Aircraft Generators Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

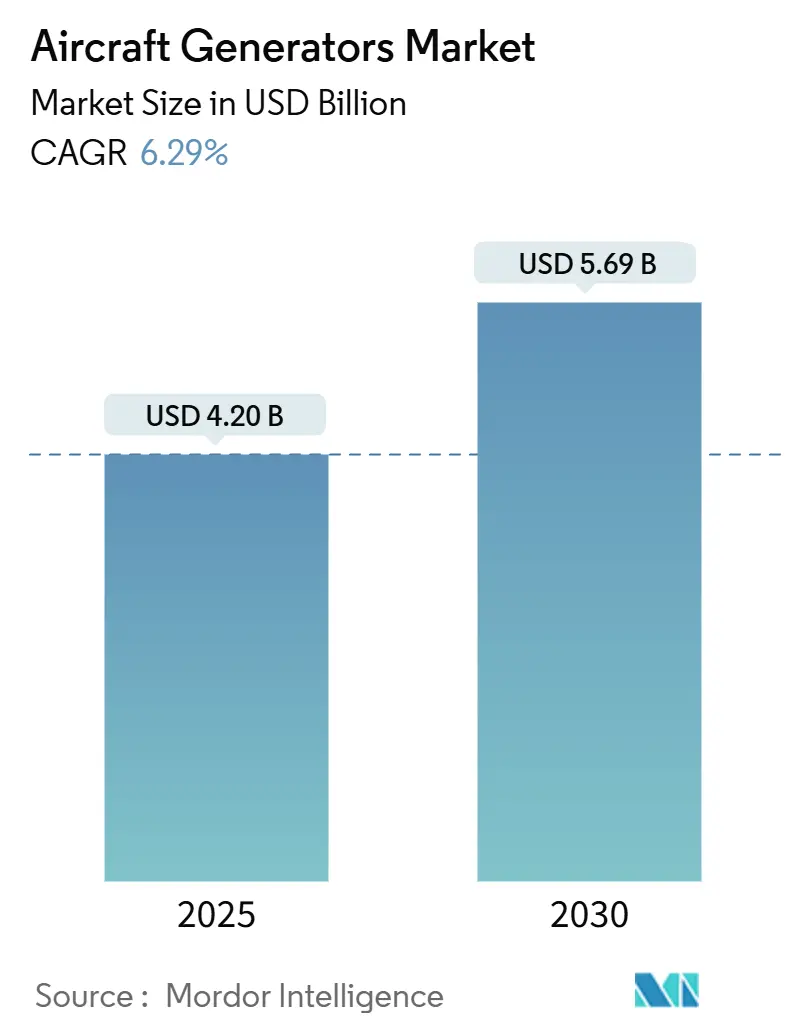

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 5.69 Billion |

| Growth Rate (2025 - 2030) | 6.29% CAGR |

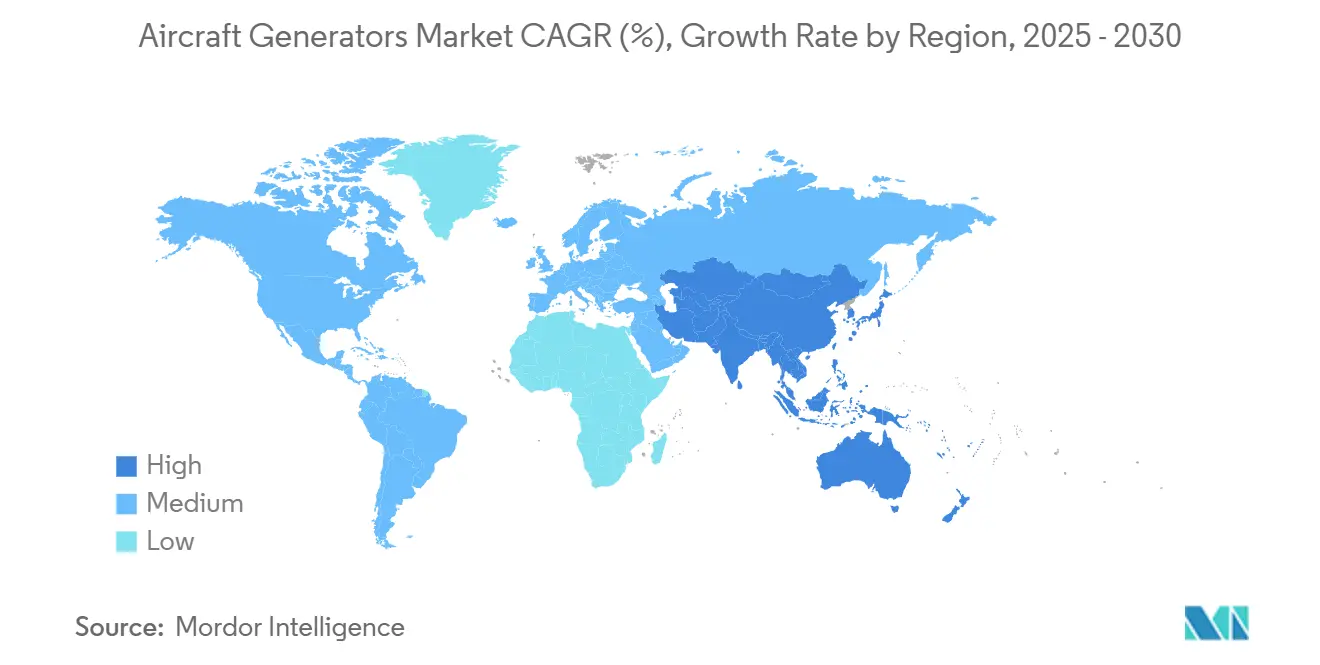

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Generators Market Analysis by Mordor Intelligence

The aircraft generators market size reached USD 4.20 billion in 2025 and is forecasted to reach USD 5.69 billion by 2030, advancing at a 6.26% CAGR. Current growth reflects a fundamental shift toward more-electric aircraft (MEA) architectures that replace hydraulic and pneumatic subsystems with higher-capacity electrical solutions. Boeing’s projection of 43,975 commercial aircraft deliveries through 2043 underpins long-term demand for original-equipment units and replacement parts.[1]Source: “Boeing Announces Fourth-Quarter Deliveries,” Boeing, boeing.com North America maintains clear volume leadership, while Asia-Pacific accelerates fastest on the back of fleet expansion and indigenous programs. Technology dynamics favor high-power-density integrated systems, starter-generator multifunctionality, and permanent-magnet topologies. Generator suppliers able to navigate certification costs, rare-earth sourcing risks, and hydrogen-ready requirements are positioned to capture incremental value across upcoming platform launches and retrofit cycles.

Key Report Takeaways

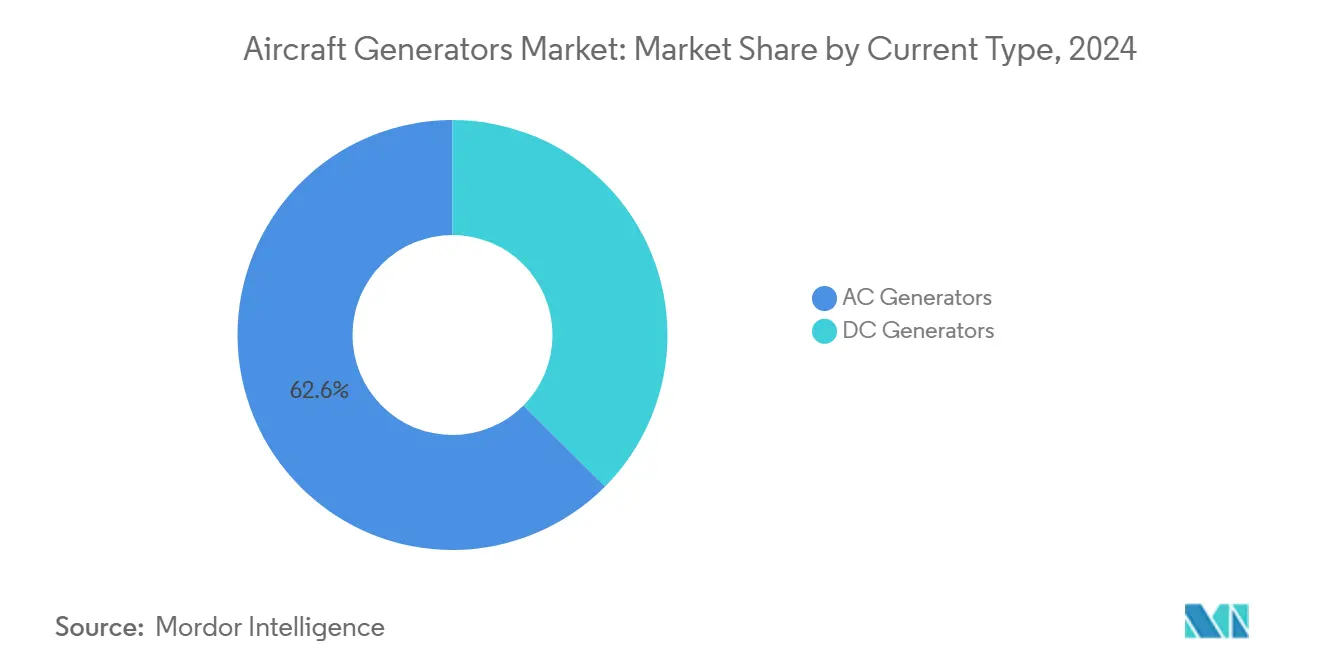

- By current type, AC generators held 62.56% of the aircraft generators market share in 2024; DC units are set to post a 7.87% CAGR to 2030.

- By generator type, integrated drive generators held a 42.35% share of the aircraft generators market in 2024, while starter generators led growth at a 9.45% CAGR through the forecast window.

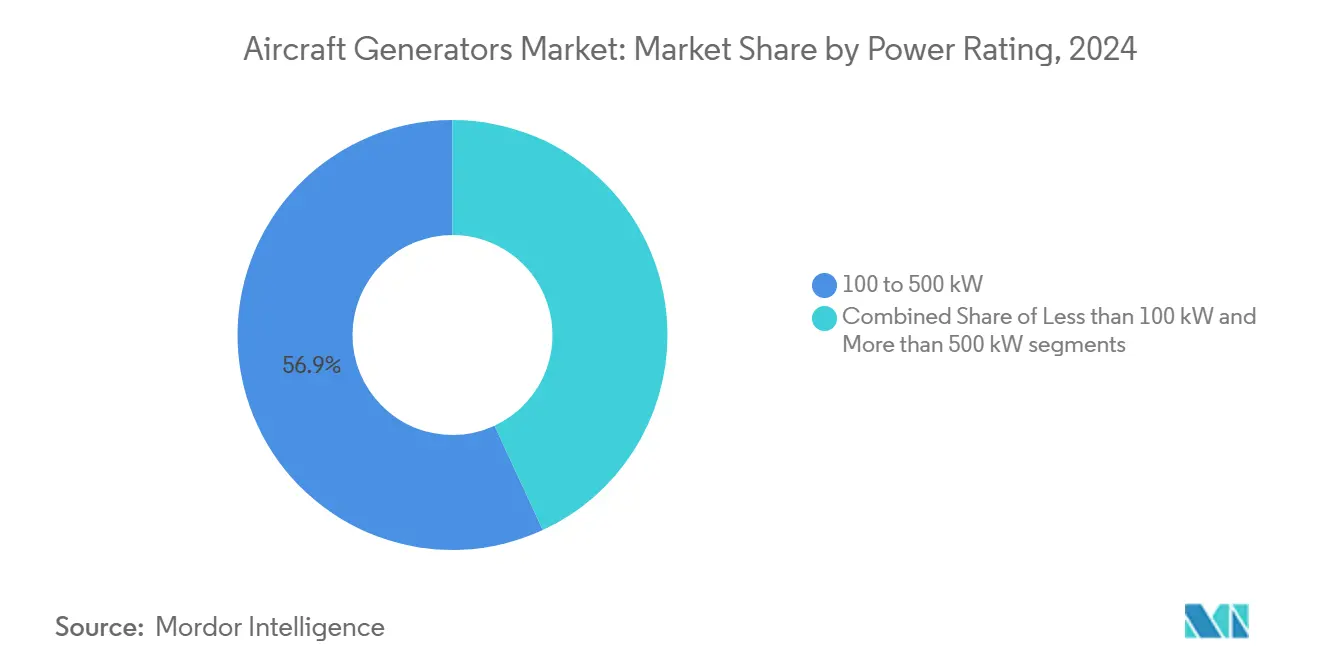

- By power rating, the 100 to 500 kW class accounted for 56.90% share of the aircraft generators market size in 2024; units above 500 kW are expanding at an 8.55% CAGR to 2030.

- By aircraft platform, fixed-wing aircraft captured 55.65% of the aircraft generators market share in 2024, whereas unmanned aerial vehicles (UAVs) are advancing at an 11.20% CAGR to 2030.

- By end use, OEM installations represented 65.80% of the aircraft generators market size in 2024; the aftermarket is rising at a 6.37% CAGR through 2030.

- By geography, North America led with a 40.15% share of the aircraft generators market size in 2024; Asia-Pacific is projected to compound at an 8.40% CAGR to 2030.

Global Aircraft Generators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating commercial aircraft deliveries | +1.8% | Global with North America, Europe, Asia-Pacific concentration | Medium term (2-4 years) |

| Transition to more-electric aircraft (MEA) architectures | +2.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Fleet modernization boosting onboard power demand | +1.4% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| eVTOL and UAV boom requires ultralight generators | +0.9% | North America, Europe, emerging APAC | Short term (≤ 2 years) |

| Hydrogen propulsion drives decentralized PM generators | +0.7% | Europe, North America, pilot APAC programs | Long term (≥ 4 years) |

| SAF-ready starter-generator retrofits mandated by regulators | +0.5% | Global, early in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Commercial Aircraft Deliveries

Global airframers increased output in 2024, with Airbus shipping 766 jets and holding an 8,658-aircraft backlog that secures generator demand well into the 2030s.[2]Source: “Airbus reports 766 commercial aircraft deliveries in 2024,” Airbus, airbus.com Boeing’s 348 deliveries and recovery plans imply additional surge requirements once supply constraints ease. Single-aisle programs, representing 76% of projected deliveries, rely on standardized 100-500 kW units that benefit from scale economies. US capacity expansions worth USD 2.8 billion across Boeing and GE Aerospace will further stabilize volumes. Suppliers capable of concurrent production and certification ramp-up are best placed to capitalize on the near-term spike and follow-on aftermarket pull.

Transition to MEA Architectures

NASA and GE Aerospace’s HyTEC research proves dual-mode motor-generator integration in turbofans, delivering 20% fuel-burn improvement targets.[3]Source: “NASA, GE Aerospace Advancing Hybrid-Electric Airliners with HyTEC,” NASA, nasa.gov Such architectures migrate aircraft electrical systems from legacy 115 V AC to high-voltage DC networks, demanding new generator electronics and thermal solutions. Airbus’s ZEROe initiative signals eventual adoption of hydrogen and fuel-cell propulsion that could eliminate traditional turbine-driven generators. Manufacturers investing in high-power-density designs, wide-bandgap semiconductors, and advanced cooling emerge as preferred partners during platform definition phases through the 2030s.

Fleet Modernization Boosting Onboard Power Demand

Extended aircraft lifecycles enabled by historically low retirement rates drive retrofit demand for higher-capacity units as airlines upgrade avionics, cabin connectivity, and environmental systems. Aftermarket generator replacements often coincide with 6-year heavy checks, creating predictable cycles with attractive margins. Regulatory pushes for sustainable aviation fuel (SAF) compatibility and modern cockpit systems further incentivize airlines to swap legacy generators for advanced starter-generators capable of smarter control, improved sealing, and higher thermal loads.

eVTOL and UAV Boom Requires Ultralight Generators

Urban air mobility (UAM) programs and military drones require compact permanent-magnet machines supporting frequent start-stop profiles and variable speeds. ZeroAvia’s 2,000 provisional hydrogen-electric engine orders and Honeywell’s new 60 kVA lightweight unit illustrate market appetite for innovations that shed mass and integrate electronics closely with propulsion stacks. Certification pathways are shorter than for commercial jets yet still demand AS9100 quality rigor, creating an opening for agile suppliers with automotive EV experience transitioning to aerospace safety standards.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and certification costs | -1.2% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Reliability concerns in high temperature zones | -0.8% | Global hot-weather operations | Medium term (2-4 years) |

| Rare-earth magnet supply volatility | -1.1% | Global, acute for PM units | Short term (≤ 2 years) |

| Thermal management limits in narrowbody equipment bays | -0.7% | Global, single-aisle fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High R&D and Certification Costs

Achieving airworthiness approval for a new aircraft generator involves a layered compliance path that stretches engineering budgets and calendars. Developers must complete altitude, vibration, humidity, lightning-strike, and electromagnetic-interference campaigns in certified chambers, then run endurance cycles that simulate service lives. Every design change triggers a partial retest under DO-160 and MIL-STD-704, extending test-article fabrication and analysis loops. Dedicated engineering-authorized representatives oversee documentation, adding schedule risk when findings require design rework. As capital remains tied up until type certification, cash-flow stress escalates. Established suppliers absorb these hurdles with existing rigs and data libraries, whereas entrants face expensive outsourcing and learning curves.

Reliability Concerns in High Temperature Zones

Persistent heat in desert and tropical regions accelerates the degradation of copper windings, varnish insulation, and bearing lubricants inside aircraft generators. At inlet air temperatures above 55 °C, internal hot spots may exceed 225 °C, driving partial discharge events and insulation cracking that precipitate in-flight electrical faults. Therefore, airlines flying dense schedules through Doha or Singapore request uprated designs featuring high-temperature epoxy resins, silver-alloy lead wires, and optimized forced-air paths. Manufacturers must validate these materials through 5,000-hour thermal soak and rapid-cycle tests that mimic take-off power spikes. Failures discovered in service trigger unscheduled removals, warranty claims, and reputational damage that outweigh redesign costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Current Type: DC Adoption Gains Momentum

AC machines delivered 62.56% of 2024 shipments, anchored by the aircraft generators market’s long-standing reliance on 115 V, 400 Hz networks. Demand stability stems from established avionics compatibility and ample MRO know-how. Yet DC units register a 7.87% CAGR as battery-rich hybrids and eVTOLs favor direct-current links that avoid conversion losses. In the 2024 base year, DC units totaled nearly USD 1.58 billion, representing the fastest-expanding slice within the aircraft generators market. Tier-one suppliers are resizing portfolios: multiple programs now standardize 540 V DC buses, encouraging OEM bids specifying brushless DC machines with embedded digital control. This pivot already influences the aircraft generators market size at the subsystem level, prompting avionics and power-electronics providers to validate compatibility around standard voltage rails.

With airlines seeking weight cuts, DC architectures deliver partial savings by eliminating constant-speed drive gearboxes. Regulatory frameworks still lag but are advancing; EASA’s SC-E19 proposal outlines fault-containment rules for high-voltage DC. Suppliers investing in wide-bandgap rectifiers and double-insulated stators will accelerate qualification. As platform counts rise, DC penetration could narrow the AC share below 55% by 2030, although legacy fleets keep total AC volumes resilient through at least mid-decade.

By Generator Type: Starter-Generators Outpace Integrated Drives

Integrated drive generators (IDGs) retained 42.35% of 2024 revenues, equal to USD 1.78 billion of the aircraft generators market size, due to pervasive fitment on current narrow-body platforms. Their constant-frequency output remains valuable for legacy loads, yet mechanical complexity drives maintenance cost dissatisfaction. Starter-generators are climbing at a 9.45% CAGR because they consolidate start and generate functions, simplifying line-replaceable-unit (LRU) counts. Airlines valuing dispatch reliability and lower spares pools are issuing RFPs with direct starter-generator line items, particularly on regional jets and emerging electric helicopters.

Permanent-magnet variants within this class attract technology investments, yet rare-earth sourcing constraints temper volume scaling. Meanwhile, variable-speed constant-frequency (VSCF) concepts attempt middle-ground solutions but face integration skepticism. The IDG cohort is countering with digital prognostics and improved lube systems, lengthening mean-time-between-overhaul to preserve incumbency. Nonetheless, by 2030, starter-generators could approach one-third of the total aircraft generators' market share if hybrid-electric timelines hold.

By Power Rating: Mid-Class Dominance, High-Power Upswing

Generators rated 100 to 500 kW contributed 56.90% of 2024 deliveries, primarily serving single-aisle and mid-range widebody programs. This level of demand anchors manufacturing lines and drives the largest spare-parts pools in the aircraft generators market. The aircraft generators market size for this band will expand steadily yet cede relative importance to units exceeding 500 kW, projected to grow 8.55% annually as twin-aisle upgrades and hydrogen-electric demonstrators push electrical loads past 1 MW.

Below 100 kW, niche needs persist for business jets and UAVs; mass adoption of electric trainers could spark incremental spikes, though overall dollar value remains smaller. Suppliers spanning multiple brackets hedge volume swings: Safran’s 300 kW GENeUS Smart platform scales modules to 1 MW, enabling coverage across two categories. High-power prospects rely on successfully mitigating thermal and electromagnetic interference, which is critical for cabin-environment safety.

By Aircraft Platform: UAV Surge Challenges Fixed-Wing Supremacy

Fixed-wing applications held 55.65% of 2024 revenues, benefiting from a global in-service fleet exceeding 25,000 jets. Replacement cycles every 20,000 flight hours sustain baseline OEM and aftermarket demand, fortifying the aircraft generators market. UAVs, however, post double-digit growth as militaries add endurance drones and parcel carriers launch pilotless logistics services. Their 11.20% CAGR reflects procurement volumes alongside frequent technology refreshes due to rapid sensor evolution.

Rotary-wing aircraft show slower adoption of new generator types because vibration and variable rotor speeds complicate certification. Nevertheless, the impending UH-60 digital cockpit upgrade path and electric tail-rotor projects may accelerate new generator orders after 2027. Successful UAV programs will influence supply chains; lightweight generators proven on drones could later migrate into manned regional air mobility aircraft, expanding addressable demand.

By End Use: Expanding Aftermarket Profit Pools

OEM channels accounted for 65.80% of 2024 units, driven by high production rates at major airframers. Yet the aftermarket’s 6.37% CAGR delivers outsized profitability: MRO markups often exceed OEM margins by 200 basis points. Fleet age above 12 years across many carriers pushes scheduled replacements, and sustainability mandates spur additional retrofits earlier in asset life, augmenting the aircraft generators market size captured by service specialists.

Partnerships such as Eaton-SIA Engineering’s Malaysia joint venture illustrate a focus on regional MRO accessibility to reduce turnaround time for Asian operators. Digital twins and usage-based maintenance further differentiate service offerings, locking customers into proprietary parts ecosystems. Supplier-controlled repair stations thus become strategic assets securing recurring revenue and spares pricing power.

Geography Analysis

North America retained 40.15% of 2024 revenues, reflecting mature OEM production and substantial defense budgets. Investments totaling USD 2.8 billion across Boeing’s St. Louis expansion and GE Aerospace’s new facilities will keep regional supply lines competitive. Labor actions such as the 2024 IAM strike highlight volatility risks yet also prompt automation upgrades that can raise generator throughput in the medium term.

Europe leverages Airbus assembly lines and advanced R&D funding for hydrogen propulsion, fueling steady generator innovation. Projects like the Airbus-Toshiba superconducting motor and HEROPS fuel-cell consortium cement the region as a proving ground for high-voltage, cryogenic architectures. Regulatory emphasis on lifecycle emissions tightens performance specs, pushing suppliers toward recyclable materials and higher efficiency at lower parasitic drag.

With an 8.40% CAGR outlook, Asia-Pacific benefits from surging traffic growth, indigenous programs, and industrial offset policies. Safran’s six-site footprint in India for LEAP engine parts and joint ventures in China illustrate localization strategies that mitigate tariff and logistics constraints. Chinese airframers’ push for domestic subsystems could shift share toward regional competitors, especially in DC generator niches optimized for new narrow-body models.

South America, the Middle East, and Africa remain smaller but are seeing incremental aftermarket demand as carriers delay fleet renewal. Regional MRO hubs in Dubai and São Paulo aim to capture generator overhaul work from transcontinental carriers, widening service coverage and lowering freight costs.

Competitive Landscape

The market structure is moderately concentrated. The key players are underpinned by entrenched airframer contracts and certification track records. They are investing in additive manufacturing of stators, integrated power electronics, and digital health monitoring to protect incumbency. Mid-tier players such as Astronics and Calnetix focus on niche high-speed or UAV segments, differentiating through agility and specialized cooling expertise.

Strategic moves include Honeywell’s 60 kVA rotary-wing upgrade, Safran’s 300 kW GENeUS Smart launch, and RTX’s expanded magnetics facility in Florida (announced April 2025). Vertical integration trends are evident: Boeing’s bid for Spirit AeroSystems could bring generator accessory-drive interfaces in-house, forcing renegotiating power-plant supply contracts. Emerging entrants from the EV sector are exploring aerospace certification, but face capital intensity barriers and lengthy approval cycles.

Aircraft Generators Industry Leaders

Honeywell International Inc.

RTX Corporation

Safran SA

General Electric Company

AMETEK, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Rostec's United Engine Corporation (UEC) launched a 400-kW turbogenerator based on the VK-650V engine for hybrid drones and aircraft. Presented at the Arctic Region forum, this innovation offers unmatched power-to-weight performance in Russia, targeting northern region operations with advanced power electronics for efficient energy conversion.

- May 2025: AMETEK MRO B&S Aircraft expanded its aircraft power generation repair capabilities at its Wichita facility, introducing overhaul services for the Power Pack Motor. This development aligns with the growing demand for aircraft generators, particularly for PT-6 engines used in King Air 200 and 300 series aircraft.

Global Aircraft Generators Market Report Scope

| AC Generators |

| DC Generators |

| Integrated Drive Generators (IDG) |

| Variable-Speed Constant-Frequency (VSCF) Generators |

| Auxiliary Power Unit (APU) Generators |

| Starter-Generators |

| Permanent-Magnet Generators |

| Less than 100 kW |

| 100 to 500 kW |

| More than 500 kW |

| Fixed-Wing Aircraft | Commercial Passenger Aircraft |

| Military Aircraft | |

| Business Jets | |

| Rotary-Wing Aircraft | Civil Helicopters |

| Military Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Current Type | AC Generators | ||

| DC Generators | |||

| By Generator Type | Integrated Drive Generators (IDG) | ||

| Variable-Speed Constant-Frequency (VSCF) Generators | |||

| Auxiliary Power Unit (APU) Generators | |||

| Starter-Generators | |||

| Permanent-Magnet Generators | |||

| By Power Rating | Less than 100 kW | ||

| 100 to 500 kW | |||

| More than 500 kW | |||

| By Aircraft Platform | Fixed-Wing Aircraft | Commercial Passenger Aircraft | |

| Military Aircraft | |||

| Business Jets | |||

| Rotary-Wing Aircraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By End Use | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft generators market in 2025?

The aircraft generators market size stands at USD 4.20 billion in 2025, and is forecasted to reach USD 5.69 billion by 2030.

What is the expected CAGR for aircraft generator revenues to 2030?

Revenues are projected to advance at a 6.26% CAGR through 2030.

Which current type leads generator demand today?

AC units maintain 62.56% market share, though DC types are growing faster.

Which region is expanding fastest for generator suppliers?

Asia-Pacific posts the highest growth, forecasted at an 8.40% CAGR to 2030.

Why are starter-generators gaining popularity?

They integrate start and power functions, reducing weight and maintenance while registering a 9.45% growth outlook.

What risk affects permanent-magnet generator costs?

Volatile rare-earth material prices and sourcing constraints pose cost and availability risks.

Page last updated on: