Psoriasis Drugs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

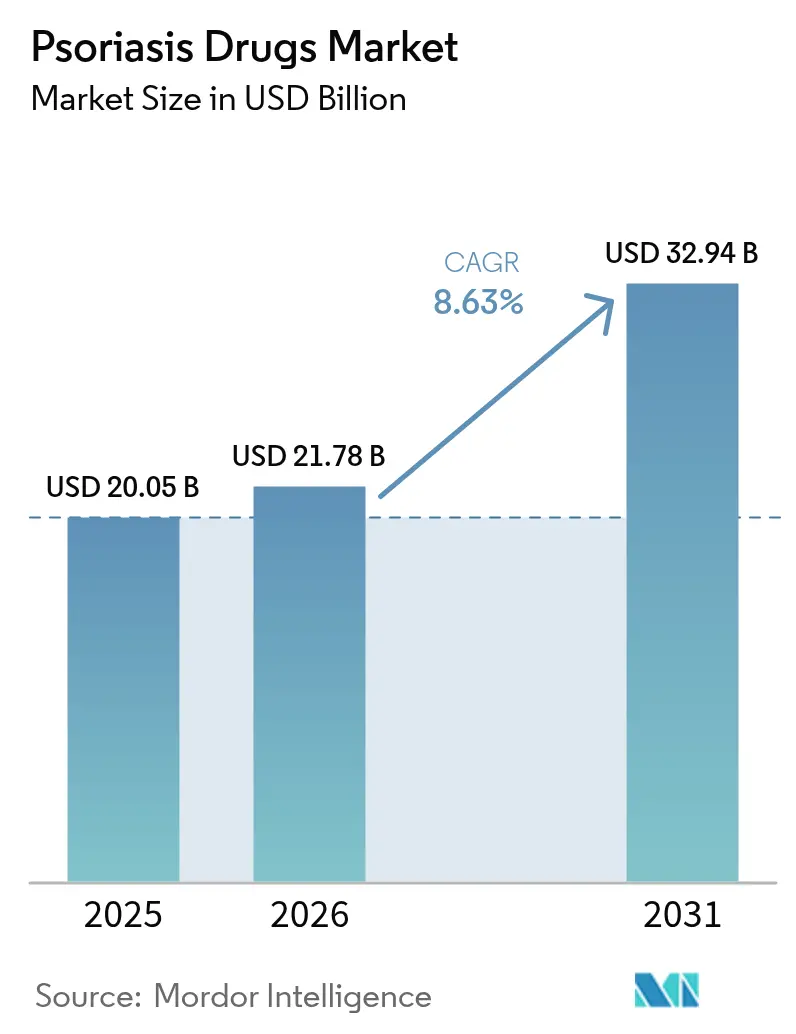

| Market Size (2026) | USD 21.78 Billion |

| Market Size (2031) | USD 32.94 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

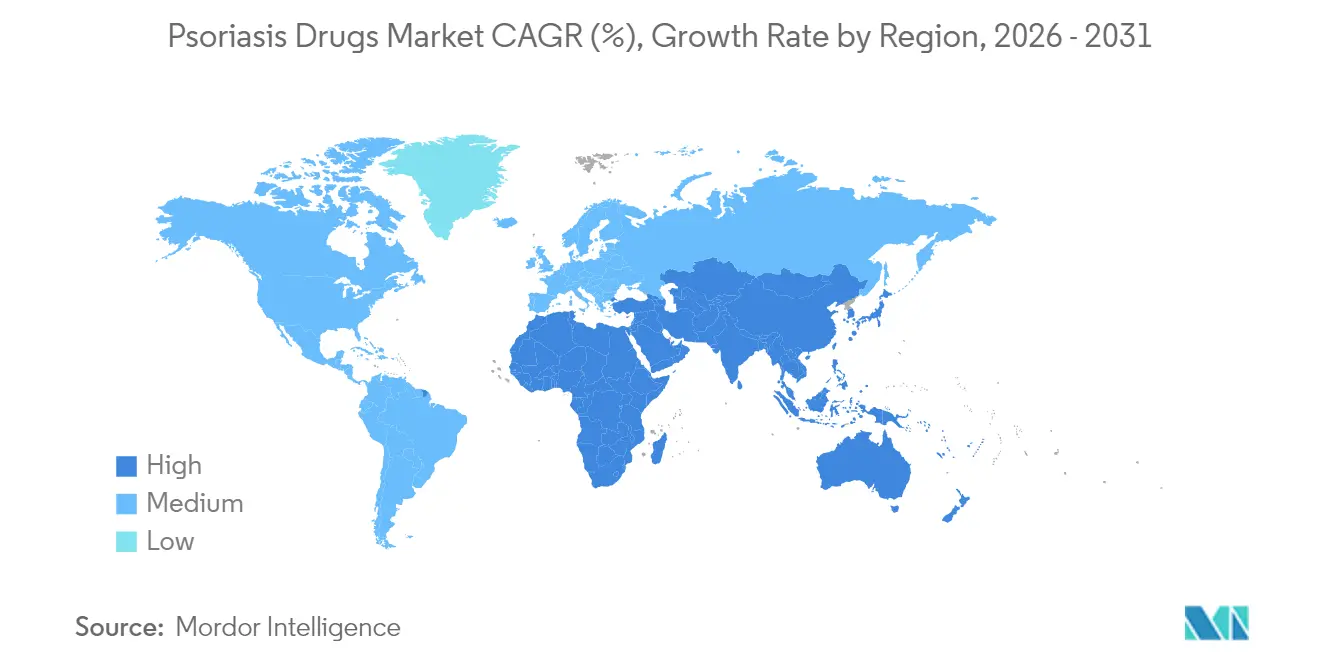

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Psoriasis Drugs Market Analysis by Mordor Intelligence

The Psoriasis Drugs Market size is expected to grow from USD 20.05 billion in 2025 to USD 21.78 billion in 2026 and is forecast to reach USD 32.94 billion by 2031 at 8.63% CAGR over 2026-2031.

The expansion is powered by breakthrough therapies such as first-in-class TYK2 inhibitors, dual IL-17A/IL-17F antibodies, and oral macrocyclic peptides that are redefining chronic inflammatory disease control. A growing pool of moderate-to-severe patients, partly tied to the global obesity upsurge, is widening the addressable base. Adoption is further stimulated by faster regulatory pathways, especially the FDA’s breakthrough and priority review programs, which shorten time-to-market for novel mechanisms. Pricing pressure from biosimilars is simultaneously expanding access while compelling innovators to differentiate through superior durability, convenience, or multi-indication positioning. Collectively, these dynamics keep the psoriasis drugs market on a steady upward trajectory through 2030.

Key Report Takeaways

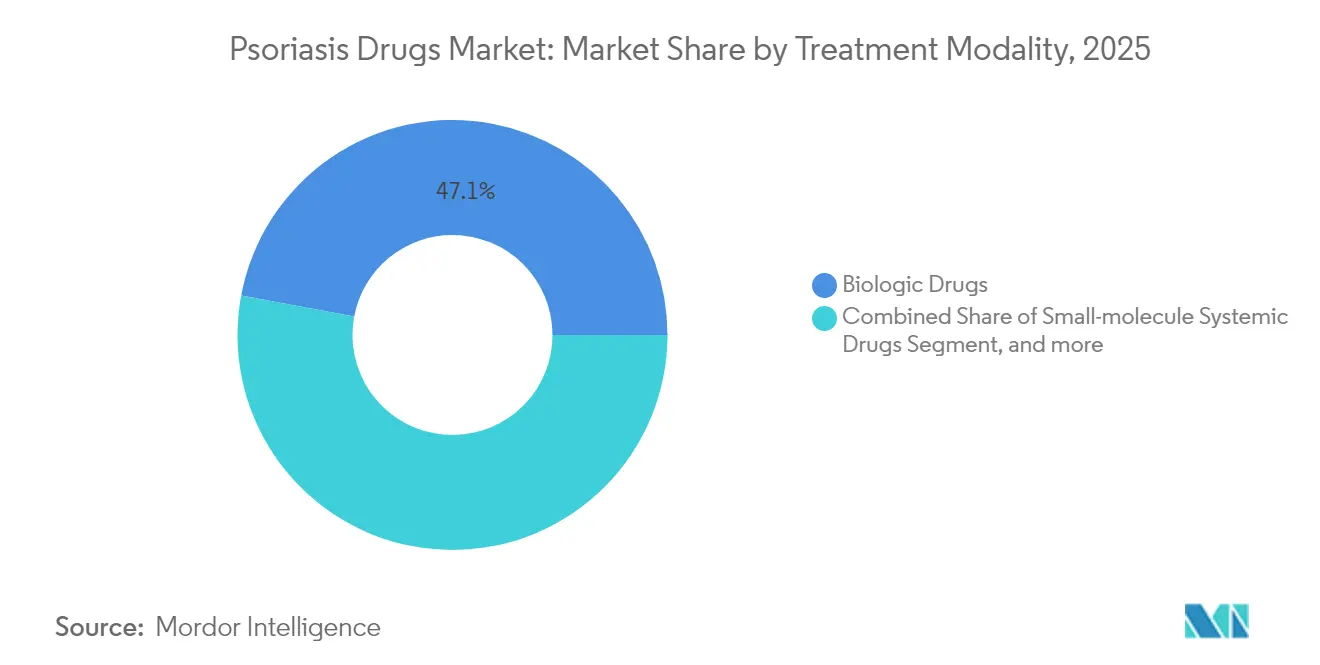

- By treatment modality, biologics held 47.05% of the psoriasis drugs market share in 2025, while small-molecule systemic drugs advanced at a 14.94% CAGR through 2031.

- By drug class, TNF-α inhibitors commanded 40.84% of 2025 revenue, whereas IL-17 agents are projected to accelerate at a 12.31% CAGR to 2031.

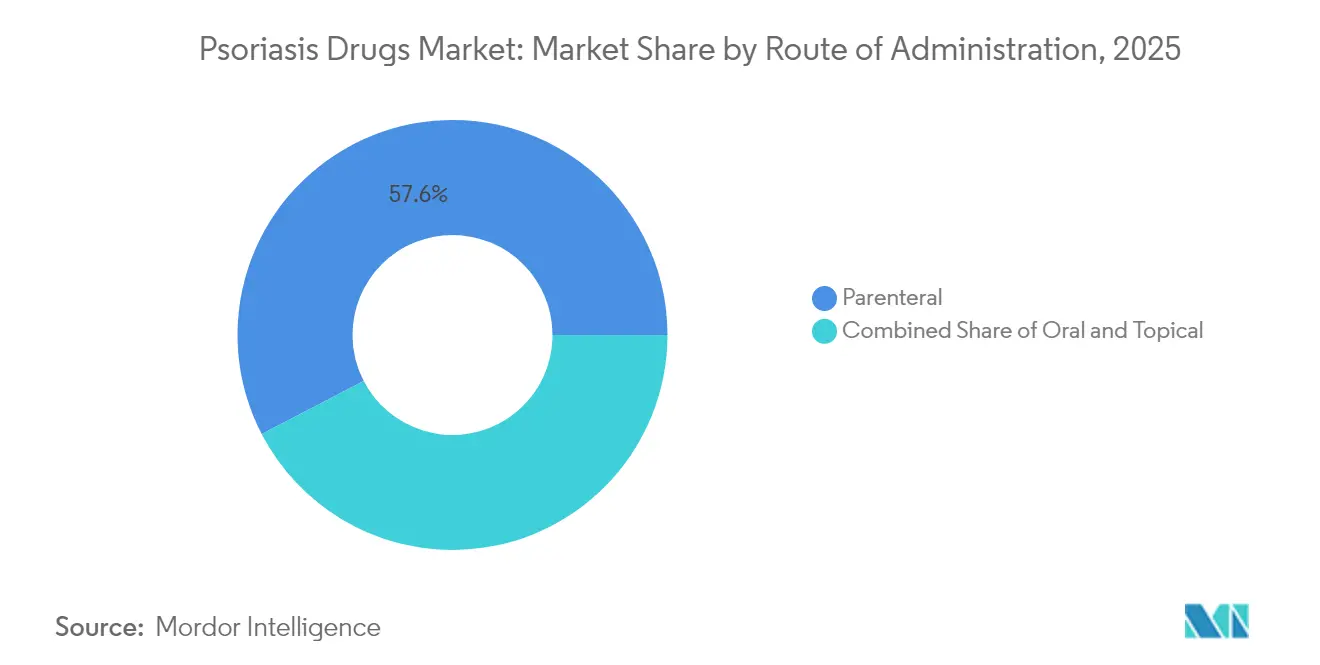

- By route of administration, parenteral formulations retained 57.62% market share in 2025; oral alternatives are growing the fastest at an 11.55% CAGR.

- By distribution channel, hospital pharmacies captured 41.02% of 2025 sales, whereas retail pharmacies are on track for an 11.22% CAGR amid rising oral therapy uptake.

- By geography, North America dominated revenue with a market share of 37.31% in 2025; Asia-Pacific represents the fastest-growing geography with 9.03% CAGR gains expected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Psoriasis Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Disease Burden and Demand for Psoriasis Medicines in Emerging Economies | +2.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Increasing Use of Combination Therapies | +1.8% | Global, with early gains in North America & EU | Short term (≤ 2 years) |

| Increase in Psoriasis Research and Pipeline Drugs | +1.5% | Global | Long term (≥ 4 years) |

| Accelerated Approvals for First-in-Class TYK2 Inhibitors | +1.3% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Obesity-Linked Growth in Moderate–Severe Psoriasis Pool | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Improved Diagnostic Capabilities and Patient Monitoring | +0.9% | Global, accelerated in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Disease Burden and Demand for Psoriasis Medicines in Emerging Economies

Improved infrastructure, payer reforms, and greater disease awareness are unlocking sizable therapy demand across China, India, Brazil, and the Gulf. China’s regulator shortened innovative-drug review from two years to six months, enabling 40 novel approvals in 2023, including multiple psoriasis biologics. Brazil’s biosimilar prescriptions expanded 43% in 2023, underscoring affordability benefits for adalimumab and etanercept.[1]GaBI Online, “Biosimilar Uptake in Brazil,” gabi-journal.net India is moving in parallel; Biocon’s ustekinumab biosimilar matched Stelara efficacy at a fraction of the cost. Although stigma and underdiagnosis persist, AI-enabled dermatology platforms now achieve 89% diagnostic accuracy, helping clinicians close the treatment gap. Collectively, these factors add momentum to the psoriasis drugs market while addressing longstanding unmet needs.

Increasing Use of Combination Therapies

Clinicians are pairing injectable biologics with oral JAK1 or TYK2 inhibitors to heighten response durability in recalcitrant plaques and joint symptoms. A multi-center case series reported pronounced improvements when such dual mechanisms were employed, especially in difficult-to-treat phenotypes.[2]BMJ, “Combination Therapy Case Series,” bmj.com Mechanistically, simultaneous blockade of IL-23/Th17 and JAK-dependent cytokine cascades yields broader inflammatory control. Retrospective analysis of 5,932 courses showed superior drug-survival for combination regimens versus monotherapy. Network meta-analysis indicates that efficacy gains are highest when mechanisms are complementary rather than duplicative, informing future trial designs. The convergence of real-world and controlled evidence is accelerating guideline inclusion and fueling innovation in co-formulated products.

Increase in Psoriasis Research and Pipeline Drugs

Pipeline intensity is near record highs. Alumis/Kaken’s allosteric TYK2 candidate ESK-001 delivered a 64.1% PASI-75 at week 12 in Phase II, triggering a USD 40 million licensing deal. Janssen’s orally stable macrocyclic peptide icotrokinra (JNJ-2113) offers biologic-level potency in pill form, signalling a potential paradigm shift in administration preference Drug Hunter. China’s Xeligekimab reached 90.7% PASI-75 in local Phase III and secured NMPA approval in August 2024. Izokibep’s Affibody design achieves high affinity with reduced molecular size, creating prospects for lower dosing volumes PMC. Beyond plaque disease, spesolimab unlocked the first IL-36-targeted option for generalized pustular psoriasis in 2024.[3] FDA, “Spesolimab Approval,” fda.gov Such diversity underpins a resilient innovation cycle for the psoriasis drugs market.

Accelerated Approvals for First-in-Class TYK2 Inhibitors

Deucravacitinib earned FDA approval and maintains durable PASI-90 rates over five years, demonstrating pseudokinase-domain selectivity that mitigates JAK safety concerns. Japanese trials confirmed consistent efficacy across ethnicities, broadening global uptake. Phase III POETYK PsA data showed 54.2% ACR20 in psoriatic arthritis, expanding the drug’s future indications. Despite strong science, sales were only USD 66 million versus Otezla’s USD 564 million in 2024, highlighting payer hurdles but leaving ample runway. Continued label expansions and improved formulary status are poised to lift the psoriasis drugs market penetration for TYK2 inhibitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Side Effects of Existing Medications | -1.4% | Global | Medium term (2-4 years) |

| High Cost of Psoriasis Treatments | -2.3% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Extensive Drug Development and Approval Process | -1.1% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Stigma and Underdiagnosis in Developing Nations | -0.8% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Side Effects of Existing Medications

Biologic labels caution about serious infections such as tuberculosis, compelling robust pre-treatment screening and ongoing monitoring that inflate costs and deter some prescribers. JAK inhibitors faced FDA safety communications linking them to cardiovascular and malignancy risks; TYK2 selectivity may ease but not erase such concerns. Elderly patients and those with multiple comorbidities remain especially vulnerable, driving discontinuation rates of 20-30% within a year. Although topical agents offer favourable safety, limited depth of response in moderate-to-severe disease restricts their utility. Until pipelines deliver equally potent yet safer options, safety-related attrition will temper the psoriasis drugs market growth.

High Cost of Psoriasis Treatments

Annual biologic therapy can surpass USD 500,000 per patient in the United States, dwarfing average household income and straining public insurers. A JAMA Dermatology efficiency-frontier study showed US net prices exceeding international benchmarks by up to sevenfold even after discounts. South Korea’s reduced-copayment program illustrated the elasticity of demand; biologic uptake quadrupled once out-of-pocket costs fell. Biosimilars entering at 85-90% discounts, exemplified by Stelara copycats, are beginning to mitigate price barriers, yet formulary negotiations and physician inertia slow conversion. The chronic, lifelong nature of therapy ensures that affordability will remain a gating factor for the psoriasis drugs market across many economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Biologics Dominate Despite Oral Innovation

Biologic therapies captured 47.05% of 2025 revenue, confirming their centrality in achieving high PASI clearance for moderate-to-severe patients. Bimekizumab, the first dual IL-17A/IL-17F inhibitor, delivered 85-91% clear or almost clear skin at week 16, sustaining the biologic edge in efficacy. Meanwhile, small-molecule systemic agents form the fastest-growing modality at a 14.94% CAGR through 2031, decisive for the broader psoriasis drugs market. Precision-medicine diagnostics from Mindera Health that forecast biologic response may decrease trial-and-error cycles and bolster long-term adherence.

Combination regimens integrating oral TYK2 or JAK1 inhibitors with injectables are rewriting treatment sequences, particularly for refractory phenotypes. Real-world data show improved drug-survival and functional scores versus monotherapy. Oral innovation, epitomised by icotrokinra’s macrocyclic peptide backbone, points to a future where high-potency blockade can be delivered without needles. As formulary committees recognise these convenience gains, the psoriasis drugs market size attributed to small molecules should expand steadily.

By Drug Class: TNF-α Inhibitors Face Biosimilar Pressure

TNF-α blockers held 40.84% market share in 2025, but multiple adalimumab biosimilars now undercut originator prices and are eroding volume. IL-17 agents are rising at a 12.31% CAGR on speed-to-response, with ixekizumab and brodalumab shaving weeks off PASI milestones. IL-23 inhibitors like guselkumab and risankizumab continue gaining traction through sustained clearance rates and convenient quarterly dosing. Otherwise, niche mechanisms PDE4, TYK2, and IL-36 inject diversity that supports long-term resilience for the psoriasis drugs industry.

Biosimilar entry is slashing reference-product costs by up to 90%, aiding health systems but squeezing innovator margins. Competitive intensity centres on differentiation claims such as rapidity, durability, or extra-cutaneous benefits. Emerging TYK2 contenders like ESK-001 hope to surpass deucravacitinib in terms of the magnitude and duration of response, potentially shifting class hierarchies.

By Route of Administration: Oral Formulations Gain Momentum

Parenteral delivery retained 57.62% market share in 2025 as high-potency monoclonal antibodies dominate severe disease management. However, patient surveys consistently show a preference for pills when efficacy is equivalent, and oral options are expanding at an 11.55% CAGR. Deucravacitinib’s five-year extension data support long-term safety, emboldening prescribers to switch needle-averse patients. Oral macrocyclic peptides further blur the line between small molecules and biologics, heralding a more convenient standard of care.

Meanwhile, next-generation topical technologies, including microneedle patches loaded with zinc-doped silica nanoparticles, aim to raise local drug concentrations without systemic exposure. Such advances enrich clinician toolkits and may protect the psoriasis drugs market size from plateauing as patient demographics shift toward convenience-centric expectations.

By Distribution Channel: Retail Expansion Accelerates

Specialist hospital pharmacies controlled 41.02% of 2025 sales on the back of cold-chain and infusion requirements. Yet the transition to oral therapies is opening retail-level dispensing, now growing at an 11.22% CAGR. Integrated hub services and e-prescription technology enable community pharmacists to monitor adherence and counsel on adverse events, expanding the psoriasis drugs market reach.

Online platforms capture refill demand for maintenance therapy, even though first doses of biologics remain largely hospital-bound due to supervision needs. Specialty pharmacy overlays across all channels deliver adherence coaching and prior-authorisation support, helping navigate payer hurdles. The resultant omnichannel architecture positions the psoriasis drugs industry for broader geographic and socioeconomic penetration.

Geography Analysis

North America generated the highest revenue with market share of 37.31% in 2025, buoyed by advanced insurance coverage, proactive screening, and rapid FDA approvals, which accelerate uptake of first-in-class agents like TYK2 inhibitors. Psoriasis affected 7.9 million US adults in 2023, with heightened prevalence among individuals with BMI ≥30, reinforcing the obesity-linked demand surge. Biosimilar competition, notably multiple ustekinumab alternatives launching at deep discounts, is reshaping price dynamics while maintaining volume momentum.

Europe follows as the second-largest region, supported by the EMA’s centralised review, robust dermatologist networks, and growing biosimilar trust that lowers costs and can speed patient onboarding. Health technology assessments across Germany, France, and the UK increasingly prioritise real-world outcomes, compelling manufacturers to support value-based contracting. The post-Brexit regulatory split obliges companies to maintain dual frameworks yet has not materially slowed access, keeping the psoriasis drugs market competitive across major European economies.

Asia-Pacific remains the fastest-growing geography with 9.03% CAGR between 2026 and 2031. China leads regional expansion thanks to streamlined NMPA reviews, fast reimbursement listings, and domestic innovation exemplified by Xeligekimab. Japan consistently demonstrates high biologic utilisation and swift adoption of global breakthroughs, with deucravacitinib showing cross-ethnic efficacy. India’s biosimilar leadership and improving payer systems are broadening affordability. Australia and South Korea offer mature infrastructures where reduced patient copays have meaningfully lifted biologic penetration. Collectively, the heterogeneity of Asia-Pacific nations delivers a sizeable incremental lift to the psoriasis drugs market.

Competitive Landscape

The market is moderately concentrated, with a diverse mix of multinational pharma and nimble biotech challengers. Johnson & Johnson faces seven FDA-cleared Stelara biosimilars launching in 2025 at discounts up to 90%, signalling unprecedented erosion in the IL-12/23 space.

Mechanism differentiation is the new battleground. UCB’s bimekizumab claims dual cytokine blockade superiority, while Bristol-Myers Squibb’s deucravacitinib builds a new TYK2 category with selective safety advantages. Macrocyclic peptide developers such as Protagonist Therapeutics and Janssen strive to unite biologic potency and oral convenience, reshaping adherence expectations. Precision-diagnostic firms like Mindera Health seek to integrate RNA-profiling into clinical workflows, promising higher responder rates and potential cost savings.

Strategic alliances, co-development deals, and multi-indication label expansions are common. Alumis’s USD 40 million licensing pact with Kaken for ESK-001 underscores regional commercialisation sharing, while Teva and Alvotech’s interchangeable ustekinumab approval reflects the biosimilar industry’s rapid maturation. Forward-looking players also invest in digital therapeutics, AI-driven adherence apps, and real-world-evidence platforms to sustain competitive edges as pricing pressures intensify.

Psoriasis Drugs Industry Leaders

Eli Lilly and Company

Pfizer Inc.

Novartis AG

Amgen Inc.

Johnson & Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva and Alvotech announced FDA approval of interchangeability for SELARSDI (ustekinumab-aekn) with Stelara (ustekinumab), enhancing patient access to affordable treatment options for psoriasis.

- April 2025: Johnson & Johnson received European Commission approval for TREMFYA (guselkumab) for adults with moderately to severely active ulcerative colitis, marking the third indication for this IL-23 inhibitor already approved for psoriasis.

- November 2024: UCB S.A. presented new two-year data validating a continuous clinical response for bimekizumab-bkzx, an inhibitor of IL-17A and IL-17F, in adults diagnosed with active psoriatic arthritis (PsA) with observable signs of reduction in inflammation.

- September 2024: Organon and Dermavant Sciences Ltd. finalized an agreement in which Organon will acquire Dermavant, a company under Roivant that specializes in the development and commercialization of cutting-edge therapeutics for immuno-dermatology. Dermavant's innovative product approved by the United States Food and Drug Administration (FDA), VTAMA (tapinarof) cream, 1%, for the topical treatment of adults with mild, moderate, and severe plaque psoriasis. By combining Dermavant’s robust dermatology commercial and field medical teams in the United States with Organon’s capabilities in market access, regulatory proficiency, and global commercial presence.

Global Psoriasis Drugs Market Report Scope

As per the scope of the report, psoriasis is a genetic condition that may or may not be present at birth but can also be triggered by certain environmental and genetic factors. Factors such as the changing lifestyles of people and their increased inclination toward alcohol consumption and smoking, unhealthy diets, and sedentary living are making people more prone to this condition. The psoriasis drugs market is segmented by type of treatment, mechanism of action, route of administration and geography. By type of treatment, the market is segmented into biologic drugs, small molecule systemic drugs, and tropical therapies. By mechanism of action, the market is segmented into TNF alpha inhibitors, PDE4 inhibitors, interleukin inhibitors, and other mechanisms of action. Other mechanism of action will include anti CD-6 monoclonal antibodies, JAK inhibitors and others. By route of administration, the market is segmented into oral, parenteral, and topical. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Biologic Drugs |

| Small-molecule Systemic Drugs |

| Topical Agents |

| Combination Regimens |

| TNF-α Inhibitors |

| IL-12/23 Inhibitors |

| IL-17 Inhibitors |

| IL-23 Inhibitors |

| PDE4 Inhibitors |

| TYK2 Inhibitors |

| Other Classes |

| Parenteral |

| Oral |

| Topical |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Biologic Drugs | |

| Small-molecule Systemic Drugs | ||

| Topical Agents | ||

| Combination Regimens | ||

| By Drug Class | TNF-α Inhibitors | |

| IL-12/23 Inhibitors | ||

| IL-17 Inhibitors | ||

| IL-23 Inhibitors | ||

| PDE4 Inhibitors | ||

| TYK2 Inhibitors | ||

| Other Classes | ||

| By Route of Administration | Parenteral | |

| Oral | ||

| Topical | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the psoriasis drugs market?

The market is valued at USD 21.78 billion in 2026 and is projected to reach USD 32.94 billion by 2031.

Which treatment modality leads revenue?

Biologic therapies held 47.05% of 2025 revenue, retaining leadership through superior skin-clearance performance.

What CAGR is expected for oral formulations?

Oral routes are forecast to expand at an 11.55% CAGR through 2031 on the back of TYK2 inhibitors and oral macrocyclic peptides.

How significant are biosimilars to future pricing?

Biosimilars launch with discounts up to 90%, notably for ustekinumab, and are expected to broaden access while intensifying price competition.

Which region is growing the fastest?

Asia-Pacific is poised for the strongest gains, driven by China’s accelerated approvals, rising disposable income, and improving awareness.

What safety issues limit therapy uptake?

Infection risk warnings on biologics and cardiovascular concerns linked to JAK inhibitors cause discontinuations and slow adoption among older or comorbid patients.

Page last updated on: