Agriculture CRO Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

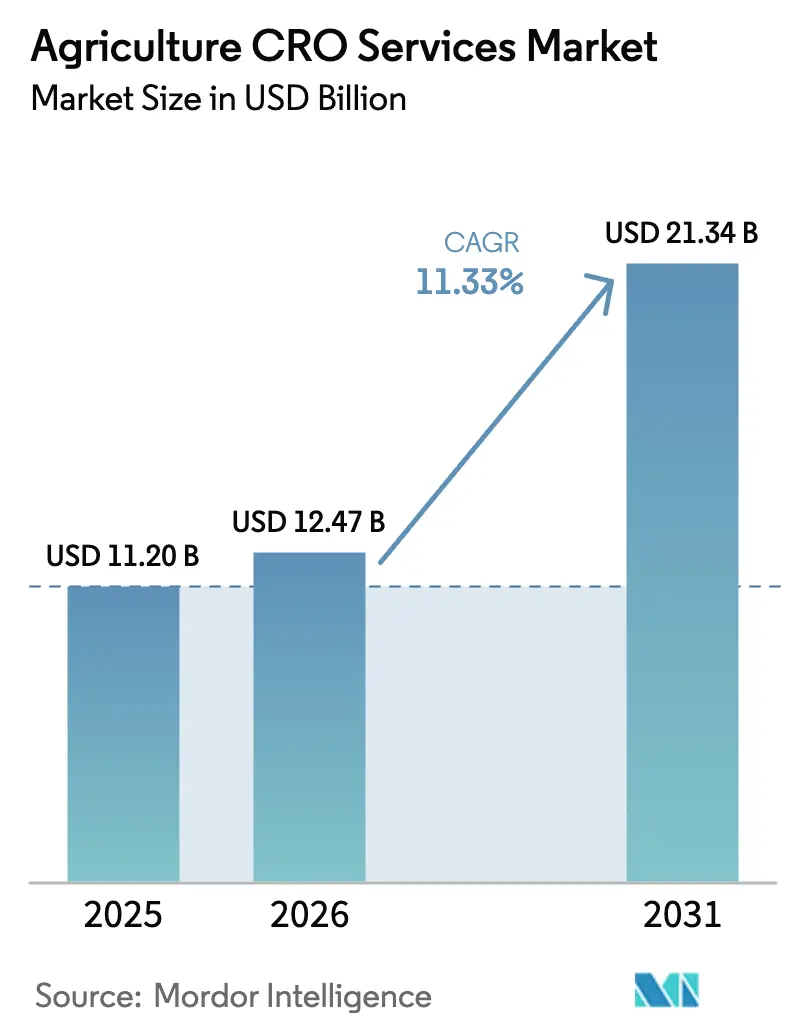

| Market Size (2026) | USD 12.47 Billion |

| Market Size (2031) | USD 21.34 Billion |

| Growth Rate (2026 - 2031) | 11.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agriculture CRO Services Market Analysis by Mordor Intelligence

The Agriculture CRO Services market size was valued at USD 11.20 billion in 2025 and estimated to grow from USD 12.47 billion in 2026 to reach USD 21.34 billion by 2031, at a CAGR of 11.33% during the forecast period (2026-2031). This growth is driven by agrochemical manufacturers increasingly outsourcing their research and development operations, as the cost of discovering a single active ingredient now exceeds USD 300 million, making in-house research financially challenging[1]Source: Food and Agriculture Organization, “Agricultural Investment and Finance,” FAO.ORG. The implementation of complex regulatory requirements, including the United States Environmental Protection Agency's 2024 biotechnology coordination framework requiring multi-agency data submissions, has increased the demand for specialized compliance services[2]Source: United States Department of Agriculture, “Biotechnology Annual Report 2024,” USDA.GOV. North America holds the largest market share due to its strict registration requirements, while the Asia-Pacific region shows the highest growth rate, driven by agricultural modernization and expanding export markets. The regulatory services segment demonstrates the strongest growth, as biologicals and gene-edited crops require comprehensive documentation and specialized expertise. The market remains fragmented, with the top five providers accounting for a minority of total revenue. This structure creates opportunities for regional specialists to develop expertise in emerging areas such as carbon credit verification and precision agriculture validation.

Key Report Takeaways

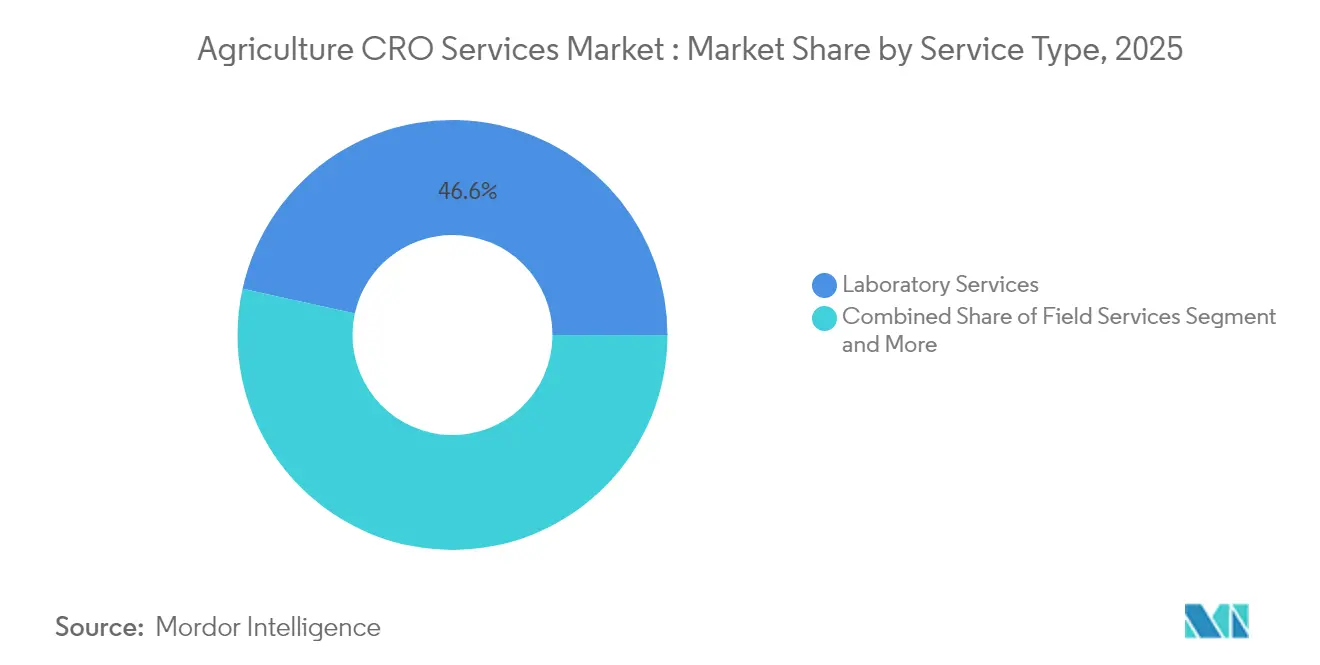

- By service type, laboratory services led with 46.55% of the agriculture CRO services market share in 2025, while regulatory services are projected to register a 12.64% CAGR through 2031.

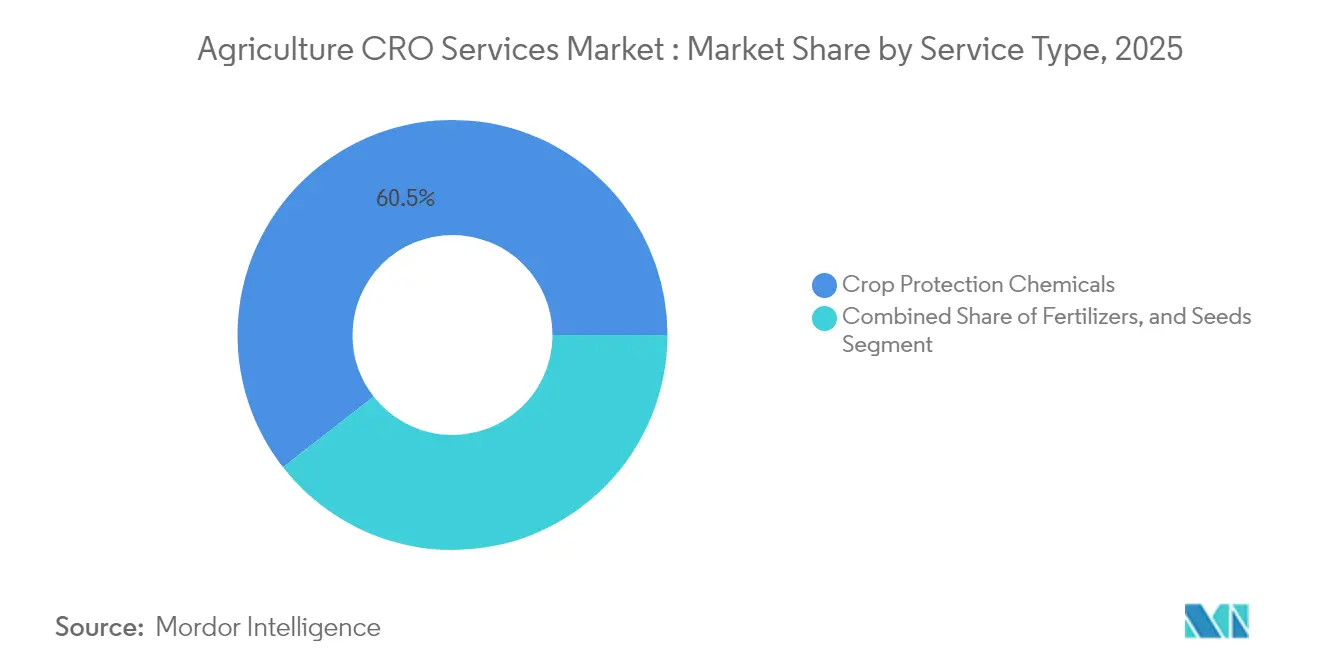

- By sector, crop protection chemicals accounted for 60.55% of the agriculture CRO services market size in 2025 and are projected to expand at a 12.36% CAGR through 2031.

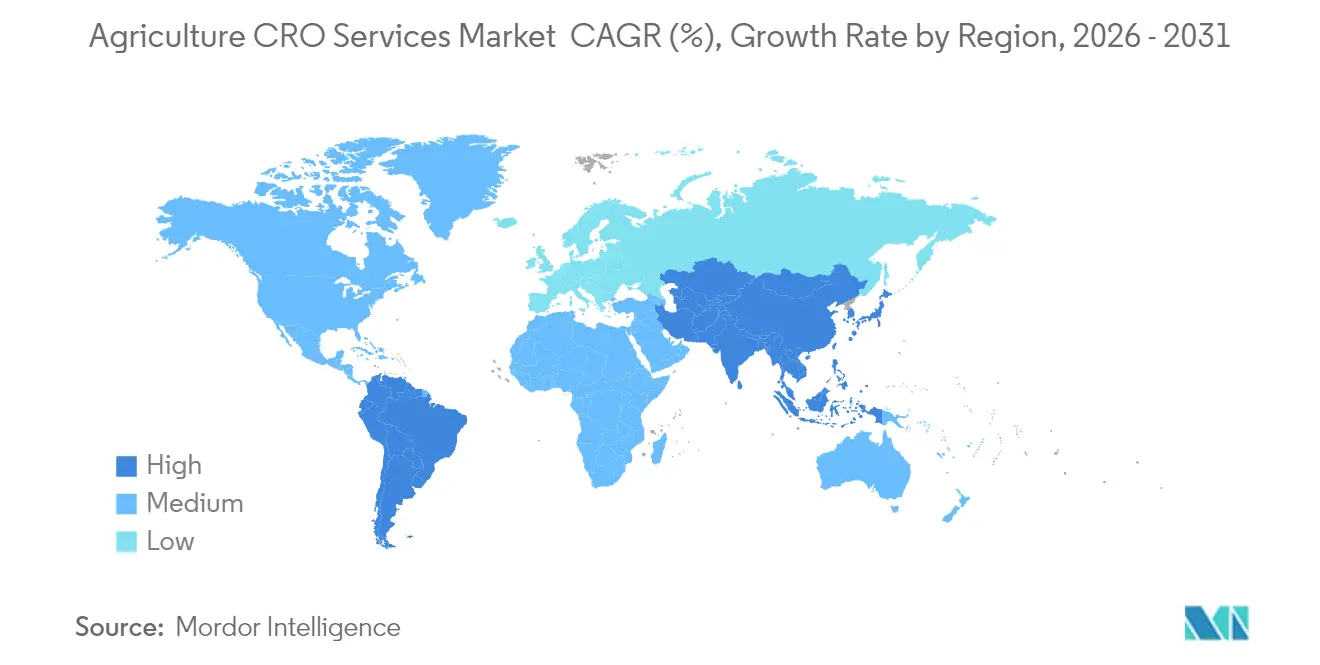

- By geography, North America held a 54.10% revenue share in 2025, while the Asia-Pacific region is forecast to deliver the highest regional CAGR of 12.11% through 2031.

- Eurofins Scientific SE, SGS SA, Charles River Laboratories International Inc., ERM International Group Limited, and Exponent Inc. hold a significant market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agriculture CRO Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising research and development outsourcing to contain soaring discovery costs | +2.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Regulatory tightening drives demand for third-party compliance expertise | +2.0% | Global, peak in North America and European Union | Short term (≤ 2 years) |

| Growth in biologicals and biosolutions requiring new efficacy trials | +1.9% | Global, led by South America and Asia-Pacific | Medium term (2-4 years) |

| Precision agriculture and digital farming tools need validation studies | +1.5% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift to data-driven portfolio optimization by agrochemical majors | +1.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Venture funding surge for ag-tech start-ups lacking in-house trial capacity | +1.1% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Research and Development Outsourcing to Contain Soaring Discovery Costs

Rising discovery costs are driving agrochemical companies to outsource non-core scientific activities. Bayer's 2024 filings demonstrate this trend, as the Crop Science division faces challenges despite the group's total research expenditure of EUR 5,860 million (USD 6,446 million). Contract Research Organization (CRO) partnerships reduce time-to-market by up to two years, enhancing returns on research investment. Companies depend on external partners for specialized services such as advanced toxicology, multi-site field trials, and predictive modeling, avoiding substantial internal infrastructure costs. Global competition emphasizes the importance of efficient capital allocation, supporting continued outsourcing growth. These dynamics increase the demand for agricultural CRO services, ranging from initial discovery screening to regulatory submission.

Regulatory Tightening Drives Demand for Third-Party Compliance Expertise

The Environmental Protection Agency's 2024 framework requires applicants to incorporate data requirements from the Environmental Protection Agency, the Food and Drug Administration, and the United States Department of Agriculture, thereby increasing dossier complexity and compliance costs. International regulatory changes include Argentina's National Service of Agri-Food Health and Quality (SENASA) Resolution 1081/2024, which updated testing protocols while maintaining strict technical requirements[3]Source: SENASA Argentina, “Resolution 1081/2024,” SENASA.GOB.AR. Companies work with specialized CRO regulatory teams to comply with regulations on formulations, microbials, and gene-edited seeds. The selection of CRO partners now depends heavily on their expertise in Good Laboratory Practice, dossier harmonization, and multi-jurisdiction submissions. As a result, regulatory consulting has become the fastest-growing service segment in the agriculture CRO services market.

Growth in Biologicals and Biosolutions Requiring New Efficacy Trials

Biological products generated USD 827 million in Brazil during the 2022-2023 season, demonstrating increased adoption across South American fruit and specialty crop systems. The evaluation of biological products requires specialized trial designs that assess beneficial insect compatibility, soil microbiome impacts, and product persistence throughout the growing season. Regulatory agencies require comparative studies between biological products and conventional synthetic pesticides, which increases trial complexity. Contract Research Organizations (CROs) with microbial testing laboratories and bioassay capabilities are well-positioned to conduct these studies. The agriculture CRO services market is expanding due to broader trial requirements that evaluate integrated pest management approaches combining chemical and biological solutions.

Shift to Data-Driven Portfolio Optimization by Agrochemical Majors

Agrochemical companies optimize their product pipelines by selecting molecules that offer the best risk-adjusted returns. This approach necessitates extensive screening, toxicology assessment, and data analytics that exceed internal capabilities. Contract Research Organizations (CROs) provide cloud platforms, statistical analysis, and decision frameworks to facilitate go-no-go decisions. Organizations benefit from external expertise and operational flexibility without fixed cost commitments, establishing sustained partnerships throughout the drug development process.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of good laboratory practice qualified field sites in key geographies | -0.9% | Global, acute in Asia-Pacific and South America | Medium term (2-4 years) |

| Privacy and cyber-security breaches undermining sponsor confidence | -0.7% | Global, concentrated in digitally advanced markets | Short term (≤ 2 years) |

| Rising cost of liability insurance for field-testing live plots | -0.6% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Weather-related trial failures increasing project risk and cost | -0.5% | Global, intensifying in climate-vulnerable regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Good Laboratory Practice Qualified Field Sites in Key Geographies

The demand for compliant test plots exceeds supply, creating waiting periods for sponsors seeking access to limited testing capacity. Obtaining certifications from organizations such as International Accreditation New Zealand (IANZ) or Australia's National Association of Testing Authorities (NATA) requires a three-year process and substantial investments in data systems, analytical equipment, and personnel training[4]Source: Institute of Accreditation New Zealand, “Laboratory Accreditation Services,” IANZ.GOVT.NZ. The restricted availability of certified facilities extends project timelines and increases costs for multi-location trials, constraining the agriculture CRO services market. Biological research faces additional challenges due to requirements for containment facilities and microbial monitoring capabilities, which are absent in most field stations.

Privacy and Cyber-Security Breaches Undermining Sponsor Confidence

CROs manage sensitive data, including genetic sequences, formulation details, and strategic documents with significant commercial value. Recent cybersecurity incidents in the life sciences industry have raised concerns among sponsors about data protection by external partners. To address these concerns, CROs must implement robust security measures such as data encryption, zero-trust security frameworks, and thorough employee screening processes. These security requirements increase operational costs, creating financial challenges for smaller CROs and potentially reducing the number of service providers in the agriculture CRO services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Laboratory Services Dominate and Regulatory Services Accelerate

Laboratory testing held 46.55% of the agriculture CRO services market share in 2025, driven by its essential functions in residue analytics, environmental fate modeling, and efficacy confirmation. Sponsors utilize chromatography, mass spectrometry, and molecular diagnostics to meet registration requirements. Eurofins Scientific increased its laboratory capacity by 98,000 square meters in 2024 to address higher throughput demands, despite experiencing a 10% decline in agrosciences revenue due to temporary client budget constraints. The integration of digital informatics and automated sample processing has become standard practice, reducing data processing time and enhancing the operational efficiency of global providers. The concentration of analytical infrastructure reinforces this segment's dominant position in the agriculture CRO services market.

Regulatory consulting services are projected to grow at a 12.64% CAGR through 2031, driven by increasing dossier complexity. The development of biologicals and gene-edited crops requires comprehensive submissions addressing mode of action, microbiome effects, and socio-economic risks. CROs with diverse teams encompassing toxicology, environmental sciences, and legal policy expertise are securing more contracts. SGS's Farm Sustainability Assessment program demonstrates this service integration by combining laboratory analysis with compliance verification and certification audits. Regional specialists maintain strong relationships with local regulators, indicating that expertise remains competitive with scale advantages in this expanding segment of the agriculture CRO services market.

By Sector: Crop Protection Chemicals Lead with Biologicals Convergence

Crop protection chemicals account for 60.55% of the agriculture CRO services market size in 2025, driven by stewardship requirements and ongoing discovery of resistance-breaking active ingredients. The segment maintains a 12.36% CAGR through 2031 as manufacturers validate integrated pest management protocols that combine chemical and biological controls. Field trials now focus on evaluating interactions between new active ingredients and microbial inoculants across multiple treatment types and locations. Major CROs, including Eurofins, Charles River Laboratories, and SynTech Research, have expanded their phytotoxicity, residue, and ecotoxicology testing capabilities to address these requirements.

The fertilizer and seed segments show strong growth due to advances in sustainability and trait development. New nutrient formulations, such as those from ICL Group Custom Ag Formulators, require extensive testing for compatibility across soil types and irrigation systems. Seed companies using CRISPR (Clustered Regularly Interspaced Short Palindromic Repeats) technology rely on genotype verification, phenotype evaluation, and environmental interaction studies, frequently conducted by specialized biotechnology CROs. These developments highlight how the agriculture CRO services market increasingly combines chemistry, biology, and genomics expertise in comprehensive testing programs, driving demand across all market segments.

Geography Analysis

North America holds 54.10% of the agriculture CRO services market share in 2025. The region's strength stems from the Environmental Protection Agency's multi-agency biotech framework, United States Department of Agriculture innovation grants, and precision farming implementation across millions of hectares. Canada's regulatory alignment and Mexico's planned glyphosate transition expand the diversity of research projects. The collaboration between Corteva and John Deere for digital agriculture validation strengthens CRO bookings, while carbon sequestration measurement under farm bill incentives creates additional revenue opportunities in sustainability verification.

Asia-Pacific demonstrates the highest growth rate at 12.11% CAGR. The region's expansion is supported by China's biotechnology regulation updates and India's export compliance requirements. Government modernization initiatives and increased venture funding facilitate early-stage biological testing. While accreditation challenges remain, the implementation of regional Good Laboratory Practices frameworks and drought resilience initiatives, including Australia's USD 40.3 million program, is reducing capacity limitations. The widespread adoption of sensor-based agronomy solutions in Southeast Asia increases the demand for third-party validation services.

Europe and South America exhibit different but complementary growth trajectories. European growth is driven by the Green Deal and Farm to Fork initiatives, generating demand for biological efficacy testing, carbon footprint verification, and circular nutrient research. South America excels in biological crop protection, with Brazil's biologicals market requiring specialized trials comparing microbial products to chemical alternatives. Argentina's relaxed laboratory selection policies attract international CROs while maintaining rigorous data requirements, demonstrating the market's regulatory evolution.

Competitive Landscape

The agriculture CRO services market demonstrates moderate concentration, with Eurofins Scientific SE, SGS SA, Charles River Laboratories International Inc., ERM International Group Limited, and Exponent Inc. holding a significant market share in 2024. Eurofins Scientific experienced a decline of more than 10% in Q3 2024 Agrosciences revenue, indicating market sensitivity to client spending patterns. SGS reported sales of CHF 6,794 million (USD 7,473 million) in 2024, strengthened by eleven acquisitions that enhanced its analytical capabilities and geographic presence. Charles River Laboratories utilizes its life sciences expertise through biotechnology assays and toxicology packages for seed and biological developers.

Strategic consolidation continues in the market. SynTech Research expanded its European field capacity, while LabAnalysis acquired Ibacon in July 2024 to enhance regulatory toxicology capabilities. Competitive positioning is influenced by technological integration as providers implement digital data capture, remote sensing, and automated analytics to reduce cycle times and improve accuracy. In the agriculture CRO services market, CROs with multi-country Good Laboratory Practice certification, integrated laboratory and regulatory services, and data-science-enhanced insights attract sponsors managing global launch campaigns.

Specialized service segments present growth opportunities. The biological testing segment remains underserved, with demand exceeding supply for microbial identification, fermentation analytics, and entomology bioassays. Precision agriculture validation, combining agronomy with data science, faces capacity constraints, leading to new entrants such as Crop.Zone to collaborate with equipment dealers for on-farm demonstrations. Carbon credit verification is rapidly expanding, with SustainCERT and Agreena securing early projects to certify soil carbon across millions of hectares. These specialized segments demonstrate how focused providers can establish strong positions against larger competitors, contributing to moderate industry concentration.

Agriculture CRO Services Industry Leaders

Eurofins Scientific SE

SGS SA

Charles River Laboratories International, Inc.

ERM International Group Limited

Exponent, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SCS Global Services verified the CNG AgriCarbon Rewards Programme Project in South Africa under Verra methodology VM0042, the first agriculture land management carbon offset in Africa, underscoring growing sustainability verification demand in emerging markets.

- January 2025: Staphyt acquired three subsidiaries of Héliantis Group, a French company specializing in agricultural seed testing and production. This acquisition strengthens Staphyt's position as a European leader in agricultural research and expands its capacity to provide agronomic research services to clients.

- July 2024: LabAnalysis, a provider of analytical services in Europe for agro, acquired Ibacon GmbH, a contract research organization specializing in ecotoxicological and chemical studies under Good Laboratory Practice (GLP). The acquisition enables LabAnalysis to expand its service offerings and market presence for the registration of agrochemical, biocidal, pharmaceutical, and REACH products.

- March 2024: Charles River Laboratories International, Inc. launched the Charles River Incubator Program (CIP) to support early-stage biotechnology companies in the discovery, development, and phase-appropriate manufacturing of advanced therapies.

Global Agriculture CRO Services Market Report Scope

Agriculture CRO services are opted for by agriculture input manufacturers on a contract basis for conducting research and development activities to enhance their operations, products, services, and business.

The Agriculture CRO Services Market is Segmented by Service Type (Field Services, Laboratory Services, Regulatory Services, and Other Services), Sector (Crop Protection Chemicals, Fertilizers, and Seeds), and Geography (North America, Europe, Latin America, and Africa). The Report Offers the Market Sizes and Forecasts in Value (USD) for the Above Segments.

| Field Services |

| Laboratory Services |

| Regulatory Services |

| Other Services (Product Development Services, Precision Agriculture Services, Seed Services, etc.) |

| Crop Protection Chemicals |

| Fertilizers |

| Seeds |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Service Type | Field Services | |

| Laboratory Services | ||

| Regulatory Services | ||

| Other Services (Product Development Services, Precision Agriculture Services, Seed Services, etc.) | ||

| By Sector | Crop Protection Chemicals | |

| Fertilizers | ||

| Seeds | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the agriculture CRO services market by 2031?

The market is forecast to reach USD 21.34 billion by 2031, reflecting an 11.33% CAGR during 2026-2031.

Why is Asia-Pacific considered the fastest-growing region?

Agricultural modernization, export-oriented compliance needs, and rising biologicals adoption lift the region at a 12.11% CAGR through 2031.

What factors are driving increased demand for regulatory consulting services?

Complex multi-agency frameworks for biologicals, gene-edited crops, and evolving formulation rules require expert dossier preparation and regulatory strategy.

Which emerging niche offers growth opportunities beyond traditional field and laboratory studies?

Carbon credit verification and precision agriculture validation present promising high-margin opportunities as sustainability and data-driven farming expand.

Page last updated on: