Elbow Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

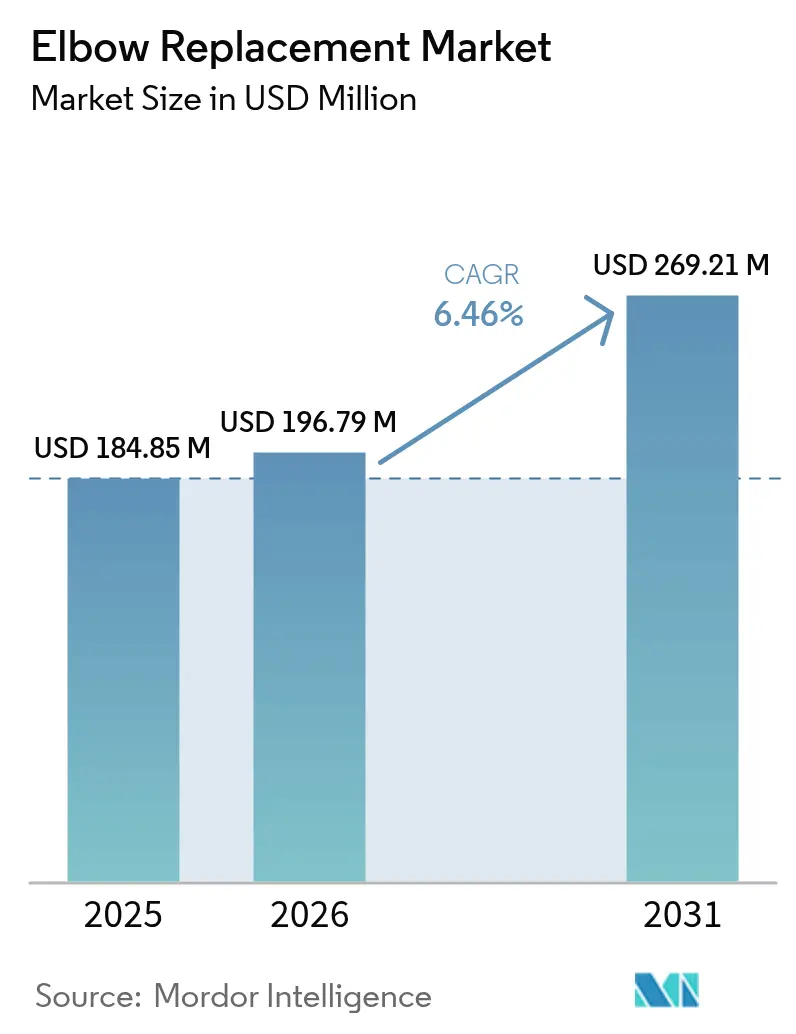

| Market Size (2026) | USD 196.79 Million |

| Market Size (2031) | USD 269.21 Million |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

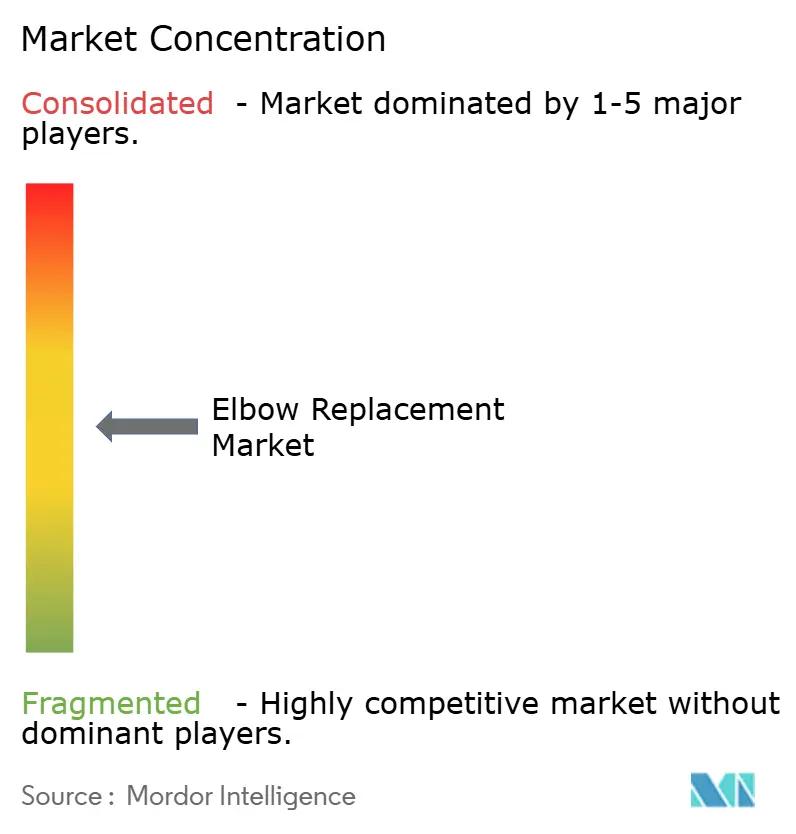

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elbow Replacement Market Analysis by Mordor Intelligence

Elbow Replacement Market size in 2026 is estimated at USD 196.79 million, growing from 2025 value of USD 184.85 million with 2031 projections showing USD 269.21 million, growing at 6.46% CAGR over 2026-2031.

Escalating end-stage elbow arthritis cases, wider surgeon familiarity with total elbow arthroplasty, and steady improvements in 3D-printed, patient-matched implants anchor this expansion. Rapid gains in outpatient surgical infrastructure, coupled with favorable reimbursement adjustments for complex extremity procedures, further widen patient access. Linked-hinge prostheses are outperforming earlier designs on revision-free survival, while antimicrobial surface technologies cut deep infection risk and drive long-term implant success. The elbow replacement market also benefits from rising procedure volumes in Asia-Pacific as hospitals modernize orthopedic theaters and local manufacturers secure regulatory clearances.

Key Report Takeaways

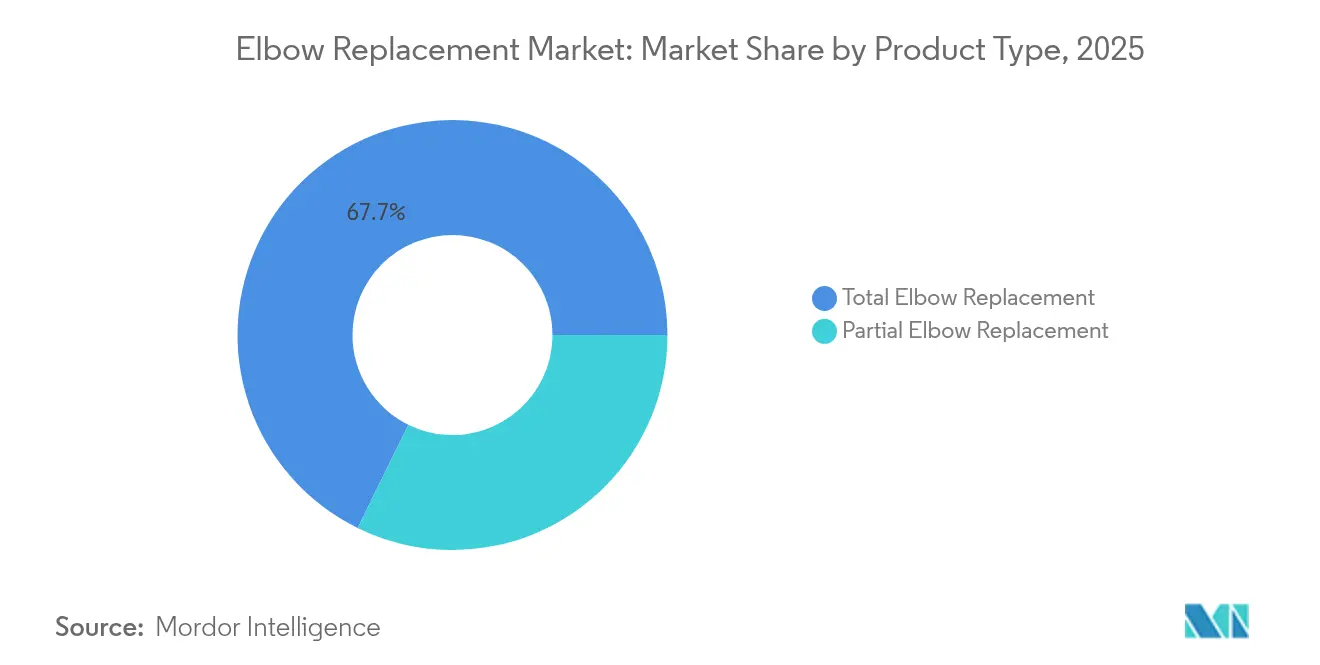

- By product type, total elbow replacement led with 67.73% revenue share in 2025; partial elbow replacement is advancing at a 6.67% CAGR through 2031.

- By implant material, cobalt-chrome alloys captured 51.10% of the elbow replacement market share in 2025; titanium alloys record the fastest growth at 6.88% CAGR to 2031.

- By fixation technique, cemented approaches maintained 62.65% dominance in 2025, while cement-less systems expand at an 7.74% CAGR through 2031.

- By end user, hospitals held 56.88% of the elbow replacement market size in 2025; orthopedic and specialty centers post the highest growth at 8.35% CAGR to 2031.

- By geography, North America accounted for 39.42% of 2025 revenues, whereas Asia-Pacific is set to climb at a 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elbow Replacement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of arthritis | +1.2% | Global, higher in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of linked-hinge designs | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Technological advances in 3D-printed implants | +1.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Shift toward outpatient/ASC settings | +1.1% | North America core, spill-over to EU & APAC | Short term (≤ 2 years) |

| Expanding reimbursement in emerging markets | +0.9% | APAC, Latin America & MEA | Long term (≥ 4 years) |

| Antimicrobial coating breakthroughs | +0.7% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Arthritis

Widespread osteo- and rheumatoid arthritis continues to swell the surgical waitlist for elbow reconstruction. Clinical registries show Mayo Elbow Performance Scores improving from 39 to 95 after total arthroplasty, validating surgery as a durable pain-relief strategy.[1]A. Smith, “Anconeus-Reflected Triceps Tongue Approach Outcomes,” Journal of Clinical Medicine, mdpi.com Population aging and higher activity expectations among seniors lock in a steady flow of candidates over the long term. New exposure-sparing techniques such as the anconeus-reflected triceps tongue approach lessen soft-tissue disruption, supporting faster rehabilitation. These advances collectively sustain procedure volumes in all key geographies and reinforce the elbow replacement market trajectory.

Rapid Adoption of Linked-Hinge Designs

Semi-constrained linked-hinge prostheses deliver greater varus-valgus stability than earlier unconstrained devices, especially for elbows with extensive bone loss. Meta-analyses report lower loosening and higher 10-year survivorship in inflammatory arthritis cases relative to non-linked systems.[2]R. Lee, “Linked-Hinge Elbow Survivorship Analysis,” ScienceDirect, sciencedirect.com As clinical curricula integrate these techniques, surgeon preference is shifting, boosting implant demand across referral centers in North America and Western Europe. Manufacturers are refining modular stems and tapered flanges that ease intraoperative alignment while safeguarding native kinematics.

Technological Advances in 3-D Printed Implants

Additive manufacturing now produces lattice-structured elbows tailored to each patient’s CT scan, delivering press-fit fixation and near-physiologic stress distribution. Surgical time savings of 44 minutes and fewer fluoroscopy checks have been documented with customized guides. Emerging PEEK-titanium hybrids pair bone-mimicking modulus with bactericidal coatings, further elevating long-term outcomes. Widespread rollout of hospital-based 3D labs in the United States accelerates adoption, while regional contract printing hubs serve European and APAC markets.

Shift Toward Outpatient/ASC Settings

Same-day discharge initiatives trim total episode cost by USD 8,400 compared with inpatient stays, even after higher outpatient therapy charges are included. CMS proposals adding various joint arthroplasties to the ASC list signal growing policy support. Comparable readmission rates and enhanced patient satisfaction are persuading private payers to reimburse elbow replacements outside hospital walls, steering case volume toward purpose-built specialty centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternatives (arthroscopy, fusion) | -0.8% | Higher adoption in developed markets | Medium term (2-4 years) |

| High procedure & device cost | -1.2% | Pronounced in emerging markets | Long term (≥ 4 years) |

| Post-operative complications and implant longevity | -0.9% | Higher impact in younger cohorts | Long term (≥ 4 years) |

| Limited availability of specialized surgeons | -0.6% | Acute in emerging & rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternatives

Minimally invasive arthroscopy offers cartilage debridement and synovectomy that defers definitive joint replacement, especially attractive to younger athletes. Elbow fusion remains a fallback for gross instability or infection, achieving fusion rates above 90% at set positions optimal for daily tasks. Regenerative injections using platelet-rich plasma and stem cells have also carved a niche in early-stage degeneration. These substitute pathways, though serving selected indications, collectively divert a measurable slice of surgical candidates away from the elbow replacement market.

High Procedure & Device Cost

Implant hardware represents up to 63% of outpatient episode cost, limiting affordability in uninsured segments.[3]B. Khan, “Cost Contribution of Implants in Outpatient Arthroplasty,” The Permanente Journal, ncbi.nlm.nih.gov Added complexity versus hip or knee arthroplasty extends operative time and intensifies resource use. Frequent revisions in younger patients inflate lifetime expense, prompting cautious payer policies in many middle-income economies. To counter, manufacturers are localizing component machining and embracing reusable instrumentation kits that trim per-case spend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Total Replacement Remains the Benchmark

Total elbow replacement generated 67.73% of 2025 revenue, underlining its role as a comprehensive solution for severe articular destruction. This dominance reflects decades of outcome data showing median Mayo scores jumping from the low 40s to the mid-90s post-surgery. Partial systems, covering hemi-arthroplasty and radial head prostheses, are climbing at a 6.67% CAGR through 2031 as they better suit younger trauma patients. Surgeons increasingly reserve total systems for inflammatory or end-stage degenerative conditions while opting for bone-preserving partial options in complex fractures, expanding the elbow replacement market addressable base.

Clinical registries corroborate these trends, noting partial implants achieve 17% reoperation rates—acceptable given the elbow’s demanding biomechanics—when postoperative weight limits are respected. Both categories benefit from intraoperative 3D navigation that sharpens component alignment. In parallel, modular ulnar stems let surgeons upsize fixation when encountering osteoporotic canals, further reducing early loosening. This blend of versatility and evidence retention secures steady volume growth across both product lines within the elbow replacement market.

By Implant Material: Titanium’s Osseointegration Edge

Cobalt-chrome retained 51.10% share owing to its proven wear resistance, yet titanium alloys are notching a 6.88% CAGR. Threaded titanium stems boost cancellous purchase and reduce stress shielding, qualities that resonate with surgeons focused on long-term bone preservation. Novel porous tantalum sleeves and PEEK composites continue in niche roles but command interest for revision cases with compromised bone stock.

Laser-textured surfaces and hydroxyapatite coatings amplify titanium’s osteoconductivity, enabling earlier functional loading. Concurrently, antimicrobial film deposition targets periprosthetic infection, a pivotal failure mode. As these enhancements mature, material mix is likely to tilt incrementally toward titanium without displacing chrome-cobalt’s seat in high-demand applications. The elbow replacement market size for titanium-based systems is therefore expected to climb meaningfully yet progressively over the forecast horizon.

By Fixation Technique: Cement-Less Uptake Accelerates

Cemented fixation still accounts for 62.65% of implantations, valued for immediate stability, especially in osteopenic bone. However, cement-less techniques outpace at an 7.74% CAGR as porous architectures and press-fit stems foster biological integration. Cases employing cement-less humeral components paired with cemented ulnar stems illustrate a pragmatic hybrid pathway that eases future revision.

Ten-year survivorship exceeding 94% for cement-less partial knees has emboldened regulators to green-light similar concepts for the elbow. Surgeons appreciate shorter operative windows and avoidance of cement mantle complications. Consequently, the elbow replacement market share of fully biological fixation is forecast to widen primarily in urban centers handling higher volumes of younger, high-demand patients.

By End User: Specialty Hubs Gain Momentum

Hospitals retained 56.88% revenue share in 2025, a function of critical-care backup and broad insurance acceptance. Specialized orthopedic centers, though smaller, are expanding at 8.35% CAGR by leveraging dedicated teams, fast-track pathways, and bundled-payment contracts. Patient satisfaction scores consistently run higher in these settings, fuelling positive word-of-mouth and surgeon alignment.

ASC-based programs are emerging where payer policy permits, bundling anesthesia, implant, and therapy in single-invoice models that streamline reimbursement. Manufacturers now partner directly with high-volume centers to field test next-gen elbows under real-world conditions, reinforcing the sector’s influence on device design and procurement.

Geography Analysis

North America preserved leadership with 39.42% of 2025 turnover, thanks to robust reimbursement frameworks and a dense network of fellowship-trained upper-extremity surgeons. Medicare fee stability and clearly defined CPT codes underpin steady procedural uptake. Europe follows, buoyed by stringent MDR standards that reassure clinicians of implant safety while still encouraging innovation through fast-track 3D printing approvals.

Asia-Pacific is the fastest riser, projected at 7.22% CAGR, as China, India, and South Korea broaden social insurance and cultivate domestic implant fabrication. National procurement drives lower unit prices, expanding hospital budgets for complex reconstructions. Latin America and the Middle East & Africa trail but show meaningful upside where urban private hospitals install advanced imaging and laminar-flow theaters. Collectively, these patterns support geographically diversified growth for the elbow replacement market.

Competitive Landscape

Market concentration is moderate, with a handful of global orthopedic firms controlling the premium segment and regional specialists catering to value-tier demand. Enovis reinforced its extremities franchise through the EUR 800 million LimaCorporate acquisition in 2024, unlocking proprietary Trabecular Titanium 3D platforms. Stryker’s prior Wright Medical purchase delivered entry to a complementary trauma and biologics pipeline. Zimmer Biomet continues to integrate AI-enabled imaging after buying OrthoGrid, aiming to refine intraoperative alignment.

Strategic priorities center on additive manufacturing, antimicrobial surfaces, and robotics-assisted alignment. Cross-licensing between implant and software vendors accelerates development cycles, while hospital-aligned partnerships foster procedural standardization. Overall, technological differentiation and emerging-market penetration remain decisive fronts in the elbow replacement market competition.

Elbow Replacement Industry Leaders

Johnson & Johnson

Stryker Corporation

Zimmer Biomet

Smith & Nephew plc

Enovis

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is procedural standardization that reduces variability in elbow arthroplasty. Patient-specific instrumentation (PSI), based on preoperative 3D planning and customized 3D-printed guides, is used to improve bone resection accuracy and component alignment in total elbow arthroplasty. This approach supports broader uptake beyond high-volume referral surgeons and fits with the report's shift toward outpatient and specialty-center pathways, where repeatable workflows and shorter operating-room time compete alongside implant pricing.

A second opportunity comes from closer convergence between reconstruction implants and adjacent extremity and trauma ecosystems, where regulatory clearances and platform launches increase surgeon touchpoints with the same vendor. US FDA 510(k) clearances for elbow and forearm fixation systems (for example, TriMed Elbow and Forearm System in March 2025 and Avanti Distal Elbow ORIF System in May 2026, plus Arthrex Elbow Fracture Plating System in November 2024) expand the installed base of elbow-specific instruments and associated vendor relationships in hospitals and specialty centers. In parallel with ongoing consolidation and portfolio expansion in extremities (including Enovis integrating LimaCorporate and its 3D-printed Trabecular Titanium capabilities), these developments are reinforcing roadmaps that bundle implants with planning, navigation, and training offerings rather than competing primarily on implant geometry.

Recent Industry Developments

- May 2026: Avanti Orthopaedics, LLC received a US FDA 510(k) clearance for its Avanti Distal Elbow ORIF System. The clearance adds another actively marketed elbow-specific fixation platform, supporting vendor pull-through of instrumentation and surgeon familiarity that can influence reconstruction and revision pathways around elbow arthroplasty.

- October 2025: Johnson & Johnson announced its intent to separate its Orthopaedics business into a standalone company to be named DePuy Synthes, with completion targeted within 18 to 24 months. The planned separation reshapes capital allocation and go-to-market focus for one of the largest orthopaedics portfolios, which can affect extremities product investment, channel strategy, and partnering across joint reconstruction.

- January 2024: Enovis completed its acquisition of LimaCorporate S.p.A. for EUR 800 million, forming a larger reconstruction platform with a substantial extremities footprint. The transaction strengthened Enovis capabilities in 3D-printed Trabecular Titanium implants and broadened its global distribution reach, raising competitive intensity in upper-extremity arthroplasty portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the elbow replacement market covers revenues from elbow arthroplasty implant systems used to replace part or all of the elbow joint, counted at the manufacturer level and converted to USD for global comparability.

Scope exclusions: We exclude trauma fixation plates, isolated radial-head prostheses, rehabilitation services, and repair consumables.

Segmentation Overview

- By Product Type

- Partial Elbow Replacement

- Total Elbow Replacement

- By Implant Material

- Titanium Alloys

- Cobalt–Chrome Alloys

- Tantalum & Others

- By Fixation Technique

- Cemented

- Cement-less

- By End User

- Hospitals

- Orthopedic & Specialty Centers

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for procedure demand and the care setting mix before the model was built. We reviewed public health statistics and orthopedic care data from sources such as the US CDC and National Center for Health Statistics, the OECD health database, and selected national health ministries, which helped us sanity-check volumes and aging trends.

Clinical and product context was further checked using sources such as the US FDA device databases, peer-reviewed orthopedic journals, and guidance from professional associations such as AAOS. We also reviewed company filings, investor presentations, and reputable press coverage to understand portfolio focus and pricing narratives, and we selectively used paid subscriptions for company financials and patent databases where they filled specific data gaps. The desk sources named here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as an elbow replacement system, how pricing differs by fixation and material mix, and how hospital purchasing patterns shift across regions. We spoke with stakeholders across manufacturing, distribution, and clinical procurement, and we used this input to stress-test assumptions when public procedure data was thin or inconsistently reported across countries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 39% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 36% |

| Smaller Players: 16% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where country demand pools are reconstructed from treated patient volumes and orthopedic procedure signals, then aligned to the portion clinically eligible for partial or total elbow replacement. Inputs that matter in this market include arthritis and trauma burden in older adults, the orthopedic surgeon base and hospital infrastructure, payer coverage and reimbursement posture, the mix of cemented versus cement-less fixation, and typical replacement prices by material and implant design.

Those totals were then corroborated using selective bottom-up checks, such as supplier share mapping, channel discussions, and sampled ASP times volume logic for key countries. This helped us adjust for underreporting and avoid double counting. When gaps appeared, they were handled with transparent proxy rules, for example by using comparable country procedure rates and scaling by population age bands and access indicators. Forecasting is based on scenario analysis, where growth drivers such as aging, elective surgery normalization, and price progression are varied within ranges agreed during interviews, and then reviewed against observed healthcare spending direction in each region.

Data Validation & Update Cycle

Validation is done through multiple passes, starting with consistency checks across procedure logic, pricing assumptions, and regional roll-ups, then moving to variance testing against independent signals such as orthopedic surgery throughput and reported implant mix trends. If any country-level result looks off, we re-check conversion rates, revisit the input series, and re-contact experts when a mismatch cannot be explained through documented assumptions.

Before sign-off, the model and narrative are reviewed by another analyst to catch anomalies and ensure included items match the written scope. Reports are refreshed annually, and interim updates are made when material events change demand or pricing assumptions, followed by a final pre-delivery review so clients receive the latest view.

Mordor Intelligence's Elbow Replacement Market Estimate Compared With Other Published Estimates

Different publishers can land on different market sizes because they do not always count the same items, use the same year definitions, or convert currencies the same way. Timing also matters, since procedure volumes and hospital purchasing can shift quickly after reimbursement changes or supply adjustments.

Isolated radial-head prostheses and trauma fixation plates are kept outside Mordor Intelligence's elbow replacement scope, which is one reason some published totals look higher even when the clinical backdrop is similar. Other gaps can come from mixing hospital selling prices with manufacturer-level values, using a single global ASP uplift without checking fixation and material mix, or relying on older base years without revalidating the key demand indicators.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 196.79 M (2026) | |

| Industry Publisher A | USD 150.74 M (2025) | Uses a different base year and forecast window, and pricing is not clearly tied back to fixation or material mix, which can shift the implied ASP and make year-over-year comparisons harder. |

| Industry Publisher B | USD 138.40 M (2023) | Anchors the size on an earlier year and does not spell out manufacturer-level versus end-user pricing, which can compress the value depending on what part of the supply chain is counted. |

Taken together, the spread is mainly explained by what is included, which year is used as the anchor, and how pricing is treated across the supply chain. By keeping the scope tied to elbow replacement systems and then checking outputs against procedure and pricing signals, we arrive at a market value that is easier to reconcile and repeat as new data comes in.

Key Questions Answered in the Report

What is the current size of the elbow replacement market?

The elbow replacement market size reached USD 196.79 million in 2026.

How fast is the market expected to grow?

It is projected to expand at a 6.46% CAGR, achieving USD 269.21 million by 2031.

Which product segment dominates the market?

Total elbow replacement accounts for 67.73% of 2025 revenue, maintaining clear leadership.

Why are titanium implants gaining popularity?

Titanium alloys promote superior bone integration and are growing at a 6.88% CAGR within the material mix.

Which region is showing the fastest growth?

Asia-Pacific is advancing at a 7.22% CAGR, driven by expanding healthcare coverage and rising surgical capacity.

How is outpatient surgery influencing the market?

Migration to ambulatory surgical centers lowers episode costs and accelerates procedure volumes, especially in North America and select European markets.

Page last updated on: