India Contract Manufacturing Organization (CMO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

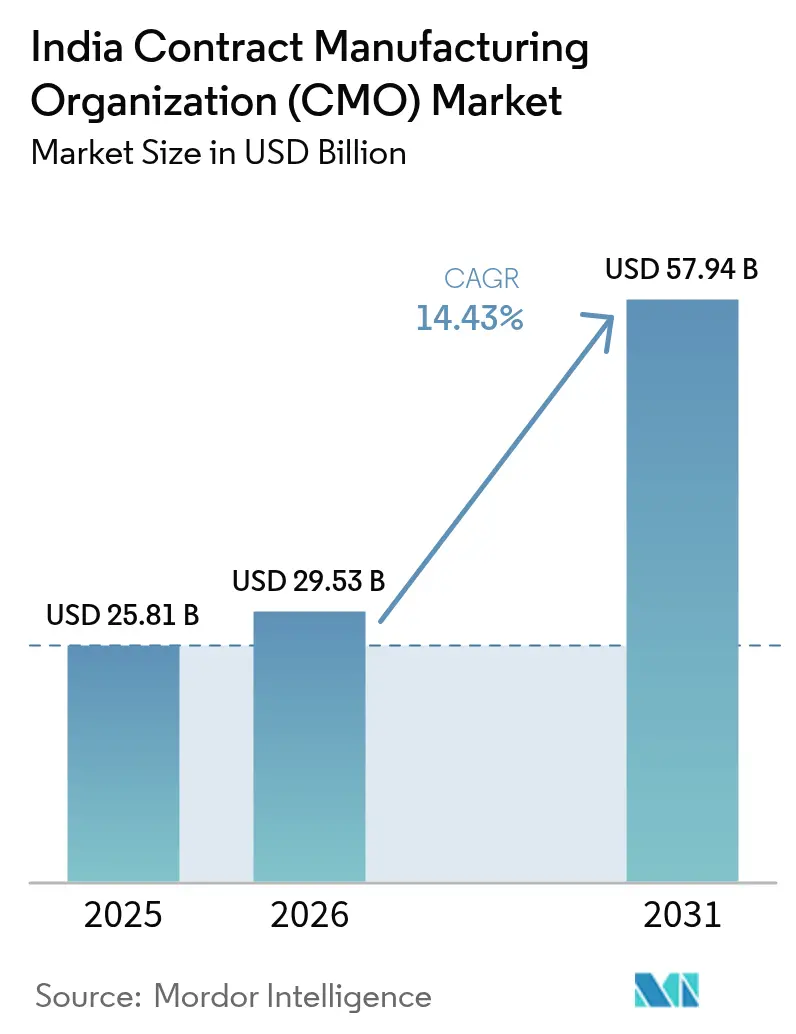

| Base Year Market Size (2025) | USD 25.81 Billion |

| Market Size (2026) | USD 29.53 Billion |

| Market Size (2031) | USD 57.94 Billion |

| Growth Rate (2026 - 2031) | 14.43% CAGR |

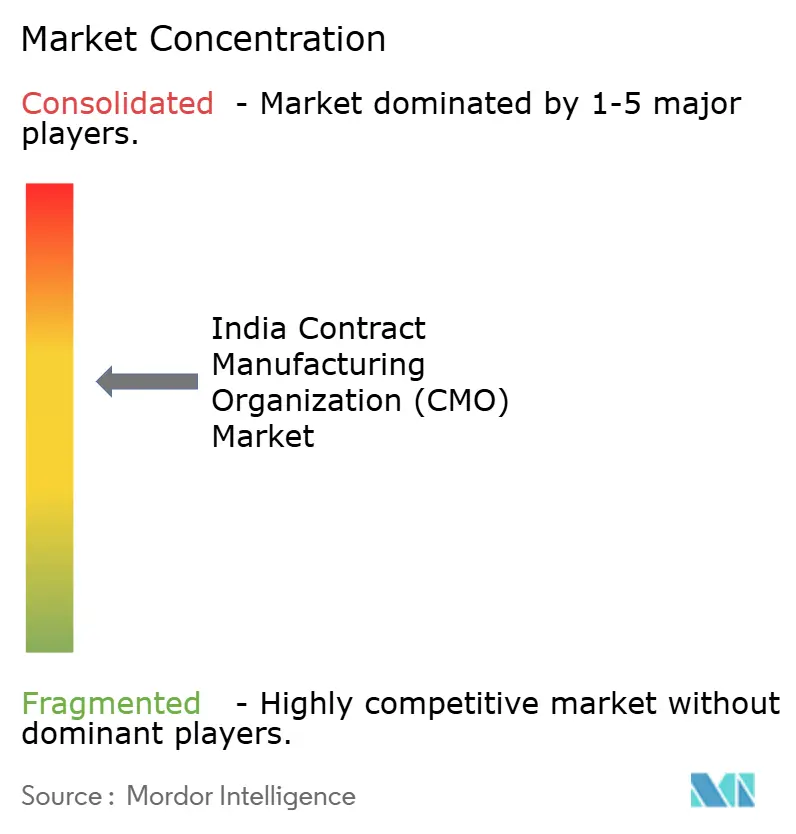

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Contract Manufacturing Organization (CMO) Market Analysis by Mordor Intelligence

The India contract manufacturing organization market size was valued at USD 25.81 billion in 2025 and estimated to grow from USD 29.53 billion in 2026 to reach USD 57.94 billion by 2031, at a CAGR of 14.43% during the forecast period (2026-2031). This rapid expansion is rooted in India’s cost-efficient production base, a technically skilled workforce, and policy catalysts such as the Production-Linked Incentive scheme that accelerate capacity additions. Global sponsors continue redirecting high-value biologics and complex injectable mandates toward India to diversify supply chains, while digitization and AI deployments shrink development timelines and enhance quality consistency. Multinational investments in new greenfield facilities, particularly around Hyderabad and Gujarat, consolidate India’s reputation as a preferred site for outsourced small- and large-molecule manufacturing. Regulatory vigilance from CDSCO and the U.S. FDA is simultaneously tightening quality systems, nudging contract manufacturers toward higher compliance expenditures that ultimately strengthen export credibility.[1]Department of Pharmaceuticals, “Production-Linked Incentive Scheme for Bulk Drugs,” pharmaceuticals.gov.in

Key Report Takeaways

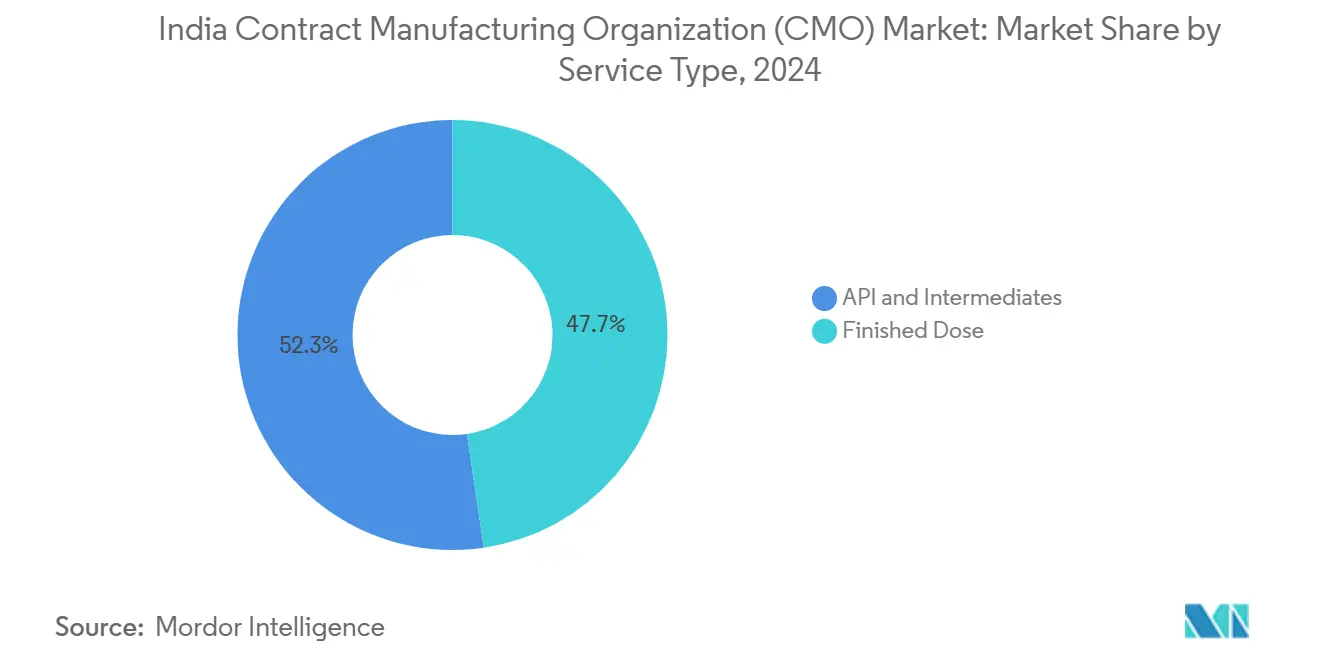

- By service type, API and intermediates led with 51.78% of the India contract manufacturing organization market share in 2025; finished dose manufacturing is projected to expand at a 15.05% CAGR through 2031.

- By molecule type, small molecules commanded 67.65% of the India contract manufacturing organization market size in 2025, whereas large molecules/biologics are poised for a 15.26% CAGR to 2031.

- By end-user, big pharma accounted for a 46.88% share of the India contract manufacturing organization market in 2025; the virtual/start-ups segment is advancing at a 15.95% CAGR through 2031.

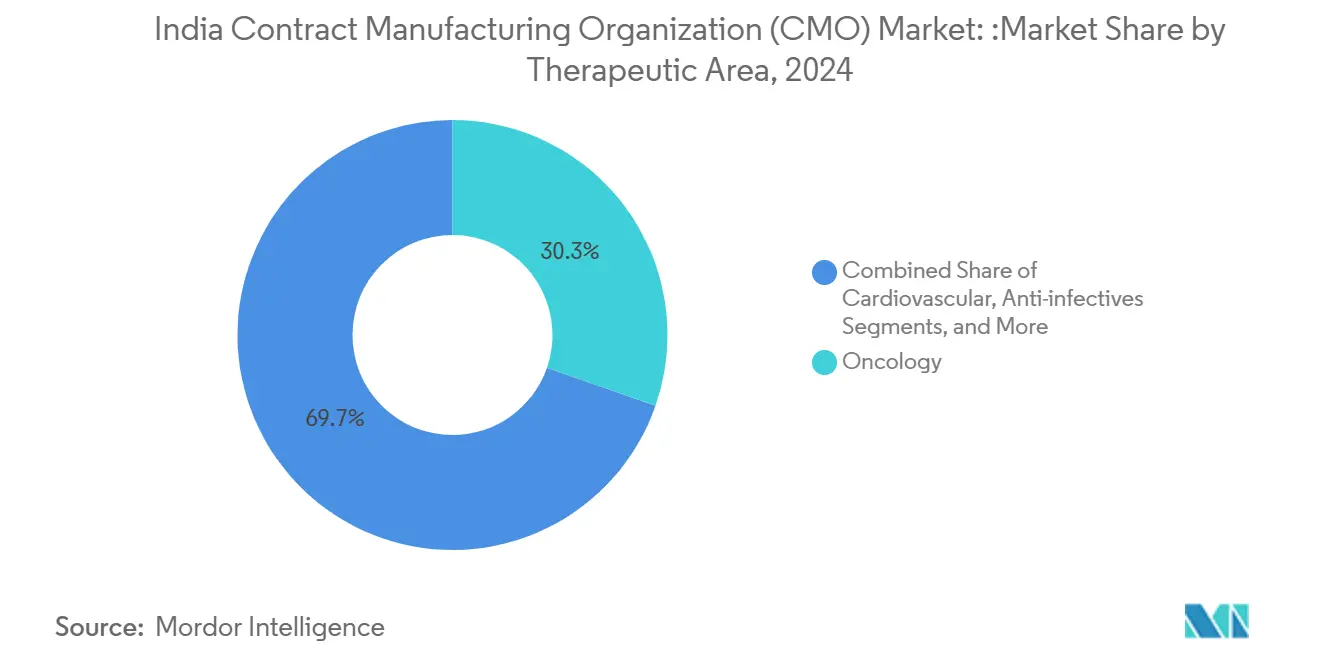

- By therapeutic area, oncology represented 30.05% of the India contract manufacturing organization market size in 2025, while central nervous system therapies are growing at a 16.10% CAGR to 2031.

- By manufacturing scale, commercial production held 61.74% of the India contract manufacturing organization market share in 2025; clinical manufacturing is projected to grow at 14.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Contract Manufacturing Organization (CMO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing biologics outsourcing pipeline | +2.8% | Hyderabad, Bangalore clusters | Medium term (2-4 years) |

| Strong demand for complex injectables | +3.2% | Telangana, Gujarat, Andhra Pradesh | Short term (≤ 2 years) |

| Capacity expansions by global big-pharma | +2.1% | Pan-India established pharma hubs | Medium term (2-4 years) |

| Government PLI schemes for APIs | +1.9% | Bulk drug parks in Himachal Pradesh, Gujarat, Andhra Pradesh | Long term (≥ 4 years) |

| Venture funding in CDMO start-ups | +1.8% | Hyderabad, Bangalore, Mumbai | Short term (≤ 2 years) |

| AI-enabled process-development efficiencies | +1.5% | Early adopters among tier-1 companies nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Biologics Outsourcing Pipeline

India is securing a rising share of global biologics contracts as sponsors pursue lower cost locations without compromising quality. Aurigene opened a 70,000-square-foot monoclonal antibody plant in Genome Valley in 2025, illustrating the industry’s pivot toward mammalian cell culture expertise. Specialized facilities command premium pricing because barriers to entry remain high, yet India still undercuts Western cost structures. CDSCO Schedule M upgrades ensure alignment with U.S. FDA and EMA standards, removing a key procurement hurdle for multinational firms. As a result, contract values for biologics projects are lengthening, and repeat orders are climbing. Sustained double-digit growth is therefore expected for this capability set through 2030.

Strong Demand for Complex Injectables

Sterile manufacturing complexity and limited global capacity are funneling injectable assignments toward Indian CDMOs. Sanofi’s USD 437 million Hyderabad expansion focuses on pre-filled syringes and lyophilized oncology products, underscoring confidence in local expertise. Domestic players are simultaneously scaling fermentation suites for high-potency intermediates. Premium pricing persists because safety regulations mandate rigorous environmental controls, while lead times from alternate Asian hubs remain long. The segment meshes with global moves toward personalized medicine, where complex delivery systems are essential. These conditions maintain a high-margin outlook over the next two years.

Capacity Expansions by Global Big-Pharma in India

Multinationals are doubling down on India to diversify supply chains after pandemic disruptions. Divi’s Laboratories commissioned its Kakinada complex in January 2025 with a USD 144 million outlay, expanding its footprint for complex APIs. Such investments leverage India’s engineering talent and cost structure, securing long-term contract volumes. Expanded footprints also foster technology transfer, raising local capabilities in continuous manufacturing and process analytics. The investment wave is concentrated in established hubs, ensuring supportive ecosystems of suppliers and regulators. Medium-term gains in output are therefore locked in.

AI-Enabled Process-Development Efficiencies

Artificial intelligence is shortening process-development cycles and cutting scrap rates. Mankind Pharma’s OpenAI tie-up integrates predictive maintenance and adaptive process control across pilot plants. Peer-reviewed research finds 15-25% cost savings alongside tighter critical-quality-attribute windows.[2]Journal of Pharmaceutical Sciences, “AI Applications in Pharmaceutical Manufacturing,” jpharmsci.org Early adopters differentiate on speed and reproducibility rather than price alone, attracting higher-margin projects. Long-term gains include real-time release testing and digital batch records that enhance audit readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices linked to China supply | -1.7% | Nationwide, acute for API producers | Short term (≤ 2 years) |

| Rising FDA warning letters to Indian sites | -1.2% | Export-oriented facilities | Medium term (2-4 years) |

| Skilled-talent attrition in key clusters | -1.8% | Hyderabad, Ahmedabad, Baddi | Medium term (2-4 years) |

| Emerging capacity glut in oral-solid dosages | -1.4% | Generic drug manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices Linked to China Supply

China supplies more than 70% of India’s key starting materials, and 2024 environmental clampdowns raised intermediate costs by 20-30%. Margin compression forces CDMOs to renegotiate long-term contracts, straining client relationships. Although PLI parks promise domestic feedstock, scale-up will take multiple years. Hedging strategies and dual sourcing add overheads, weighing on near-term profitability. Sponsors may also withhold multi-year awards until price visibility improves.

Rising FDA Warning Letters to Indian Sites

Fifteen Indian facilities received FDA warning letters in 2024, spotlighting data-integrity lapses and GMP deviations.[3]FDA, “Warning Letters,” fda.gov Remediation diverts cash toward quality upgrades and can halt export shipments. Reputational spillovers affect the broader India contract manufacturing organization market as wary sponsors intensify audits. However, firms that rapidly close observations emerge stronger, often winning new work from competitors that fail to comply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

India Contract Manufacturing Organization (CMO) Market Trends

By Service Type: Finished Dose Growth Outpaces API Dominance

API and intermediates captured 52.32% share of the India contract manufacturing organization market in 2024, underscoring India’s legacy competence in complex chemistry and mature export pathways. The segment benefits from economies of scale in solvent recovery, continuous processing, and effluent treatment, which keep cost-per-kg metrics low. Clients value long operating histories and proven regulatory track records when selecting API partners. Nevertheless, finished dose mandates are expanding quickly, reflected in the 15.42% CAGR projected for 2025-2030. The trend mirrors sponsor preferences to consolidate supply chains under one roof, enabling seamless tech transfer from intermediates to final dosage. Growth is especially sharp in semi-solids and injectables, where specialized isolators and aseptic suites offer defensible margins. Contract manufacturers that integrate serialization, cold-chain packaging, and late-stage customization capture larger wallet share from global clients.

Finished dose providers are also deploying advanced analytics to monitor line yields and reduce deviations, strengthening audit outcomes. Investments in continuous-manufacturing skids for oral solids aim to restore utilization above 50% over the medium term. As more Indian facilities secure U.S. FDA Pre-Approval Inspections, outsourcing of lifecycle management batches rises. Although price pressure persists for commodity tablets, differentiated formulations such as abuse-deterrent opioids and fixed-dose combinations shore up revenue per line. Accordingly, the India contract manufacturing organization market anticipates balanced growth across both chemistry and formulation services through 2030.

By Molecule Type: Biologics Momentum Challenges Small-Molecule Stronghold

Small molecules represented 68.23% of the India contract manufacturing organization market size in 2024, thanks to decades of generic-drug expertise, dense supply networks, and favorable operating economics. Process-chemistry talent and reactor infrastructure allow rapid scale-up from grams to multi-ton output, meeting volume demands of chronic therapies. However, biologics contracts are accelerating, posting a 15.79% CAGR forecast that could lift their share well above 30% by decade-end. Sponsors view Indian CDMOs as credible alternatives to U.S. and European biologics plants, chiefly due to lower fixed costs and proven regulatory compliance. Recent investments span upstream mammalian cell culture, downstream protein A chromatography, and single-use systems that cut turnaround times.

Biocon’s commercial-scale monoclonal antibody facilities validate the country’s technical maturity in large molecules. CDMOs are layering in high-resolution analytics such as mass spectrometry to satisfy stringent comparability requirements. Subsidized biologics parks further reduce greenfield capex, enticing mid-tier sponsors. Continuous-processing pilots in perfusion bioreactors promise higher yields, which could compress cost-of-goods and reinforce India’s price edge. Nonetheless, talent shortages in cell biology and bioinformatics remain a watch point. The dual-molecule landscape positions India as a one-stop destination for sponsors running diversified pipelines.

By End-user: Virtual Players Accelerate While Big Pharma Anchors Volume

Big pharma absorbed 47.42% of 2024 demand, leveraging long-standing partnerships with Indian suppliers for scale economics on blockbuster assets. Engagement models often bundle multi-year volumes across API and finished dose, creating sticky relationships. Yet the rise of virtual and start-up sponsors is reshaping the opportunity mix. Fueled by venture inflows such as Truemeds’ USD 85 million round, asset-light companies outsource every manufacturing stage, driving a 16.43% CAGR in their contracting spend. Mid-size pharma plays a bridging role, frequently piloting new CDMOs before big pharma boards qualify them.

CDMOs are customizing commercial terms-such as milestone-based pricing and development bundles-to align with the cash-flow realities of small, clinical-stage firms. Flexible batch sizes, modular manufacturing suites, and rapid tech-transfer protocols appeal to virtual clients seeking speed over large volumes. Conversely, big pharma remains sensitive to geopolitical risk and quality metrics, prompting exhaustive audits and digital twin validations before onboarding sites. This dual-client landscape compels service providers to balance agility with compliance rigor, a capability mix that few regions outside India can match at similar cost.

By Therapeutic Area: CNS Growth Outstrips Oncology Leadership

Oncology products led the 2024 revenue table with a 30.33% share, a reflection of sustained innovation in targeted therapies and potent compounds that demand specialized containment. Aseptic isolators, hormone handling units, and stringent operator-exposure limits form high barriers to entry, empowering capable CDMOs to capture premium margins. Nonetheless, central nervous system (CNS) projects are advancing at a 16.65% CAGR, buoyed by heightened public-health focus on mental-health disorders and neurodegenerative diseases. Many CNS assets involve modified-release or multiparticulate technologies, areas where Indian formulators possess deep know-how.

Cardiovascular and anti-infective volumes remain significant but face generics competition that dampens price points. Diversification into orphan indications and immunology is gathering pace as sponsors chase fast-track regulatory pathways. CDMOs that combine high-potency suites with flexible packaging for personalized dosing forms are well placed to secure longer contracts. Regulatory familiarity with class-IV APIs and Schedule H1 substances adds another layer of differentiation for Indian partners.

By Manufacturing Scale: Clinical Supply Demand Rises Amid Commercial Base

Commercial lots still constitute 62.32% of 2024 revenue, reflecting the ongoing need to serve global blockbusters and mature generics at scale. Decades-old campuses with multi-product trains sustain low cost-per-unit metrics and provide bulk volumes to global distribution centers. However, clinical manufacturing revenues are expanding swiftly at 15.12% CAGR, driven by record trial activity and biotech-heavy pipelines. Sponsors favor CDMOs able to pivot from small Phase I lots to Phase III scales without plant changeovers, reducing tech-transfer risks.

Sai Life Sciences’ recent clinical-suite ramp-up exemplifies this strategy, offering segregated Grade C/D rooms and adaptive single-use flow paths. Pre-clinical demand, though smaller, cements early-stage relationships that can blossom into decade-long supply deals. To capture heightened clinical activity, Indian CDMOs are integrating Quality by Design protocols and digital batch records to cut regulatory review times. The resulting full-lifecycle proposition positions India favorably in global outsourcing matrices.

Geography Analysis

Telangana dominates the India contract manufacturing organization market through an ecosystem that blends policy incentives, academic linkages, and real-estate readiness. The state’s Green Pharma City spans 19,000 acres and hosts six anchor investors committing INR 5,260 crore (USD 632 million) to integrated plants with shared utilities, effluent treatment, and warehouse clusters. Hyderabad alone employs over 560,000 pharma professionals, ensuring readily available talent. Adjacent research institutes facilitate continuous technology transfer, elevating innovation density.

Gujarat retains an indispensable role, especially for APIs, thanks to historical chemical-industry roots and port access that accelerates export cycles. Ankleshwar and Vadodara parks provide common effluent plants and bonded logistics zones, supporting cost-efficient scale-up. Several multinationals maintain dedicated campuses here, leveraging seamless raw-material imports from proximate petrochemical complexes. Andhra Pradesh is fast emerging as a biologics node, benefiting from dedicated bulk-drug parks under the PLI umbrella and favorable land-lease terms.

Maharashtra, anchored by Mumbai and Pune, skews toward research, formulation development, and corporate headquarters. Its dense venture-capital network finances emerging CDMOs and supports clinical research organizations that feed into manufacturing contracts elsewhere. Karnataka’s Bangalore cluster adds digital-health and AI prowess, enriching process-development capabilities for statewide plants. Collectively, these regional strengths create a distributed yet integrated national manufacturing grid that clients can leverage to mitigate single-site risk, reinforcing the India contract manufacturing organization market’s resilience.

Competitive Landscape

The India contract manufacturing organization market exhibits moderate concentration, with scale-intensive incumbents sharing space with nimble specialists. Divi’s Laboratories, Dr. Reddy’s, and Sun Pharma command sizeable revenue bases built on vertically integrated chemistry, multi-regulatory approvals, and long-tenure client rosters. Their operational breadth spans APIs to finished dosage, allowing one-stop engagements that attract big-pharma volumes. These leaders are sinking capital into biologics modules, advanced aseptic lines, and digital quality systems to defend margins against emerging rivals.

Venture-backed players such as Aragen Life Sciences and Maiva Pharma are disrupting with focused value propositions in discovery support, high-potency formulations, and cell-line development. Their lighter asset structures and rapid decision cycles resonate with virtual sponsors pursuing speed to clinic. Strategic alliances with AI vendors and cloud-based quality-management providers amplify their process-efficiency claims, enabling bids for complex, high-margin projects traditionally reserved for global CDMOs.

Technology is the battlefield for differentiation. AI-enabled predictive analytics, continuous-manufacturing skids, and single-use bioreactors are becoming table stakes. Quality culture remains the ultimate gatekeeper; firms receiving zero-483 observations post-inspection convert that clean track record into premium pricing. Consolidation pressures linger in oversupplied oral-solid dosage capacity, and distressed assets may change hands, further altering market structure. Ultimately, those blending scale, specialization, and impeccable compliance are positioned to gain share in the evolving India contract manufacturing organization market.

India Contract Manufacturing Organization (CMO) Industry Leaders

Divi’s Laboratories Limited

Dr. Reddy’s Laboratories Limited

Sun Pharmaceutical Industries Limited

Aurobindo Pharma Limited

Zydus Lifesciences Limited (Cadila Healthcare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Divi’s Laboratories commissioned its new Kakinada manufacturing facility with investments exceeding INR 1,200 crore (USD 144 million), adding significant capacity for complex API manufacturing and positioning the company for enhanced market share in high-value pharmaceutical intermediates.

- January 2025: Aurigene Pharmaceutical Services inaugurated a 70,000-square-foot biologics facility in Genome Valley, Hyderabad, specifically designed for mammalian cell culture and monoclonal antibody production, marking a strategic expansion into the high-growth biologics manufacturing segment.

- January 2025: Aragen Life Sciences secured USD 100 million in funding from Quadria Capital, representing one of the largest CDMO funding rounds in Indian pharmaceutical history and enabling the expansion of specialized manufacturing capabilities for global pharmaceutical partners.

- December 2024: Telangana Government signed MoUs with six major pharmaceutical companies (MSN Laboratories, Laurus Labs, Gland Pharma, Dr. Reddy's, Aurobindo, Hetero Drugs) for INR 5,260 crore (USD 632 million) investments in Green Pharma City, creating an integrated pharmaceutical manufacturing ecosystem.

India Contract Manufacturing Organization (CMO) Market Report Scope

Contract manufacturing organizations (CMOs) assist pharmaceutical and biotechnology firms in producing cutting-edge drug substances. CMOs typically offer various services, including commercial production, drug development, formal stability assessments, formulation development, etc. The market study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

India Contract Manufacturing Organization is Segmented by Service Type (API and Intermediates and Finished Dose). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for the Above Segments.

| API and Intermediates | |

| Finished Dose | Solids |

| Liquids | |

| Semi-solids and Injectables |

| Small Molecules |

| Large Molecules / Biologics |

| Big Pharma |

| Mid-Size Pharma |

| Virtual / Start-ups |

| Oncology |

| Cardiovascular |

| Anti-infectives |

| Central Nervous System (CNS) |

| Other Therapeutic Areas |

| Pre-clinical |

| Clinical |

| Commercial |

| By Service Type | API and Intermediates | |

| Finished Dose | Solids | |

| Liquids | ||

| Semi-solids and Injectables | ||

| By Molecule Type | Small Molecules | |

| Large Molecules / Biologics | ||

| By End-user | Big Pharma | |

| Mid-Size Pharma | ||

| Virtual / Start-ups | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| Anti-infectives | ||

| Central Nervous System (CNS) | ||

| Other Therapeutic Areas | ||

| By Manufacturing Scale | Pre-clinical | |

| Clinical | ||

| Commercial | ||

Key Questions Answered in the Report

How large is the India contract manufacturing organization market in 2026?

The India contract manufacturing organization market size stands at USD 29.53 billion in 2026.

What is the expected CAGR for contract drug manufacturing in India through 2031?

Revenue is forecast to increase at a 14.43% CAGR between 2026 and 2031.

Which service category leads current revenues?

API and intermediates hold 51.78% of 2025 revenue, maintaining leadership over finished dose services.

Which segment is expanding the fastest by molecule type?

Large molecules/biologics are projected to grow at a 15.26% CAGR, challenging small-molecule dominance.

Why is Hyderabad critical to pharmaceutical outsourcing?

Hyderabad hosts the 19,000-acre Green Pharma City, dense talent pools, and recent multinational investments, making it the country’s most integrated manufacturing hub.

What challenges could slow growth for Indian CDMOs?

Supply volatility from China-sourced raw materials and heightened FDA scrutiny pose near-term headwinds that can compress margins and delay exports.

Page last updated on: