Pharma And Medical Device Sterile Packaging Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

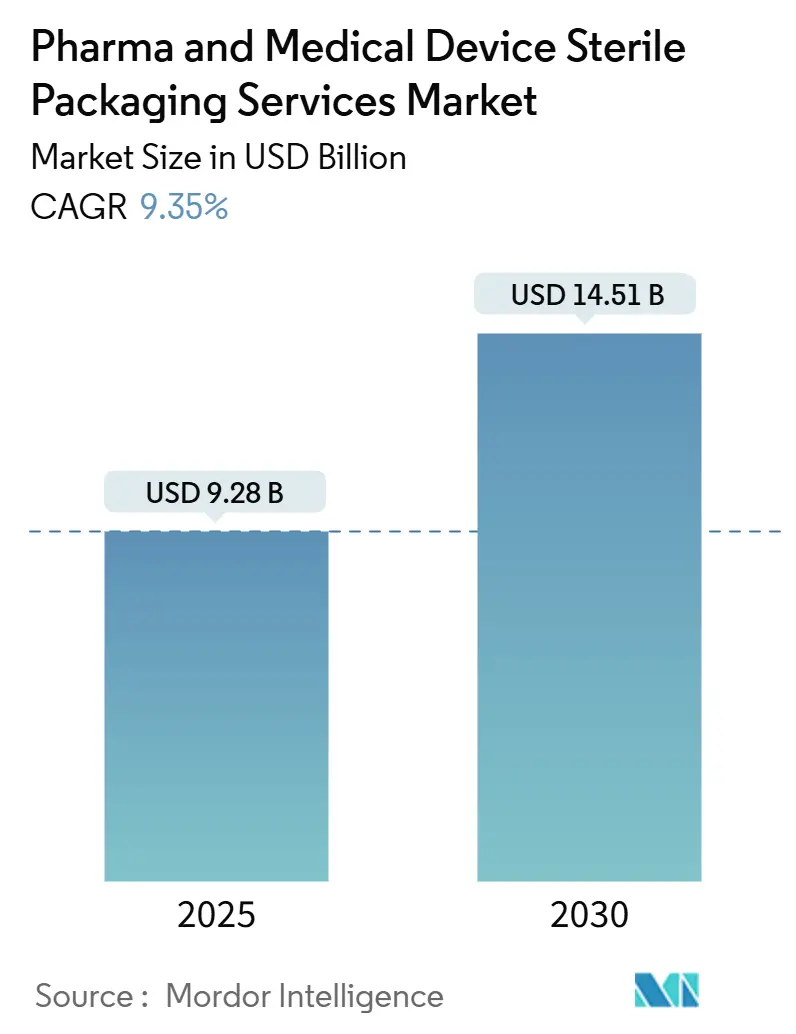

| Market Size (2025) | USD 9.28 Billion |

| Market Size (2030) | USD 14.51 Billion |

| Growth Rate (2025 - 2030) | 9.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

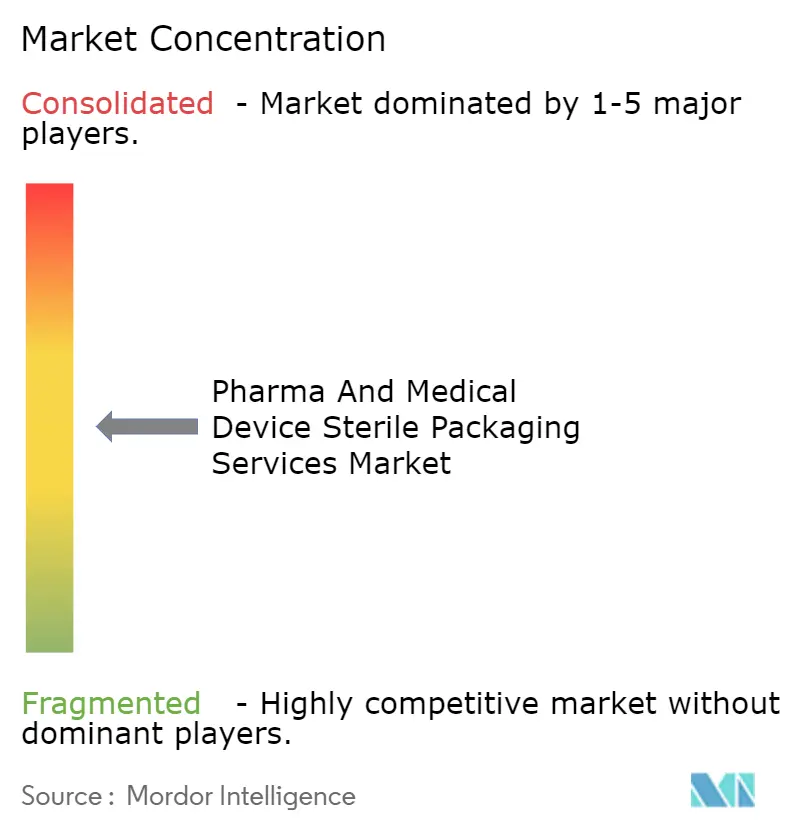

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharma And Medical Device Sterile Packaging Services Market Analysis by Mordor Intelligence

The Pharma and Medical Device Sterile Packaging Services market size reached USD 9.28 billion in 2025 and is projected to climb to USD 14.51 billion by 2030, advancing at a 9.35% CAGR. The Pharma and Medical Device Sterile Packaging Services Market continues to expand as biologics commercialization accelerates, serialization rules tighten, and drug makers redirect capital toward external packaging partners. The demand for unit-dose formats suited to personalized therapies, persistent EtO sterilization bottlenecks, and the rapid adoption of Industry 4.0 automation all influence service mix, pricing, and capacity planning across the value chain. North America preserves leadership, buoyed by established cold-chain infrastructure and strict FDA oversight, while Asia-Pacific registers the sharpest expansion as China and India upgrade GMP rules. Electron-beam sterilization is gaining attention as a greener option for temperature-sensitive products, even as ethylene oxide remains its dominant role. Competitive intensity remains high because integrated CDMOs are absorbing niche providers, broadening geographic footprints, and investing in alternative sterilization assets to hedge regulatory risk.

Key Report Takeaways

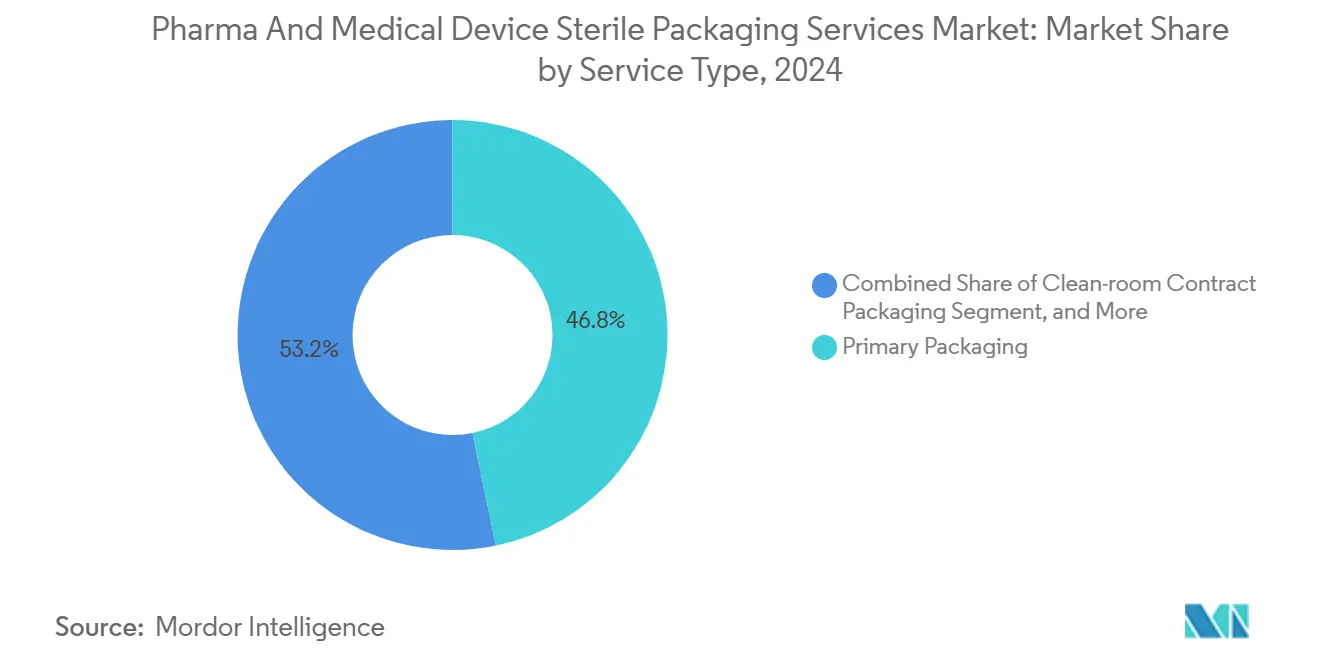

- By service type, primary packaging captured 46.78% of the Pharma and Medical Device Sterile Packaging Services Market share in 2024.

- By packaging format, the Pharma and Medical Device Sterile Packaging Services Market size for blister and strip packs is projected to grow at a 10.95% CAGR between 2025–2030.

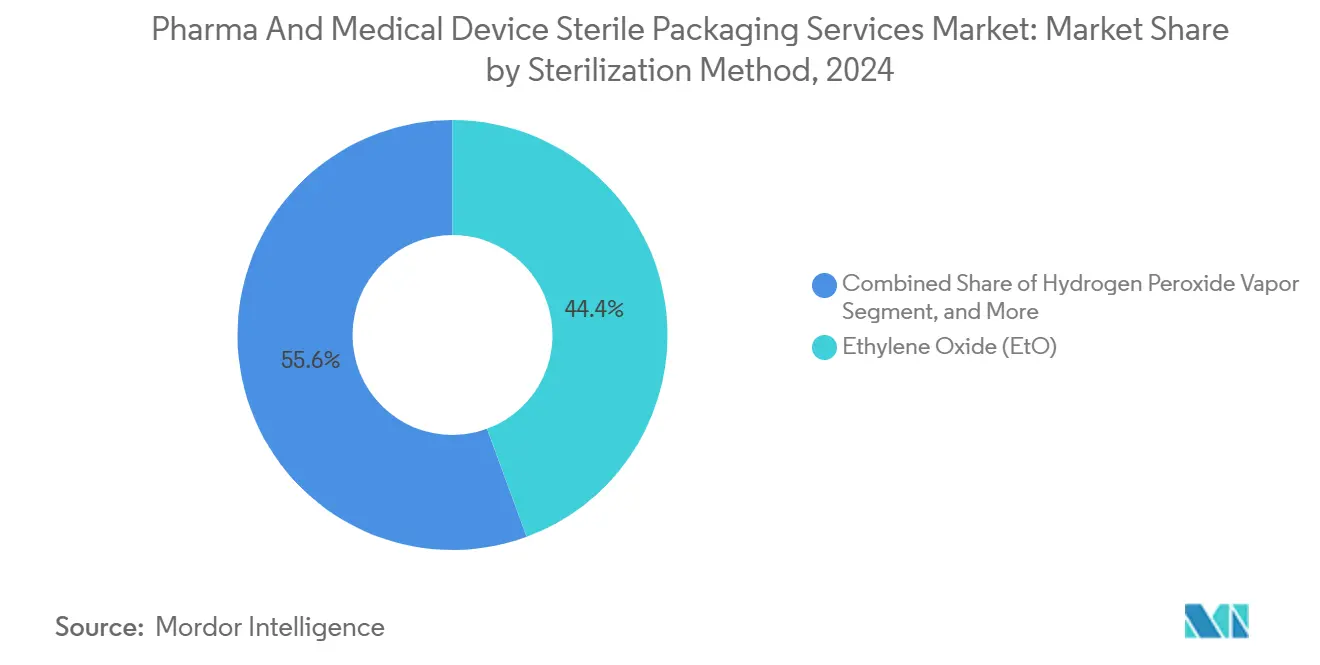

- By sterilization method, ethylene oxide captured 44.38% of the Pharma and Medical Device Sterile Packaging Services Market share in 2024.

- By end-use industry, Pharma and Medical Device Sterile Packaging Services Market size for CDMOs/CMOs/CROs is projected to grow at 10.74% CAGR between 2025–2030.

- By geography, North America captured 37.56% of the Pharma and Medical Device Sterile Packaging Services Market share in 2024.

Global Pharma And Medical Device Sterile Packaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Biologics and Cell-Gene Therapies | +2.1% | Global, with early gains in North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Expansion Of Contract Packaging Outsourcing Among Mid-Tier Pharma | +1.8% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Stricter Global Sterility and Serialization Mandates | +1.5% | Global, with regulatory influence from the FDA, EMA, and WHO | Long term (≥ 4 years) |

| Mini-Batch, Personalized-Medicine Demand for Flexible Sterile Fills | +1.3% | North America and the EU, expanding to APAC | Medium term (2-4 years) |

| Automation And Industry 4.0 Boosting Clean-Room Productivity | +1.2% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Shift to Eco-Friendly Sterile Barrier Materials | +0.9% | Europe and North America core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Biologics and Cell-Gene Therapies

Explosive biologics pipelines and regulatory momentum behind advanced therapy medicinal products are reshaping the requirements for sterile packaging. Cell and gene therapies often ship at temperatures below -80 °C, compelling providers to validate cryogenic vials, bags, and overwraps that guard sterility throughout ultra-cold chains. Personalized doses require mini-batch fills, serialized labels, and chain-of-identity safeguards integrated into packaging workflows. Single-use, gamma-compatible polymer assemblies help producers cut cross-contamination risk during small runs. The Pharma and Medical Device Sterile Packaging Services Market, therefore, channels capital toward high-integrity stoppers, dual-chamber syringes, and tamper-evident formats. North America and Europe dominate early demand, but funding for local biologics plants in the Asia-Pacific is accelerating capability transfer.

Expansion of Contract Packaging Outsourcing Among Mid-Tier Pharma

Rising biologic complexity and multi-jurisdictional labeling rules are pushing mid-sized drug makers to outsource sterile packaging to CDMOs. Maintaining GMP-compliant cleanrooms, conducting environmental monitoring, and providing ready-to-use components can strain internal budgets, making fee-for-service models more attractive. Recent acquisitions, including Novo Holdings’ USD 16.5 billion Catalent deal, show how investors prize end-to-end packaging depth. CDMOs respond with modular fill-finish suites, online vision inspection, and site-wide serialization, enabling sponsors to launch regionally tailored packs more quickly. The Pharma and Medical Device Sterile Packaging Services Market thus benefits from predictable outsourcing pipelines as innovators focus capital on R&D rather than plant upkeep.

Stricter Global Sterility and Serialization Mandates

The FDA Drug Supply Chain Security Act and the EU Falsified Medicines Directive mandate item-level traceability, elevating packaging investment. Installing vision cameras, aggregation modules, and compliant data repositories costs an average of EUR 600,000 per line. The revised EU GMP Annex 1 extends risk management concepts to packaging, compelling service providers to reassess airflow zoning and sterile barrier validation. Medical device packaging must also comply with ISO 11607-1, which specifies the tightening of material and seal strength. These layered rules keep barriers high for new entrants, but position established vendors to offer premium compliance packages, thereby boosting the overall trajectory of the Pharma and Medical Device Sterile Packaging Services Market.

Automation and Industry 4.0 Boosting Clean-Room Productivity

Real-time particle monitoring, robotic syringe plunger feed systems, and digital twins are transforming aseptic packaging. Predictive analytics cuts unplanned downtime, while machine-learning models detect seal integrity deviations before the product reaches release testing. Remote human-machine interfaces enable quality teams to audit operations without the need for gowning, thereby minimizing human bioburden. Closed-loop feedback to servo-driven crimpers stabilizes mechanical force profiles, strengthening container closure integrity. The Pharma and Medical Device Sterile Packaging Services Market advantages providers that adopt smart systems, as sponsors favor partners who can deliver higher yields and audit-ready data logs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Eto Capacity and Environmental Scrutiny | -1.4% | North America and the EU, regulatory influence from the EPA, state authorities | Short term (≤ 2 years) |

| High Validation and Compliance Costs for SMEs | -0.9% | Global, with a higher impact on emerging markets | Medium term (2-4 years) |

| Volatile Polymer and Tyvek Input Prices | -0.7% | Global, with supply chain dependencies | Short term (≤ 2 years) |

| Supply-Chain Fragility for Gamma Irradiators | -0.5% | Global, with a concentration in established markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited EtO Capacity and Environmental Scrutiny

Only 88 EtO facilities operate in the United States, and utilization exceeds 90%. The Environmental Protection Agency’s 2024 rule mandating 90% emission reductions forces multimillion-dollar upgrades, threatening shutdowns where retrofits prove uneconomic. Approximately 56% of critical medical devices still rely on EtO, leaving little room for error if even a handful of plants go offline. Packaging firms hedge by validating electron-beam and X-ray methods, but face multi-year material compatibility studies. Until proven alternatives scale, EtO bottlenecks can delay launches and inflate lead times across the Pharma and Medical Device Sterile Packaging Services Market.[1]ECRI Institute, “The EtO Sterilization Dilemma,” ecri.org

High Validation and Compliance Costs for SMEs

Small enterprises pay roughly EUR 27,100 per GMP inspection and must repeat audits for each export jurisdiction. Serialization adds operating costs of 4.1 cents per pack, eroding margins on low-volume generics. Capital tied up in redundant cleanroom HVAC and sterility testing blocks R&D outlays, nudging SMEs toward outsourcing. Without scale, many cannot amortize digital track-and-trace platforms or automated in-line leak testing, limiting in-house competitiveness. The resulting consolidation funnels volume toward large CDMOs, shaping demand patterns in the Pharma and Medical Device Sterile Packaging Services Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Solutions Drive Market Evolution

Primary packaging captured 46.78% of the Pharma and Medical Device Sterile Packaging Services market share in 2024, reflecting drug makers’ priority on container closure integrity at the dose level. Integrated suppliers deliver ready-to-fill syringes, nested vials, and barrier-coated stoppers that pass Annex 1 visual quality thresholds. Sponsors rely on validated media fill runs and helium leak tests to secure global batch release, locking in long-term contracts that stabilize revenue streams. Clean-room contract packaging is poised to lead the field with an 11.86% CAGR as biologic pipelines expand and personalized therapies require agile batch sizes. CDMOs that combine fill-finish, sterile assembly, and post-sterilization labeling within modular isolators shorten technology transfer timelines for mid-tier companies.

Digital twins widen the productivity gap by simulating airflow, equipment cycles, and dwell times before physical validation. Service suites bundle lyophilization, visual inspection, and serialization, offering a one-stop path to global launch. Validation and testing add incremental revenue because sponsors outsource particulate count studies and accelerated aging on Tyvek overwraps. Secondary packaging remains vital for tamper-evidence and aggregation codes, albeit at lower gross margins, given the commoditization of carton erecting.[2]DuPont, “Tyvek with Renewable Attribution Launch,” dupont.com The Pharma and Medical Device Sterile Packaging Services Market thus gravitates toward integrated partners that can deliver cradle-to-gate compliance.

By Packaging Format: Innovation Drives Format Diversification

Pouches and bags commanded a 38.41% share in 2024, anchored by Tyvek-based overwraps that withstand EtO cycles while ensuring microbial barrier. They remain go-to choices for surgical kits, drug-device combinations, and bulk catheter sets. Blister and strip packs are projected to post the fastest 10.95% CAGR to 2030 as oral oncology and highly potent tablets migrate to unit-dose regimens that aid adherence. Tight pocket tolerances guard dose integrity, and integrated QR codes promote traceability.

Rigid trays support procedure-ready bundles, but they face substitution from form-fill-seal rolls where transportation weight savings are a concern. Bottles still house bulk liquids and suspensions, yet are migrating toward recyclable cyclic olefin copolymer resins to fulfill sustainability pledges. Wraps and rolls serve niche autoclave applications where porous, medical-grade paper is sufficient. Innovations such as Tyvek with Renewable Attribution underscore the stakeholder push for verified, lower-carbon footprints. Material science, therefore, remains central as the Pharma and Medical Device Sterile Packaging Services Market meets eco standards without compromising sterility.

By Sterilization Method: Technology Diversification Addresses Capacity Constraints

Ethylene oxide retained a 44.38% share in 2024, thanks to unmatched penetrability through complex device geometries and corrugated shippers. Residual gas aeration chambers and validated outgassing hold times preserve patient safety, though extended cycle turnarounds strain capacity. Electron-beam sterilization is forecasted to grow at an 11.39% CAGR, offering dry, low-temperature treatment with superior process control, making it suitable for temperature-sensitive biologics kits. On-site e-beam cells installed at packaging facilities cut transportation risk and cycle lead times.

Gamma irradiation remains the mainstream method for sterilizing single-use sets and bag assemblies, yet it struggles with the fragility of the Co-60 isotope supply chain. X-ray serves as a bridge technology that mimics gamma dose distribution while easing licensing constraints. Hydrogen peroxide vapor scales within isolators for small footprint operations. Ongoing ASTM studies comparing polymer oxidation under gamma, e-beam, and X-ray guide material selection. Diversification mitigates EtO chokepoints and widens choice for sponsors, reinforcing resilience across the Pharma and Medical Device Sterile Packaging Services Market.

By End-Use Industry: CDMO Growth Reshapes Market Dynamics

Pharmaceutical companies accounted for 41.16% of the 2024 volume, as both branded and generic players maintain a baseline need for sterile vials, syringes, and catheter kits. Tight launch windows and portfolio rationalization drive in-house capacity rationalization, yet legacy blockbusters still anchor demand. CDMOs/CMOs/CROs are expected to outpace the market at a 10.74% CAGR, mirroring broader outsourcing trends and private-equity interest. Integrated service models package formulation, aseptic fill-finish, and downstream kit-building, enticing innovators chasing speed-to-market.

Biotechnology startups often favor pay-per-batch structures, which help de-risk capital expenditures during clinical phases. Hospitals and specialty clinics are experimenting with point-of-care compounding, which requires pre-validated modular isolators and tamper-evident shipping totes. Medical device makers rely on kitting and just-in-time pouching before EtO runs, while diagnostics firms request low-bioburden tray loading for rapid antigen tests. Collectively, these shifts expand the addressable pool of the Pharma and Medical Device Sterile Packaging Services Market as service providers tailor vertical bundles to each user group.

Geography Analysis

North America accounted for 37.56% of global revenue in 2024, driven by the United States’ leadership in biologics R&D and stringent FDA oversight of container closure integrity. EtO utilization levels surpass 90%, and impending emission controls heighten the urgency for alternative capacity. Serialization deadlines under the Drug Supply Chain Security Act sustain demand for data-rich labeling and aggregation. Canada and Mexico contribute incremental growth through the production of generic injectables and the near-shoring of packaging runs.

Asia-Pacific is forecast to register an 11.31% CAGR, reflecting aggressive capacity additions and updated national GMP codes. China’s 2025 sterile medicine rules elevate cleanroom standards, while India’s revised Schedule M pushes local fillers to upgrade HVAC and monitoring. Southeast Asian members, including Malaysia, now require foreign GMP inspection certificates, which raises entry thresholds but harmonizes quality. Regional wage advantages attract multinational production; yet, sponsors still rely on Western CDMOs for first-in-human studies. Progressive harmonization with ICH guidelines is expected to sustain double-digit gains for the Pharma and Medical Device Sterile Packaging Services Market in the region.

Europe maintains steady momentum as the EU Falsified Medicines Directive standardizes serialization and tamper evidence. Germany and the United Kingdom innovate in sustainable materials, exemplified by the rollout of Tyvek with Renewable Attribution. PFAS restrictions shape resin choices, and the forthcoming Packaging and Packaging Waste Regulation tightens recycled-content mandates. Brexit continues to alter logistics flows, though mutual recognition of GMP inspections reduces friction. EtO emission rules mirror U.S. trends, prompting investments in X-ray and hydrogen peroxide lines, particularly in Ireland and Belgium. Together, these factors keep the continent a mature yet technologically progressive node within the Pharma and Medical Device Sterile Packaging Services Market.

Competitive Landscape

The Pharmaceutical and medical device sterile packaging services market exhibits moderate concentration, with the top five companies controlling an estimated 42% of the global revenue. Catalent, West Pharmaceutical Services, and Gerresheimer leverage scale and integrated offerings that span ready-to-fill glass, elastomer components, and terminal sterilization. Novo Holdings’ 2025 acquisition of Catalent illustrates investor appetite for end-to-end packaging depth. Gerresheimer’s USD 725 million Centor purchase adds U.S. amber vial capacity aligned with controlled-substance packaging.

Technology leadership differentiates incumbents: West deploys real-time container closure inspection using vision analytics, whereas SCHOTT Pharma pairs borosilicate cartridges with prevalidated nest-and-tub platforms. Electron-beam and X-ray pilots, offered by Steris and Sterigenics, diversify sterilization portfolios, reducing reliance on EtO. Sustainability gains traction, with Tekni-Plex integrating bio-based resins into blister webs and DuPont reducing Tyvek’s carbon footprint through mass-balance claims.[3]DuPont, “Tyvek with Renewable Attribution Launch,” dupont.com

Emerging challengers focus on niche biologic fills, flexible isolators, and digital batch-record platforms. Nelipak’s new Asia-Pacific site boosts pouch supply for device OEMs. Dec Group’s 2025 BAUSCH Germany acquisition unites powder handling and sterile fill centrifugation, expanding turnkey scope. Pricing pressure persists, but automation lifts margins via lower touch-time per unit. Strategic contracts increasingly bundle formulation, fill-finish, and sterile packaging under capped service agreements, locking in volume visibility for suppliers.

Pharma And Medical Device Sterile Packaging Services Industry Leaders

Catalent Pharma Solutions, Inc.

West Pharmaceutical Services, Inc.

Packaging Coordinators, Inc.

Sharp Services, LLC

Gerresheimer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SCHOTT Pharma completed a EUR 25 million expansion of ready-to-use cartridge capacity in Germany.

- April 2025: PCI Pharma Services allotted USD 365 million to enlarge its global sterile packaging network.

- May 2025: Gerresheimer finalized a USD 725 million acquisition of Centor, adding North American capacity.

- March 2025: Simtra BioPharma Solutions committed USD 250 million to expand sterile packaging infrastructure.

Global Pharma And Medical Device Sterile Packaging Services Market Report Scope

| Primary Packaging |

| Secondary Packaging |

| Clean-room Contract Packaging |

| Sterilization |

| Validation and Testing Services |

| Pouches and Bags |

| Trays and Clamshells |

| Blister and Strip Packs |

| Bottles and Containers |

| Wraps and Rolls |

| Ethylene Oxide (EtO) |

| Gamma Irradiation |

| Electron-Beam |

| Steam and Autoclave |

| Hydrogen Peroxide Vapor |

| Pharmaceutical Companies |

| Biotechnology Companies |

| CDMOs/CMOs/CROs |

| Hospitals and Specialty Clinics |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Primary Packaging | ||

| Secondary Packaging | |||

| Clean-room Contract Packaging | |||

| Sterilization | |||

| Validation and Testing Services | |||

| By Packaging Format | Pouches and Bags | ||

| Trays and Clamshells | |||

| Blister and Strip Packs | |||

| Bottles and Containers | |||

| Wraps and Rolls | |||

| By Sterilization Method | Ethylene Oxide (EtO) | ||

| Gamma Irradiation | |||

| Electron-Beam | |||

| Steam and Autoclave | |||

| Hydrogen Peroxide Vapor | |||

| By End-use Industry | Pharmaceutical Companies | ||

| Biotechnology Companies | |||

| CDMOs/CMOs/CROs | |||

| Hospitals and Specialty Clinics | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Pharma and Medical Device Sterile Packaging Services market in 2025?

It is valued at USD 9.28 billion, with expectations to reach USD 14.51 billion by 2030.

Which region grows fastest through 2030?

Asia-Pacific shows the highest forecast CAGR at 11.31%, spurred by new GMP rules in China and India.

What segment records the quickest expansion?

Clean-room contract packaging services are projected to grow at an 11.86% CAGR, reflecting mid-tier pharmaceutical outsourcing.

Why is ethylene oxide still dominant despite scrutiny?

EtO can sterilize complex, moisture-sensitive devices inside corrugated cartons, a capability still unmatched at scale.

How is automation shaping sterile packaging?

Industry 4.0 tools, such as predictive maintenance and digital twins, enhance throughput and data integrity while minimizing human intervention.

How do new serialization rules affect costs?

Compliance can add EUR 600,000 per packaging line in capital and about 4.1 cents per pack in ongoing expenses, nudging companies toward CDMOs.

Page last updated on: