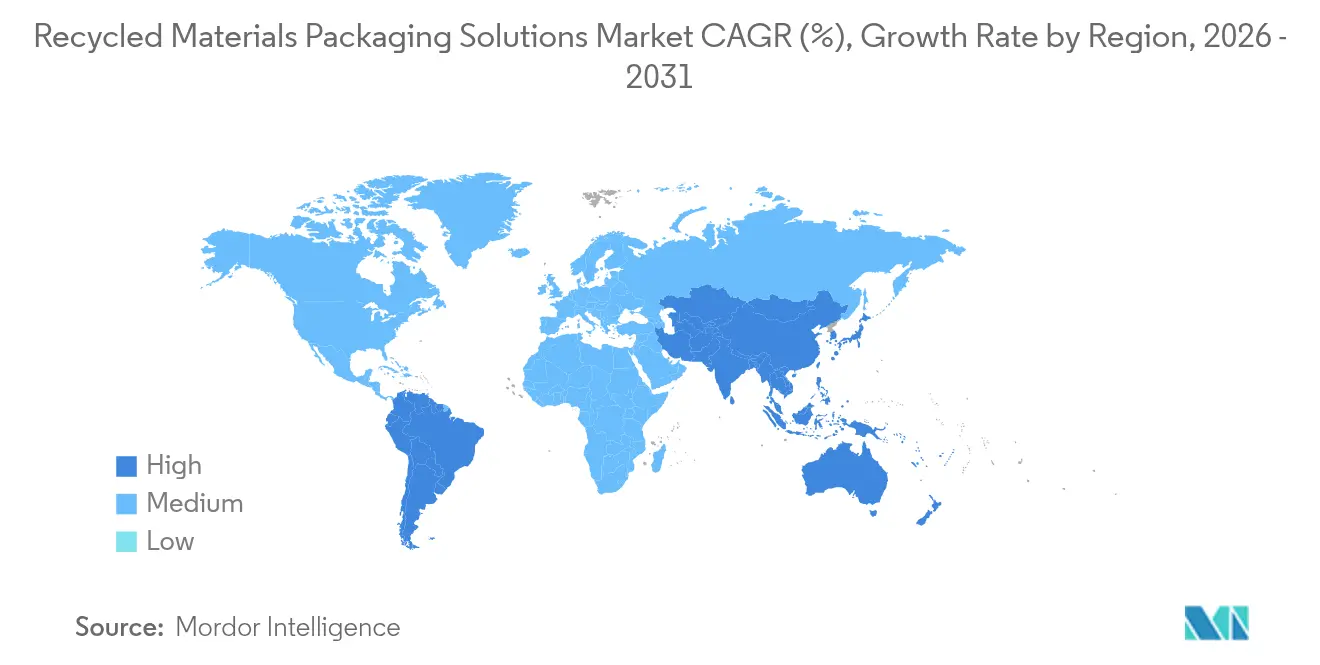

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recycled Materials Packaging Solutions Market Analysis by Mordor Intelligence

The recycled materials packaging solutions market size in 2026 is estimated at USD 210.35 billion, growing from 2025 value of USD 199.93 billion with 2031 projections showing USD 271.42 billion, growing at 5.21% CAGR over 2026-2031. Rising Extended Producer Responsibility mandates, brand-owner recycled-content targets, and investments in artificial-intelligence sortation are collectively positioning the recycled materials packaging solutions market for sustained growth. Asia-Pacific secures early-mover advantages through evolving regulations and large-scale infrastructure projects, while North America and Europe build capacity through chemical recycling and vertically integrated feedstock procurement. Demand is reinforced by consumers willing to pay premiums for low-carbon packaging, which smooths cost differentials between recycled and virgin materials. At the same time, supply-side innovations such as dissolution-based recycling and mono-material flexible pouches are narrowing performance gaps against incumbent virgin solutions.

Key Report Takeaways

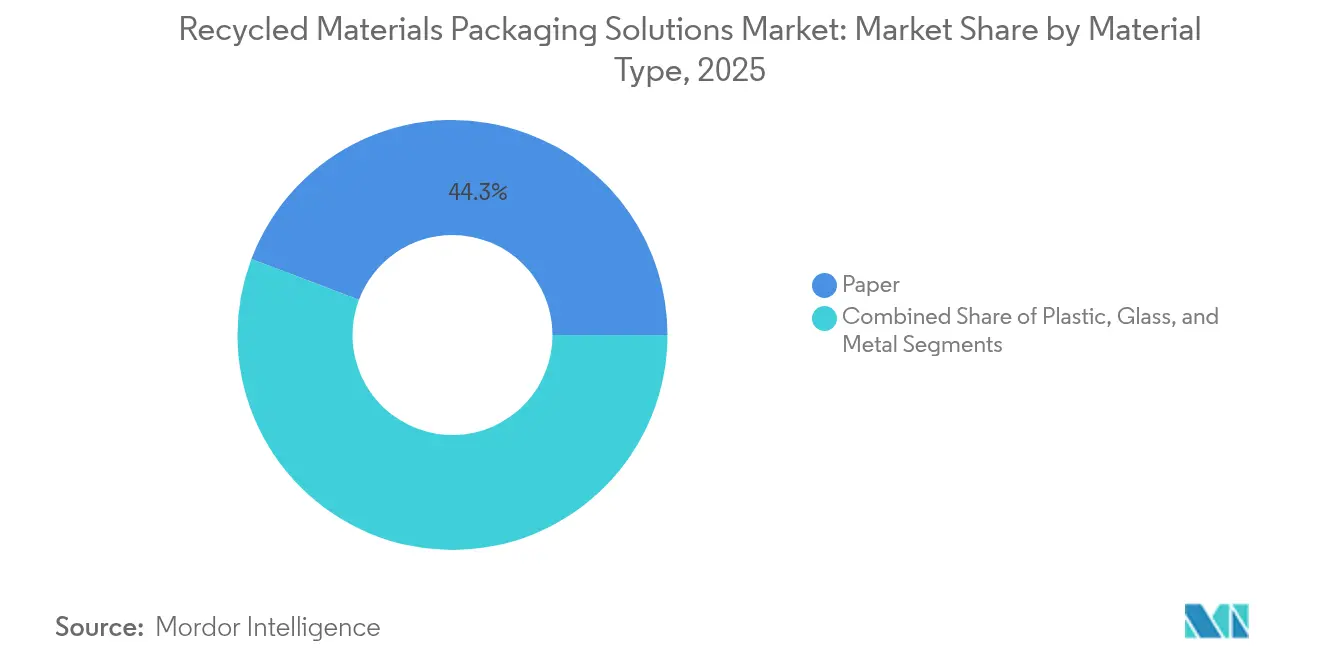

- By material type, paper captured 44.25% of the recycled materials packaging solutions market share in 2025, whereas the plastic segment is projected to grow at a 6.03% CAGR between 2026-2031.

- By end-user industry, food applications captured 36.20% of the recycled materials packaging solutions market share in 2025, whereas the home and personal care segment is projected to grow at a 6.58% CAGR between 2026-2031.

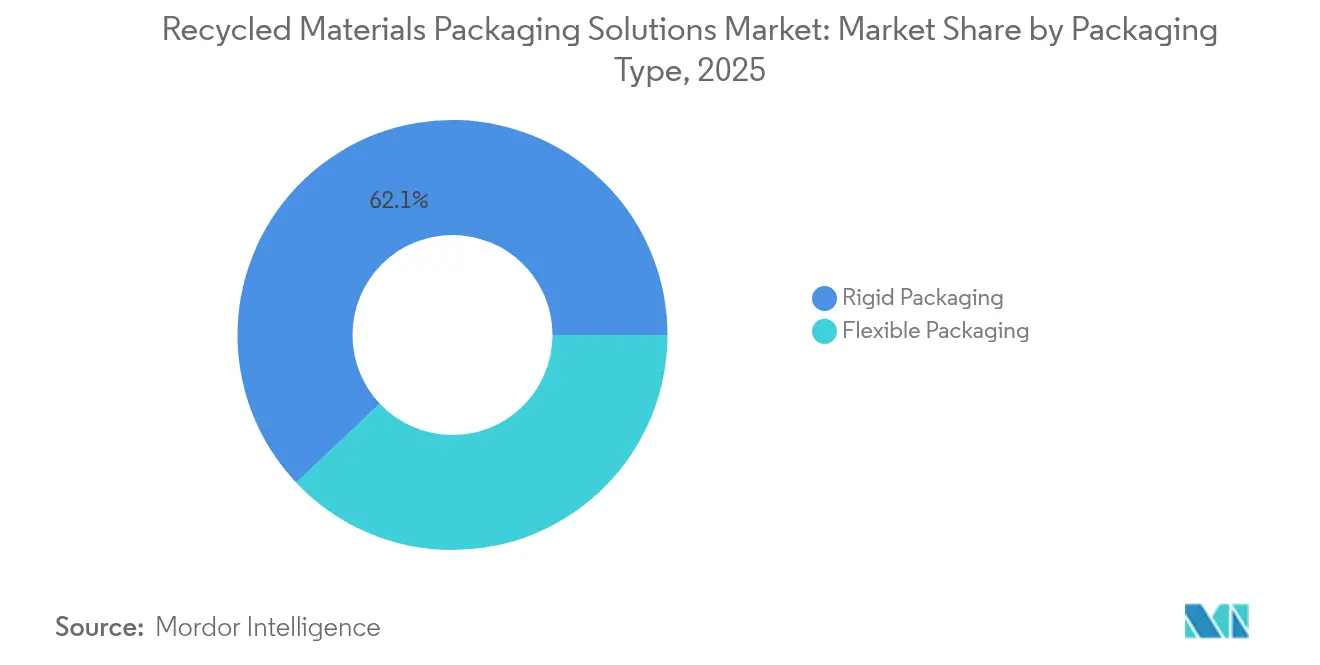

- By packaging type, the rigid packaging segment captured 62.05% of the recycled materials packaging solutions market share in 2025. The flexible packaging segment is projected to grow at a 6.84% CAGR between 2026-2031.

- By source of recycled material, post-consumer recyclate captured 48.55% of the recycled materials packaging solutions market share in 2025. The ocean-bound waste segment is projected to grow at a 7.32% CAGR between 2026-2031.

- By geography, Asia-Pacific captured 45.80% of the recycled materials packaging solutions market share in 2025 and is projected to grow at a 7.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recycled Materials Packaging Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Producer Responsibility (EPR) Mandates Expansion | +1.2% | Global, with early gains in Europe, North America, and the Asia-Pacific | Medium term (2-4 years) |

| Brand-Owner 2025 Recycled-Content Targets | +0.9% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Advanced Sortation Technologies: Reducing Contamination | +0.7% | North America & EU, spill-over to the Asia-Pacific core | Medium term (2-4 years) |

| Consumer Preference for Low-Carbon Packaging | +0.8% | Global, with premium markets leading adoption | Long term (≥ 4 years) |

| Corporate Net-Zero Commitments Accelerating PCR Procurement | +1.1% | Global, with multinational corporations driving demand | Medium term (2-4 years) |

| Surging Investment in Chemical Recycling Capacity | +0.6% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility (EPR) Mandates Expansion

EPR statutes shift end-of-life costs from municipalities to producers, making recycled content economically attractive. Vietnam’s 2024 rules require 22% recycling for rigid PET and 40% material recovery rates, sparking rapid equipment upgrades. South Korea is boosting the required recycled plastic in PET bottles from 3% to 10% and targets 30% by 2030. Thailand’s label-free PET initiative trims contamination and considers tax credits for recycled resin. The EU Packaging and Packaging Waste Regulation mandates 30% recycled PET in food packaging by 2030.[1]National Law Review, “EU Proposal on Packaging Waste Regulation,” natlawreview.com India now allows specified recycled plastics in food packaging, requiring traceability labelling.

Brand-Owner 2025 Recycled-Content Targets

Global brands are voluntarily outpacing regulation. Estée Lauder seeks at least 25% PCR and to halve virgin plastic by 2030. Mars moved key confectionery jars to 100% recycled resin, cutting 1,300 tonnes of virgin plastic each year. Mondelēz will package 300 million Cadbury sharing bars in 80% attributable recycled plastic. Cadbury Australia sourced 1,000 tonnes of chemically recycled polypropylene for Dairy Milk bars.

Advanced Sortation Technologies: Reducing Contamination

AI-enabled optical sorters now reach 99% purity in PET, boosting mechanical recycling yields.[2]Packaging World, “Cadbury Uses Chemically Recycled Plastic,” packworld.com Real-time contamination analytics at more than 150 materials-recovery facilities increase capture rates by 30% and enhance feedstock predictability. Computer-vision platforms accurately classify 28 materials, informing designers of recyclability trade-offs. Flexible packaging streams benefit most, as AI unlocks higher value from what was previously landfill-bound.

Consumer Preference for Low-Carbon Packaging

Around 73% of global shoppers say they will change buying habits to cut environmental impact, with sustainable packaging ranking just behind price and quality. Willingness-to-pay premiums reaches 81% among Europeans, reinforcing recycled content strategies in premium segments. Millennials and Gen Z lead demand, driving rapid uptake in personal care and food categories that can justify premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Supply of High-Quality Recycled Feedstock | -0.8% | Global, with acute shortages in the Asia-Pacific and MEA | Short term (≤ 2 years) |

| Competing Demand from Fiber-Based Substitute Packaging | -0.5% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Unfavorable Economics when Virgin Resin Prices Decline | -0.7% | Global, with oil-dependent regions most affected | Short term (≤ 2 years) |

| Recycling Infrastructure Gaps in Emerging Markets | -0.6% | Asia-Pacific core, MEA, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Supply of High-Quality Recycled Feedstock

Pricing for recycled PET and high-density polyethylene swings widely, imposing budgeting challenges for converters. Beverage brands recently queued 6-8 weeks for food-grade rPET while virgin alternatives were available in 3 weeks. Contamination means 15-25% of collected plastics fail food-grade tests, forcing some brands to under-fulfill recycled-content pledges. The volatility is most acute for barrier materials that demand specialty grades.

Competing Demand from Fiber-Based Substitute Packaging

Molded fiber solutions now mimic plastic barriers, eroding share in cosmetics, electronics, and convenience food packaging. Compostable fiber pouches with water-based coatings meet grease-resistance requirements at a lower unit cost. Established paper recycling networks ease consumer disposal, pulling demand away from recycled plastic whenever barrier performance is acceptable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Dominance Faces Plastic Innovation

In 2025, paper commanded 44.25% of the recycled materials packaging solutions market share, reflecting mature fiber collection systems and corrugated recovery rates above 90% in North America. Plastic is projected to post a 6.03% CAGR through 2031 as chemical recycling improves food-grade quality and unlocks new applications. Glass continues serving premium beverage and cosmetic niches where brand equity values tactile heft. Metal offers infinite recyclability that attracts closed-loop purchasers, buttressing its role in aerosol, beverage, and cosmetics packaging even when volumes remain modest.

Paper maintains steady growth due to global e-commerce, but plastics claim future upside. Investment topping USD 8 billion accelerates chemical recycling to offset the shortfall in food-grade rPET. Examples such as Eastman’s Gemini compact underscore plastics’ progress into cosmetics using molecularly recycled resins. Consequently, the recycled materials packaging solutions market expects a gradual convergence in the material mix between paper and plastic solutions.

By End-User Industry: Food Leadership Yields to Personal Care Growth

Food applications generated 36.20% of 2025 demand, but regulatory safety thresholds constrain growth. India’s new allowance of specific recycled plastics in food packaging under strict traceability slightly relaxes barriers. Beverage brands such as PepsiCo demonstrate 50% recycled polypropylene snack packs, hinting at broader adoption where performance permits.

Home and personal care is set to rise at a 6.58% CAGR, as consumers accept premiums for low-carbon formats. Ball Corporation financed Meadow to launch fully recyclable aluminum cartridges for soaps and shampoos, showing brand readiness to switch materials swiftly. Secondary industries such as e-commerce and industrial packaging also incorporate more PCR as collection networks mature, broadening the recycled materials packaging solutions market.

By Packaging Type: Rigid Formats Leverage Deposit Systems and Reuse Models

Rigid packaging captured 62.05% of the recycled materials packaging solutions market share in 2025. Deposit return schemes for bottles and containers deliver high-purity feedstock that underpins the segment’s reliable recovery economics. Formats such as bottles, jars, and molded containers maintain dimensional stability that protects products and simplifies downstream sortation relative to flexible laminates. Glass preserves premium status in cosmetics and beverages, while aluminum cans average 75% recycled content and circulate indefinitely, reinforcing closed-loop economics. Deposit infrastructure also curbs contamination, enabling rigid plastics to satisfy food-grade thresholds more consistently than flexible counterparts.

Mature curbside and take-back networks grant rigid formats cost advantages when extended producer responsibility fees hinge on recyclability scores. Brother Industries’ cartridge remanufacturing program exemplifies how sturdy housings can be refurbished multiple times, lengthening material life spans well beyond single-use cycles. Reusable shipping boxes from The Ocean Package highlight the segment’s pivot toward e-commerce, achieving several delivery cycles before entering recycling streams. Regulatory momentum reinforces this outlook: the EU will require all packaging to meet recyclability grades of at least 70% by 2030, a benchmark most mono-material rigid items already satisfy. Taken together, these factors point to steady volume growth for rigid formats even as flexible packaging advances technologically, preserving their central role in circular value chains.

By Source of Recycled Material: Ocean-Bound Waste Emerges

Post-consumer recyclate supplied 48.55% of feedstock in 2025, underscoring reliance on curbside collection infrastructure. Ocean-bound and recovered waste streams are set for a 7.32% CAGR as companies monetize marine pollution prevention. Clear Ocean and better-packaging alliances collect coastal plastic that commands brand premiums. PlastX provides traceable recovered plastic across Asia, meeting supply-chain transparency requirements.

Post-industrial recyclate keeps its role as a low-contamination material for specialty applications. Yet ocean-bound initiatives supply new narratives that translate into shelf differentiation, reinforcing the recycled materials packaging solutions market trend toward diverse feedstock portfolios.

Geography Analysis

Asia-Pacific held 45.80% of the recycled materials packaging solutions market size in 2025 and will grow at a 7.55% CAGR. Regulatory clarity, such as Vietnam’s EPR targets, South Korea’s recycled-content thresholds, and Thailand’s tax incentives, is reinforcing investment flows. Infrastructure financing across ASEAN nations addresses collection bottlenecks, closing gaps that historically impeded supply consistency.

North America benefits from USD 8 billion in announced recycling expansions since 2017, adding capacity to process almost 9 million tonnes of waste annually. Extended Producer Responsibility laws in Oregon and Colorado that take effect in July 2025 clarify producer fees and spur redesign toward recyclability. Corporate procurement commitments secure offtake, supporting a stable investment outlook. Europe sustains regulatory leadership. Mandatory 30% recycled PET for food packaging by 2030 and design-for-recycling criteria foster innovation pipelines. Collaborative platforms such as 4evergreen and FINAT develop technical guidance for paper and label liner recycling, respectively. Moderate growth in South America and the Middle East & Africa reflects emerging grant funding and nascent EPR frameworks that gradually enlarge the recycled materials packaging solutions market.

Regulatory Landscape

Regulation (EU) 2025/40 on packaging and packaging waste (PPWR) entered into force on 11 February 2025 and is scheduled to apply generally from 12 August 2026, replacing Directive 94/62/EC. The PPWR tightens EU-wide requirements on recyclability performance and circularity, prompting converter and brand actions on recycled-content sourcing, packaging design, and labeling ahead of the 2026 application date.

Implementation detail is also becoming more explicit: the European Commission issued PPWR guidance (C/2026/3084) on 10 June 2026 to support uniform application across Member States. In parallel, marketing-claim compliance continues to shape packaging choices in the United States, where the Federal Trade Commission Green Guides remain the key federal reference point for environmental claims (with revision status pending as of mid-2026).

Value Chain Analysis

The value chain spans (1) waste generation and collection (municipal and commercial), (2) sorting and beneficiation at materials-recovery facilities, (3) recycling and upgrading via mechanical and advanced/chemical routes, (4) resin, pulp, cullet, and secondary metal production, and (5) conversion into rigid and flexible packaging formats for food, beverage, home and personal care, healthcare, and other end users. Quality-control steps (contamination removal, de-inking, de-odorization/decontamination, and traceability documentation) determine whether output can be used in higher-value applications such as food-contact packaging.

Bottlenecks center on feedstock availability and consistency, particularly for food-grade PCR, and on the economic spread between virgin and recycled inputs. These constraints are driving tighter integration between upstream waste-management and sortation players and downstream resin, paper, and packaging converters through long-term feedstock contracts, off-take agreements, and facility acquisitions, alongside increased use of certification and chain-of-custody mechanisms to validate recycled-content claims and support compliance with rules such as the EU PPWR applying from August 2026.

Competitive Landscape

Regional fragmentation defines the recycled materials packaging solutions industry, though vertical integration is increasing. Paper recycling shows higher consolidation due to capital intensity, while plastic recycling welcomes new entrants deploying proprietary chemical processes. Partnerships such as Plastipak with Kraft Heinz on 100% rPET ketchup containers illustrate brand-converter collaboration aimed at locking in secure feedstock.

Technology firms specializing in AI sortation, ocean-bound plastic recovery, and dissolution recycling introduce competitive tension. ExxonMobil, Dow, and Eastman invest heavily in technologies that yield food-safe resins, often protected by patent portfolios. Industry-wide programs like GreenBlue’s Recycled Material Standard offer certification frameworks that underpin transparent trade in recycled content.

As consolidation progresses, major converters acquire regional recyclers to assure supply security and quality control. This trend, combined with joint ventures in chemical recycling, positions the recycled materials packaging solutions market for gradual but decisive movement toward an integrated circular value chain.

Recycled Materials Packaging Solutions Industry Leaders

Amcor plc

Smurfit WestRock plc

International Paper Company

Mondi plc

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is scalable, regulation-aligned food-contact recyclate supply for plastics, where converters and brand owners need repeatable quality at industrial throughputs. In June 2026, Coperion received a US FDA Letter of No Objection for its HDPE and PP recycling technology, supporting food-grade recyclate production at capacities up to 6,000 kg/h, which strengthens the toolkit for closing the food-grade rHDPE and rPP gap beyond rPET.

Another opportunity is simplifying recycled-content integration for high-volume packaging lines and flexible formats. Plastipak introduced its PakPET Single Pellet Solution in July 2026, a PET resin with 30% recycled content produced in Verbania, Italy, positioned for direct use in PET food packaging production lines. On the demand side, mass balance and attributed-recycled-content approaches are being used to accelerate circular polymers into flexible packaging workflows, including LyondellBasell and Mondelez collaborating in July 2026 to supply CirculenRevive polymers with 100% attributed recycled content for Marabou chocolate flexible packaging, aligning packaging redesign with recycled-content procurement while keeping performance requirements for flexible packs in view.

Recent Industry Developments

- May 2026: Mondi and Dreco co-launched a pillow bag for powder detergent in Germany containing 50% post-consumer recycled content. The project expands recycled-content adoption in home care flexible packaging while maintaining pack functionality, supporting brand sustainability commitments and compliance-readiness as EU requirements tighten.

- March 2026: Smurfit WestRock completed the acquisition of Cartomanabi, a corrugated packaging company in Montecristi, Ecuador, adding more than 50,000 tons of annual production capacity. The acquisition strengthens regional integration and positions the company closer to local demand centers where recycled fiber availability and collection economics shape competitiveness.

- July 2024: Cadbury Australia adopted 1,000 tonnes of certified-circular biaxially oriented polypropylene produced via ExxonMobil Exxtend pyrolysis technology for Dairy Milk packaging, with volumes cited as sufficient for roughly 500 million family-sized blocks. The switch highlighted how advanced recycling and certification models can open flexible-pack applications that face food-contact and performance constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers packaging solutions where recycled material is intentionally used as a key input, and the sizing is expressed in revenue terms for these packaging solutions sold across end-user industries worldwide.

Scope exclusions: Virgin-only packaging, and recycled-material products used outside packaging applications, are excluded from the totals.

Segmentation Overview

- By Material Type

- Plastic

- Paper

- Glass

- Metal

- By End-User Industry

- Food

- Beverage

- Home and Personal Care

- Healthcare

- Other End-user Industries

- By Packaging Type

- Rigid Packaging

- Flexible Packaging

- By Source of Recycled Material

- Post-consumer Recyclate (PCR)

- Post-industrial Recyclate (PIR)

- Ocean-bound and Recovered Waste

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build a clean list of addressable materials, and anchor the model inputs to public signals that can be checked. We leaned on sources such as UN Comtrade trade statistics, OECD environment and waste indicators, EPA materials and waste datasets, and Eurostat packaging and recycling statistics to understand the recycling supply base and cross-border flows.

To connect recycled feedstock availability to packaging demand, we also reviewed sources such as patent databases for recycling and packaging innovations, peer-reviewed journals on recycled-content performance, and trade-association publications on packaging recycling rates and collection systems. Company filings, investor presentations, and reputable press were used to interpret capacity moves, recycled-content commitments, and pricing discussions, with selective use of paid subscriptions for company financials, news and financials, and shipment-level trade tracking where it helped validate scale. These are illustrative sources only, and many other public and paid references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with packaging converters, recycled resin and recycled fiber suppliers, recyclers, brand procurement teams, and channel participants, so assumptions could be stress-tested in plain commercial terms. Because this is a global market, inputs were checked across major demand regions and then reconciled against differences in regulation, collection rates, and recycled-content targets.

We also re-contacted selected experts when desk indicators and initial model outputs showed unusual jumps, which helped tighten ASP logic and adoption timing for recycled inputs in flexible and rigid formats.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 43% | EMEA: 29% |

| Smaller Players: 15% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build, where packaging output and consumption signals are translated into recycled-material packaging value using recycled-content penetration by material and format, and then mapped to end-use buying patterns. Once that structure is set, results are corroborated with selective bottom-up approximations, including sampled supplier and converter revenue checks, and volume-to-value bridges using observed price bands for recycled inputs.

Key model inputs included recycled-content targets by brand and category, collection and sorting rates that influence usable recycled supply, recycled versus virgin price spreads that affect switching, regulatory drivers like EPR and recycled-content mandates, and the split between rigid and flexible packaging where adoption differs. When bottom-up checks had gaps, we filled them using adjacent market ratios (for example, material-level packaging shares) and then tightened the totals through interview feedback.

For forecasting, scenario analysis was applied around recycled feedstock availability and policy enforcement timing, and then smoothed with trend-based checks so year-to-year adoption does not jump unrealistically. The final forecast path reflects what experts expect on penetration, pricing progression, and capacity additions by region over the period.

Data Validation & Update Cycle

Outputs were validated through cross-checks that compare implied volumes and values against independent signals like recycled resin and recycled paper availability, trade movement direction, and typical packaging intensity by end use. Outliers were investigated, and assumptions were revised when a region or material showed a mismatch between modeled penetration and what interviews described as practical buying behavior.

A multi-step analyst review is used before sign-off, with re-checks triggered when new regulations, major capacity announcements, or sharp input cost moves materially change the near-term picture. Reports are refreshed annually, and interim updates are made when events are large enough to alter adoption or pricing, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Global Recycled Materials Packaging Solutions Packaging Solutions Market Estimate Compared With Other Published Estimates

Published market values for recycled-material packaging often differ because companies do not always count the same thing, even when the title looks similar. Differences usually come from whether the estimate is truly packaging-only, how post-consumer versus post-industrial inputs are treated, and whether value is counted at recycled resin level, converter selling price, or brand-level packaged product value.

In this study, the spread is mainly explained by scope and monetization choices, where some estimates fold in a wider set of recyclable or recycled packaging definitions or mix primary, secondary, and tertiary packaging without consistent end-use mapping. Another driver is how pricing is handled, since recycled input price volatility and currency timing can change the total if averages are taken from different quarters or if aggressive penetration assumptions are applied without checks on collection rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 210.35 B (2026) | |

| Industry Publisher A | USD 200.20 B (2025) | Uses a broader recycled materials packaging framing that explicitly spans primary, secondary, and tertiary packaging forms, which can shift totals versus a packaging-solution revenue view tied to recycled-content adoption by format. |

| Industry Publisher B | USD 54.14 B (2026) | Appears closer to a narrower recycled packaging definition with selected materials and product types, which can undercount converter-level packaging solutions that use recycled inputs across wider end-use industries. |

The table shows that scope width and where value is captured (input material versus packaging solution revenue) are the big levers behind the range, and those choices also interact with recycled-content penetration assumptions. By keeping the estimate linked to recycled input usage by material and format, and then checking it against supply and adoption signals, a consistent sizing path is maintained in the model used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the recycled materials packaging solutions market?

The recycled materials packaging solutions market size is USD 210.35 billion in 2026.

How fast is the Asia-Pacific region growing?

Asia-Pacific is advancing at a 7.55% CAGR and holds the largest geographic share.

Which packaging type is expanding the quickest?

Flexible formats are growing at a 6.84% CAGR, supported by mono-material design progress.

Why are brands investing in ocean-bound plastic feedstock?

Verified ocean-bound sources provide brand differentiation and help meet recycled-content mandates.

What are the chief restraints limiting recycled content adoption?

Supply volatility for food-grade feedstock and competition from fiber-based alternatives curb faster uptake.

Page last updated on: