Neurophotonics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.42 Billion |

| Growth Rate (2026 - 2031) | 10.24% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

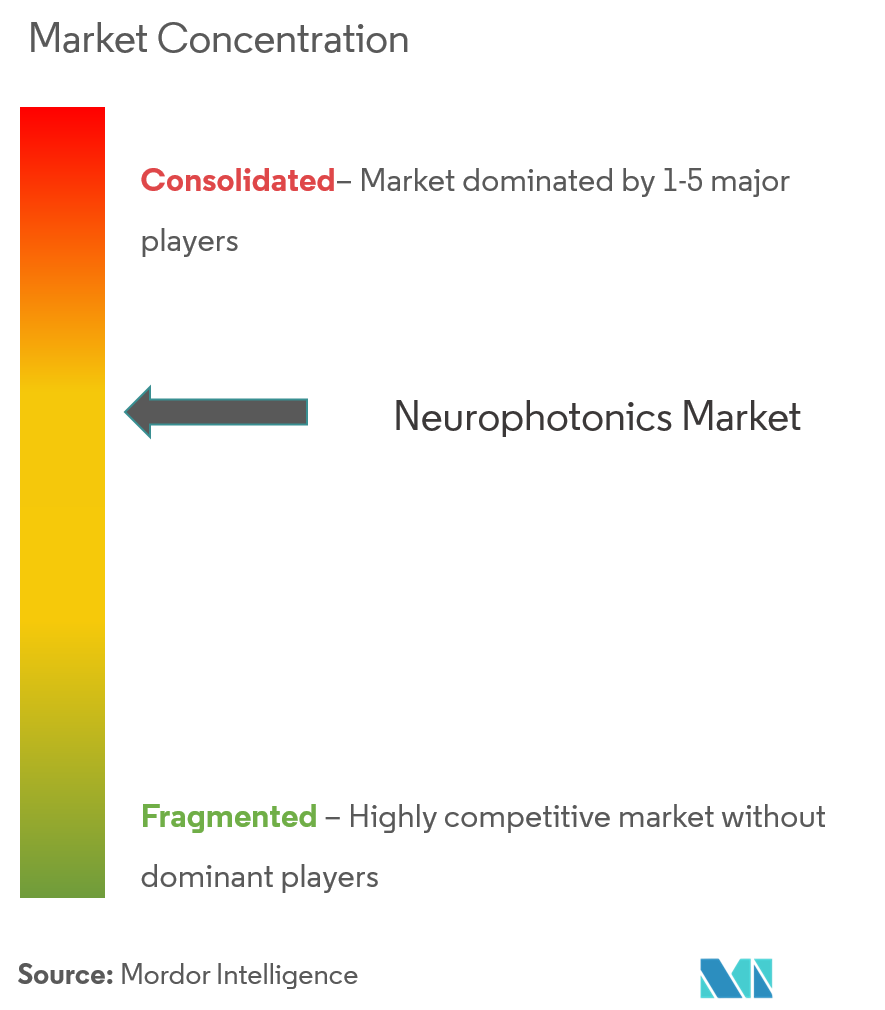

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurophotonics Market Analysis by Mordor Intelligence

The Neurophotonics market size is expected to grow from USD 1.9 billion in 2025 to USD 2.09 billion in 2026 and is forecast to reach USD 3.42 billion by 2031 at 10.24% CAGR over 2026-2031.

Rapid progress in deep-tissue optical imaging, artificial-intelligence-enabled data analytics, and minimally invasive brain interfaces is widening the technology’s clinical relevance. Government funding through programs such as the United States BRAIN Initiative and Japan’s Moonshot Goal 1 fuels a steady flow of laboratory discoveries that migrate into commercial platforms. Capital inflows from venture investors and strategic acquisitions by large optical equipment makers strengthen the innovation pipeline and shorten product‐development cycles. North America keeps its leadership position through an integrated ecosystem of academic centers, medical-device regulators, and reimbursement stakeholders, while Asia-Pacific accelerates on the back of Japan’s global photonics manufacturing footprint and rising R&D outlays in China and India.

Key Report Takeaways

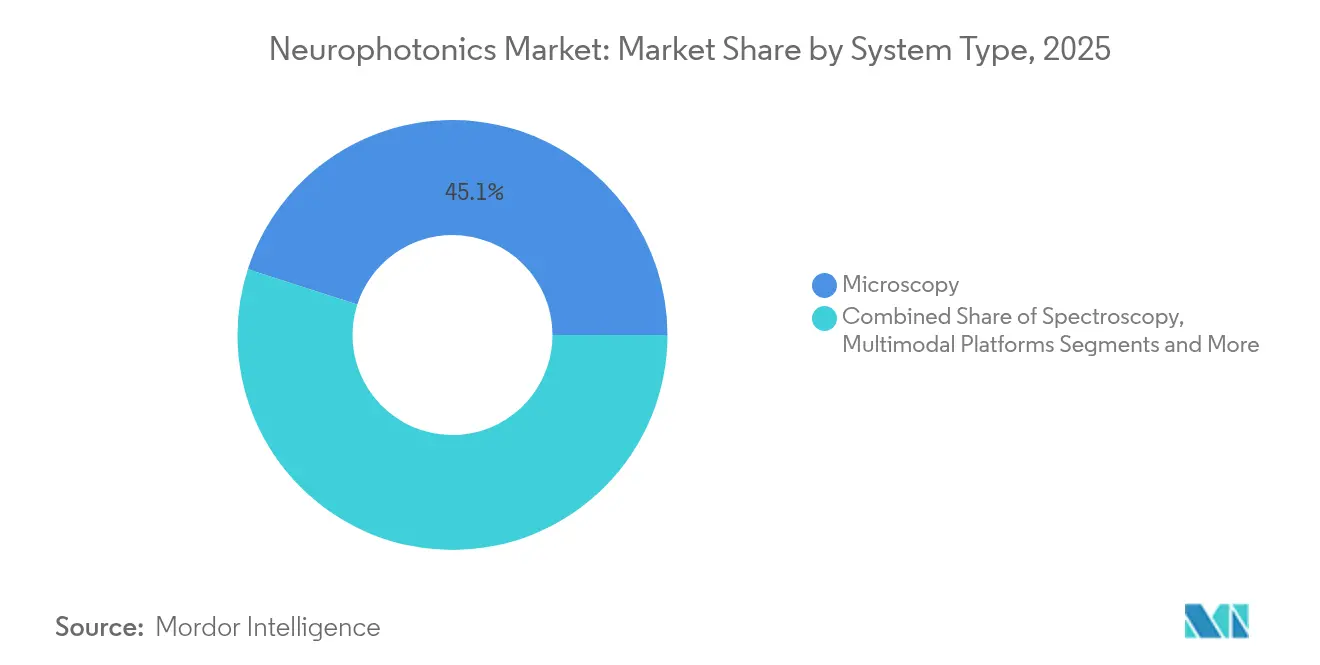

- By system type, microscopy systems led with 45.05% of neurophotonics market share in 2025; spectroscopy platforms are projected to register an 11.03% CAGR to 2031.

- By application, research held 63.10% of the neurophotonics market size in 2025, while therapeutic use cases are set to expand at a 11.82% CAGR through 2031.

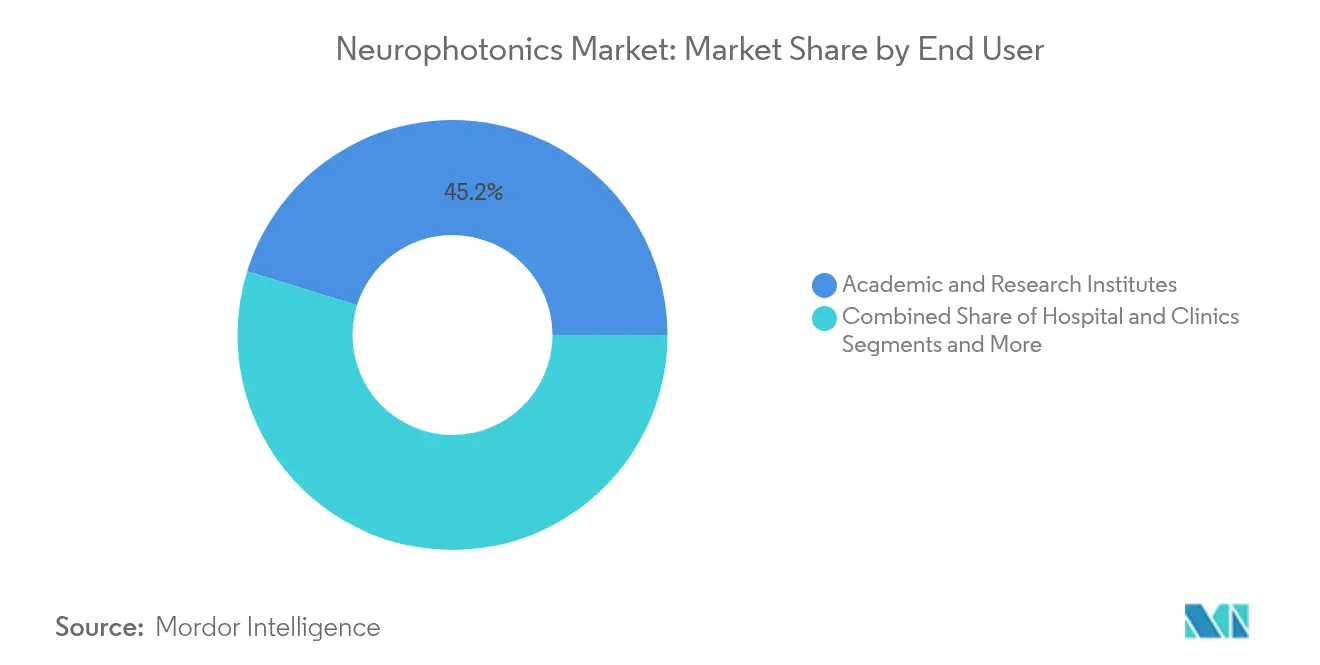

- By end-user, academic and research institutes commanded 45.20% revenue share in 2025; hospitals and clinics record the fastest growth at 12.18% CAGR to 2031.

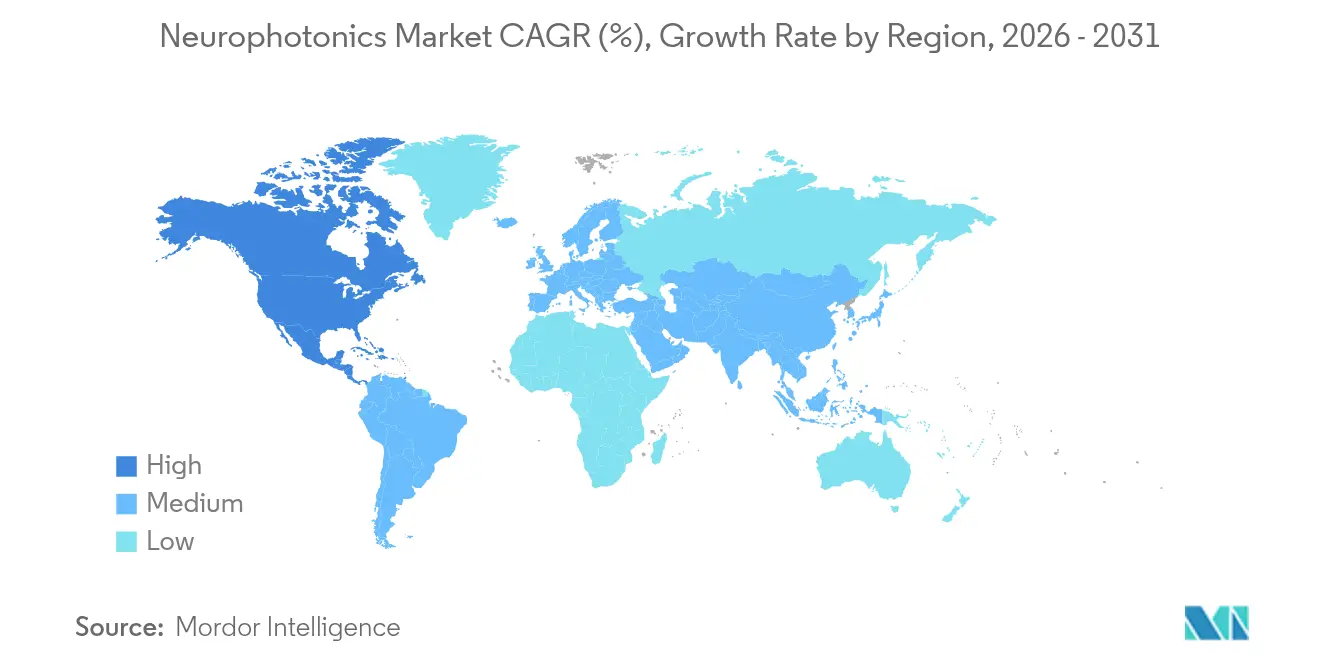

- By geography, North America captured 42.10% revenue share in 2025; Asia-Pacific is anticipated to post a 12.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurophotonics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Neurological Disorders | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expanding Government Funding For Brain-Mapping R&D | +2.1% | North America, Europe, APAC core markets | Long term (≥ 4 years) |

| Miniaturization & Portability Of Optical Neuro-Imaging Devices | +1.9% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Rapid Adoption Of Optogenetics & fNIRS In Academic Labs | +1.6% | North America, Europe, expanding to APAC | Medium term (2-4 years) |

| Integration With Immersive XR & BCI Platforms | +1.4% | North America, Europe, selective APAC markets | Long term (≥ 4 years) |

| Growth Of Neonatal/Peri-Operative Monitoring Use-Cases | +1.2% | Global, with early gains in developed healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neurological Disorders

Neurodegenerative and psychiatric conditions impose growing social and economic burdens as global life expectancy rises. More than 55 million individuals live with Alzheimer’s disease, and incidence continues to rise in aging populations. Functional near-infrared spectroscopy (fNIRS) and photobiomodulation techniques provide real-time cerebral oxygenation data that conventional magnetic resonance imaging cannot deliver cost-effectively [1]University of California San Francisco, “Near-Infrared Photobiomodulation Improves Cognitive Function in Dementia,” ucsf.edu. Clinical studies at the University of California San Francisco reported notable gains in Mini Mental State Exam scores following near-infrared light therapy, strengthening the clinical case for optical interventions. Hospitals adopt the technology to monitor cognitive rehabilitation progress, while device makers focus on user-friendly systems suited for outpatient environments. As prevalence expands, the neurophotonics market draws sustained demand from both diagnostic and therapeutic workflows.

Expanding Government Funding for Brain-Mapping R&D

The United States BRAIN Initiative earmarks multiyear grants specifically targeting optical neural-interface innovations such as non-degenerate two-photon microscopy. Similar funding frameworks in Europe and Asia-Pacific bring research labs, device makers, and clinical centers into shared consortia, accelerating technology maturation. Japan’s Moonshot Goal 1 forecasts a domestic neurotechnology sector worth USD 520 million in 2025, signaling long-term policy commitment. These programs underwrite high-risk projects, subsidize pilot manufacturing lines, and create open-access data repositories that speed reproducibility. Public-sector support draws matching private investment, allowing startups to scale prototypes into regulatory grade systems without prohibitive dilution. As grants transition from basic science to translational milestones, industry players capture earlier commercial payoffs, reinforcing the upward trajectory of the neurophotonics market.

Miniaturization and Portability of Optical Neuro-Imaging Devices

The shift from benchtop rigs to handheld or wearable formats unlocks new settings ranging from athletic performance labs to home-based cognitive therapy. Advances in light-emitting diodes, micro-optics, and battery efficiency enable helmet-style fNIRS caps that record cortical activity while subjects walk or play a sport [2]SPIE, “Miniaturized Miniscopes Capture Bioluminescent Signals in Freely Moving Mice,” spie.org . Researchers using modified miniscopes have achieved chronic bioluminescent recording in freely moving rodents, underscoring translational potential for human ambulatory monitoring. The portability argument resonates with pediatric neurologists who avoid sedation protocols required for conventional imaging. Consumer health companies prototype neurofeedback headsets for stress management, broadening addressable demand beyond hospitals. Initial price premiums taper as component volumes rise, supporting faster adoption in cost-sensitive markets.

Rapid Adoption of Optogenetics and fNIRS in Academic Labs

Academic centers deploy optogenetics to control neural circuits with cell-type specificity, creating fresh demand for ultrafast lasers, optical fibers, and genetically encoded indicators. Standardized data schemas such as NIRS-BIDS and SNIRF enhance interoperability, letting multi-lab collaborations pool datasets and validate findings more quickly. Wide use in animal models generates highly trained cohorts of graduate researchers who transition into clinical fellowships and industry R&D labs, propagating expertise. Publications citing optogenetic readouts have grown steadily since 2023, reflecting toolchain maturity and cost reductions. Equipment vendors bundle turnkey software that automates artifact removal and hemodynamic correction, lowering the skill barrier and widening the user base.

Integration with Immersive XR and BCI Platforms

Mixed-reality headsets equipped with embedded optical sensors visualize neural activation in real time, aiding neurorehabilitation and immersive therapy. Brain-computer-interface (BCI) developers integrate fiber-optic probes for bidirectional neural data flow, enhancing command resolution and reducing latency. Prototype systems achieve millisecond-level temporal precision during hand-tracking tasks, hinting at future neuro-adaptive gaming and prosthetics control. Regulatory bodies extend breakthrough-device designations to such hybrid platforms, shaving approval cycles. The convergence of neurophotonics with XR and BCI ecosystems positions optical techniques at the core of next-generation neuro-digital interfaces.

Growth of Neonatal and Peri-Operative Monitoring Use Cases

Neonatal intensive care units require continuous cerebral oxygenation assessment in preterm infants, a niche where fNIRS outperforms pulse oximetry. Surgeons employ intraoperative optical fluorescence to delineate tumor margins, reducing repeat procedures. Cardiac anesthesiologists use spectroscopy probes to monitor brain perfusion during bypass, preventing postoperative cognitive decline. Evidence from multicenter trials drives guideline updates that incorporate optical monitoring as standard of care. Device makers respond with sterile disposable sensors and touchscreen interfaces tailored for operating room workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Penetration Depth In Adult Cortical Imaging | -1.8% | Global, particularly affecting deep brain applications | Long term (≥ 4 years) |

| High CAPEX & OPEX Of Multiphoton Platforms | -1.5% | Global, more pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Lack Of Data-Format Interoperability Across Vendors | -1.2% | Global, with higher impact in multi-vendor environments | Short term (≤ 2 years) |

| Phototoxicity & Tissue-Heating Risks In Long-Duration Studies | -0.9% | Global, particularly affecting research applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Penetration Depth in Adult Cortical Imaging

Light scatters in adult brain tissue, restricting two-photon and three-photon modalities to superficial layers roughly 2–3 mm deep. Subcortical targets involved in Parkinson’s disease or refractory epilepsy remain out of reach, compelling clinicians to adopt alternative modalities such as deep-brain electrodes or high-field MRI. Extended illumination elevates tissue temperature; PhotoniX reports that cumulative light exposure above 400 mW causes thermal damage, capping imaging duration. To mitigate the issue, researchers explore wavefront-shaping optics and terahertz-photon stimulation, yet commercial readiness sits several years away. Meanwhile, the depth limitation curtails immediate revenue potential for high-end imaging vendors.

High CAPEX and OPEX of Multiphoton Platforms

State-of-the-art multiphoton microscopes cost several hundred thousand USD, and service contracts can add 10% of purchase price annually [3]PubMed Central, “Operational Costs of Advanced Multiphoton Platforms,” ncbi.nlm.nih.gov . Smaller institutions hesitate to dedicate scarce capital budgets when reimbursement pathways remain nascent. Skilled technicians require months of training, and staff turnover inflates operational expenditures. Publicly funded core facilities offset costs through shared-use models, though access queues slow project timelines. Vendors develop leasing and pay-per-scan schemes, yet uptake remains uneven outside well-funded centers. Cost hurdles therefore suppress diffusion in emerging economies, tempering global revenue growth for the neurophotonics market.

Lack of Data-Format Interoperability Across Vendors

Electrophysiology, imaging, and stimulation modules often use proprietary file standards, complicating integration with electronic medical records and analytics software. Hospitals operating multi-vendor fleets face redundant data-conversion workflows that erode productivity. The neuroimaging community responds with open schemas such as SNIRF, but broad vendor adoption lags. Absence of plug-and-play interoperability slows health system procurement decisions, delaying capital allocation. Market participants that champion open standards stand to gain competitive advantage once interoperability guidance becomes a purchasing criterion.

Phototoxicity and Tissue-Heating Risks in Long-Duration Studies

Ultrafast lasers deliver high photon flux that can generate reactive oxygen species and local heat, damaging delicate neural tissue during prolonged studies. Phototoxic artifacts confound data interpretation, obliging researchers to shorten imaging sessions or add cooling hardware that increases instrument complexity. Corporate R&D teams accelerate development of red-shifted fluorophores and lower-power excitation schemes, but widespread commercial deployment remains in progress. Safety concerns therefore restrict certain longitudinal applications and prompt conservative institutional review board policies, imposing soft limits on installed-base utilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Microscopy Dominance Drives Innovation

Microscopy platforms accounted for 45.05% of neurophotonics market share in 2025, consolidating their role as the workhorse modality for circuit-level visualization. The ZEISS FLUOVIEW FV4000MPE and Bruker OptoVolt modules exemplify how fast resonant scanners and adaptive optics yield sub-micron resolution over millimeter-scale fields. Demand for ever finer structural insight sustains a healthy upgrade cycle, especially within core imaging facilities at top neuroscience institutes. Spectroscopy systems record the fastest 11.03% CAGR to 2031 by tackling functional hemodynamic mapping with portable hardware. Multimodal configurations that fuse fluorescence lifetime imaging with Raman spectroscopy attract pharmaceutical customers seeking comprehensive compound-brain interaction profiles. Vendors integrate GPU-accelerated algorithms to deliver near-instantaneous volumetric reconstructions, saving researchers hours of post-acquisition processing. Sustained innovation coupled with rising translational projects keeps the microscopy sub-category at the spine of the broader neurophotonics market.

The neurophotonics market size for spectroscopy solutions is set to rise sharply as hospitals deploy bedside fNIRS for stroke triage. Artificial-intelligence classifiers embedded in acquisition software flag ischemic trends in under three seconds, guiding immediate intervention. Corporate activity intensifies; Hamamatsu’s acquisition of NKT Photonics secures an ultrafast-laser supply chain, while Leica Microsystems formalizes a distribution pact with Inscopix to co-market cellular-resolution miniscope kits. Consortia such as the Microscopy Metadata Working Group finalize 3D-imaging metadata standards, promoting data pooling across global cohort studies. Collectively, these moves lower barriers to entry for new research groups, reinforcing microscopy’s pre-eminent place in the neurophotonics market.

By Application: Research Foundation Enables Therapeutic Expansion

Research activities represented 63.10% of the neurophotonics market size in 2025 as grant-funded laboratories continued to dominate purchase orders. Optogenetics remains central to dissecting depressive and anxiety circuits, while light-sheet microscopy resolves neuronal ensembles during behavioral assays. Translational milestones accelerate; photobiomodulation improved Autism Treatment Evaluation Checklist scores by up to 40% in recent pediatric trials, boosting clinical interest. The therapeutic segment therefore leads future growth with a 11.82% CAGR, promising fresh revenue streams in dementia, traumatic brain injury, and chronic pain management. Diagnostic utilities also gain traction as hyperspectral fluorescence imagery assists neurosurgeons in real-time tumor delineation, preventing residual malignancy.

Neurophotonics market share figures underline how therapeutic players capture risk-capital attention. Start-ups developing helmet-style transcranial photobiomodulation devices secure multi-million seed rounds, citing Alzheimer’s and post-stroke rehabilitation as immediate addressable indications. Regulatory bodies expedite clearances after Precision Neuroscience’s implant passed FDA review in 2024, setting precedent for subsequent optical-interface submissions. Industry alliances with hospital networks test payer acceptance, and early reimbursement codes emerge under elective neuro-rehabilitation categories. Together, these advances carve a credible pathway from bench to bedside, enlarging the total addressable neurophotonics market.

By End-User: Academic Leadership Shifts Toward Clinical Adoption

Academic and research institutes commanded 45.20% revenue share in 2025, serving as crucibles for tool development and validation. Core facilities centralize high-value instruments, extending access to multi-disciplinary teams studying cognition, psychiatric disorders, and neuro-immune cross-talk. Hospitals and clinics, however, post a 12.18% CAGR, reflecting growing clinician confidence in optical neuromonitoring for peri-operative and intensive care scenarios. FDA clearance for QuantalX Neuroscience’s Delphi stimulator, which detects Parkinson’s disease progression with 85% accuracy, underscores therapeutic viability and encourages hospital procurement boards.

Pharmaceutical and biotechnology companies increasingly incorporate optical endpoints into early-phase trials to parse mechanism-of-action nuances. Automated read-outs from voltage-sensitive dye imaging slash analysis times, enabling adaptive trial designs. Vendor service models bundle instrument rentals with data-science consulting, supporting drug sponsors that lack in-house neuroimaging expertise. Collectively, the shift toward clinical and commercial settings diversifies revenue exposure and reduces reliance on cyclical grant funding, lifting near-term visibility for suppliers across the neurophotonics market.

Geography Analysis

North America generated 42.10% of global revenue in 2025 thanks to deep federal funding pools and a transparent regulatory pathway that accelerates first-in-human studies. The FDA’s breakthrough-device designation awarded to Precision Neuroscience and ClearPoint Neuro in 2024 exemplifies swift review for transformative platforms. Favorable reimbursement policies for intraoperative fluorescence guidance further solidify regional demand. Rich venture-capital ecosystems surrounding Boston, San Francisco, and Toronto attract entrepreneurial talent and de-risk early commercial launches. However, high equipment prices and value-based-care mandates compel suppliers to develop robust health-economic dossiers to defend capital budgets.

Asia-Pacific posted the fastest 12.95% CAGR and is poised to erode North American share as local supply chains mature. Japan maintains roughly 30% of global photonics output through more than 180 manufacturers, creating economies of scale that cut bill-of-materials cost for domestic device assemblers. Chinese provincial governments fund neurotechnology parks and offer expedited registrations for Class II medical devices, shortening go-to-market timelines. India’s Production-Linked Incentive scheme for medical electronics lures component fabricators, shaping a nascent export hub. Cross-border academic partnerships with Australian neuroscience centers generate translational prototypes, broadening regional expertise.

Europe holds a balanced landscape where established research universities and cohesive data-privacy laws foster collaborative multi-site trials. Germany champions optogenetics standardization through joint industry-academia working groups, while the United Kingdom pilots reimbursement pathways for fNIRS cognitive assessments in stroke follow-up care. Local manufacturers, facing Asian cost competition, pivot to premium service models that emphasize workflow integration and lifecycle support. Regulatory alignment under the EU Medical Device Regulation introduces additional documentation overhead, but also harmonizes product quality expectations, smoothing intra-European distribution for neurophotonics suppliers.

Competitive Landscape

The neurophotonics market features moderate fragmentation that allows specialized innovators to coexist with diversified optical conglomerates. Carl Zeiss Meditec AG and Leica Microsystems leverage decades of optics know-how and extensive sales networks to bundle laser sources, objectives, and image-analysis suites. Hamamatsu Photonics secured ultrafast laser capacity by completing its acquisition of NKT Photonics in 2024, bolstering component security amid global supply uncertainties. Inscopix continues to focus on miniature fluorescence microscopes tailored to freely moving animal studies, extending into translational partnership programs with pharmaceutical companies.

White-space opportunities concentrate on cost-optimized spectroscopy devices for outpatient neurology clinics and plug-and-play data platforms that bridge equipment from multiple vendors. Spryte Medical revealed an AI-enhanced optical coherence tomography system capable of extracting microvascular biomarkers relevant to concussion management, illustrating the slope at which newcomers can carve niche beachheads. Patent filings spike in areas combining optical stimulation with closed-loop electrophysiology, hinting at an arms race for multifunctional brain–computer interfaces. Market participants recognizing the value of open APIs and cloud-based analytics create stickier ecosystems that lock in recurring revenue, while laggards risk relegation to component-supplier status.

The competitive field also witnesses joint ventures where medical imaging software specialists align with optics manufacturers to deliver integrated solutions. JuneBrain partners with hospital networks to deploy portable retinal imaging systems that infer neuro-degenerative progression, generating subscription income from data-interpretation software. Strategic collaborations such as Charles River Laboratories and Insightec’s five-year focused-ultrasound alliance in September 2024 illustrate horizontal expansion into adjacent neuromodulation modalities, reinforcing ecosystem breadth around shared neurological end markets.

Neurophotonics Industry Leaders

Cairn Research

Artinis Medical Systems

Hitachi, Ltd.

Femtonics Ltd

Carl Zeiss AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Charles River Laboratories International Inc. and Insightec launched a five-year strategic collaboration to offer a global platform for focused-ultrasound drug-discovery services in neuroscience.

- November 2022: Bruker expanded its neuro-imaging portfolio through the acquisition of Neurescence and Inscopix, integrating miniature imaging expertise into its broader optical instrumentation line.

Global Neurophotonics Market Report Scope

Neurophotonics is a field that spans the intersection of light and neurons for fundamental discovery and clinical translation. The field employs a range of optical methodologies, from microscopies to spectroscopies, to achieve a multiscale understanding of the structure and function of healthy and diseased brain as well as the nervous system. The scope of this report is limited to North America, Europe, Asia-Pacific, and Rest of World.

| Microscopy |

| Spectroscopy |

| Multimodal Platforms |

| Other System Types |

| Research |

| Diagnostics |

| Therapeutics |

| Academic & Research Institutes |

| Hospitals & Clinics |

| Pharma & Biotech Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By System Type | Microscopy | |

| Spectroscopy | ||

| Multimodal Platforms | ||

| Other System Types | ||

| By Application | Research | |

| Diagnostics | ||

| Therapeutics | ||

| By End-user | Academic & Research Institutes | |

| Hospitals & Clinics | ||

| Pharma & Biotech Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Neurophotonics Market size?

The neurophotonics market is valued at USD 2.09 billion in 2026 and is forecast to reach USD 3.42 billion by 2031.

Who are the key players in Neurophotonics Market?

Cairn Research, Artinis Medical Systems, Hitachi, Ltd., Femtonics Ltd and Carl Zeiss AG are the major companies operating in the Neurophotonics Market.

Which system type generates the most revenue?

Microscopy systems lead with 45.05% of neurophotonics market share in 2025, driven by continual resolution improvements and widespread research adoption.

Why is Asia-Pacific considered the fastest-growing region?

Asia-Pacific posts a 12.95% CAGR due to Japan’s strong photonics manufacturing base and rising neurotechnology investments in China and India.

Page last updated on: