NOR Flash For Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.04 Billion |

| Growth Rate (2025 - 2030) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

NOR Flash For Communication Market Analysis by Mordor Intelligence

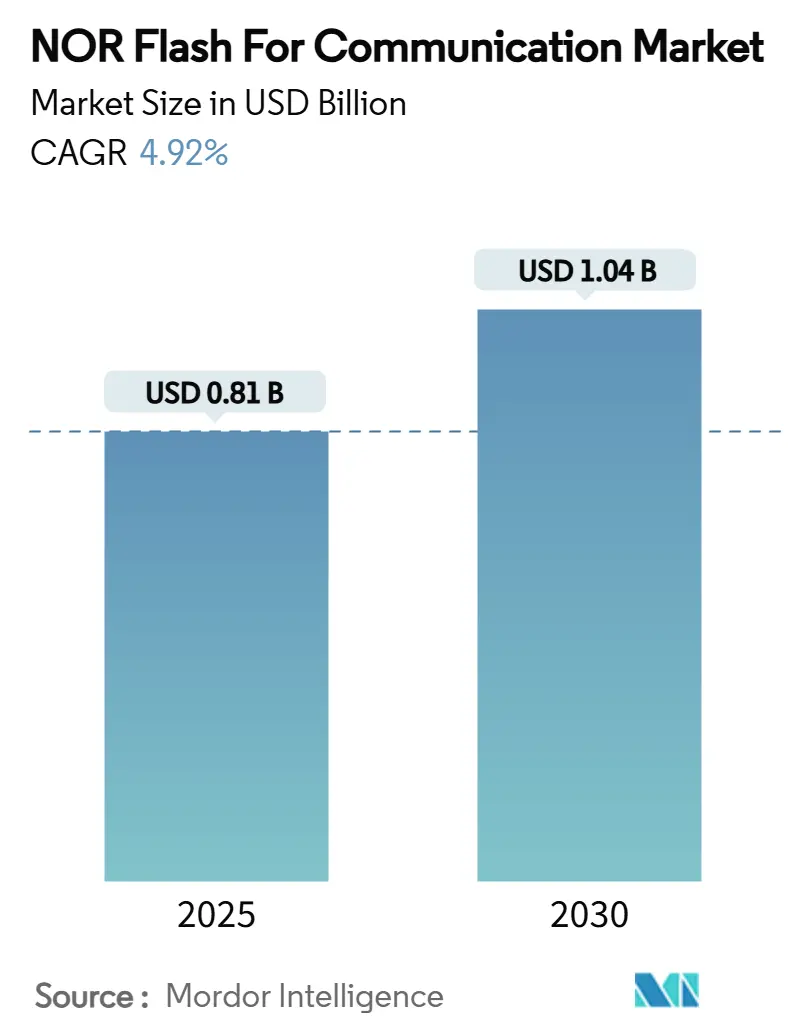

The NOR flash for communication market size is valued at USD 0.81 billion in 2025 and is forecast to reach USD 1.04 billion by 2030, advancing at a 4.92% CAGR. Growth is anchored in 5G roll-outs that demand low-latency boot code memory and in rising security requirements for over-the-air firmware updates. Small-cell deployments, Wi-Fi 6/6E gateways, and optical transport upgrades are boosting high-density serial devices, while satellite-linked applications encourage radiation-hardened variants. Interface innovation, chiefly the leap from QSPI to Octal/HyperBus, is intensifying performance competition and nudging average densities upward. Meanwhile, escalating mask-set costs curb new fab entrants, tightening supply diversity even as edge computing and LPWAN IoT nodes extend product lifecycles.

Key Report Takeaways

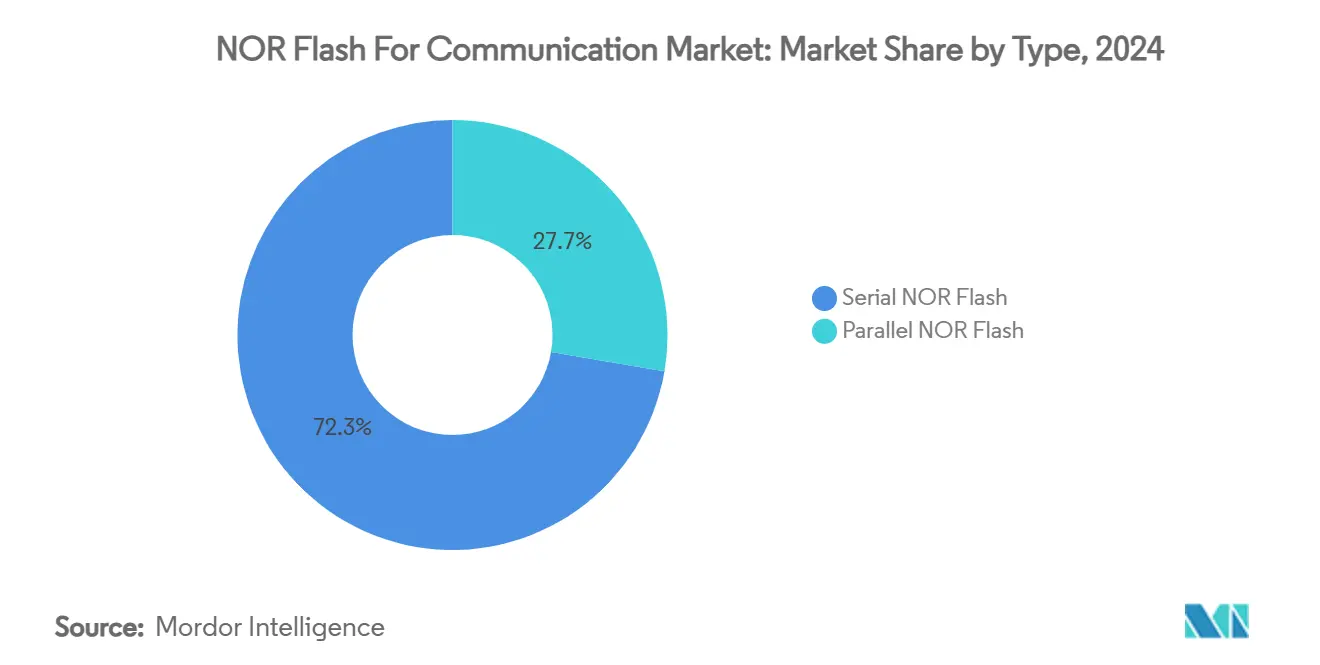

- By type, Serial NOR led with 72.3% revenue share in 2024; Octal SPI variants are forecast to grow at a 5.0% CAGR through 2030.

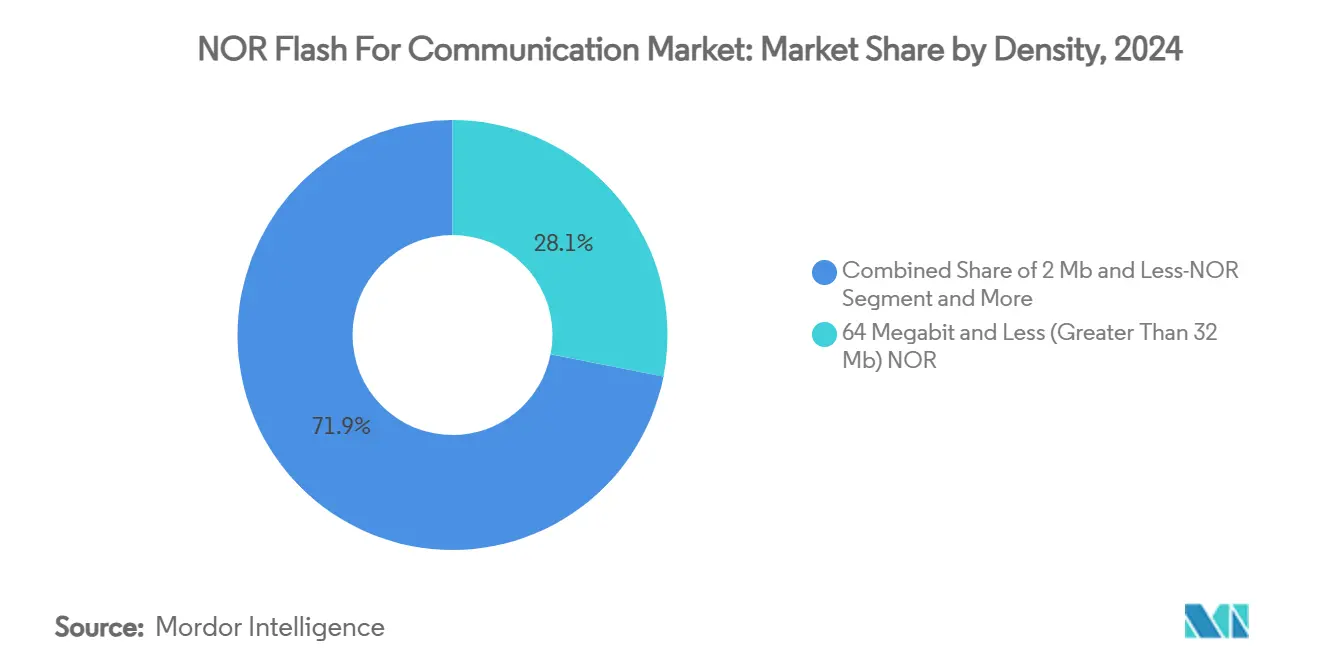

- By density, the 32-64 Mb tier held 28.1% of the NOR flash for communication market size in 2024, while greater than 256 Mb parts are set to expand at a 5.2% CAGR to 2030.

- By interface, QSPI commanded 45.4% revenue share in 2024; Octal SPI/HyperBus grows quickest at a 5.1% CAGR.

- By voltage, the 3 V class held 39.7% market share in 2024; wide-voltage (1.65 V–3.6 V) solutions are projected to post a 5.4% CAGR between 2025-2030.

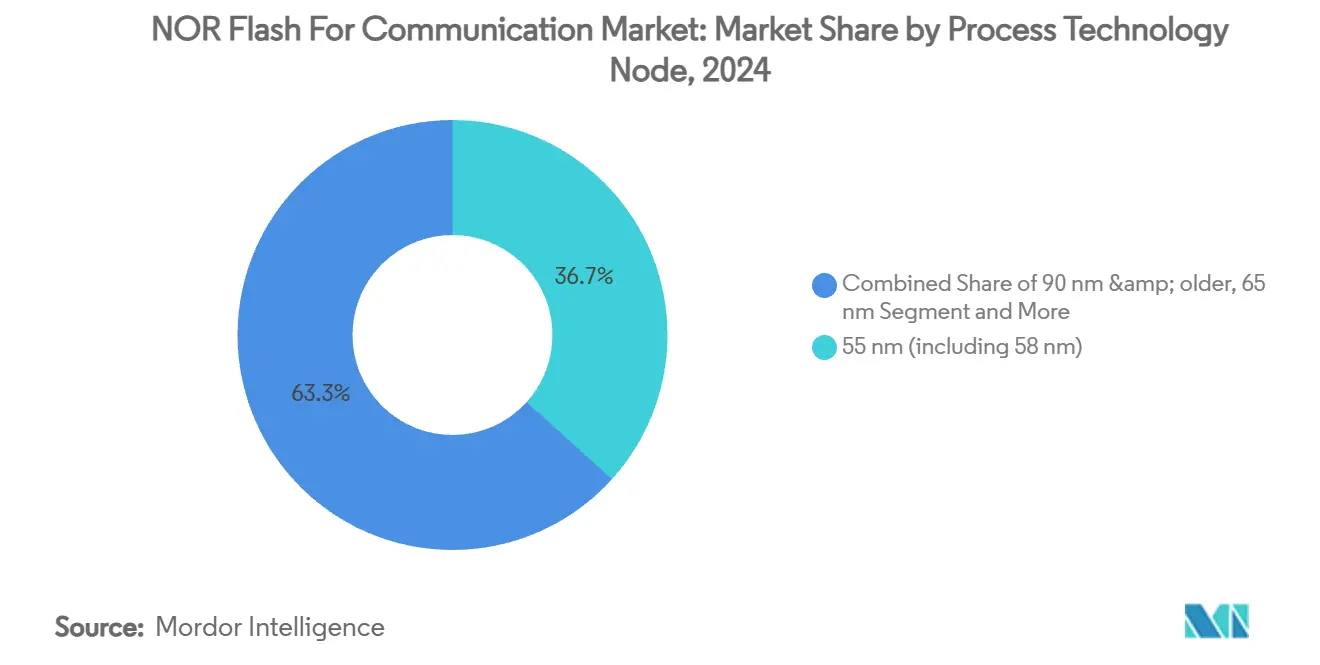

- By process node, 55 nm devices accounted for 36.7% of 2024 sales; 28 nm and below nodes are expected to grow at a 5.3% CAGR.

- By packaging, BGA/FBGA dominated with a 37.2% share in 2024; WLCSP/CSP formats will register a 5.1% CAGR through 2030.

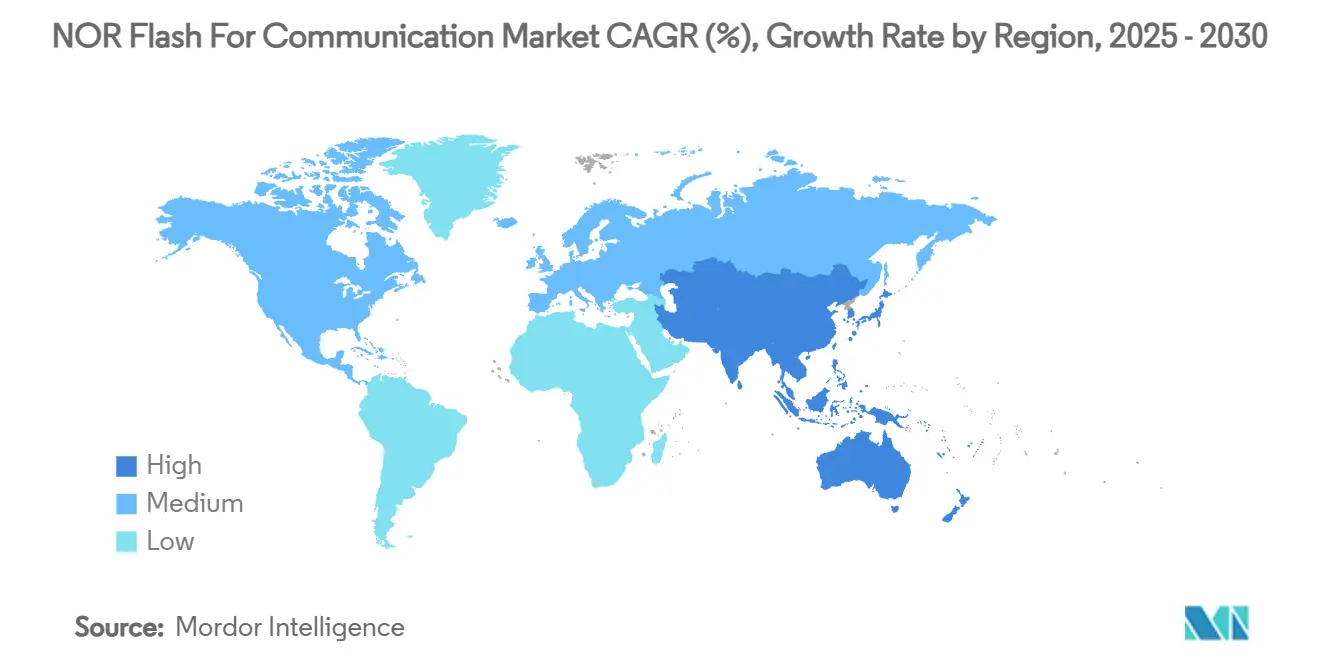

- By geography, Asia-Pacific retained 30.1% of 2024 revenue and will expand at the highest regional CAGR of 5.6% during 2025-2030.

Global NOR Flash For Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of 5G small-cell base stations | 3.40% | East Asia, spillover to North America and Europe | Medium term (2-4 years) |

| Migration of optical transport to 25G+ PAM-4 | 3.00% | North America and Europe | Medium term (2-4 years) |

| Wi-Fi 6/6E gateway adoption | 2.50% | North America, spillover to Europe and developed APAC | Short term (≤ 2 years) |

| Chinese IoT modules shifting to MCU-based LPWAN | 2.00% | China and broader APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of 5G Small-Cell Base Stations Driving NOR Flash Demand

The ongoing densification of 5G networks in China, South Korea, and Japan is translating into millions of small cells that each embed one to four serial NOR devices for secure boot and configuration storage. Densities from 32 Mb to 256 Mb prevail, with Octal SPI parts gaining traction for their 400 MB/s read rates that help radios resume in milliseconds. Functional safety certifications such as Infineon’s SEMPER ASIL-D grade are increasingly specified for edge-mounted radios exposed to harsh climates[1]Infineon Technologies AG. "Infineon delivers industry's first radiation-hardened-by-design 512 Mbit QSPI NOR Flash memory for space and extreme environment applications." November 18, 2024. . Vendors that align with telecom-class temperature and vibration standards capture early-stage design-ins, locking in multiyear volumes and underpinning the NOR flash for communication market.

Optical Transport Systems Upgrade Driving Resilient Memory Demand

Global carriers are shifting long-haul and metro links toward 25 Gbaud and PAM-4 modulation, doubling firmware complexity and pushing memory endurance to new limits. QuadSPI and Octal SPI devices with robust error-correction architectures are favored to ensure deterministic boot in high-EMI racks. STMicroelectronics integrated dual-die schemes that isolate mission-critical boot images from updatable code, ensuring continuous operation during field upgrades. As vendors refresh gear on a seven-year cadence, demand concentrates in 128 Mb–512 Mb tiers, cushioning ASP erosion and reinforcing the NOR flash for communication market.

Wi-Fi 6/6E Gateway Adoption Accelerates NOR Flash Integration

North American broadband providers are aggressively swapping legacy gateways for Wi-Fi 6/6E models that sustain gigabit throughput. Firmware sizes swell, pushing average NOR density from 16 Mb to 32 Mb, while EU Radio Equipment Directive compliance propels built-in cryptographic accelerators. Winbond’s secure flash series meets the 2025 cybersecurity mandate, enabling rapid drive-by updates without service interruption. This refresh wave feeds a double-digit unit surge and enlarges the NOR flash for communication market.

Chinese IoT Module Makers Pivot to Octal SPI NOR Solutions

Low-power wide-area modules for metering and asset tracking are migrating from discrete MCU plus SPI to integrated SoCs that exploit Octal interfaces for near-XIP performance. GigaDevice’s GD25/55 family reaches 400 MB/s and spans 2 Mb–2 Gb, aligning with industrial safety norms and battery life goals[2]GigaDevice. "Embedded World: GigaDevice Showcases Advances in Flash and ..." March 10, 2025. . Expanding volumes across smart-city deployments in Shenzhen and Shanghai propel localized supply chains and intensify competition within the NOR flash for communication market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mask-set costs beyond 28 nm | -3.00% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Substitution by eMMC/UFS in mid-range phones | -2.50% | China, South Korea, Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Mask-Set Costs Creating Barriers to Market Entry

Advanced mixed-signal BCD flows require up to USD 1 million per mask set, deterring startups and constraining differentiated offerings. Capital-rich incumbents therefore enjoy longer node monopolies, slowing price competition. The Semiconductor Industry Association notes that more than USD 540 billion in announced US fabrication investment still aggregates around a handful of firms, reinforcing moderate concentration[3]Semiconductor Industry Association. "SIA-Comments-Section-232-Investigation." May 7, 2025. . Limited diversification could leave OEMs exposed to supply hiccups and temper unit elasticity in the NOR flash for communication market.

Smartphone Storage Shift Impacting Mid-Range NOR Flash Demand

Mid-tier handsets increasingly bundle high-density UFS 4.0 packages that combine code and user storage, displacing discrete NOR. Kioxia’s 4,640 MB/s UFS parts exemplify the performance delta that tempers NOR attach rates in handset motherboards. As densities surpass 256 Gb, OEMs rationalize BOM counts, trimming the smartphone contribution to the NOR flash for communication market even though embedded NOR retains footholds in RF transceivers and power-management subsystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type Serial NOR Dominates Communication Infrastructure

Serial NOR controlled 72.3% of 2024 revenue, benefiting from small footprints and straightforward host controllers that suit compact radios and optical modules. In 2025, the NOR flash for communication market size for Serial devices is already growing, reflecting entrenched design wins. Transition momentum favors Octal variants because their eight-lane bus elevates read rates to 400 MB/s without costly pin counts, a feature prized by 5G distributed units. Infineon’s SEMPER portfolio, now ASIL-D certified, underscores how safety credentials differentiate the supplier.

Parallel NOR’s niche persists in legacy backplanes where true memory-mapped execution eliminates latency. Although share slips below 20%, rugged base-band cards still source 128-Mb parallel devices for deterministic boot. Caching mechanisms in modern SoCs reduce the penalty of serial reads, yet defense and industrial customers value parallel synchronous throughput. GigaDevice’s GD25NE dual-supply family shows how vendors repackage power rails to bridge new SoC voltages with existing boards. Such cross-generation compatibility sustains parallel demand and underpins supplier revenue continuity in the NOR flash for communication market

By Interface Standard QSPI Dominance Challenged by Octal Innovations

QSPI commanded a 45.4% share in 2024, owing to four-lane efficiency and backward compatibility. Microchip’s SuperFlash tech slashes sector-erase times, enabling swift field upgrades that minimize downtime in telecom cabinets. The ubiquity of QSPI controllers across MCU portfolios keeps integration friction low and accelerates time-to-revenue for the NOR flash for communication market.

Octal SPI and HyperBus lines, however, are surging at 5.1% CAGR. HyperBus pairs 400 MB/s bandwidth with only 12 pins, permitting slim PCB traces in massive MIMO radios. Infineon’s companion HyperRAM shares the bus, consolidating interconnects and trimming BoM costs. As ASICs adopt xSPI JESD251 compliance, eight-lane devices will siphon share, widening differentiation levers for suppliers inside the NOR flash for communication market.

By Density 32-64 Mb Sweet Spot Balances Performance and Cost

The 32-64 Mb class held a 28.1% NOR flash for communication market share in 2024 by addressing typical boot, configuration, and secure firmware storage for gateways and small cells. Mature 55-nm processes mean yields exceed 95%, capping die cost and preserving margins.

256 Mb densities are accelerating at 5.2% CAGR because complex 5G radios and encrypted optical line cards demand larger images and redundancy partitions. Micron’s 1 Gb SPI NOR introduces 200-MHz QIO mode, allowing near-instant context restoration[4]Micron Technology, Inc. "Micron Unveils Complete High-Density 45nm Automotive-Grade NOR Flash Portfolio." November 13, 2018. . For satellite payloads, Infineon’s 512 Mb radiation-hardened QSPI extends data retention to 20 years in orbit. Such breakthroughs expand viable use cases and diversify revenue streams inside the NOR flash for communication market.

By Voltage: Broad 3 V Base Transitions Toward Wide-Voltage Flexibility

The 3 V class commanded 39.7% of the NOR flash for communication market share in 2024, reflecting decades of design inertia across base stations, switches, and industrial routers. The demand has increased as OEMs favor the proven reliability of 3.3 V parts for robust power-supply margins. Infineon’s SEMPER portfolio supports this standard, providing drop-in upgrades that keep qualification cycles short. The large installed base ensures steady replacements even as other voltage tiers attract new projects.

Wide-voltage (1.65 V–3.6 V) devices are forecast to post a 5.4% CAGR, the fastest among voltage classes, as designers consolidate multiple rails and strive for greater energy efficiency. These solutions allow a single part number to serve battery-powered CPE, PoE small cells, and line-card controllers, cutting SKU complexity. GigaDevice’s GD25NE dual-supply SPI illustrates the pivot toward parts that run at 1.2 V logic yet tolerate 3.3 V flash erase. Ultra-low-voltage subsets below 1.8 V remain niche, powering coin-cell sensors where waking firmware straight from flash keeps quiescent draw in the nanowatt range.

By Process Technology Node: Mature 55 nm Leads While 28 nm Accelerates

The 55 nm node delivered 36.7% of 2024 revenue, its favorable cost-yield balance and well-characterized reliability make it the default for 32 Mb–128 Mb serial parts. Micron leverages similar 65 nm flows to hit quad I/O speeds that outpace older generations. OEMs value predictable supply, and many telecom qualifications expressly name 55 nm lots for production stability.

Advanced 28 nm and below processes are projected to climb at a 5.3% CAGR as 1 Gb and 2 Gb densities gain steam for edge AI radios and secure satellite payloads. Shrinking cell sizes cut cost per bit and lower active power, but mask-set expenses and yield maturation temper the ramp. Radiation-hardened 40 nm flows bridge the gap for space-borne gear where cost is secondary to single-event immunity, showing how various nodes coexist to meet divergent risk and price targets.

By Packaging Type: BGA/FBGA Platform Confronts WLCSP Miniaturization

BGA/FBGA packages captured 37.2% of 2024 sales. Their low-inductance solder spheres and superior heat dissipation align with Octal SPI’s 400 MB/s bursts and with base-band cards that cycle through harsh temperature swings. SEMPER parts in BGA form keep impedance controlled across multilayer PCBs, ensuring signal fidelity at 200 MHz reads. QFN/SOIC frames serve cost-driven gateways where single-lane SPI suffices and board space is less constrained.

WLCSP/CSP options will register a 5.1% CAGR as handset RF modules, wearable radios, and system-in-package assemblies squeeze footprints below 25 mm². Die-level redistribution layers shorten electrical paths, raising signal integrity while reducing z-height to under 300 µm. IoT makers shift to this format to free antenna clearance and simplify automated optical inspection. Stacked die and custom cavity packages fill specialized slots such as in-line memory with adjacent microcontrollers for tamper-resistant smart meters, illustrating how packaging strategy shapes long-term supplier positioning within the NOR flash for communication market.

Geography Analysis

Asia-Pacific contributed 30.1% of 2024 revenue and is set to expand at 5.6% CAGR, powered by China’s self-sufficiency push and Japan’s early 6G pilot sites. Winbond expects balanced supply-demand in 2025 as the automotive and smart-home sectors rebound, underscoring how regional fabs anchor resilience. Local sourcing reduces logistics risk and trims lead-time variance, keeping OEM production on schedule and magnifying the NOR flash for communication market impact.

North America ranks second, buoyed by cloud and edge infrastructure buildouts. The CHIPS Act unlocks domestic capacity, complementing Micron’s high-density lines and cushioning geopolitical uncertainties. A strong pipeline of Wi-Fi 6/6E gateway deployments further widens the addressable NOR flash for communication market, while strict cybersecurity rules propel secure-element integration.

Europe holds a steady share as operators modernize 5G core networks and industrial clients digitalize production. The EU Radio Equipment Directive enforces device-level encryption and authenticated boot, compelling OEMs to embed security-enhanced NOR variants. Meanwhile, the Middle East and Africa ramp up metro fiber and smart-city grids, creating fresh volume pockets. South America advances 4G-to-5G migration across urban clusters, ensuring a diverse, though fragmented, contribution to the NOR flash for communication market.

Competitive Landscape

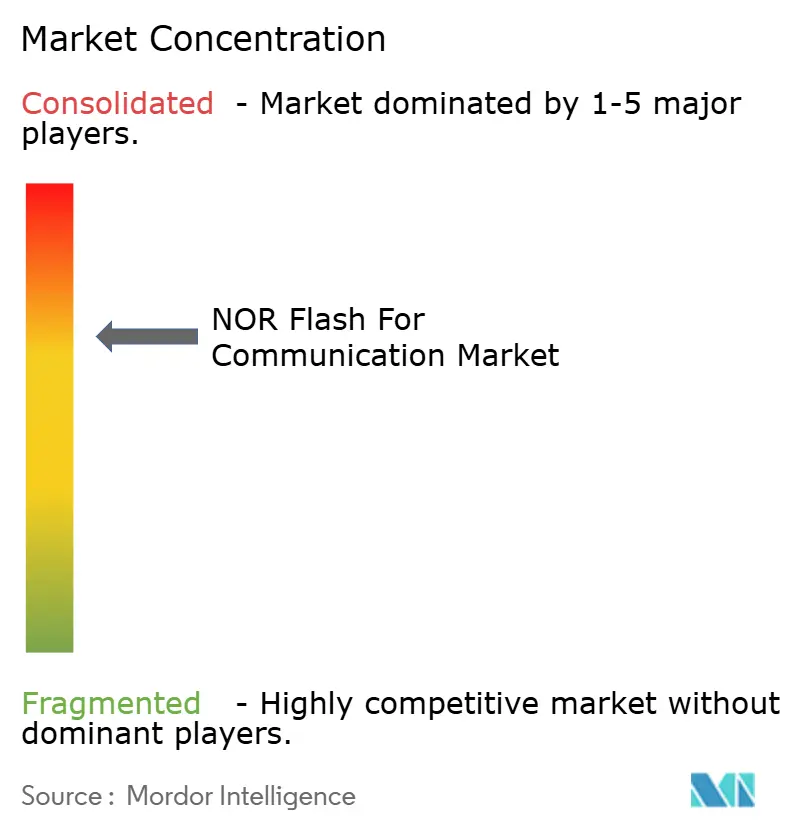

The top five suppliers capture roughly 65-70% of sales, indicating moderate concentration. Winbond led the market, trailed by Macronix and GigaDevice. Chinese challengers raise scale quickly, narrowing process gaps and offering price leverage to OEMs. Patent filings such as mixed NOR-NAND arrays that share peripheral circuits hint at future density leaps without node shrinks. Vendors differentiate via interface breadth, functional safety credentials, and supply chain transparency. Strategic alliances with foundries and controller IP houses expedite next-gen product releases, ensuring the NOR flash for communication market remains innovation-intensive.

Established firms focus on application-specific variants, for example, radiation-hardened parts for satellite constellations. Infineon’s 512 Mb QSPI delivers class-leading SEE immunity for LEO and GEO orbits. Macronix counters with 3D NOR prototypes that break planar density ceilings. Smaller players target 1.2 V serial NOR for wearables, leveraging niche voltage compatibility to secure sockets. Such maneuvers keep pricing rational and sustain a balanced yet dynamic NOR flash for communication market.

NOR Flash For Communication Industry Leaders

-

Infineon Technologies AG

-

Micron Technology Inc.

-

GigaDevice Semiconductor Inc.

-

Macronix International Co. Ltd.

-

Winbond Electronics Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon’s SEMPER NOR family secured ASIL-D certification from SGS-TÜV.

- March 2025: GigaDevice showcased GD25/55 serial NOR family with ISO 26262 ASIL-D compliance at Embedded World 2025.

- March 2025: GigaDevice launched GD25NE dual-supply SPI NOR targeting 1.2 V SoCs.

- January 2025: Macronix introduced 3D NOR flash technology to overcome planar capacity limits.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the communication NOR flash memory market as the revenue generated from stand-alone serial and parallel NOR chips that embed boot code, secure firmware, and configuration data inside telecom and networking equipment such as 5G small-cell base stations, fiber-optic transport systems, carrier gateways, and Wi-Fi 6/7 access points. Parts mounted inside smartphones, PCs, or generic consumer devices are excluded from this scope.

Scope exclusion: Consumer electronics, automotive, and industrial NOR demand are outside the present assessment.

Segmentation Overview

-

By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

-

By Density (Value)

- 2 Megabit And Less NOR

- 4 Megabit And Less-NOR (greater than 2mb) NOR

- 8 Megabit And Less (greater than 4mb) NOR

- 16 Megabit And Less (greater than 8mb) NOR

- 32 Megabit And Less (greater than 16mb) NOR

- 64 Megabit And Less (greater than 32mb) NOR

- 128 Megabit and Less (greater than 64MB) NOR

- 256 Megabit and Less (greater than 128MB) NOR

- Greater than 256 Megabit

-

By Interface Standard (Value)

- SPI / QSPI

- Octal SPI / HyperBus

- Parallel (x8/x16)

-

By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others (<1.8 V, 2.5 V, 5 V)

-

By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (incl. 58 nm)

- 45 nm

- 28 nm and Below

-

By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Others

-

By Geography (Value, Volume)

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- Taiwan

- India

- South East Asia

- Rest of Asia-Pacific

- Rest of the World

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with memory marketing managers, telecom OEM design leads, and contract manufacturers across Asia-Pacific, North America, and Europe. These discussions validated real-world ASP brackets, secure-boot density preferences, and lead-time constraints, and they filled data gaps around Octal SPI migration timelines spotted in secondary sources.

Desk Research

We start with authoritative electronics trade statistics from sources such as the World Semiconductor Trade Statistics program, UN Comtrade shipment data, and tariff filings that separate serial NOR from other memory classes. Regional telecom regulators, including the FCC and China's MIIT, publish quarterly deployment totals for 5G and fiber nodes, which help our desk team relate memory attach rates to active equipment counts. Standards bodies like JEDEC, GSMA, and the IEEE supply interface roadmaps and density transition timelines. Financial filings, investor decks, and press releases from listed memory vendors enrich average selling price (ASP) tracking, while Dow Jones Factiva provides hard-to-find pricing resets after supply shocks. This list is illustrative; scores of other open sources were consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of annual telecom hardware output. Node shipments by technology (macro, small-cell, edge router, GPON OLT, Wi-Fi CPE) are multiplied by verified NOR attach rates and blended ASPs to create a preliminary demand pool. Bottom-up checks, such as supplier revenue roll-ups and channel inventory audits, are then used to fine-tune totals. Key variables influencing the forecast include 5G base-station installation growth, average firmware image size, interface migration from QSPI to Octal, regional sourcing policies, and silicon wafer yield trends. A multivariate regression that links NOR density mix and telecom node growth to ASP movement drives the 2025-2030 projection, after which scenario analysis adjusts for policy or foundry shocks. Any residual gaps in bottom-up evidence are bridged through conservative density substitution assumptions reviewed with industry experts.

Data Validation & Update Cycle

Outputs pass three rounds of variance and anomaly checks, followed by peer review inside Mordor. We refresh the model annually and trigger mini-updates when pricing spikes, embargoes, or major design wins materially shift outlooks. Before release, an analyst revalidates every data point so clients receive the latest view.

Why Mordor's NOR Flash For Communication Baseline Earns Trust

Published values often diverge because firms bundle wider end-markets, apply undisclosed ASP ladders, or rely on single-source shipment data.

Key gap drivers for our market include scope creep into consumer devices, aggressive density-mix assumptions, and differing update cadences. Mordor keeps the lens fixed on true communication infrastructure demand, aligns densities with telecom qualification logs, and recalibrates ASPs each quarter, which is where Mordor Intelligence differentiates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.81 B (2025) | Mordor Intelligence | - |

| USD 5.27 B (2025) | Global Consultancy A | Counts all end-user segments, applies vendor shipment totals without attach-rate filters |

| USD 1.21 B (2025) | Trade Journal B | Derives NOR share from broader flash market and excludes primary interviews |

| USD 3.15 B (2023) | Industry Portal C | Uses historic global revenue, no telecom-specific segmentation, infrequent refresh |

In sum, our disciplined scope selection, quarterly variable tracking, and mixed-method validation deliver a balanced baseline that decision-makers can trace, question, and reproduce with confidence.

Key Questions Answered in the Report

Which density range will capture the bulk of future demand?

The Greater than 256 Megabit tier is forecast to post a 5.2% CAGR, fueled by complex firmware and security partitions in next-generation radios and optical transport systems.

Why are Octal SPI and HyperBus interfaces gaining attention?

They deliver up to 400 MB/s read bandwidth with modest pin counts, enabling near-DRAM performance for execute-in-place architectures in advanced communication equipment.

How will Europe’s Radio Equipment Directive influence supplier roadmaps?

The August 2025 cybersecurity deadline accelerates adoption of secure NOR parts with hardware-based encryption, compelling vendors to integrate cryptographic engines and secure key storage.

What obstacles limit new entrants in the NOR flash for communication industry?

Mask-set costs above USD 1 million for nodes finer than 28 nm deter fresh fabs, restricting competition and reinforcing reliance on incumbent suppliers.

Page last updated on: