Psychotropic Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

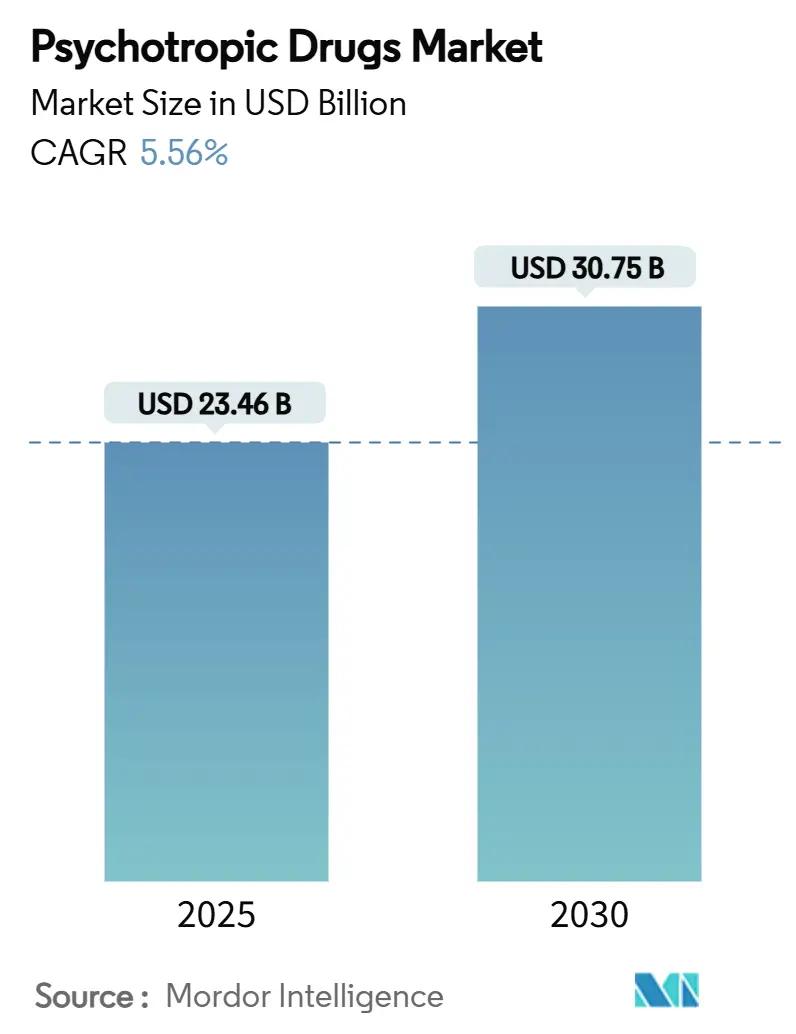

| Market Size (2025) | USD 23.46 Billion |

| Market Size (2030) | USD 30.75 Billion |

| Growth Rate (2025 - 2030) | 5.56% CAGR |

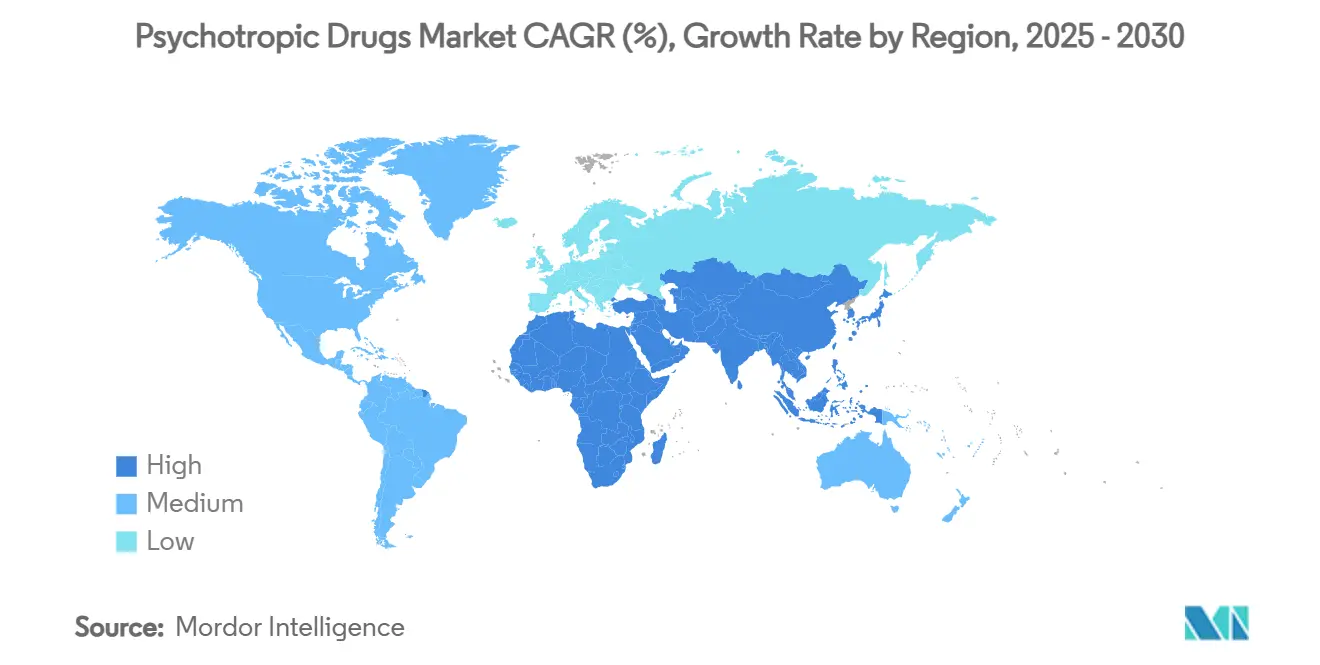

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Psychotropic Drugs Market Analysis by Mordor Intelligence

The psychotropic drugs market stood at USD 23.46 billion in 2025 and is projected to reach USD 30.75 billion by 2030, translating into a 5.56% CAGR over the forecast horizon. Rapid population aging, broader primary-care prescribing, and the rise of AI-enabled diagnostic platforms are widening the treated patient pool, while regulatory bodies are demonstrating greater flexibility toward novel mechanisms such as NMDA-modulating agents and psychedelics. Demand also benefits from value-based reimbursement schemes that reward routine depression screening in hospital settings, feeding prescriptions through both inpatient and outpatient channels.[1]U.S. Centers for Medicare & Medicaid Services, “Fiscal Year 2025 Medicare Inpatient Psychiatric Facilities Prospective Payment System Updates,” cms.gov Competitive intensity is rising as multinational firms pursue bolt-on acquisitions—Johnson & Johnson’s USD 14.6 billion purchase of Intra-Cellular Therapies being a leading case—and as biotech specialists shepherd late-stage psychedelic assets through Phase III pipelines. Against this backdrop, the psychotropic drugs market is navigating both pricing headwinds from looming patent expiries and access frictions tied to tighter prior-authorization algorithms at major U.S. payers.

Key Report Takeaways

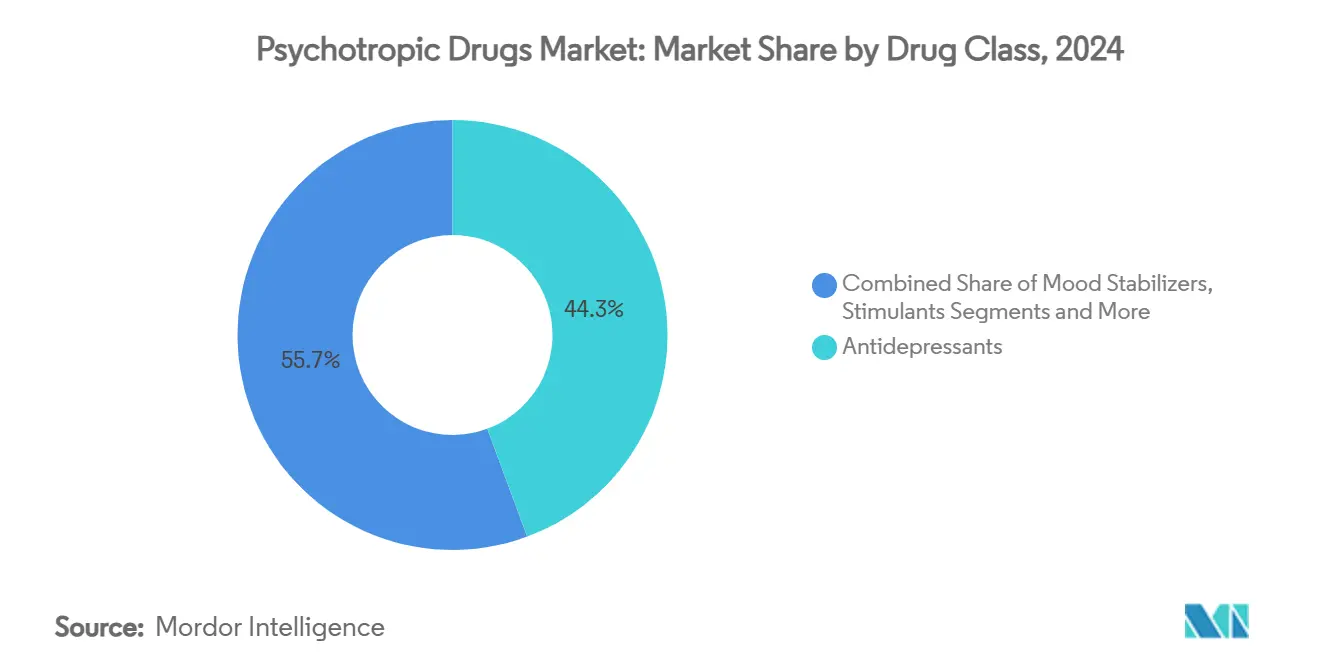

- By drug class, antidepressants held 44.34% of psychotropic drugs market share in 2024.Stimulants are forecast to advance at an 8.63% CAGR through 2030—the fastest among all drug classes.

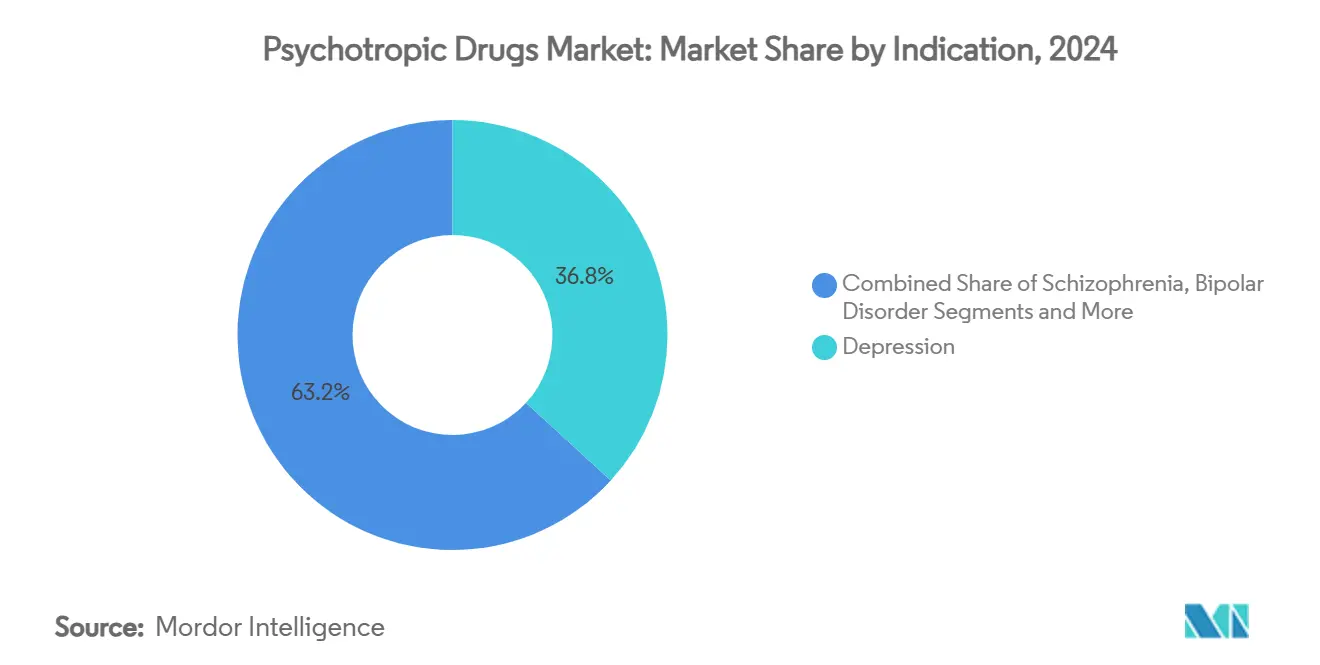

- By indication, depression represented 36.83% of the psychotropic drugs market size in 2024, whereas ADHD medications are projected to grow at an 8.26% CAGR to 2030.

- By distribution channel, hospital pharmacies commanded 52.37% of revenue in 2024, while online pharmacies are poised to expand at a 9.47% CAGR through 2030.

- North America accounted for 39.54% of global revenue in 2024; Asia-Pacific is on track for a 7.81% CAGR over the forecast period.

Global Psychotropic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Related Surge In Mood Disorders | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rising SSRI Prescriptions In Primary Care | +0.8% | Global, with highest penetration in North America | Medium term (2-4 years) |

| Expanding Digital Mental-Health Diagnosis Funnel | +0.9% | North America & EU leading, APAC catching up | Short term (≤ 2 years) |

| Neuro-Innovation (NMDA-Modulating Agents, Psychedelics) | +0.7% | North America & Australia pioneering, EU following | Long term (≥ 4 years) |

| Hospital Pay-For-Performance Tying Reimbursement To Depression Screening | +0.4% | United States primarily | Medium term (2-4 years) |

| Employer-Funded Neuro-Wellness Benefits Boosting Drug Adherence | +0.3% | North America & select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-related Surge in Mood Disorders

Geriatric populations are experiencing high rates of late-onset depression and anxiety, forcing clinicians to employ intensified pharmacological regimens that often combine antidepressants, mood stabilizers, and cognitive enhancers for persistent symptoms. Social isolation, multimorbidity, and neurodegenerative processes converge to drive long-term drug utilization, particularly in Medicare-funded systems where reimbursement models now accommodate lengthier treatment courses. As life expectancy rises in high-income economies, this cohort secures a durable demand base for the psychotropic drugs market. Emerging biomarker research further supports proactive prescribing by flagging subclinical depressive phenotypes, thereby expanding the therapeutic funnel.

Rising SSRI Prescriptions in Primary Care

General practitioners now initiate antidepressant therapy in roughly two-thirds of East-Asian cases, reflecting greater confidence in second-generation SSRIs and the operational efficiencies of AI-assisted decision tools. This decentralization shortens referral times, boosts adherence, and normalizes mental-health treatment within holistic primary-care encounters. Although diagnostic sophistication improves, complex or treatment-resistant cases often circle back to psychiatric specialists, creating multilayer demand across the care continuum. Pharmaceutical manufacturers therefore pivot marketing toward primary-care channels while investing in companion apps that facilitate dose titration and monitoring.

Expanding Digital Mental-Health Diagnosis Funnel

Telehealth platforms, employee wellness portals, and consumer apps leverage natural-language processing to screen millions for depression, PTSD, and anxiety, often outperforming traditional in-office questionnaires on sensitivity and reach.[2]Michael Darden et al., “Cost-effectiveness of Automated Digital CBT for Generalized Anxiety Disorder,” plos.org Earlier detection improves outcomes and enlarges cumulative drug-treated years per patient, particularly in rural or underserved locales where psychiatric capacity remains scarce. Cost-effectiveness studies show automated CBT yielding net monetary benefits topping USD 1,800 for payers, strengthening the economic rationale for upstream screening programs. For the psychotropic drugs market, the digital funnel operates as a volume accelerator without cannibalizing established prescription channels.

Neuro-Innovation: NMDA Modulators & Psychedelics

Ketamine, esketamine, and investigational agents such as psilocybin introduce rapid-acting mechanisms that address neuroplasticity deficits in treatment-resistant depression and schizophrenia.[3]Uriel Heresco-Levy and Bernard Lerer, “Synergistic Psychedelic–NMDAR Modulator Treatment for Neuropsychiatric Disorders,” nature.com Regulators are signaling receptivity: China cleared esketamine nasal spray in 2023 under controlled-use protocols, while the U.S. FDA has advanced MDMA-assisted therapy for PTSD into priority review. Capital flows follow science; Compass Pathways and MindMed have each raised fresh rounds exceeding USD 200 million to fund Phase III programs. These pipelines promise step-change efficacy and potentially premium pricing, expanding the top end of the psychotropic drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent-Cliff Pricing Pressure On Blockbuster Antidepressants | -0.9% | Global, most severe in North America | Short term (≤ 2 years) |

| Stringent Psychotropic Scheduling & REMS Programs | -0.6% | United States primarily, spreading to other markets | Medium term (2-4 years) |

| Adverse-Event Driven Class-Action Litigation Risk | -0.4% | North America & EU | Long term (≥ 4 years) |

| Algorithmic Prior-Authorization Cuts By U.S. Payers | -0.7% | United States, with similar trends in other developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Patent-cliff Pricing Pressure on Blockbuster Antidepressants

Patent expiries for leading antidepressants expose billions in revenue to generic erosion, with Stelara and Entresto among the high-profile losses in 2025. Generic substitution mandates in OECD markets compound the impact, compressing prices and forcing originators to pivot toward novel formulations or pursue defensive life-cycle strategies. Short-term revenue dips can dampen R&D budgets, although the urgency to replace lost income often accelerates investment in next-generation neuropsychiatric assets.

Stringent Psychotropic Scheduling & REMS Programs

Placement of new molecules into restrictive schedules, as seen with zuranolone’s Schedule IV classification, increases prescriber paperwork and slows uptake. REMS programs add mandatory training and monitoring costs that small community practices struggle to absorb. While these safeguards curb misuse, they hamper speed-to-patient metrics and can disincentivize innovators from developing compounds with perceived abuse liability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Stimulants Gain Momentum Amid Antidepressant Leadership

Antidepressants retained 44.34% of 2024 revenue thanks to broad indications and entrenched primary-care usage, cementing their role as the anchor of the psychotropic drugs market. Stimulants, however, clocked the fastest trajectory at an 8.63% CAGR to 2030 as adult ADHD recognition surged in Europe, where medicine consumption exceeded pre-COVID projections by 16.4% across 26 countries. Antipsychotics are undergoing a mechanism renaissance—muscarinic agonist xanomeline-trospium offers metabolic-sparing benefits that could lift adherence among schizophrenia patients. Anxiolytics contend with tighter benzodiazepine rules, whereas mood stabilizers enjoy steady demand amid broader bipolar diagnostic criteria. Cognitive enhancers are embryonic but attractive, especially as employers weigh productivity-boosting benefits.

Stimulant growth rides on post-pandemic healthcare catch-up, telehealth evaluations, and lenient adult prescribing guidelines that began in 2024. European regulators now permit extended-release formulations with lower diversion risk, attracting middle-aged professionals seeking symptomatic relief. Pharmaceutical companies respond with once-daily delivery systems that improve compliance, bolstering psychotropic drugs market share gains for the class. Meanwhile, antidepressant portfolios diversify: triple reuptake inhibitors and rapid-acting compounds are entering late-stage development, potentially arresting market share slippage once generic SSRIs saturate formularies.

By Indication: ADHD Acceleration Begins to Challenge Depression

With a 36.83% slice of 2024 revenue, depression remains the bedrock indication, yet ADHD prescriptions are rising sharply—England alone reported an 18% annual jump post-pandemic. Adult diagnosis protocols and employer-led screenings widen eligibility, lifting ADHD’s contribution to the psychotropic drugs market. Schizophrenia uptake maintains single-digit expansion aided by long-acting injectables, while bipolar disorder growth follows improved recognition of mixed episodes. Anxiety disorders benefit from digital self-assessment tools, promoting earlier pharmacological intervention and cross-selling opportunities with CBT apps. Neurodegenerative-related psychiatric symptoms are gaining clinical attention, particularly agitation in Alzheimer’s disease, drawing pipeline focus toward serotonergic modulators and antipsychotics optimized for the elderly.

The ADHD momentum pushes stimulant innovation—prodrugs with smoother pharmacokinetics and non-stimulant alternatives entering Phase II. Depression’s dominance endures due to high baseline prevalence, but its growth pace moderates as generics capture incremental volumes. Indication diversification therefore helps manufacturers hedge against revenue compression, anchoring overall psychotropic drugs market growth at mid-single-digit levels.

By Distribution Channel: Digital Dispensing Rises

Hospital pharmacies captured 52.37% of 2024 revenue on the strength of acute care and controlled-substance dispensing protocols. Online pharmacies, however, are expanding at a 9.47% CAGR, underpinned by telehealth convenience and permanent shifts in consumer behavior. Teleconsult uptake soared from 11% in 2019 to 46% by 2021, normalizing remote prescription fulfillment. Specialty clinics grab share by bundling prescribing, therapy, and monitoring, particularly for treatment-resistant depression where esketamine administration requires observed dosing. Retail pharmacies still command walk-in volumes but face eroding margins as direct-to-patient delivery gains traction within the psychotropic drugs market.

Controlled-substance regulations create a bifurcated channel landscape—online dispensing remains constrained for Schedule II stimulants or Schedule III esketamine, steering those scripts toward hospital or specialty clinic settings. Nevertheless, regulatory sandboxes in select U.S. states allow pilot e-pharmacy programs with biometric ID verification, signaling potential future liberalization. Manufacturers are thus investing in omnichannel distribution strategies that safeguard compliance while accommodating consumer expectations for doorstep delivery.

Geography Analysis

North America led with 39.54% revenue in 2024, propelled by comprehensive insurance coverage, abundant specialist capacity, and rapid adoption of novel agents such as esketamine. The United States upgrades to value-based reimbursement models reward hospitals for screening and early pharmacologic intervention, reinforcing dominance in the psychotropic drugs market. Canada’s Special Access Program green-lit limited psilocybin therapy, underscoring the region’s tolerant stance toward psychedelic innovation.

Europe follows as a mature but slower-growing arena, where harmonized EMA frameworks streamline approvals yet generic penetration curbs topline expansion. The continent’s ADHD catch-up—highlighted by 16.4% excess stimulant consumption versus forecasts—supports ongoing volume growth. Centralized tenders in Scandinavia and price-volume agreements in France promote predictable uptake patterns, preserving psychotropic drugs market share for established molecules while offering payers leverage on pricing.

Asia-Pacific is set for the swiftest pace at 7.81% CAGR. China’s conditional clearance of esketamine under Category I conditions illustrates balancing access with abuse safeguards. Japan focuses on deprescribing benzodiazepines, indirectly steering prescribers toward newer anxiolytics. Emerging economies in Southeast Asia press ahead with universal-health-coverage agendas that increasingly reimburse psychotropics, though affordability remains a hurdle. Regional prescription patterns vary: polypharmacy is more common in East Asia, while Australia leads per-capita antidepressant use.

Competitive Landscape

The psychotropic drugs market shows moderate consolidation. Johnson & Johnson’s acquisition of Intra-Cellular Therapies fortified its bipolar depression and schizophrenia franchise, exemplifying big pharma’s return to neurology. Otsuka leverages digital therapeutics, pairing Abilify MyCite with adherence-tracking sensors. Pfizer maintains a broad neuroscience pipeline but faces erosion from generic Lyrica and Effexor XR. Biotechs such as Compass Pathways, MindMed, and Atai Life Sciences pursue serotonergic psychedelics with large-scale Phase III trials, banking on orphan-drug or breakthrough-therapy designations to streamline approval.

Strategic imperatives include mechanism diversification, extended-release formulations, and real-world-evidence generation to satisfy payers. Litigation risk encourages conservative labeling, while REMS obligations favor larger incumbents capable of funding compliance programs. Market entrants attempt differentiation through digital support services, such as AI-driven side-effect monitoring apps that feed pharmacovigilance datasets.

Innovation pipelines skew toward treatment-resistant depression, negative-symptom schizophrenia, and Alzheimer’s agitation. NMDA modulators like REL-1017 and muscarinic agonists typify investments aimed at first-in-class status, commanding premium pricing potential. Generics houses remain active: Teva and Sandoz expand portfolio breadth, targeting 2025 post-cliff molecules. Overall, therapeutic novelty coexists with price pressure, creating a dynamic equilibrium that sustains mid-single-digit growth for the psychotropic drugs market.

Psychotropic Drugs Industry Leaders

Pfizer

Eli Lilly and Company

Johnson & Johnson

Otsuka Holdings

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Johnson & Johnson completed its USD 14.6 billion purchase of Intra-Cellular Therapies, adding lumateperone (CAPLYTA) to its portfolio and signaling deeper commitment to neuropsychiatry.

- January 2025: The FDA cleared a supplemental NDA for SPRAVATO (esketamine) as the first monotherapy for adults with major depressive disorder unresponsive to two oral antidepressants.

- July 2024: Lundbeck ended its 17-year partnership with Takeda on Trintellix, converting to a royalty setup to prioritize resources for REXULTI, whose patent security runs to 2029.

Global Psychotropic Drugs Market Report Scope

| Antidepressants |

| Antipsychotics |

| Anxiolytics & Hypnotics |

| Mood Stabilizers |

| Stimulants |

| Cognitive Enhancers & Nootropics |

| Other Psychotropics |

| Depression |

| Schizophrenia |

| Bipolar Disorder |

| Anxiety Disorders |

| ADHD |

| Neurodegenerative-related Psychiatric Symptoms |

| Other Indications (PTSD, OCD, etc.) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antidepressants | |

| Antipsychotics | ||

| Anxiolytics & Hypnotics | ||

| Mood Stabilizers | ||

| Stimulants | ||

| Cognitive Enhancers & Nootropics | ||

| Other Psychotropics | ||

| By Indication | Depression | |

| Schizophrenia | ||

| Bipolar Disorder | ||

| Anxiety Disorders | ||

| ADHD | ||

| Neurodegenerative-related Psychiatric Symptoms | ||

| Other Indications (PTSD, OCD, etc.) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large was the psychotropic drugs market in 2025?

It generated USD 23.46 billion in revenue in 2025.

What CAGR is forecast for psychotropic drug sales to 2030?

Aggregate sales are expected to expand at a 5.56% CAGR to reach USD 30.75 billion by 2030.

Which drug class is set to grow fastest through 2030?

Stimulants lead with an 8.63% projected CAGR, driven by broader adult ADHD diagnosis and telehealth prescribing.

Which region shows the highest growth outlook?

Asia-Pacific is poised for a 7.81% CAGR, supported by expanding healthcare access and mental-health awareness.

How are online pharmacies influencing psychotropic dispensing?

Online channels are forecast to grow at 9.47% annually as telemedicine normalizes remote prescription fulfillment.

What innovation trend is reshaping treatment-resistant depression?

Rapid-acting NMDA modulators and psychedelic-assisted therapies are moving through late-stage trials, offering novel mechanisms and premium pricing opportunities.

Page last updated on: