Size and Share of NOR Flash Memory Market for the Automotive Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

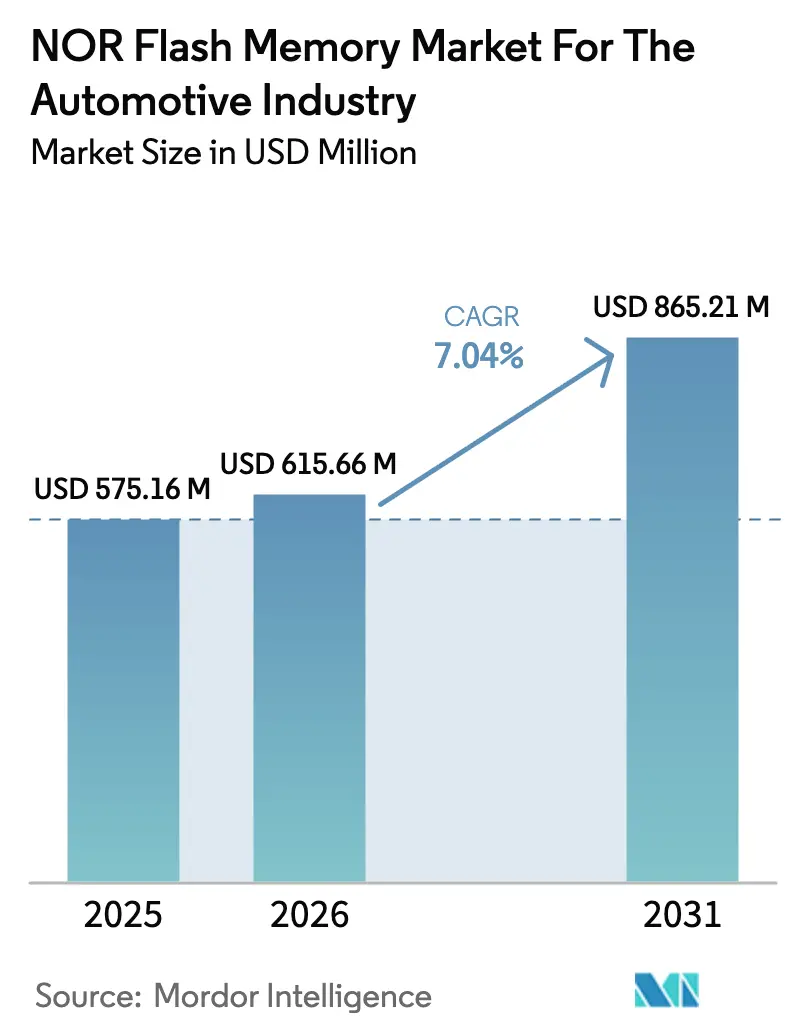

| Market Size (2026) | USD 615.66 Million |

| Market Size (2031) | USD 865.21 Million |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

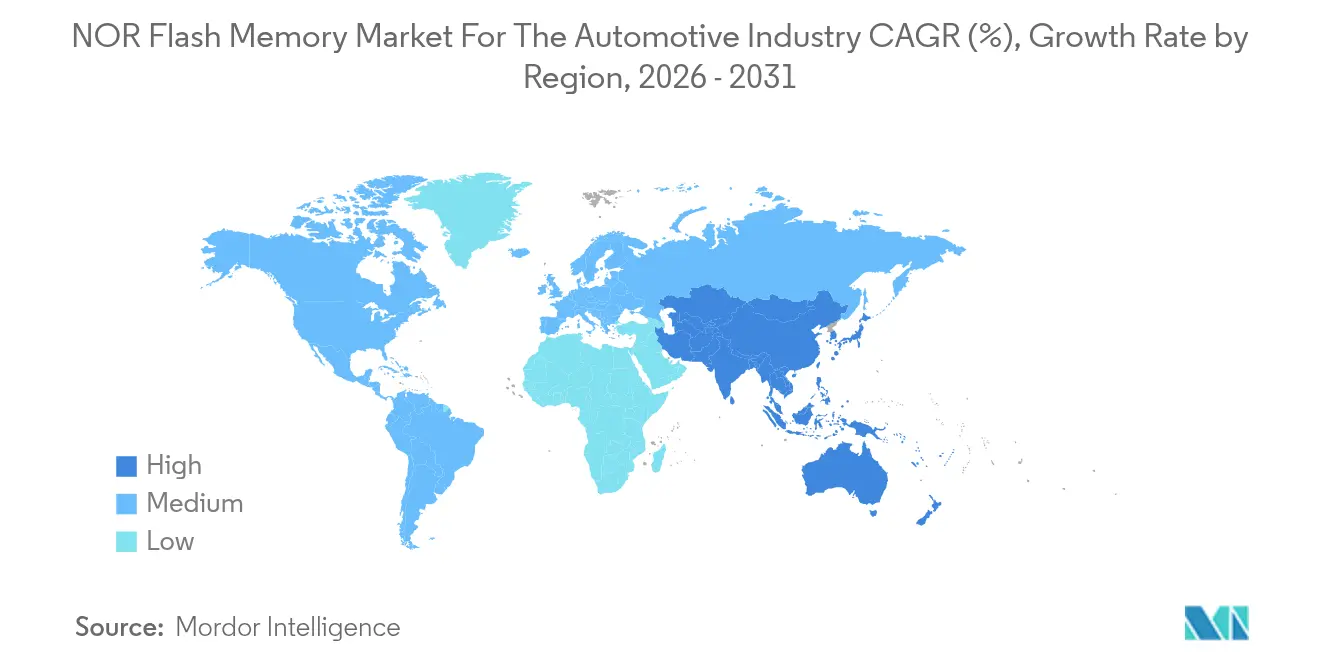

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of NOR Flash Memory Market for the Automotive Industry by Mordor Intelligence

NOR flash memory market size for the automotive industry market size in 2026 is estimated at USD 615.66 million, growing from 2025 value of USD 575.16 million with 2031 projections showing USD 865.21 million, growing at 7.04% CAGR over 2026-2031. Demand is accelerating as software-defined vehicles, advanced driver-assistance systems (ADAS), and domain controllers require instant-on, fail-safe code storage. Octal and xSPI interfaces are shortening secure-boot times to below 20 milliseconds, while the transition to zonal electrical/electronic (E/E) architectures multiplies code density needs. Vehicle electrification adds further momentum because battery-management and power-train controllers operate in harsh thermal and electromagnetic conditions that favor high-reliability NOR. Meanwhile, Chinese wafer expansions are reshaping supply economics and intensifying price competition, prompting incumbents to differentiate through functional-safety certification and low-voltage performance.

Key Report Takeaways

- By type, Serial NOR commanded 80.65% of the NOR flash memory market for the automotive industry share in 2025; Parallel NOR is retreating as pin-count and board-space pressures rise.

- By interface, Quad SPI held 40.62% of the NOR flash memory market for the automotive industry share in 2025, while Octal SPI is projected to expand at 7.12% CAGR through 2031 and will be the fastest-growing cohort.

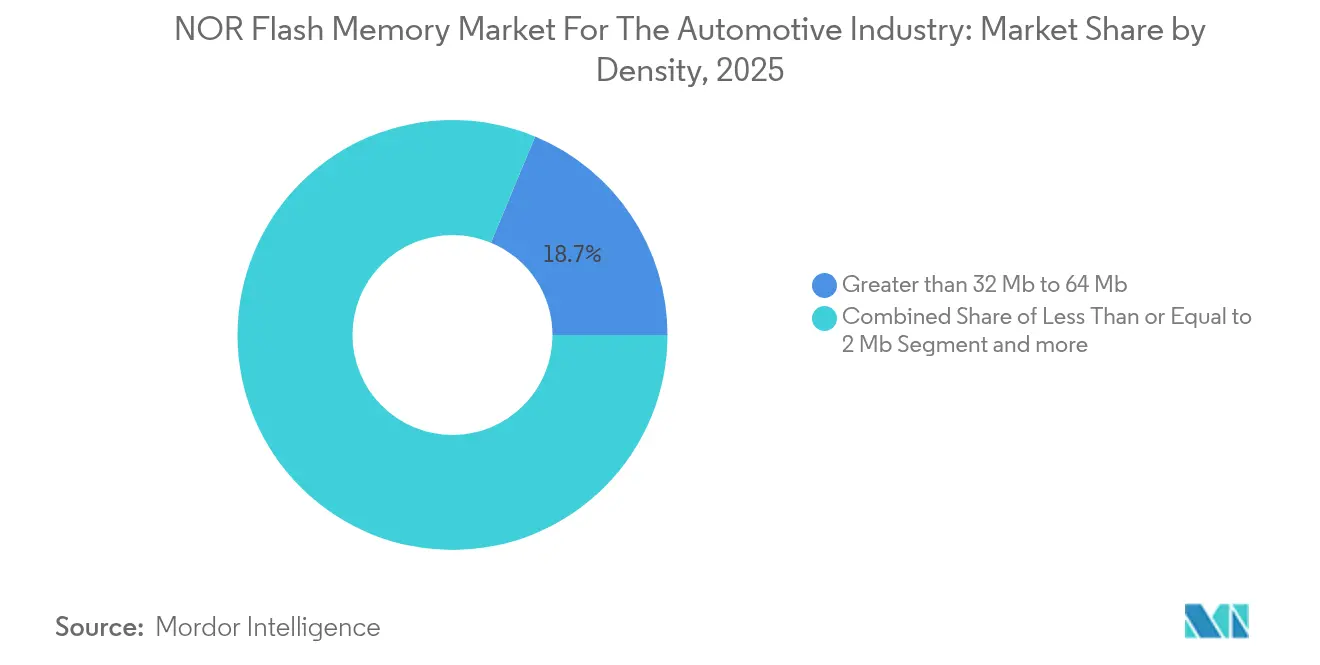

- By density, the greater than 32 Mb to 64 Mb segment led with a 18.72% of the NOR flash memory market for the automotive industry share in 2025, whereas the greater than 128 Mb to 256 Mb category is set to grow at a 7.21% CAGR to 2031.

- By voltage class, 3 V solutions retained a 40.58% of the NOR flash memory market for the automotive industry share in 2025; 1.8 V parts are advancing at a 7.10% CAGR thanks to energy-efficiency mandates in EV designs.

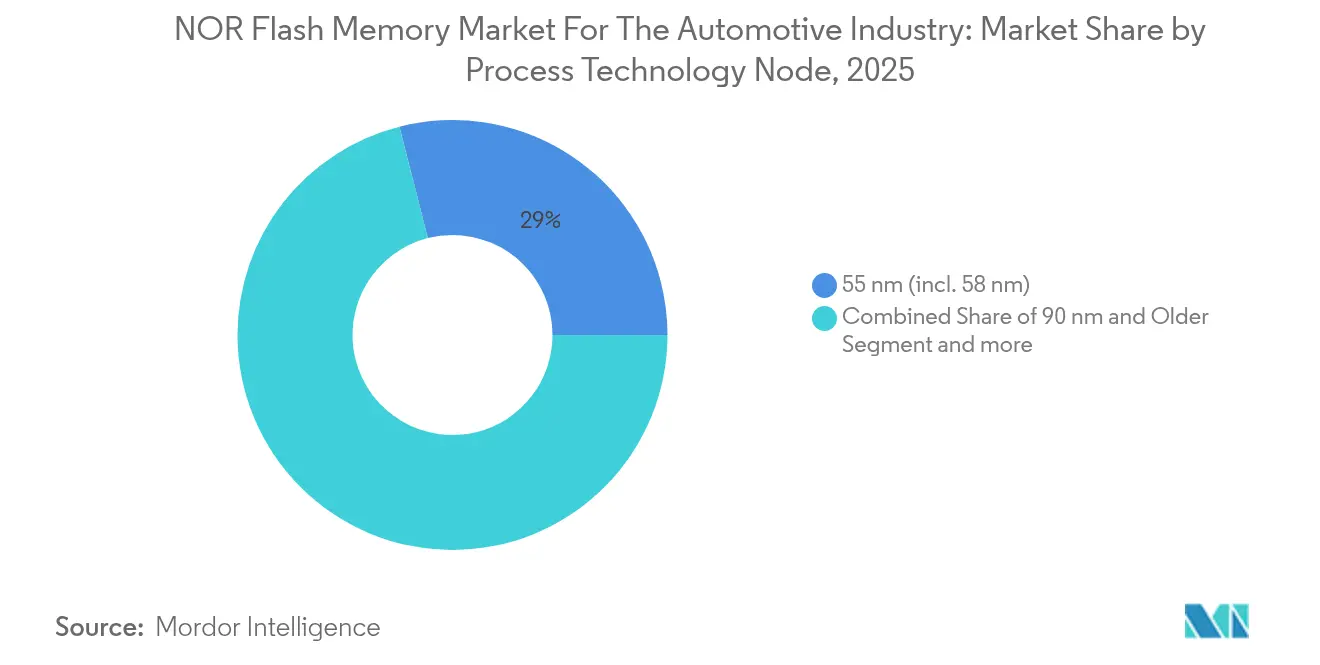

- By process node, 55 nm captured 28.97% of the NOR flash memory market for the automotive industry share in 2025, but 28 nm and below will accelerate at 7.28% CAGR as suppliers pursue higher density.

- By packaging type, QFN / SOIC held a 30.74 % of the NOR flash memory market for the automotive industry share in 2025; WLCSP / CSP are forecast to expand at a 7.33% CAGR.

- By geography, Asia-Pacific remained the largest consumer of the NOR flash memory market for the automotive industry share in 2025; North America and Europe are adopting functional-safety-certified devices fastest.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of NOR Flash Memory Market for the Automotive Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS and domain-controller code expansion | +2.4% | North America, Europe, China | Medium term (2-4 years) |

| Zonal/service-oriented architectures | +1.8% | Global | Medium term (2-4 years) |

| Octal and xSPI proliferation | +1.5% | Global | Short term (≤ 2 years) |

| China 55 nm/40 nm capacity build-out | +1.2% | China; spillover worldwide | Short term (≤ 2 years) |

| EV power-train electrification | +1.1% | Europe, China, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ADAS and Domain-Controller Code Size Explosion Elevating Automotive-grade Serial NOR Demand

Modern vehicle software now exceeds one billion lines of code, pushing firmware footprints well beyond legacy storage limits. ADAS modules already account for a significant share of application demand and require up to four times more code than distributed ECU designs. Micron projects total memory per vehicle to triple by 2026, with high-end models soaring toward 4 TB by 2030.[1]Micron Staff, “Functional Safety for Automotive,” Micron, April 17, 2025, micron.com. This trajectory positions Serial NOR as the de facto instant-boot store for safety-critical logic, creating a measurable uplift in the NOR flash memory market for the automotive industry.

Zonal/Service-Oriented E/E Architectures Requiring Instant-On Boot Memories

Zonal architectures cluster functions by physical domain, obliging memories to wake core subsystems in under 100 milliseconds. Execute-in-place (XIP) ability makes Serial NOR the preferred boot medium, and when coupled with Octal interfaces, read throughput reaches 400 MB/s. Micron’s functional-safety roadmap aligns with this pivot by embedding ASIL mechanisms that address autonomy, electrification, and connectivity in one device suite.[2]Micron Staff, “Micron Xccela Flash Memory,” Micron, April 17, 2025, avnet.com.OEM migration from distributed to zonal topologies is forecast to cover a majority of new platforms by 2030, cementing demand for low-latency NOR.

Octal and xSPI Proliferation Enabling Less Than 20 ms Secure Boot for Software-Defined Vehicles

JEDEC’s xSPI specification and Macronix OctaBus solutions raise transfer bandwidth by 4× over Quad SPI, removing the boot-time bottleneck for safety controllers. Data authentication and over-the-air (OTA) re-flashing complete in seconds instead of minutes, which supports continuous feature deployment in software-defined vehicles. Standardized pinouts reduce engineering risk and have catalyzed cross-vendor adoption during the last design cycle, translating into outsized interface-driven revenue growth for the NOR flash memory market for the automotive industry.

China's 55 nm/40 nm Automotive NOR Capacity Build-Out Supporting OEM Localization

State-backed investment accelerated wafer starts at mainland foundries, allowing GigaDevice and Puya Semiconductor to ship over 100 million automotive-grade units by early 2025. Localization reduces logistics cost and hedges geopolitical risk, but it also amplifies competitive pressure as aggressive pricing compresses ASPs in sub-64 Mb densities. Short-run supply elasticity gives Chinese carmakers greater bargaining power and nudges global incumbents toward advanced-node differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost premium over QSPI NAND Beyond 256 Mb | -0.9% | Global | Medium term (2-4 years) |

| Scaling wall at ≤ 40 nm nodes | -0.7% | North America, Europe | Long term (≥ 4 years) |

| Foundry concentration in Taiwan and PRC | -0.6% | Global | Medium term (2-4 years) |

| ASP compression from new Chinese entrants | -0.5% | Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Premium over QSPI NAND Beyond 256 Mb Limiting Infotainment Deployments

NOR maintains roughly a 35% price delta versus QSPI NAND at greater than 256 Mb densities, discouraging adoption in cost-sensitive infotainment head units. GigaDevice’s hybrid GD5F1GM9 aims to replicate NOR-like reads at NAND-like cost, eroding NOR’s incumbency in non-safety domains. Mid-segment OEMs are therefore deferring high-density NOR design-ins, which tempers the overall NOR flash memory market for the automotive industry trajectory.

Scaling Wall at ≤ 40 nm Steering Roadmaps Toward MRAM/ReRAM for Greater Than 1 Gb Code

Tunnel-oxide physics limit charge retention at deep-submicron dimensions. TSMC’s 22 nm embedded MRAM and 12 nm ReRAM pilots signal industry readiness to pivot for larger code images. NOR vendors must either adopt 3D architectures or cede high-density sockets, introducing structural uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Consolidates Leadership Through Integration Efficiency

Serial NOR captured 80.65% of the 2025 NOR flash memory market for the automotive industry, benefiting from lower pin count and superior electromagnetic compatibility versus parallel devices. The technology’s execute-in-place capability allows direct code execution, which minimizes boot latency, an imperative for ADAS and domain controllers. This dominance is expected to hold as Octal interfaces close the bandwidth gap with parallel variants, preserving Serial NOR’s board-space advantage. Parallel NOR persists chiefly in legacy or bandwidth-saturated infotainment modules, yet its share is projected to decline steadily.

The segment’s momentum hinges on innovations such as Microchip’s split-gate SuperFlash architecture that slashes erase time below 25 ms. As carmakers shift toward centralized and zonal platforms, firmware volume rises, but the preference remains for pin-efficient packages. Consequently, Serial NOR’s share of the NOR flash memory market for the automotive industry size is forecast to edge higher even while absolute capacity per socket grows.

By Interface: Octal SPI Becomes the Fastest-Growing Bus Standard

Quad SPI delivered 40.62% revenue share in 2025, but Octal SPI is advancing at 7.12% CAGR through 2031, propelled by its 400 MB/s read ceiling. The interface enables sub-20 ms cryptographically secure boot, meeting regulatory as well as end-user expectations for instantaneous start-up. Micron’s Xccela family exemplifies this leap by coupling high bandwidth with AEC-Q100 Grade 1 reliability. As JEDEC’s xSPI creates vendor interchangeability, system designers favor Octal to future-proof platforms.

Single/Dual SPI retains a cost niche in basic body-electronics modules but is unlikely to reclaim lost ground. NOR flash memory market for the automotive industry size for Octal solutions is forecast to grow significantly by 2031, while the demand for Quad is anticipated to gradually migrate upward in pursuit of OTA throughput parity.

By Density: Code Expansion Drives High-Density Upswing

The greater than 32 Mb to 64 Mb tier led with a 18.72% share in 2025, yet the greater than 128 Mb to 256 Mb tier is projected to deliver the highest compound growth at 7.21% through the decade. ADAS, domain controllers, and electrified power-train firmware require large executable images plus dual banks for A/B redundancy, driving NOR adoption at densities that were niche five years ago. Serial NOR solutions at 1 Gbit are now sampling for premium trims, a milestone once reserved for NAND.

Lower-density segments, including less than or equal to 2 Mb parts, will continue to service window-lifter modules and sensor interfaces but will account for a diminishing slice of the overall NOR flash memory market for the automotive industry. Conversely, the greater than 256 Mb cohort is entering pilot production for 2026 model-year electric SUVs, indicating future upside despite current ASP sensitivity.

By Voltage: Low-Voltage Devices Sharpen Efficiency in EV Platforms

While 3 V class memories remained mainstream with 40.58% share during 2025, 1.8 V parts are growing at 7.10% CAGR thanks to battery-driven efficiency targets. Winbond’s 1.2 V NOR claims 45% power savings over 1.8 V predecessors. Such savings reduce the need for auxiliary power-management ICs, trimming bill-of-materials costs and thermal load in dashboard clusters.

Wide-voltage (1.65–3.6 V) devices continue to benefit zonal nodes that traverse multiple supply rails. Nevertheless, sub-1.8 V innovation will likely dictate vendor selection as OEM climate targets tighten, reinforcing a gradual mix shift that underpins value growth inside the NOR flash memory market for the automotive industry.

By Process Technology Node: 28 nm and Below Nodes Break Density Ceilings

The 55 nm (including 58 nm) process node secured a 28.97% share in 2025, but 28 nm and below will rise at a 7.28% CAGR, largely to meet code-size expansion while containing die area. Macronix has validated 4 Gb 3D NOR concepts on 45 nm and is migrating select derivatives to 28 nm pilot lines. Advanced lithography reduces read latency and power, furnishing headroom for integrating cryptographic blocks.

Legacy ≥90 nm flows remain profitable where cost trumps density. However, once automotive OEMs mandate 1 GB boot stores, suppliers operating only on mature nodes risk strategic marginalization in the broader NOR flash memory market for the automotive industry.

By Packaging Type: Thermal and Space Constraints Guide Selection

QFN and SOIC formats still dominate under-hood modules due to proven thermals and straightforward automated optical inspection via wettable flanks. In contrast, wafer-level CSPs are penetrating camera ECUs and digital instrument clusters where height and mass are tightly bounded. BGA/FBGA holds ground in head units and domain controllers that demand high I/O counts to exploit Octal throughput.

Specialized packages with enhanced vibration damping are emerging for electric power-trains. These form-factor choices illustrate how mechanical integration strategy directly influences the NOR flash memory market for the automotive industry adoption patterns.

Geography Analysis

North America contributed a substantial share of the Automotive NOR flash shipments in 2025 as Detroit and Silicon Valley allies accelerated software-defined vehicle programs. Regulatory focus on cybersecurity pushes adoption of secure-boot, authenticated update memory. Policy incentives under the CHIPS Act aim to localize crucial semiconductors, which could gradually derisk trans-Pacific logistics.

Europe remains pivotal because premium marques embed zonal architectures first, pulling through high-bandwidth NOR. Stringent ISO 26262 compliance norms continue to shape procurement toward ASIL-certified devices. The European Union’s plan to double chip manufacturing capacity by 2030 concentrates on larger-node automotive flows, a strategic hedge against Far-East disruptions.

Asia-Pacific is the volume engine of the NOR flash memory market for the automotive industry; China’s aggressive fabrication build-out at 55 nm/40 nm unlocks supply for its surging EV sector while exerting downward price pressure globally. Japan and South Korea rely on established IDM ecosystems for consistent automotive-grade quality, whereas Taiwan’s centrality to advanced lithography introduces systemic geopolitical risk. The ASEAN+3 bloc forecasts steady macroeconomic growth through 2026, sustaining electronics export momentum.

Competitive Landscape

Infineon, Winbond, Macronix, and GigaDevice together control roughly 60-65% of global automotive NOR revenue. Infineon deepens defensibility by coupling SEMPER NOR with its AURIX microcontrollers, creating a platform-level lock-in. Winbond differentiates through low-voltage innovation aimed at EV range maximization. Macronix focuses on Octal performance and acquired ISO 26262 ASIL-D credentials earlier than rivals, securing sockets in European flagship models.

Chinese challenger GigaDevice leverages domestic foundry partnerships to offer aggressive pricing and local support, pursuing a share-gain strategy in smart cockpit and ADAS ECUs. Incumbents respond with roadmaps for 3D NOR and embedded MRAM to leapfrog density constraints, signaling a strategic pivot to heterogeneous memory portfolios. Foundry concentration remains a latent fragility; thus, multi-sourcing agreements and strategic inventory buffers have become standard in long-term supply contracts.

Leaders of NOR Flash Memory Market for the Automotive Industry

Winbond Electronics Corporation

Macronix International Co. Ltd

Infineon Technologies AG

Micron Technology Inc.

Gigadevice Semiconductor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon’s SEMPER NOR family achieved ASIL-D certification, underpinning a market-access strategy focused on functional-safety leadership for consolidated domain controllers.

- April 2025: TSMC disclosed 12 nm ReRAM and 22 nm embedded MRAM roadmaps, positioning itself as the manufacturing partner of choice for next-generation code-storage technologies and signaling a hedging strategy against NOR scaling limits

- March 2025: GigaDevice rolled out GD5F1GM9 high-speed QSPI NAND, an adjacency move to capture cost-sensitive infotainment sockets and widen its portfolio moat.

- April 2024: Kioxia completed its Kitakami Fab 2 construction to secure incremental flash capacity; although mainly directed at AI-datacenter demand, the geographic diversification underpins resilience for automotive customers.

Scope of Report on NOR Flash Memory Market for the Automotive Industry

The market is defined by the revenue accrued by products offered by the vendors. For the scope of the study, the report includes segmentation by density, application, and geography. The study also covers the activities of major players in the market along with their current strategies and recent developments.

The NOR flash memory market for the automotive industry is segmented by density (low (less than 32Mb), medium (32Mb to 128Mb), high (> 128Mb)), by application (ADAS, infotainment, instrument cluster, and other), and by geography (Americas, Europe, Japan, China, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Serial NOR Flash |

| Parallel NOR Flash |

| SPI Single / Dual |

| Quad SPI |

| Octal and xSPI |

| Less than or equal to 2 Mb |

| Greater than 2 Mb – 4 Mb |

| Greater than 4 Mb – 8 Mb |

| Greater than 8 Mb – 16 Mb |

| Greater than 16 Mb – 32 Mb |

| Greater than 32 Mb – 64 Mb |

| Greater than 64 Mb – 128 Mb |

| Greater than 128 Mb – 256 Mb |

| Greater than 256 Mb |

| 3 V Class |

| 1.8 V Class |

| Wide-Voltage (1.65-3.6 V) |

| Other Voltage |

| 90 nm and Older |

| 65 nm |

| 55 nm (incl. 58 nm) |

| 45 nm |

| 28 nm and Below |

| WLCSP / CSP |

| QFN / SOIC |

| BGA / FBGA |

| Other Packaging Type |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | Serial NOR Flash | ||

| Parallel NOR Flash | |||

| By Interface | SPI Single / Dual | ||

| Quad SPI | |||

| Octal and xSPI | |||

| By Density | Less than or equal to 2 Mb | ||

| Greater than 2 Mb – 4 Mb | |||

| Greater than 4 Mb – 8 Mb | |||

| Greater than 8 Mb – 16 Mb | |||

| Greater than 16 Mb – 32 Mb | |||

| Greater than 32 Mb – 64 Mb | |||

| Greater than 64 Mb – 128 Mb | |||

| Greater than 128 Mb – 256 Mb | |||

| Greater than 256 Mb | |||

| By Voltage | 3 V Class | ||

| 1.8 V Class | |||

| Wide-Voltage (1.65-3.6 V) | |||

| Other Voltage | |||

| By Process Technology Node | 90 nm and Older | ||

| 65 nm | |||

| 55 nm (incl. 58 nm) | |||

| 45 nm | |||

| 28 nm and Below | |||

| By Packaging Type | WLCSP / CSP | ||

| QFN / SOIC | |||

| BGA / FBGA | |||

| Other Packaging Type | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| Taiwan | |||

| India | |||

| South East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How big is the NOR Flash Memory For Automotive Market?

The NOR Flash Memory For Automotive Market size is expected to reach USD 615.66 million in 2026 and grow at a CAGR of 7.04% to reach USD 865.21 million by 2031.

What is driving the rapid growth of the NOR Flash For Automotive Market?

The surge stems from software-defined vehicles that need instant-boot code storage, the shift toward zonal and domain architectures, and the electrification of power-trains—all of which favor high-reliability Serial NOR.

Why are Octal and xSPI interfaces important?

They raise read bandwidth to 400 MB/s, enabling secure boot in under 20 ms and supporting fast over-the-air software updates in safety-critical ECUs.

What regions represent the greatest opportunity?

Asia-Pacific holds the major share, but North America and Europe are leading adoption of ASIL-certified, low-voltage NOR, offering premium-margin opportunities.

Will emerging memories replace NOR flash?

For densities above 1 Gb, MRAM and ReRAM are contenders as NOR scaling hits physical limits, yet Serial NOR is expected to remain dominant for instant-on code up to at least 512 Mb during this decade.

Page last updated on: