Concussion Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

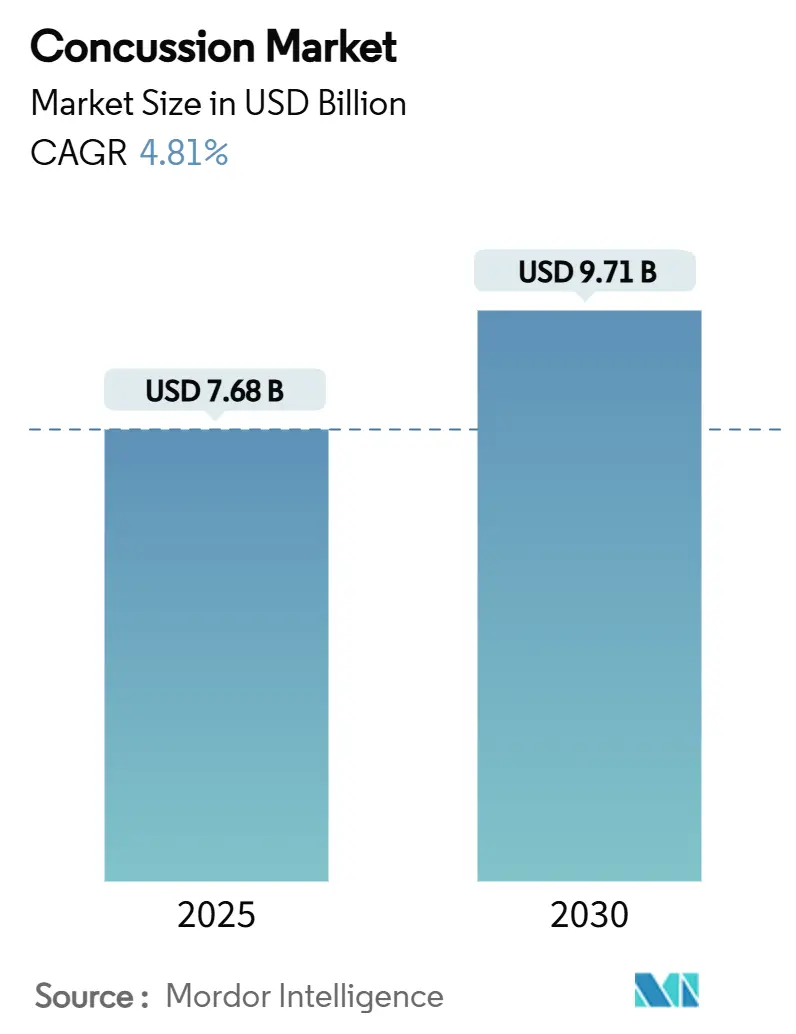

| Market Size (2025) | USD 7.68 Billion |

| Market Size (2030) | USD 9.71 Billion |

| Growth Rate (2025 - 2030) | 4.81% CAGR |

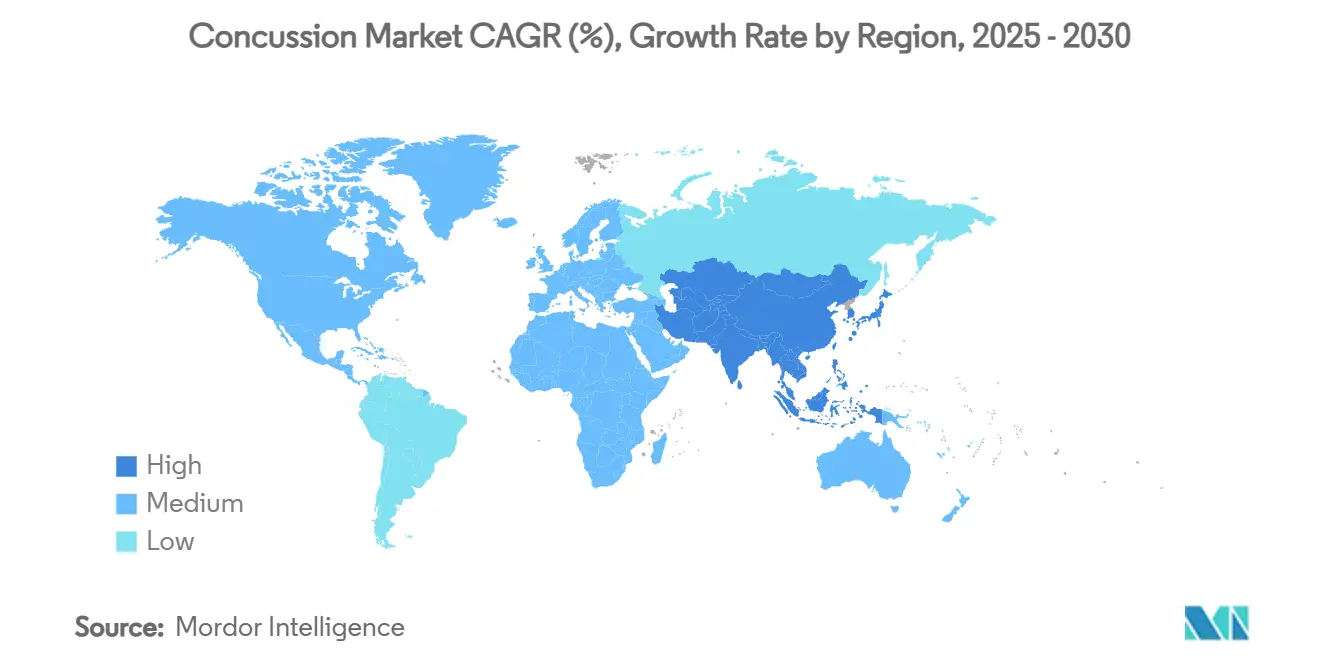

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concussion Market Analysis by Mordor Intelligence

The concussion market reached USD 7.68 billion in 2025 and is projected to rise to USD 9.71 billion by 2030, advancing at a 4.81% CAGR; market size expansion reflects growing clinical recognition of mild traumatic brain injuries and the shift toward biomarker-driven diagnostics. Hospitals, sports organizations, and military programs now prioritize rapid blood tests that measure GFAP and UCH-L1 proteins, replacing symptom-only assessments and reducing unnecessary imaging. North America preserves global leadership thanks to well-funded research, while Asia-Pacific records the fastest uptake as Japan and China update device approval rules. Consolidation among diagnostic firms continues because healthcare buyers increasingly prefer integrated assessment-to-treatment pathways instead of single-purpose tools. Overall growth momentum remains strongest where regulatory “return-to-play” mandates align with portable point-of-care technologies, widening access across schools, sports venues, and emergency settings.

Key Report Takeaways

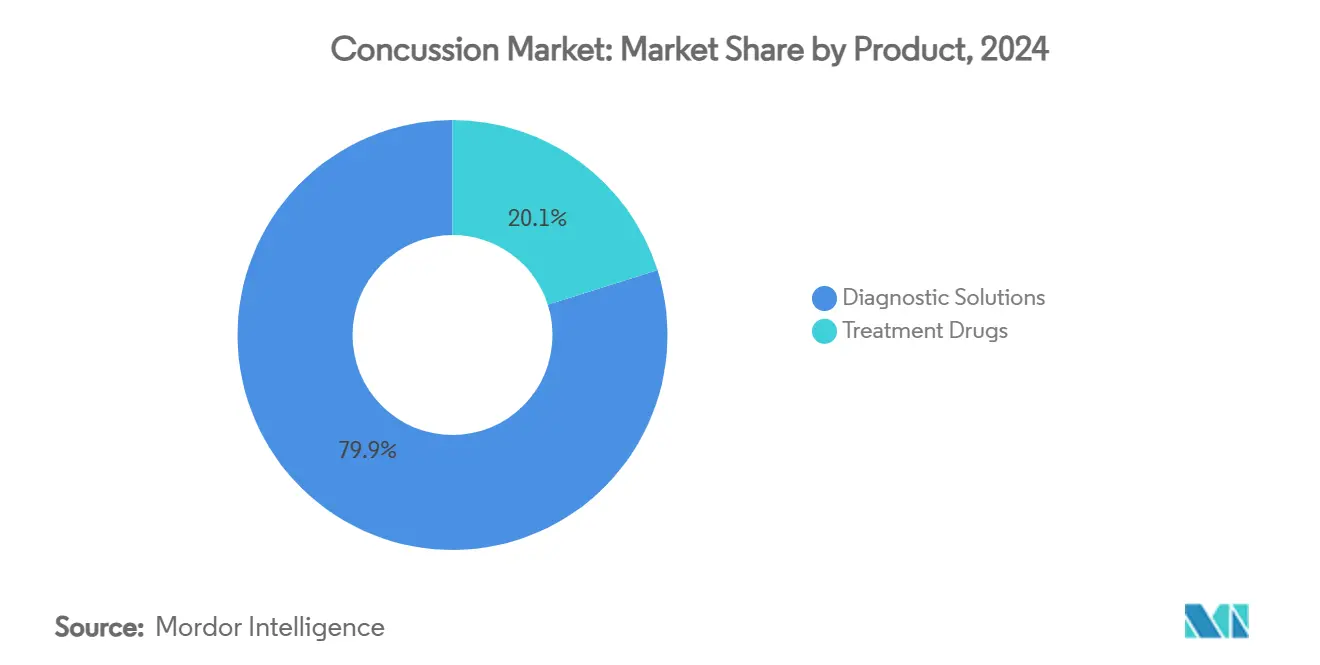

- By product, diagnostic solutions held 79.88% of the concussion market share in 2024 and are poised to expand at a 7.43% CAGR through 2030.

- By end user, hospitals and trauma centers led with 39.44% revenue share in 2024; sports organizations and academies are forecast to advance at an 8.53% CAGR to 2030.

- By severity grade, mild (Grade 1) concussions accounted for 63.24% of cases in 2024, whereas moderate (Grade 2) injuries are projected to grow at a 7.42% CAGR through 2030.

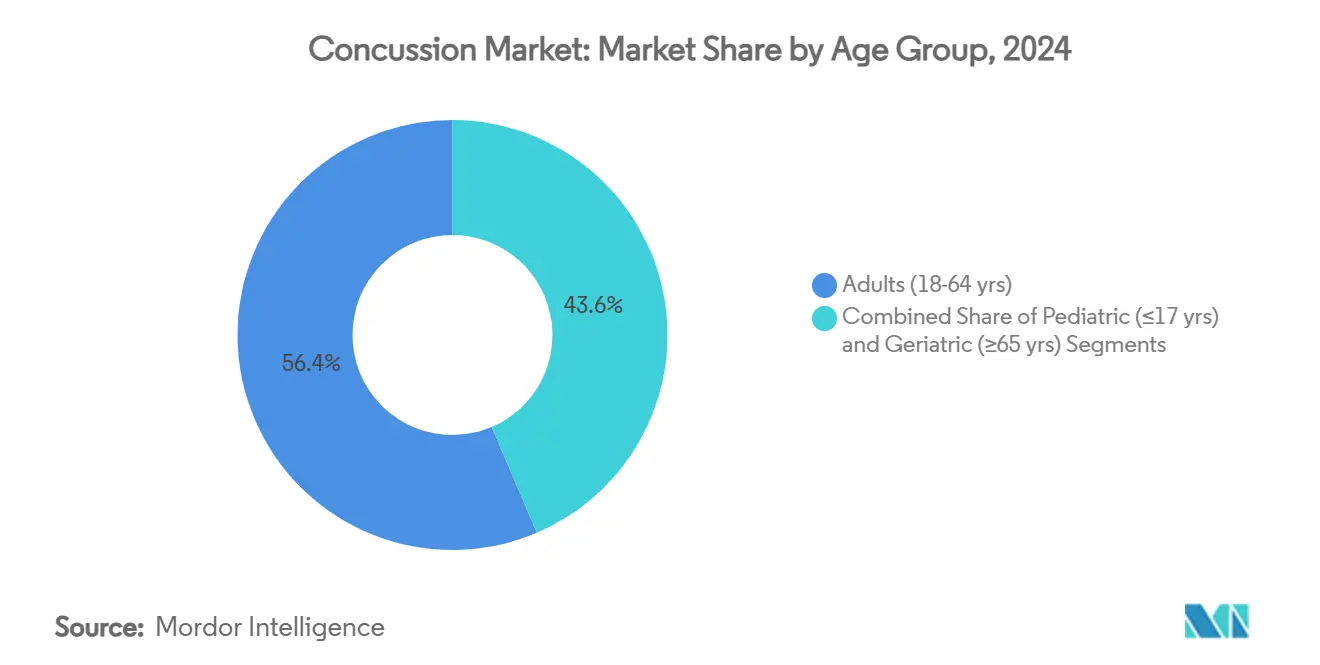

- By age group, adults (18–64 years) represented 56.43% of the concussion market share in 2024, while the pediatric segment is anticipated to rise at a 6.18% CAGR up to 2030.

- By injury mechanism, falls contributed 34.61% of the 2024 value; sports and recreation injuries are set to expand at a 6.71% CAGR to 2030.

- By geography, North America dominated with a 43.26% share in 2024, yet Asia-Pacific is projected to register the highest 6.33% CAGR through 2030.

Global Concussion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sports-Related Concussion Awareness Surge | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Regulatory "Return-To-Play" Mandates | +0.8% | North America, expanding to Europe & APAC | Short term (≤ 2 years) |

| Portable Neuro-Diagnostic Device Innovation | +1.0% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rising Traumatic Brain Injuries In Aging & Traffic Accidents | +0.9% | Global, with highest impact in APAC & Europe | Long term (≥ 4 years) |

| Blood-Based Biomarker Panels Enter Point-Of-Care Kits | +1.1% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| AI-Enabled Eye-Tracking Gains Sideline Adoption | +0.7% | North America & Europe, early APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sports-related concussion awareness surge

Professional leagues now demand objective testing, exemplified by MotoAmerica’s sideline deployment of Abbott’s 15-minute blood assay in 2025. The National Football League refined its protocol into six recovery phases that require clinician sign-off, driving downstream technology needs.[1]Centers for Disease Control and Prevention Editorial Staff, “Returning to Sports,” CDC, cdc.govYouth leagues replicate these standards, and the U.S. Army applies baseline testing to high-risk personnel. As awareness rises across school, collegiate, and recreational programs, demand for rapid, portable diagnostics elevates the concussion market.

Regulatory “return-to-play” mandates

CDC pediatric guidelines now emphasize clinical decision rules over routine CT scans, encouraging blood-based diagnostics in children.[2]Centers for Disease Control and Prevention Editorial Staff, “Safety Guidelines for Pediatric Mild TBI,” CDC, cdc.gov Health Canada cleared the i-STAT TBI test in mid-2025, expanding regulatory acceptance beyond the United States. The U.S. Defense Department mandates cognitive baseline testing every three years for new recruits, thereby institutionalizing periodic assessments. Collectively, these rules build recurring demand for compliant diagnostic platforms that streamline clearance decisions across sports and military environments.

Portable neuro-diagnostic device innovation

Miniaturization transforms concussion evaluation from hospital-centric workflows to field or bedside testing. Abbott’s i-STAT cartridge delivers whole-blood results in 15 minutes. Zeto’s FDA-cleared headset automates 21-lead EEG acquisition without trained technologists. BrainScope’s handheld scanner determines CT necessity within 15 minutes, helping emergency teams conserve imaging resources. These tools broaden access and accelerate triage, driving the concussion market forward.

Rising traumatic brain injuries in aging & traffic accidents

Falls account for 80% of mild TBIs in older adults, with hospital mortality as high as 16%. Traffic injuries further elevate incidence, especially in populous APAC nations where vehicle growth outpaces safety infrastructure. Japan’s authorities encourage imports of cost-effective devices to manage elderly TBI, and U.S. suppliers meet roughly 60% of demand. Growing senior populations worldwide ensure sustained diagnostic need.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Imaging & Monitoring | -0.6% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Shortage Of Neuro-Specialist Workforce | -0.4% | Global, acute in rural and developing regions | Long term (≥ 4 years) |

| Biomarker Specificity Skepticism Among Clinicians | -0.3% | North America & Europe, decreasing over time | Short term (≤ 2 years) |

| Data-Privacy Concerns With Head-Impact Wearables | -0.2% | Global, highest in Europe due to GDPR | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of advanced imaging & monitoring

Capital budgets for CT, MRI, and continuous EEG remain tight, particularly in low-resource hospitals. Reimbursement policies lag behind diagnostic innovation, discouraging procurement despite clinical value. Consumable costs for biomarker cartridges further strain finances, limiting reach in emerging economies.

Shortage of neuro-specialist workforce

Global neurologist deficits slow adoption of complex diagnostic protocols. Zeto’s auto-configured EEG responds to this gap by enabling non-specialists to capture diagnostic-grade signals. Until training supply improves, workforce scarcity constrains market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostic solutions consolidate leadership

Diagnostic solutions captured 79.88% of concussion market share in 2024 and are set to grow at 7.43% CAGR through 2030. Blood and salivary assays lead expansion because FDA-cleared GFAP and UCH-L1 panels provide quantitative confirmation within 15 minutes, positioning them as frontline triage tools. Portable EEG and eye-tracking systems complement biochemical approaches, while neuro-cognitive software remains a staple for baseline testing. Treatment drugs occupy a smaller share as no pharmacologic agent has secured specific approval for concussion; research continues around hypothermic therapy and neuro-stimulants.

The concussion market size for diagnostic imaging is stable, yet relative weighting declines because handheld devices reduce reliance on CT for mild cases. Eye-tracking accuracy improvements and head-impact sensors embedded in smart mouthguards bring preventive monitoring into routine practice. Collectively, these trends signal customer preference for integrated multi-modality platforms that bundle assays, imaging, and cognitive metrics.

By End User: Sports organizations accelerate adoption

Hospitals and trauma centers supplied 39.44% of spending in 2024, reflecting their role as first-line treatment hubs. However, sports organizations and academies are projected to outpace all others at an 8.53% CAGR, as sideline diagnostics become standard for athlete clearance. The concussion market size for ambulatory and urgent-care centers grows with the spread of point-of-care cartridges that eliminate the need for hospital referral.

Military and defense healthcare facilities deploy portable systems in remote locations, supported by Department of Defense research grants exceeding USD 1.5 billion in FY 2024. Occupational-health chains, highlighted by Concentra’s acquisition of Nova Medical Centers, integrate concussion management into workforce safety offerings, widening commercial exposure.

By Severity Grade: Moderate cases gain momentum

Mild injuries constituted 63.24% of total volume in 2024, yet moderate cases generate the highest 7.42% CAGR as objective biomarkers uncover damage invisible to symptom scales. The concussion market share for severe cases remains smallest but commands premium monitoring fees, encouraging suppliers of continuous EEG systems. NIH’s CBI-M framework, which merges clinical, imaging, and biomarker data, is prompting reassessment of legacy grading algorithms.

Clinical evidence indicates that 45% of athletes test at or above baseline on cognitive screens despite concussion, driving investment in protein panels that enhance diagnostic confidence.[3]Kimberly G. Harmon, “Diagnosis of Sports-Related Concussion Using Symptom Report or Standardized Assessment of Concussion,” JAMA Network Open, jamanetwork.com Vendors that can correlate biochemical, electrophysiological, and cognitive measures are set to outperform within the concussion market.

By Age Group: Pediatric demand rises fastest

Adults delivered 56.43% revenue in 2024, yet the pediatric segment is forecast to climb at 6.18% CAGR as schools adopt mandatory baseline and return-to-learn programs. Approximately 750,000 U.S. children suffer mild TBIs annually, and NFL biomarker levels remain elevated for months, underscoring the need for age-tailored assessment. The concussion market size for geriatric care expands steadily due to the high fall incidence in seniors.

Guidelines discourage routine imaging in children, favoring blood assays and symptom monitoring. Product developers therefore prioritize low-volume sample requirements and child-specific reference ranges to penetrate pediatric clinics.

By Injury Mechanism: Sports and recreation accelerate

Falls produced 34.61% of injuries in 2024. Yet sports and recreation cases will grow at 6.71% CAGR through 2030, propelled by expanding athletic participation and better detection. The concussion market size tied to motor-vehicle collisions rises in emerging economies where traffic injury rates remain high. Assault and combat mechanisms drive military procurement of ruggedized devices that withstand field conditions.

Impact-sensor mouthguards and helmet chips deliver real-time telemetry, helping coaches intervene before symptomatic collapse. This preventative orientation broadens market potential beyond post-injury assessment toward continuous monitoring.

Geography Analysis

North America generated 43.26% of 2024 revenue, underpinned by professional sports mandates, robust insurance coverage, and Department of Defense funding. The concussion market size growth in the region remains healthy as Canada authorizes rapid blood assays and U.S. payers move toward bundled reimbursement models. Major hospital systems now integrate point-of-care biomarker kits into emergency triage, shrinking CT utilization rates and accelerating discharge workflows.

Europe follows with steady uptake as the European Union harmonizes device regulations and elite football organizations standardize sideline screening. Scandinavian healthcare systems adopt blood-based biomarker panels widely, citing cost savings from reduced imaging. The United Kingdom’s National Institute for Health and Care Excellence is assessing real-world outcomes data that may trigger broader National Health Service coverage decisions.

Asia-Pacific records the strongest 6.33% CAGR. Japan’s rapidly aging population, combined with a USD 40 billion domestic device market, encourages import of U.S. diagnostic technologies that enhance geriatric fall management. China’s NMPA streamlines Class II and III device approvals, shortening commercialization timelines for blood assays. India aligns its medical-device rules with EU standards, and with 70% of devices currently imported, suppliers see substantial headroom for concussion market penetration.

Middle East and Africa expand gradually as new trauma centers open and governments invest in emergency medicine. South America adopts concussion protocols at a slower pace due to economic headwinds, yet multinational sports federations drive incremental demand in Brazil and Argentina. Across all regions, the presence of clear regulatory guidance and reimbursement pathways remains the chief determinant of uptake.

Competitive Landscape

The concussion market is moderately fragmented but trending toward consolidation as large diagnostics firms acquire niche neurotechnology innovators. Nihon Kohden’s September 2024 purchase of NeuroAdvanced Corp strengthens its EEG and intracranial electrode offering, targeting 5 million drug-resistant epilepsy patients whose pathways overlap with concussion monitoring needs. Abbott maintains front-runner status via its FDA-cleared i-STAT TBI cartridge, which delivers 15-minute objective results at the point of care and has now secured Health Canada approval.

Strategic alliances accelerate product pipelines. bioMérieux invested USD 7 million in Banyan Biomarkers to co-develop blood-based TBI assays for an estimated 10 million annual global cases. Smaller players such as BrainScope focus on AI-driven electrophysiology, while Quanterix pioneers ultra-sensitive Simoa technology for protein detection. Wearable sensor start-ups pursue partnerships with helmet manufacturers and sports leagues, aiming to embed impact telemetry into everyday equipment.

Competitive advantage increasingly hinges on offering an end-to-end pathway that covers baseline screening, acute diagnosis, and rehabilitation monitoring. Vendors capable of integrating biochemical panels, EEG data, and cognitive metrics within a unified dashboard are best placed to capture hospital and sports-league contracts. Pricing pressure remains, but customers show willingness to invest in platforms that demonstrably reduce unnecessary imaging and shorten return-to-play cycles.

Concussion Industry Leaders

Abbott

BrainScope

Koninklijke Philips N.V.

GE Healthcare

Natus Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Health Canada granted approval for Abbott’s i-STAT TBI test, enabling nationwide use in emergency departments and sports clinics.

- May 2025: MotoAmerica implemented Abbott’s rapid blood test track-side, marking the first professional sports adoption of an objective biomarker assay.

- August 2024: Orlando Health became the first hospital worldwide to deploy Abbott’s new blood test for traumatic brain injury triage.

Global Concussion Market Report Scope

| Diagnostic Solutions | Diagnostic Imaging | Neuro-cognitive Assessment Software |

| Blood & Salivary Biomarker Assays | ||

| Portable EEG & Brain Monitoring Devices | ||

| Eye-Tracking & Oculomotor Systems | ||

| Head-Impact Wearable Sensors | ||

| Therapeutics & Neuro-protective Drugs | ||

| Treatment Drugs | Neuro-stimulants | Anti-inflammatory agents |

| Others | ||

| Hospitals & Trauma Centers |

| Specialty Neurology & Rehabilitation Clinics |

| Sports Organizations & Academies |

| Military & Defense Healthcare Facilities |

| Ambulatory Surgical & Urgent-Care Centers |

| Mild (Grade 1) |

| Moderate (Grade 2) |

| Severe (Grade 3) |

| Pediatric (≤17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (≥65 yrs) |

| Sports & Recreation |

| Falls |

| Motor-Vehicle Accidents |

| Assault & Combat |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostic Solutions | Diagnostic Imaging | Neuro-cognitive Assessment Software |

| Blood & Salivary Biomarker Assays | |||

| Portable EEG & Brain Monitoring Devices | |||

| Eye-Tracking & Oculomotor Systems | |||

| Head-Impact Wearable Sensors | |||

| Therapeutics & Neuro-protective Drugs | |||

| Treatment Drugs | Neuro-stimulants | Anti-inflammatory agents | |

| Others | |||

| By End User | Hospitals & Trauma Centers | ||

| Specialty Neurology & Rehabilitation Clinics | |||

| Sports Organizations & Academies | |||

| Military & Defense Healthcare Facilities | |||

| Ambulatory Surgical & Urgent-Care Centers | |||

| By Severity Grade | Mild (Grade 1) | ||

| Moderate (Grade 2) | |||

| Severe (Grade 3) | |||

| By Age Group | Pediatric (≤17 yrs) | ||

| Adults (18-64 yrs) | |||

| Geriatric (≥65 yrs) | |||

| By Injury Mechanism | Sports & Recreation | ||

| Falls | |||

| Motor-Vehicle Accidents | |||

| Assault & Combat | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the concussion market?

The concussion market reached USD 7.68 billion in 2025 and is forecast to grow to USD 9.71 billion by 2030.

Which segment holds the largest concussion market share?

Diagnostic solutions accounted for 79.88% of global revenue in 2024 due to rapid adoption of blood-based biomarker panels.

Why are sports organizations driving concussion market growth?

Mandatory sideline testing and structured return-to-play rules push sports bodies to install point-of-care diagnostics, producing an 8.53% CAGR in the segment.

Which region is expanding fastest in the concussion market?

Asia-Pacific is projected to rise at a 6.33% CAGR through 2030, supported by favorable regulatory changes in Japan, China, and India.

How do blood-based tests reduce CT scans?

GFAP and UCH-L1 assays deliver objective results in 15 minutes, allowing clinicians to rule out intracranial bleeding and reserve CT for high-risk patients.

What limits broader concussion market adoption today?

High equipment costs, a shortage of neuro-specialists, and data-privacy concerns with wearable sensors remain key restraints despite strong growth drivers.

Page last updated on: