Vaccine Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

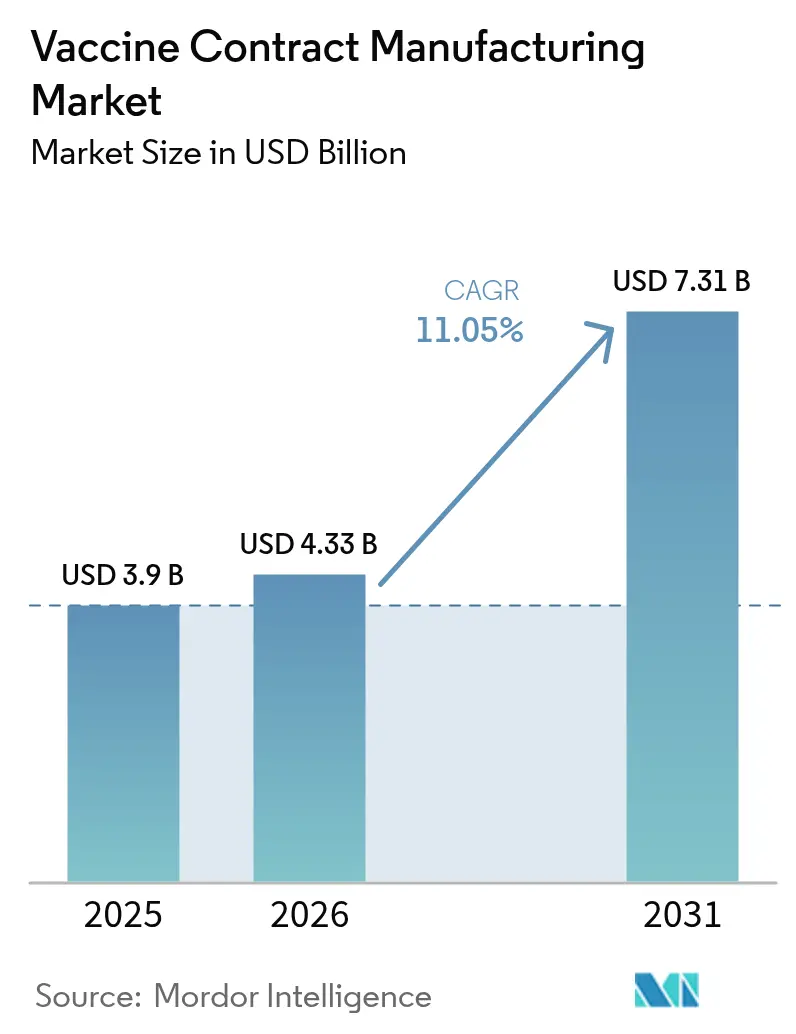

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 7.31 Billion |

| Growth Rate (2026 - 2031) | 11.05% CAGR |

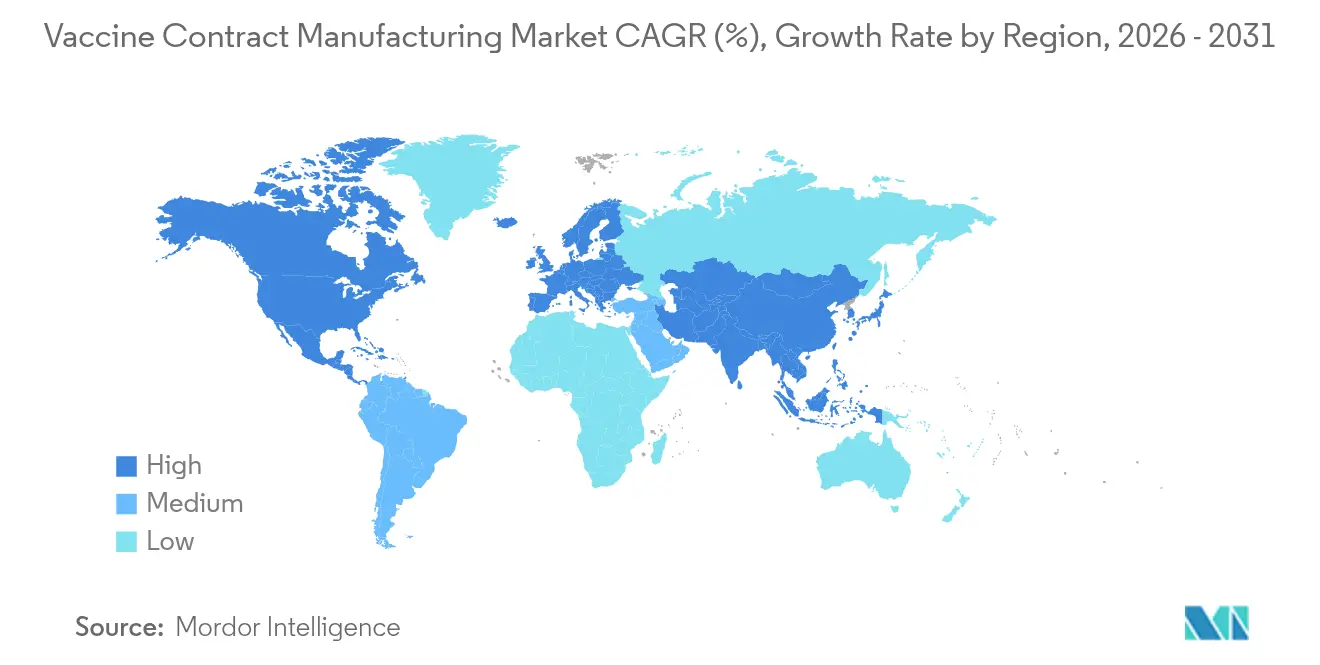

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vaccine Contract Manufacturing Market Analysis by Mordor Intelligence

The vaccine contract manufacturing market size in 2026 is estimated at USD 4.33 billion, growing from 2025 value of USD 3.90 billion with 2031 projections showing USD 7.31 billion, growing at 11.05% CAGR over 2026-2031. Rapid adoption of modular, single-use production lines reduces facility lead-times while allowing quick product changeovers, giving the vaccine contract manufacturing market the agility needed for future outbreak response. Government pandemic-preparedness funds, near-shoring mandates, and an expanding pipeline of RNA and viral-vector candidates keep outsourced capacity tight. CDMOs now win work by pairing platform breadth with regulatory know-how rather than low cost alone. As mRNA, adjuvant, and fill-finish capabilities converge under fewer roofs, buyers have clearer line-of-sight on timelines and quality, further accelerating the vaccine contract manufacturing market.

Key Report Takeaways

- By vaccine type, inactivated vaccines held 33.02% of the vaccine contract manufacturing market share in 2025, while RNA vaccines are projected to post an 18.07% CAGR to 2031.

- By process, downstream processing accounted for 57.62% of the vaccine contract manufacturing market size in 2025.

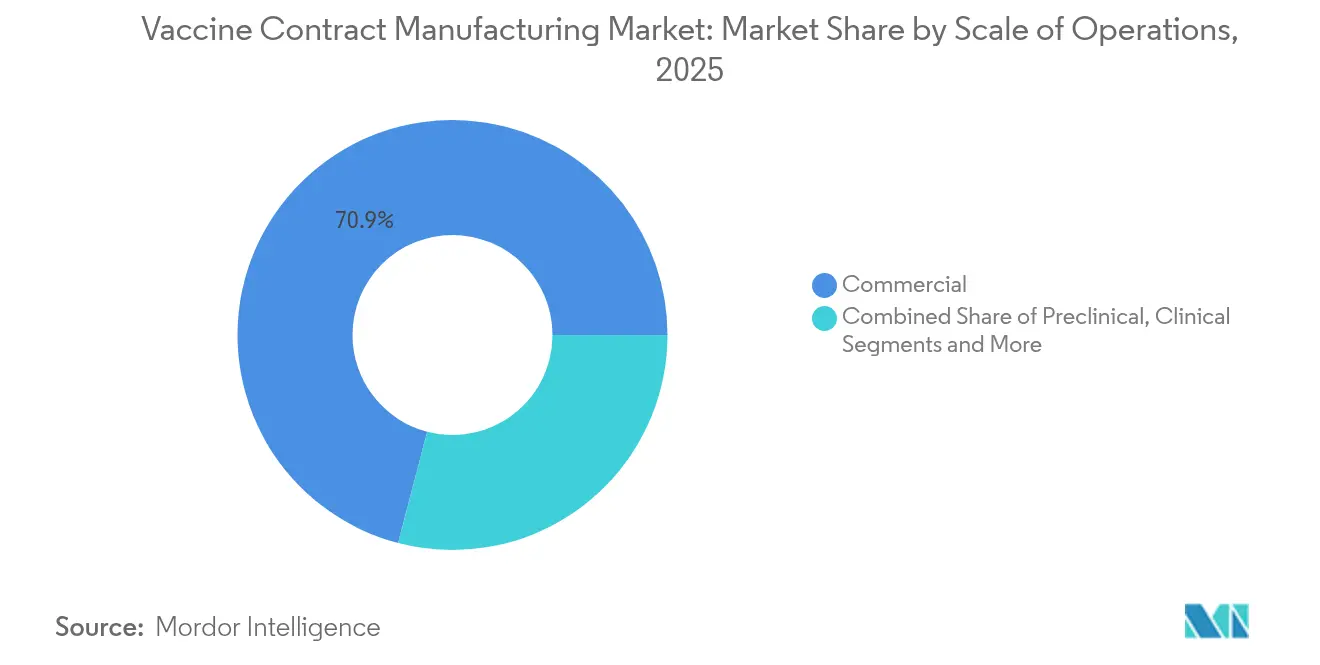

- By scale, commercial-scale production commanded 70.93% share of the vaccine contract manufacturing market size in 2025; preclinical services are expanding at a 13.98% CAGR through 2031.

- By region, North America contributed 46.21% of the vaccine contract manufacturing market size in 2025, whereas Asia Pacific is set to grow at an 11.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vaccine Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in single-use and modular sites | 2.10% | North America, Europe | Medium term (2-4 years) |

| Government immunization funding pools | 2.80% | Global, Gavi-supported and high-income markets | Long term (≥ 4 years) |

| Expanded pediatric vaccine schedules | 1.40% | Asia Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| CDMO platform bundling for mRNA & viral tech | 1.90% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Near-shoring mandates | 1.60% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Digital quality-by-design analytics | 1.20% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advancements In Single-Use and Modular Facilities

Single-use bioreactors and prefabricated cleanrooms cut green-field build times from seven years to under two, letting sponsors align capital outlay with demand surges. Wacker Chemie’s EUR 102 million (USD 119 million) modular mRNA plant shows how standardized blocks can be lifted into multiple jurisdictions without lengthy redesigns, giving the vaccine contract manufacturing market elasticity for pathogen shifts. Capital-light developers gain access to late-phase capacity, while regulators now treat modular suites as equivalent to traditional spaces, trimming validation cycles and smoothing global dossier filings.

Government Immunization Initiatives and Funding Pools

Public buyers now couple purchase budgets with local-capacity targets. Gavi’s USD 1.2 billion African Vaccine Manufacturing Accelerator ties grant disbursement to in-country output, and the U.S. Project NextGen steers USD 5 billion of next-generation COVID-19 spending to domestic partners, giving the vaccine contract manufacturing market multi-year volume visibility.[1]Gavi Secretariat, “African Vaccine Manufacturing Accelerator,” gavi.org

Expansion Of Global Pediatric Vaccine Schedules

Routine programs now include HPV, rotavirus, and complex pneumococcal combinations. WHO’s HPV recommendation alone creates tens of millions of additional adolescent doses each year, pushing CDMOs to scale fill-finish and lyophilization lines for thermostable formulations.[2]World Health Organization, “HPV Vaccination Position Paper,” who.int Combination products raise formulation complexity, favoring operators with broad analytical toolkits.

CDMO Platform Bundling For mRNA And Viral-Vector Tech

Lonza’s USD 1.2 billion acquisition of Roche’s Vacaville site folds lipid nanoparticle, mRNA synthesis and viral-vector suites under one quality system, shortening tech-transfer chains and supporting premium pricing. Similar moves by Evonik and Samsung Biologics show buyers’ preference for one-stop capacity that minimizes regulatory hand-offs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Biologics-Grade Raw-Material Costs | -1.80% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Cold-Chain Gaps In Emerging Markets | -1.20% | Sub-Saharan Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Regulatory Lag In Tech-Transfer Validation | -0.90% | Global, with concentration in emerging regulatory markets | Medium term (2-4 years) |

| Post-COVID Idle Capacity Creating Price Pressure | -1.40% | North America & EU, with spillover to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Biologics-Grade Raw-Material Costs

More than half of lab suppliers raised catalog prices by end-2023, with chromatography resin inflation outpacing general inputs. This eroded CDMO margins locked into fixed-price master service agreements. Limited lipid vendors intensified cost swings for RNA vaccines, and smaller plants lacked hedging scale.

Cold-Chain Gaps in Emerging Markets

Ultra-cold storage needs to curb mRNA rollout in Africa and parts of Latin America. Single excursion events can wipe entire production lots, driving higher insurance and packaging spend while slowing the uptake of advanced platforms.[3]Nature Editorial, “Global Cold-Chain Inequities for mRNA Vaccines,” nature.com Thermostable R&D is underway, but raises time and validation hurdles for smaller firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: RNA Platforms Drive Innovation

The vaccine contract manufacturing market continues to be led by inactivated products, which secured a 33.02% share in 2025 due to decades-long safety data and established demand from public programs. However, RNA vaccines are posting the strongest expansion at 18.07% CAGR, propelled by adaptable sequence design and shorter pre-clinical timelines. Live-attenuated candidates still serve pediatric clusters where durable mucosal immunity is essential, but growth remains slower as regulators favor non-replicating vectors for new pathogens.

CDMOs run parallel stainless and single-use lines, allowing high-balance-sheet clients to keep legacy volume steady while ramping RNA batches without cross-contamination risk. Adjuvant-ready subunit shots gain traction for elderly and immunocompromised cohorts, supported by new saponin and toll-like receptor agonists that boost titers at lower antigen load. Toxoid volumes plateau, limited to booster campaigns in markets with established herd immunity, yet remain critical for manufacturers seeking steady baseline utilization. The diverging technology mix pushes the vaccine contract manufacturing market to invest in capex-flexible suites that can shift between inactivated and genetic platforms with minimal downtime.

By Process: Downstream Bottlenecks Create Value

Downstream steps captured 57.62% of 2025 revenue, making purification and fill-finish the most lucrative node in the vaccine contract manufacturing market. Purity specs tightened post-COVID-19, compelling CDMOs to install high-capacity chromatography skids and single-use depth filters that cut changeover hours. In contrast, upstream runs are scaling through fed-batch intensification and microbial continuous modes, trimming the cost of goods but driving more load into downstream bottlenecks.

Between 2026 and 2031, upstream activities are projected to grow at 14.82% CAGR, spurred by improved insect-cell systems for multivalent proteins. To prevent idle stainless systems, plants adopt hybrid seeds—stainless seed trains feeding single-use production bioreactors, balancing speed and depreciation costs. Analytical quality control weaves through each node, now embracing at-line spectroscopy for in-process release. Fill-finish services fetch premium fees because regulators see syringe integrity and particulate inspection as final risk barriers. Vetter’s EUR 1.5 billion dual-site build illustrates the defensive moat around sterile capacity in the vaccine contract manufacturing market.

By Scale of Operations: Commercial Dominance with Preclinical Growth

Commercial supply held 70.93% of the 2025 value share, reflecting global pediatric schedules and adult booster programs that demand multi-million-dose lots. Yet preclinical orders are rising 13.98% annually through 2031 as oncology vaccines and autoimmune modulators flood discovery stages. Sponsors seek 1-to-5 liter runs with rapid changeovers, prompting CDMOs to carve dedicated suites shielded from GMP commercial traffic.

Clinical-scale lines remain the swing factor, absorbing overflow when commercial plants pause for requalification. Flexible batch sizes—ranging from 50 liters for first-in-human to 2,000 liters for pivotal trials—require modular utilities and mobile isolators. The vaccine contract manufacturing market leverages such infrastructure to shepherd clients from animal proof-of-concept to launch without costly tech transfer. Early engagement builds stickiness; preclinical wins often translate into decade-long commercial contracts once candidates clear Phase III.

By End User: Human Vaccines Drive Growth with Veterinary Opportunities

Human applications dominated 92.05% of 2025 revenue as governments placed pandemic-reserve orders and Gavi expanded procurement budgets. Canine and poultry segments, however, are forecast to record 9.37% CAGR, driven by food-safety imperatives and rising pet ownership in urban Asia. Veterinary rules allow antigen-matching fast-tracks, shortening R&D cycles to three years versus seven in human settings. This makes the vaccine contract manufacturing market attractive for spill-over capacity between flu seasons.

Companion-animal vaccines command a higher price per dose, supporting margins even at smaller lots. Livestock vaccines benefit from multi-antigen blends that reduce farm labor, but stringent reverse-cold-chain demands persist for avian influenza variants. CDMOs experienced in human mRNA and vector technologies now find new revenue in zoonotic-risk mitigation, illustrated by Zoetis’s conditional H5N2 license that taps RNA encapsulation know-how built initially for human respiratory pathogens.

Geography Analysis

North America contributed 46.21% of vaccine contract manufacturing market revenue in 2025 on the back of sizable public incentives and rapid permitting pathways for green-field bioprocess sites. Merck’s USD 1 billion Durham facility integrates 3D-printed components and generative-AI inspection, setting new benchmarks for cycle-time metrics. Canada augments regional depth, with Moderna’s 100-million-dose Laval plant expected online by 2025, underscoring commitment to reshoring supply.

Asia Pacific is the fastest-growing territory, posting an 11.68% CAGR, as China’s biopharma sales hit CNY 650.6 billion in 2023 and India leverages volume efficiencies built on decades of UNICEF procurement. Samsung Biologics’ USD 1.4 billion long-term contract shows multinational trust in Korean quality frameworks, while Indonesia and Thailand roll out tax holidays to lure green-field RNA suites. The region’s skill base widens as universities funnel chemical engineers into GMP apprenticeships, narrowing historical gaps in validation and documentation.

Europe remains a strategic pillar, supported by cohesive EMA guidance and cross-border batch release recognition. Germany’s EUR 600 million pledge to Gavi signals alignment of industrial policy with global health goals, keeping EU plants central to UNICEF tenders. Eastern European states pitch lower labor costs while adopting EU quality codes, drawing second-tier CDMOs seeking cost arbitrage without customs delays. The Middle East & Africa and South America represent smaller shares today but showcase ambitious build programs like the African Vaccine Manufacturing Accelerator. These initiatives could shift the vaccine contract manufacturing market geography by 2030 as technology transfer agreements mature. Infrastructure gaps persist, especially in ultra-cold warehousing, yet funding streams earmark upgrades that dovetail with regional disease-burden priorities.

Competitive Landscape

Competitive intensity in the vaccine contract manufacturing market centers on technology breadth rather than pure volume. Lonza, Samsung Biologics, and Catalent collectively hold roughly one-third of outsourced revenue, bolstered by investments that pull mRNA synthesis, lipid encapsulation, and viral-vector purification under one quality umbrella. Lonza’s Vacaville buyout and Samsung’s Songdo Plant 5 expansion both emphasize dual-suite redundancy, insulating clients from single-site shutdown risks.

Mid-sized specialists gain ground by focusing on niche competencies. Viralvector Core doubles down on insect-cell baculovirus lines, offering sub-18-month tech-transfer commitments that larger peers struggle to match. Meanwhile, Evonik channels BARDA co-funding into U.S. lipid nanoparticle capacity, positioning itself as a critical orchestrator for mRNA supply chains. Vetter and PCI Pharma Services capitalize on fill-finish scarcity, winning multi-year take-or-pay deals that smooth capex recovery.

Digital adoption differentiates operators. Recipharm deploys cloud-based multivariate analysis that predicts deviations, earning on-time batch-release bonuses. FUJIFILM Diosynth’s North Carolina mega-site adds single-use microbial suites next to mammalian lines, touting seamless scale-up from 200 liters to 20,000 liters. The vaccine contract manufacturing market thus rewards firms combining high-mix agility with data-driven batch release. Emerging regional players escalate competition. SK Bioscience’s majority stake in IDT Biologika grants the Korean group a European footprint and vector expertise. Africa-based start-ups leverage Gavi grants to license modular suites from western OEMs, potentially pressuring pricing by the decade’s end. Still, regulatory trust and audit readiness remain high entry barriers, preserving margins for incumbents.

Vaccine Contract Manufacturing Industry Leaders

Lonza

Catalent

Samsung Biologics

WuXi Biologics

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oxford University and Recipharm expanded their malaria vaccine partnership, adding R78C and RH5.1 production. Recipharm is responsible for full fill-finish oversight.

- May 2025: Merck Animal Health committed USD 895 million to boost vaccine R&D and manufacturing in De Soto, Kansas.

- April 2025: FUJIFILM Diosynth Biotechnologies secured a 10-year, USD 3 billion contract with Regeneron for large-scale biologics at its new Holly Springs plant.

- March 2024: Merck opened a USD 1 billion HPV vaccine facility in Durham, North Carolina, featuring generative-AI quality systems.

- March 2025: CordenPharma started construction of a EUR 500 million peptide site in Switzerland, targeting vaccine component demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the vaccine contract manufacturing market as the revenue earned by contract development and manufacturing organizations that deliver upstream fermentation, downstream purification, analytical testing, fill-finish, and packaging for human and veterinary vaccines produced under cGMP conditions.

Scope exclusion: income from monoclonal-antibody therapeutics, small-molecule APIs, and stand-alone pre-clinical research services is not included.

Segmentation Overview

- By Vaccine Type

- Inactivated Vaccines

- Live-attenuated Vaccines

- RNA Vaccines

- Subunit Vaccines

- Toxoid-based Vaccines

- By Process

- Downstream

- Analytical & QC Studies

- Fill & Finish

- Packaging

- Other Downstream Processes

- Upstream

- Bacterial Expression Systems

- Baculovirus / Insect Expression Systems

- Mammalian Expression Systems

- Yeast Expression Systems

- Other Upstream Processes

- Downstream

- By Scale of Operations

- Preclinical

- Clinical

- Commercial

- By End User

- Human

- Veterinary

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with CDMO executives, vaccine-sponsor procurement leads, and regulatory advisers across North America, Europe, and Asia-Pacific let us validate batch sizes, utilization rates, and outsourcing intent over the next five years.

Desk Research

We gathered foundational data from public sources such as WHO and CDC immunization budgets, UN Comtrade shipment codes, and trade bodies like BioPharmaChem, then layered in peer-reviewed articles on single-use bioreactors. Company 10-Ks, investor decks, and press releases supplied capacity, CAPEX, and pricing bands. Paid tools, D&B Hoovers for CDMO sales, Dow Jones Factiva for deal flow, and Questel for mRNA patent counts, helped apportion revenue by service line. These examples illustrate the mix; many other references informed checks and clarifications.

Our analysts filtered every datapoint for date, geography, and definition fit before entry, discarding items that blended prophylactic and therapeutic biologics or mixed bulk API with finish-dose earnings.

Market-Sizing & Forecasting

We established the 2025 baseline with one top-down production and trade reconstruction, then cross-checked it through selective bottom-up supplier roll-ups of average selling price times filled-dose volumes. Key variables modeled include UNICEF procurement history, installed single-use bioreactor liters, RNA vaccine pipeline counts, cold-chain capital spend, and regional labor indices. Multivariate regression projected each driver and supported scenario analysis. When bottom-up totals under-reported regions with sparse disclosure, proportional adjustments used local immunization coverage ratios. This is where Mordor Intelligence adds a disciplined adjustment layer.

Data Validation & Update Cycle

Our outputs pass variance screens against independent metrics, receive a second analyst review, and gain practice lead sign-off. The model refreshes every year, with interim updates triggered by major capacity additions or policy changes, so clients always see the latest view.

Credibility Anchored in Vaccine Contract Manufacturing Baselines

Published estimates diverge because studies choose different service mixes, include or exclude veterinary lines, and convert currencies at varying dates.

By anchoring on cGMP revenue from commercial and clinical vaccine batches and by refreshing assumptions annually, Mordor Intelligence delivers a dependable midpoint for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.90 Billion (2025) | Mordor Intelligence | - |

| USD 2.29 Billion (2024) | Global Consultancy A | Omits fill-finish revenue and uses 2023 FX rates |

| USD 2.70 Billion (2023) | Industry Journal B | Derives value from installed capacity, excludes veterinary doses |

These contrasts show that our clear scope choices, variable selection, and yearly updates give decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current value of the vaccine contract manufacturing market?

The vaccine contract manufacturing market size stands at USD 4.33 billion in 2026 and is predicted to reach USD 7.31 billion by 2031.

Which region leads the vaccine contract manufacturing market?

North America held 46.21% of global revenue in 2025, supported by major federal funding programs and rapid facility permitting.

Why are RNA vaccines important for contract manufacturers?

RNA vaccines grow at an 18.07% CAGR through 2031, demanding specialized mRNA synthesis and lipid nanoparticle expertise that many CDMOs now bundle with fill-finish services.

What drives outsourced downstream processing demand?

Tight sterility regulations and limited global syringe capacity make purification and fill-finish the highest-value stage, capturing 57.62% of 2025 market revenue.

How do government policies influence manufacturing location?

Initiatives such as Gavi’s African Vaccine Manufacturing Accelerator and the U.S. BIOSECURE Act tie funding to domestic or regional production, pushing sponsors toward near-shored CDMOs.

Which scale of operation is expanding fastest?

Preclinical manufacturing services are advancing at a 13.98% CAGR as more early-stage vaccine pipelines, including oncology candidates, enter animal and Phase I testing.

Page last updated on: