Biopharmaceuticals Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

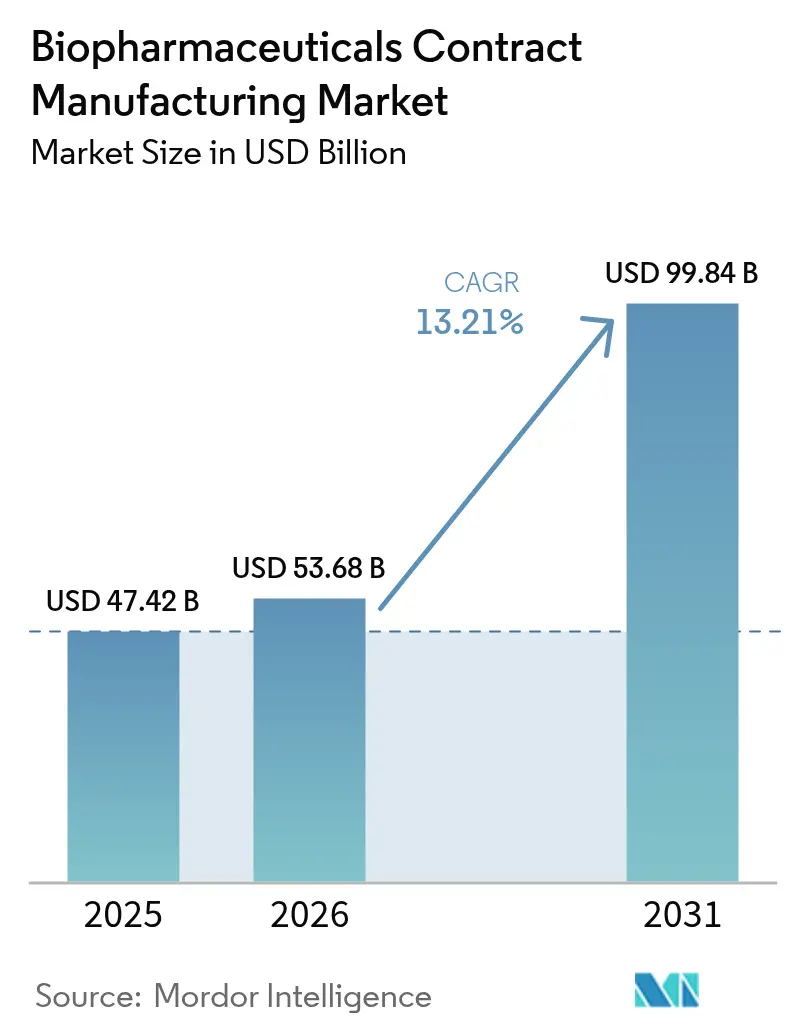

| Market Size (2026) | USD 53.68 Billion |

| Market Size (2031) | USD 99.84 Billion |

| Growth Rate (2026 - 2031) | 13.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biopharmaceuticals Contract Manufacturing Market Analysis by Mordor Intelligence

Biopharmaceuticals contract manufacturing market size in 2026 is estimated at USD 53.68 billion, growing from 2025 value of USD 47.42 billion with 2031 projections showing USD 99.84 billion, growing at 13.21% CAGR over 2026-2031. This advancement outpaces the wider pharmaceutical sector because large sponsors are accelerating outsourcing to conserve capital and tap specialized expertise. Growth is amplified by the unrelenting expansion of biologic and biosimilar pipelines, rapid commercial uptake of single-use production systems, and widening capacity gaps for cell and gene therapy vectors. Geographic demand is broad-based, yet North America holds sway through its entrenched biotech clusters, while Asia Pacific posts the quickest gains as multinationals execute China-plus-one sourcing strategies. Technology investments in AI-driven predictive control, continuous bioprocessing, and modular facilities lift yields and compress timelines, sharpening the competitive edge of digital-first CDMOs.

Key Report Takeaways

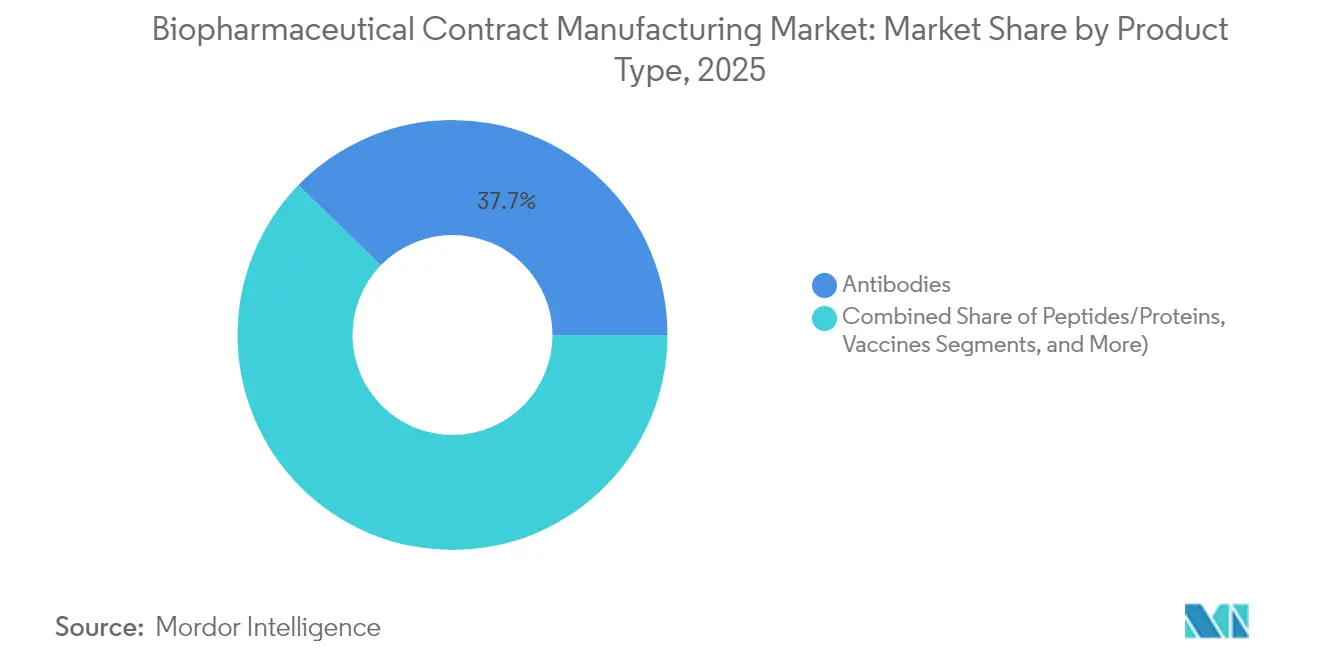

- By product type, antibodies led with 37.74% of biopharmaceuticals contract manufacturing market share in 2025, while cell and gene therapy vectors are forecast to expand at an 17.76% CAGR to 2031.

- By service type, cGMP drug substance manufacturing held 41.85% revenue share in 2025; process development services carry the highest projected CAGR at 16.45% through 2031.

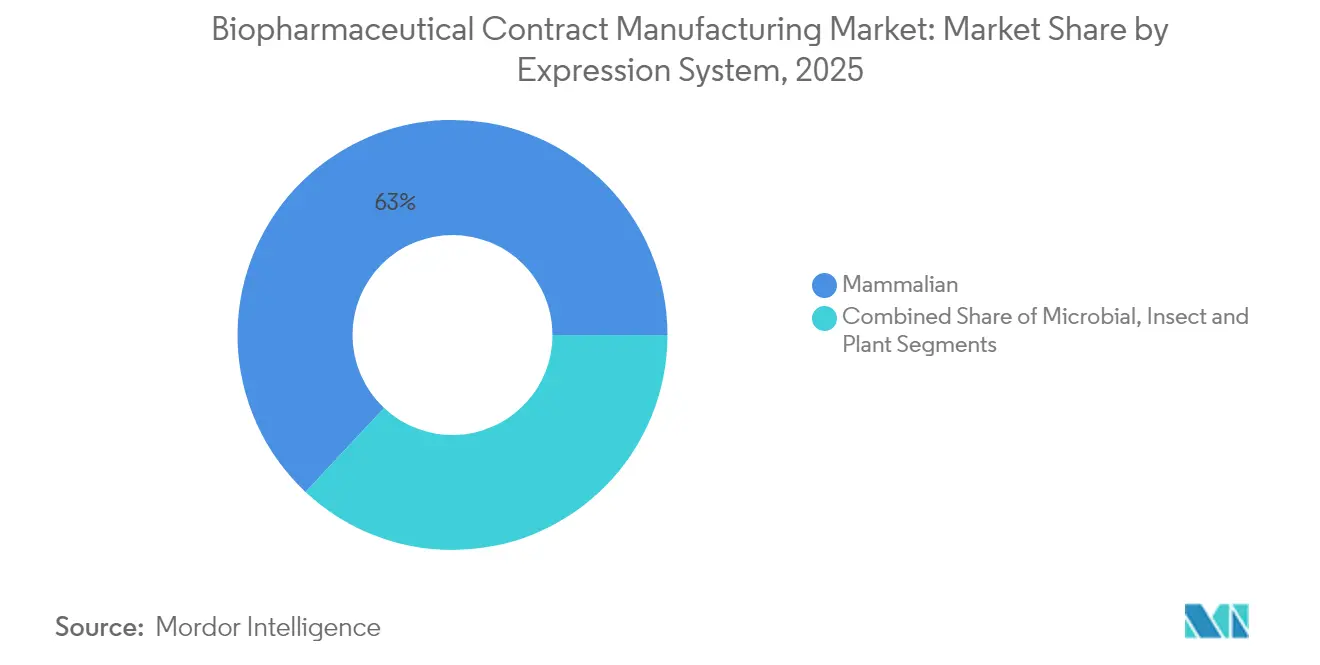

- By expression system, mammalian platforms accounted for 63.02% share of the biopharmaceuticals contract manufacturing market size in 2025 and are advancing at a 14.36% CAGR through 2031.

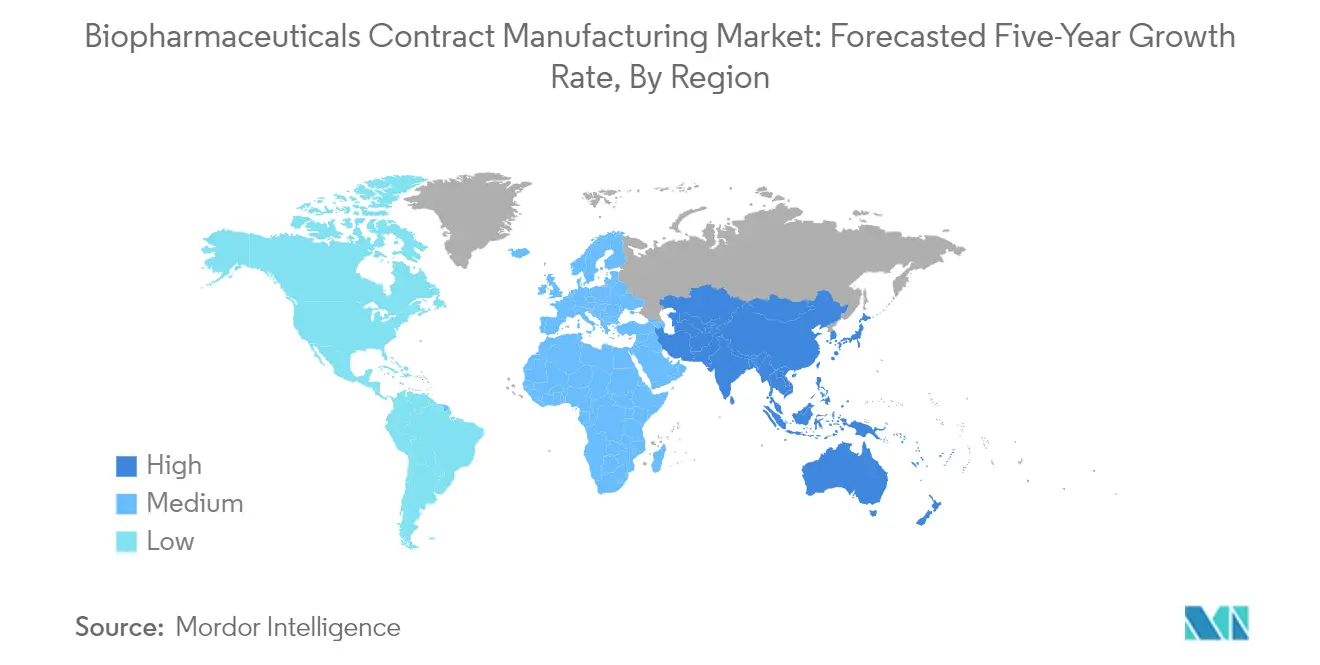

- By geography, North America captured 36.25% of the biopharmaceuticals contract manufacturing market in 2025, while Asia Pacific records the fastest regional CAGR at 11.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biopharmaceuticals Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of biologics / biosimilar pipelines | +3.20% | Global with APAC acceleration | Long term (≥ 4 years) |

| Outsourcing surge among large bio-pharma sponsors | +2.80% | Global, particularly North America & Europe | Medium term (2–4 years) |

| Adoption of single-use & modular bioprocess skids | +2.10% | North America & EU; expanding to APAC | Short term (≤ 2 years) |

| Capacity gap for cell- & gene-therapy vectors | +1.90% | North America & EU core markets | Medium term (2–4 years) |

| China-plus-one procurement shift benefiting Korean/EU CDMOs | +1.40% | APAC core, spill-over to EU | Short term (≤ 2 years) |

| AI-driven predictive bioprocess control boosting yield | +1.20% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Surge Among Large Bio-Pharma Sponsors

The proportion of developers outsourcing at least one major activity rose to 86.9% in 2024 as firms sought flexibility and capital efficiency. Sponsors increasingly turn to CDMOs for complex modalities such as antibody-drug conjugates and autologous cell therapies that require niche expertise and rigorous regulatory stewardship. Outsourcing also shortens clinical timelines, with integrated providers offering process development, analytics, and commercial scale-up under a single quality system. Capacity reservations tied to multi-year master service agreements have become the norm, ensuring priority access as pipeline demand surges. Together, these forces embed the CDMO partnership model firmly within corporate manufacturing strategies, reinforcing the growth trajectory of the biopharmaceuticals contract manufacturing market.

Rapid Expansion of Biologics / Biosimilar Pipelines

More than 700 gene-based therapies and 450 biosimilar molecules are advancing through global development programs in 2025. Small and mid-sized innovators rarely possess industrial-scale capability, so they depend on external manufacturers that bring cell-culture know-how, global regulatory track records, and agility to pivot among regional filings. Harmonized guidelines across the United States, Europe, and key Asia Pacific jurisdictions further reward CDMOs with multinational site networks. As biologics complexity rises, differentiated purification, formulation, and delivery technologies become critical value drivers, prompting deep collaboration and technology-transfer frameworks that embed CDMOs across the product life cycle.

Adoption of Single-Use & Modular Bioprocess Skids

Modern facilities outfitted with single-use bioreactors can lift overall volumetric capacity by 20% while trimming fixed costs by 40%, according to bioprocess benchmarking data.[1]BioProcess International, “Single-Use Systems Slash Biopharma Costs,” bioprocessintl.com Disposable flow-paths reduce cross-contamination risk, underpinning multiproduct suites that pivot quickly between campaigns. Off-the-shelf modular skids such as the FlexFactory platform arrive pre-validated, compressing green field build times by 70% and cutting carbon footprints by 55% compared with stainless-steel plants. These efficiencies resonate strongly with biosimilar developers focused on price competitiveness and with emerging-market sponsors facing stringent capital allocation hurdles.

Capacity Gap for Cell- & Gene-Therapy Vectors

Industry analyses peg vector manufacturing shortfalls at 500%, pushing lead times for qualified CMO slots to 18 months. Heavy investment is underway; examples include Fujifilm Diosynth’s USD 120 million Advanced Center for Gene Therapies in Texas, but demand still outruns supply. This scarcity incentivizes novel solutions such as allogeneic platforms aimed at scalable off-the-shelf therapies. In tandem, continuous perfusion processes are gaining traction to stretch bioreactor output. Developers now view strategic CDMO alliances as essential for locking in capacity and de-risking commercialization plans, cementing long-term revenue visibility for service providers across the biopharmaceuticals contract manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent cGMP & data-integrity compliance burden | –1.8% | Global, particularly stringent in EU & US | Long term (≥ 4 years) |

| Global shortage of skilled bioprocess engineers | –1.5% | Global, acute in developed markets | Medium term (2–4 years) |

| Sustainability pressure on single-use plastics | –0.9% | EU leading, expanding globally | Long term (≥ 4 years) |

| Over-building risk creating idle stainless & SU capacity | –0.7% | Global, concentrated in high-investment regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent cGMP & Data-Integrity Compliance Burden

Implementation of EU GMP Annex 1 heightens sterile-manufacturing requirements, compelling extensive contamination-control and quality monitoring upgrades. FDA warning letters in 2024 spotlighted governance lapses and software validation gaps, reinforcing regulators’ focus on ALCOA+ data principles. Smaller CDMOs face disproportionate financial pressure when deploying electronic batch-record systems, track-and-trace platforms, and advanced environmental monitoring. The compliance load can delay facility utilization, tempering short-term revenue growth even as it lifts long-term quality standards across the biopharmaceuticals contract manufacturing industry.

Global Shortage of Skilled Bioprocess Engineers

Cytiva’s 2025 industry index shows that only 20% of executives find talent acquisition straightforward for upstream and downstream roles. Digitalization intensifies the gap: 80% of manufacturers report mismatches between existing skills and biopharma 4.0 requirements. Singapore projects a 30% jump in executive-level vacancies by 2032, mirroring broader global trends. CDMOs counter with accelerated academies, apprenticeships, and partnerships with universities. Yet, near-term workforce scarcity constrains ramp-ups, nudging some sponsors to continue dual-sourcing or invest in captive capacity as a hedge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Antibodies Lead While Cell & Gene Therapies Surge

The antibodies segment generated 37.74% market share in 2025, cementing its role as the anchor modality for oncology and autoimmune indications. Continued clinical activity sustains high batch volumes, while process intensification lifts titers and economics. In parallel, biosimilar monoclonal antibodies stimulate incremental demand from cost-sensitive health systems in Latin America, Eastern Europe, and parts of Asia.

Cell and gene therapy vectors are expanding at an 17.76% CAGR due to the scarcity of GMP vector capacity, bespoke analytics, and stringent regulatory oversight, which combine to create high-margin opportunities for specialized CDMOs. Viral vector innovation, including next-generation AAV serotypes and non-viral delivery alternatives, deepens the service scope and accelerates convergence between development and manufacturing skill sets in the biopharmaceuticals contract manufacturing market.

By Service Type: Manufacturing Dominance with Development Acceleration

Mammalian expression platforms, chiefly CHO cells, held 63.02% of market share in 2025 as advances in cell-line engineering, vector design, and media optimization boost specific productivity, reinforcing this platform’s dominance for glycosylated proteins and complex mAbs.

Bacterial and yeast systems remain cost-efficient for simple recombinant proteins and enzymes, especially in emerging economies where pricing pressure is acute. Plant and insect cell technologies show promise for niche applications, yet regulatory familiarity limits broader adoption. Providers balance portfolios across systems to meet client needs while maximizing facility utilization, an increasingly important lever as single-use suites enable flexible switching between platforms.

By Expression System: Mammalian Systems Maintain Technology Leadership

Mammalian expression platforms, chiefly CHO cells, held 63.02% of market share in 2025 as advances in cell-line engineering, vector design, and media optimization boost specific productivity, reinforcing this platform’s dominance for glycosylated proteins and complex mAbs.

Bacterial and yeast systems remain cost-efficient for simple recombinant proteins and enzymes, especially in emerging economies where pricing pressure is acute. Plant and insect cell technologies show promise for niche applications, yet regulatory familiarity limits broader adoption. Providers balance portfolios across systems to meet client needs while maximizing facility utilization, an increasingly important lever as single-use suites enable flexible switching between platforms.

By Development Phase: Commercial Manufacturing Drives Growth

Commercial and Phase III projects represent the revenue backbone, providing predictable multi-year volume commitments that justify large-scale stainless or disposable bioreactor installations. Long-term supply agreements often incorporate technology-progress clauses to embed continuous improvement initiatives, safeguarding cost and quality competitiveness.

Pre-clinical and Phase I projects, however, fuel the future pipeline, with venture-backed startups outsourcing nearly all CMC activities to conserve cash. Rapid-turn proof-of-concept runs in 50–200 L single-use bioreactors bridge the data gap from discovery to IND filings. Phase II demand hinges on fast scale-up and validated analytical suites, emphasizing those CDMOs that offer end-to-end lifecycle management within one quality and digital infrastructure.

Geography Analysis

North America remained the largest regional contributor with a 36.25% biopharmaceuticals contract manufacturing market share in 2025, sustained by deep venture funding, advanced regulatory ecosystems, and dense talent pools in Boston-Cambridge and the San Francisco Bay Area. Capacity expansions such as Fujifilm Diosynth’s USD 3.2 billion North Carolina campus and WuXi Biologics’ Massachusetts site broaden service breadth and keep the region at the forefront of late-stage and commercial projects. Potential enactment of the BIOSECURE Act could reshape vendor selection by favoring domestic and allied suppliers, yet strong demand and diversified pipelines maintain robust outlooks across modalities.

Asia Pacific is the fastest-growing territory, advancing at an 11.18% CAGR to 2031. China’s regulatory reforms and infrastructure build-out elevate its status as a manufacturing option for early-stage runs, although geopolitical tensions influence dual-sourcing habits. South Korea’s Samsung Biologics commands global attention with a cumulative capacity of 784,000 L by 2025, underscoring the region’s ascent. India leverages cost advantages and English-language talent, while Singapore markets its stringent quality oversight and government incentives to capture advanced-therapy projects.

Europe sustains its position through incumbents such as Lonza, Boehringer Ingelheim, and Catalent, each reinforcing local ecosystems with billion-dollar investments in Switzerland, Germany, and Austria. The Vacaville acquisition adds 330,000 L of capacity to Lonza’s network, highlighting continued commitment despite Brexit-related supply chain complexity. EMA’s harmonized review pathways and robust IP protections entice U.S. and Asian clients seeking regulatory diversification. Collectively, mature infrastructure, automation initiatives, and green-manufacturing incentives place Europe firmly in the strategic plans of multinational sponsors evaluating the biopharmaceuticals contract manufacturing market.

Competitive Landscape

The market is moderately concentrated and in the midst of consolidation. Novo Holdings’ USD 16.5 billion takeover of Catalent stands as the largest CDMO transaction to date, marrying upstream biologics expertise with expansive fill-finish capabilities.

Leading players are recasting themselves as innovative partners rather than commodity manufacturers. Samsung Biologics’ S-Cellerate program integrates cell-line development, process optimization, and regulatory documentation to compress timelines. Lonza’s One Lonza framework unites biologics, advanced synthesis, and cell-and-gene platforms under uniform digital and quality systems. Technology investments in AI-enabled digital twins, continuous perfusion lines, and end-to-end electronic batch history improve productivity and reduce deviation rates, sharpening competitive differentiation across the biopharmaceuticals manufacturing market.

White-space opportunities cluster around antibody-drug conjugates and advanced viral vectors, both capital-intensive niches with steep learning curves. Disruptive entrants such as PAK BioSolutions target continuous bioprocessing with USD 12 million in seed funding, promising reductions in footprint and operating costs. Meanwhile, regional specialists leverage proximity advantages and tailored service offerings, for example, SK pharmteco’s peptide expansion in South Korea or Ardena’s move into U.S. drug-product manufacturing to carve defensible positions.

Biopharmaceuticals Contract Manufacturing Industry Leaders

Boehringer Ingelheim GmbH

Lonza Group

Samsung Biologics

WuXi Biologics

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ardena signed agreement to acquire advanced drug-product manufacturing facility from Catalent to expand U.S. footprint, enhancing capabilities in biopharmaceutical contract manufacturing.

- February 2025: WuXi Biologics partnered with Candid Therapeutics in a USD 925 million deal to advance trispecific T-cell engagers, leveraging the WuXiBody platform for multispecific antibody development.

- February 2025: SK Pharmateco invested USD 260 million in a new facility in Sejong, South Korea, to expand global small-molecule and peptide production. The facility will begin operations in late 2026 and create over 300 jobs.

- January 2025: Samsung Biologics signed a manufacturing agreement worth over USD 1.4 billion with a European pharmaceutical company through December 2030, with production at the Songdo, South Korea, site.

- December 2024: Novo Holdings completed the acquisition of Catalent for USD 16.5 billion, creating an integrated manufacturing powerhouse with over 50 global sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biopharmaceutical contract manufacturing market as all revenue earned by specialized CDMOs from producing drug substance and drug product for biologics, monoclonal antibodies, recombinant proteins, viral and non-viral vaccines, cell and gene therapy vectors, and biosimilars at clinical or commercial scale. These values reflect fees for process development, cGMP manufacturing, fill-finish, analytical testing, and integrated packaging that are booked by the CDMO, not by the sponsor firm.

Scope Exclusions: Small-molecule APIs, stand-alone pre-clinical CRO services, and pure distribution logistics lie outside this scope.

Segmentation Overview

- By Product Type

- Peptides/Proteins

- Antibodies (mAbs & ADCs)

- Vaccines

- Biosimilars

- Other Biologics

- By Service Type

- Process Development

- cGMP Drug Substance Manufacturing

- Fill-Finish & Lyophilization

- Analytical & QC Services

- Packaging & Logistics

- By Expression System

- Mammalian

- Microbial

- Insect & Plant

- By Development Phase

- Pre-clinical

- Phase I

- Phase II

- Phase III & Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews and short surveys with CDMO commercial leads, biologics CMC directors, regional regulators, and equipment vendors helped us verify typical mammalian culture batch sizes, clean room downtime norms, and future slot bookings. These conversations, spanning North America, Europe, and high-growth Asian hubs, also tested our price-volume assumptions before the model was frozen.

Desk Research

We began by mapping the global installed bioreactor base through open datasets from the US FDA Biologics License Application approvals, the EMA Community Register, World Health Organization vaccine pipeline tracker, and customs trade codes for HS 3002 and 3003. Capacity expansion press releases and SEC 10-K filings were screened on Dow Jones Factiva, while firm-level revenue splits came from D&B Hoovers. Industry position papers from groups such as IFPMA and the Biotechnology Innovation Organization supplied benchmark utilization rates and batch failure statistics.

Public domain figures underpin starting values; however, we also reference subscription sources (e.g., BioPlan annual capacity survey extracts) to validate average titers, single-use adoption, and prevailing fill-finish pricing. The sources listed serve as illustrations only; our analysts reviewed many additional documents to cross-check numbers, definitions, and regulatory context.

Market-Sizing & Forecasting

A top-down build starts with 2024 biologics production volumes by expression system, reconstructed from approval counts, average grams per dose, and commercial demand; these volumes are then multiplied by blended outsourcing penetration and median fee per gram. Selected bottom-up roll-ups, sampled CDMO revenue disclosures and channel checks, reconcile the totals. Key variables include: (1) global mAb clinical pipeline size, (2) average microbial titer improvements, (3) approved cell therapy batches, (4) single-use system penetration, and (5) biologics share of overall R&D spend. We forecast through 2030 using multivariate regression on these drivers, with scenario analysis around regulatory lead time and capacity addition slippage to capture upside and downside bounds.

Data Validation & Update Cycle

Outputs pass variance checks against historical CDMO margins, currency effects, and regional capacity announcements. A second analyst reviews anomalies; senior reviewers sign off only after discrepancies fall within predefined thresholds. The dataset refreshes each year, with interim updates triggered by material events such as major greenfield plants or sudden regulatory pauses.

Why Mordor's Biopharmaceutical Contract Manufacturing Baseline Stands Firm

Published estimates often disagree because each publisher chooses its own service mix, base year, and currency treatment before modeling future demand.

Key gap drivers include whether finished drug product services are counted, how pipeline attrition is modeled, the currency conversion date, and the frequency with which fresh capacity announcements are folded into the baseline. Mordor analysts capture both drug substance and drug product revenues, apply rolling 12-month average exchange rates, and refresh assumptions annually, whereas some peer studies lock inputs for multiple years or limit scope to mammalian drug substance alone.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 47.42 B | Mordor Intelligence | - |

| USD 44.73 B | Global Consultancy A | Excludes packaging and logistics; updates every two years |

| USD 19.00 B | Industry Journal B | Focuses only on mammalian drug substance fees and applies static EUR-USD rate from 2022 |

Taken together, the comparison shows that figures shrink when critical revenue streams or the latest capacity upgrades are left out. By capturing the full biologics value chain and keeping assumptions current, Mordor Intelligence provides a dependable, decision-ready baseline.

Key Questions Answered in the Report

How big is the Biopharmaceuticals Contract Manufacturing Market?

The Biopharmaceuticals Contract Manufacturing Market size is expected to reach USD 53.68 billion in 2026 and grow at a CAGR of 13.21% to reach USD 99.84 billion by 2031.

What is the current Biopharmaceuticals Contract Manufacturing Market size?

In 2026, the Biopharmaceuticals Contract Manufacturing Market size is expected to reach USD 53.68 billion.

Who are the key players in Biopharmaceuticals Contract Manufacturing Market?

Boehringer Ingelheim GmbH, JRS Pharma (Celonic), Lonza Group, Rentschler Biotechnologie GmbH and Inno Biologics Sdn Bhd are the major companies operating in the Biopharmaceuticals Contract Manufacturing Market.

Which is the fastest growing region in Biopharmaceuticals Contract Manufacturing Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Biopharmaceuticals Contract Manufacturing Market?

In 2025, the North America accounts for the largest market share in Biopharmaceuticals Contract Manufacturing Market.

What years does this Biopharmaceuticals Contract Manufacturing Market cover, and what was the market size in 2025?

In 2025, the Biopharmaceuticals Contract Manufacturing Market size was estimated at USD 53.68 billion. The report covers the Biopharmaceuticals Contract Manufacturing Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Biopharmaceuticals Contract Manufacturing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: