Collision Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

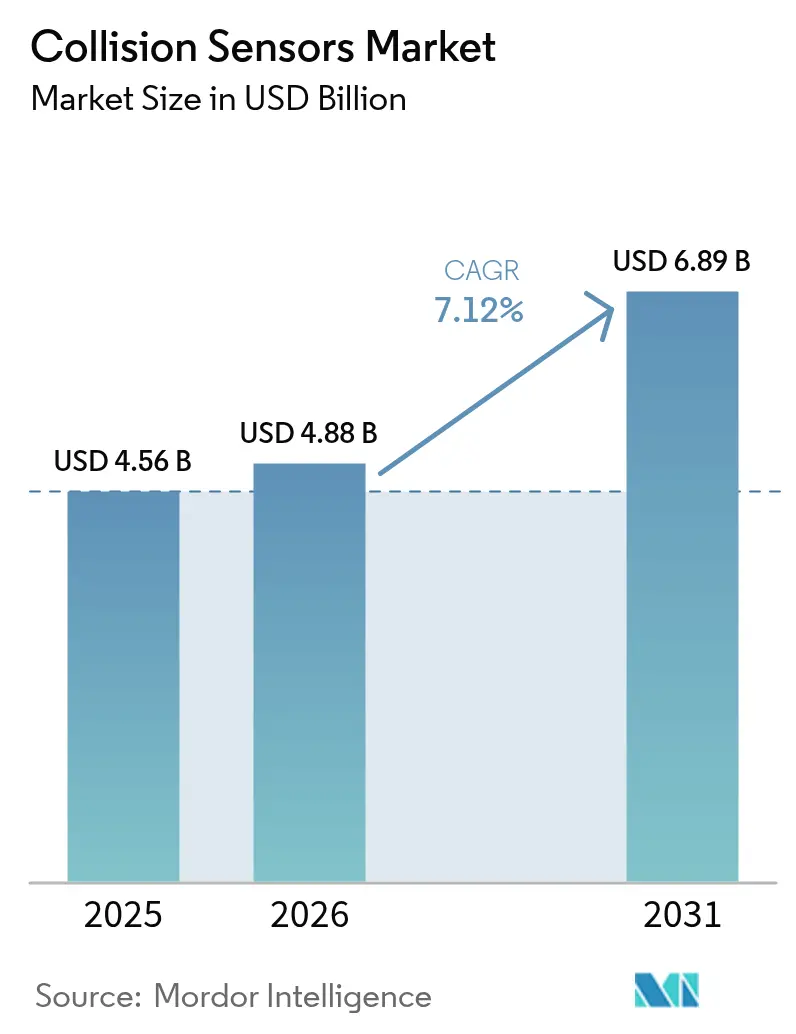

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 6.89 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Collision Sensors Market Analysis by Mordor Intelligence

The collision sensors market size is expected to grow from USD 4.56 billion in 2025 to USD 4.88 billion in 2026 and is forecast to reach USD 6.89 billion by 2031 at 7.12% CAGR over 2026-2031. Heightened safety mandates, the rapid proliferation of Level 2-plus autonomy, and falling solid-state LiDAR prices are reinforcing demand as OEMs redesign vehicle electrical architectures around multi-sensor fusion. The United States, Europe, and China now require or strongly encourage the use of automatic emergency braking (AEB) and pedestrian detection, persuading automakers to standardize radar–camera hybrids even on entry-level trims. Mature 77 GHz radar supply chains still dominate, but LiDAR specialists cut unit costs below USD 500 in 2025, unlocking mid-tier adoption. Autonomous mobile robot deployments in logistics and defense retrofit programs add non-automotive growth runways, while cybersecurity and adverse-weather reliability remain headwinds that suppliers must address with redundant architectures.

Key Report Takeaways

- By application, adaptive cruise control led with 38.35% of the collision sensors market share in 2025; automatic emergency braking is advancing at an 7.71% CAGR through 2031.

- By technology, radar captured a 62.15% share of the collision sensor market size in 2025, whereas LiDAR is forecast to accelerate at an 8.45% CAGR through 2031.

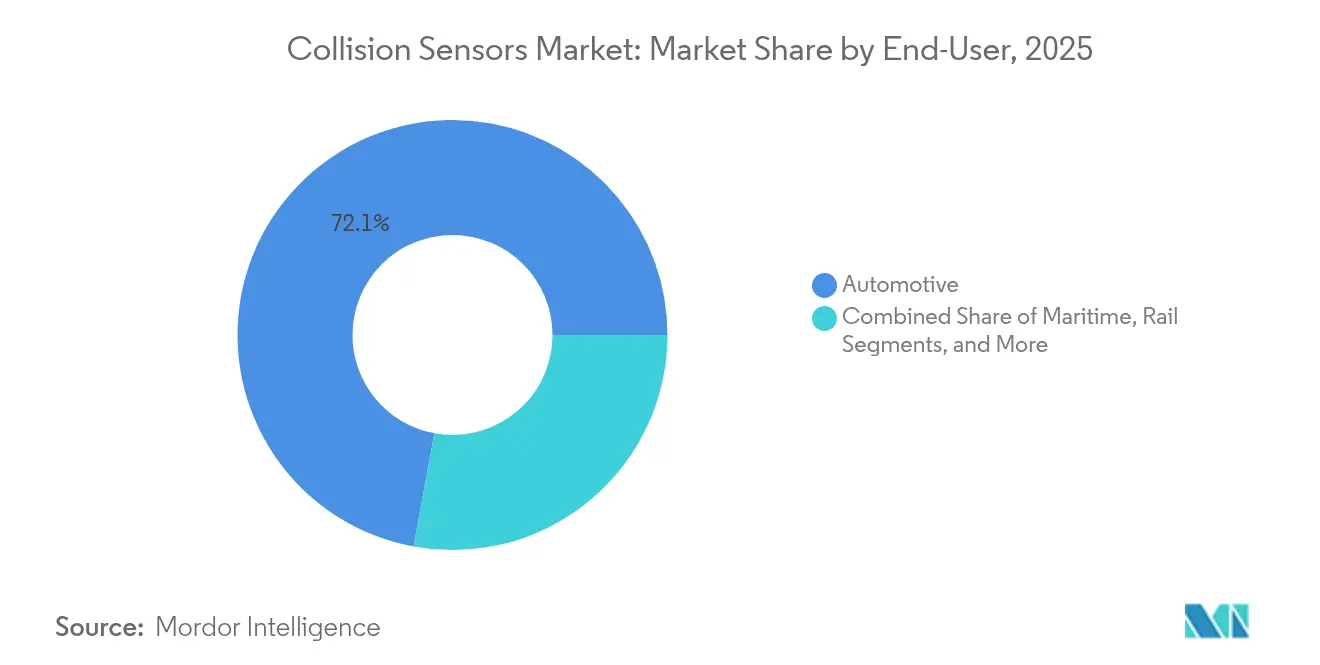

- By end-user, the automotive sector commanded 72.10% of the revenue in the collision sensors market in 2025; industrial robotics is expected to expand at a 8.88% CAGR from 2026 to 2031.

- By autonomy level, Level 2-3 systems held 49.35% of the collision sensors market in 2025, while Level 4-5 platforms are poised for an 8.02% CAGR to 2031.

- By geography, North America dominated with 45.20% revenue in 2025 in the collision sensors market; Asia-Pacific is tracking an 8.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Collision Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enhanced automotive safety regulations | +1.8% | Global, early in North America, Europe, China | Short term (≤ 2 years) |

| Rapid ADAS and autonomous-driving rollout | +2.1% | North America, Europe, China, Japan | Medium term (2-4 years) |

| Falling solid-state LiDAR cost curve | +1.3% | Global, volume in China, North America | Medium term (2-4 years) |

| V2X-enabled predictive collision alert | +0.9% | North America, Europe, China | Long term (≥ 4 years) |

| Electrified-vehicle production surge | +1.0% | Global, led by China, Europe, North America | Medium term (2-4 years) |

| Military retrofit programs for legacy fleets | +0.4% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enhanced Automotive Safety Regulations

Regulators in the United States finalized a rule in 2024 that requires pedestrian AEB on new passenger vehicles by 2029, prompting OEMs to integrate thermal or near-infrared cameras with millimeter-wave radar, incurring an additional USD 120–180 in bill-of-materials costs. Insurers reward this investment through 8–12% premium discounts.[1]National Highway Traffic Safety Administration, “AEB Technology Mandate,” nhtsa.gov Euro NCAP’s 2024 protocol withholds five-star ratings from models lacking cyclist protection at urban intersections, accelerating the rollout of corner radar. China’s C-NCAP added vulnerable-road-user scoring in 2024, prompting domestic suppliers to combine low-cost ultrasonic sensors with radar to keep sedans under strict price ceilings. India drafted mandates that retrofit 1.2 million heavy trucks with forward-collision warning by 2028, while Japan subsidizes aftermarket kits for vehicles older than 10 years.

Rapid ADAS and Autonomous-Driving Rollout

Waymo surpassed 2 million paid robotaxi rides after expanding to Los Angeles and Austin in late 2024, proving Level 4 scalability once sensor suites marry long-range LiDAR with imaging radar. Tesla shipped FSD v12.5 to 1.8 million cars, relying on cameras only, but critics question redundancy during complex edge cases. Mercedes-Benz secured Level 3 approval in California and Nevada using stereo cameras plus LiDAR at speeds up to 40 mph, shifting liability from driver to OEM. China’s 2026 Level 2 ADAS mandate equips roughly 28 million vehicles annually, solidifying a captive sensor market for Huawei and Desay. GM’s 2025 integration of Mobileye EyeQ6 Lite targets sub-USD 200 camera-radar fusion to counter Tesla’s vision-only path

Falling Solid-State LiDAR Cost Curve

Hesai slashed the AT128 price by half in January 2025 to USD 500, reaching a crossover where LiDAR can be optioned on mid-tier vehicles. Volume gains stem from 905 nm VCSEL arrays on 8-inch silicon wafers that deliver 40% higher photon efficiency. Luminar, Innoviz, and Continental each locked sub-USD 1,000 unit pricing for series production, while Valeo shipped 150,000 scanning modules to Chinese OEMs in 2024.

V2X-Enabled Predictive Collision Alert

A U.S. Notice of Proposed Rulemaking in 2024 proposes mandating V2X radios on light-duty vehicles by 2028, thereby extending the collision-alert range beyond the reach of on-board sensors. Qualcomm and Michigan DOT trials achieved sub-100 ms latency for intersection warnings. China plans to install roadside C-V2X on 10,000 km of highways by the end of 2024. ETSI has updated ITS-G5 to support cooperative perception, allowing vehicles to share raw sensor packets. Autoliv embedded V2X receivers into its radar-camera fusion module, eliminating the need for extra hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM cost for multi-sensor fusion | -1.2% | Global, acute in India, SE Asia, Latin America | Short term (≤ 2 years) |

| Reliability limits in snow, fog and debris | -0.8% | North America, Northern Europe, mountains | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.6% | Global, 77 GHz radar and image sensors | Short term (≤ 2 years) |

| Cyber-security exposure of sensor networks | -0.5% | Global, regulation in Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High BOM Cost for Multi-Sensor Fusion

Full radar-camera-LiDAR stacks add USD 600–1,200 to vehicles, limiting penetration in price-sensitive markets. Tier-one ECUs account for up to 45% of ADAS hardware cost because they need high-performance SoCs. Maruti Suzuki postponed Level 2 ADAS on compact sedans in 2024 to avoid breaching key price thresholds. Fleet buyers often forgo hands-free options in favor of payload and fuel economy, and Stellantis reported sub-15% ADAS take-up across Southern Europe and South America.

Reliability Limits in Snow, Fog and Debris

Camera accuracy drops by up to 60% in snow or fog, and radar maintains range but creates clutter from spray. Bosch documented false positives and is refining signal processing. Velodyne introduced heated LiDAR lenses for operation down to −40 °C. Continental invested EUR 120 million in self-cleaning radomes that use ultrasonic vibration to shed debris. Aftermarket heated camera mounts are proliferating in Nordic EV communities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: AEB Gains as Insurers Reward Crash Prevention

In 2025, adaptive cruise control commanded a dominant 38.35% share of the collision sensors market, while automatic emergency braking is projected to grow at an 7.71% CAGR, continuing through 2031. Insurance incentives worth 8–12% of premiums and U.S. federal mandates catalyze uptake, while forward-collision warning remains bundled with AEB in most regions. Blind-spot monitoring already exceeds a 60% fitment rate in North America and Europe, but growth is slowing now that the feature is standard. Ultrasonic parking sensors face pressure from surround-view cameras, suppliers react by adding automated-parking software to preserve value.

Other advanced functions, including pedestrian and cyclist detection, are rapidly gaining popularity in dense urban markets. Euro NCAP credits for motorcycle intersection protection force OEMs to integrate corner radar and wide-angle cameras. Volvo’s City Safety system cut insurance claims by 28%, validating ROI for vulnerable-road-user solutions. Denso’s compact radar module targets India’s vast two-wheeler market, opening up a new adjacency.

By Technology: LiDAR Narrows Gap as Solid-State Costs Halve

Radar retained 62.15% revenue in 2025 thanks to year-round reliability and supply maturity, but LiDAR’s 8.45% forecast CAGR will chip away as sub-USD 500 solid-state units become attainable for mass-market trims. Cameras gain from high-resolution CMOS sensors yet remain sensitive to low light, limiting solo use beyond Level 2. Ultrasonic sensors continue to dominate low-speed maneuvers due to their low cost. Infrared modules for night pedestrian detection and MEMS pressure sensors, which bridge the gap between passive and active safety, drive niche growth.

Bosch shipped more than 100 million radar units in 2024, leveraging SiGe transceivers and antenna-in-package designs. Continental’s fifth-generation short-range radar is expected to deliver 4-degree azimuth resolution at a sub-USD 40 price point by 2026. Omnivision launched a 5MP sensor with 140 dB dynamic range, improving tunnel-exit performance. Murata raised the ultrasonic output 40% to serve Chinese EVs

By End-User: Industrial Robotics Outpaces Automotive Growth

Automotive accounted for 72.10% of 2025 revenue, while warehouse automation drives industrial robotics to a 8.88% CAGR, surpassing overall collision sensor market growth. Amazon alone operates 750,000 autonomous mobile robots, each laden with LiDAR and ultrasonics. Aerospace, maritime and rail consume fewer units but command USD 2,000–5,000 sensor modules under harsh-environment specs.

Passenger cars still account for the largest volumes, while light commercial vehicles are rising the fastest as last-mile delivery fleets seek lower insurance premiums. Heavy trucks integrate radar-camera fusion to meet Euro VII idle penalties. Agriculture and construction machinery adopt ultrasonics to cut job-site accidents amid stricter safety rules.

By Vehicle Autonomy Level: Level 4-5 Pipelines Drive Sensor Complexity

Level 2-3 systems contributed 49.35% of the collision sensor market in 2025, mirroring the mass adoption of Highway-Assist. Waymo’s sixth-generation suite combines 29 cameras, six LiDARs and five radars to sustain perception despite occlusion, underscoring the complexity required for Level 4. Level 4-5 CAGR stands at 8.02% as Cruise, Zoox, and Aurora scale freight pilots.

Liability hand-off and redundancy drive bills of material beyond USD 1,500 per vehicle. GM’s Super Cruise already spans 400,000 miles of mapped roads, charging users a subscription after the trial. Chinese OEMs launch comparable navigation-on-pilot features to differentiate EVs in a crowded market.

Geography Analysis

North America contributed 45.20% of the 2025 revenue, as AEB mandates and premium-vehicle penetration created the world’s largest collision sensor market. Consumers are willing to pay USD 1,500–2,500 for Level 2-plus bundles, and insurers reward forward-collision warning systems with lower premiums. Canada aligns its standards with those of the NHTSA for a 2028 deadline, while Mexico’s domestic sales grow as safety awareness increases. Semiconductor allocations continue to favor the region’s premium OEMs during shortages, thereby reinforcing supply resilience.

The Asia-Pacific region is set for an 8.16% CAGR, the highest regional growth rate. China’s 2026 Level 2 mandate affects 28 million annual vehicles, ensuring a large captive base for domestic radar and camera suppliers. India plans to retrofit 1.2 million heavy trucks with forward-collision warning systems by 2028, and the six-airbag rules have already lifted the sensor content per vehicle. Japan, South Korea and Taiwan exploit optics and packaging expertise to export LiDAR modules, while ASEAN nations start with ultrasonic parking sensors before ascending the technology ladder.

Europe captured roughly 27% share in 2025 on the back of Euro NCAP’s influential five-star criteria and the EU General Safety Regulation that requires AEB and lane-keeping assist on all new models from 2024 onward. Germany’s supplier triad, Bosch, Continental and ZF, keeps value in-region through vertical integration. The Netherlands pilots V2X cooperative perception across 2,000 km of highways, while France and Italy expand electric-vehicle incentives that also mandate advanced safety functions.

South America plus the Middle East and Africa form a nascent market below 10% revenue. Brazil enforces electronic stability control and rear cameras, positioning for future collision-sensor uptake. Gulf states deploy premium sensor suites in smart-city pilots, and South Africa installs sensors mainly for export models bound for Europe.

Competitive Landscape

Continental, Bosch, Denso, and ZF held an estimated 55% share in 2024, underscoring a moderately consolidated market for collision sensors. Their vertical integration, including transceivers, camera modules, and sensor-fusion ECUs, offers OEMs turnkey solutions and guarantees a global supply. Mobileye disrupted the camera space by pricing its SuperVision package at USD 1,200 in China, winning contracts with Geely and Nio. Hesai, Luminar, and Innoviz leverage steep LiDAR cost curves to pitch full perception stacks, shifting emphasis from hardware to data services.

Semiconductor vendors like NXP and Infineon command bargaining power by controlling radar processors and microcontrollers with built-in cybersecurity, as ISO/SAE 21434 requires encryption and intrusion detection across external sensors. Allocation decisions in 2024 favored premium OEMs, delaying mid-tier vehicle launches. Suppliers diversify with in-house wafer fabs (Bosch Dresden) and joint ventures (Continental–Qualcomm) to secure critical components.

White-space opportunities center on aftermarket retrofit kits for aging commercial fleets where operators seek crash avoidance without buying new vehicles. Software-defined stacks allow over-the-air upgrades that boost detection accuracy, a capability Tesla monetized in 2024. Patent filings show Aptiv developing machine-learning fault isolation to keep Level 3 features active even when one sensor type is impaired.

Collision Sensors Industry Leaders

Continental AG

NXP Semiconductors N.V.

Delphi Automotive LLP

Infineon Technologies AG

Murata Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zoox began commercial robotaxi operations in Las Vegas using purpose-built vehicles with bi-directional sensor arrays, eliminating the need for a human safety driver and reducing per-mile operating costs by an estimated 30% compared to retrofitted platforms.

- March 2025: Hesai Technology announced a USD 150 million expansion of its solid-state LiDAR production facility in Shanghai, targeting annual capacity of 1 million units by 2027 to meet demand from Chinese OEMs and autonomous-vehicle developers. The investment includes automated assembly lines and in-house production of VCSEL arrays, reducing per-unit costs below USD 400 and positioning Hesai to compete with incumbent radar suppliers on price.

- February 2025: Continental AG and Qualcomm Technologies formed a joint venture to develop integrated radar-V2X modules for commercial vehicles, combining 77 GHz radar with C-V2X direct communication to enable predictive collision warnings in connected corridors. The partnership targets series production in 2027 and aims to reduce bill-of-materials costs by 25% compared to standalone systems.

- January 2025: General Motors announced a USD 500 million investment to establish a dedicated ADAS sensor production line in Michigan, targeting 5 million radar and camera modules annually to supply its Chevrolet, GMC and Cadillac lineups with Level 2+ capabilities by 2028. The facility will employ 1,200 workers and leverage vertical integration of image sensors and radar transceivers to reduce reliance on external suppliers.

Global Collision Sensors Market Report Scope

Collision sensors are placed within a car which provides a warning to the driver if there are any dangers that lie ahead on the road. These sensors include how close the car is to other cars, how much its speed needs to be reduced when obstacles closer to the car, how close the car going off the road, and the system consists of audio warning to prompt the driver, initiates braking if the driver fails to respond to the warning.

The Collision Sensors Market Report is Segmented by Application (Adaptive Cruise Control, Forward Collision Warning, Blind Spot Monitoring, Lane Departure Warning, Parking Sensors, Rear Cross-Traffic Alert, Automatic Emergency Braking, Other Applications), Technology (Ultrasonic, Radar, Camera/Vision, LiDAR, Infra-red, Pressure/MEMS), End-User (Automotive [Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles], Aerospace and Defense, Maritime, Rail, Industrial Robotics, Other End-Users), Vehicle Autonomy Level (Level 0-1, Level 2-3, Level 4-5), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Adaptive Cruise Control |

| Forward Collision Warning |

| Blind Spot Monitoring |

| Lane Departure Warning |

| Parking Sensors |

| Rear Cross-Traffic Alert |

| Automatic Emergency Braking |

| Other Applications |

| Ultrasonic |

| Radar |

| Camera / Vision |

| LiDAR |

| Infra-red |

| Pressure / MEMS |

| Automotive | Passenger Vehicles |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Aerospace and Defense | |

| Maritime | |

| Rail | |

| Industrial Robotics | |

| Other End-Users |

| Level 0-1 |

| Level 2-3 |

| Level 4-5 |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Adaptive Cruise Control | ||

| Forward Collision Warning | |||

| Blind Spot Monitoring | |||

| Lane Departure Warning | |||

| Parking Sensors | |||

| Rear Cross-Traffic Alert | |||

| Automatic Emergency Braking | |||

| Other Applications | |||

| By Technology | Ultrasonic | ||

| Radar | |||

| Camera / Vision | |||

| LiDAR | |||

| Infra-red | |||

| Pressure / MEMS | |||

| By End-User | Automotive | Passenger Vehicles | |

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Aerospace and Defense | |||

| Maritime | |||

| Rail | |||

| Industrial Robotics | |||

| Other End-Users | |||

| By Vehicle Autonomy Level | Level 0-1 | ||

| Level 2-3 | |||

| Level 4-5 | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the collision sensors market?

The collision sensors market size stands at USD 4.88 billion in 2026.

How fast is demand expected to grow?

Market revenue is forecast to climb to USD 6.89 billion by 2031, equivalent to a 7.12% CAGR.

Which application is expanding the quickest?

Automatic emergency braking posts the fastest growth at an 7.71% CAGR through 2031, driven by regulatory mandates and insurance incentives.

Why are LiDAR prices falling sharply?

Suppliers moved to 905 nm VCSEL arrays on larger silicon wafers, doubling output and halving the AT128 unit price to roughly USD 500.

Which region offers the highest growth upside?

Asia-Pacific is projected for the strongest regional CAGR at 8.16% thanks to China’s compulsory Level 2 ADAS rule commencing in 2026.

Page last updated on: