Intracranial Aneurysm Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 4.44 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

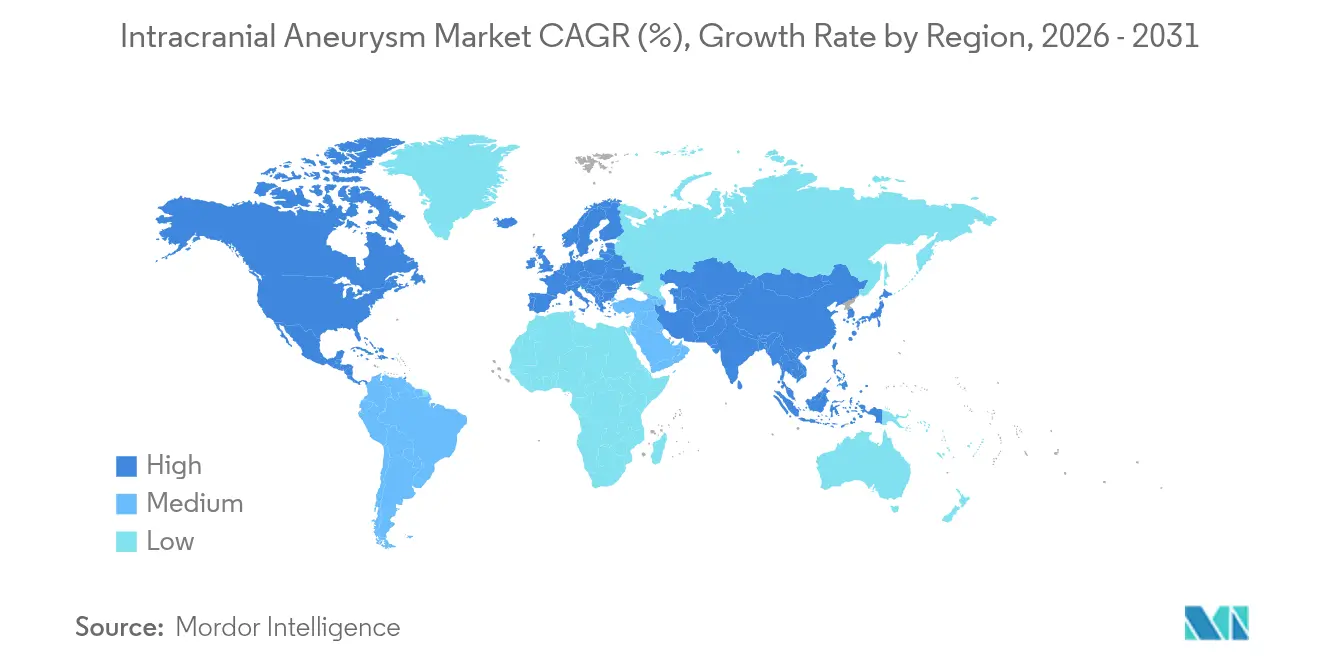

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intracranial Aneurysm Market Analysis by Mordor Intelligence

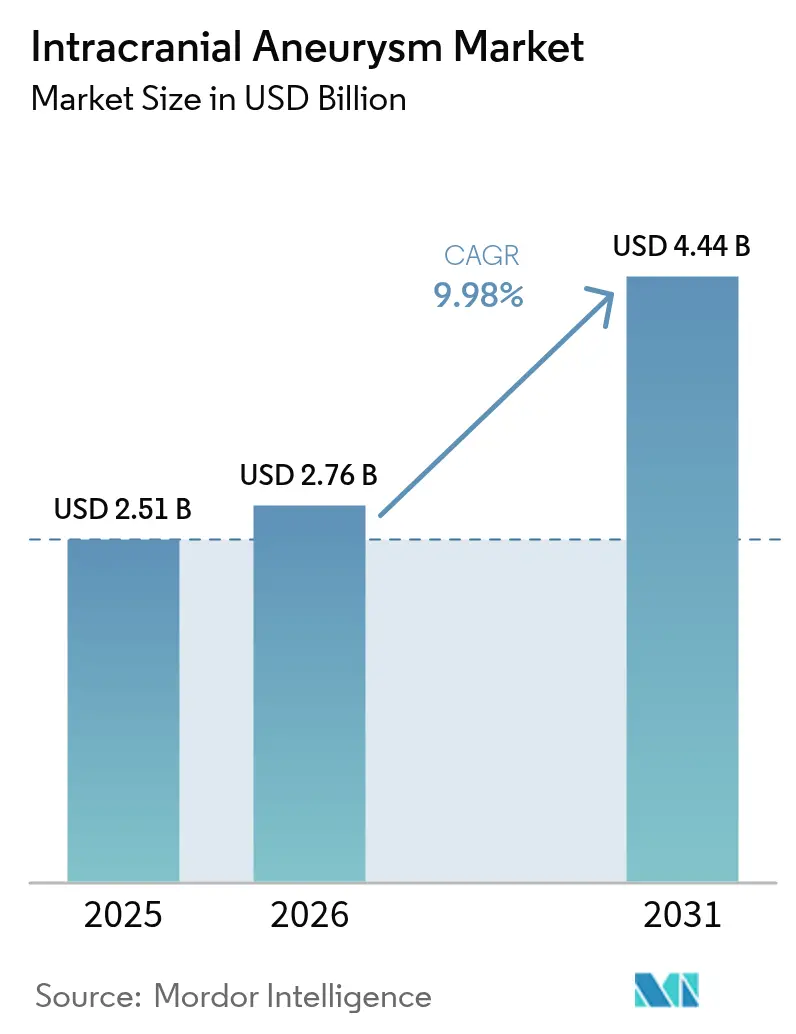

The intracranial aneurysm market size is expected to grow from USD 2.51 billion in 2025 to USD 2.76 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at 9.98% CAGR over 2026-2031. Flow diverters and intrasaccular devices are shifting care pathways away from bare platinum coiling, which held a 22.76% share in 2024, as single-device strategies reduce adjuncts and shorten catheterization times. Ambulatory surgical centers are gaining procedural volume on same-day discharge economics, challenging hospitals that still dominate emergent cases. Asia-Pacific is the fastest-growing region at 11.45% as imaging penetration improves and interventional capacity expands, while North America’s 43.56% revenue share reflects a mature ecosystem built around comprehensive stroke centers and iterative device upgrades. Regulatory fast-tracks that compress review timelines create brief windows where insurgent products can scale before incumbents match indications, intensifying product cycles and clinical evidence races.

Key Report Takeaways

- By treatment type, endovascular coiling led with 22.36% revenue share in 2025, while flow diverters are forecast to expand at a 12.34% CAGR through 2031.

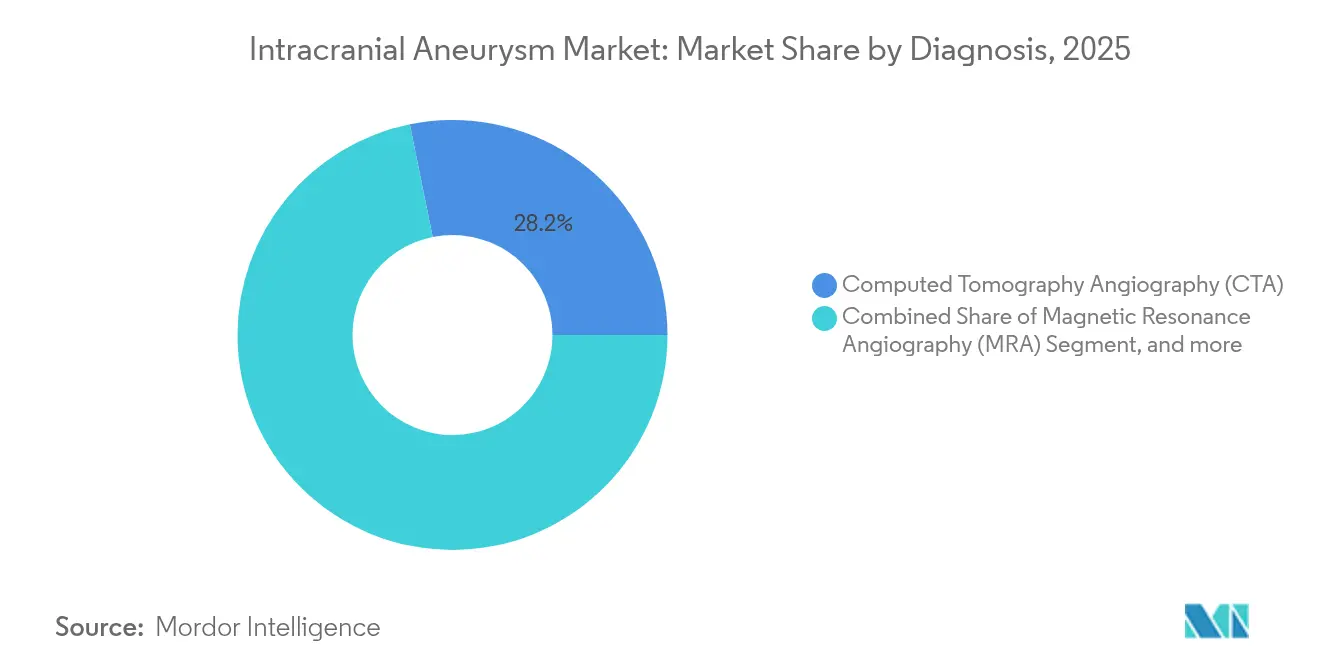

- By diagnosis, computed tomography angiography accounted for a 28.18% share in 2025, and 3D rotational angiography is projected to grow at a 11.88% CAGR to 2031.

- By end-user, hospitals represented 54.94% of revenue in 2025, while ambulatory surgical centers are expected to progress at a 12.52% CAGR.

- By geography, North America held 43.14% of revenue in 2025, and Asia-Pacific is estimated to advance at an 11.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Intracranial Aneurysm Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally invasive endovascular procedures | +3.2% | Global, concentrated in North America, Western Europe, and urban China and India | Medium term (2-4 years) |

| Growing detection of unruptured IA through incidental brain imaging | +2.8% | Global, led by North America and Western Europe, accelerating in APAC urban centers | Short term (≤ 2 years) |

| Aging-linked hypertension and smoking prevalence in developing economies | +2.1% | APAC core including China, India, and Indonesia, with spill-over to Latin America and the Middle East | Long term (≥ 4 years) |

| Regulatory fast-tracks compressing approval timelines (e.g., FDA Breakthrough) | +1.4% | United States with harmonization effects across the EU, Japan, and select APAC markets | Medium term (2-4 years) |

| Emergence of AI-guided robotic neuro-intervention platforms | +0.9% | High-income markets with early adopters in the U.S., Western Europe, and Japan, pilots in select APAC hubs | Medium term (2-4 years) |

| Venture funding into nano-engineered coil/implant surface technologies | +0.7% | Europe, China, and U.S. trial centers, with in-licensing by incumbents for broader portfolio integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Endovascular Procedures

Endovascular coiling has moved from a focus on ruptured lesions to broad use in unruptured aneurysms, setting lower treatment thresholds and favoring earlier intervention as centers optimize catheter-based workflows. Patients see shorter hospital stays and faster returns to normal activity compared with open surgery because craniotomy is avoided and perioperative risk is reduced. Flow diverters extend minimally invasive logic to complex and large aneurysms by redirecting blood flow across the neck and encouraging sac thrombosis, which streamlines device counts and reduces need for adjunctive stents. U.S. regulatory programs that prioritize devices addressing life-threatening conditions support faster review of next-generation flow-diverter and intrasaccular systems, which accelerates the cadence of therapeutic innovation. Increased procedural volumes motivate hospitals and specialized centers to invest in biplane angiography suites and higher resolution imaging, which in turn expands treatable anatomy and broadens the candidate pool among patients previously deemed unsuitable. Credentialing and training requirements shape adoption curves, but the cumulative direction of travel favors catheter-based modalities in both elective and acute settings[1]Medicare Payment Advisory Commission, “2024 Data Book: Health Care Spending and the Medicare Program,” medpac.gov .

Growing Detection of Unruptured IA Through Incidental Brain Imaging

Routine CT and MRI use for non-specific neurologic symptoms and trauma is identifying aneurysms in 2-3% of asymptomatic individuals as scanner resolution and utilization rise. The increase in incidental findings pushes more triage decisions into specialty clinics, where physicians weigh the low annual rupture risk of small aneurysms against patient anxiety and medico-legal considerations. High-income health systems with abundant imaging capacity register the highest detection rates, with Japan’s scanning intensity serving as a benchmark among OECD countries. Centralized stroke networks help absorb referral surges by consolidating neuro-intervention expertise in accredited centers that maintain round-the-clock access to endovascular care. AI algorithms now embedded in radiology workflows flag candidate lesions for review, which lifts sensitivity but can also lengthen worklists and channel more patients into surveillance or treatment pathways. The combined effect is a sustained pipeline of unruptured aneurysm referrals that strengthens the procedure base for the intracranial aneurysm market[2]U.S. Food and Drug Administration, “510(k) Premarket Notification – Viz ANEURYSM,” fda.gov.

Aging-Linked Hypertension and Smoking Prevalence in Developing Economies

Urbanizing populations across Asia-Pacific face high rates of hypertension, a major risk factor for aneurysm formation, while tobacco use remains elevated in several large middle-income countries. The demographic shift toward older age cohorts will grow the pool of patients who present with aneurysms in later decades of life. Expanding access to CT and MRI in emerging health systems exposes more aneurysms before rupture, but growth in detection outpaces specialist supply in many markets. Health system capacity building is uneven, so patients in secondary cities often travel to metro hubs or pay privately for access to advanced interventional services. Over the forecast period, epidemiology and access trends together underpin robust latent demand for endovascular treatment, especially where public and private investment in stroke centers and neuro-endovascular staffing is accelerating. Long-term cardiovascular risk control policies on hypertension and tobacco will also modulate regional treatment volumes over time[3].

Regulatory Fast-Tracks Compressing Approval Timelines

Breakthrough pathways for devices treating life-threatening conditions enable faster review cycles for technologies that improve on standard care, allowing earlier patient access and faster clinical learning. European device regulation and guidance have adapted to the specific risk-benefit profiles of neurovascular implants, which has helped restore approval predictability after initial transitions to the current framework. Japan’s regulatory authority has introduced expedited pathways for important devices in cerebrovascular disease, and review programs in parts of Asia prioritize domestic innovation while improving standards alignment. These fast-tracks sharpen competitive timelines as incumbents and new entrants aim to launch devices and expand indications before rivals build similar clinical evidence. Post-market surveillance shifts into sharper focus as devices reach real-world use with smaller pre-approval datasets, so hospitals and clinical societies rely more on registries and credentialing reviews. This regulatory tempo supports frequent iterations in flow diverters and intrasaccular options, increasing the pace of product cycles in the intracranial aneurysm market.

Restraints Impact Analysis of Intracranial Aneurysm Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device and procedural costs with uneven reimbursement coverage | -1.9% | Global, acute in emerging APAC and Latin America, and in U.S. self-pay or high-deductible segments | Short term (≤ 2 years) |

| Shortage of dual-trained endovascular neurosurgeons in emerging markets | -1.3% | APAC excluding Japan and South Korea, Sub-Saharan Africa, and parts of Latin America | Long term (≥ 4 years) |

| Device-related thrombo-embolic risks and DAPT adherence challenges | -0.8% | Global, higher burden where follow-up adherence and antiplatelet monitoring infrastructure are limited | Short term (≤ 2 years) |

| Exposure to platinum/cobalt price volatility across the supply chain | -0.6% | Global supply chains, with higher pass-through sensitivity in price-constrained emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Dual-Trained Endovascular Neurosurgeons in Emerging Markets

Endovascular aneurysm care requires combined skill sets in neurosurgery and interventional techniques that take years to develop. Training pipelines in developed regions supply enough operators to sustain volumes, but emerging geographies train far fewer specialists than current prevalence and detection would suggest. This mismatch creates geographic access gaps outside major cities and leads to patient travel or delayed treatment for elective cases. Building comprehensive stroke centers involves investments in angiography, neuro-ICU, and on-call neurosurgery, which slows ramp-up in resource-constrained environments. Policy initiatives that tie reimbursement to stroke center accreditation and outcomes have improved coverage in select countries, yet workforce scale remains a binding constraint. Tele-proctoring pilots indicate avenues for skill transfer and scale, but liability and credentialing ambiguity still limit reach.

High Device and Procedural Costs With Uneven Reimbursement Coverage

Device and supply costs for complex endovascular aneurysm repair are high, and facility fees, anesthesia, and specialist time add to total episode expense. In the U.S., inpatient DRG payment structures reimburse hospitals for neurovascular procedures, but margins depend on operating efficiency and complication avoidance. Private payer rates vary and can exceed public benchmarks, yet patient cost-sharing in high-deductible plans can deter elective treatment of unruptured aneurysms. In several emerging markets, flow diverters remain outside standard reimbursement lists, which shifts costs to patients and constrains access to advanced devices. European case-based payment varies by country, with some systems bundling device costs and others restricting advanced implants to defined criteria. Manufacturers balance pricing strategies between widening access in emerging markets and maintaining reference pricing in high-income countries, an equilibrium that affects adoption speed and site-of-service shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Intracranial Aneurysm Market Segment Analysis

By Treatment Type:

Flow Diverters Propel Device InnovationEndovascular coiling held a 22.36% share in 2025, and its durability across rupture status and aneurysm sizes keeps it foundational, while single-device architectures are rising for wide-necked lesions. Flow diverters are the fastest-growing category at a 12.34% CAGR to 2031 as operators reduce adjunctive stenting and coil counts for large and fusiform anatomies that previously demanded multi-device stacks. Intrasaccular flow disruptors attract use at bifurcations where coil retention is challenging and parent-vessel protection is essential. Adjunctive balloon- and stent-assisted coiling still contribute in anatomies where vessel geometry or neck configuration requires additional stabilization. Microsurgical clipping is increasingly reserved for younger patients with select bifurcations or cases where mass effect compels decompression, which sustains a smaller but essential surgical niche. Credentialing and training requirements have tightened after delayed ischemic events were observed in post-market registries for certain implants, prompting additional proctoring and center-level reviews to standardize use.

Device profile miniaturization now enables distal navigation through 0.017-inch microcatheters for newer flow diverters, extending reach beyond first-generation systems and increasing the proportion of treatable cases. Surface-engineered implants aim to cut the duration of dual antiplatelet therapy, and early clinical experience suggests faster endothelialization without compromising deliverability. For operators and centers, fewer devices per case and shorter procedure times improve resource utilization and throughput. As regulatory oversight emphasizes traceability and quality, device makers align with ISO 13485 and MDR standards to maintain compliant production and surveillance systems. The intracranial aneurysm market benefits from these engineering and process improvements because complex cases can be treated in a broader set of facilities with predictable protocols. The intracranial aneurysm market size for flow diverters is projected to expand at 12.34% CAGR between 2026-2031, reinforcing their role in reshaping therapy mix.

By Diagnosis:

3D Rotational Angiography Captures Intra-Procedural ValueComputed tomography angiography accounted for a 28.18% diagnostic share in 2025, serving as the noninvasive gatekeeper that triggers most specialist referrals. Magnetic resonance angiography remains a preferred surveillance tool for patients monitored over time when radiation exposure is a concern, especially where MRI availability is strong. Digital subtraction angiography with biplane systems provides the highest spatial resolution and is the intra-procedural reference standard for planning and navigation. The fastest-growing modality is 3D rotational angiography, supported by a 11.88% CAGR as operators verify stent apposition and coil compaction while reducing contrast administration. High-resolution vessel wall MRI is emerging as a tool to identify inflammatory signatures suggestive of elevated rupture risk in small aneurysms, which could refine thresholds for intervention. AI-enhanced detection inside PACS platforms improves sensitivity, which can elevate surveillance cohorts and spur earlier specialist consults in the intracranial aneurysm market.

Reimbursement for neuroimaging follows established codes for CTA and MRA, while advanced techniques like vessel wall MRI often require prior authorization and are selectively reimbursed. Academic centers with research funding tend to pioneer adoption of novel imaging sequences and AI applications before community practices follow. Vendors are integrating preoperative CTA with intraoperative fluoroscopy to reduce contrast and procedure time, which adds workflow value for high-volume centers. Imaging upgrades and software packages now play a direct role in procedural efficiency, influencing site-of-service economics and quality metrics. As diagnostic accuracy improves, more patients can transition from evaluation to treatment in a single session, which tightens care pathways. The intracranial aneurysm market responds favorably to this convergence of diagnosis and treatment, as resource use becomes more predictable and patient throughput increases.

By End-User:

Ambulatory Surgical Centers Exploit Outpatient EconomicsHospitals held 54.94% of revenue in 2025 because ruptured aneurysm care requires intensive monitoring and multidisciplinary resources available continuously. Ambulatory surgical centers are the fastest-growing site at a 12.52% CAGR due to favorable case selection and same-day discharge pathways for low-risk unruptured aneurysms. Coverage determinations that expanded ASC-eligible neuro-endovascular procedures support the migration of suitable cases, particularly in states with mature outpatient infrastructure. ASC operating models can reduce overhead compared with inpatient facilities, which aligns incentives with payers looking for lower total episode costs. Specialty neurosurgical centers continue to concentrate complex referrals that drive investigational use of new devices and accrual into registries. The intracranial aneurysm market benefits from expanded site-of-service choice as patients and payers balance convenience, cost, and clinical complexity.

State-level variation in scope and credentialing shapes which procedures ASCs can perform and which devices are allowed in outpatient settings. Hospitals argue that outpatient growth can siphon profitable elective cases, leaving higher acuity cases that strain inpatient budgets. Payers increasingly support outpatient pathways when safety is demonstrated, which drives investment by ASC operators in imaging and staffing that can meet neuro-interventional standards. Academic centers play a dual role by continuing to handle complex cases while serving as early adopters for device trials that inform guidelines. Over time, protocols and stakeholder alignment determine the pace at which outpatient programs capture volumes beyond coiling-only cases. The intracranial aneurysm market size for ambulatory surgical centers is projected to grow at a 12.52% CAGR as payers and providers scale proven outpatient pathways.

Geography Analysis

North America Intracranial Aneurysm Market

North America represented 43.14% of revenue in 2025, with growth normalizing to the 7-8% range as detection and treatment penetration reach mature levels. The region’s structure relies on a large base of accredited comprehensive stroke centers that maintain 24/7 neuro-interventional capabilities and robust quality management. Canada centralizes neuro-intervention in provincial hubs, which sustains expertise while increasing wait times for non-urgent cases compared with private U.S. centers. Innovation cycles in microcatheters, surface-engineered flow diverters, and imaging software differentiate vendors and shape purchasing committees in a market where reimbursement already supports advanced devices. Payers rely on DRG frameworks and negotiated rates that reward efficiency and low complications, so centers focus on reducing fluoroscopy exposure, shortening time to hemostasis, and optimizing discharge. The intracranial aneurysm market remains competitive in North America as vendors seek clinical and economic advantages that sway hospital value analysis committees.

Europe Intracranial Aneurysm Market

Europe shows country-level variability around similar clinical care standards, with reimbursement and assessment bodies determining access to advanced implants such as flow diverters. Social insurance systems in markets like Germany often bundle device costs in case rates, while centralized HTA processes in others constrain indications or restrict coverage to larger aneurysms. Strong registry cultures in parts of Europe generate comparative outcomes evidence that influences practice and supports protocol standardization. Under the MDR framework, device makers maintain traceable quality systems and generate more extensive clinical evidence in post-market surveillance, which favors firms with established regulatory infrastructure. Academic centers across the region enroll heavily in pivotal neurovascular device trials, improving speed of evidence generation for new indications. The intracranial aneurysm market in Europe remains stable and evidence-led, with adoption gated by value assessments and clinical data production cycles.

APAC Intracranial Aneurysm Market

Asia-Pacific is the fastest-growing region at an 11.19% CAGR through 2031 as governments and private systems expand imaging access and designate stroke centers in more cities. China’s policies prioritize stroke-center expansion and interventional training, contributing to higher volumes in tier-two urban markets and gradual diffusion into surrounding regions. Japan’s established interventional ecosystem achieves high treatment rates, and its regulatory system maintains rigorous local review processes that can delay imported devices while creating room for domestic players. India’s payer mix and uneven facility distribution create a two-speed pattern, with metropolitan private hospitals adopting the latest neurovascular devices while many secondary cities still lack angiography suites. Southeast Asian countries expand capacity with external training partnerships and medical tourism programs that attract patients from less developed neighbors. Regional regulatory frameworks range from Singapore’s close alignment with U.S. standards to China’s acceleration of domestic approvals, shaping the sequence and breadth of device introductions in the intracranial aneurysm market.

Regulatory Landscape

Intracranial aneurysm devices span multiple risk classes and routes to market, with U.S. clearance or approval commonly proceeding via FDA 510(k) for many neurointerventional devices and PMA for higher-risk implants such as certain flow diverters and intrasaccular systems. FDA special controls guidance for vascular and neurovascular embolization devices anchors expectations for performance testing, labeling, and premarket submissions under 21 CFR 807 Subpart E, while post-market evidence generation remains integral for implants that enter practice with narrower pre-approval datasets.

In Europe, the Medical Device Regulation (EU MDR 2017/745) continues to shape clinical evaluation, traceability, and post-market surveillance requirements for neurovascular implants. In 2026, the EU updated its clinical investigation exemption list through Commission Delegated Regulation (EU) 2026/1451 (adopted 20 March 2026), explicitly including endovascular embolization coils and particles among implantable and class III devices covered by the update. That change shifts documentation expectations toward more robust clinical evaluation files. Separately, the EMA breakthrough device pilot progressed through Phase 1a in 2026, with an EMA information session held on 24 April 2026 and an application deadline of 22 May 2026. Across markets, standards such as ISO 9713:2022 define technical and safety requirements for permanent self-closing intracranial aneurysm clips, supporting harmonized design controls and MRI and sterilization labeling expectations.

Value Chain Analysis

The intracranial aneurysm device value chain starts with specialized raw materials and precision components, including platinum-based alloys for coils and nitinol feedstock for braided mesh used in flow diversion. Downstream steps include microfabrication, braiding, coating or surface treatment, sterilization, and final assembly under quality systems aligned with ISO 13485 and regional requirements (e.g., EU MDR). Supplier concentration in critical inputs such as nitinol alloys can tighten availability and increase qualification demands, and periodic manufacturing or supplier changes may require regulatory notification or review. FDA-documented supplier-related updates affecting established embolization device platforms illustrate how qualification and documentation requirements can affect continuity.

Commercialization typically follows direct sales and distributor networks into hospitals, ambulatory surgical centers, and specialty neurosurgical centers. Purchasing has increasingly shifted toward centralized value analysis and longer-term contracting in many integrated delivery networks. Clinical evidence and post-approval surveillance commitments also function as a core value-chain currency, helping vendors compete on portfolio breadth (access catheters, microcatheters, coils, flow diverters, and intrasaccular devices) alongside proctoring and training capabilities that support credentialing. Logistics resilience and dual-sourcing remain important because tariffs and cost pressure on imported precision components can disrupt pricing and availability, driving qualification of near-shore options while preserving regulatory traceability and performance equivalence expectations used by hospital procurement teams.

Competitive Landscape

The top five players account for an estimated 60-65% of revenue, creating a moderately consolidated field where portfolio breadth and clinical evidence shape buying decisions. Incumbents use bundles across aneurysm therapy, stroke thrombectomy, and access tools to secure multi-year supply agreements with hospitals. Specialists differentiate on niche anatomies, ultra-low-profile delivery systems, and device visibility under fluoroscopy, which can win specific case types even when broader portfolios dominate. Manufacturing footprints commonly rely on external suppliers for platinum wire and sterilization, which makes supply chain reliability and dual sourcing important to avoid back orders. Sales scale and proctoring networks are essential to reach hospital device committees and support credentialing, which often determines the pace of product uptake. The intracranial aneurysm market remains receptive to evidence that shows shorter procedure times, fewer devices per case, and lower complication rates because these translate to sustained hospital value.

Recent strategic moves underscore the importance of scaling flow-diverter portfolios and imaging integrations. Investments in European manufacturing and MDR readiness support supply resilience and export plans into the Middle East and Africa. Portfolio updates in microcatheters and large-volume coils target distal anatomy and giant aneurysms where prior device stacks were long and expensive. Broad commitments to integrate procedural planning software into angiography systems help reduce contrast and fluoroscopy time, which matters for radiation exposure limits and throughput. Select partnerships aim to tailor flow-diverter design to regional vascular anatomy, especially in Asia where vessel diameters and bifurcations differ from Western datasets. The intracranial aneurysm market rewards firms that can pair device innovation with field training, peer-reviewed publications, and KOL engagement to shorten the time from approval to guideline alignment.

Clinical evidence pipelines drive competitive positioning as registries and case series compare occlusion rates, retreatment, and delayed ischemic events across device classes. Devices that reduce dual antiplatelet therapy duration without raising thromboembolic risk address a key need for patients who cannot tolerate current pharmacology. Robotic and AI-assisted platforms are piloted for complex anatomies and to standardize steps across operators, which can appeal to ASC programs focused on predictable, shorter cases. Companies that navigate post-market surveillance and coding changes effectively can gain early advantage in reimbursement environments where new technologies often share existing procedure codes. As comprehensive stroke center density rises in fast-growing regions, sales teams that support outreach and referral patterns can accelerate case volumes. The intracranial aneurysm market continues to balance engineering differentiation with the practical realities of credentialing and reimbursement that govern device choice at the site of care.

Intracranial Aneurysm Industry Leaders

Stryker

B. Braun Melsungen AG

Medtronic

Terumo Corporation

MicroPort Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Intracranial Aneurysm Market Companies Covered in this Report

- Acandis

- ASAHI INTECC

- B. Braun (Aesculap)

- Balt

- Cerus Endovascular

- Evasc Neurovascular

- GE HealthCare (angiography/CT)

- Integra LifeSciences (Codman Specialty Surgical)

- Johnson & Johnson (CERENOVUS)

- Kaneka

- Medtronic

- MicroPort

- Penumbra

- Perflow Medical

- Philips (angiography/CT/MR)

- Rapid Medical

- Route 92 Medical

- Siemens Healthineers (angiography/CT/MR)

- Stryker

- Terumo (MicroVention)

- United Imaging (CT/MR/angiography)

- Wallaby Medical

Market Opportunities and Future Outlook

White space is most visible in wide-neck and complex anatomies, where single-device strategies can reduce procedure steps, adjunctive implants, and workflow variability. Existing regulatory and evidence activity provides concrete support for this opportunity: Stryker secured an FDA-approved line extension for the Surpass Elite Flow Diverter System in February 2025 by adding intermediate diameters (3.75 mm, 4.25 mm, and 4.75 mm), and in June 2025 initiated the GUARD trial (NCT06872684) to evaluate Surpass Elite with the Guardian Flow Diverter System. Phenox also initiated recruitment in March 2026 for NCT07143019 evaluating its p48/p64 MW HPC Flow Modulation Device in wide-neck intracranial aneurysms, indicating sustained clinical investment around next-generation flow diversion design and coatings.

A second opportunity centers on durability and long-term safety proof, especially for intrasaccular flow disruption and flow diversion, where payers and hospital committees increasingly seek registries and post-approval endpoints. MicroVention received FDA approval in March 2026 for a revised post-market surveillance protocol for the WEB System (PMA P170032/S019), highlighting how manufacturers are formalizing longer-term datasets to support broader confidence and contracting. At the same time, published comparative clinical findings in 2026 noting that flow diversion did not demonstrate superiority over standard coiling (with or without stents) for certain small unruptured ophthalmic aneurysm subsets reinforce the need for better patient selection tools, imaging-based stratification, and indication-specific evidence that clarifies where advanced implants deliver measurable benefit.

Recent Industry Developments in Intracranial Aneurysm Market

- June 2026: Medtronic completed its acquisition of Scientia Vascular for USD 550 million, adding dedicated neurovascular access products to its portfolio. The combination strengthens end-to-end procedure support where distal navigation and stable access are critical. It also increases bundling leverage in hospital contracting for aneurysm and adjacent neurovascular interventions.

- July 2025: Stryker initiated the commercial launch of the Surpass Elite Flow Diverter in the United States, Europe, and South Korea. The multi-region rollout broadened availability of a newer-generation flow diversion platform. It supported competitive positioning as centers expand single-device strategies for complex aneurysm anatomies.

- July 2024: Micro Therapeutics, Inc. (ev3 Neurovascular) received FDA approval for updates to the braid dipping inspection and sampling plan for the Pipeline Flex and Pipeline Vantage Embolization Devices (PMA P100018/S046). The change points to ongoing manufacturing and quality-control refinement for braided flow diversion systems. It can affect supply continuity and consistency at high-volume centers.

Intracranial Aneurysm Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenues earned from diagnosing and treating intracranial (brain) aneurysms, including the key endovascular and surgical approaches used in routine clinical practice, and the related consumable devices used during these procedures.

Scope exclusions: We exclude basic neuroimaging equipment sales (for example, CT, MRI, and angiography suites), general neurosurgical tools that are not specific to aneurysm care, and downstream rehabilitation services.

Segments Covered in This Report

- By Treatment Type

- Endovascular Coiling

- Stent-Assisted Coiling

- Balloon-Assisted Coiling

- Flow Diverter Stents

- Intrasaccular Flow Disruptors (e.g., WEB, Contour)

- Microsurgical Clipping

- By Diagnosis

- Computed Tomography Angiography (CTA)

- Magnetic Resonance Angiography (MRA)

- Digital Subtraction Angiography (DSA; incl. biplane, 3DRA)

- 3D Rotational Angiography / 4D CTA

- High-Resolution Vessel Wall MRI

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty Neurosurgical Centers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and commercial boundaries before any modeling was done. We reviewed public health and epidemiology references on aneurysm prevalence and rupture risk, along with procedure and utilization signals that indicate where demand is actually generated in hospitals.

We also checked official and public sources, such as the Centers for Disease Control and Prevention for stroke related context, the World Health Organization for mortality and health system indicators, the National Institutes of Health and PubMed indexed journals for treatment patterns, and US FDA public databases for device clearances and safety updates. In parallel, we used company filings, investor presentations, reputable medical society websites, and press releases to understand product launches and pricing direction. Where needed, approved paid subscriptions were used to standardize company financials, track patents, and confirm cross border shipment signals for relevant device categories. This list is not exhaustive, and many other sources were reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on validating how diagnosis pathways convert into treated cases and what devices are being used by procedure type. We spoke with clinicians involved in neurointervention and neurosurgery, procurement and cath lab administrators, and distribution side participants to confirm utilization, replacement cycles, and typical pricing corridors.

Because treatment access and adoption vary by geography, we also checked inputs across the Americas, EMEA, and APAC so regional growth assumptions could be tested against real world capacity, referral patterns, and reimbursement direction.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 46% |

| Mid tier: 57% | Functional/Unit leaders: 36% | EMEA: 33% |

| Smaller Players: 17% | Managers: 52% | Americas: 21% |

Market-Sizing & Forecasting

The sizing starts from a top-down build where treated case pools are reconstructed by region using aneurysm detection rates, rupture incidence, hospital access, and the share of cases routed to endovascular versus surgical care. Those demand pools are then translated into revenue using procedure mix (coiling, flow diversion, intrasaccular approaches, and clipping) and typical device use per case, which is then adjusted for replacement and adjunct device attach rates.

To keep the totals grounded, we corroborate results with selective bottom-up checks, such as rolling up a sample of supplier revenues by product category, cross checking distributor feedback on unit movements, and using sampled ASP times implied volumes where pricing ranges were available. Key model inputs we track include procedure volumes, adoption curves for flow diversion versus coiling, payer coverage and reimbursement stability, clinician preference shifts by aneurysm location, and the pace of new device approvals that can expand indications.

For forecasting, scenario analysis is used so growth can flex with changes in treated penetration, capacity constraints in neurointervention centers, and expected pricing movement. Assumptions are finalized only after expert feedback is aligned by region, and any missing bottom-up points are handled through conservative ranges that are later tightened during validation rounds.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, including procedure trend direction, reported adoption of newer techniques, and the consistency of implied pricing against interview feedback. When a country or region shows a sharp change, the drivers are reviewed, the input series is rechecked, and follow-up calls are triggered if the variance cannot be explained by policy, access, or product cycle changes.

Every release goes through multi-step analyst review, including a final pass to confirm that the market boundary, unit logic, and currency conversions are applied consistently. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, guideline shifts, or step changes in utilization.

Mordor Intelligence's Intracranial Aneurysm Market Size Versus Other Published Estimates

Published market sizes for intracranial aneurysm can look far apart because the scope line is drawn differently, and the demand base is built with different clinical conversion assumptions. Differences also come from whether revenues are counted only for procedure specific consumables, or if broader neurovascular device baskets and diagnostic spend are added in.

By tracking procedure mix and pricing progression, and then rechecking scope boundaries annually, Mordor Intelligence keeps the estimate tied to treated aneurysm demand rather than mixing in adjacent stroke or general imaging revenues, which changes the starting value and the pace of growth.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.76 B (2026) | |

| Regional Consultancy A | USD 1.51 B (2024) | Uses an earlier base year and appears to emphasize a narrower treatment and end user lens, which can undercount regions where endovascular adoption is growing and where procedure volumes are expanding quickly. |

| Trade Journal B | USD 1.41 B (2024) | Relies on broad segment labels and headline growth rates, with limited clarity on how treated case conversion, procedure mix, and adjunct device usage per case are built into the revenue model. |

The spread in values is mainly explained by base year choice and what is counted inside the revenue basket. When treated penetration, procedure mix, and device use per case are made explicit, the result becomes easier to reproduce and to update when clinical practice shifts.

Key Questions Answered in the Report

What is the intracranial aneurysm market outlook through 2031?

The intracranial aneurysm market size is USD 2.76 billion in 2026, and it is projected to reach USD 4.44 billion by 2031 at a 9.98% CAGR.

Which therapies are driving growth in the intracranial aneurysm market?

Flow diverters and intrasaccular devices are expanding at the expense of bare platinum coiling, with flow diverters advancing at a 12.34% CAGR on single-device efficiency in wide-necked and large aneurysms.

How is site-of-service mix changing in the intracranial aneurysm market?

Hospitals still dominate emergent cases with 54.94% share in 2025, but ambulatory surgical centers are growing at a 12.52% CAGR as outpatient pathways expand for selected unruptured aneurysms.

Which regions lead and which grow fastest in the intracranial aneurysm market?

North America held 43.14% of revenue in 2025, while Asia-Pacific is the fastest-growing region with an 11.19% CAGR through 2031 on improving imaging access and stroke-center density.

What are the key cost and workforce barriers to adoption?

High device and total procedure costs with uneven reimbursement and a shortage of dual-trained endovascular neurosurgeons in emerging markets remain the main constraints on faster access and utilization.

Which diagnostics are most influential in care pathways?

CTA served as the gatekeeper with a 28.18% share in 2025, while 3D rotational angiography is growing at a 11.88% CAGR as it supports intra-procedural decisions and reduces contrast usage.

Page last updated on: