Cosentyx Drug Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.72 Billion |

| Market Size (2030) | USD 9.51 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

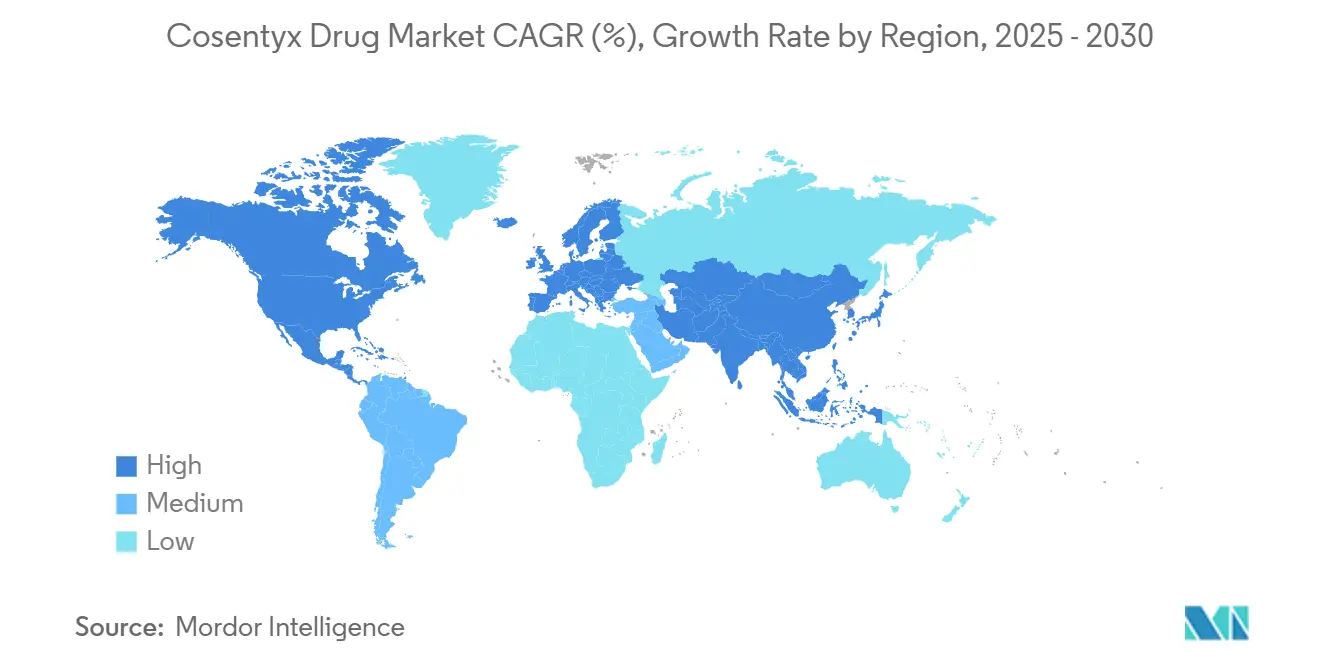

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosentyx Drug Market Analysis by Mordor Intelligence

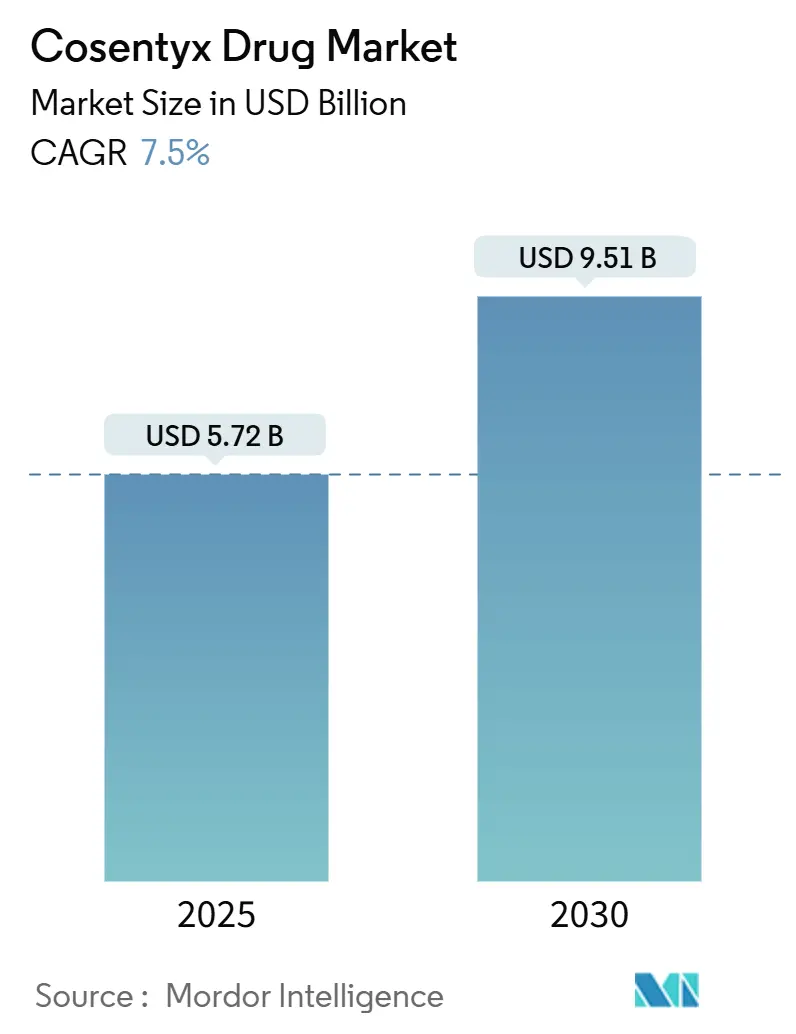

The cosentyx drug market size stands at USD 5.72 billion in 2025 and is forecast to reach USD 9.5 billion by 2030, translating to a 7.5% CAGR over the outlook period. Demand accelerates as the therapy’s label broadens beyond plaque psoriasis, supported by 2024 approvals for hidradenitis suppurativa and an intravenous (IV) formulation that collectively unlock new revenue pools. First-in-class positioning within the interleukin-17 (IL-17) category underpins sustained pricing power, even as biosimilar programs progress. Geographic expansion remains a core growth lever: North America retains the most significant revenue base, Asia Pacific logs the fastest uptake, and Europe delivers stable prescriptions under mature reimbursement frameworks. Strategic manufacturing investments—including a USD 256 million antibody site in Singapore—reinforce supply resilience and localize production for emerging markets.

Key Report Takeaways

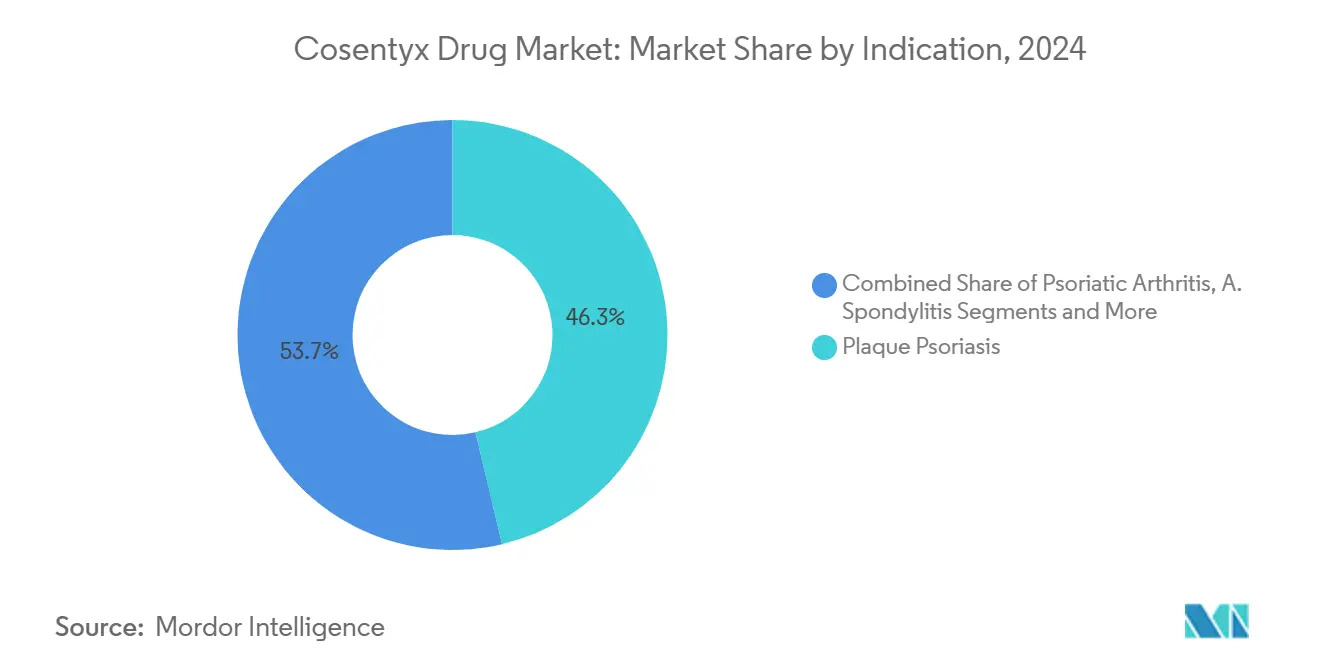

- By indication, plaque psoriasis held a 46.3% share of the Cosentyx drug market in 2024, while non-radiographic axial spondyloarthritis is advancing at a 7.8% CAGR through 2030.

- By distribution channel, specialty pharmacies captured 55.7% of the Cosentyx drug market share in 2024; online pharmacies record the highest projected CAGR at 11.4% to 2030.

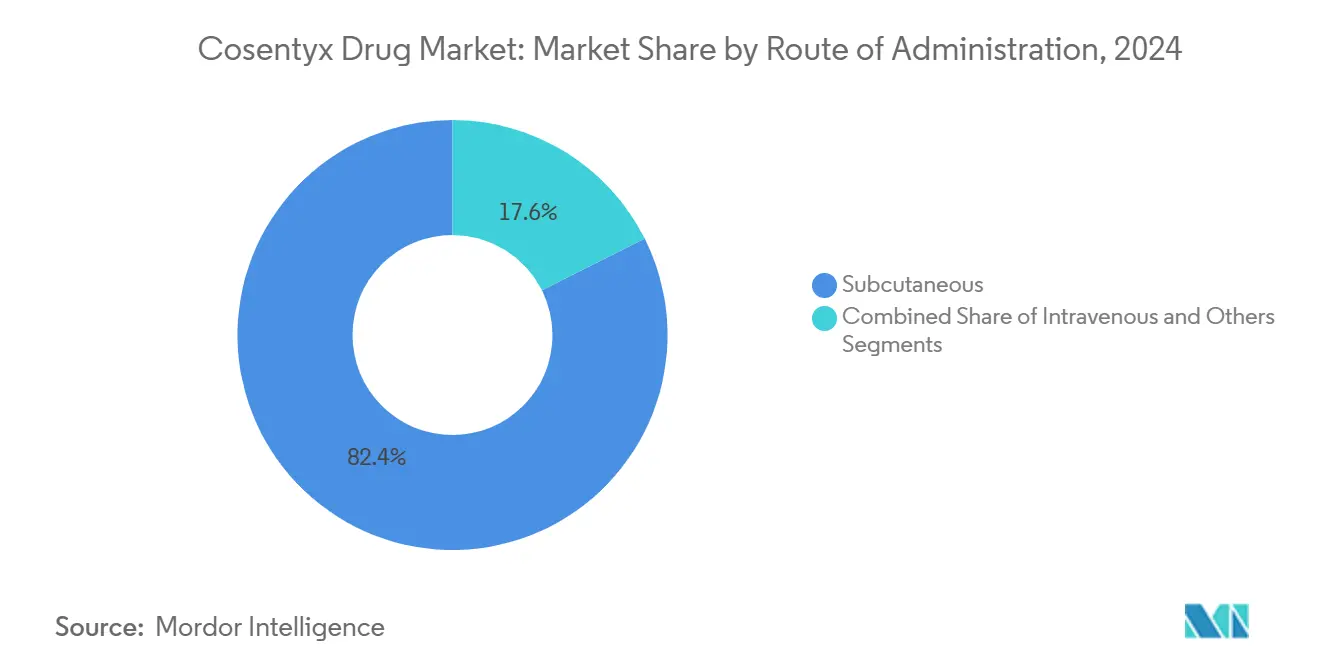

- By route of administration, subcutaneous delivery accounted for 82.4% of the Cosentyx drug market size in 2024 and is expanding at a 9.9% CAGR over the forecast window.

- By geography, North America commanded 46.9% revenue share in 2024, whereas Asia Pacific is set to climb at an 8.8% CAGR through 2030.

Global Cosentyx Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding label approvals for axial spondyloarthritis | +1.20% | Global, early gains in North America & EU | Medium term (2-4 years) |

| Rising biologic adoption in moderate-to-severe plaque psoriasis | +1.80% | Global | Long term (≥ 4 years) |

| Shift to self-administered pens in specialty pharmacies | +0.90% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Increased reimbursement coverage across OECD markets | +1.10% | OECD countries | Medium term (2-4 years) |

| Accelerated uptake in China’s volume-based procurement channel | +0.70% | China, with regional APAC influence | Short term (≤ 2 years) |

| Dermatology tele-prescribing models boosting refills | +0.60% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Label Approvals for Axial Spondyloarthritis

FDA endorsement of the IV formulation for non-radiographic axial spondyloarthritis (nr-axSpA) in 2024 shortened diagnostic-to-treatment timelines that historically averaged almost a decade. Roughly 1.4 million eligible patients now have a first-line option that can slow structural progression when introduced early. Guidelines from global rheumatology societies increasingly recommend aggressive intervention, giving Cosentyx an edge as physicians pivot away from conventional disease-modifying antirheumatic drugs. Novartis projects USD 500–700 million in incremental peak revenue from this single label extension, anchored by Phase 3 data that outperformed standard care. The move also diversifies revenue ahead of biosimilar entry, strengthening lifecycle management.

Rising Biologic Adoption in Moderate-To-Severe Plaque Psoriasis

Biologics have displaced dated systemic therapies as payers recognize the long-term economic benefits of rapid, durable skin clearance. Cosentyx achieves Psoriasis Area and Severity Index (PASI) 90 rates above 70% within 16 weeks, a benchmark that resonates with dermatologists and patients alike. Insurers signal support: U.S. specialty-drug spending climbed 14% in 2024, mirroring broader coverage gains in OECD markets. As prevalence rises in emerging economies, earlier diagnoses increase the treatable population. Practice consolidation further accelerates uptake because large dermatology groups possess dedicated infusion suites and adherence programs that favor established brands.

Shift To Self-Administered Pens in Specialty Pharmacies

Citrate-free pens lessen injection pain and lift adherence by roughly 15–20% versus syringes, addressing a common barrier to persistence. Specialty pharmacies leverage training modules and telehealth check-ins to simplify onboarding and improve refill consistency. Health-system cost savings accrue as patients self-inject at home, reducing clinic visits. Digital integration reminder apps, adverse-event trackers, and secure messaging further embed patients within branded ecosystems. The convenience factor supports pay-for-performance contracts that reward demonstrable adherence.

Increased Reimbursement Coverage Across OECD Markets

Policy shifts cement access. The 2025 Medicare Part D redesign caps annual out-of-pocket costs at USD 2,000, dramatically easing financial barriers to therapies such as Cosentyx. Parallel decisions by Germany’s G-BA and France’s HAS expand coverage earlier in the disease course, reflecting favorable health-economic models that tally downstream savings. Real-world evidence shows biologics cut hospitalizations and comorbidity costs, strengthening the case for widespread reimbursement. As formulary hurdles drop, initiation rates and persistence both rise, enlarging the addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Loss-of-exclusivity pressure from IL-17 biosimilars | –1.4% | Global, initial impact in EU, then U.S. | Medium term (2-4 years) |

| Stringent long-term safety monitoring requirements | –0.8% | Global; stricter in EU & North America | Long term (≥ 4 years) |

| Pay-for-performance contracts capping net price growth | –0.9% | North America & EU | Medium term (2-4 years) |

| Needle-phobia limiting persistence in adolescent segment | –0.5% | Global, stronger in high-income markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Loss-Of-Exclusivity Pressure From IL-17 Biosimilars

Celltrion’s CT-P55 is now in global Phase 3, positioning for launch once U.S. patents lapse in January 2029. Europe faces an even earlier cliff in 2030, historically a launchpad for biosimilar pricing erosion. Although IL-17 inhibitors are bio-complex, Humira’s erosion to 77% share within 18 months of biosimilar entry illustrates the commercial stakes. Novartis counters with lifecycle plays: device upgrades, new indications, and payer contracting, but margin compression post-2029 remains inevitable.

Stringent Long-Term Safety Monitoring Requirements

Regulators demand extensive post-marketing surveillance, including registry participation and periodic cardiovascular malignancy assessments.[1]FDA/CDER, “Label for Cosentyx,” accessdata.fda.gov Compliance hikes administrative costs and may deter lower-resource clinics from prescribing. Emerging markets often lack robust pharmacovigilance infrastructure, complicating rollout. As the patient pool widens to earlier-stage disease, risk–benefit analyses become more nuanced, extending approval timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Diversifying Beyond Psoriasis Leadership

Plaque psoriasis generated 46.3% of the Cosentyx drug market size in 2024. Non-radiographic axial spondyloarthritis, while smaller today, is growing the fastest at 7.8% CAGR, helped by IV uptake that enables rheumatologists to maintain in-office infusion revenue. Psoriatic arthritis remains a stable driver as enhanced screening captures comorbid patients earlier. Ankylosing spondylitis prescriptions benefit from long-term efficacy data that validate spinal symptom control. Hidradenitis suppurativa, approved in 2024, already commands more than 60% new-start share, highlighting the brand’s first-mover advantage in dermatology niches. The evolving mix cushions revenue against biosimilar entrants that often target legacy psoriasis volumes first. Forward-looking trials in giant cell arteritis and polymyalgia rheumatica could unlock multi-billion-dollar upside, reinforcing dependency diversification.

Label expansion supports a defensive IP strategy, extending protection via new patents around indications and dosing. Rheumatology societies’ pivot to early biologic intervention brings younger, longer-duration patients into the funnel, enlarging lifetime value. Real-world visibility of radiographic progression delay in axial disease further strengthens prescribing confidence. Collectively, these trends keep the Cosentyx drug market on an upward trajectory despite competitive headwinds.

By Distribution Channel: Specialty Dominance, Online Momentum

Specialty outlets managed 55.7% of the Cosentyx drug market share in 2024. Integrated patient-management platforms drive high refill rates and data-rich care coordination prized by payers. Online pharmacies, while just 6% of 2024 revenue, are scaling at 11.4% CAGR as Medicare redesign caps out-of-pocket spending. Hospital pharmacies maintain relevance for IV initiation but face margin compression as alternate-site infusions spread. Retail chains struggle under cold-chain handling burdens and rising payer steerage to lower-spread channels.

Vertically integrated pharmacy-benefit-manager ecosystems such as CVS Specialty and Accredo employ predictive analytics to flag adherence risk and trigger interventions. These models demonstrate 8–10 percentage-point improvements in persistence, a metric closely watched in value-based contracts. Direct-to-patient delivery further reduces abandonment attributable to travel or scheduling barriers, boosting total prescription volume within the Cosentyx drug industry.

By Route of Administration: Subcutaneous Pen Preference Prevails

Subcutaneous injections represent 82.4% of revenue and are the fastest-expanding part of the Cosentyx drug market at 9.9% CAGR. Citrate-free pens minimize discomfort, and one-button activation simplifies self-administration, supporting persistence. IV share grew modestly after 2024 FDA clearance across major rheumatology indications, aided by a permanent J-code that clarifies reimbursement. Physicians choose IV for patients with severe disease or prior injection-site reactions, generating predictable infusion-center utilization.

Device optimization remains a core differentiator as biosimilars typically launch in syringe form first. Embedded near-field-communication chips that log injection time and temperature are under pilot, promising payer-verifiable adherence. These upgrades anchor brand loyalty as biosimilar options multiply closer to patent expiry.

Geography Analysis

North America led with USD 2.69 billion in 2024, translating to a 46.9% Cosentyx drug market share. Medicare Part D reform, lowering annual caps, fuels prescription growth, while private insurers expand first-line biologic coverage for moderate psoriasis. Physician familiarity with IL-17 mechanisms and robust patient-support programs sustains high initiation and refill rates.[2]Centers for Medicare & Medicaid Services, “Final CY 2025 Part D Redesign Program Instructions,” cms.govCanada’s provincial plans widened eligibility in late 2024, boosting volumes particularly in Ontario and Québec.

Europe presents a mature yet resilient landscape where centralized health-technology assessments anchor uniform access. Germany and France drive continental revenue through early-adopter specialist clinics and favorable reimbursement dossiers. Post-Brexit, the U.K. Medicines and Healthcare products Regulatory Agency streamlined its own fast-track evaluations, ensuring minimal launch delays. Southern Europe shows accelerating growth as budget expansion earmarks additional biologic spending, with Italy’s Agenzia Italiana del Farmaco approving broader criteria for moderate disease severity.

Asia Pacific is the growth pacesetter, posting an 8.8% CAGR through 2030 as healthcare infrastructure modernizes. China rises fastest: Novartis’s USD 100 million local facility trims lead-times and wins government goodwill. Japan continues as the most penetrated APAC market, aided by universal insurance and specialist density. India’s urban hospitals adopt secukinumab more quickly after inclusion in select private insurer formularies. Singapore’s role as a regional logistics hub expands following the USD 256 million antibody plant, securing supply for Southeast Asian demand spikes.

Competitive Landscape

The Cosentyx drug market sits in a moderately concentrated arena where first-in-class status clashes with next-generation rivalry. UCB’s BIMZELX, the inaugural dual IL-17A/IL-17F inhibitor, differentiates on mechanism and has already launched across psoriatic arthritis and axial spondyloarthritis segments. AbbVie’s Skyrizi pivot illustrates successful lifecycle engineering—leveraging entrenched rheumatology relationships to recover share lost by Humira.[3]The Center for Biosimilars, “Skyrizi Overtakes Humira: ‘Product Hopping’ Leaves Biosimilar Market in Limbo,” centerforbiosimilars.comAmgen and Eli Lilly monitor the field with early-phase pipeline assets targeting IL-17C or IL-23/IL-17 cross-talk pathways.

Defensive strategies dominate. Novartis amplifies patient-engagement platforms, pairs device innovation with adherence analytics, and co-promotes with dermatology societies to lock in prescriber loyalty. Biosimilar threat timing shapes contracting posture: payer discounts deepen from 2027 onward as purchasers anticipate Celltrion's entry. Real-world evidence accrual remains pivotal as value-based contracts weigh long-term clinical outcomes; Cosentyx’s five-year sustained efficacy dataset arms Novartis with credible negotiation leverage.

Consolidation underlines supply-chain security: the Singapore and planned U.S. biologics campuses ensure regional redundancy. Strategic collaborations with Chinese biotech firms shorten regulatory cycles and localize formulation tweaks, strengthening competitive insulation in high-growth territories. As patents near expiration, originators lean on indication breadth and premium service bundles to justify pricing while nurturing brand equity that biosimilars struggle to emulate.

Cosentyx Drug Industry Leaders

Novartis International AG

Mitsubishi Tanabe Pharma Corp.

Sun Pharmaceutical Industries Ltd.

Celltrion Healthcare Co., Ltd.

Bio-Thera Solutions Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The late-stage GCAptAIN study missed its primary endpoint in giant cell arteritis, curbing near-term prospects for expanding Cosentyx into this inflammatory segment.

- March 2025: UCB unveiled two-year data demonstrating durable efficacy and a consistent safety profile for BIMZELX in hidradenitis suppurativa, heightening competitive pressure on Cosentyx in this newest market space.

- January 2024: The FDA cleared Cosentyx’s IV formulation for major rheumatology indications.

Global Cosentyx Drug Market Report Scope

| Plaque Psoriasis |

| Psoriatic Arthritis |

| Ankylosing Spondylitis |

| Non-Radiographic Axial Spondyloarthritis |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| Clinics & Physician Offices |

| Subcutaneous |

| Intravenous |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Plaque Psoriasis | |

| Psoriatic Arthritis | ||

| Ankylosing Spondylitis | ||

| Non-Radiographic Axial Spondyloarthritis | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Specialty Pharmacies | ||

| Online Pharmacies | ||

| Clinics & Physician Offices | ||

| By Route of Administration | Subcutaneous | |

| Intravenous | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global Cosentyx drug market in 2025?

It is valued at USD 5.72 billion and is projected to grow at a 7.5% CAGR through 2030.

Which indication supplies most Cosentyx revenue today?

Plaque psoriasis remains the largest contributor, holding 46.3% of 2024 revenue.

What drives the fastest regional growth for Cosentyx?

Asia Pacific leads with an 8.8% CAGR, buoyed by Chinese manufacturing investments and expanding reimbursement.

When might biosimilar competition arrive in the United States?

The key patent expires in January 2029, allowing the first IL-17 biosimilars to launch afterward.

Why are specialty pharmacies central to Cosentyx distribution?

They manage cold-chain handling, patient training, and adherence programs that enhance refill rates and meet payer requirements.

How is Novartis defending Cosentyx against upcoming biosimilars?

Strategies include new indications, device upgrades, patient-support platforms, and multi-region manufacturing expansions.

Page last updated on: