Blister And Thermoform Contract Packaging Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

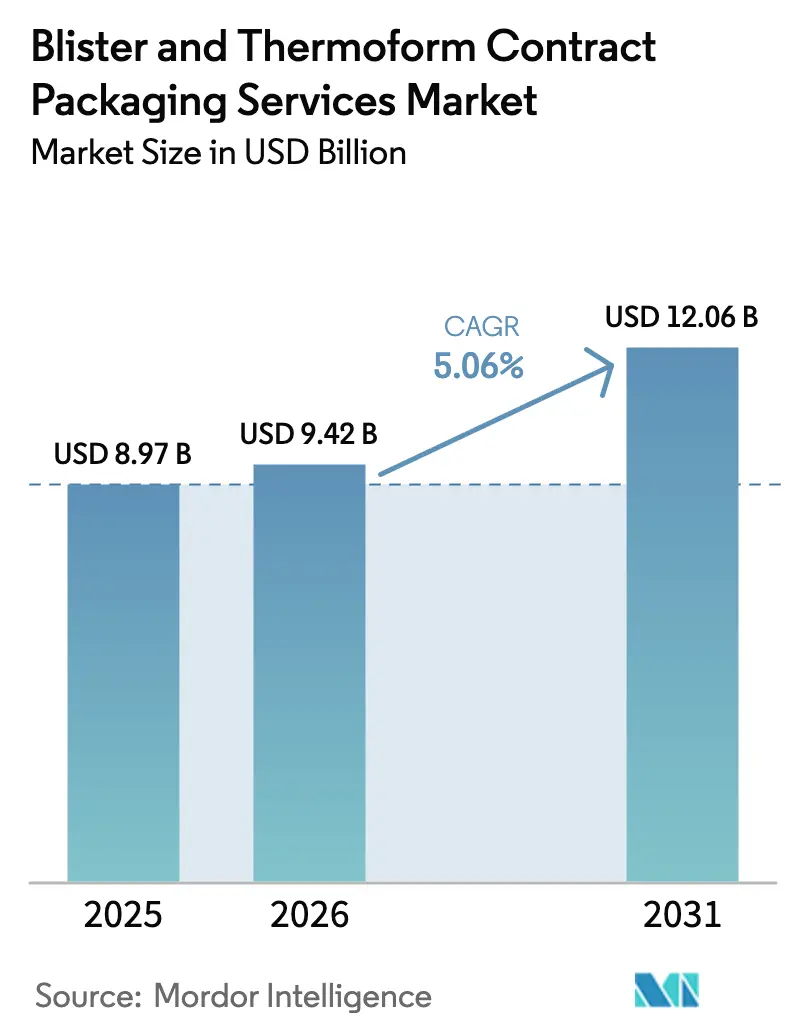

| Market Size (2026) | USD 9.42 Billion |

| Market Size (2031) | USD 12.06 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

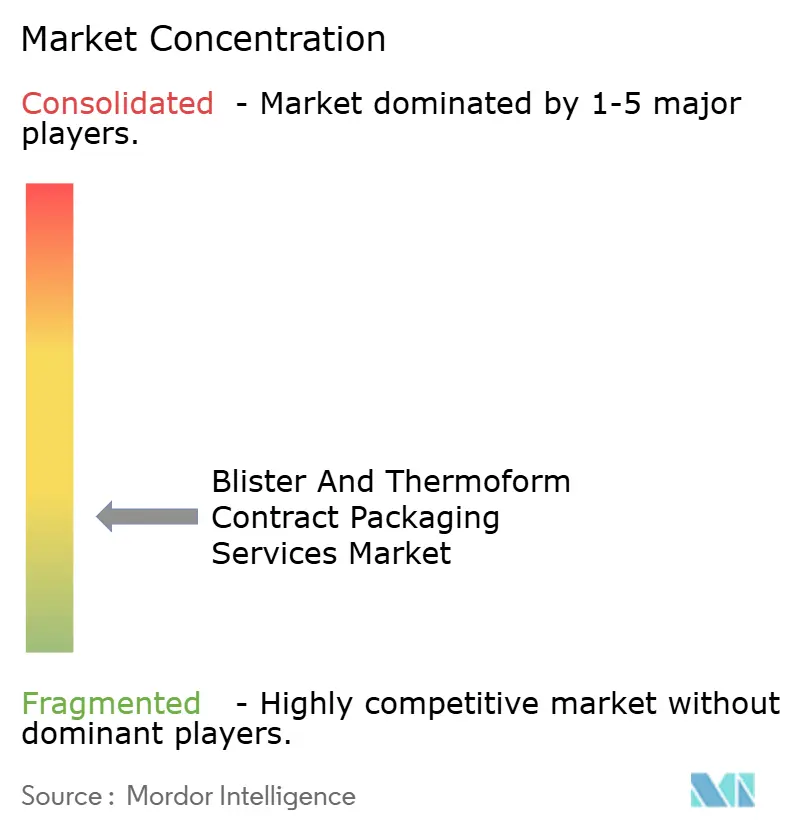

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blister And Thermoform Contract Packaging Services Market Analysis by Mordor Intelligence

The Blister And Thermoform Contract Packaging Services market size is expected to grow from USD 8.97 billion in 2025 to USD 9.42 billion in 2026 and is forecast to reach USD 12.06 billion by 2031 at 5.06% CAGR over 2026-2031. This steady trajectory stems from pharmaceutical companies' growing preference for outsourcing serialization-ready blister lines, the food sector’s accelerating shift toward unit-dose packaging, and the Asia-Pacific’s cost-efficient manufacturing base. Providers with Industry 4.0 production cells, AI-driven defect detection, and multi-market regulatory expertise capture the strongest demand waves as clients seek to shorten launch cycles and avoid capital-intensive in-house lines. Material upgrades, particularly aluminum foil formats that provide high-barrier protection, further drive revenue, while sustainability mandates prompt investment in mono-material films. Ongoing merger activity and private-equity roll-ups are fostering gradual consolidation; however, the field remains moderately fragmented due to diverse regional regulations and niche service requirements.

Key Report Takeaways

- By material type, plastic films captured 66.02% of the Blister and Thermoform Contract Packaging Services Market share in 2025.

- By service type, the Blister and Thermoform Contract Packaging Services Market size for serialization and track-and-trace services is projected to grow at a 6.89% CAGR between 2026–2031.

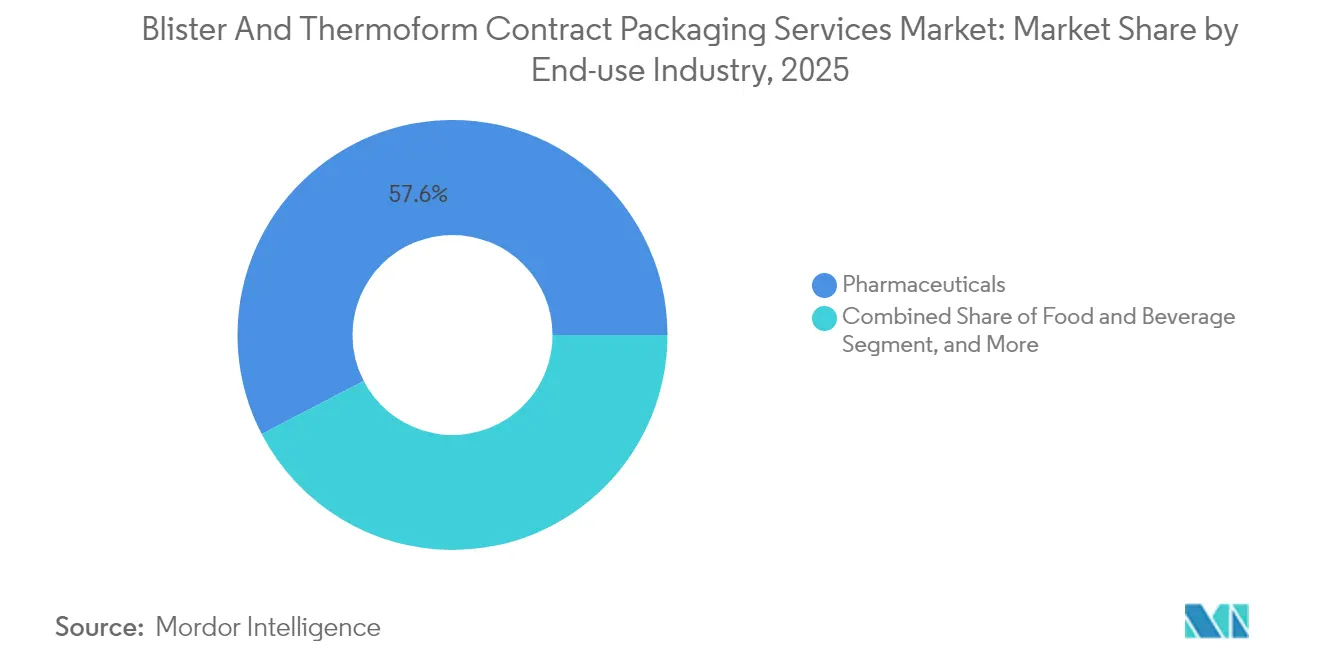

- By end-use industry, pharmaceuticals captured 57.62% of the Blister and Thermoform Contract Packaging Services Market share in 2025.

- By geography, the Blister and Thermoform Contract Packaging Services Market size in Asia-Pacific is projected to grow at a 6.51% CAGR between 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blister And Thermoform Contract Packaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Pharmaceutical Outsourcing to Specialist Packagers | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Growth In Unit-Dose and Compliance-Friendly Blister Demand | +1.2% | Global | Long term (≥ 4 years) |

| Rising Requirement for Child-Resistant / Senior-Friendly Formats | +0.9% | North America and the EU, spill-over to APAC | Medium term (2-4 years) |

| Cost-Efficiency Versus In-House Packaging Operations | +1.1% | Global | Short term (≤ 2 years) |

| Adoption Of Mono-Material Recyclable Blister Lines | +0.7% | EU core, expanding to North America | Long term (≥ 4 years) |

| Packaging-Integrated Nitrosamine-Mitigation Solutions | +0.4% | Global, with regulatory influence from the FDA, EMA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Pharmaceutical Outsourcing to Specialist Packagers

The blister and thermoform contract packaging services market continues to gain momentum as drug makers maximize flexibility by outsourcing packaging runs to partners holding GMP certification, on-site laboratories, and multi-level serialization architecture. Sharp Services allocated USD 100 million across its United States and European sites in 2025 to meet surging demand for sterile and solid-dose products, illustrating the capital intensity that smaller pharmaceutical companies often avoid through outsourcing.[1]“Sharp Commits $100 Million to Expand Sterile and Packaging Capacity,” BioPharma Boardroom, biopharmaboardroom.com Contract providers deliver rapid changeovers, validated line clearance, and region-specific data-exchange connectivity, enabling faster market entry. Outsourcing also helps clients navigate Italy’s 2025 FMD transition and a patchwork of Asia-Pacific traceability rules without incurring the costs associated with owning and maintaining costly aggregation servers. The widening pipeline of specialty drugs and orphan therapies, often produced in small lots, further raises demand for agile blister suites. As these dynamics scale, the blister and thermoform contract packaging services market benefits from recurring, multi-year agreements anchored on quality and compliance performance metrics.

Growth in Unit-Dose and Compliance-Friendly Blister Demand

Healthcare stakeholders are increasingly linking packaging to therapeutic outcomes, driving the adoption of calendar, wallet, and smart blister formats that record each pill removal. Schreiner MediPharm’s conductive Smart Blister Card, paired with electronic diaries, exemplifies the convergence of digital health and packaging. Unit-dose designs improve adherence among elderly patients managing polypharmacy and reduce medication errors in clinical trials. Contract packagers respond by installing robotic feeders and modular forming stations that accommodate batch sizes ranging from 50 to 1 million blisters, eliminating the need for lengthy tooling resets. Calendar graphics, QR codes, and near-field communication tags personalize therapy while meeting FDA human factors guidelines.

Rising Requirement for Child-Resistant and Senior-Friendly Formats

Regulators mandate packaging that frustrates child access yet remains easy for seniors with limited dexterity. Achieving United States F=1 child-resistance alongside 90% senior-friendliness demands precise force-displacement mechanics and rigorous panel testing. Keystone Folding Box Co.’s Push-Pak wallet achieved perfect senior-friend test rates, underscoring engineering sophistication. Amcor’s Opening Feature technology reduces overall pack dimensions by 40% while maintaining push-through access, enabling brand owners to lower logistics costs. Contract packaging providers invest in prototyping software and ASTM/ISO test rigs to validate new mechanisms quickly, making them indispensable partners as demographic shifts raise the proportion of senior consumers worldwide. These innovations reinforce brand safety credentials and accelerate uptake inside the blister and thermoform contract packaging services market.

Cost-Efficiency Versus In-House Packaging Operations

Capital outlays for a single high-speed thermoformer can top USD 2 million, excluding clean-room retrofits and serialization servers. Contract packagers spread these costs across multiple clients, delivering per-unit pricing competitive with in-house lines, especially for seasonal or clinical trial volumes. On-demand digital printing eliminates the need for pre-printed foil inventory, reducing wastage typically associated with 10%-20% over-ordering and enabling serial numbers to be assigned in real-time. Variable costing models let drug makers scale output without locking capital into depreciating equipment. For consumer brands, outsourcing converts fixed overhead into a cost-of-goods line item, thereby aiding margin management amid input price volatility. These financial advantages draw a steady flow of contracts, bolstering the blister and thermoform contract packaging services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility (PVC, Aluminum) | -0.8% | Global | Short term (≤ 2 years) |

| Tightening Regulations on PVC And Single-Use Plastics | -0.6% | EU core, expanding globally | Long term (≥ 4 years) |

| Supply Constraints in High-Barrier Eco-Film Capacity | -0.5% | Global, with acute shortages in Europe | Medium term (2-4 years) |

| Complexity And Cost of Multi-Market Serialization | -0.7% | Global, with regulatory influence from multiple agencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (PVC, Aluminum)

Feedstock disruptions and energy-price swings lift PVC and aluminum costs, squeezing margins for contract packagers locked into multi-year service agreements. Spot PVC hikes tracked in March 2025 illustrate rapid 15% price jumps traced to Asian chlor-alkali outages. Aluminum premiums climbed amid smelter curtailments and logistics congestion, amplifying material cost exposure because blister webs often contain 20-25 grams of foil per square meter. While some providers hedge with long-term supply contracts, volatility still pressures working capital and prompts surcharges that brand owners resist. These conditions temper profit expansion inside the blister and thermoform contract packaging services market until commodity prices stabilize.

Tightening Regulations on PVC and Single-Use Plastics

Europe’s Packaging and Packaging Waste Regulation requires every consumer pack to meet recyclability criteria by 2030, effectively phasing out multilayer PVC/PVdC structures. Contract packagers must retrofit forming stations for polypropylene or polyethylene monomaterial substrates and validate heat-seal integrity. SÜDPACK Medica’s polypropylene NutriGuard blister demonstrates that compliance is possible, but it requires new tooling and forming curves. Extended Producer Responsibility fees add direct costs for non-recyclable formats, prompting brand owners to accelerate material transitions. Providers that lag in sustainable-material processing risk client churn, constraining near-term growth in the blister and thermoform contract packaging services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Foil Gains Momentum Despite Plastic Dominance

Plastic films anchored 66.02% of the blister and thermoform contract packaging services market share in 2025. However, aluminum foil packs are forecast to grow at a 6.55% CAGR through 2031, as life-science clients demand moisture-oxygen barriers, tamper-evident packaging, and premium metallic aesthetics. The blister and thermoform contract packaging services market size tied to aluminum platforms could rise notably as OTC brands pivot toward wallet cards with printable instructions. Providers expand their capabilities by installing dual-reel stations that switch seamlessly from PVC to cold-form foil, eliminating lengthy downtimes and supporting mixed material orders within the same shift.

Foil’s ascendancy also reflects regulatory pushback on chlorinated plastics. Nevertheless, polypropylene single-web designs are emerging as sustainable contenders, especially in Europe, where fee structures escalate for non-recyclable laminates. Contract packagers invest in inline vision systems to detect micro-cracking in formed cavities and maintain vacuum-integrity testing for foil webs. Paper laminate concepts remain niche, primarily used in nutraceuticals seeking eco-credentials, but industrialization barriers persist around moisture ingress. As a result, plastic retains volume leadership while foil captures value growth, ensuring balanced material portfolios inside the blister and thermoform contract packaging services market.

By Service Type: Serialization Drives Premium Service Growth

Primary operations, forming, filling, and heat sealing, accounted for 41.05% of 2025 revenue, underpinning long-term supply contracts. Yet, serialization and track-and-trace lines are on pace for a 6.89% CAGR through 2031, as more jurisdictions legislate for traceability. The blister and thermoform contract packaging services market size, attached to compliance services, will expand as Italy completes its Bollino sunset and the Asia-Pacific markets adopt GS1-compatible protocols. Providers integrating Level-3 repositories and EPCIS messaging secure multi-year extensions because switching vendors mid-rollout is prohibitively complex.

Secondary packs such as cartons and wallet assemblies deliver margin-enhancing extras, including booklet labels or RFID tags. Design-for-manufacture consulting helps clients shrink pack footprints and cut freight costs. Meanwhile, validation and stability testing grow in tandem with nitrosamine mitigation guidelines that call for packaging as a critical control point. Together, these premium services deepen customer stickiness and differentiate suppliers in the blister and thermoform contract packaging services market.

By End-use Industry: Food Segment Accelerates While Pharma Dominates

Pharmaceuticals retained 57.62% dominance in 2025, underpinned by strict GMP audits and the need for USP-class contact materials. Prescription brands value partners that combine blister agility with clinical packaging suites, driving predictable baseline volumes. At the same time, the food and beverage channel is expected to log a 6.63% CAGR as portion control and e-commerce-ready packs gain traction. Convenience-oriented formats honey sticks, vitamin gummies, and instant coffee tablets, shift into aluminum-foil blisters to prolong shelf life and deter tampering. The blister and thermoform contract packaging services market size, as represented by food clients, should expand accordingly.

Consumer electronics and cosmetics each occupy smaller niches, relying on clamshells or thermoformed trays for visual merchandising and anti-theft security. Cross-industry expertise enables contract packagers to incorporate child-resistant features from pharmaceuticals into household cleaner pods, broadening revenue diversity. While pharma remains the anchor segment, providers investing in allergen-free food halls and ISO 13485-certified medical-device cells can weather cyclical swings and capture a broader wallet share within the blister and thermoform contract packaging services market.

Geography Analysis

Asia-Pacific held 42.73% of global revenue in 2025 and is projected to grow at a 6.51% CAGR through 2031, reflecting robust ingredient manufacturing clusters and supportive policy frameworks. China’s National Medical Products Administration will enforce updated GMP rules on packaging materials from January 2026, raising barriers to entry but favoring compliant contract packagers. Malaysia, Indonesia, and Vietnam each introduced staggered serialization mandates, steering multinational drug makers toward pan-regional suppliers that already run EU FMD-ready lines.

North America ranks second in scale, benefiting from supply-chain resilience programs that aim to increase domestic API output from its current 10% share. PCI Pharma Services and Sharp Services have together earmarked USD 465 million for United States expansions in 2025, with new blister rooms incorporating digital twin models to optimize uptime. FDA proximity and faster label-change approvals enhance the region’s appeal for rapid launches and orphan-drug packaging.

Europe maintains substantial demand, driven by dense innovator pipelines and stringent sustainability legislation. The region’s Extended Producer Responsibility fees already tilt the cost models in favor of recyclable polypropylene blisters, prompting contract packagers to expand their mono-material capacity. Italy’s February 2025 switch to EU FMD coding, combined with Germany’s advanced e-health card integration, pushes average serialization complexity higher than any other continent. [2]“Italy Serialization,” SEA Vision Group, seavision-group.com. Collectively, these geographic dynamics ensure the blister and thermoform contract packaging services market continues balancing volume leadership in Asia-Pacific with compliance-driven value creation in mature Western economies.

Competitive Landscape

The blister and thermoform contract packaging services market remains moderately fragmented, with the top five providers controlling approximately 45% of the global revenue. Expansion has centered on capacity and technology upgrades rather than pure price competition. Aenova devoted EUR 20 million (USD 22 million) to lift German blister output to 220 million units annually, illustrating how European providers scale niche centers of excellence.[3]Bobby Douglas, “Blister Packaging Solutions,” Packaging Strategies, packagingstrategies.com Sharp and PCI invested in AI-guided vision systems that cut defect rates by 40% while enabling real-time release, a significant qualifier in high-margin biologic launches.

M&A activity accelerated in 2024 as private equity funds assembled regional specialists into global platforms, boosting purchasing power for aluminum foil and serialization software licences. Providers differentiate by bundling design testing, cold-chain logistics, and regulatory consulting into turnkey packages. Sustainable-material expertise also emerges as a competitive moat; firms that validated polypropylene blisters early now enjoy first-mover pricing premiums. Smaller regional players carve out niches in dietary supplements or veterinary therapeutics, leveraging lower overhead to serve mid-tier brands. This strategic segmentation keeps buyer options open and prevents rapid market concentration inside the blister and thermoform contract packaging services market.

Looking forward, digital thread integration from ERP to packaging lines will underpin next-generation competitiveness. Predictive maintenance based on digital twins helps maximize uptime during multi-SKU campaigns, and blockchain-linked traceability adds tamper-proof audit trails. Providers that master these technologies alongside recyclability innovations will capture disproportionate contract renewals. However, ongoing raw-material volatility and labor-skill shortages pose headwinds, maintaining a balanced yet dynamic structure within the blister and thermoform contract packaging services market.

Blister And Thermoform Contract Packaging Services Industry Leaders

Packaging Coordinators, Inc.

Catalent Pharma Solutions, Inc.

Wasdell Contract Packing Ltd.

Ropack Inc.

Sharp Services, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sharp Services announced a USD 100 million expansion across United States and European sites to add sterile filling and new blister suites, with Pennsylvania and Belgium lines due online by December 2025.

- September 2025: SÜDPACK Medica introduced NutriGuard, a polypropylene recyclable blister for nutraceuticals, allowing integration into standard recycling streams and lower Extended Producer Responsibility fees.

- July 2025: The WHO released TRS 1060 guidelines that include packaging-centric chapters on nitrosamine risk control, prompting contract packagers to upgrade material risk assessments.

- May 2025: Amcor Flexibles launched its patented Opening Feature child-resistant lidding, reducing pack size by 40% while retaining 98% senior-friendliness.

Global Blister And Thermoform Contract Packaging Services Market Report Scope

| Plastic Films |

| Aluminum Foil |

| Paper and Paperboard |

| Other Material Types |

| Primary Packaging |

| Secondary and Tertiary Packaging |

| Design and Prototyping |

| Testing and Validation |

| Serialization and Track-and-Trace |

| Pharmaceuticals |

| Consumer Electronics |

| Food and Beverage |

| Personal Care and Cosmetics |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Plastic Films | ||

| Aluminum Foil | |||

| Paper and Paperboard | |||

| Other Material Types | |||

| By Service Type | Primary Packaging | ||

| Secondary and Tertiary Packaging | |||

| Design and Prototyping | |||

| Testing and Validation | |||

| Serialization and Track-and-Trace | |||

| By End-use Industry | Pharmaceuticals | ||

| Consumer Electronics | |||

| Food and Beverage | |||

| Personal Care and Cosmetics | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

Which region leads in terms of revenue for contract blister and thermoform services?

Asia-Pacific held 42.73% of global revenue in 2025 and is also the fastest-growing region.

Why are serialization services growing so quickly?

Regulatory mandates in Europe, North America, and emerging Asia-Pacific markets require unit-level traceability, pushing serialization services to a 6.89% CAGR over 2026-2031.

Which material is gaining popularity over traditional PVC films?

Aluminum foil blisters are posting a 6.55% CAGR due to their superior barrier protection and tamper-evident properties.

How fragmented is the competitive landscape?

The top five providers account for slightly more than 45% of global revenue, indicating moderate fragmentation.

What drives food and beverage companies to adopt blister formats?

Unit-dose convenience and extended shelf life are propelling food and beverage blister adoption at a 6.63% CAGR.

Page last updated on: