Australia Contract Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

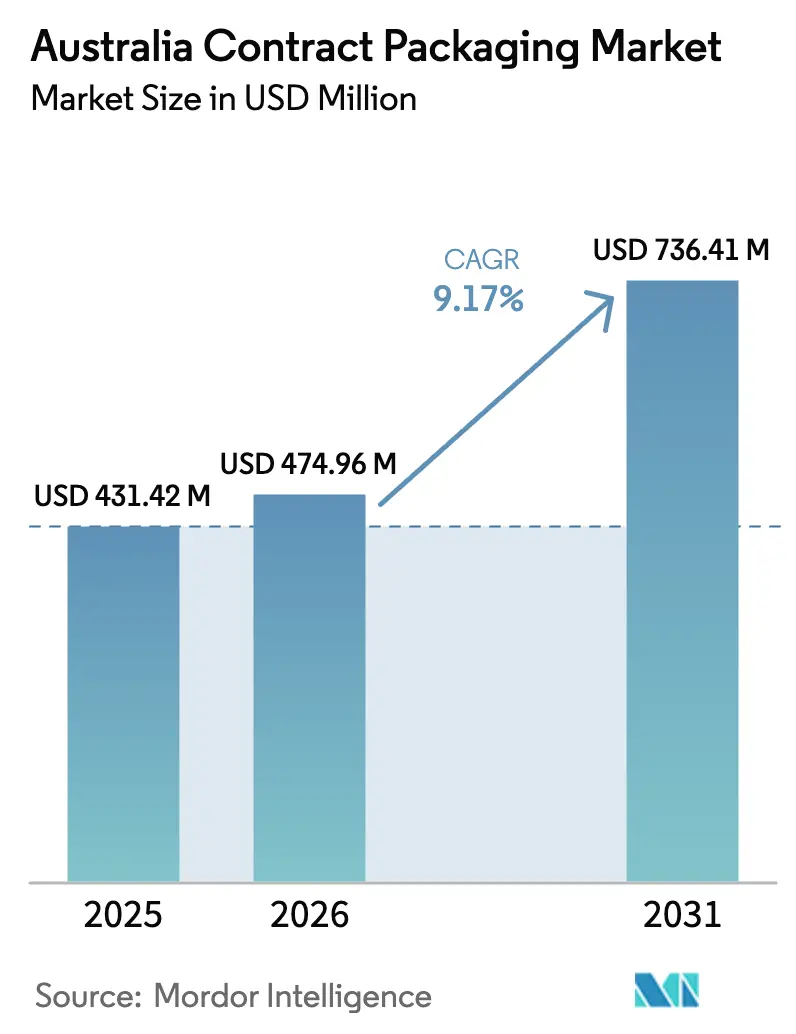

| Base Year Market Size (2025) | USD 431.42 Million |

| Market Size (2026) | USD 474.96 Million |

| Market Size (2031) | USD 736.41 Million |

| Growth Rate (2026 - 2031) | 9.17% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Contract Packaging Market Analysis by Mordor Intelligence

The Australia contract packaging market size is expected to grow from USD 431.42 million in 2025 to USD 474.96 million in 2026 and is forecast to reach USD 736.41 million by 2031 at 9.17% CAGR over 2026-2031. Brand owners are moving capital away from fixed packaging lines toward flexible co-packing partnerships that absorb demand swings and compliance risk. Retail e-commerce expansion, polymer-price volatility after the 2024 Qenos closure, and Australian Packaging Covenant Organisation (APCO) recycled-content rules are all steering volumes to external specialists. Large retailers are automating primary fulfilment while still outsourcing promotional bundles, export labelling, and reverse logistics, supporting steady throughput for co-packers. Meanwhile, investment in robotics and artificial intelligence is shortening payback periods to under 18 months, helping operators offset the 36,200 manufacturing vacancies counted in December 2024.

Key Report Takeaways

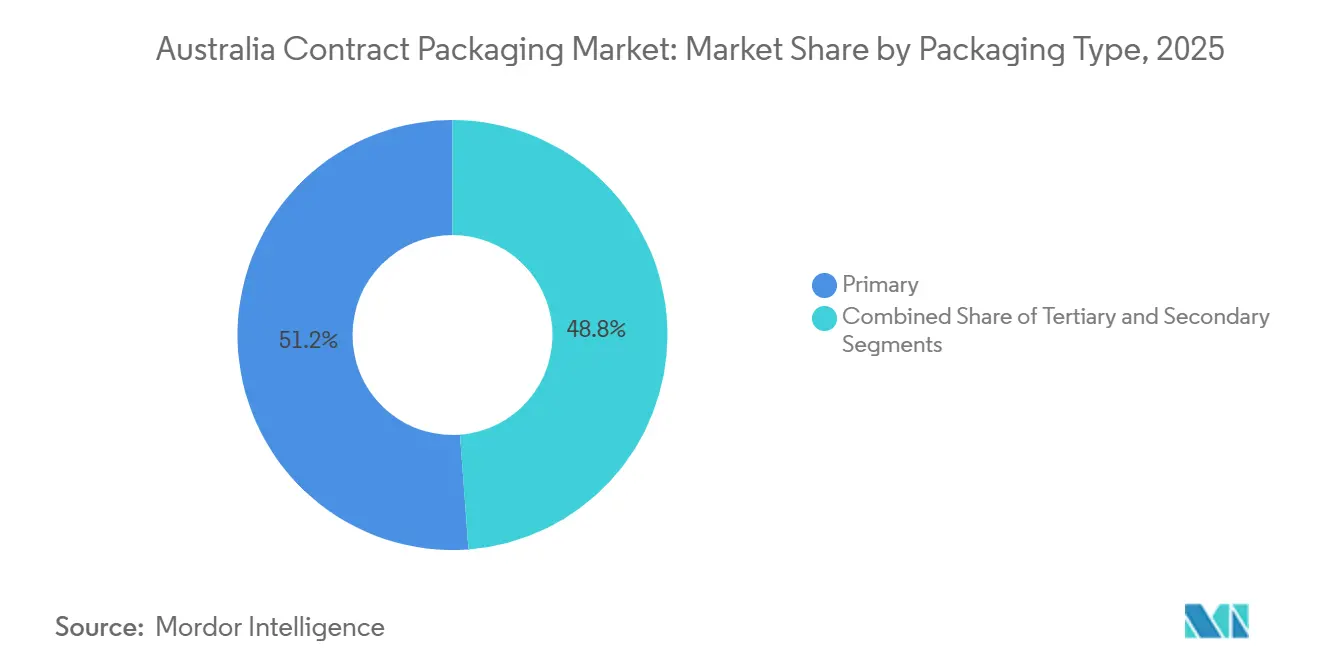

- By packaging type, primary packaging led with 51.18% revenue share in 2025, while tertiary packaging is projected to expand at a 9.43% CAGR through 2031.

- By end-user industry, food applications accounted for 37.47% revenue share in 2025; pet food is forecast to record a 10.21% CAGR over 2026-2031.

- By service offering, packaging and labeling captured 42.61% revenue share in 2025, whereas fulfillment and logistics services are expected to advance at a 10.17% CAGR during the same period.

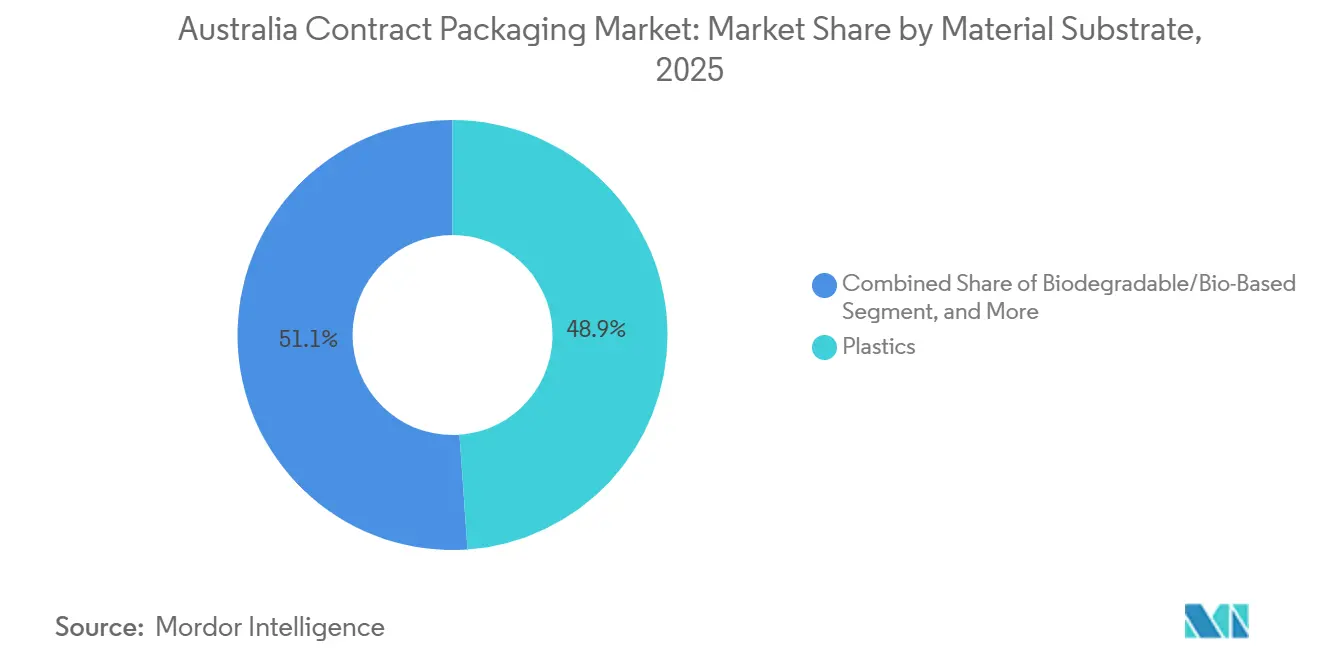

- By material substrate, plastics represented 48.89% of demand in 2025, yet biodegradable and bio-based alternatives are poised to grow at a 9.89% CAGR through 2031.

- By automation level, fully automated lines accounted for 46.27% revenue share in 2025; robotics-integrated systems are projected to rise at a 9.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Contract Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FMCG Demand Sustains Co-Packing Volumes | +2.30% | National, with concentration in NSW, Victoria, Queensland | Medium term (2-4 years) |

| E-Commerce SKU Proliferation and Micro-Batch Fulfillment | +2.10% | National, early gains in Sydney, Melbourne metro areas | Short term (≤ 2 years) |

| Sustainability Compliance Outsourcing Surge Due to APCO 2025/2030 Targets | +1.80% | National, driven by APCO member brands in NSW, Victoria | Medium term (2-4 years) |

| AI-Enabled Pack Optimization Lowers Cost and Waste | +1.20% | National, pilot deployments in Victoria, NSW | Long term (≥ 4 years) |

| Outsourcing Non-Core Operations by Brand Owners | +0.90% | National, concentrated in FMCG and pharmaceutical sectors | Medium term (2-4 years) |

| Near-Shoring to Mitigate Indo-Pacific Supply-Chain Risk | +0.70% | Queensland, Western Australia ports; Tasmania export hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FMCG Demand Sustains Co-Packing Volumes

Seasonal promotions and new-product rotations are pushing fast-moving consumer goods companies to favour variable-cost outsourcing. Coles’ USD 264 million Wetherill Park customer-fulfilment center automates primary picking yet still contracts out palletization and export labelling, giving co-packers multi-SKU work that amortizes changeovers across thousands of products. Woolworths’ USD 39.6 million Adelaide site follows the same pattern, showing that even digitally advanced retailers rely on third parties for tertiary tasks. Co-packers offering modular equipment capable of sub-5,000-unit runs are therefore winning repeat business. Labor scarcity 36,200 open manufacturing roles in late 2024 strengthens the appeal of outsourcing, because multi-client plants can recruit year-round rather than only for peak seasons.[1]Australian Bureau of Statistics, “Labour Force Statistics December 2024,” abs.gov.au

E-Commerce SKU Proliferation and Micro-Batch Fulfilment

Online grocery penetration surpassed 8-10% of Australian food sales by mid-2025, fragmenting order profiles down to each-pick units. Toll Group’s USD 132 million Kemps Creek site processes 37 million items annually, supporting split-case sortation that traditional brand plants cannot match. Retailers like Coles still delegate promotional kit assembly, such as seasonal gift packs, to nearby co-packers that can turn lines in under 30 minutes. Flexible mailers and lightweight films preferred in e-commerce also drive the Australia contract packaging market, because specialist converters can certify performance while meeting dimensional-weight rules. As same-day delivery expands beyond capital cities, micro-batch packaging will accelerate across NSW and Victoria warehouses.[2]Australian Packaging Covenant Organisation, “Annual Report 2023-24,” apco.org.au

Sustainability Compliance Outsourcing Surge Due to APCO 2025/2030 Targets

APCO’s 2025 interim rule of 20% post-consumer recycled content and future penalties of up to AUD 0.50 per kilogram of non-compliant material creates clear economic incentives to outsource. Pact Group’s 18,000-tonne recycled-plastic deal with Woolworths shows how large co-packers can aggregate demand and lock in supply, a feat uneconomic for individual brands. Contract facilities that invest in wash plants, densifiers, and traceability software are monetizing compliance as a service. BioPak’s compostable formats give foodservice chains an off-the-shelf path to council organics mandates. Because recovery rates for rigid plastics sat at only 28% in 2023-24, packaging producers with certified recycled content pipelines are positioned as irreplaceable partners.[3]Pact Group, “Annual Report 2024,” pactgroup.com.au

AI-Enabled Pack Optimization Lowers Cost and Waste

Artificial-intelligence deployments are trimming freight and material expense. Phantm’s algorithm, used by Opal Australian Paper for a cosmetics client, right-sizes cartons in real time, cutting corrugated waste by 30%. Omron vision-guided robots inspect fill levels at over 120 units per minute, justifying investment even for medium-volume lines. Machine learning is also appearing in waste sortation, where vision systems divert contaminated material and protect recycled-content quality. These capabilities differentiate co-packers in bids were brand owners demand cost transparency and environmental metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin Costs and Qenos Closure Supply Risk | -1.40% | National, acute impact in NSW, Victoria manufacturing hubs | Short term (≤ 2 years) |

| In-House Packaging Expansion by FMCG Majors | -1.10% | National, concentrated in Coles and Woolworths supply chains | Medium term (2-4 years) |

| Skilled Automation-Operator Shortage | -0.80% | National, most severe in regional Queensland, South Australia | Medium term (2-4 years) |

| High Capex and Accreditation Hurdle for New Entrants | -0.60% | National, barriers highest for pharmaceutical and food sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin Costs and Qenos Closure Supply Risk

The 2024 shutdown of Qenos removed Australia’s only domestic virgin polyethylene source, adding a 12-18% import premium and extending lead times to as long as eight weeks. Large incumbents signed multi-year contracts with Asian resin producers, but mid-tier firms remain exposed to spot pricing. APCO’s low rigid-plastic recovery rate leaves insufficient recycled feedstock to offset virgin shortages, so sudden crude-oil spikes can still squeeze margins. Great Wrap’s 2025 insolvency illustrates the fragility of smaller material innovators when resin costs swing unpredictably.

In-House Packaging Expansion by FMCG Majors

Coles and Woolworths invested USD 1.04 billion in automated distribution centers between 2024-2025, reclaiming some secondary packaging work they once outsourced. Coles’ USD 580.8 million Truganina facility alone will handle 4.6 million cartons weekly once fully operational. Such vertical integration narrows addressable volumes for co-packers tied heavily to grocery promotions. While specialized pharma and pet-food segments remain insulated, ambient grocery lines now face enhanced buyer power from retailers that can benchmark external quotes against internal capability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Tertiary Formats Close the Growth Gap

Tertiary packaging is forecast to grow at 9.43% a year during 2026-2031, slightly ahead of the Australia contract packaging market size average. This momentum traces to e-commerce hubs that need modular pallets, corner-boards, and returnable crates customized for each delivery route. In 2025, primary packaging still dominated at 51.18% of the Australia contract packaging market share, reflecting brand owners’ desire to control consumer-facing formats. However, those same owners outsource export shrouds, stretch wrap, and mixed-SKU pallets to co-packers equipped with automated palletizers that switch recipes in minutes.

Contract packers are also aligning with pallet-pooling networks such as CHEP, integrating reusable platforms into their reverse-logistics loops. Visy’s USD 13.2 million Tasmanian hub demonstrates the capital needed to guarantee phytosanitary standards for Asian exports a niche where tertiary packaging expertise becomes a competitive edge. As parcel carriers introduce stricter dimensional-weight billing, filler pads and void-reduction solutions are seeing accelerated take-up, sustaining tertiary-format demand through the forecast horizon.

By End-User Industry: Pet Food Commands the Fast Lane

Food products generated 37.47% of 2025 revenue, anchoring the Australia contract packaging market. Yet growth now tilts toward pet food, which is set to climb at 10.21% CAGR as premium brands insist on domestic micro-batching that keeps ingredient provenance intact. Frontier Pets shifted freeze-dried runs back to Australia after offshore co-packing failed traceability audits, while Mackle Petfoods moved to small-lot air-dried lines near its ingredient farms.

Pharmaceutical co-packaging remains lucrative because Therapeutic Goods Administration audits deter new entrants. Probiotec’s new Kemps Creek campus centralizes formulation and blistering under one validated roof, shortening lead times for clinical-trial clients. Beverage-sector co-packers are benefiting from Orora’s extra aluminium-can lines, filling ready-to-drink cocktails and craft seltzers whose brand owners lack retort capacity. Automotive and electronics work stays marginal, constrained by anti-static and moisture-barrier specifications that demand unique equipment many co-packers cannot justify.

By Service Offering: Fulfilment and Logistics Stretch Ahead

Packaging and labelling pulled in 42.61% of 2025 revenue, but fulfilment and logistics should grow faster at 10.17% CAGR as retailers favour variable-cost, same-day networks. The Australia contract packaging market size for fulfilment services is expanding on the back of Toll Group’s healthcare cold-chain rollouts and on grocery box subscriptions that spike ahead of holidays. Reverse logistics is a companion opportunity, handling damaged goods and recycling streams that APCO compliance now monetizes.

Filling and assembly lines are migrating to aseptic designs that handle plant-based milks needing 12-month ambient shelf life. Formulation and blending stays a pharmaceutical-centric niche, where each batch must be traceable to active-ingredient lots. Co-packers that bolt value-added testing or real-time IoT shipment tracking onto traditional kitting are widening margins and fending off price competition.

By Material Substrate: Biodegradable Films Edge Toward Parity

Plastics commanded 48.89% of volume in 2025 and will remain the workhorse, but biodegradable and bio-based substrates are slated for 9.89% annual growth as APCO bans polystyrene foam after 2025. The Australia contract packaging market share for bioplastics is still modest because resin costs exceed fossil benchmarks, yet multi-client co-packers can spread the premium across wider order books. Pact Group’s recycled-crate loop with Woolworths confirms that post-consumer content can win large supermarket bids.

Paperboard is also regaining share thanks to Visy’s lightweight fluting upgrade, which cuts weight by 12% without losing stacking strength. Metal cans hold niche status outside beverages, but lifecycles changes could revive aerosol refurbishment services. Glass loses ground except in premium spirits and injectable drugs, areas where barrier needs override freight penalties.

By Automation Level: Collaborative Robots Earn the Spotlight

Fully automated lines provided 46.27% of 2025 revenue, yet robotics-integrated systems should rise at a 9.92% CAGR through 2031 because labour gaps persist. Collaborative arms with adaptive grippers routinely shift between pouch loading and case packing in under half an hour, fitting the micro-batch model defining the Australia contract packaging market. OnRobot’s tooling now handles irregular flexibles without custom-machined fingers, a gamechanger for seasonal SKUs.

Semi-automated and manual setups survive where batch sizes fall below 5,000 or regulatory clearance times outpace line speeds, such as orphan-drug blistering. Nonetheless, the pool of operators qualified to run older equipment is shrinking, reinforcing the shift toward vision-guided pick-and-place systems whose user interfaces resemble consumer tablets.

Geography Analysis

New South Wales and Victoria sit at the core of the Australia contract packaging market, thanks to Sydney and Melbourne consumer demand, intermodal freight nodes, and access to skilled labour. Special Activation Precincts in Wagga Wagga and Parkes are dangling concessional land to attract food-grade co-packing facilities that can back-haul exports through Port Botany rail shuttles. Victoria’s USD 990 million Freight Plan links Dandenong and Somerton to national distribution centers, trimming same-day delivery cut-offs for brand owners.

Queensland is emerging as a near-shoring springboard for Indo-Pacific brands hedging tariff exposure. Orora’s Rocklea aluminium-can line feeds craft beverage exporters tapping Port of Brisbane short-sea routes into Southeast Asia. The state also benefits from Toll Group’s additional healthcare cold-chain capacity at Richlands, ensuring biologic shipments meet stringent temperature excursions.

Western Australia and South Australia draw industrial-packaging demand from resource firms, though FMCG volumes stay lower due to dispersive populations. Visy’s Tasmanian cold-chain hub, finished in February 2026, positions the island as an export consolidation point for boutique cheese and seafood brands. In the Northern Territory and the Australian Capital Territory, small populations limit scale, yet government procurement under the National Reconstruction Fund is encouraging pharmaceutical co-packers to locate blistering plants closer to defense and public-health contracts.

Labor shortages are deeper in regional Queensland and South Australia, were population growth trails warehouse expansion. That scarcity accelerates robotic adoption and nudges new projects to metropolitan fringes with vocational-training pipelines. APCO data shows NSW and Victoria still contribute roughly 60% of packaging tonnage placed on market, but Queensland’s share is climbing as fulfilment centers sprout near port terminals.

Competitive Landscape

The Australia contract packaging market balances scale and specialization. Giants such as Pact Group, Orora, and Visy exploit vertical integration in rigid plastics, corrugate, and metals, locking in resin and paperboard under multi-year supply deals. Their negotiating power shields margins against volatile polyethylene imports after the Qenos shutdown. Niche operators including Probiotec in pharmaceuticals and Toll Group in e-commerce fulfilment win business where Therapeutic Goods Administration audits or real-time cold-chain visibility raise entry barriers for generalists.

Pro-Pac’s 2025 voluntary administration revealed the dangers of staying mid-sized without investing in robotics or recycled-content capabilities demanded by APCO signatories. In response, rivals doubled down on capital spending: Pact earmarked USD 9.9–13.2 million of extra working capital for imported resin, while Toll Group sunk USD 66 million into healthcare cold-chain sites. Technology innovators such as Phantm and OnRobot are selling AI design algorithms and adaptive tooling to co-packers aiming to trim labour hours per finished case.

Retailers remain both customers and competitive threats. Coles and Woolworths poured USD 1.04 billion into automated distribution complexes that now produce part of their secondary packaging in-house, squeezing volumes available to external partners. Co-packers are responding by seeking white-space niches: premium pet food requiring freeze-dry lines, biodegradable clamshells for organics-diversion mandates, and serialized vials for cell-therapy trials where batch integrity is paramount.

Australia Contract Packaging Industry Leaders

Multipack-LJM Pty Ltd

Pakco International Co. Ltd

FoodPak Pty Ltd

Probiotec Pharma Pty Ltd

Vacupack Australia Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Space Machines Company and CSIRO produced a multi-material rocket thruster via metal 3D printing, showcasing advanced manufacturing spillovers into precision packaging tooling.

- September 2025: The U.S. announced 100% tariffs on branded pharmaceuticals unless domestic production commences, prompting CSL to review USD 2 billion in exports and potential repatriated packaging work.

- May 2025: The Food and Beverage Accelerator issued a Sustainable Packaging Trends Report outlining 12 pathways for circular design.

- February 2025: TGA updated its Code of Practice for Tamper-Evident Packaging, tightening design and validation guidance.

Australia Contract Packaging Market Report Scope

The Australia Contract Packaging Market Report is Segmented by Packaging Type (Primary, Secondary, Tertiary), End-User Industry (Food, Beverage, Pharmaceutical, Home and Personal Care, Automotive, Electronics and High-Tech, Pet Food, Other End-User Industry), Service Offering (Formulation and Blending, Filling and Assembly, Packaging and Labeling, Fulfillment and Logistics), Material Substrate (Paper and Paperboard, Plastics, Metals, Glass, Biodegradable/Bio-Based), Automation Level (Manual, Semi-Automated, Fully Automated, Robotics-Integrated), and Geography (New South Wales, Victoria, Queensland, Western Australia, South Australia, Tasmania, Northern Territory, Australian Capital Territory). The Market Forecasts are Provided in Terms of Value (USD).

| Primary |

| Secondary |

| Tertiary |

| Food |

| Beverage |

| Pharmaceutical |

| Home and Personal Care |

| Automotive |

| Electronics and High-Tech |

| Pet Food |

| Other End-User Industry |

| Formulation and Blending |

| Filling and Assembly |

| Packaging and Labeling |

| Fulfillment and Logistics |

| Paper and Paperboard |

| Plastics |

| Metals |

| Glass |

| Biodegradable/Bio-Based |

| Manual |

| Semi-Automated |

| Fully Automated |

| Robotics-Integrated |

| By Packaging Type | Primary |

| Secondary | |

| Tertiary | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical | |

| Home and Personal Care | |

| Automotive | |

| Electronics and High-Tech | |

| Pet Food | |

| Other End-User Industry | |

| By Service Offering | Formulation and Blending |

| Filling and Assembly | |

| Packaging and Labeling | |

| Fulfillment and Logistics | |

| By Material Substrate | Paper and Paperboard |

| Plastics | |

| Metals | |

| Glass | |

| Biodegradable/Bio-Based | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated | |

| Robotics-Integrated |

Key Questions Answered in the Report

How large will Australia contract packaging be by 2031?

It is forecast to reach USD 431.42 billion, expanding at 9.17% CAGR from 2026-2031.

Which packaging type is growing the quickest?

Tertiary formats, driven by e-commerce pallet customization, are projected to rise at 9.43% annually.

Why is pet food important for co-packers?

Premium brands are localizing micro-batch runs for traceability, pushing pet-food contract volumes to a 10.21% CAGR through 2031.

How are APCO rules changing material choices?

A 20% recycled-content mandate for 2025 and stricter 2030 penalties are accelerating biodegradable and recycled-plastic adoption in new projects.

What technology investments earn the fastest payback?

Collaborative robots with vision systems often recover costs in under 18 months by trimming labor and inspection time.

Are retailers a threat to external co-packers?

Yes, Coles and Woolworths added over USD 1 billion in automated distribution centers, internalizing some secondary packaging but still outsourcing niche and promotional tasks.

Page last updated on: