Physician Dispensed Cosmeceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

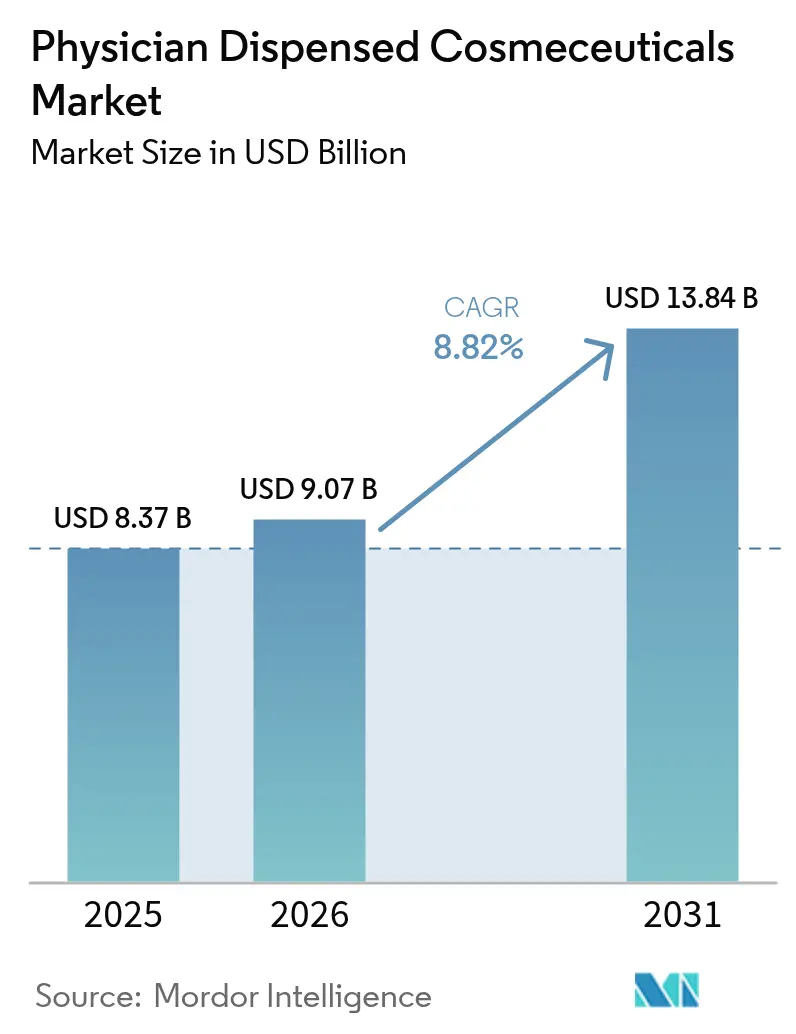

| Market Size (2026) | USD 9.07 Billion |

| Market Size (2031) | USD 13.84 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

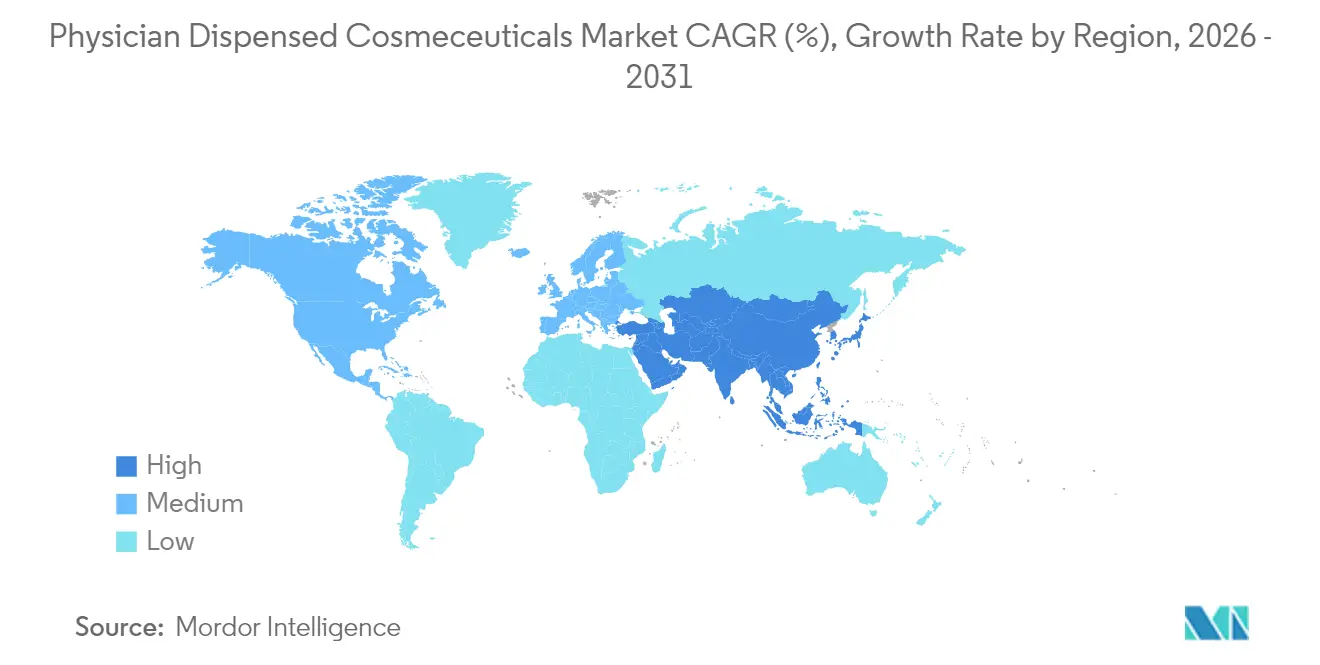

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Physician Dispensed Cosmeceuticals Market Analysis by Mordor Intelligence

The Physician Dispensed Cosmeceuticals Market size is expected to grow from USD 8.37 billion in 2025 to USD 9.07 billion in 2026 and is forecast to reach USD 13.84 billion by 2031 at 8.82% CAGR over 2026-2031.

Elevated demand for clinically validated skincare, the rapid rise of tele-dermatology platforms, and clinic-based premiumization are reinforcing the channel’s pricing power. Dermatologists, aesthetic physicians, and medical spas are capitalizing on integrated service-and-product models that monetize consultation time and dispense protocols during the same visit. North American practices are leveraging AI-powered diagnostic tools to convert more consultations into purchases, while Asia Pacific clinics are scaling rapidly as disposable incomes climb. Competitive dynamics are intensifying as pharmaceutical companies, prestige beauty houses, and digital health start-ups converge on the channel.

Key Report Takeaways

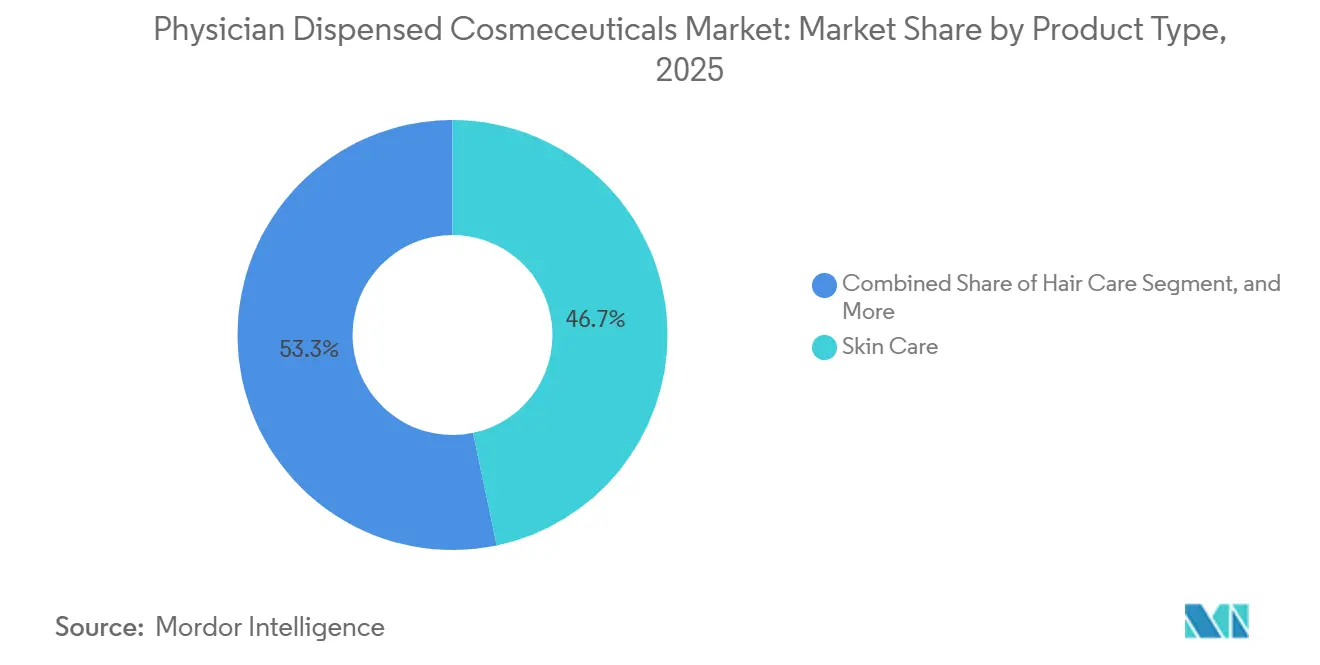

- By product type, skin care led with 46.71% of physician dispensed cosmeceuticals market share in 2025 and hair care is forecast to grow at a 9.06% CAGR through 2031.

- By skin concern, anti-aging accounted for a 37.29% share of the physician dispensed cosmeceuticals market size in 2025, while acne and seborrheic conditions are advancing at a 10.63% CAGR to 2031.

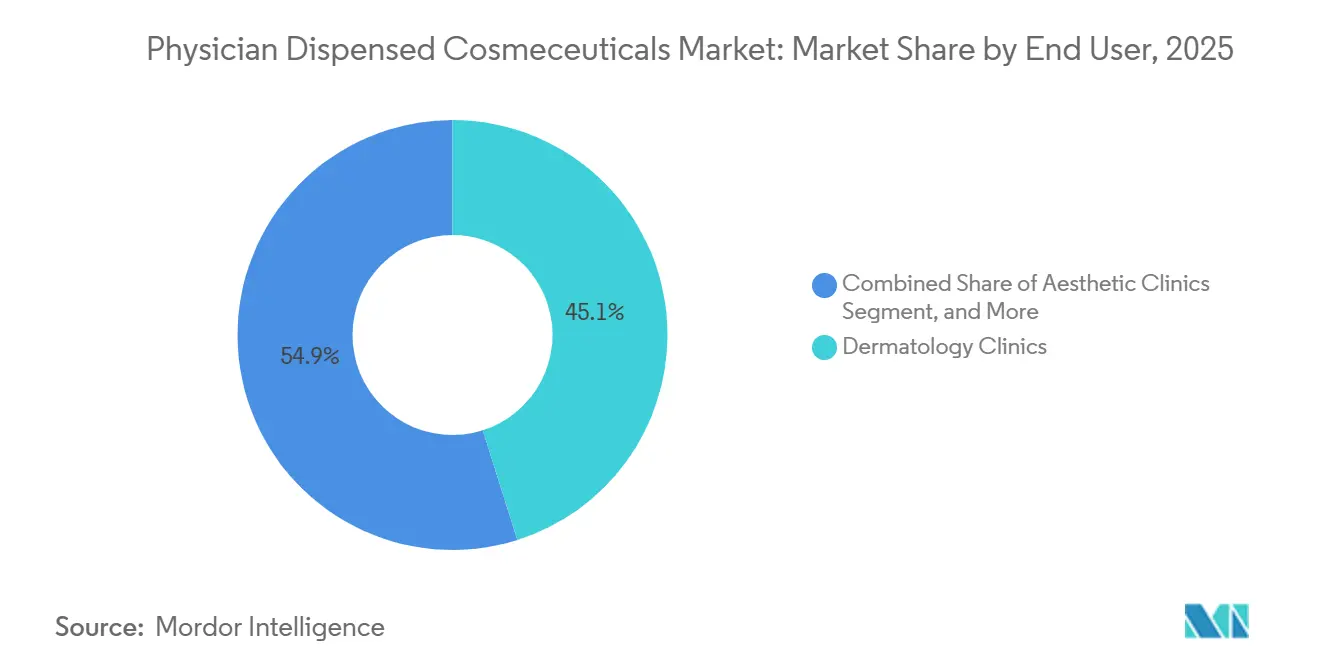

- By end user, dermatology clinics held 45.12% of the physician dispensed cosmeceuticals market share in 2025; aesthetic clinics record the highest projected CAGR at 11.18% through 2031.

- By geography, North America commanded 39.91% revenue share in 2025 and Asia Pacific is projected to achieve a 9.63% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Physician Dispensed Cosmeceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population fueling demand for anti-aging physician-grade skincare | +1.8% | Global, peak in North America, Western Europe, Japan | Long term (≥ 4 years) |

| Expansion of dermatology and aesthetic clinics worldwide | +1.5% | Asia Pacific core, spill-over to Middle East & Latin America | Medium term (2-4 years) |

| Rising disposable incomes and premiumization in emerging economies | +1.2% | Asia Pacific, Latin America | Medium term (2-4 years) |

| Regulatory preference for clinically validated formulations increases consumer trust | +0.9% | North America & EU | Long term (≥ 4 years) |

| Tele-dermatology platforms bundling e-prescriptions with in-office refills | +0.8% | North America, expanding to EU & urban Asia Pacific | Short term (≤ 2 years) |

| AI-powered diagnostic devices in clinics boosting rates of cosmeceuticals | +0.7% | North America, early EU & select Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population Fueling Demand for Anti-Aging Physician-Grade Skincare

By 2030, the global citizen population aged 60 and above will reach 21.5%, creating a sizeable cohort willing to pay for clinically substantiated anti-aging interventions.[1]United Nations Department of Economic and Social Affairs, “World Population Ageing 2020 Highlights,” un.org Japan’s “doctor’s cosmetics” segment grew 11.8% year-on-year to JPY 121.2 billion in fiscal 2022, underscoring demand for evidence-based formulations targeting dermal atrophy. Peptide technologies that up-regulate collagen synthesis feature prominently in physician portfolios; peer-reviewed studies confirm palmitoyl pentapeptide-4’s stimulatory effect on extracellular matrix proteins. Galderma expanded its Alastin range into China in September 2025, pairing TriHex peptide science with dermatologist endorsements to position the line as a surgical alternative. Manufacturers are prioritizing peptide synthesis, growth-factor stabilization, and novel delivery systems that justify premium price points within the physician-dispensed cosmeceuticals market.

Expansion of Dermatology & Aesthetic Clinics Worldwide

The American Med Spa Association counted 7,420 U.S. medical spas in 2024, 28% more than in 2019, and projects USD 47.7 billion in revenue by 2030.[2]American Med Spa Association, “Medical Spa Industry Statistics 2025,” americanmedspa.org Merz Aesthetics Korea expects annual sales of KRW 300 billion, with 55% growth from mid-2024 to mid-2025, reflecting clinic build-outs in Seoul and secondary cities. India and China are easing clinic licensing requirements, while Brazil’s Eurofarma acquired a 60% stake in Dermage in March 2025 to capture local physician demand. As clinics multiply, procedure-adjacent skincare sales, particularly for post-laser barrier repair, generate recurring revenue, reinforcing the physician-dispensed cosmeceuticals market trajectory.

Rising Disposable Incomes and Premiumization in Emerging Economies

L’Oréal’s dermocosmetics division grew 16.4% in China in 2024, confirming a consumer pivot toward clinical efficacy over mass prestige.[3]L’Oréal, “2024 Universal Registration Document,” loreal-finance.com Brazil’s dermocosmetics revenue reached BRL 6.89 billion in 2024, buoyed by premium clinic-only lines in São Paulo and Rio de Janeiro. Southeast Asian medical tourism hubs, led by Bangkok and Singapore, expose regional consumers to physician regimens, accelerating premiumization. The outcome is shrinking price elasticity, enabling 2-3 times retail pricing inside the physician-dispensed cosmeceuticals market.

Tele-Dermatology Platforms Bundling E-Prescriptions with In-Office Refills

Hims & Hers reported Q3 2024 revenue of USD 401.6 million, up 77%, by prescribing finasteride and tretinoin online and shipping directly to patients. Curology and Amazon One Medical replicate the model, collapsing physical consult barriers. Galderma’s digital education portals help physicians integrate e-prescriptions with in-clinic refills, sustaining lifetime value. Maintenance regimens such as retinoids and peptide serums benefit most because automated replenishment lowers compliance friction across the physician-dispensed cosmeceuticals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product and consultation cost limiting access in lower-income segments | -0.6% | Global, acute in South Asia & rural Latin America | Medium term (2-4 years) |

| Potent OTC dermocosmetics diluting physician channel share | -0.5% | North America & Western Europe | Short term (≤ 2 years) |

| Shortage of trained aesthetic dermatologists in high-growth regions | -0.4% | Asia Pacific & MEA | Long term (≥ 4 years) |

| Cold-chain fragility for biologic actives | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Product and Consultation Cost Limiting Access in Lower-Income Segments

Physician-grade UV recovery SPF retails near USD 50, while an urban India clinic visit often exceeds USD 60, straining households with a monthly income below USD 500. Limited insurance coverage compounds affordability gaps, keeping penetration low in rural Brazil and Southeast Asia. Some manufacturers introduce tiered lines premium in clinics and lighter-strength variants in pharmacies to serve both price points, yet the physician-dispensed cosmeceuticals market remains heavily skewed to affluent consumers.

Potent OTC Dermocosmetics Diluting Physician Channel Share

La Roche-Posay and CeraVe stock drugstores with niacinamide and ceramide formulas approaching clinic-grade concentrations. L’Oréal’s dermocosmetics unit outperformed corporate averages in 2024, proving retail products can convey scientific credibility without prescriptions. Dermatologists now emphasize higher-dose actives, randomized trials, and post-procedure niches to preserve differentiation inside the physician dispensed cosmeceuticals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hair Care Outpaces Skin Care

Skin care accounted for 46.71% of 2025 revenue, anchored by retinoid serums and post-procedure barrier repair lines. Hair care, however, is projected to lead growth at a 9.06% CAGR to 2031. The physician-dispensed cosmeceuticals market for hair care is poised to expand as compounded topical finasteride reduces systemic exposure and pairs well with telehealth.

Direct-to-consumer platforms drive conversions by reducing stigma and automatically shipping refills. Meanwhile, skin care is saturated in North America, with differentiation shifting toward procedure-specific applications. Eye care, though smaller, commands high average selling prices because bimatoprost remains prescription-only. Injectable neurotoxins and fillers, while not take-home products, stimulate in-office recovery kit sales, reinforcing cross-selling opportunities in the physician-dispensed cosmeceuticals market.

By Skin Concern: Acne & Seborrheic Conditions Surge

Anti-aging retained 37.29% share in 2025, yet acne & seborrheic conditions are forecast to grow 10.63% annually to 2031. Rising tele-acne consults reduce patient hesitation, and lower-dose isotretinoin protocols improve adherence. The physician-dispensed cosmeceuticals market share for anti-aging products remains robust but is maturing, while microbiome-driven acne products promise fresh differentiation. Hyperpigmentation regimens are thriving in Asia Pacific, though regulatory limits on hydroquinone constrain some SKUs.

By End User: Aesthetic Clinics Accelerate

Dermatology clinics accounted for 45.12% of 2025 revenue, but aesthetic clinics will grow fastest at a 11.18% CAGR by bundling injectables and post-treatment products. High patient turnover and nurse-practitioner staffing models compress consultation costs, widening market reach. Hospital channels remain tied to post-surgical recovery, whereas plastic surgery centers operate at lower volumes yet command premium spend. Regulatory debates over the non-physician scope of practice will influence future channel mix but are unlikely to derail the momentum of the physician-dispensed cosmeceuticals market.

Geography Analysis

North America accounted for 39.91% of 2025 sales, thanks to a dense dermatologist network and a mature medical spa ecosystem. Asia Pacific, nevertheless, will post a 9.63% CAGR through 2031. South Korea’s aesthetic boom, China’s regulatory streamlining, and India’s expansion of tier-2 cities underpin this surge. Japan’s doctor cosmetics market climbed 11.8% year on year, and Chinese tier-1 clinics are integrating cosmeceutical counters into treatment flow. Europe remains steady but slower as maintenance regimens overtake corrective therapies. GCC countries drive Middle East demand through medical tourism, while Brazil dominates South American volumes.

Competitive Landscape

Moderate fragmentation characterizes the physician-dispensed cosmeceuticals industry. Galderma’s March 2024 IPO funds its injectables-to-skincare vertical play and supported Alastin’s September 2025 China launch. L’Oréal’s August 2024 10% stake in Galderma forges synergies between pharmaceutical rigor and beauty marketing. Merz Pharma allocates 18% of topline to R&D; July 2024 FDA approval for XEOMIN’s three-area treatment broadens its neurotoxin moat. Eurofarma’s Dermage acquisition secures a Latin American footprint, while AI diagnostics, such as DermaSensor, convert clinical insights into real-time product recommendations. Cold-chain innovation is also advancing; a December 2024 paper in Nature Communications on perfluorocarbon carriers suggests a route to room-temperature peptide stability.

Digital disrupters intensify rivalry. Hims & Hers scales asynchronous prescriptions and direct fulfillment to bypass clinics, capturing both service and product margins. Curology follows a similar script, and Amazon’s One Medical adds integrated primary-derm care to the mix. Established manufacturers respond with clinical trials, physician education, and procedure-adjacent product lines to retain premium positioning within the physician-dispensed cosmeceuticals market.

Physician Dispensed Cosmeceuticals Industry Leaders

Merz Pharma

Obagi Cosmeceuticals LLC

SkinCeuticals International

Abbvie Inc (Allergan PLC)

Innovative Skincare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allergan Aesthetics showcased the AA Signature program and 11 new research posters at AMWC 2025, reinforcing data-driven treatment planning for physician-supervised protocols.

- January 2025: L’Oréal Groupe introduced portable Cell BioPrint at CES 2025 to deliver five-minute proteomic skin analyses in clinics

- August 2024: Kenvue launched Neutrogena Collagen Bank with micro-peptide technology for deeper collagen support, marketed exclusively through U.S. dermatology offices

Global Physician Dispensed Cosmeceuticals Market Report Scope

As per the scope of the report, physician-dispensed cosmeceuticals refer to products that are only accessible through a medically directed business and are geared toward creating actual biological actions on the skin below the stratum corneum. Many physicians whose practices or specialties involve skin health choose to dispense these cosmeceuticals or have them specially compounded to offer heightened results to their patients and to enhance their results with other treatments.

The Physician Dispensed Cosmeceuticals Market Report is Segmented by Product Type (Skin Care, Hair Care, Eye Care, Injectable/Parenteral), Skin Concern (Anti-Aging, Hyperpigmentation & Brightening, Acne & Seborrheic Conditions, Hair Loss, Post-Procedure Recovery), End User (Hospital, Dermatology Clinics, Aesthetic Clinics, Plastic Surgery Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Skin Care |

| Hair Care |

| Eye Care |

| Injectable / Parenteral |

| Anti-Aging |

| Hyper-pigmentation & Brightening |

| Acne & Seborrheic Conditions |

| Hair Loss |

| Post-Procedure Recovery |

| Hospital |

| Dermatology Clinics |

| Aesthetic Clinics |

| Plastic Surgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Skin Care | |

| Hair Care | ||

| Eye Care | ||

| Injectable / Parenteral | ||

| By Skin Concern/ Application | Anti-Aging | |

| Hyper-pigmentation & Brightening | ||

| Acne & Seborrheic Conditions | ||

| Hair Loss | ||

| Post-Procedure Recovery | ||

| By End User | Hospital | |

| Dermatology Clinics | ||

| Aesthetic Clinics | ||

| Plastic Surgery Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the physician dispensed cosmeceuticals market be by 2031?

Revenue is forecast to reach USD 13.84 billion by 2031 at an 8.82% CAGR.

Which region is growing fastest for physician-guided cosmeceutical sales?

Asia Pacific is projected to expand at 9.63% CAGR through 2031 on rising clinic density and income growth.

Which product type is gaining momentum within clinic channels?

Hair care shows the strongest outlook with a 9.06% CAGR, fueled by topical finasteride and minoxidil formulations.

Which skin concern segment will outpace others through 2031?

Acne and seborrheic condition treatments are expected to grow 10.63% annually, the highest among all concerns.

What is driving physician clinics to adopt tele-dermatology commerce models?

Bundling e-prescriptions with automated refills boosts lifetime patient value and reduces friction in follow-up purchases.

Page last updated on: