Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

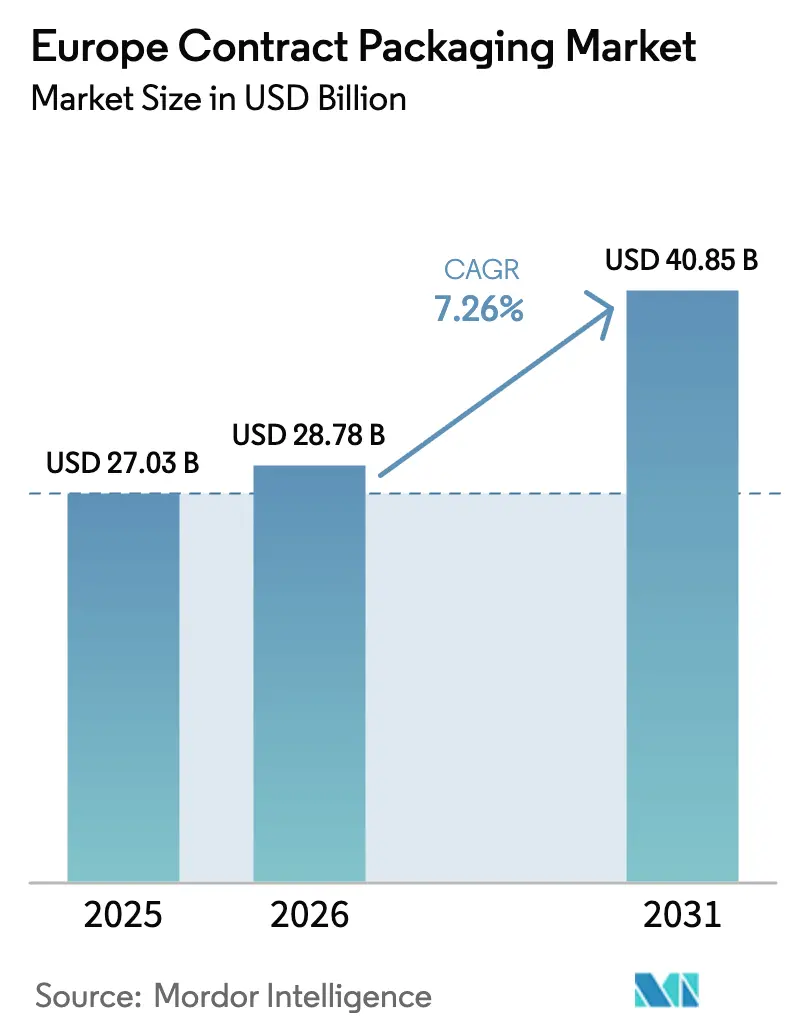

| Base Year Market Size (2025) | USD 27.03 Billion |

| Market Size (2026) | USD 28.78 Billion |

| Market Size (2031) | USD 40.85 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

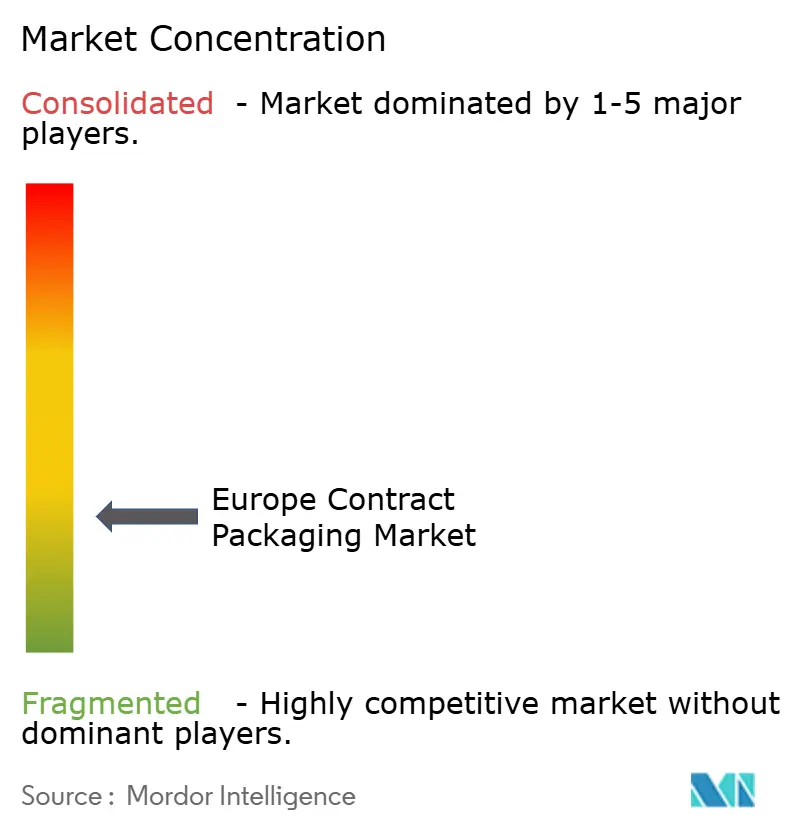

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Contract Packaging Market Analysis by Mordor Intelligence

The Europe contract packaging market size is expected to increase from USD 27.03 billion in 2025 to USD 28.78 billion in 2026 and reach USD 40.85 billion by 2031, growing at a CAGR of 7.26% over 2026-2031. The steady rise reflects the surge in outsourced fulfillment for e-commerce orders, the growing number of direct-to-consumer (DTC) brand launches, and retailers’ preference for shelf-ready packs that minimize in-store labor. Demand for mono-material solutions is accelerating as producers strive to comply with the European Union's Packaging Waste Directive, while short-run digital printing enables rapid SKU changes without prohibitive plate costs. Post-Brexit supply-chain near-shoring is concentrating volumes within continental co-packing hubs, which, in turn, is stimulating investments in semi- and fully automated lines. Competitive intensity is increasing as logistics players, converters, and specialized co-packers vie for fast-growing, value-added projects, especially in food and cosmetics.

Key Report Takeaways

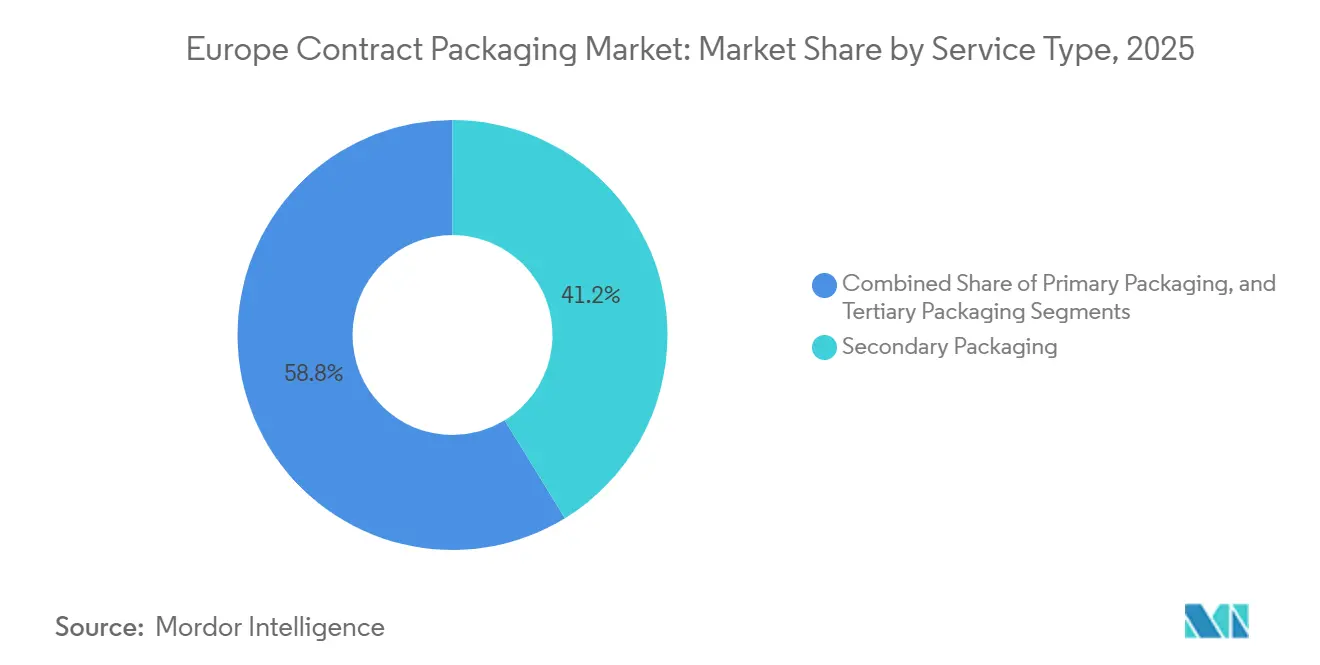

- By service type, secondary packaging led with 41.23% of the Europe contract packaging market share in 2025; tertiary packaging is forecast to expand at an 8.34% CAGR to 2031.

- By packaging format, rigid formats accounted for 52.32% share of the Europe contract packaging market size in 2025, while flexible formats are advancing at an 8.84% CAGR through 2031.

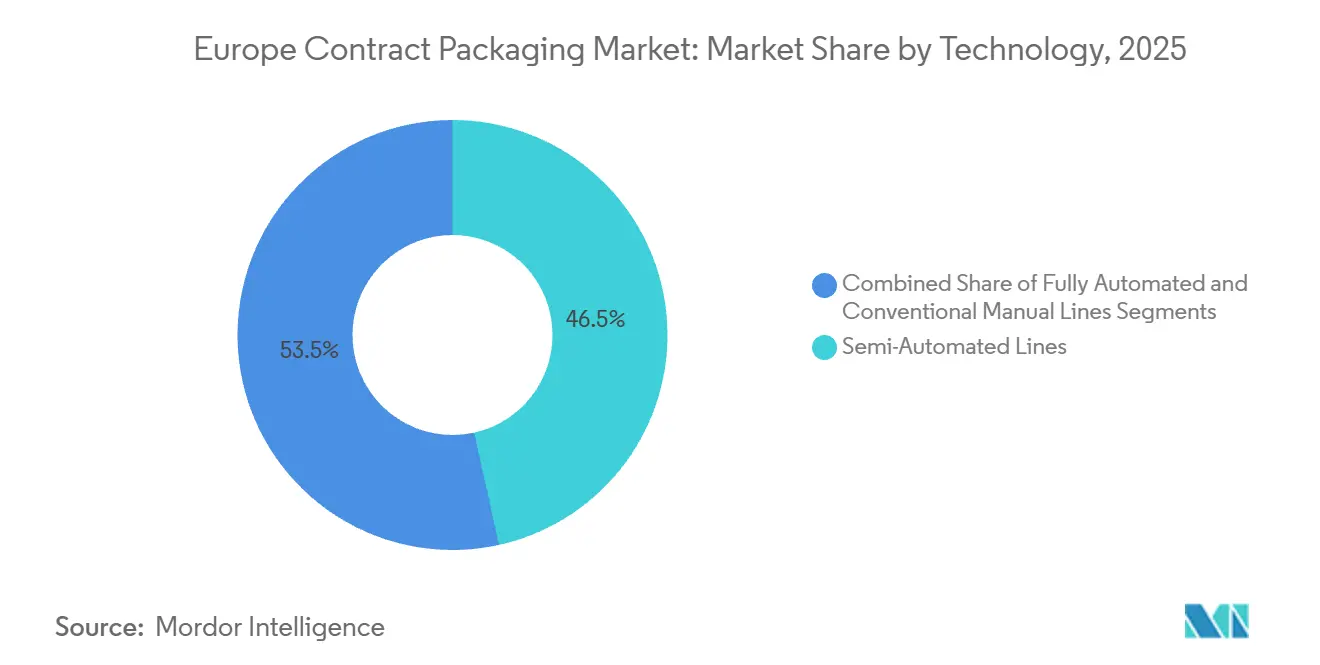

- By technology, semi-automated lines held 46.53% of the Europe contract packaging market share in 2025; fully automated and robotics-enabled lines are expected to post a 9.32% CAGR over 2026-2031.

- By end-user industry, food captured 28.62% revenue share in 2025, whereas cosmetics and personal care is the fastest-growing segment with a 9.56% CAGR to 2031.

- By country, Germany dominated with a 22.42% share in 2025, while Spain is poised for the quickest growth at a 9.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Contract Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Fulfillment Volumes | +1.8% | Pan-European, concentrated in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Proliferation of DTC (Direct-to-Consumer) Brands | +1.5% | UK, Germany, France, Spain | Medium term (2-4 years) |

| Retailer Shift to Shelf-Ready Packaging Formats | +1.2% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Growth of Sustainable Mono-Material Substrates | +1.4% | EU27, driven by PPWR compliance | Long term (≥ 4 years) |

| Adoption of Digital Printing for Short-Runs | +0.9% | Western Europe, early adoption in Germany and UK | Short term (≤ 2 years) |

| Near-shoring of Supply Chains Post-Brexit | +0.7% | UK, Ireland, Netherlands, Belgium | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Fulfilment Volumes

Online retail parcels jumped throughout 2025 as grocery, health supplements, and premium beverages migrated to direct shipment models. Contract packers that offer pick, fill, and ship services witnessed double-digit order growth, prompting them to standardize box sizes, install print-on-demand labelers, and add late-stage customization cells. Medium enterprises opted to outsource instead of building captive lines, citing the need for seasonal flexibility and avoiding capital outlay. Higher parcel velocity has made automated weigh-check-label modules essential for maintaining carrier compliance. Providers located near parcel sortation centers in Germany, the Netherlands, and France are benefiting from lower last-mile fees.[1]European Parcel Delivery Association, “B2C Parcel Volumes Europe 2025,” ecsda.org

Proliferation of DTC Brands

More than 480 new DTC labels opened regional web shops in 2025, targeting niche markets in health, beauty, and eco-friendly home care. These founders prefer variable-count cartons and influencer kits that must be assembled in small batches, accompanied by kitting instructions and QR-enabled inserts. Contract packers able to combine secondary packaging, fulfillment, and returns handling gained multi-year contracts that include periodic product restaging. Subscription-box curators also accelerated demand for insert printing and data-driven personalization, resulting in lead times of three days or less for short runs. As private-equity inflows sustain this launch cycle, co-packers that embed real-time order-status APIs are capturing repeat volumes.[2]European Startup Network, “Direct-to-Consumer Startups 2025 Landscape,” european-startup-network.eu

Retailer Shift to Shelf-Ready Packaging Formats

Large grocery chains now mandate shelf-ready cases for over-the-counter food and beverage assortments. The requirement increases the number of die-cut displays, tear-off perforations, and combination packs that must be erected and filled prior to distribution center delivery. Contract packers have responded by adding multi-lane cartoning machinery that forms, glues, and loads corrugated blanks at a rate of up to 60 units per minute. Retail compliance audits penalize misaligned print registers and improper tear lines, reinforcing the need for in-line vision inspection. The trend is particularly strong in Germany and the Benelux region, where Aldi, Carrefour, and Edeka expanded private label penetration in 2025.[3]EDEKA Group, “Private Label Shelf-Ready Requirements,” edeka.de

Growth of Sustainable Mono-Material Substrates

European consumer goods companies committed to meeting the 2030 recyclability pledge are phasing out multi-layer laminates. Mono-material polyethylene and polypropylene structures simplify recycling streams yet require delicate heat-sealing parameters. Contract packers invested in servo-driven pouch lines with precise temperature profiling to prevent seal failure. Sustainability scorecards attached to retailer listings make PCR content and end-of-life recovery mandatory, thus, co-packers offering film sourcing, line testing, and third-party certification are winning bid tenders. Upstream collaboration with substrate manufacturers has reduced downtimes associated with film gauge variability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU Packaging Waste Directive Targets | -1.1% | EU27, compliance costs highest in Germany, France, Netherlands | Long term (≥ 4 years) |

| Rising Labour Costs in Western Europe | -0.9% | Germany, France, Netherlands, Belgium | Short term (≤ 2 years) |

| Competition from In-house Packaging Operations | -0.6% | Pan-European, most acute in food and beverage sector | Medium term (2-4 years) |

| Limited Access to Recycled PCR Material | -0.8% | EU27, supply constraints most severe in Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Packaging Waste Directive Targets

The revised directive requires producers to reduce packaging waste by 15% per capita by 2030 and to achieve 65% recycling rates. Such mandates prompt brands to reduce over-packaging, thereby directly reducing the volume flowing through contract packers. Additionally, forthcoming eco-modulation fees penalize non-recyclable formats, forcing co-packers to requalify equipment for new substrates and thinner gauges with limited stretch tolerance. Compliance monitoring and reporting add administrative overhead, especially for small and mid-size facilities. While the rule accelerates innovation, it simultaneously delays investment as converters await definitive specifications for recycled content.

Rising Labour Costs in Western Europe

Nominal wages for machine operators and warehouse assistants increased by 5-7% in 2025 in Germany, France, and the Netherlands. To keep hourly rates competitive, some packers relocated low-complexity projects to Eastern Europe, fragmenting capacity and extending lead times. High labor expenses narrow margins on seasonal SKUs that require hand assembly, prompting providers to automate case loading, palletizing, and inspection. However, automation carries capital intensity and a learning curve in maintenance. Small co-packers without scale face erosion in profit, leading to consolidation or acquisition by large logistics groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Secondary Leadership, Tertiary Momentum

Secondary packaging generated the highest volume of assemblies, capturing 41.23% of the Europe contract packaging market share in 2025. The dominance reflects ongoing retailer and e-commerce requirements for bar-coded cartons, security seals, and promotional over-wraps. In 2026, demand for automated cartoning and shrink bundling systems continues to climb as brand portfolios expand their SKU counts. Secondary workflows remain attractive due to recurring orders, high labor content, and the scope for late-stage pack differentiation. Providers are bolstering line flexibility, retrofitting robotic pick-and-place units that switch formats within 30 minutes to serve multi-client halls.

Tertiary operations, encompassing palletizing and stretch-hooding, are forecast to outpace all other service tiers with an 8.34% CAGR. The upswing aligns with wider adoption of integrated warehouse management and the transition to mixed-SKU pallet configurations favored by omnichannel retailers. Robotics-enabled pallet cells equipped with vision-guided tooling support higher output and ergonomic relief. Contract packers are marketing predictive-maintenance dashboards that lower downtime, appealing to fast-moving consumer goods customers under just-in-time restock pressure. Consequently, tertiary volumes are expected to chip away at in-house logistics, reinforcing the Europe contract packaging market narrative of specialized fulfillment partners.

By Packaging Format: Rigid Dominance, Flexible Upswing

Rigid formats, including glass bottles, aluminum cans, and high-density polyethylene jugs, led with a 52.32% share of the Europe contract packaging market size in 2025. Beverage filling, personal-care bottling, and pharma blistering rely on rigid systems due to product protection and dosing accuracy. Co-packers owning clean-room and cold-fill infrastructure enjoy high barriers to entry, leading to steady throughput. Moreover, returnable glass loops in Germany expand bottling line utilization. Brand owners remain keen on rigid packs for premiumization as well as real and perceived recyclability in closed loops.

Conversely, flexible substrates are set to be the fastest-growing category, advancing at an 8.84% CAGR during 2026-2031. Re-closable pouches, stand-up spouts, and sachets reduce material usage and shipping weight, appealing to retailers’ sustainability scorecards. Contract packers that certify migration-safe films for acidic foods and pharma powders are landing multi-year volumes. Integration of digital pouch printing allows shorter runs tied to geographic and language variations, bolstering agile marketing programs. Thus, flexible share is predicted to narrow the gap with rigid formats, reinforcing diversification across the Europe contract packaging market.

By Technology: Semi-Automated Prevalence, Robotics Acceleration

Semi-automated lines accounted for 46.53% of the Europe contract packaging market share in 2025, proving popular among mid-volume projects that balance labor flexibility with mechanical consistency. These cells often pair manual loading with motor-driven sealing or bundling, delivering cost-effective outputs without full capital lock-in. Operators appreciate the capability to add or remove stations as project scope fluctuates. Nevertheless, the ongoing wage inflation and demands for traceability are nudging facilities toward higher digitalization, including vision systems and industrial IoT sensors.

Fully automated and robotics-enabled lines are projected to post a 9.32% CAGR, the steepest among the three technology tiers. Six-axis robots with quick-change grippers now manage mixed product in-feeds, while collaborative robots undertake end-of-line packing within minimal footprints. Conveyorized inspection equipped with artificial intelligence detects label skew and fill-level variance in real time. Although upfront costs can exceed EUR 3 million (USD 3.2 million) per hall, payback periods shorten to three years in high-throughput beverage or cosmetics programs. Automation capability also positions co-packers as preferred partners during retailer audits, reinforcing premium billing rates within the Europe contract packaging market.

By End-User Industry: Food Hegemony, Cosmetics Growth

Food customers generated the largest demand, accounting for 28.62% share in 2025. Shelf-stable snacks, chilled ready meals, and organic pantry staples migrate to contract facilities to accommodate promotional spikes. The channel shift to grocery e-commerce intensifies unit picking and variety-pack assembly, workloads ideally suited for specialized pack halls. Food safety certifications such as BRCGS and IFS segregate allergen lines, bolstering customer confidence and repeat orders. Advanced traceability modules ensure instant recall mapping in compliance with EU Regulation 178/2002.

Cosmetics and personal care is the fastest-moving vertical, predicted to post a 9.56% CAGR. Clean beauty start-ups outsource blending, filling, and kitting to co-packers with ISO 22716 environments, avoiding capital lock-in. Secondary demand arises from European Union Cosmetics Regulation (EC) 1223/2009 documentation, which a full-service packer can streamline. Single-dose sachets, influencer gift sets, and sampler pouches underpin growth, especially in Spain, Italy, and France where tourism recovery pushes duty-free and travel retail orders. This evolution supports a broader shift toward premium, customization-oriented jobs across the Europe contract packaging market.

Geography Analysis

Germany held a 22.42% share in 2025, reflecting mature food, beverage, and household chemicals outsourcing, extensive cold-chain freight corridors, and a dense network of certified co-packers around North Rhine-Westphalia. Facilities benefit from proximity to large converters of rigid and flexible substrates, ensuring just-in-time material flow. Brands leverage the country’s engineering talent to pilot automated case erecting and palletizing robotics that lift line availability above 95%. Despite high labor costs, government subsidies for Industry 4.0 retrofits support efficiency drives, helping maintain Germany’s pole position in the Europe contract packaging market.

The United Kingdom is grappling with post-Brexit customs declarations, prompting some pharmaceutical and beverage filler projects to relocate to continental Europe. However, specialized health and nutrition packers in the Midlands continue to grow as DTC channels aimed at domestic consumers pay premiums for faster delivery. Regional players are expanding in-house printing to counter label-sourcing challenges stemming from rules-of-origin paperwork. Ireland’s proximity to major biologics plants sustains demand for serialization and aggregation services, even as shipping costs for raw materials rise.

Southern Europe demonstrates the fastest regional momentum, with Spain expected to register a 9.18% CAGR through 2031. A booming cosmetics hub in Barcelona and Valencia fuels growth, while Andalusia’s agritech sector increases fresh juice bottling contracts. Italy exploits strong design capability to attract premium chocolate and luxury fragrance owners seeking intricate gift assemblies. Eastern European nations, led by Poland and the Czech Republic, gain from lower wages and EU transport subsidies, enticing overflow projects from German and French customers. Overall, varying cost structures and regulatory regimes shape a dynamic landscape that keeps the Europe contract packaging market in constant capacity alignment.

Competitive Landscape

The supplier base blends specialized co-packers like Budelpack Poortvliet, Kompak, and Tjoapack with diversified 3PLs such as DHL Supply Chain and Staci Group. Large logistics operators leverage scale in warehousing and freight to cross-sell contract packaging as a value-added extension, placing pressure on mid-sized independents. Yet niche providers defend share through certifications, formulation know-how, or rapid line changeover capability. Several outfits completed strategic acquisitions in 2025, including Cygnia Logistics purchasing a regional cosmetics filler to deepen end-to-end fulfillment. Cross-border expansion is equally active; Driessen United Blenders added a French site to serve EU-mainland nutritional powders after border controls tightened.

Automation investments dominate capital expenditure. Marvinpac deployed six collaborative robotic cells for kitting prestige confectionery, shaving 20% unit labor. Similarly, NOMI Co-Packing integrated thermal inkjet coding across all pouch lanes, achieving real-time variable data. Financing often occurs via operating leases, permitting technology upgrades ahead of depreciation cycles. Partnering with equipment OEMs allows pilot programs, which later expand into permanent installations upon performance proof. Market participants also see sustainability credentials as a differentiator, with Total Pack implementing solar arrays to offset 40% of plant electricity usage.

Pricing remains project-specific, factoring in format complexity, line speed, run length, and compliance documentation. Large consumer packaged goods firms issue multi-year volume benches, whereas start-ups accept higher per-unit rates to secure agile capacity. Contract packers routinely add value-added services such as digital asset management, demand planning, and reverse logistics, building sticky relationships. The competitive stakes underpin an environment where technological sophistication and service breadth dictate longer-term positioning within the Europe contract packaging market.

Europe Contract Packaging Industry Leaders

Budelpack Poortvliet BV

Complete Co-Packaging Services Ltd.

Driessen United Blenders

Harke Packserve GMBH

Cygnia Logistics Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kompak signed a three-year agreement with a leading vegan protein bar brand to supply secondary cartoning and display erection for 20 million units per year.

- October 2025: Budelpack Poortvliet upgraded its snack plant with servo-driven pouch lines compatible with mono-material polypropylene films.

- September 2025: Tjoapack Netherlands launched an automated bottling cell with in-line serialization to expand clinical trial packaging capacity.

- June 2025: Cygnia Logistics implemented a cloud-based WMS to synchronize co-packing inventory with DTC clients’ Shopify storefronts.

Europe Contract Packaging Market Report Scope

Contract packaging is a business arrangement where a third-party company manages the packaging of products for another company. This outsourcing model allows businesses to concentrate on their core competencies while leveraging the expertise of specialized packaging providers.

The Europe Contract Packaging Market Report is Segmented by Service Type (Primary Packaging, Secondary Packaging, and Tertiary Packaging), Packaging Format (Rigid Packaging, and Flexible Packaging), Technology (Conventional Manual Lines, Semi-Automated Lines, and Fully Automated/Robotics-Enabled Lines), End-user Industry (Beverages, Food, Pharmaceuticals, Cosmetics and Personal Care, and Other End-user Industries), and Country (United Kingdom, Germany, France, Italy, Spain, Netherlands, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Primary Packaging | Bottling and Filling |

| Pouching | |

| Canning | |

| Blister Packaging | |

| Other Primary Packaging | |

| Secondary Packaging | Cartoning |

| Labeling | |

| Shrink Wrapping | |

| Other Secondary Packaging | |

| Tertiary Packaging | Palletizing |

| Bundling | |

| Other Tertiary Packaging |

By Packaging Format

| Rigid Packaging |

| Flexible Packaging |

By Technology

| Conventional Manual Lines |

| Semi-Automated Lines |

| Fully Automated / Robotics-Enabled Lines |

By End-user Industry

| Beverages |

| Food |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Other End-user Industries |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Service Type | Primary Packaging | Bottling and Filling |

| Pouching | ||

| Canning | ||

| Blister Packaging | ||

| Other Primary Packaging | ||

| Secondary Packaging | Cartoning | |

| Labeling | ||

| Shrink Wrapping | ||

| Other Secondary Packaging | ||

| Tertiary Packaging | Palletizing | |

| Bundling | ||

| Other Tertiary Packaging | ||

| By Packaging Format | Rigid Packaging | |

| Flexible Packaging | ||

| By Technology | Conventional Manual Lines | |

| Semi-Automated Lines | ||

| Fully Automated / Robotics-Enabled Lines | ||

| By End-user Industry | Beverages | |

| Food | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Other End-user Industries | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe contract packaging market in 2026?

The Europe contract packaging market size is valued at USD 28.78 billion in 2026.

What CAGR will define growth through 2031?

Revenue is projected to rise at a 7.26% CAGR between 2026 and 2031.

Which service type leads the market?

Secondary packaging accounts for the highest share at 41.23% in 2025.

Which technology segment will grow fastest?

Fully automated and robotics-enabled lines are forecast to expand at a 9.32% CAGR during 2026-2031.

Which country shows the strongest growth outlook?

Spain is expected to register the quickest expansion, posting a 9.18% CAGR through 2031.

How does e-commerce influence demand?

Rising online order volumes boost demand for agile, late-stage customization, favoring contract packers that integrate fulfillment and packaging services.

Page last updated on: