Incretin-based Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

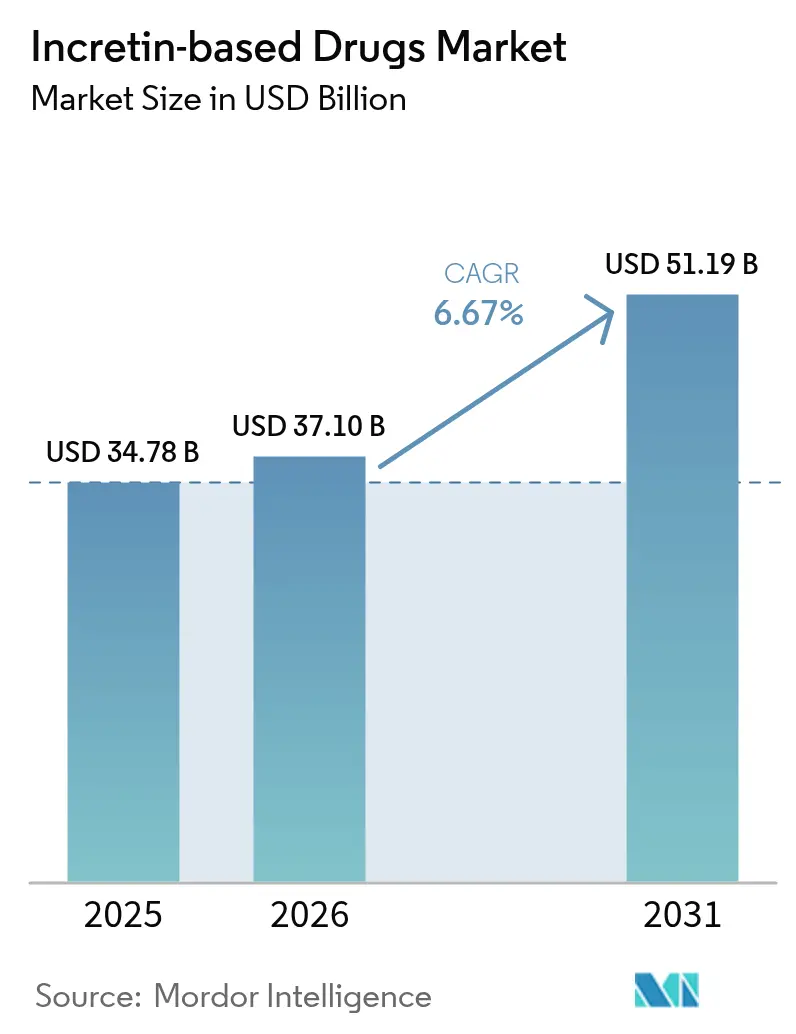

| Market Size (2026) | USD 37.1 Billion |

| Market Size (2031) | USD 51.19 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

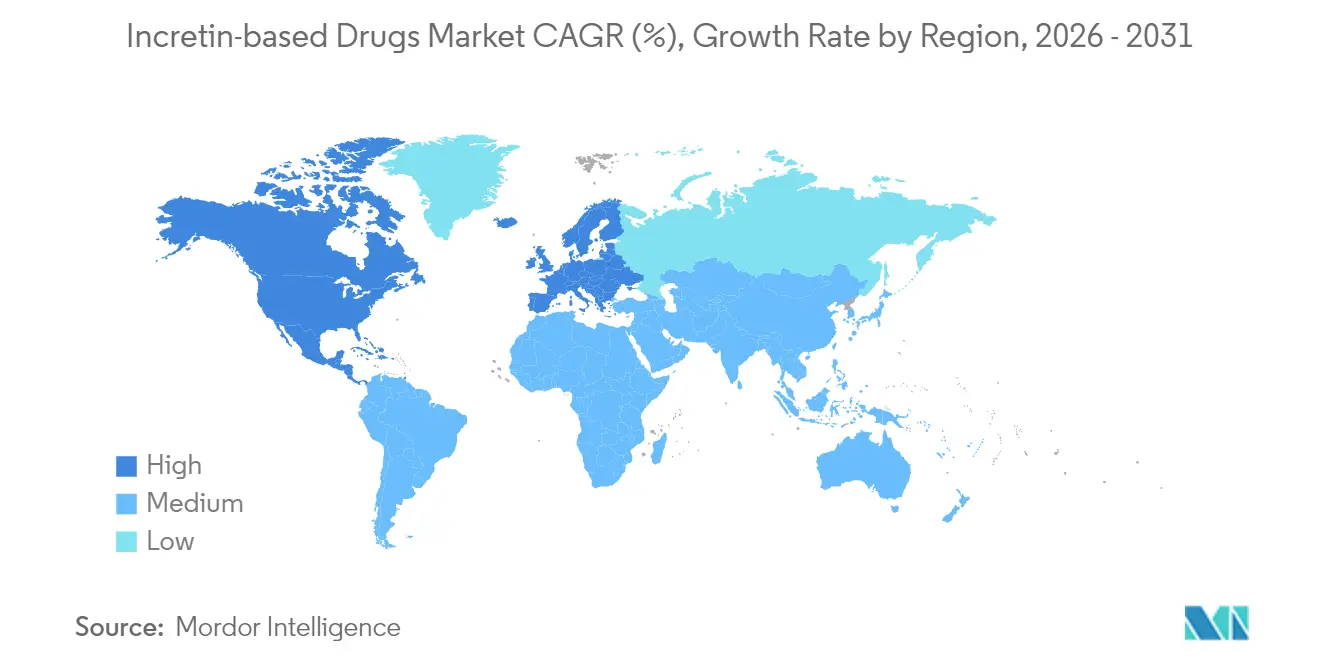

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Incretin-based Drugs Market Analysis by Mordor Intelligence

The incretin based drugs market size is expected to grow from USD 34.78 billion in 2025 to USD 37.10 billion in 2026 and is forecast to reach USD 51.19 billion by 2031 at 6.67% CAGR over 2026-2031. Current growth is fueled by swift label expansions into obesity and cardiometabolic indications, rapid uptake of dual-mechanism agents, and record-high manufacturing investments that seek to relieve the supply bottlenecks that constrained sales in 2024. Converging clinical evidence showing 20%–25% weight-loss efficacy has broadened physician support and accelerated guideline inclusion for earlier intervention, while oral formulations remove adherence barriers linked to injections. Parallel API scale-up in India and China is lowering production costs, enabling tiered pricing strategies for price-sensitive regions. The incretin based drugs market now competes directly with lipid-lowering therapies for cardiometabolic disease management, signaling a medium-term shift toward combination prevention regimens.

Key Report Takeaways

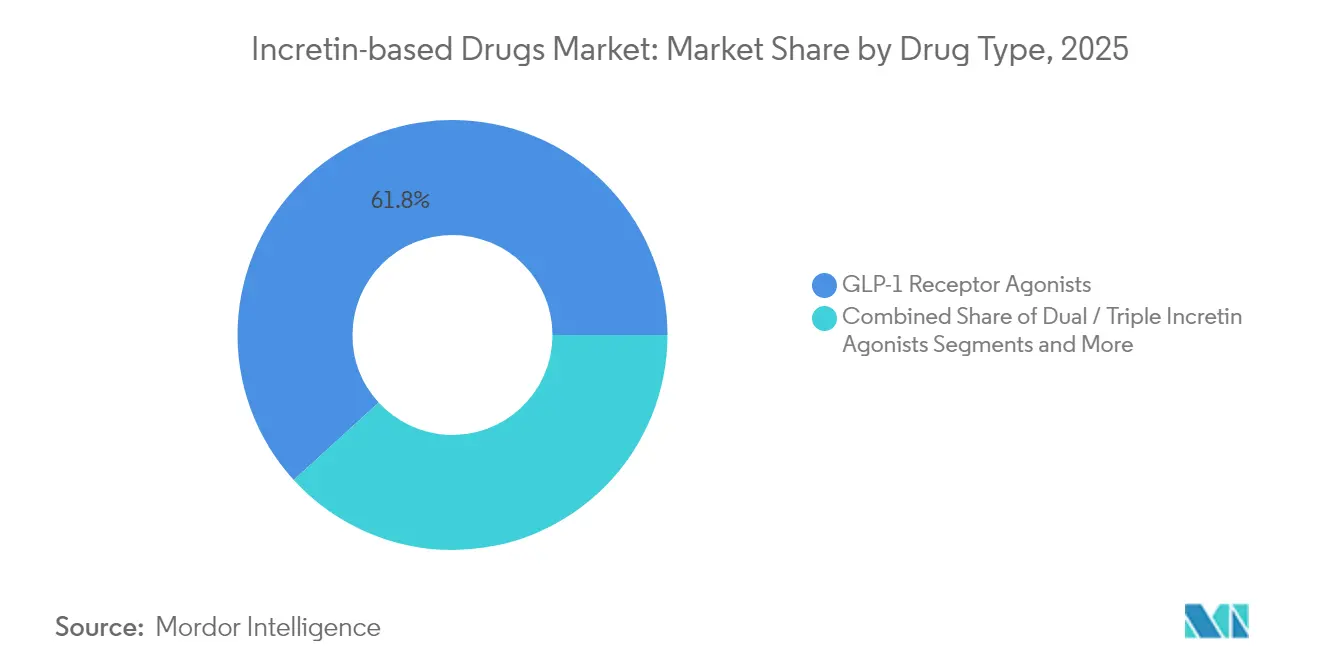

- By drug type, GLP-1 receptor agonists led with 61.78% of the incretin based drugs market share in 2025; dual/triple incretin agonists post the fastest growth at a 6.85% CAGR to 2031.

- By route of administration, injectable formats captured 77.85% share of the incretin based drugs market size in 2025, while oral delivery is projected to expand at a 7.01% CAGR through 2031.

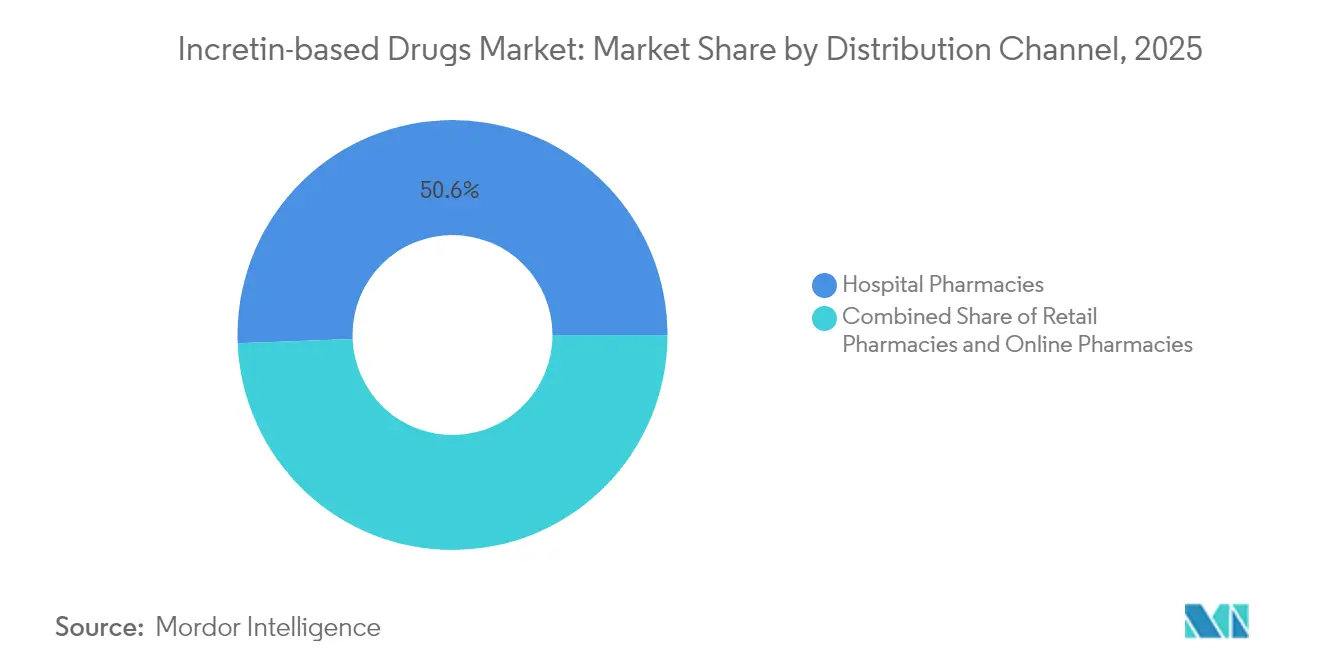

- By distribution channel, hospital pharmacies commanded 50.62% revenue in 2025; online/specialty pharmacies are rising at a 7.55% CAGR to 2031.

- By primary indication, type 2 diabetes accounted for 42.35% of the incretin based drugs market size in 2025, whereas obesity/weight management climbs at an 7.68% CAGR to 2031.

- North America held 43.10% share of the incretin based drugs market in 2025; Asia-Pacific records the highest regional CAGR at 7.98% heading to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Incretin-based Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 blockbuster launches outpacing supply | +1.2% | Global, acute shortages in North America & Europe | Short term (≤ 2 years) |

| Rapid obesity-centric label expansions | +0.8% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Surge in self-pay channels & digital DTC | +1.1% | Global, early adoption in North America | Short term (≤ 2 years) |

| Oral small-molecule GLP-1 pipeline | +0.9% | Global, premium markets first | Medium term (2-4 years) |

| Dual/triple incretin agonists >20% weight loss | +1.3% | Global, led by North America & Europe | Long term (≥ 4 years) |

| API scale-up in India & China cuts COGS | +0.7% | Global supply chains, emerging-market access | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Blockbuster Launches Outpacing Supply

Severe manufacturing bottlenecks persisted in 2024, leaving patients waiting months for prescriptions and prompting premium pricing that protected revenue despite volume gaps. Eli Lilly earmarked USD 23 billion for new peptide facilities across three continents to relieve the deficit, yet analysts expect tight supply until mid-2026. Pharmacies in major U.S. cities introduced rationing lists, while European wholesalers prioritized cardiovascular-risk patients. The dislocation spurred parallel import and compounding channels that challenge quality oversight. As capacity comes online, the incretin based drugs market will likely see a burst of deferred demand, lifting unit sales faster than price cuts can dilute revenue.

Rapid Obesity-Centric Label Expansions

Regulatory agencies accelerated weight-management approvals after trials confirmed up to 22.5% body-weight reduction and 93% diabetes-progression risk decline with tirzepatide [1]Melanie Davies, “Tirzepatide for overweight and obesity management,” TAYLORANDFRANCIS.COM. FDA and EMA green-lit cardiovascular benefit claims for GLP-1s, widening prescribing beyond endocrinology to cardiology and primary care. The broader labeling creates multiple reimbursement pathways and encourages earlier intervention, especially in high-risk prediabetes populations. Payors in the United States now reimburse obesity use for patients with heart failure or chronic kidney disease, a decision mirrored by private insurers in Germany and Australia. As label scope grows, routine polysymptomatic screening is expected to lift diagnosis rates, feeding additional volume to the incretin based drugs market.

Surge in Self-Pay Channels & Digital DTC Prescribing

Telehealth platforms such as Hims, Ro and Sequence recorded triple-digit subscription growth, offering rapid e-prescription of GLP-1s through online questionnaires. Cash-pay packages, priced at USD 350–500 per month, bypass prior-authorization delays and resonate with consumers motivated by cosmetic weight-loss goals. The channel now accounts for an estimated 12% of U.S. retail volume, up from 5% in 2023. While access broadens, clinician groups warn of fragmented follow-up and inconsistent laboratory monitoring. Manufacturers embrace the model by integrating direct-fulfillment services that protect list prices and gather real-time adherence data, reinforcing digital as a strategic route for the incretin based drugs market.

Oral Small-Molecule GLP-1 Pipeline Improving Adherence

Real-world evidence from Saudi Arabia showed oral semaglutide delivering 3.1% HbA1c reduction at six months with parallel weight gains similar to injectable counterparts. Oral formats eliminate injection anxiety, appeal to primary-care clinicians with limited training budgets, and streamline chronic-disease polypharmacy. Formulations leveraging permeation enhancers and nanoparticle carriers are advancing through late-stage trials, targeting once-daily dosing. The adherence boost could materially expand the incretin based drugs market into moderate-risk and elderly cohorts historically under-treated due to injection reluctance.

Dual/Triple Incretin Agonists Showing >20% Extra Weight Loss

Tirzepatide’s dual GIP/GLP-1 profile outperformed semaglutide by 5-6 percentage points of body-weight reduction in head-to-head studies. Early-phase triple agonists that add glucagon receptor activation have recorded 25% weight-loss markers, signaling a leap in efficacy that could reset patient and payer expectations. The superior outcomes justify premiums of 20%–30% over legacy GLP-1 monotherapies, insulating innovators from biosimilar erosion. Successive multi-hormone launches keep the incretin based drugs market on a steep innovation-led growth slope through the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement outside US & select EU payors | -0.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Persistent global supply shortages through 2026 | -1.2% | Global, severity varies by region | Short term (≤ 2 years) |

| Safety-signal overhangs (thyroid C-cell, GI) | -0.7% | Global, stricter oversight in EU | Long term (≥ 4 years) |

| Margin squeeze for retail / independent pharmacies | -0.5% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Outside US & Select EU Payors

Brazil’s ANVISA approved tirzepatide yet monthly therapy costs between BRL 1,883 and BRL 4,007 (USD 376–800) put it beyond reach of average wage earners. Similar affordability gaps exist in India, Indonesia and South Africa where public payors restrict coverage to severe cases or require prior failure of cheaper oral agents. The reimbursement divide creates a two-tier adoption curve that slows volume growth outside premium economies, capping upside for the incretin based drugs market until flexible contracting or local manufacturing narrows cost gaps.

Persistent Global Supply Shortages Through 2026

Device-component scarcities, peptide synthesis cycle times and sterile-fill limitations converged to restrict finished-product availability in 2024, forcing rationing protocols even in high-income systems. Although manufacturers have announced expansions, validation timelines and regulatory inspections prolong relief. The shortage curbs prescriber confidence and delays new-patient starts, lopping up to 1.2 percentage points off the forecast CAGR for the incretin based drugs market during the next two years.

Safety-Signal Overhangs (Thyroid C-Cell, GI Events)

Pharmacovigilance databases logged elevated cholelithiasis and rare medullary thyroid carcinoma signals, triggering EMA directives for enhanced labeling and ultrasound monitoring. The precautionary moves heighten clinician scrutiny and prompt conservative dosing in elderly and renal-compromised cohorts. Resulting drop-outs and slower titration rates temper near-term uptake, although long-term risk-benefit assessments remain favorable for most patients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Dual Mechanisms Drive Innovation

GLP-1 receptor agonists generated 61.78% of the incretin based drugs market size in 2025 on the strength of broad clinical evidence and payer familiarity. Dual/triple agonists, however, outpace all classes at a 6.85% CAGR through 2031 as superior 20%–25% weight-loss efficacy drives physician switching. Early real-world data show tirzepatide cutting HbA1c by 2.3 points in uncontrolled diabetics versus 1.7 points for liraglutide . DPP-4 inhibitors decline in relevance yet retain footing in fixed-dose combinations aimed at cost-sensitive segments. Pipeline entrants such as survodutide and cotadutide showcase triple-pathway modulation, positioning the incretin based drugs market for continual therapeutic breakthroughs.

The dual-mechanism surge reshapes competitive moats; innovators secure new composition-of-matter patents that defer biosimilar threats and sustain premium positioning. As clinical guidelines migrate toward weight-first management, single-hormone GLP-1s risk price erosion and must pivot to once-weekly depot or oral formats to defend share. Consequently, the incretin based drugs market sees an arms race of mechanistic complexity, with multi-agonists establishing a new standard for metabolic disease control.

By Route of Administration: Oral Delivery Gains Momentum

Injectables dominated the incretin based drugs market with 77.85% share in 2025 due to reliable bioavailability and clinician comfort. Yet oral formats post a 7.01% CAGR as permeability enhancers and stabilizing excipients offset digestive degradation, delivering efficacy on par with subcutaneous routes. Patient surveys indicate 68% preference for pills over pens when cost parity exists, highlighting latent demand. Primary-care physicians report shorter education sessions and higher refill persistence among oral users, translating into durable revenue accrual.

Scaling oral GLP-1 manufacturing requires separate tableting suites and stringent moisture controls, raising capex. However, those investments enable differentiated brand stories that reduce rebate exposure in the crowded injectable category. Over the forecast, oral penetration should lift overall adherence, enlarging the incretin based drugs market and lowering late-stage complication costs for health systems.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies retained 50.62% share of the incretin based drugs market in 2025 given initial titration and monitoring needs. Online and specialty pharmacies, nevertheless, are expanding fastest at 7.55% CAGR, propelled by direct-to-consumer telemedicine bundles and auto-replenishment logistics. Retail chains feel a margin squeeze as manufacturer direct-shipment and hub-service models bypass front-of-store dispensing.

Digital channels capture self-pay clients eager for discretion and speed, facilitating premium price realization outside payer formularies. Integrated data capture enhances real-world-evidence generation, feeding post-marketing safety analytics. As virtual care normalizes, the incretin based drugs market gains a scalable path to reach under-served metro and rural populations without brick-and-mortar footprint expansion.

By Primary Indication: Obesity Applications Surge

Type 2 diabetes contributed 42.35% revenue to the incretin based drugs market in 2025 owing to entrenched guideline placement and near-universal reimbursement in developed regions. Obesity and weight management applications log the strongest outlook at an 7.68% CAGR to 2031 as high-visibility cardiovascular-outcome studies shift payer calculus toward preventive weight control. Cardiometabolic comorbidity segments, including heart failure with preserved ejection fraction, represent nascent but promising niches that could add incremental USD 4 billion by the period end.

The broadened indication scope enables lifetime-value stacking, with patients cycling through obesity, diabetes prevention and lipid-control regimens under a single therapeutic umbrella. Such continuum-of-care positioning entrenches the incretin based drugs market within chronic-disease ecosystems once dominated by statins and ACE inhibitors.

Geography Analysis

North America held 43.10% of the incretin based drugs market in 2025, supported by employer-based insurance that absorbs USD 1,000-plus monthly list prices and by active telehealth uptake that accelerates initiation. FDA fast-track designations for cardiometabolic uses keep the approval pipeline robust, and bipartisan legislative interest in obesity care hints at future Medicare coverage expansion. Canada mirrors U.S. clinical enthusiasm but negotiates lower net pricing through centralized procurement, moderating revenue per patient.

Europe delivers steady but heterogeneous demand. Germany and the United Kingdom reimburse GLP-1s for BMI ≥30 kg/m² plus comorbidities, while Italy and Spain impose stricter BMI triggers, dampening volume. Health technology assessment agencies increasingly factor cardiovascular benefits into cost-effectiveness models, a shift likely to unlock broader access by 2027. Regional purchasing alliances may, however, pressure list prices, nudging manufacturers toward outcomes-based contracts to protect margin within the incretin based drugs market.

Asia-Pacific is the fastest-growing region at 7.98% CAGR, driven by rapid urbanization and rising obesity prevalence. China’s cost-utility studies validate tirzepatide’s economic merit despite premium positioning, paving the way for volume-based procurement frameworks. Japan authorized obesity labeling in 2025, creating new reimbursement pathways, while Australia struggles with restricted formulary budgets, relying on patient copay programs. India straddles producer-consumer roles: domestic peptide output lowers COGS, yet public reimbursement remains limited, fostering a robust private-pay segment that nevertheless enlarges the incretin based drugs industry footprint.

Competitive Landscape

The incretin based drugs market remains oligopolistic. Novo Nordisk and Eli Lilly together control more than two-thirds of global revenue, leveraging patent depth, biologics manufacturing scale and integrated device portfolios. Both firms pursue 24-month capacity buildouts, dual-sourcing API and pen components to secure supply continuity. Novo’s once-weekly oral semaglutide tablet and Lilly’s auto-reconstitution pen exemplify device-formulation synergies that fortify brand stickiness.

Second-tier players such as AstraZeneca, Sanofi and Boehringer Ingelheim pivot toward partnership models to share peptide R&D risk. AstraZeneca’s licensing of ECC5004 adds an oral entry that complements its SGLT-2 franchise [3]Ana Luiza de Carvalho, “Brazilian drugmakers race for generic Ozempic,” VALORINTERNATIONAL.GLOBO.COM . Meanwhile, Asian firms Biocon and Shanghai Desano scale GLP-1 analog APIs for contract supply, eyeing biosimilar pathways post patent expiry. The emergence of high-purity, low-cost Asian capacity erodes the manufacturing moat, compelling incumbents to differentiate through multi-agonist innovation.

Digital health companies integrate vertically by bundling teleconsultations, fulfillment and coaching under subscription models, capturing data that refine dosage algorithms. Such tech-enabled entrants lack manufacturing assets yet influence prescribing pathways and patient loyalty, creating partnership or acquisition targets for pharma majors intent on direct-to-patient engagement. The resulting ecosystem positions the incretin based drugs market at the intersection of biopharma, med-tech and consumer health.

Incretin-based Drugs Industry Leaders

AstraZeneca

Novo Nordisk

Eli Lilly

Novartis AG

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Eli Lilly partnered with Amazon Pharmacy to deliver diabetes, migraine and obesity drugs, including GLP-1 agent Zepbound, improving patient convenience and brand reach.

- November 2023: AstraZeneca secured exclusive rights to ECC5004, an investigational oral once-daily GLP-1 receptor agonist, bolstering its obesity and type 2 diabetes pipeline.

- March 2023: England’s NHS approved Wegovy (semaglutide) for weight management, providing thousands with GLP-1 therapy through public funding.

Global Incretin-based Drugs Market Report Scope

As per the scope of the report, incretin-based treatments control post-meal glucagon and help reduce post-meal blood sugars. These medicines also refer to blood sugar normalizing medications or euglycemic, i.e., drugs that help retain the blood sugar to the normal range. The incretin-based medicines are available in two families of medicines, i.e., DPP-4 Inhibitors and GLP-1 analogs. The Incretin-based Drugs Market is Segmented by Drug Type (Glucagon-like Peptide-1 (GLP-1) Receptor Agonists, Dipeptidyl Peptidase-4 (DPP-4) Inhibitors), Route of Administration (Oral and Injectable), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| GLP-1 Receptor Agonists |

| Dual / Triple Incretin Agonists |

| DPP-4 Inhibitors |

| Others / Pipeline Classes |

| Injectable |

| Oral |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online / Specialty Pharmacies |

| Type 2 Diabetes |

| Obesity / Weight Management |

| Cardiometabolic Co-morbidities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | GLP-1 Receptor Agonists | |

| Dual / Triple Incretin Agonists | ||

| DPP-4 Inhibitors | ||

| Others / Pipeline Classes | ||

| By Route of Administration | Injectable | |

| Oral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online / Specialty Pharmacies | ||

| By Primary Indication | Type 2 Diabetes | |

| Obesity / Weight Management | ||

| Cardiometabolic Co-morbidities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Incretin-based Drugs Market size?

The market is projected to reach USD 51.19 billion by 2031 based on a 6.67% CAGR.

Which segment grows fastest within this space?

Dual/triple incretin agonists record the highest CAGR at 6.85% through 2031 thanks to superior weight-loss efficacy.

Why are supply shortages expected to persist until 2026?

Peptide synthesis complexity, device-component scarcities and lengthy validation timelines slow capacity expansion despite large capital outlays.

Which region has the biggest share in Incretin-based Drugs Market?

In 2025, the North America accounts for the largest market share in Incretin-based Drugs Market.

Page last updated on: