Talent Acquisition In IT And Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

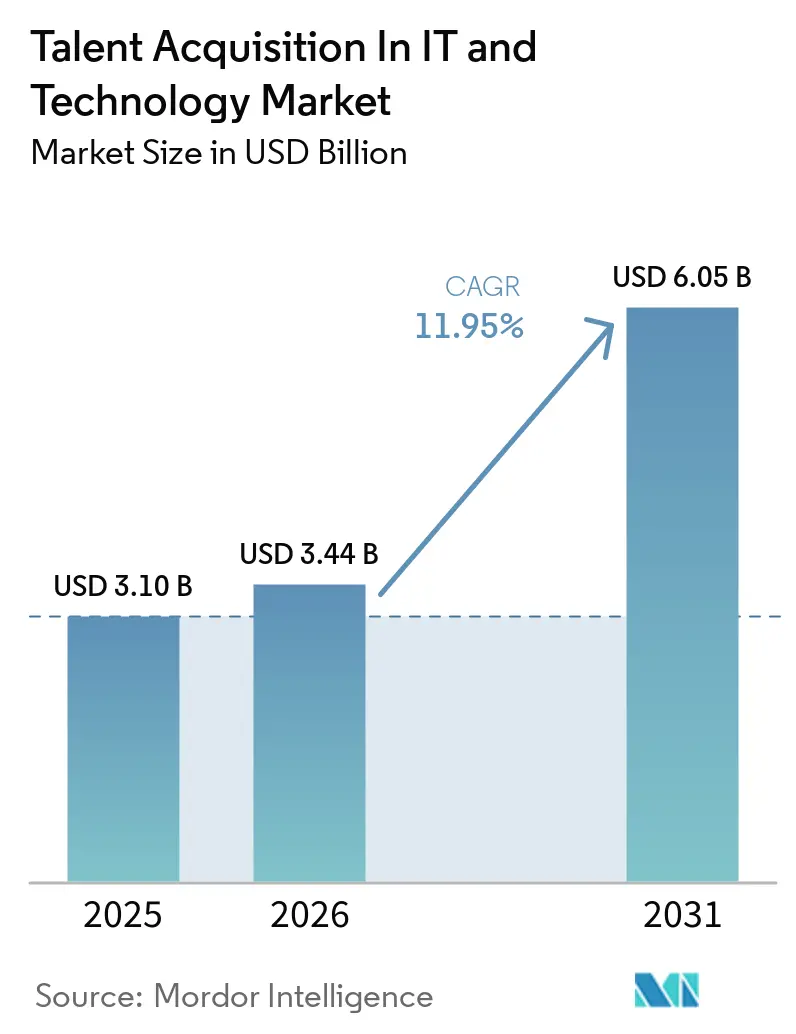

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 11.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Acquisition In IT And Technology Market Analysis by Mordor Intelligence

The talent acquisition in IT and technology market was valued at USD 3.1 billion in 2025 and is estimated to grow from USD 3.44 billion in 2026 to USD 6.05 billion by 2031, at a CAGR of 11.95% during the forecast period (2026-2031). Growth remains durable because employers are still operating in a talent environment where demand for advanced technology roles is outpacing supply. Hiring pressure has also shifted from general software and infrastructure roles toward AI model development, AI literacy, data engineering, and related skills, which makes older recruiting methods less effective. This is increasing demand for platforms that can source, assess, screen, and engage technical candidates with more precision. The market is also being shaped by a clear move toward broader HCM suite integration, as major acquisitions in 2025 pushed buyers to choose between suite-based recruiting architecture and specialized standalone tools. Compliance pressure around AI-led hiring decisions is adding urgency to vendor selection, as employers increasingly seek platforms that support governance, transparency, and audit readiness alongside speed and automation.

Key Report Takeaways

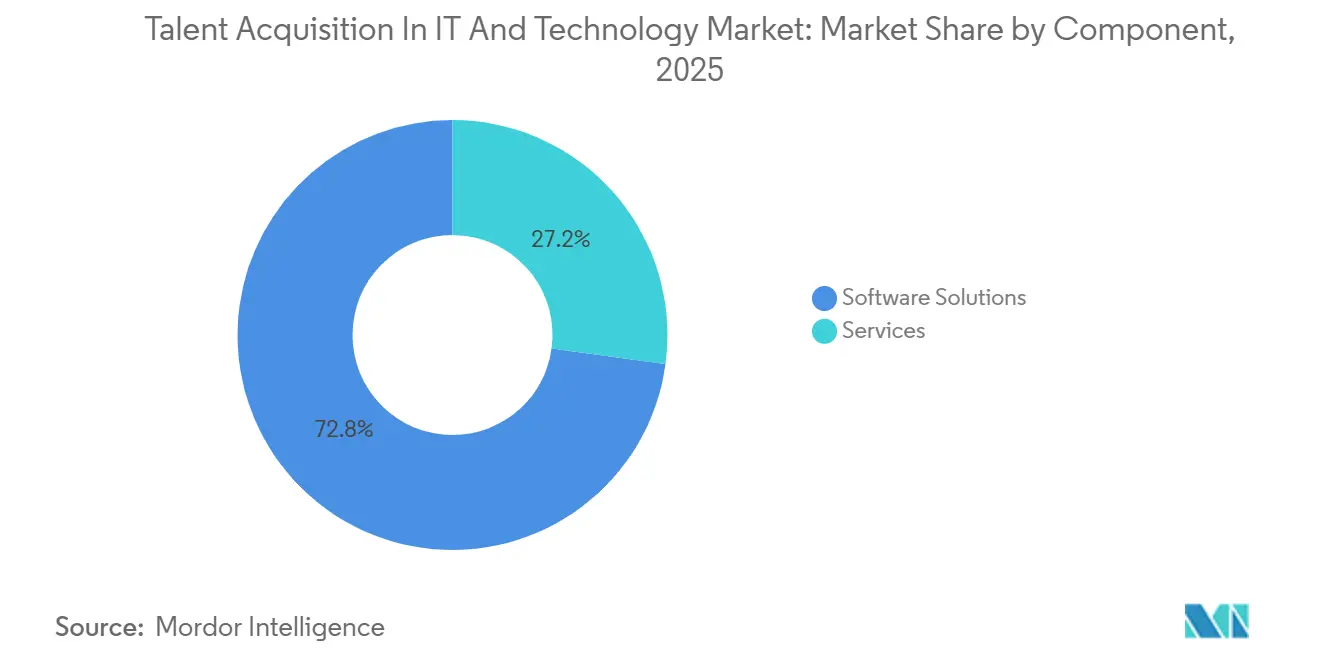

- By component, software solutions accounted for 72.84% of talent acquisition in IT and technology market in 2025, while services are projected to expand at a 12.46% CAGR through 2031.

- By deployment mode, cloud accounted for 71.12% of the talent acquisition in IT and technology market in 2025, while hybrid deployment is projected to grow at a 13.92% CAGR through 2031.

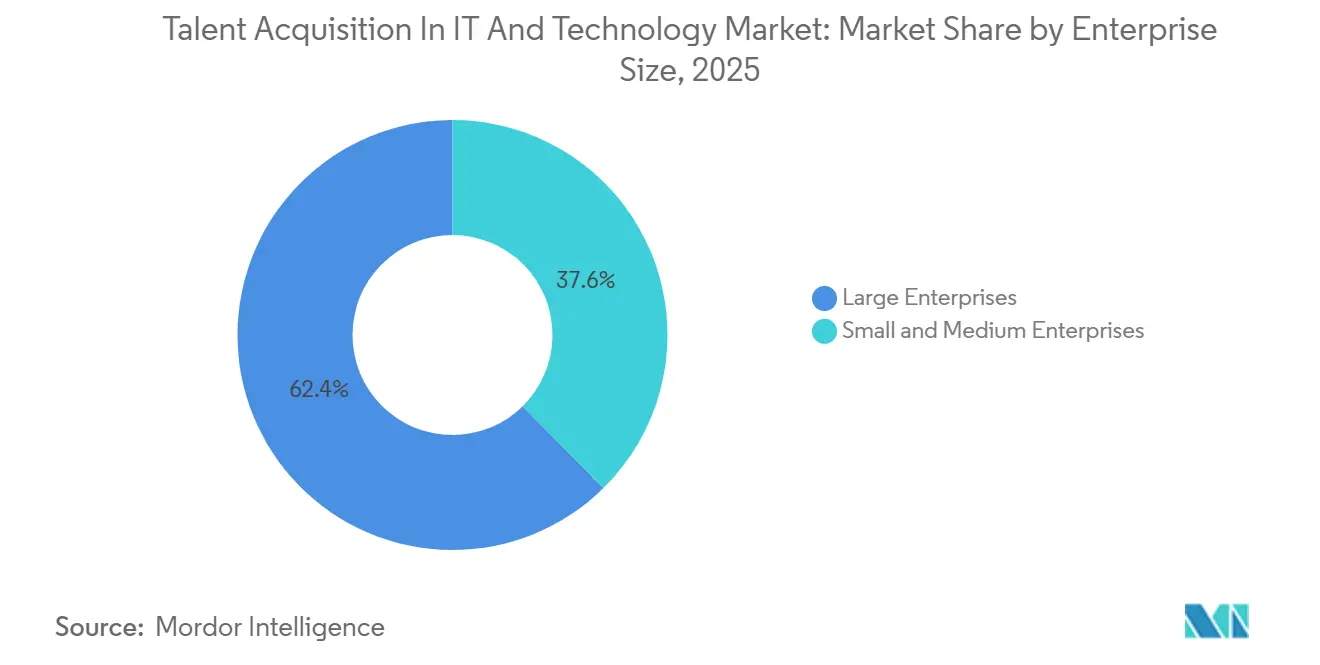

- By enterprise size, large enterprises accounted for 62.39% of revenue in 2025, while small and medium enterprises are expected to expand at a 14.18% CAGR through 2031.

- By geography, North America held 39.42% of the talent acquisition in IT and technology market share in 2025, while Asia-Pacific is projected to expand at a 15.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Talent Acquisition In IT And Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Skills Shortage in Emerging Technologies | +2.1% | Global, acute in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Accelerating Digital Transformation Among Tech Employers | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Mainstream Adoption of AI-Powered Recruitment Automation | +1.5% | Global, early in North America and Europe | Short term (≤ 2 years) |

| Rising Preference for Remote and Hybrid Work Models | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of Venture-Backed Tech Start-ups in Asia-Pacific | +0.9% | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Increasing Compliance Requirements for Tech Hiring | +0.6% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Skills Shortage in Emerging Technologies

Digital investment is still expanding the number of technical roles employers need to fill, which is supporting steady demand in the IT and technology talent acquisition market. U.S. tech employment was projected to grow by 1.9% in 2026, adding nearly 128,000 roles and reinforcing the hiring burden on employers competing for scarce technical skills. This hiring need is becoming more selective because employers now want candidates with AI, cloud, data, and security capabilities that are harder to validate through simple resume filters. As a result, the talent acquisition in IT and the technology market is benefiting from stronger demand for precision sourcing, technical assessment, and structured screening workflows rather than broad application intake alone. The spending cycle behind digital transformation is therefore acting as a leading signal for platform investment, especially where technology hiring volumes are rising faster than internal recruiting capacity.

Accelerating Digital Transformation Among Tech Employers

A sharper shortage of emerging technology skills is also driving talent acquisition in IT and technology market. Seventy-two percent of organizations had difficulty filling open roles in 2026, and AI model development and AI literacy moved ahead of traditional engineering skills as the hardest capabilities to source for the first time in the survey’s history.[1]ManpowerGroup, “Global Talent Shortage Reaches Turning Point as AI Skills Claim Top Spot,” nasdaq.com AI skill requirements appeared in 71% of U.S. tech job postings by April 2026, up from less than 10% in 2023, which shows how quickly employer demand has shifted. This change underscores the importance of assessment-led hiring, as technical ability in AI and machine learning cannot be reliably screened through keyword searches alone. That is lifting demand in the IT and technology talent acquisition market for platforms that combine validated coding tests, structured interviews, and skill benchmarking with traditional applicant tracking.

Mainstream Adoption of AI-Powered Recruitment Automation

AI adoption has moved from experimentation to regular use, changing the operating model of talent acquisition in IT and technology market. In 2026, 77% of HR teams used AI regularly in hiring workflows, while 71% of candidates also used AI tools during the job search.[2]HireVue, “2026 Global AI in Hiring Report,” hirevue.com Firms using AI in recruitment were 3.5 to 4.5 times more likely to have grown revenue in 2026, providing AI adoption with a clearer business case for recruiting teams and staffing providers. Peer-reviewed research also found a strong positive relationship between AI use and recruitment efficiency, even as trust and transparency remained important concerns. 52% of talent leaders planned to add AI agents to their hiring teams in 2026, pointing to a broader move toward autonomous sourcing, screening, and scheduling in the IT and technology talent acquisition market.

Rising Preference for Remote and Hybrid Work Models

Work model changes continue to support talent acquisition in IT and the technology market, even as fully remote arrangements have moderated. Fully remote work fell to 10% of the global workforce in 2026 from 18% in 2025, while structured hybrid work became the clearer operating norm across employers. That shift does not reduce recruiting complexity, because employers still need to source talent across wider geographies while managing location rules, scheduling needs, and workforce coordination. Hybrid work also broadens the addressable candidate base for many technical roles, as teams can now hire beyond a single office market without reverting to a fully office-based model. This is helping talent acquisition in the IT and the technology market by raising demand for multilingual workflows, cross-border verification, and candidate engagement tools that work across multiple labor markets.[3]JLL, “Structured Hybrid Work Becomes the Global Norm as Strategic Focus Shifts to AI-Readiness,” jll.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy Concerns in Candidate Analytics | -0.8% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Volatility in Venture Capital Funding Cycles | -0.7% | Global, pronounced in Asia-Pacific and North America | Short term (≤ 2 years) |

| High Switching Costs for Enterprise ATS Platforms | -0.5% | Global, concentrated in large enterprises | Medium term (2-4 years) |

| Fragmented Global Tech-Talent Regulations | -0.4% | Global, diverging across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy Concerns in Candidate Analytics

Candidate analytics is becoming more useful, but it is also becoming harder to govern across multiple hiring systems. As AI tools take on a larger role in screening and evaluation, employers face greater pressure to explain decisions, maintain review controls, and make candidate handling more transparent. Findings in 2026 also show that AI is now used regularly by both employers and candidates, increasing the volume of automated interactions and underscoring the importance of confidence in how those systems operate. The practical challenge is that candidate data often flows through applicant tracking systems, CRM tools, interview software, and analytics layers simultaneously, creating more points where governance can break down. This slows parts of the talent acquisition in IT and technology market because buyers increasingly prefer vendors with built-in controls and auditable workflows over point solutions that require manual oversight across several systems.

Volatility in Venture Capital Funding Cycles

Venture funding cycles remain a real restraint on talent acquisition in IT and technology market, as many fast-growing buyers are also the most budget-sensitive. There were 133 global HCM transactions in Q1 2026, up from 117 in Q1 2025, indicating that deal activity remained active even as funding conditions remained selective.[4]PMCF, “Human Capital Management M&A Pulse Q1 2026,” pmcf.com Early-stage technology companies tend to cut software spend quickly when hiring plans slow, and talent acquisition platforms are often exposed to this pattern because contract size is closely tied to recruiting volume. This creates a mismatch between vendor growth plans and customer purchasing capacity, especially in start-up-heavy ecosystems where headcount expansion depends on external funding. The effect is not large enough to halt demand, but it does create uneven buying behavior within the talent acquisition market for IT and technology, particularly among smaller and high-growth technology employers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Changes The Revenue Mix

Software solutions accounted for 72.84% of revenue in 2025, making them the largest component of the IT and technology talent acquisition market. ATS platforms, candidate relationship management tools, interview suites, and assessment technologies remain the core infrastructure for enterprise technology hiring because they organize high-volume workflows and reduce manual screening. Demand in software is shifting toward technical assessment and interview tools as employers seek to validate AI, machine learning, and coding skills with greater rigor. By April 2026, AI skills were required in 71% of U.S. tech job postings, underscoring the need for more specialized screening and evaluation tools.

This shift is affecting product demand, with an enterprise suite that includes more than 7,500 validated questions and AI-powered plagiarism detection with 93% accuracy. In one deployment, a structured technical assessment reduced false-positive screening flags from 10% to 4%, underscoring why buyers are willing to pay more for skill validation than to rely solely on generic filtering. Services are projected to expand at a 12.46% CAGR from 2026 to 2031, indicating that this part of talent acquisition in IT and technology market is growing faster as employers outsource implementation, managed recruiting support, and AI workflow governance. The service layer is becoming increasingly important because many organizations want AI-enabled recruiting systems, but far fewer have the internal expertise to implement, monitor, and refine them at scale.

By Deployment Mode: Cloud Leads While Hybrid Advances

Cloud deployment accounted for 71.12% of revenue in 2025, giving it the largest share of the talent acquisition market in IT and technology. Cloud has become the default architecture for enterprise and mid-market buyers because it supports faster deployment, subscription pricing, and easier integration with broader HCM environments. The largest platform vendors are focused on cloud delivery, further reinforcing cloud as the standard buying path for modern recruiting systems. This gives cloud a durable lead because most new product releases, AI features, and workflow upgrades are arriving first through cloud environments rather than legacy installations.

Hybrid deployment is projected to expand at a 13.92% CAGR from 2026 to 2031, making it the fastest-growing configuration in the IT and technology talent acquisition market. Growth is being supported by employers in regulated sectors that want cloud-scale performance but still need stronger control over where candidate data is stored or processed. That makes hybrid models especially relevant for financial services, defense, and public sector hiring environments where full cloud migration is not always acceptable. On-premises deployment continues to lose ground as a primary mode, but it still matters in legacy environments and for organizations gradually moving toward more modern recruiting architectures.

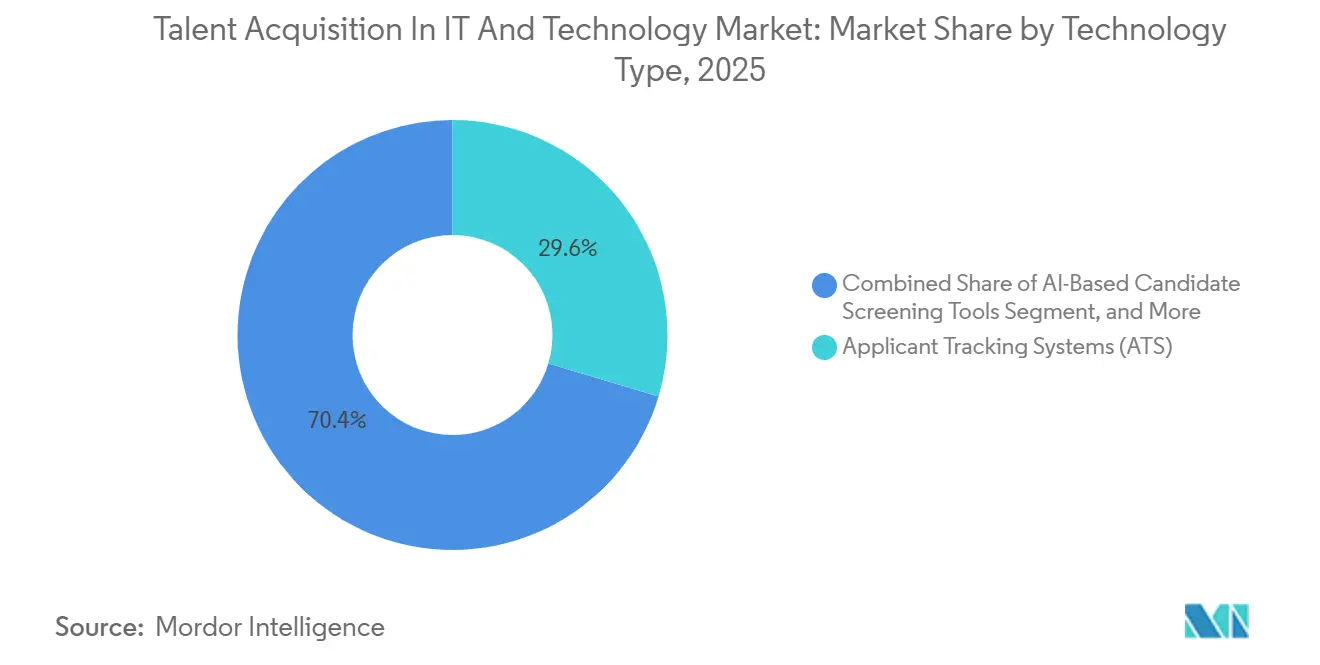

By Technology Type: AI Screening Disrupts Legacy ATS Workflows

Applicant tracking systems accounted for 29.62% of revenue in 2025 and remain the primary systems for requisitions, interview schedules, and offer letters. Nonetheless, AI-based candidate screening tools are growing at an 11.12% CAGR because employers need faster shortlists without compromising quality. Coding assessment suites now include anti-plagiarism checks and AI-generated interview questions, while video interviewing solutions support asynchronous reviews across time zones.

Integration is key. Modern stacks bundle ATS, AI screening, coding tests, and candidate relationship management, raising switching costs. Vendors unable to provide open APIs are losing ground as customers insist on unified analytics across the hiring funnel. Over the forecast period, the talent acquisition in IT and technology market will reward providers that combine high assessment accuracy, regulatory compliance, and user-friendly dashboards.

By Enterprise Size: SME Adoption Narrows The Gap

Large enterprises accounted for 62.39% of revenue in 2025, giving them the largest share of the IT and technology talent acquisition market. Their lead reflects higher hiring volumes, broader geographic footprints, and greater complexity across workforce planning, compliance, and technical recruitment. The 2025 consolidation wave also focused directly on enterprise demand, as Workday completed the Paradox acquisition and SAP completed the SmartRecruiters acquisition to strengthen high-volume and enterprise recruiting workflows. Enterprise buying remains active rather than static because many large organizations are still rationalizing multi-system recruiting environments and deciding how quickly to move into suite-based architecture.

Small and medium enterprises are projected to grow at a 14.18% CAGR from 2026 to 2031, making them the fastest-growing segment of the IT and technology talent acquisition market. Subscription pricing, easier onboarding, and ready-made integrations have lowered the cost and skill barriers that once limited advanced recruiting tools to large companies. This matters in technology hiring because smaller employers often cannot win on compensation alone and instead need faster sourcing, stronger candidate experience, and better technical validation. A 30% increase in hiring intentions among technology SMEs in 2026 suggests adoption demand in this customer group is already active rather than only forecast.

Geography Analysis

North America accounted for 39.42% of revenue in 2025, giving the region the largest share of the IT and technology talent acquisition market. The region benefits from a dense concentration of technology employers, mature use of applicant tracking systems, and earlier deployment of AI in hiring workflows. A 41% U.S. tech and IT Net Employment Outlook for Q2 2026, up 8 points from Q1 2026, signals stronger hiring confidence after a period of workforce adjustment. Canada and Mexico are also supporting regional demand as employers expand nearshore hiring models and search for more flexible access to engineering talent. Europe remains an important market because shortages are severe and compliance expectations around AI-led hiring are rising.

Asia-Pacific is projected to expand at a 15.12% CAGR from 2026 to 2031, making it the fastest-growing regional segment in talent acquisition for the IT and technology market. Growth is being supported by start-up formation, enterprise digitization, and continuing shortages in AI and advanced software roles across major economies. The region also benefits from a large addressable workforce base, but employers still face strong competition for specialized talent, especially in AI and cloud roles. Talent policy changes in Singapore in 2026 were designed to improve access to top international talent, supporting broader regional hiring activity and making recruiting platforms more valuable to employers operating across borders.

South America remains smaller than North America, Europe, and the Asia-Pacific, but demand is improving as multinational employers expand hiring for cost-competitive technology talent. Brazil and Argentina are the main regional centers, and growth is tied increasingly to cloud adoption and the buildout of global capability centers. The Middle East is still an emerging market, with Saudi Arabia and the United Arab Emirates supporting demand through digital economy programs and technology hub development. Africa remains an early-stage market, though hiring activity in cities such as Nairobi, Lagos, and Cape Town is creating a longer-term opportunity for platforms that can support multilingual and cross-border recruiting workflows.

Competitive Landscape

Talent acquisition in IT and technology market shows moderate concentration, with a small group of HCM suite vendors leading enterprise platform spending, while a broader field of staffing firms, RPO providers, and specialist platforms compete below them. SAP, Workday, and Oracle strengthened their positions after the 2025 acquisition cycle reduced the number of independent enterprise-scale ATS options. SAP expanded agentic AI capabilities in SuccessFactors in May 2026, positioning Joule and Winston as connected agents across recruiting and onboarding workflows. Oracle introduced eight Fusion Agile Applications for HR in April 2026, embedding deeper autonomous decision support into hiring workflows and raising the competitive standard for enterprise automation. Workday’s completion of the Paradox acquisition in October 2025 added conversational AI and frontline hiring capabilities to its broader recruiting stack, making the suite-versus-specialist decision more important for large buyers.

The competitive landscape is broader than software alone, as staffing and RPO firms still have an advantage in delivery depth and sector specialization. ManpowerGroup’s Experis brand reported a 44% global Tech and IT Net Employment Outlook for Q2 2026, which supports the role of staffing-led providers during hiring recovery periods. Adecco reported 245 basis points of consolidated market share gains in 2025, helped by its Akkodis technology engineering unit, which shows that specialized staffing capabilities can still take share from broader workforce competitors. This keeps talent acquisition in IT and technology market from becoming overly concentrated, even as software platform ownership narrows among the largest enterprise vendors.

Competition is also shifting toward governance, skills intelligence, and workflow depth rather than simple automation claims. iCIMS introduced its Coalesce AI framework in 2026 to make responsible AI governance more central to its enterprise positioning, while its Spring 2026 release added frontline AI, trigger-based workflow automation, and AI-powered sourcing. Eightfold AI also integrated agentic interviewing with Oracle Fusion Cloud Recruiting in May 2026, demonstrating that specialist vendors can still expand by attaching high-value capabilities to large enterprise suites. Open competitive space remains strongest in regulated hiring, multilingual candidate engagement, and emerging technical skill assessment, where buyers still want more flexibility than a core suite alone can offer.

Talent Acquisition In IT And Technology Industry Leaders

Adecco Group AG

Randstad N.V.

ManpowerGroup Inc.

Allegis Group Holdings Inc.

Korn Ferry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: HackerRank unveiled AI fluency assessments, an unguarded AI assistant for coding tests, code-repository questions, integrity signals, and Chakra AI interviewer features, enabling large-scale technical evaluations at speed.

- March 2026: Accenture Australia reported AUD 3 billion (USD 2 billion) revenue and a 20% profit surge, expanding tech hiring to support cloud and analytics engagements.

- January 2026: The UAE’s Stargate project announced plans to hire up to 3,000 AI professionals in Q3-Q4 2026 to execute a USD 30 billion infrastructure build-out.

- September 2025: SAP completed its acquisition of SmartRecruiters, folding the platform into SuccessFactors to offer unified talent acquisition.

Global Talent Acquisition In IT And Technology Market Report Scope

The Talent Acquisition in IT and Technology market refers to the ecosystem of platforms, services, and processes that enable organizations to source, screen, and hire specialized technical talent. It encompasses permanent, contract, and freelance staffing models, driven by digital transformation, regulatory compliance, and demand for agile, cloud-enabled recruitment solutions.

The Talent Acquisition in IT and Technology market report is segmented by Component (Software Solutions, [Applicant Tracking System (ATS), Candidate Relationship Management (CRM), Recruitment Marketing Suite, Interview and Assessment Tools, and Onboarding Solutions] and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Solutions | Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) | |

| Recruitment Marketing Suite | |

| Interview and Assessment Tools | |

| Onboarding Solutions | |

| Services |

| On-Premises |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software Solutions | Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) | ||

| Recruitment Marketing Suite | ||

| Interview and Assessment Tools | ||

| Onboarding Solutions | ||

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By Enteprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the talent acquisition in IT and technology market?

The market was valued at USD 3.1 billion in 2025, reached USD 3.44 billion in 2026, and is forecast to reach USD 6.05 billion by 2031 at an 11.95% CAGR.

What is driving hiring platform demand in the technology sector?

Strong demand for AI, cloud, data, and security talent is the main driver, as employers increasingly need better sourcing, assessment, and screening tools to fill hard-to-hire roles.

Which component is leading revenue in this space?

Software solutions led with 72.84% of revenue in 2025 because ATS platforms, CRM tools, interview suites, and assessment systems remain the operational core of technical hiring.

Why are services growing faster than software in talent acquisition for IT roles?

Services are projected to grow at 12.46% CAGR through 2031 because employers often need outside help to implement AI-led recruiting workflows, manage RPO models, and handle governance.

Which region is growing the fastest for technology hiring solutions?

Asia-Pacific is expected to post the fastest regional growth at 15.12% CAGR through 2031, supported by start-up activity, enterprise digitization, and continued shortages in advanced technical skills.

How concentrated is competition among recruiting technology providers?

Competition is moderate because SAP, Workday, and Oracle lead enterprise platform spending, but staffing firms, RPO providers, and specialist vendors still hold meaningful space across the broader market.

Page last updated on: