Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

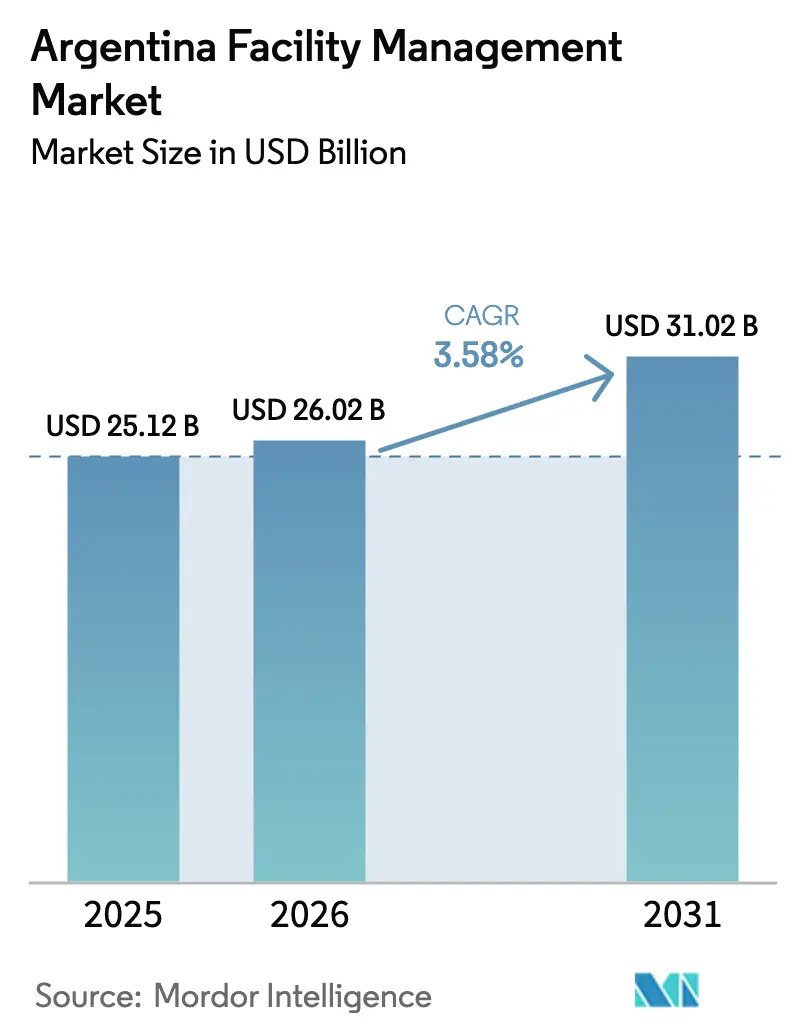

| Base Year Market Size (2025) | USD 25.12 Billion |

| Market Size (2026) | USD 26.02 Billion |

| Market Size (2031) | USD 31.02 Billion |

| Growth Rate (2026 - 2031) | 3.58% CAGR |

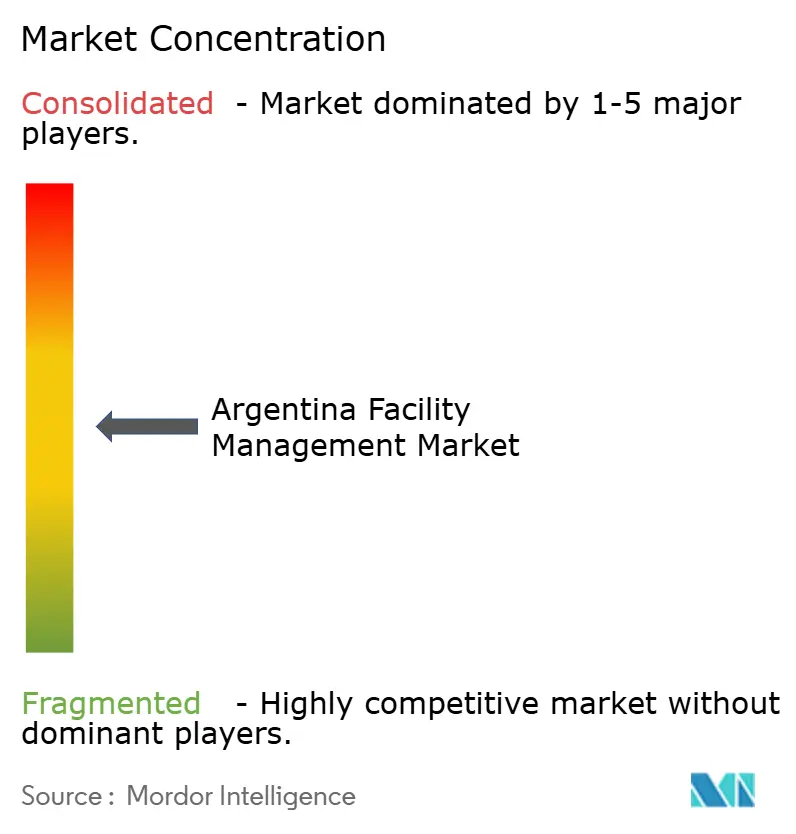

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Facility Management Market Analysis by Mordor Intelligence

The Argentina facility management market size was valued at USD 25.12 billion in 2025 and estimated to grow from USD 26.02 billion in 2026 to reach USD 31.02 billion by 2031, at a CAGR of 3.58% during the forecast period (2026-2031). Rising outsourcing adoption, expanding critical-infrastructure investments, and stricter post-pandemic hygiene requirements collectively anchor demand, while currency volatility and skilled-labour shortages temper margins. Technology-enabled hard-service offerings—especially predictive maintenance and IoT-driven asset monitoring—are increasingly bundled with traditional soft services to deliver integrated value propositions. The Buenos Aires corporate hub supplies 60% of revenues, but secondary cities outpace the capital in growth as decentralization gains traction. International providers deepen competitive pressure by pairing global standards with local execution capabilities, prompting domestic firms to modernize service portfolios rapidly.[1]Resolución 906/2023, “Integración de Sistemas de Almacenamiento de Energía,” Ministerio de Economía, economia.gob.ar

Key Report Takeaways

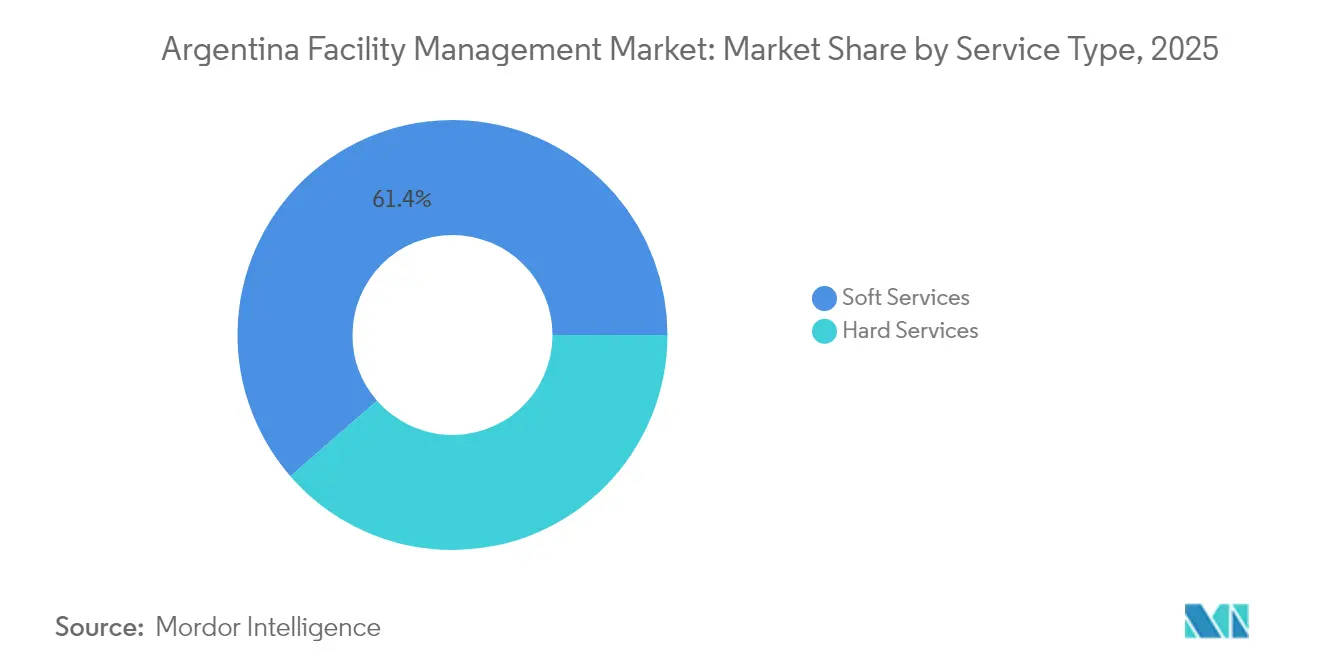

- By service type, soft services held 61.40% of the Argentina facility management market share in 2025, whereas smart-asset hard services are advancing at an 8.62% CAGR through 2031.

- By offering type, in-house delivery retained 67.35% of the Argentina facility management market size in 2025, but outsourced solutions are expanding at a 9.18% CAGR to 2031.

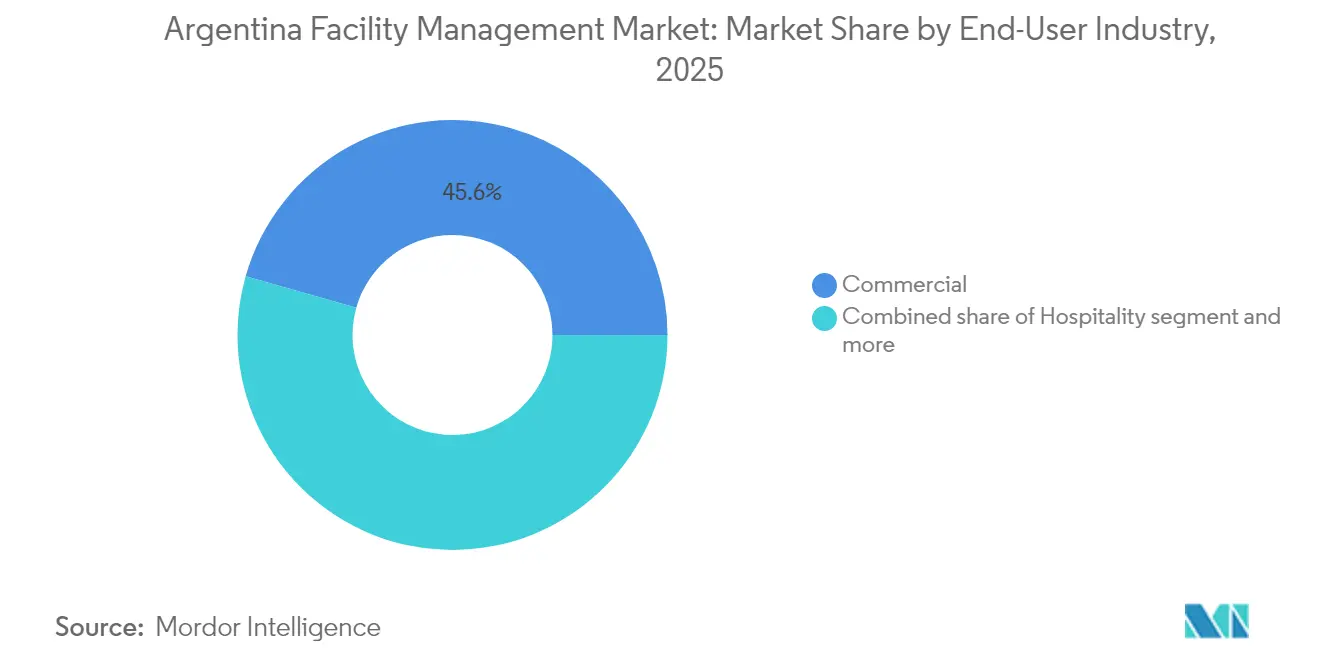

- By end-user industry, commercial facilities led with 45.60% revenue share in 2025; healthcare facilities are projected to grow at a 7.54% CAGR through 2031.

- By facility type, commercial buildings accounted for a 50.45% share of the Argentina facility management market size in 2025, while critical infrastructure facilities are growing at an 7.96% CAGR to 2031.

- CBRE, ISS, and Sodexo collectively captured the largest contractual pipeline among international providers in 2024, edging ahead of leading local firms that traditionally dominated the sector.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising outsourcing penetration among corporates | 0.80% | Buenos Aires & major metros, expanding to secondary cities | Medium term (2-4 years) |

| Post-pandemic hygiene & indoor-air-quality standards enforcement | 0.60% | National, with concentration in healthcare and commercial sectors | Short term (≤ 2 years) |

| Expansion of renewable-energy and advanced industrial facilities | 0.50% | Patagonia, Mendoza, and Buenos Aires Province | Long term (≥ 4 years) |

| Government incentives for energy-efficiency retrofits in public buildings | 0.40% | National, with early adoption in CABA and provincial capitals | Medium term (2-4 years) |

| Rapid growth of data centers in Buenos Aires spurring specialized FM demand | 0.30% | Buenos Aires metropolitan area, expanding to Córdoba | Short term (≤ 2 years) |

| Adoption of BIM-IoT integrated CAFM platforms enabling predictive maintenance | 0.20% | Buenos Aires, Córdoba, Rosario, with gradual provincial expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing Penetration Among Corporates

Argentina-based multinationals are accelerating the shift toward external service partners to convert fixed overheads into variable costs and focus internal resources on core revenue streams. Bundled and integrated contracts deliver immediate savings by folding multiple soft and hard services into outcome-oriented agreements. Technology, healthcare, and life-sciences tenants in Buenos Aires increasingly demand enterprise-grade energy management dashboards and automated SLA reporting, prompting suppliers to scale predictive-maintenance tools rapidly. Growing acceptance among domestic conglomerates in automotive and food processing extends the opportunity to secondary cities. As outsourcing volume deepens, service-level benchmarking and transparent performance metrics become critical differentiators in vendor selection.

Post-Pandemic Hygiene & Indoor-Air-Quality Standards Enforcement

Elevated cleaning frequencies and advanced filtration have evolved into baseline expectations across offices, hospitals, and retail venues. Argentine healthcare regulators now require antimicrobial surface treatments and routine indoor-air-quality audits, steering facilities toward HEPA-grade ventilation upgrades and ultraviolet disinfection options. Commercial landlords bundle hygiene analytics with tenant-experience apps that display near-real-time particulate counts, fostering occupant trust and boosting space utilization. Providers offering certified cleaning protocols gain preferred-vendor status in public tenders, especially where compliance documentation must accompany invoicing. The result is a structural uptick in contract values for soft services tied directly to measurable health and safety outcomes.[2]“Building Operations & Experience Launch,” CBRE Group Press Release, cbre.com

Expansion of Renewable-Energy and Advanced Industrial Facilities

Wind and solar projects in Patagonia, lithium-ion battery parks in Salta, and a planned LNG megaproject in Río Negro all require specialized operations-and-maintenance regimes. Asset managers must monitor turbine blade integrity, substation switchgear, and high-pressure LNG cryogenic lines under stringent safety standards. Facility management providers able to align preventive maintenance with remote-sensing data capture premium rates and long-term contracts, often indexed to energy-yield metrics. Local skill development initiatives focus on electrical, instrumentation, and control-systems certifications, expanding the technical labour pool needed for these high-complexity environments. Cross-training technicians for both renewable- and conventional-energy assets further boosts provider utilization rates.

Government Incentives for Energy-Efficiency Retrofits in Public Buildings

Federal energy-labelling mandates now cover municipal buildings, schools, and social housing, unlocking retrofit budgets for envelope insulation, LED revamping, and sensor-controlled HVAC. Performance-based public-private contracts share verified utility savings with service providers, extending predictable revenue over multi-year horizons. Facility management firms with accredited energy auditors and IRAM 11900 compliance expertise win competitive advantage, especially in Buenos Aires Province where procurement frameworks have been pre-funded through multilateral programs. Integrated retrofits often trigger follow-on maintenance scope, amplifying lifetime contract value while accelerating the adoption of building-automation systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortage and wage inflation pressures | -0.70% | National, with acute impact in Buenos Aires and technical specializations | Short term (≤ 2 years) |

| Currency volatility increasing costs of imported FM equipment | -0.50% | National, with higher impact on technology-intensive services | Medium term (2-4 years) |

| Fragmented provincial oversight causing compliance ambiguity | -0.30% | Provincial markets outside Buenos Aires, particularly interior regions | Long term (≥ 4 years) |

| High vacancy rates in Grade-B office stock limiting contract renewals | -0.20% | Buenos Aires commercial district, secondary office markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage and Wage Inflation Pressures

Technical trades such as HVAC automation, high-voltage electrical maintenance, and fire-system commissioning suffer from limited apprenticeship pipelines, lifting average wages well above national inflation. Providers invest in on-site academies, pairing classroom instruction with supervised fieldwork to accelerate credential attainment. Union negotiations increasingly include technology-training clauses, reflecting employer willingness to co-fund certifications in exchange for multiyear retention. Nevertheless, bid prices factor in wage-escalation risk, pressing clients to lock contracts to consumer-price indices, thereby shifting volatility back to providers. Margins narrow most on low-complexity soft services where labour cost dominates total price.

Currency Volatility Increasing Costs of Imported FM Equipment

Sharp peso swings inflate the landed cost of chillers, BMS controllers, and IoT sensors denominated in USD or EUR, compressing capital budgets devoted to modernization. Larger suppliers maintain foreign currency hedging lines and stock strategic spares locally to mitigate lead-time and cost spikes. Smaller domestic firms face working-capital constraints that impede technology refresh cycles, widening the capability gap with multinational competitors. Clients increasingly favour multi-year fixed-rate leases on equipment bundled within FM contracts, transferring currency risk to providers with broader treasury capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Smart Technology Elevates Hard-Service Uptake

Hard-service revenue climbed faster than any other category in 2025 as IoT-enabled asset monitoring became standard in new contract tenders. The Argentina facility management market size for smart-asset hard services is set to expand at an 8.62% CAGR, closing the gap with soft-service dominance. Integrated MEP and HVAC sensor suites feed predictive-maintenance engines that cut unplanned downtime, justifying premium fees. Simultaneously, the Argentina facility management market continues to rely on soft services—cleaning, security, catering—for steady cash flow due to their non-discretionary nature. Security assignments increasingly include video analytics and real-time access-control reporting, demonstrating how technology now permeates both service clusters.

The Argentina facility management market benefits from cross-selling opportunities when providers bundle cleaning, manned guarding, and smart-maintenance under unified account management. As building owners seek single-invoice simplicity, modular dashboards display KPI compliance across diverse workstreams, reinforcing integrated-service contract renewals. Providers investing in robotics for floor care and drones for façade inspection further differentiate on efficiency, signalling an ongoing shift toward data-rich delivery even in traditionally low-tech soft services.

By Offering Type: Outsourcing Gains Ground Without Displacing In-House Control

Corporations historically maintained direct control of janitorial, security, and minor maintenance crews, preserving a 67.35% share of in-house delivery in 2025. The Argentina facility management market share held by outsourced providers nonetheless expanded rapidly as CFOs prioritized variable-cost structures. Bundled FM contracts lower procurement overhead, while integrated FM agreements stabilize service quality across multisite portfolios. In absolute terms, the Argentina facility management market size attached to outsourced delivery is forecast to grow at 9.18% CAGR to 2031, outpacing overall industry expansion.

Single-service outsourcing remains the entry point for risk-averse clients; however, bundled and integrated formats command higher margins and longer tenures. Multinationals operating in pharmaceuticals and tech anchor flagship integrated FM agreements that include space planning and energy optimization KPIs. Domestic mid-market firms increasingly emulate these models to access expertise unavailable in house, signalling a structural shift rather than a cyclical response to cost pressures.

By End-User Industry: Healthcare Outpaces a Stable Commercial Core

Hospitals and clinics require stringent environmental controls, specialized waste disposal, and regulated cleaning protocols that push contract values above those in general office space. Consequently, healthcare exhibits the highest forecast growth, widening its footprint within the Argentina facility management market. The Argentina facility management market size captured by healthcare providers is slated to accelerate at 7.54% CAGR, underpinned by modernization of public-sector facilities and private-sector capacity expansions.

Commercial real estate nevertheless remains the revenue anchor, anchored by Grade-A office towers, shopping centers, and hybrid workplaces that collectively generate 45.60% of 2025 turnover. Ongoing refurbishment of premium offices to attract tenants supports steady spend on energy-efficient retrofits and workplace-experience enhancements. Institutional facilities—schools, museums, municipal complexes—follow closely, particularly where public-private partnerships tie performance fees to user satisfaction metrics.

By Facility Type: Critical Infrastructure Commands Premium Growth

Data centers, transport hubs, and power-generation sites constitute a niche yet highly technical slice of the Argentina facility management market. Mission-critical uptime requirements and rigorous regulatory oversight enable providers to price contracts at a meaningful premium, which explains the 7.96% CAGR outlook for critical-infrastructure facilities. Predictive analytics surrounding server-room cooling loads and substation transformer health minimize downtime risks, reinforcing client willingness to engage long-term service alliances.

Commercial buildings still dominate volumetrically, accounting for 50.45% of 2025 revenue, thanks to Buenos Aires’ dense high-rise stock and nationwide retail portfolios. The Argentina facility management market share held by commercial premises is expected to remain substantial as mixed-use developments proliferate. Residential complexes, educational campuses, and specialty venues such as wineries create incremental niches where providers tailor amenity-centric service bundles to enhance resident and visitor experiences.

Geography Analysis

Buenos Aires anchors the Argentina facility management market with 59.40% of 2025 turnover, reflecting a deep concentration of corporate headquarters, government ministries, and institutional landlords. Sophisticated tenant expectations sustain demand for integrated FM, CAFM platforms, and ESG-aligned performance metrics. While the region expands more slowly than the national average, contract renewals are sizable and typically multiyear, bolstering revenue certainty.

Rural provinces benefit indirectly from federal transport and renewable-energy programs that extend rail connectivity and install wind-farm clusters. Facility management providers with mobile, tech-enabled workforces seize early-mover advantages in these geographies but must navigate fragmented inspection regimes where provincial codes differ materially from national standards. Training local subcontractors on corporate compliance frameworks becomes a strategic imperative to sustain service-quality consistency across Argentina’s expanding economic map.

Competitive Landscape

The Argentina facility management market hosts a mix of global leaders and entrenched local specialists. CBRE leverages its Building Operations & Experience platform to integrate FM with workplace-flexibility services, winning multi-site bundled contracts among technology and life-science tenants. ISS prioritizes ESG credentials, embedding carbon-reduction dashboards within service agreements to appeal to sustainability-oriented clients. Sodexo focuses on operational discipline, reducing contract-mobilization times and deploying standardized digital toolkits for real-time KPI monitoring.

Local champions such as Plural and Facility Service retain competitive footholds through deep municipal relationships and cultural familiarity, often subcontracting advanced hard-service elements to niche engineering firms. The technology race intensifies as both international and domestic players adopt BIM-IoT solutions, drone inspections, and robotics to boost productivity. Consolidation is likely: mid-sized providers lacking capital for digital upgrades may seek mergers or strategic alliances to preserve market relevance. Labor availability remains a universal challenge, prompting competitors to fund joint vocational programs to secure technician pipelines and meet rising service-level obligations.[4]“Banco Provincia Data Center Recertification,” Uptime Institute Case Study, uptimeinstitute.com

Argentina Facility Management Industry Leaders

CBRE Group Inc.

ISS Facility Services Argentina S.A.

Cushman & Wakefield S.R.L.

Sodexo Argentina S.A.

Grupo EULEN Argentina S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: YPF and Petronas selected Río Negro for a USD 30-50 billion LNG complex, signaling large-scale technical FM demand during construction and operations.

- May 2025: Hyatt Hotels Corporation unveiled the Casa Duhau luxury project in Mendoza, opening specialized FM opportunities for premier hospitality assets.

- March 2025: Sodexo reported 3.5% organic revenue growth in the first half of fiscal 2025 and secured a seven-year GBP 137.2 million annual contract with the UK Department of Work and Pensions.

- January 2025: CBRE Group acquired Industrious National Management Company and formed the Building Operations & Experience segment, creating a USD 20 billion annual revenue platform with integrated workplace and facility services.

Argentina Facility Management Market Report Scope

Facility Management Services are essential for the effective operation of the business as they ensure smooth functioning of an organization and assist them in focusing on core business competence. Organizations are outsourcing these services from facility management companies that provide cost-effective solutions.

The Argentina facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Argentina facility management market?

The market stands at USD 26.02 billion in 2026 and is projected to reach USD 31.02 billion by 2031.

Which service type is expanding the fastest?

Smart-asset hard services deliver the highest growth at an 8.62% CAGR through 2031.

Why are outsourced facility services gaining traction?

Corporations are shifting toward variable-cost structures and tapping external expertise, pushing outsourced contracts to a 9.18% CAGR.

Which end-user segment leads growth prospects?

Healthcare facilities are expected to rise at a 7.54% CAGR owing to modernization and stringent hygiene standards.

How significant is Buenos Aires within the national market?

The capital region generates roughly 59.40% of total facility-management revenues, though secondary cities now exhibit higher growth rates.

Page last updated on: