Brazil Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

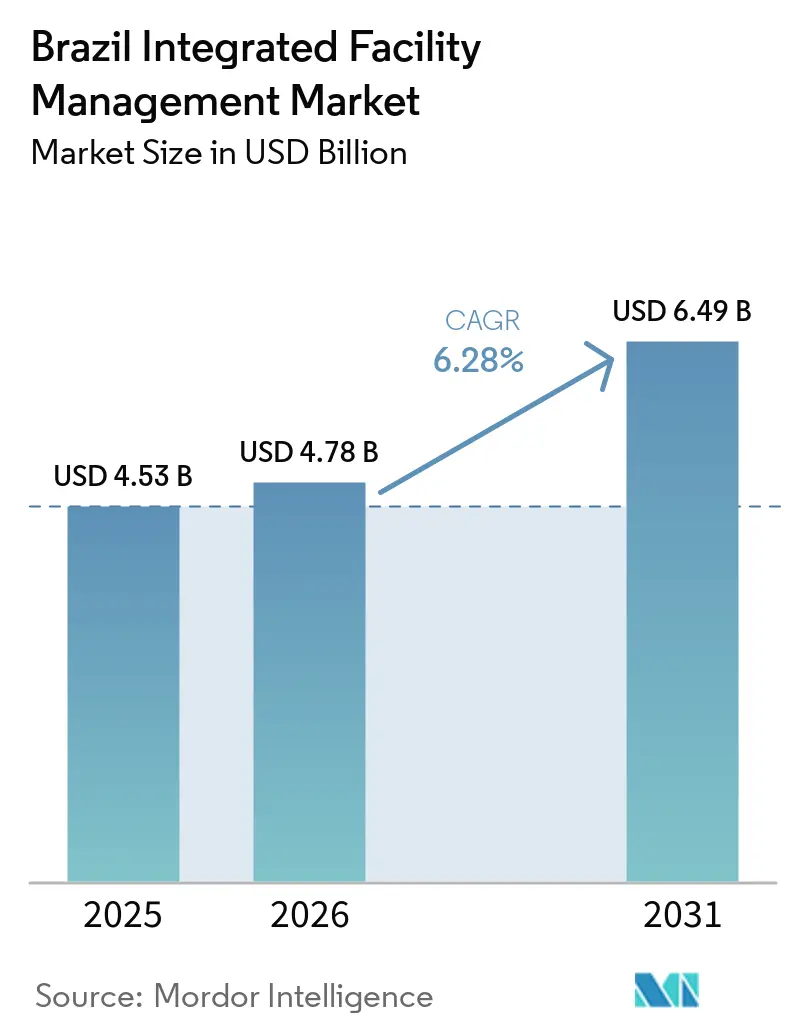

| Base Year Market Size (2025) | USD 4.53 Billion |

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

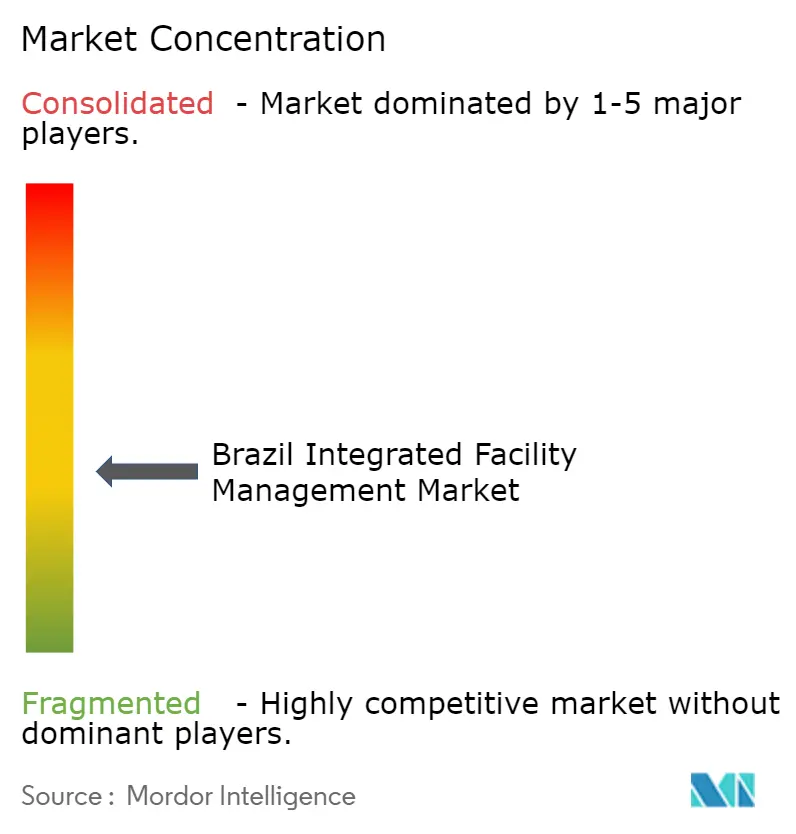

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Integrated Facility Management Market Analysis by Mordor Intelligence

The Brazil Integrated Facility Management Market size is projected to be USD 4.53 billion in 2025, USD 4.78 billion in 2026, and reach USD 6.49 billion by 2031, growing at a CAGR of 6.28% from 2026 to 2031.

Public infrastructure spending remains a core support because Novo PAC disbursed BRL 47.4 billion (USD 8.2 billion) from the federal budget in 2025 and reached 95% financial execution against its authorized BRL 49.8 billion (USD 8.6 billion) allocation, which is expanding the stock of schools, hospitals, transport assets, and housing projects that require long-term operations and maintenance support. Private participation is reinforcing that cycle because private capital represented 46.3% of cumulative PAC execution by August 2025, which shows that publicly backed projects are also creating privately managed assets that can move into structured service contracts. The Brazil integrated facility management (IFM) market is also benefiting from broader corporate outsourcing, stronger legal clarity, and a data center buildout that is increasing demand for higher-skill contracts tied to uptime, energy monitoring, and predictive maintenance. Competitive conditions remain fragmented, but consolidation is becoming more visible as Grupo GPS expands through acquisitions while global providers defend large accounts through command centers, compliance systems, and multi-site operating platforms. Skilled labour shortages, higher labour costs, import tariff pressure on equipment, and elevated office vacancy in Rio de Janeiro are limiting short-term margin expansion. However, the Brazil IFM market still has room to grow because a meaningful share of services remains in-house and public-private contracts are widening the recurring service base.

Key Report Takeaways

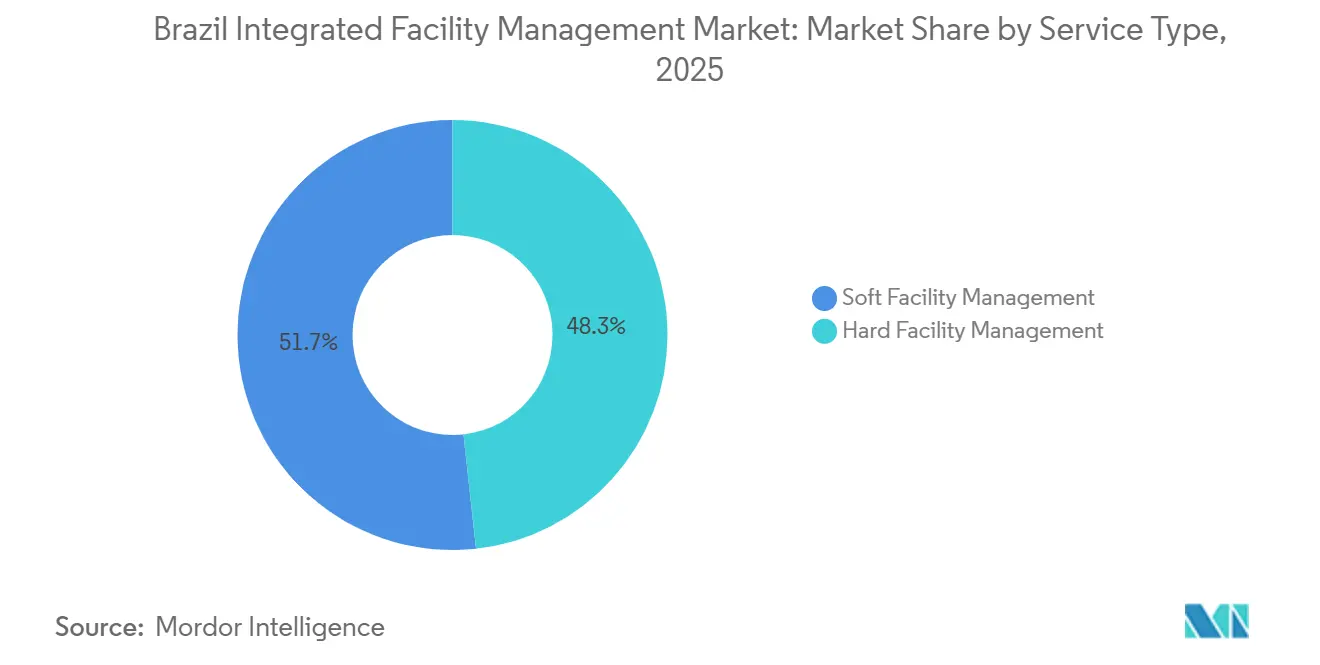

- By service type, soft facility management segment in the Brazil integrated facility management market led with 51.74% revenue share in 2025, while hard facility management segment is projected to expand at a 6.87% CAGR through 2031.

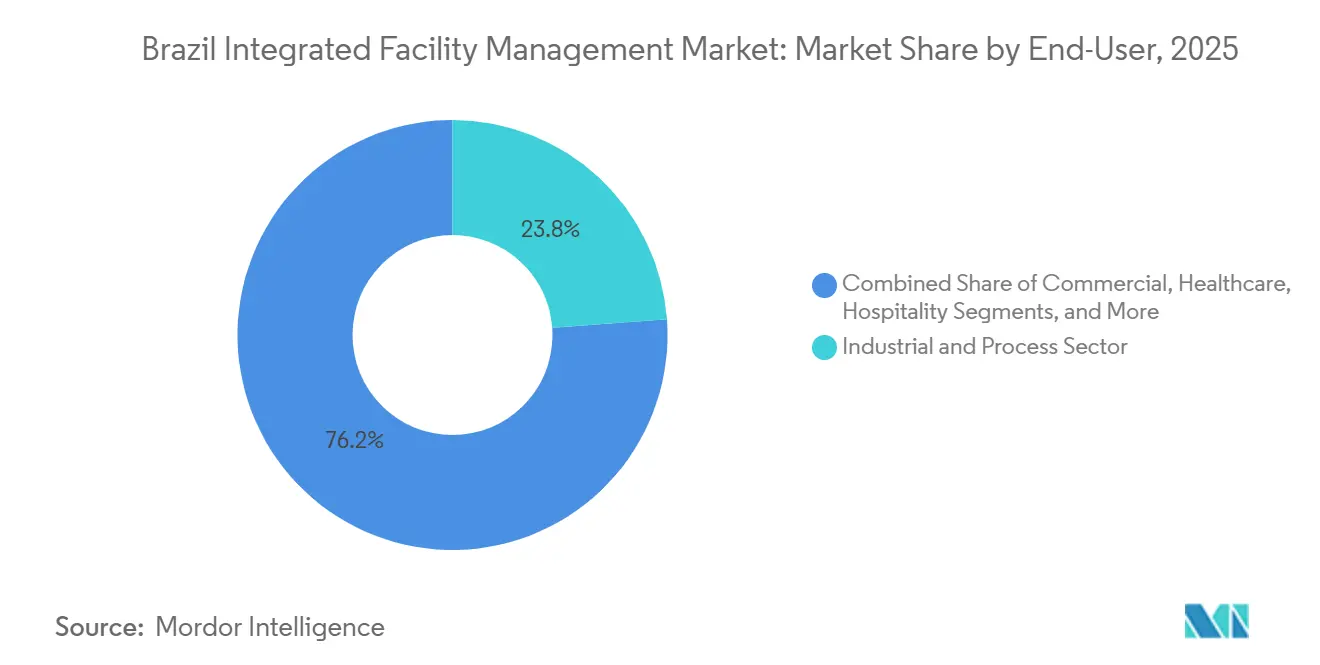

- By end user, industrial and process sector in the Brzail integrated facility management (IFM) market held 23.84% of revenue in 2025, while commercial segment is forecast to grow at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Public-Private Infrastructure Pipeline | +1.20% | Brazil-wide, concentrated in São Paulo, Rio de Janeiro, Minas Gerais, and Northeast states | Medium term (2-4 years) |

| Accelerated Digitalization of Building Operations | +1.00% | São Paulo, Rio de Janeiro, Belo Horizonte, with spillover to Curitiba and Porto Alegre | Long term (≥ 4 years) |

| Hyperscale and Edge Data Center Proliferation | +0.90% | São Paulo and Rio de Janeiro core, with new hubs in Fortaleza and Porto Alegre | Long term (≥ 4 years) |

| Rising Outsourcing of Non-Core Operations | +0.80% | Brazil-wide, led by Southeast industrial and commercial clusters | Short term (≤ 2 years) |

| ESG Protocol and Compliance Requirements | +0.60% | São Paulo, Rio de Janeiro, Belo Horizonte, with spillover to Curitiba and Porto Alegre | Medium term (2-4 years) |

| ESG-Linked Financing Driving Green Certifications | +0.50% | Institutional capital markets, with project concentration in the São Paulo metropolitan area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Public-Private Infrastructure Pipeline

Brazil’s public-private project cycle is creating one of the clearest long-duration demand channels for the Brazil integrated facility management market. Novo PAC had executed BRL 944.8 billion (USD 163.3 billion) by August 2025, equal to 70.8% of its BRL 1.3 trillion (USD 224.6 billion) cycle target for 2023-2026, and private capital represented the largest share of that execution at 46.3%. That matters because many newer concession and PPP structures now include direct obligations for cleaning, security, maintenance, conservation, and service-level monitoring after construction is completed. The São Paulo state government awarded the 30-year concession for its new Administrative Center in February 2026, and the concessionaire is responsible for service delivery over the life of the asset under LEED Gold requirements. Federal budget execution in 2025 also remained high, which indicates that projects were not only announced but also pushed forward into assets that will require structured support over many years. As more schools, hospitals, transport facilities, and social infrastructure projects move from construction into operation, the Brazil integrated facility management (IFM) market is gaining a wider installed base of assets that require recurring service contracts rather than one-off maintenance work.

Accelerated Digitalization of Building Operations

Digital monitoring is changing how the Brazil integrated facility management market is sold, priced, and delivered across commercial, healthcare, and industrial properties. An ABRAFAC survey reported that 57.1% of healthcare institutions already used operational dashboards and 52.7% had real-time automatic alerts, while 47.3% of managers still identified limited awareness of IoT benefits as a barrier to adoption.[1]ABRAFAC, “Technical Labor Availability in Facilities Services,” ABRAFAC That gap creates room for professional providers to win work by packaging software, sensors, and reporting into their service offerings instead of competing only on labour intensity. The transition is also being reinforced by smart metering and model-based workflows, including the Siemens and CPFL Energia program launched in 2025 to install 1.6 million smart meters and the federal BIM mandate applied to projects above BRL 20 million (USD 3.5 million). Early adopters reported maintenance cost reductions of 8-12%, which supports the shift from reactive maintenance to planned intervention and energy optimization. As a result, the Brazil IFM market is moving away from purely headcount-based competition and toward contracts that reward providers able to combine CMMS tools, sensor data, and documented performance reporting.

Hyperscale and Edge Data Center Proliferation

The data center buildout is creating a technically distinct demand layer inside the Brazil integrated facility management (IFM) market. Brasscom projected cumulative sector investment of USD 92 billion from 2025 to 2031, including USD 69 billion in equipment and USD 23 billion in physical infrastructure, which points to a long runway for high-specification facility support.[3]Equinix, “SP6 Data Center Expansion,” Equinix These sites require continuous uptime, dense MEP systems, formal escalation procedures, and service windows that are much tighter than those found in standard office or retail environments. Equinix opened its SP6 AI-ready site in Santana de Parnaíba in April 2026 after a USD 114 million investment, while new projects are also moving outside the São Paulo and Rio de Janeiro corridor into locations such as Ceará.[2]Brasscom, “Digital Infrastructure Investment Outlook,” Brasscom That regional spread means operators must build technical teams and response networks beyond their traditional bases if they want to compete for Smart Hands, First Line Maintenance, and critical systems monitoring work. The Brazil IFM market, therefore, gains not only higher contract volume from data centers but also a richer mix of contracts that are longer, more specialized, and less exposed to commoditized pricing.

Rising Outsourcing of Non-Core Operations

Outsourcing remains one of the strongest structural supports for the Brazil integrated facility management market because the shift is moving beyond labour arbitrage and into risk management, compliance, and operational focus. A Deloitte survey published in early 2026 found that 97% of Brazilian service providers expected contract volume growth in the coming years, while 84% of client organizations reported improved legal certainty after the consolidation of Brazil’s outsourcing framework. The Associação Brasileira de Serviços Terceirizados also reported 18% growth in outsourced facilities contracts between June and October 2024, which shows that the shift was already accelerating before the latest 2026 demand cycle. The opportunity remains large because 43% of the addressable FM service market was still handled in-house, leaving substantial room for migration into integrated contracts as employers face higher funding costs, labour complexity, and greater ESG documentation needs. Client outcomes also remained favourable, with 96% citing improved service quality and 89% pointing to simpler production and management processes after outsourcing. That combination of legal clarity, performance benefits, and internal cost pressure continues to widen the addressable base for the Brazil integrated facility management (IFM) market across both private and public accounts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Skilled Technical Labor | -0.60% | Brazil-wide, most acute in secondary metros and the Northeast | Medium term (2-4 years) |

| Wage Inflation Compressing Provider Margins | -0.50% | Brazil-wide, with the highest intensity in São Paulo and Rio de Janeiro | Short term (≤ 2 years) |

| High Import Tariffs on Cost-Cutting Equipment | -0.40% | Technology-intensive IFM providers operating nationwide | Medium term (2-4 years) |

| Persistent Commercial Vacancy in Secondary Cities | -0.30% | Rio de Janeiro, with spillover to Recife, Fortaleza, and Salvador | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Skilled Technical Labor

Skilled labour availability remains a major operational restraint for the Brazil IFM market, especially in hard FM categories that depend on certified technical staff. The HVAC and refrigeration segment has identified the shortage of qualified professionals as a critical constraint, and companies reported suspended projects, reduced service offerings, and higher prices as direct consequences. The problem is not limited to entry-level supply because many trained technicians are also leaving formal employment for autonomous work, which weakens institutional accountability and reduces access to continuous training. The shortage is more severe outside major hubs because specialized roles such as automation technicians, fire safety engineers, and MEP specialists remain concentrated in São Paulo and Belo Horizonte, which can delay commissioning in secondary markets by 3-6 months. Qualification hurdles also remain high because engineering-grade maintenance often requires CREA-linked credentials and provider-led training programs before teams can meet contract standards. Until training capacity scales more broadly, the Brazil integrated facility management market will continue to face limits in how quickly it can expand higher-value technical service lines across the country.

Wage Inflation Compressing Provider Margins

Wage inflation is constraining profitability across the Brazil integrated facility management market because labour remains the largest cost component in most contracts. Brazil’s aggregate labour cost index reached 189.15 points in February 2026, which shows how quickly the cost base has increased for employers operating under fixed-price agreements. The 2026 collective labour convention for the facilities and building conservation segment also approved a 7% minimum wage adjustment and added a fixed monthly benefit of BRL 315 (USD 54) for workers in São Paulo and Greater São Paulo, which raised baseline employee costs regardless of attendance patterns. Grupo GPS reported that its 2025 EBITDA margin declined by 0.4 percentage points despite 17% revenue growth, partly because new contract implementation required faster hiring and higher operating costs. Providers that still rely heavily on manual cleaning, routine inspection, and labour-dense site coverage are more exposed because they have fewer tools to offset recurring cost increases through automation. This margin pressure does not stop growth in the Brazil integrated facility management (IFM) market, but it does increase the premium attached to pricing discipline, contract mix, and technology adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Builds Momentum While Soft FM Keeps the Largest Base

Soft facility management (FM) held 51.74% of Brazil integrated facility management market share in 2025, which confirms that cleaning, catering, office support, and related services still form the broadest revenue base in the country. That scale reflects years of outsourcing adoption among corporate, institutional, and multi-site clients that chose bundled non-core services before moving deeper into integrated technical contracts. The segment still benefits from recurring demand because these services remain essential across offices, hospitals, education assets, and industrial support facilities. At the same time, wage adjustments in 2026 are putting more pressure on service lines such as cleaning and catering because payroll is the main cost driver in those activities. As more buyers shift toward integrated operating models, standalone soft FM is becoming a smaller share of total contracting value, even when its absolute revenue base continues to rise within the Brazil integrated facility management (IFM) market.

Hard FM is forecast to grow at a 6.87% CAGR through 2031, placing it ahead of the total Brazil IFM market and making its mix more important than the headline growth rate alone. Within the Brazil integrated facility management industry, asset management, MEP services, and fire protection are drawing more capital because they support longer contracts, greater technical depth, and lower commoditization risk. Predictive maintenance is now moving closer to a baseline requirement in tenders tied to data centers, hospitals, and retrofitted commercial buildings, especially in São Paulo and Rio de Janeiro. The updated hospital fire-systems inspection manual implemented in January 2026 also raised inspection frequency and training obligations, which strengthens the position of providers that can train in-house teams and document compliance at scale. This is why hard FM is not only expanding faster but also reshaping how the Brazil integrated facility management market differentiates technical operators from labor-only vendors.

By End-User: Industrial Scale Anchors Revenue While Commercial Growth Accelerates

Industrial and Manufacturing accounted for a 23.84% share of the Brazil integrated facility management market size in 2025, making it the largest end-user base by revenue. That leadership reflects the operating intensity of oil and gas, mining, heavy industry, refining, and logistics assets that require continuous maintenance, safety systems, and site infrastructure support. Petrobras alone committed USD 109 billion in its 2026-2030 business plan, including USD 69 billion in upstream and USD 16 billion in refining, transport, and commercialization, which supports multi-year demand for maintenance and integrated services across industrial facilities. Demand in this segment is usually weighted toward hard FM because uptime, regulatory compliance, and technical certification matter more than simple labour scale. Public and institutional clients are also widening the addressable base because PPP contracts for schools, hospitals, and administrative assets increasingly include ongoing operations and non-core service obligations rather than only basic cleaning and guarding.

Commercial is projected to grow at a 6.95% CAGR through 2031, which makes it the fastest-growing end-user segment in the Brazil IFM market. São Paulo office vacancy fell from 20.8% at the end of 2024 to 15.9% by December 2025, which is bringing deferred maintenance, retrofits, and service-level upgrades back into the active spending cycle. ESG adoption is also reinforcing that shift because 71% of Brazilian companies began implementing ESG practices in 2024 and 78% identified environmental and social impact as the main driver, which raises expectations for energy, water, and indoor air management instead of reactive-only maintenance. Within the Brazil integrated facility management industry, the commercial base now extends across build-to-suit assets, IT parks, retail centers, warehouses, and green-certified properties, which are increasingly procured as integrated packages rather than isolated service lines. Brazil also ranked among the global top five markets for LEED project volume in 2025, which is widening the role of operating standards and certification-linked service scopes in commercial contracts.

Geography Analysis

The Southeast accounted for an estimated 55-60% of the Brazil integrated facility management market share in 2026, which keeps the regional base of the Brazil integrated facility management market firmly centered on São Paulo, Rio de Janeiro, Belo Horizonte, and Campinas. São Paulo remains the national anchor because it hosts more than 30% of domestic data center capacity and originates many of the multi-site contracts that later expand into other states. The Tamboré corridor is becoming an especially dense cluster of technical demand because it is absorbing large data center campuses from operators such as Scala Data Centers and Equinix, both of which require high-availability MEP, fire safety, and monitoring support. That concentration favours providers with deep engineering teams, faster response coverage, and the ability to standardize workflows across large campus environments. It also reinforces the role of São Paulo as the pricing and capability benchmark for the wider Brazil integrated facility management (IFM) market.

Rio de Janeiro remains the second major hub even though commercial office vacancy remained elevated at 25.6% in 2025, which limits revenue density in parts of the office stock. The city still sustains large facility services demand through Petrobras-linked operations, offshore logistics, refineries, and industrial infrastructure that require continuous maintenance and safety support. The Northeast is now emerging as the most important new geographic pivot because Ceará has attracted a BRL 11 billion (USD 1.9 billion) first-phase data center project at the Pecém Port Complex, which brings hyperscale-grade facility requirements into a region that previously had a more limited technical FM profile. Tax incentives, proximity to 16 submarine cables, and renewable energy availability are making Fortaleza and nearby municipalities more relevant to investors that require power-intensive digital infrastructure. That shift means the Brazil IFM market is becoming less dependent on the traditional São Paulo and Rio de Janeiro corridor for future high-specification demand.

The South and selected inland cities are also becoming more relevant as operators build broader service networks. Tecto Data Centers planned five new Brazilian sites for 2026, with regional distribution that included Porto Alegre, Recife, Belém, and Brasília, which pushes facility service providers to support national coverage rather than remain concentrated in the Southeast. Curitiba and Porto Alegre stand out for early smart-city and IoT deployment, where integrated traffic, energy, and security systems are creating demand niches for providers with stronger digital and systems integration capability. Curitiba also hosted the world’s first LEED v5 Platinum certification, which can accelerate the spread of higher operating standards and more formal performance tracking across the South’s commercial stock. As those reference projects multiply, the Brazil integrated facility management market should see a more even national distribution of complex contracts, even if the Southeast retains the largest revenue base.

Competitive Landscape

The Brazil integrated facility management market remains moderately fragmented, and the top five outsourced services providers collectively held 10.7% of the addressable market in 2026, which shows that no single operator has national control. This structure remains looser than the one seen in the United States and Western Europe, where concentration is materially higher and platform scale is more established. Grupo GPS is the clearest domestic consolidator because it had completed 26 acquisitions since its April 2021 IPO and served 4,635 customers with 185,000 employees in 2025. The company generated BRL 17.28 billion (USD 3.0 billion) in net revenue in 2025 and entered 2026 with a stated plan to add BRL 1.5-2.5 billion through further M&A, which shows that consolidation is active rather than theoretical. That strategy mirrors the playbook used by larger European multi-service operators, where acquired food, security, logistics, and maintenance capabilities are cross sold through an existing client base.

Global groups remain important in large-account competition across the Brazil integrated facility management market because they can defend contracts through operating systems, certification, and technology. Sodexo manages 1,150 FM contracts in Brazil, employs 17,000 facilities workers, and identifies Brazil as its fourth-largest market globally, which underlines the country’s scale within international portfolios. Providers at the upper tier are differentiating through ISO 41001, centralized command centers, ESG-linked reporting, and multi-site SLA monitoring instead of relying only on labour scale. This is creating a more visible split between labour-heavy, price-led services on one side and higher-value integrated platforms on the other side of the Brazil integrated facility management market.

White-space opportunities remain strongest in hyperscale data center support and industrial maintenance where local specialization is still limited. Smart Hands and First Line Maintenance for data centers, especially under sub-four-hour SLA structures, are still open categories for Brazilian operators willing to invest in training, certifications, and escalation processes. Industrial maintenance is also underpenetrated by full IFM models because many contracts are still organized around single-service equipment work instead of integrated multi-trade management. Technology-first competition is rising at the same time, with Johnson Controls expanding OpenBlue capabilities in Brazil in November 2024 and adding a dedicated service unit in Chapecó in March 2026, which raises the performance bar for digitally enabled hard FM delivery. Sodexo also expanded its command center model and innovation footprint, while Grupo GPS continued using acquisitions to deepen cross-selling breadth, which means the Brazil integrated facility management market is moving toward stronger platform competition even though the base remains highly fragmented.

Brazil Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Grupo GPS

Sodexo S.A.

Jones Lang LaSalle Incorporated (JLL)

Cushman & Wakefield plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Elea Data Centers completed the first phase of a BRL 2.3 billion (USD 470 million) data center project for Petrobras, one of the most significant industrial IFM service contracts executed in Brazil's oil and gas digital infrastructure segment, requiring continuous 24/7 technical facility operations.

- April 2026: Equinix opened the SP6 AI-ready data center in Santana de Parnaíba, São Paulo, following a USD 114 million (BRL 569.1 million) investment as part of a BRL 1.5 billion (USD 259 million) Brazil expansion plan for 2026. SP6 is part of Equinix's simultaneous execution of four Brazil expansion projects, a company first, directly generating multi-year IFM contract opportunities for MEP, fire safety, and site security services.

- March 2026: Omnia Data Centers, Pátria Investimentos, broke ground on a BRL 11 billion (USD 2.1 billion) first-phase data center at the Pecém Port Complex, Ceará, for TikTok and ByteDance, representing the largest facility-intensive infrastructure project in Brazil's Northeast and generating demand for specialist hard FM services outside the São Paulo and Rio de Janeiro corridor.

- March 2026: Johnson Controls expanded its Brazil operations with a new dedicated service unit in Chapecó, Santa Catarina, targeting the agro-industrial cluster with HVAC maintenance, FRICK compressor services, and energy-efficiency facility management, reinforcing IFM coverage in Brazil's food processing heartland.

Brazil Integrated Facility Management Market Report Scope

The Brazil Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End-user Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current size of Brazil integrated facility management services?

The Brazil integrated facility management market was valued at USD 4.5 billion in 2025 and is projected to reach USD 6.5 billion by 2031 at a 6.3% CAGR over 2026-2031.

Which service category leads revenue in Brazil?

Soft FM led with 51.74% of revenue in 2025 because cleaning, catering, and office support still form the broadest outsourced service base across corporate and institutional assets.

Which end-user group generates the largest demand?

Industrial and Manufacturing held 23.84% of revenue in 2025, supported by oil and gas, refining, mining, and heavy industrial sites that require continuous technical maintenance and safety services.

Why are data centers becoming important for facility services in Brazil?

New hyperscale and edge projects require 24/7 uptime, dense MEP systems, Smart Hands support, and stronger preventive maintenance, which raises contract value and technical complexity.

Which region has the strongest concentration of demand?

The Southeast accounted for an estimated 55-60% of national revenue in 2026, with São Paulo acting as the main contract origin point and technical benchmark for national service delivery.

What are the biggest near-term challenges for providers?

The main issues are limited skilled technical labour, wage inflation, tariff pressure on imported equipment, and elevated office vacancy in some cities, especially Rio de Janeiro.

Page last updated on: