Talent Management In IT And Telecom Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 6.98 Billion |

| Growth Rate (2026 - 2031) | 13.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Management In IT And Telecom Market Analysis by Mordor Intelligence

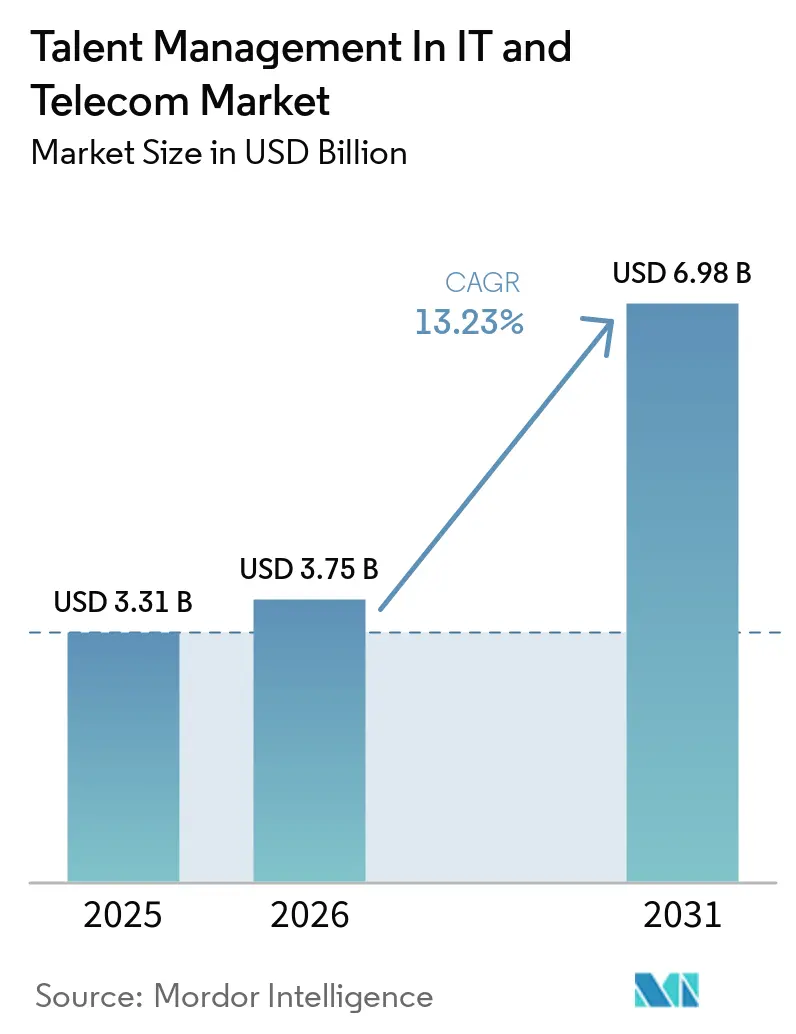

The talent management in IT and telecom market size was valued at USD 3.31 billion in 2025 and estimated to grow from USD 3.75 billion in 2026 to reach USD 6.98 billion by 2031, at a CAGR of 13.23% during the forecast period (2026-2031). Demand for purpose-built talent platforms is rising as IT service firms and telecom operators manage cloud-led workforce restructuring, wider AI use in HR workflows, and employee populations spread across time zones. This shift has moved HR beyond an administrative role, because workforce decisions now affect software delivery schedules, internal mobility, and network rollout speed. Software remained the revenue anchor in 2025, which shows that buyers still prefer broad platforms that combine recruiting, analytics, skills management, and compliance in one system. Cloud deployment, SME adoption, and stronger spending on learning and development show that buyers are moving toward scalable SaaS tools and faster workforce reskilling rather than isolated HR modules. Competition remains layered between full-suite vendors and specialist providers, while legacy integration issues and data-sovereignty rules continue to slow adoption in selected regions.

Key Report Takeaways

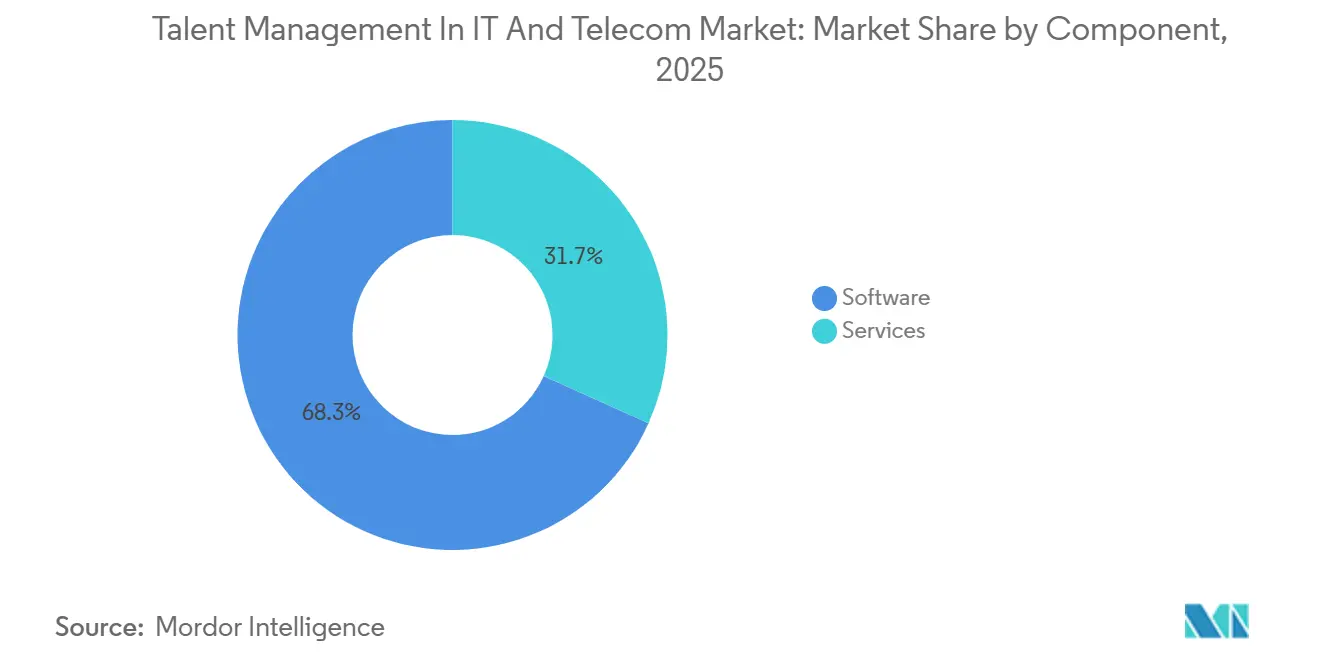

- By component, software held 68.26% revenue share in 2025 in the talent management in IT and telecom market, while services are projected to expand at 14.36% CAGR through 2031.

- By deployment mode, cloud accounted for 74.24% share in 2025 and is also the fastest-growing deployment model at 14.21% CAGR through 2031.

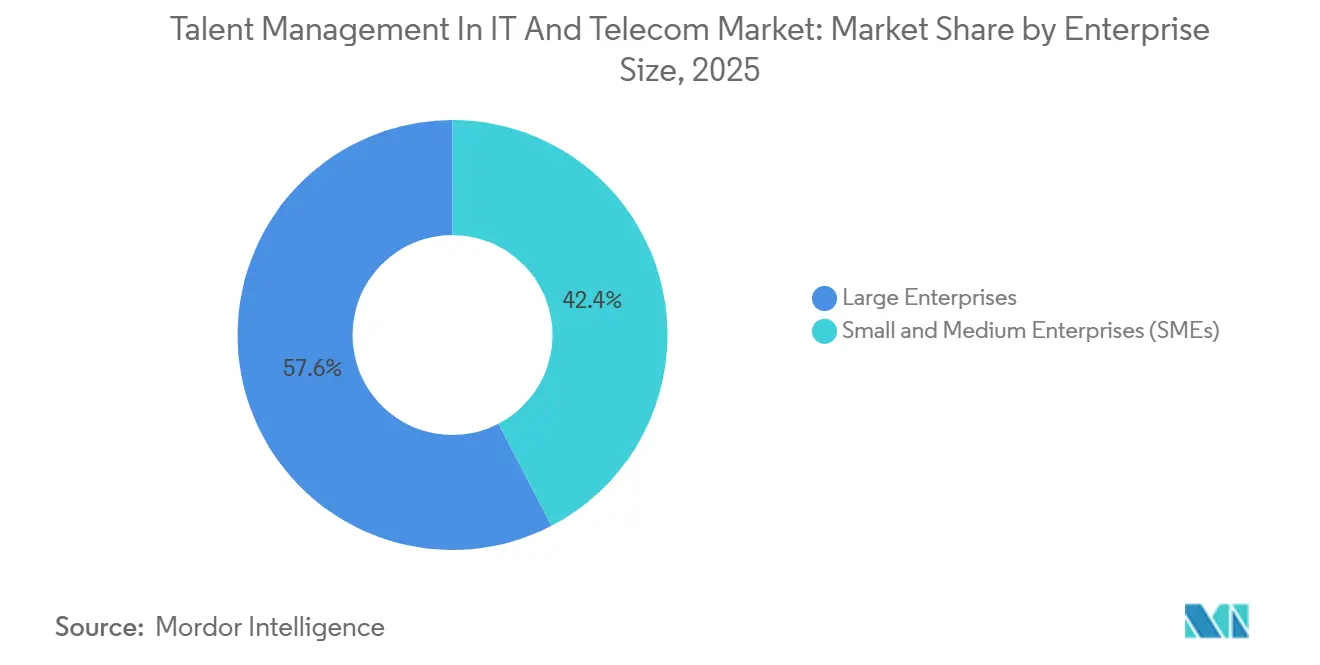

- By enterprise size, large enterprises represented 57.62% of revenue in 2025, while SMEs are forecast to record the highest CAGR at 15.46% through 2031.

- By application, recruitment and talent acquisition captured 29.31% share in 2025, while learning and development is projected to grow at 16.62% CAGR through 2031.

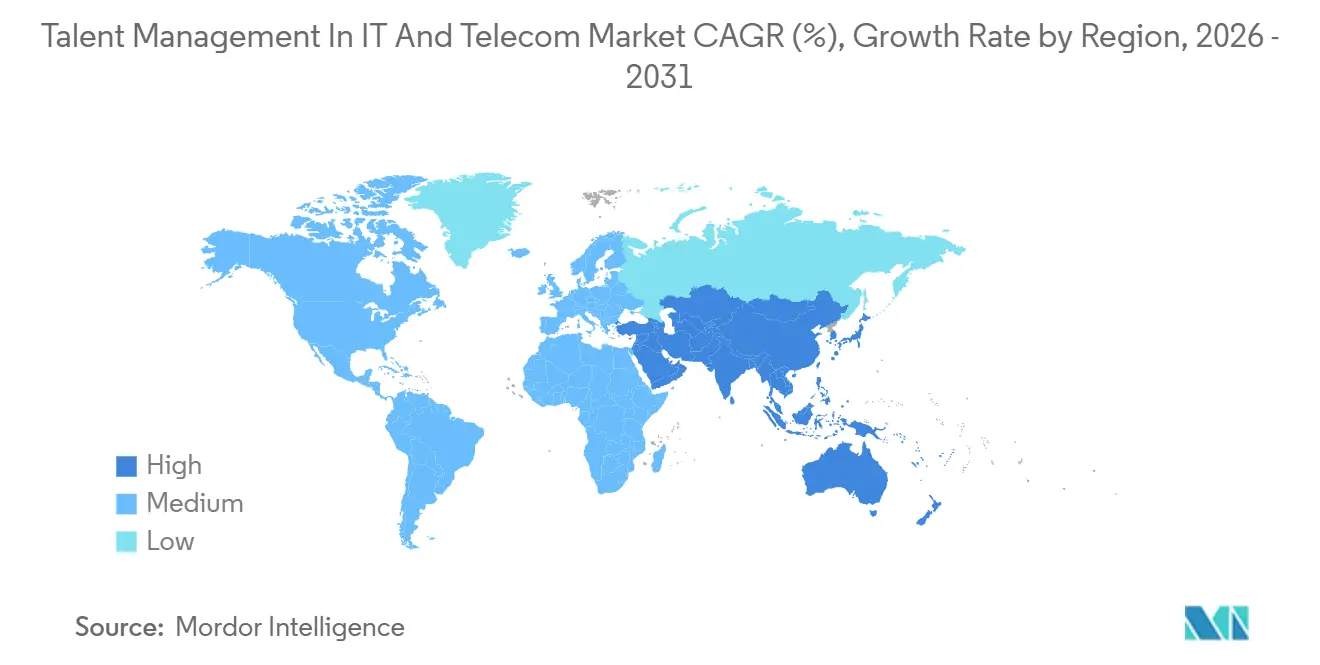

- By geography, North America led with 42.36% share in 2025, while the Asia-Pacific is forecast to advance at 14.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Talent Management In IT And Telecom Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Adoption of AI-Powered Recruiter Bots | +2.8% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Cloud Migration Boosting SaaS Talent Suites | +2.5% | Global, particularly North America, Western Europe, and Australia | Short term (≤ 2 years) |

| Remote and Hybrid Work Scaling Digital Performance Management | +1.8% | Global, with strongest impact in North America and Asia-Pacific core | Medium term (2-4 years) |

| Unified HR Data Security and Compliance Controls | +1.5% | North America, EU, and Asia-Pacific, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Skills Taxonomies Tied to 5G and Network Virtualization | +1.2% | Global, with highest urgency in India, Southeast Asia, and Europe | Medium term (2-4 years) |

| Internal Talent Marketplaces in Tier-2 Asian Tech Hubs | +0.9% | Asia-Pacific core, including India, Vietnam, Indonesia, Philippines, and Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption Of AI-Powered Recruiter Bots For Tech Roles

Autonomous recruiting is becoming a defining operating model in the talent management in IT and telecom market, because employers need to screen technical talent faster and with less recruiter effort. Product launches from Oracle and Eightfold AI show that vendors now position agentic interviewing and automated hiring actions as core functions rather than optional add-ons.[1]Eightfold AI, “TalentForge and AI Interviewing Announcements,” Eightfold AI, eightfold.ai In telecom hiring, this matters most for field engineering, cloud, and cybersecurity roles, where delays can slow service delivery and infrastructure programs. In the talent management in IT and telecom market, the advantage is shifting toward platforms that connect sourcing, interviewing, and skills data with the wider workforce stack. Vendors that still rely on disconnected recruiter tools face a higher risk of being bypassed as autonomous agents take over larger parts of the hiring flow.

Cloud Migration Wave Boosting SaaS Talent Suites

Cloud migration is strengthening talent management in the IT and telecom markets because buyers want a single workforce system that can keep pace with changing headcounts and project mixes. SAP's SuccessFactors 1H 2026 release added bi-directional, zero-copy data sharing with AWS and linked planning across SAP Cloud ERP, SAP Fieldglass, and SAP SuccessFactors, reflecting this push toward a connected cloud architecture. Workday's spring 2026 release also introduced Workday Data Lake using open standards for bi-directional access with platforms such as Databricks, Google Cloud, and Snowflake. These moves matter in IT and telecom, because workforce, finance, and delivery planning need to stay aligned when hiring or redeployment changes quickly. That makes cloud architecture not just a hosting choice but also a retention and operating lever within talent management in the IT and telecom markets.

Remote and Hybrid Work Models Scaling Digital Performance Management

Flexible work has become a structural condition in talent management in the IT and telecom market because engineering teams now operate across locations, shifts, and time zones. SHRM found that organizations offering flexible work arrangements reported a 22% recruitment difficulty rate, compared with 29% for those without such arrangements. This widens the need for performance tools that can capture continuous feedback, track output across asynchronous teams, and surface risks earlier. Workday made its Employee Sentiment Agent generally available in 2026, which shows how vendors are turning constant employee signals into manager-ready actions. In France, higher pay for cloud- and cybersecurity-certified network engineers adds another reason for employers to use structured performance systems to differentiate and retain scarce talent.

Compliance-Driven Demand For Unified HR Data Security Controls

Compliance pressure is elevating talent management in the IT and telecom markets because fragmented employee data now creates direct legal and operational exposure across jurisdictions. The UK Information Commissioner's Office reported nearly 43,000 personal data complaints in 2024-25, up from under 40,000 a year earlier. For employers using AI in recruitment or workforce decisions, the EU AI Act, GDPR, Saudi data rules, and UAE residency requirements are pushing tighter data-processing agreements, impact assessments, retention rules, and audit trails. Platforms with ISO/IEC 42001:2023, SOC 2 Type II, GDPR, or FedRAMP credentials are therefore gaining procurement preference, as seen in Eightfold AI's positioning with enterprise buyers. That preference increases switching costs and extends contract life, making compliance a growth lever as well as a control function in talent management in the IT and telecom markets.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Integration Complexity With Legacy HRIS Stacks | -2.0% | Global, most acute in large enterprise IT and telecom environments with long system histories | Short term (≤ 2 years) |

| High Subscription Cost of Analytics-Rich Platforms | -1.5% | Emerging markets across Asia-Pacific, South America, and Middle East and Africa, and the SME segment globally | Medium term (2-4 years) |

| Talent Data Sovereignty Rules in Middle East and Africa | -1.0% | Middle East, especially Saudi Arabia and UAE, and parts of Africa, with spillover to Turkey | Long term (≥ 4 years) |

| Algorithmic Bias Concerns Slowing AI Recruitment Tools | -0.8% | North America and Europe, with rising global attention | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy HRIS Stacks

Integration complexity remains the clearest near-term brake on the talent management in IT and telecom market, especially for large operators with multi-country HR estates. Many telecom groups still run a mix of PeopleSoft, SAP HCM on-premises, and custom payroll engines built through years of mergers, which makes field mapping and workflow harmonization difficult. The problem is not only technical, because each integration project also forces agreement on job architecture, compensation fields, and local compliance rules. When data stays split across payroll, performance, and headcount systems, workforce analytics arrive too late to guide live staffing decisions. Vendors are responding with more open data layers and prebuilt connectors, but the talent management in IT and telecom market still sees longer time-to-value where legacy stacks dominate.

High Subscription Cost Of Analytics-Rich Platforms

High subscription cost is holding back talent management in IT and telecom markets among smaller firms and buyers in more price-sensitive regions. Microsoft Dynamics 365 Human Resources lists at USD 135 per user per month for full capabilities, which shows how quickly analytics-rich HR software can move beyond SME budgets.[2]Microsoft, “Dynamics 365 Human Resources Pricing,” Microsoft, microsoft.com When smaller companies stay on spreadsheets or basic tools, they also create the messy data that makes later analytics adoption harder. Workday's Flex Credits, launched in September 2025, signaled a move toward incremental AI consumption instead of large upfront license commitments. That pricing shift should ease adoption over time, but the talent management in IT and telecom market still faces a slower conversion path in Southeast Asia, South America, and parts of the Middle East and Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Revenue While Services Expand With Deployment Complexity

Software accounted for 68.26% of the talent management market in the IT and telecom market in 2025, keeping the platform layer at the center of buyer spending. That lead persisted because employers wanted to bring recruiting, analytics, compliance, and workflow automation under one commercial relationship rather than across separate tools. In the talent management market for IT and telecom, software also benefits from SaaS delivery, as vendors can release new AI capabilities without customer-side hardware changes. That keeps software central to talent management in the IT and telecom markets, especially in large accounts where standardization matters as much as feature depth.

Services are projected to grow at a 14.36% CAGR from 2026 to 2031, as implementation, change management, and support work become harder in AI-led HR environments. The need for services is rising because every new skills framework or internal mobility layer has to be configured around local processes and legacy data. Regular release cycles add to this demand, with vendors like Cornerstone and Workday continuing to ship frequent updates that can affect custom workflows. That means talent management in the IT and telecom markets continues to create recurring work for integration specialists and managed service partners.

By Deployment Mode: Cloud Scale Continues To Reset Platform Economics

Cloud held 74.24% share of the talent management in IT and telecom market size in 2025 and is projected to grow at 14.21% CAGR through 2031. In the talent management in IT and telecom market, cloud remains the preferred model because distributed engineering teams need live data access across regions and functions. Cloud deployment also supports faster AI rollout, easier compliance updates, and lower friction when companies add new business units or contractors. SAP and Workday both expanded cloud data-sharing and planning capabilities in 2026, which supports this shift toward connected workforce architectures.

On-premises systems still matter where workforce data must stay inside national boundaries or within tightly controlled operator environments. That is why cloud adoption does not fully displace local hosting in Gulf markets governed by in-country data rules. Even so, the direction of spend in the talent management in IT and telecom market continues to favor cloud platforms that can combine planning, hiring, and skills data in one environment. Vendors that can support regional hosting without losing analytical depth are likely to hold the strongest position over the next cycle.

By Enterprise Size: Large Accounts Dominate Today While SMEs Form The Growth Frontier

Large enterprises held 57.62% of the talent management in IT and telecom market share in 2025, supported by the buying power of global IT services firms and network operators. These buyers often need several modules at once, which makes broad HCM suites easier to justify than stand-alone tools. In the talent management in IT and telecom market, large contracts also favor vendors that can meet multi-country governance, payroll, and workforce planning needs in one program. This keeps the top enterprise accounts closely tied to vendors with mature partner ecosystems and strong implementation depth.

SMEs are forecast to expand at 15.46% CAGR from 2026 to 2031, which makes them the clearest growth frontier for the talent management in IT and telecom market. Lower-entry SaaS delivery and consumption-based pricing are reducing the barrier that once kept advanced talent systems out of smaller firms, with UKG and Workday both moving toward more flexible consumption models.[3]UKG, “Talent Marketplace and Flexible Workforce Updates,” UKG, ukg.com Viettel's Digital Talent Program drew more than 12,000 applications for its 2025-2026 cohort across 8 strategic technology areas, which shows why mid-tier operators need structured digital tracking and development tools. For these customers, fast onboarding and templates matter more than long feature lists, because smaller HR teams cannot absorb year-long deployment cycles.

By Application: Hiring Stays Largest While Learning Gains The Strongest Momentum

Recruitment and talent acquisition accounted for 29.31% of the talent management in IT and telecom market size in 2025, which kept hiring workflows as the largest application area. That position reflects the continued shortage of cloud, AI, network, and cybersecurity skills across the talent management in IT and telecom market. Employers still need better sourcing, faster screening, and clearer candidate matching, especially when project timelines depend on quick staffing. Agentic recruiting tools from Oracle, Eightfold, and iCIMS show how automation is moving deeper into frontline and technical hiring flows.

Learning and development is projected to grow at 16.62% CAGR from 2026 to 2031, which makes it the fastest-rising application in the talent management in IT and telecom market. 5G deployment, network virtualization, and AI adoption are forcing employers to reskill existing staff faster than external hiring pipelines can supply them. Ericsson and the Telecom Sector Skill Council expanded this pattern in India by targeting 10,000 ITI students across 100 institutes for 5G deployment training. That need will keep learning central to the talent management in IT and telecom market, while succession, engagement, and career tools also gain relevance as vendors use AI to reduce the administrative load that once limited adoption.

Geography Analysis

North America captured 42.36% of the talent management in IT and telecom market share in 2025, which kept the region in the lead. The region benefits from the concentration of hyperscalers, a mature HR-tech ecosystem, and faster enterprise adoption of AI-enabled workforce tools. In the United States, California's AI hiring rules and Illinois civil rights liability for discriminatory AI use in employment are pushing buyers toward auditable and governance-ready platforms.[4]California Civil Rights Department, “Automated Decision Systems and Employment Rules,” California Civil Rights Department, calcivilrights.ca.gov Workday's position with more than 65% of the Fortune 500 also gives North American buyers early access to scaled platform rollouts and ecosystem support. That combination keeps the talent management in IT and telecom market strongest in North America for both large-enterprise demand and compliance-led product development.

Europe remains a major revenue center in the talent management in IT and telecom market, supported by strict data governance and a large telecom and IT services base. GDPR has encouraged buyers to consolidate fragmented HR data into auditable platforms instead of managing scattered tools across countries. Deutsche Telekom's growth hub, which serves 200,000 employees and won a national HR Tech award, shows that internal mobility and skills platforms have moved beyond pilot status in the region. The EU AI Act compliance deadline in August 2026 is now accelerating procurement toward systems with clearer governance, documentation, and AI management standards.

Asia-Pacific is forecast to grow at 14.95% CAGR from 2026 to 2031, making it the fastest-growing regional block in the talent management in IT and telecom market. Growth comes from expanding digital infrastructure, younger labor pools, and the rise of Tier-2 tech hubs in India, Vietnam, Indonesia, and the Philippines that need more formal talent processes. India's Telecom Sector Skill Council is targeting placement of 150,000 trained telecom workers annually, while Ericsson's training partnership spans 100 institutes, which shows the scale of workforce development now underway. South America remains more price sensitive, which limits adoption of analytics-rich suites among smaller IT employers, while Gulf markets are investing in sovereign-compliant platforms to meet national employment mandates and local data rules. This leaves the talent management in IT and telecom market with fast structural upside in Asia-Pacific, selective compliance-led demand in the Middle East and Africa, and a more measured adoption curve in South America.

Competitive Landscape

The talent management in IT and telecom market remains moderately consolidated at the suite level, but it is still fragmented across recruiting, learning, and skills applications. SAP, Oracle, and Workday continue to hold the upper tier because they bundle payroll, planning, talent acquisition, and governance into one HCM environment. SAP's acquisition of SmartRecruiters in October 2025 tightened that end-to-end position by linking candidate sourcing and onboarding more closely with SuccessFactors.[5]SAP, “SmartRecruiters Acquisition and Autonomous HCM Announcements,” SAP, sap.com Workday strengthened its own stack through its agreement to acquire Sana and through the broader rollout of Illuminate AI capabilities in 2025 and 2026. That keeps the talent management in IT and telecom market tilted toward vendors that can connect HR data to broader business systems rather than only automate one workflow.

Specialist vendors still have room to grow in the talent management in IT and telecom market, especially in fast-moving hiring and skills use cases. Eightfold AI, iCIMS, and Cornerstone are expanding by focusing on agentic interviewing, talent marketplaces, and skills intelligence that reduce manual recruiter and manager workload. Cornerstone Workforce AI, launched in May 2026, added a data layer built on 45 million users and more than 55,000 skills, which strengthens its role in workforce readiness. Eightfold TalentForge, released in May 2026, pushed the category toward custom HR software built on top of a talent intelligence base rather than only fixed modules. This means competition now depends as much on data structure and deployment flexibility as on feature breadth.

Technology leadership in the talent management in IT and telecom market is now centered on agentic AI, where vendors try to move from recommendations to autonomous multi-step actions. Oracle's April 2026 launch of 8 Fusion Agentic Applications for HR and SAP's autonomous HCM push both show how quickly this shift is moving into mainstream enterprise suites. The real white space remains telecom-specific workforce analytics, network-skills forecasting, and vendor-neutral internal talent marketplaces for mid-tier operators. The competitive set is therefore defined more by vendors with dedicated talent products and telecom-ready implementation depth than by telecom software suppliers that lack a distinct talent platform.

Talent Management In IT And Telecom Industry Leaders

SAP SE

Oracle Corporation

Workday, Inc.

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP announced a new era of Autonomous HCM at SAP Sapphire 2026, deploying Joule AI assistants across recruiting, payroll, HR service delivery, and workforce planning within the SuccessFactors suite, embedding agentic AI that coordinates multiple agents end-to-end without manual HR workflow triggers.

- May 2026: Eightfold AI announced the general availability of TalentForge, enabling enterprises to build fully custom HR software on top of its talent intelligence foundation, alongside next-generation AI Interviewing and Workforce Readiness capabilities.

- April 2026: Oracle launched 8 Fusion Agentic Applications for HR at the Oracle AI World Tour in New York, including Career Advancement Command Center, Hiring Workspace, and Workforce Operations Command Center, all built on the new Oracle AI Agent Studio, enabling no-code agentic automation.

- September 2025: Oracle announced new AI agents for Oracle Fusion Cloud HCM, including Job Discovery Agent, Interview Management Agent, and Succession Planning Advisor Agent, prebuilt with advanced security and running on Oracle Cloud Infrastructure at no additional cost.

Global Talent Management In IT And Telecom Market Report Scope

Talent management in the IT and telecom sectors refers to the strategic approach of attracting, recruiting, developing, and retaining highly skilled technology professionals. In industries characterized by rapid advancements such as cloud computing, AI, and 5G deployment, it plays a critical role in ensuring organizations maintain a competent and adaptable workforce to drive innovation and sustain growth.

The Talent Management in IT and Telecom Market is Segmented by Component (Software, and Services), Deployment Mode ( On-premises, and Cloud), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Performance Management, Learning and Development, Succession Planning, Compensation Management, Recruitment and Talent Acquisition, Workforce Planning, Employee Engagement and Career Development, Other Talent Management Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Professional Services |

| Support and Maintenance Services |

| On-premises |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Performance Management |

| Learning and Development |

| Succession Planning |

| Compensation Management |

| Recruitment and Talent Acquisition |

| Workforce Planning |

| Employee Engagement and Career Development |

| Other Talent Management Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Software | ||

| Services | Professional Services | ||

| Support and Maintenance Services | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| By End-Use Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Application | Performance Management | ||

| Learning and Development | |||

| Succession Planning | |||

| Compensation Management | |||

| Recruitment and Talent Acquisition | |||

| Workforce Planning | |||

| Employee Engagement and Career Development | |||

| Other Talent Management Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the talent management in IT and telecom market?

The talent management in IT and telecom market was valued at USD 3.31 billion in 2025, reached USD 3.75 billion in 2026, and is forecast to reach USD 6.98 billion by 2031 at a 13.23% CAGR.

Which deployment model leads spending in this space?

Cloud leads spending, with a 74.24% share in 2025, and it is also the fastest-growing deployment model at a 14.21% CAGR through 2031.

Why is learning and development growing so quickly for IT and telecom employers?

Learning and development is projected to grow at 16.62% CAGR because 5G, network virtualization, and AI adoption are pushing employers to reskill existing staff faster than external hiring can keep up.

Which buyer group offers the strongest growth opportunity?

SMEs are the fastest-growing buyer group, with a 15.46% CAGR through 2031, as SaaS delivery and more flexible pricing reduce the barrier to adoption.

Which region currently leads global demand?

North America led with a 42.36% share in 2025, supported by a mature HR-tech ecosystem, major hyperscaler presence, and faster adoption of governance-ready AI tools.

What is the biggest near-term challenge for vendors and buyers?

Integration complexity remains the biggest near-term obstacle, because many large IT and telecom employers still operate fragmented HR, payroll, and workforce systems built over long periods and across multiple countries.

Page last updated on: