Neurotoxin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

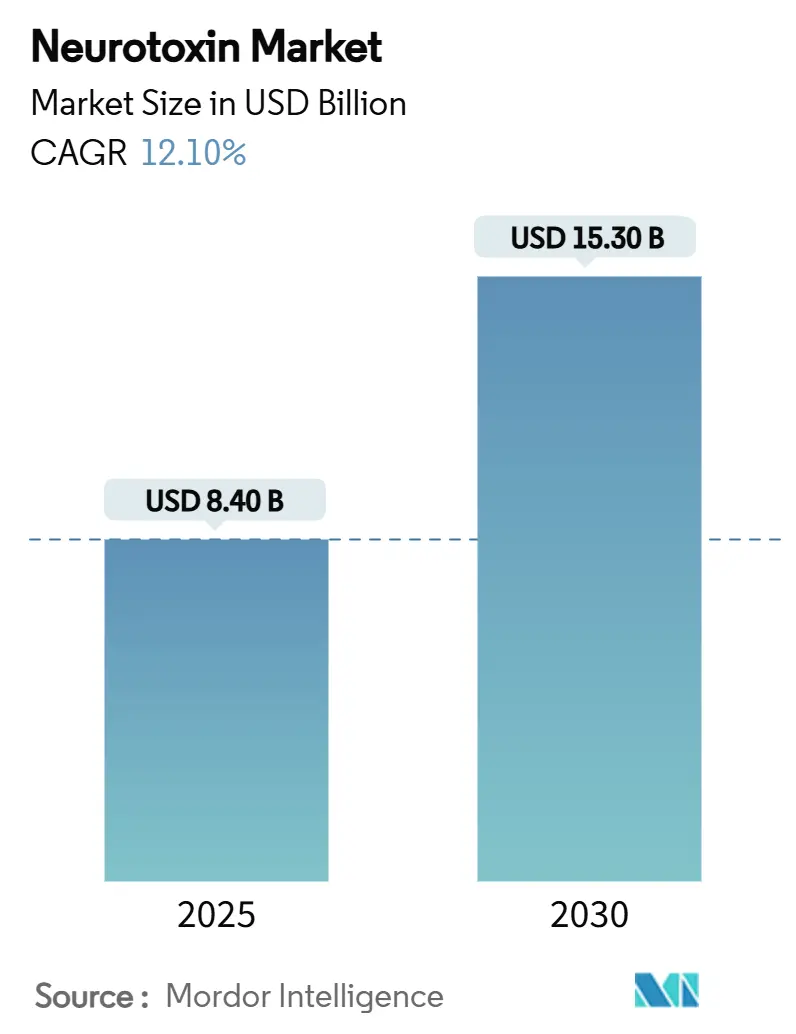

| Market Size (2025) | USD 8.40 Billion |

| Market Size (2030) | USD 15.30 Billion |

| Growth Rate (2025 - 2030) | 12.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

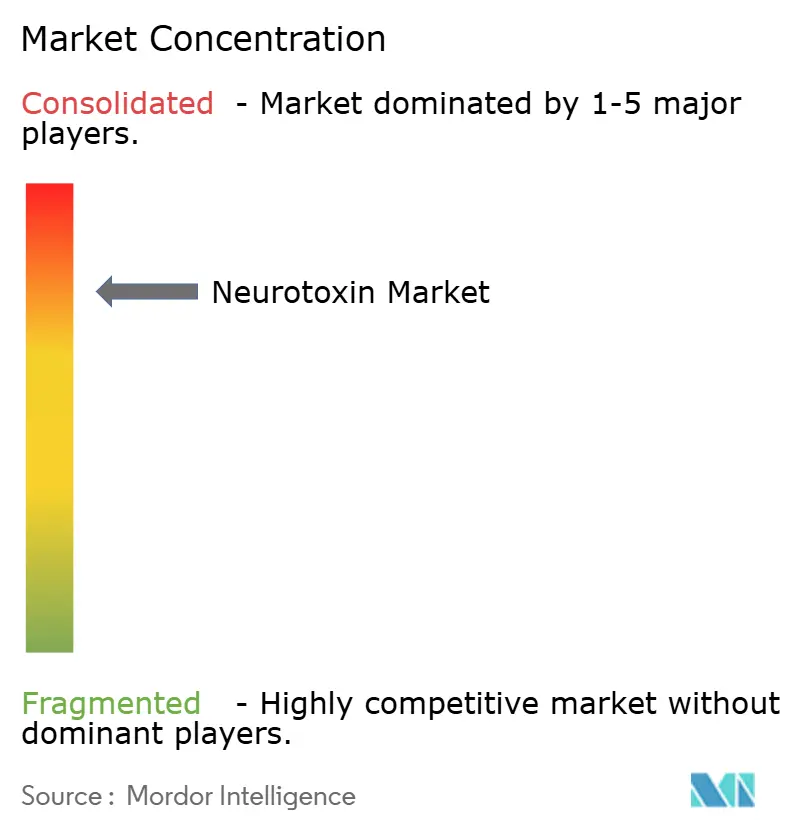

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurotoxin Market Analysis by Mordor Intelligence

The Neurotoxin market size reached USD 8.4 billion in 2025 and is forecast to reach USD 15.3 billion by 2030, registering a 12.1% CAGR during the period. Continuous diversification from purely cosmetic use toward reimbursed therapeutic indications, coupled with strong consumer demand for minimally invasive procedures, underpins this momentum. North American procedure volumes remain stable despite macroeconomic fluctuations, while regulatory convergence across Asia Pacific accelerates product approvals and local manufacturing scale-ups. Pipeline progress in long-acting and liquid formulations enhances brand differentiation and supports premium pricing. In parallel, precision-guided injection systems improve clinical outcomes, reinforcing practitioner confidence and encouraging wider adoption across age groups.

Key Report Takeaways

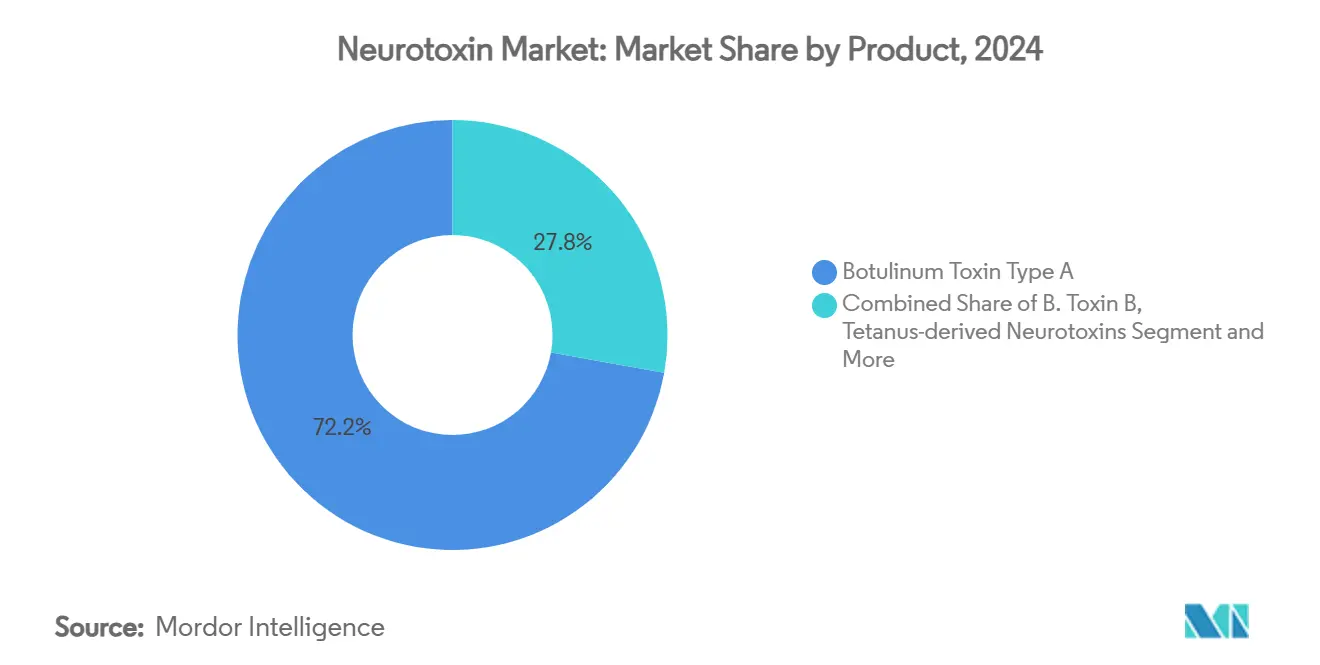

- By product type, botulinum toxin Type A captured 72.2% of 2024 revenue, solidifying its position as the dominant formulation.

- By therapeutic application, aesthetic indications accounted for 53.3% share of the Neurotoxin market size in 2024.

- By end user, hospitals and clinics delivered 45.9% of global injections in 2024, maintaining the largest distribution footprint.

- By region, North America held 43.7% of the Neurotoxin market share in 2024, remaining the single-largest geographic contributor.

Global Neurotoxin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding aesthetic procedure volumes | +3.20% | Global, concentration in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of chronic migraine & spasticity | +2.80% | Global, aging high-income economies | Long term (≥ 4 years) |

| Favorable reimbursement for therapeutic uses | +2.10% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Pipeline long-acting & liquid neurotoxins | +1.90% | Early uptake in North America | Long term (≥ 4 years) |

| Emergence of biosimilar/biobetter toxins in Asia | +1.40% | Asia Pacific core, spill-over to emerging markets | Medium term (2-4 years) |

| AI-guided injection techniques improving outcomes | +0.80% | North America, Europe, selective Asia Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Aesthetic Procedure Volumes

Consumers increasingly view neurotoxin treatments as routine self-care rather than discretionary luxury, sustaining demand even during economic slowdowns. Procedure counts remain higher than other minimally invasive options due to predictable safety profiles and short recovery times. Rising acceptance among younger cohorts, particularly those in their late twenties seeking preventative interventions, establishes recurrent revenue cycles for clinics. Rapid proliferation of accredited medical spas improves geographic accessibility and broadens the customer base. Private investment continues to flow into dedicated aesthetic platforms, supporting staff training, marketing reach and technology adoption that collectively enlarge the addressable population.

Rising Prevalence of Chronic Migraine & Spasticity

Chronic migraine affects roughly 1% of the global population and imposes substantial quality-of-life burdens; botulinum toxin has demonstrated superior prophylactic efficacy compared with traditional oral regimens.[1]Neurology Editorial Board, “Efficacy and Safety of DaxibotulinumtoxinA,” neurology.org Similarly, post-stroke and cerebral palsy-related spasticity rise in tandem with aging populations, prompting first-line adoption of neurotoxin injections that reduce long-term care expenditure. Stable reimbursement codes in major markets create predictable revenue for providers and manufacturers alike. Ongoing trials in depression and anxiety suggest further expansion of reimbursed therapeutic indications, reinforcing the Neurotoxin market’s resilience to cosmetic demand cycles. Combined, these factors secure a broad, clinically validated platform for sustained volume growth beyond aesthetic usage.

Favorable Reimbursement for Therapeutic Uses

Medicare and analogous European payers acknowledge the cost-effectiveness of neurotoxin therapy for several neurological conditions, providing structured coverage criteria and dose ceilings that encourage appropriate utilization.[2]Centers for Medicare & Medicaid Services, “Botulinum Toxin Injections LCD,” cms.gov Alignment by commercial insurers mirrors these policies, minimizing patient out-of-pocket exposure and accelerating uptake. Clear CPT and ICD-10 coding frameworks streamline provider billing, lowering administrative overhead. Countries across Asia Pacific are progressively integrating neurotoxin reimbursement into national formularies, broadening geographic penetration and smoothing revenue variability for manufacturers. Such supportive payor environments underpin capital investment in expanded manufacturing and distribution capabilities worldwide.

Pipeline Long-Acting & Liquid Neurotoxins

Extended-duration products such as daxibotulinumtoxinA achieve median efficacy lasting up to 24 weeks, thereby halving injection frequency relative to legacy brands and raising patient satisfaction. Liquid presentations remove reconstitution steps, reducing preparation errors and clinic chair time while preserving potency under standard refrigeration. Nanoparticle carriers under investigation promise tunable release profiles, introducing the possibility of individualized retreatment schedules. Regulatory agencies offer established pathways for these innovations, and early clinical milestones support premium launch pricing that improves overall market value. Collectively, next-generation formulations differentiate portfolios and sustain competitive barriers to entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Botox circulation in gray markets | -1.80% | Global, emphasis on unregulated channels | Short term (≤ 2 years) |

| Stringent cold-chain logistics for biologics | -1.20% | Global, higher impact in resource-limited settings | Medium term (2-4 years) |

| Adverse event visibility on social media | -0.90% | Worldwide, social-media-active demographics | Short term (≤ 2 years) |

| Patent cliffs & IP litigation risk | -0.70% | Developed markets with strong IP enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Botox Circulation in Gray Markets

Seventeen counterfeit-related botulism cases across nine US states required hospitalization, underscoring patient safety risks and eroding brand trust.[3]Centers for Disease Control and Prevention, “Investigation Update on Harmful Reactions Linked to Counterfeit Botox,” cdc.gov Social media advertising by unlicensed practitioners amplifies exposure to substandard vials, while online cross-border shipments complicate regulatory policing. Such incidents heighten scrutiny from health authorities, potentially delaying new indication approvals and increasing compliance costs for legitimate manufacturers. Clinics and pharmacies intensify supplier vetting, investing in serialization and authentication tools that raise operational expenses. Persistent counterfeiting, therefore, constrains short-term growth by provoking caution among consumers and regulators alike.

Stringent Cold-Chain Logistics for Biologics

Botulinum toxin requires uninterrupted 2-8 °C storage from factory to point of use; temperature excursions degrade potency and introduce liability risk. Maintaining validated refrigeration throughout transport, warehousing and in-clinic handling elevates distribution costs, especially in emerging markets with fragile infrastructure. Smaller practices face upfront investment in monitoring equipment, hampering service expansion into rural areas. Liquid formulations, while convenient, may demand tighter controls than lyophilized powders, adding complexity. Manufacturers respond with temperature-stable packaging and real-time tracking systems, yet the capital burden continues to temper near-term penetration in cost-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Type A Stability Meets Biosimilar Competition

Type A botulinum toxin remained the mainstay, reflecting decades of clinical usage and broadest regulatory clearance. The Neurotoxin market size for Type A accounted for the largest revenue slice in 2024, anchored by onabotulinumtoxinA’s entrenched physician familiarity. Neutralizing antibody incidence remains low, preserving long-term patient responsiveness. However, Korean developers have achieved US approval for Letybo, signaling a wave of Asian biosimilar entries that will gradually erode price premiums. Type B agents cater to patients who develop resistance to Type A, yet dosing complexities and localized pain limit volume. Tetanus-based investigational neurotoxins aim to bypass existing patents, potentially diversifying therapeutic options post-2030. Over the forecast window, Type A dominance persists but its Neurotoxin market share edges downward as biosimilar competition intensifies and alternative serotypes secure niche footholds.

The innovation race now centers on duration-enhanced and ready-to-use Type A variants, which reinforce brand differentiation while maintaining legacy safety profiles. Manufacturers deploy education programs to reaffirm efficacy advantages relative to lower-cost generics, yet payer focus on budget impact accelerates formulary inclusion of proven biosimilars. Overall, differentiated premium offerings occupy the upper price tier, while bulk-produced regional brands penetrate volume-driven segments, collectively broadening patient access.

By Therapeutic Application: Aesthetic Volume Leads, Chronic Migraine Accelerates

Aesthetic procedures contributed the greatest portion of 2024 revenue as self-pay clients favor predictable, short-downtime interventions. Clinics leverage subscription-style treatment packages that lock in return visits every three to four months, creating consistent cash flow. Chronic migraine indications expand fastest, posting a 9.9% CAGR through 2030 on the back of strong Phase III evidence and payer recognition of emergency visit avoidance savings. Spasticity care remains stable, underpinned by aging demographics and broad neurology adoption. Hyperhidrosis application growth accelerates as consumer awareness of minimally invasive options rises, supported by favorable reimbursement in select European countries. Emerging psychiatric uses, including treatment-resistant depression, continue in development and may augment the Neurotoxin market by the late decade when pivotal data matures.

Across therapeutic categories, bundled payment models encourage multidisciplinary collaboration, integrating neurotoxin injections into holistic neurology and rehabilitation pathways. Long-acting formulations will particularly benefit chronic migraine and dystonia patients by extending intervals, thereby improving adherence and reducing annual injection counts without ceding efficacy.

By Distribution Channel: Online Expansion Reconfigures Fulfillment

Hospital and specialty-clinic pharmacies commanded 49.5% of 2024 sales value, reflecting entrenched hospital purchasing contracts and reimbursement alignment. Nonetheless, online pharmacies, leveraging verified telehealth consultations, are advancing at a 15.8% CAGR through 2030, driven by post-pandemic acceptance of remote care and direct-to-consumer convenience. Certified e-dispensaries integrate temperature-controlled packaging with track-and-trace authentication, appealing to tech-savvy users wary of counterfeit risk. Wholesale distributors modernize with blockchain-based monitoring to reassure regulators and insurers that supply integrity is maintained. The resulting omni-channel ecosystem reduces access disparities, especially in suburban and rural zones where brick-and-mortar pharmacies lack specialized biologics storage.

Competitive interplay intensifies as manufacturers offer differentiated support programs, including drop-shipping and nurse training, to maintain brand loyalty across both institutional and digital outlets. While regulatory frameworks still evolve regarding biologic e-commerce, early pilot programs in the United States and South Korea illustrate scalable compliance models that other countries are likely to emulate.

By End User: Med Spas Redefine Patient Experience

Hospitals and clinics delivered nearly half of injections in 2024, yet the experiential model popularized by medical spas is reshaping expectations. Purpose-built aesthetic centers merge hospitality ambience with physician oversight, creating premium environments that encourage cross-selling of adjunct dermal therapies. Med spas now perform an estimated 40–55% of cosmetic neurotoxin sessions in high-income economies, signaling a shift from purely medical settings toward lifestyle-oriented venues. Mobile nurse injectors supported by tele-supervision extend reach to homebound or time-constrained clients, further diversifying the delivery landscape. Regulatory variance concerning non-physician injectors creates both opportunity and risk; jurisdictions with relaxed supervision rules witness faster establishment rates but must address quality assurance gaps.

Research laboratories, though a minor revenue contributor, play a pivotal role in expanding therapeutic frontiers through investigator-initiated trials and device-drug combination studies. Their collaborations with academic institutions accelerate translational research, ensuring that emerging indications are swiftly validated and commercialized.

Geography Analysis

North America retained leadership with 38.4% revenue share in 2024, supported by robust insurance coverage and well-defined FDA guidance that streamlines supplemental indication approvals. Concentrations of board-certified injectors in metropolitan hubs sustain procedure density, while mobile services extend cosmetic offerings to suburban locales. Investment in domestic fill-finish capacity, illustrated by ongoing USD 2 billion facility expansion plans, enhances supply security and shortens lead times.

Asia Pacific posts the fastest expansion, advancing at a 9.2% CAGR to 2030 on the strength of middle-class consumption growth and proactive regulatory harmonization that expedites dossier review. Local biosimilar manufacturing in South Korea and China lowers average selling prices and stimulates wider uptake beyond urban elites. Government-funded practitioner training programs elevate injection quality, mitigating early safety concerns and fostering community acceptance.

Europe follows steady growth amid mature healthcare systems and stringent pharmacovigilance. National reimbursement disparity remains the primary barrier, yet aging populations and chronic neurological disease prevalence sustain baseline demand. Post-Brexit supply adjustments have largely stabilized, with parallel import programs cushioning price pressures and ensuring consistent product availability across member states.

Competitive Landscape

The Neurotoxin market exhibits a high concentration, with AbbVie controlling 68% share via the Botox franchise. Entrants counterbalance this dominance through differentiated claims, such as 24-week duration and rapid onset, that appeal to both clinicians and patients. Active portfolio management drives consolidation; Crown Laboratories’ USD 924 million purchase of Revance.

Therapeutics exemplifies strategic moves to acquire technology platforms that promise durable competitive edges. Biosimilar originators leverage price-value positioning, targeting tender-driven public systems and offering volume rebates to secure formulary inclusion.

Leaders invest in AI-guided injector systems that standardize dosing depth and placement, reducing variance and adverse event rates. Partnerships with device firms accelerate this capability, leading to integrated product-service bundles that lock in practitioner loyalty. Government defense contracts, such as the USD 250 million award to Resilience for toxin countermeasures, highlight dual-use relevance and provide incremental funding for process innovation. Collectively, R&D pipelines focus on serotype diversity, novel indications and scalable biomanufacturing that sustains gross margins despite gradual price erosion.

Neurotoxin Industry Leaders

AbbVie (Allergan)

Ipsen

Merz Pharma

Revance Therapeutics

Daewoong Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AbbVie submitted a Biologics License Application for trenibotulinumtoxinE, targeting expanded neurological indications.

- August 2024: Crown Laboratories closed its USD 924 million acquisition of Revance Therapeutics, adding Daxxify to its aesthetic portfolio.

- March 2024: Hugel received United States approval for letibotulinumtoxinA, the first Korean-manufactured toxin authorized across US, Chinese and European markets simultaneously.

Global Neurotoxin Market Report Scope

| Botulinum Toxin Type A |

| Botulinum Toxin Type B |

| Tetanus-derived Neurotoxins |

| Other Neurotoxins |

| Aesthetic Indications |

| Chronic Migraine |

| Spasticity |

| Cervical Dystonia |

| Hyperhidrosis |

| Other Therapeutic Uses |

| Hospitals & Clinics |

| Dermatology & Cosmetic Centers |

| Research Laboratories |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Botulinum Toxin Type A | |

| Botulinum Toxin Type B | ||

| Tetanus-derived Neurotoxins | ||

| Other Neurotoxins | ||

| By Therapeutic Application | Aesthetic Indications | |

| Chronic Migraine | ||

| Spasticity | ||

| Cervical Dystonia | ||

| Hyperhidrosis | ||

| Other Therapeutic Uses | ||

| By End User | Hospitals & Clinics | |

| Dermatology & Cosmetic Centers | ||

| Research Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected global value of the Neurotoxin market in 2030?

The market is forecast to reach USD 15.3 billion by 2030, expanding at a 12.1% CAGR.

Which region shows the fastest future growth for neurotoxins?

Asia Pacific leads with a projected 9.2% CAGR through 2030, driven by regulatory harmonization and local manufacturing scale-up.

How long can next-generation long-acting neurotoxins maintain clinical effect?

Clinical trials report median durations up to 24 weeks, twice that of traditional 1216-week formulations.

Which therapeutic indication currently grows quickest?

Chronic migraine prophylaxis leads with a 9.9% CAGR attributable to strong clinical efficacy and reimbursement support.

What percentage of 2024 revenue did hospital pharmacies capture?

Hospital pharmacies accounted for 49.5% of global sales, though online channels are expanding much faster.

Why is counterfeit Botox considered a major industry restraint?

Confirmed hospitalization cases linked to counterfeit injections highlight patient safety risks and prompt stricter regulatory oversight, dampening short-term demand growth.

Page last updated on: