Traffic Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

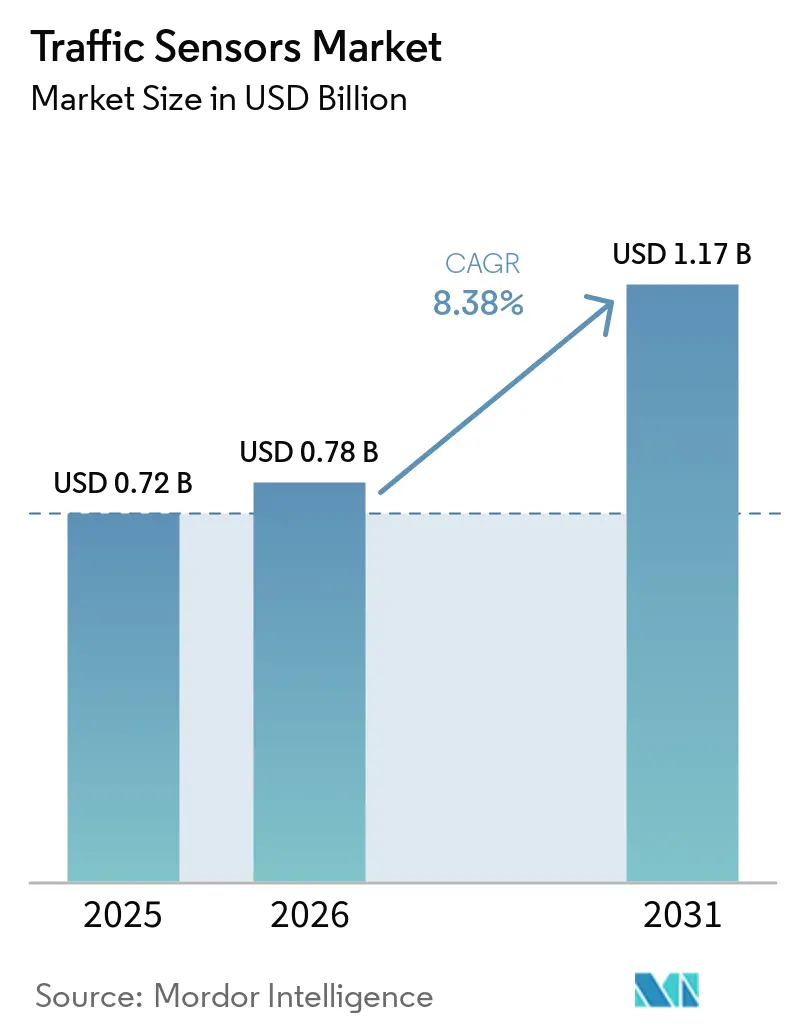

| Market Size (2026) | USD 0.78 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Traffic Sensors Market Analysis by Mordor Intelligence

The traffic sensors market size is expected to grow from USD 0.72 billion in 2025 to USD 0.78 billion in 2026 and is forecast to reach USD 1.17 billion by 2031 at 8.38% CAGR over 2026-2031. Demand rises as cities scale intelligent transportation systems to relieve congestion and cut emissions, and as national agencies lock in multi-year funding for sensor-enabled infrastructure. Statutory real-time data requirements for congestion pricing, dynamic tolling and safety programs anchor new procurement cycles, while edge-AI and 5G connectivity shift the competitive focus from stand-alone hardware to data-rich, upgrade-ready platforms. Asia-Pacific leads adoption on the back of China’s and Japan’s large-scale smart-city pilots, whereas North America prioritizes retrofits that minimize lane closures. Vendors able to bundle non-intrusive detection, predictive analytics and open-standards communications secure the widest addressable base, especially as governments press for multi-modal coverage that includes pedestrians and micromobility devices.

Key Report Takeaways

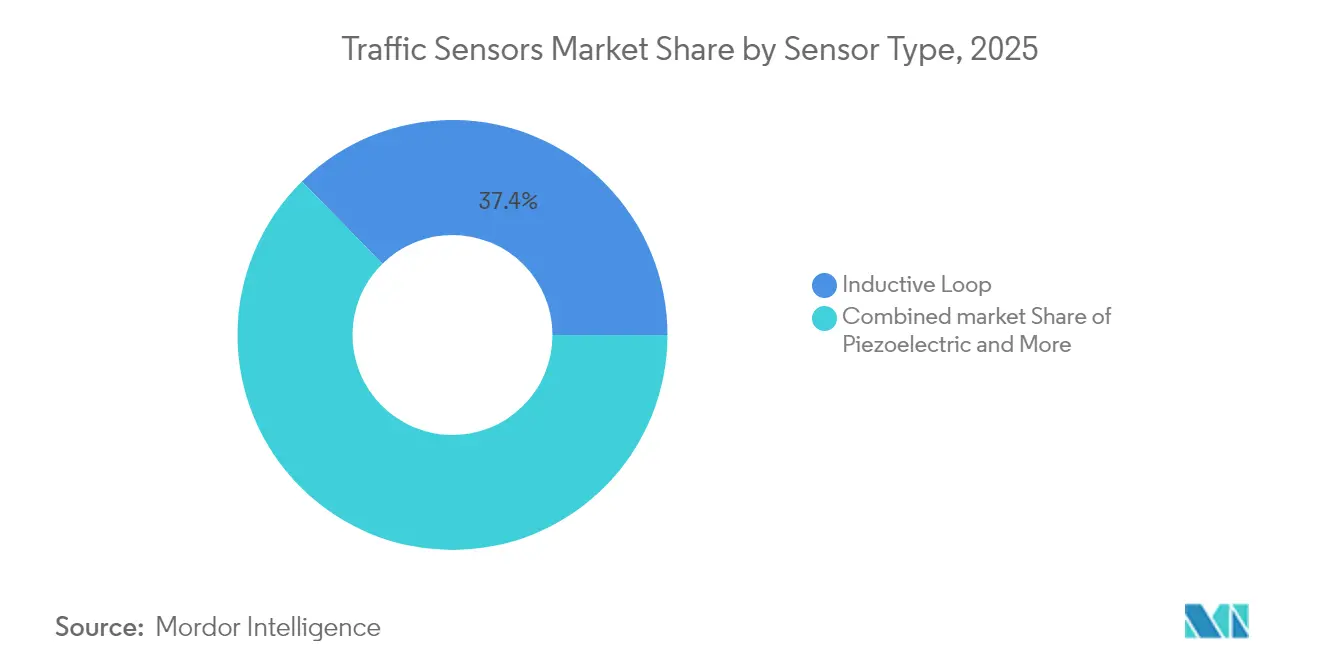

- By sensor type, inductive loops held 37.35% of traffic sensors market share in 2025; LiDAR is forecast to record the fastest 12.02% CAGR to 2031.

- By installation method, intrusive deployments retained 53.40% revenue share in 2025, while portable systems are projected to expand at a 11.84% CAGR.

- By application, traffic monitoring commanded 45.50% of the traffic sensors market size in 2025; incident detection is advancing at an 11.62% CAGR.

- By deployment location, urban intersections led with 40.55% share; bridge and tunnel projects deliver the highest 12.32% CAGR outlook.

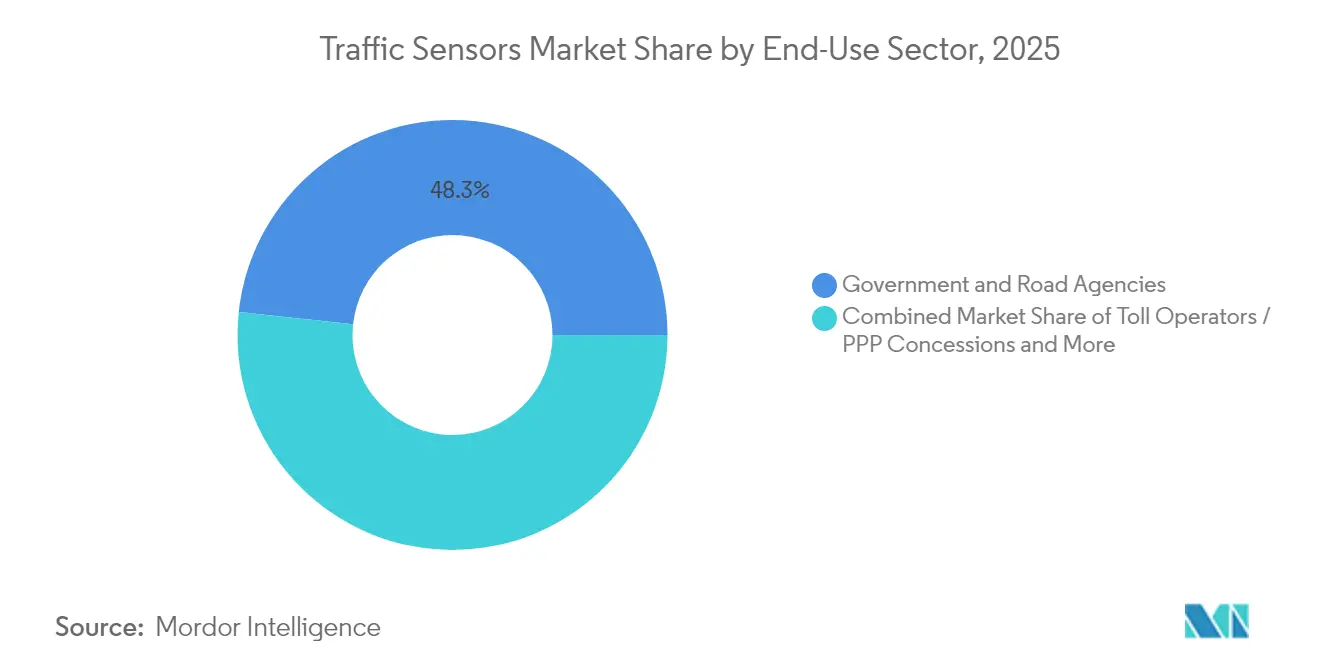

- By end-use sector, government and road agencies accounted for 48.30% share; smart-city integrators post a 12.39% CAGR through 2031.

- By connectivity, wired links made up 42.40% of 2025 revenue, yet cellular-IoT solutions are growing at 13.16% CAGR.

- By geography, Asia-Pacific contributed 34.70% revenue in 2025 and remains the fastest-growing region at 11.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Traffic Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanisation and Congestion Pressure | +1.8% | Global, strong in APAC megacities | Medium term (2–4 years) |

| Smart-City and ITS Funding Surge | +2.1% | North America and EU core, expanding to APAC | Short term (≤ 2 years) |

| Mandated Real-Time Data for Tolling and Congestion Pricing | +1.5% | North America & EU, pilots in APAC | Medium term (2–4 years) |

| Electrification-Linked Grid-Aware Traffic Management | +1.3% | Europe, China, and advanced EV-adoption corridors | Medium term (2–4 years) |

| Edge-AI Low-Power Non-Intrusive Sensors | +1.4% | Global, led by North America and EU innovation hubs | Long term (≥ 4 years) |

| Multimodal Micromobility Detection Standards | +1.1% | Urban centers in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanisation & Congestion Pressure

Metropolitan congestion costs New York USD 20 billion each year, prompting large-scale sensor roll-outs that shorten travel times by as much as 25% and trim CO₂ output up to 20% trafficmobilityreviewboard. Federal Highway Safety Improvement funds of USD 3.4 billion embed detection into roadway upgrades to cut fatalities.[1]Federal Highway Administration, “Budget Estimates Fiscal Year 2025” FHWA, fhwa.dot.gov China’s nearly 800 smart-city pilots further accelerate deployments that span vehicles, pedestrians and micromobility users, broadening the traffic sensors market beyond road vehicles alone[2].Central Committee of the Communist Party of China, “Opinions on Promoting New Urban Infrastructure”, State Council PRC gov.cn

Smart-City & ITS Funding Surge

The USD SMART Grants program disbursed USD 50 million across 34 projects in 2024, setting precedents for sensor-rich intersections and edge servers .[3]U.S. Department of Transportation, “SMART Grants Program”, U.S. DOT, transportation.govHorizon Europe earmarked EUR 254 million (USD 276 million) to digital transport infrastructure that mandates interoperable detection. City-level initiatives, such as Alexandria’s USD 5 million smart-mobility plan, confirm that funding is cascading rapidly to municipal procurement

Mandated Real-Time Data for Tolling & Congestion Pricing

New York’s congestion pricing program relies on automated camera and weigh-in-motion arrays to generate USD 15 billion for transit modernization. Federal spectrum waivers accelerate cellular V2X pilots in Utah and Virginia, underpinning sensor demand for toll collection with sub-second latency . Lane-specific dynamic pricing has spread to 41 U.S. corridors, each requiring robust sensors for axle-based billing accuracy

Edge-AI Low-Power Non-Intrusive Sensors

Tennessee’s AI-enhanced fusion engine improved detection accuracy by 5% compared with legacy models. FLIR’s multispectral TrafiBot integrates thermal and visual imaging with embedded AI to address tunnel and bridge hazards. Edge processing cuts backhaul costs and shields sensitive data, a decisive benefit for European operators subject to strict privacy laws

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Skilled Talent Pool | -2.2% | Global, especially emerging markets | Short term (≤ 2 yrs) |

| Security and Compliance Complexities | -3.1% | Global, acute in regulated sectors | Medium term (2-4 yrs) |

| Control-Plane Cost Escalation under Autoscaling | -1.5 % | Global | Medium term (2-4 yrs) |

| Hyperscaler Dominance Limits OSS Monetisation | -1.0 % | Global | Long term (≥ 4 yrs) |

| Source: Mordor Intelligence | |||

High Up-Front Deployment CAPEX

ITS America estimates USD 6.5 billion is needed to equip 250,000 U.S. intersections with V2X technology, a burden intensified by paving, labor and maintenance costs . Developing economies face financing gaps that delay roll-outs, although low-cost wireless nodes such as Oklahoma’s USD 40 prototype ease entry barriers Contracts like Rhode Island’s USD 2.759 million bridge monitoring deal highlight the sizable capital commitment even for individual assets

Data-Privacy & Cyber-Security Compliance Costs

The EU AI Act introduces traceability rules that raise development overhead for intelligent traffic platforms . U.S. GAO reports cite privacy as a top barrier, forcing agencies to invest in encryption, authentication and continuous monitoring. Divergent DSRC and C-V2X standards amplify testing expenses and prolong procurement cycles

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: LiDAR Disrupts Legacy Detection

Inductive loops retained 37.35% traffic sensors market share in 2025, yet LiDAR’s 12.02% CAGR signals a pivot to non-intrusive, high-resolution mapping. The traffic sensors market size attached to LiDAR solutions is projected to outpace loops as operators seek vehicle classification and pedestrian safety in one package. Seyond’s system posts 99% vehicle accuracy and 92% pedestrian recognition, outperforming loop-based alternatives simpl.. Radar and thermal imaging complement LiDAR in adverse weather, while piezoelectric arrays remain vital for weigh-in-motion. Edge-ready sensors that combine modalities collect richer data with lower lifecycle cost, a priority under federal SMART guidance

LiDAR’s upward curve is reinforced by falling component prices, smaller form factors and automotive-grade reliability. Traditional loops struggle with pavement wear and lane additions, and their inability to detect cyclists limits suitability for multimodal grids. Infrared and magnetometer solutions hold niche roles where cost or site constraints dictate. A diverse supplier ecosystem is emerging, yet integration skill remains a differentiator as agencies favor turnkey analytics over raw feed delivery.

By Installation Method: Portable Systems Gain Momentum

Intrusive installs made up 53.40% revenue in 2025 as legacy loops dominate signalized junctions, but portable sensors are forecast for 11.84% CAGR. The traffic sensors market increasingly rewards quick-deploy, solar-powered units that avoid lane closures and asphalt cutting. Oklahoma’s USD 40 wireless node underscores cost competitiveness even for cash-constrained districts. Portable LiDAR kits now underpin work-zone situational awareness, easing contractor compliance with safety mandates.

Traffic managers prioritize flexibility to realign sensors with construction phases, events or pop-up bus lanes. Non-intrusive over-road gear delivers multi-lane coverage and diagnostics without disturbing pavement integrity. Long-term, loop retrofits shift toward radar-camera combos delivering higher data fidelity and lower lifetime spend.

By Application: Incident Detection Rises in Priority

Traffic monitoring captured 45.50% revenue in 2025, yet incident detection sits on an 11.62% CAGR curve as safety targets tighten. The traffic sensors market size tied to wrong-way driving mitigation alone is rising fast after thermal-AI solutions demonstrated sharp false-alarm reductions. Weigh-in-motion additions like the Brooklyn-Queens Expressway deployment cut overweight truck violations by 50% within one month.

Real-time video analytics combined with on-edge processing enables sub-second alerts to traffic control centers. Vehicle classification data supports tiered tolling, congestion pricing and freight policy enforcement, cementing sensors as revenue-enabling assets rather than cost centers.

By Deployment Location: Bridges and Tunnels Accelerate

Urban intersections held 40.55% of 2025 spend, but bridge and tunnel sites show the strongest 12.32% CAGR. Structural health monitoring and early fire detection requirements merge with traffic sensing, prompting integrated bids such as Rhode Island’s USD 2.759 million Washington Bridge contract. Sensors in confined tunnel environments must resist humidity, dust and vibration, favoring ruggedized, multispectral units. Highway lanes continue to demand axle-classifying accuracy for toll revenue assurance, while parking facilities deploy occupancy sensors that feed mobile payment platforms.

By End-Use Sector: Smart-City Integrators Lead Growth

Government agencies still represent 48.30% revenue, yet smart-city integrators enjoy the fastest 12.39% CAGR as municipalities outsource design-build-operate contracts. The traffic sensors market rewards vendors that bundle hardware, cloud analytics and maintenance into outcome-based service level agreements. Public-private partnerships, such as New York’s Smart Cities Innovation Partnership, funnel grants toward integrated sensor-platform packages.

Toll-road concessionaires sustain stable replacement cycles, emphasizing metrological certification for revenue grade accuracy. Logistics firms demand portable counting kits that align with fleet telematics to optimize routing.

By Connectivity Technology: Cellular-IoT Takes the Lead

Wired Ethernet and CAN buses secured 42.40% revenue in 2025, but cellular-IoT segments expand at 13.16% CAGR. The traffic sensors market share for cellular links is rising as 5G roll-outs and C-V2X chipsets mature. U.S. DOT’s USD 60 million pilot program for nationwide V2X relies on cellular low-latency channels suited for multimodal data. LoRa and Sigfox address battery-powered remote stations, while DSRC maintains a foothold in select corridors pending spectrum reallocation.

Geography Analysis

Asia-Pacific generated 34.70% 2025 revenue and posts a 11.93% CAGR through 2031. China’s smart-city pilots, anchored in the Made in China 2025 program, keep urban infrastructure budgets flowing toward AI-enabled detection. Japan’s advanced traffic systems sector targets USD 7.239 billion by 2033 as Ministry-approved projects integrate flow prediction and visualization. India’s USD 1.4 trillion National Infrastructure Pipeline underlines rising demand for multimodal logistics monitoring .

North America commands mature install bases yet continues to invest in retrofit upgrades. USD 100 million annual SMART allocations and congestion pricing in New York spur edge-ready replacements. Retrofit-friendly, non-intrusive sensors dominate procurements that must minimize lane closures. Canada modernizes corridor management through federal-provincial cost sharing, whereas Mexico focuses on freight corridors linked to USMCA trade flows.

Europe links sensor projects to decarbonization targets. Horizon Europe and the EUR 1 billion Connected, Cooperative and Automated Mobility program fund multi-modal detection interoperability. Germany and the UK channel funds into rail and high-speed roadways that embed next-gen sensors suitable for future autonomous deployment. Middle East and Africa exhibit selective adoption tied to flagship smart-city schemes, though oil-exporting states fund toll and weigh-in-motion networks to safeguard heavy-load corridors.

Competitive Landscape

The sector shows moderate concentration: top five players hold near-60% combined revenue, underpinned by multi-year concessions. Siemens Mobility secured EUR 2.8 billion (USD 3.0 billion) German rail control deals, adding an MRT maintenance contract in Malaysia and HS2 packages in Britain, thereby extending lifecycle revenue and regional footprint. Iteris’ USD 335 million buy-out by Almaviva highlights private equity appetite for data-rich mobility assets and signals continued consolidation.

Technology differentiation pivots on AI embedded at the edge. FLIR’s TrafiBot marries thermal and visual channels with machine learning to widen use cases from incident detection to early fire warning . Kistler’s combined weigh-in-motion and structural monitoring package for Washington Bridge demonstrates cross-disciplinary value creation that lifts switching barriers. Standards bodies such as ISWIM promote open data protocols that may level the field for new entrants, yet incumbents with mature integration stacks retain procurement advantages, particularly where public agencies favor single-source, long-term service contracts.

Strategic partnerships form around platform ecosystems. Yunex, Swarco and Kapsch align climate-oriented mobility offerings, combining sensor data with adaptive signal control. Chipset suppliers collaborate with infrastructure vendors to fast-track C-V2X roll-outs, cementing cellular-IoT momentum. Firms with internal analytics talent and secure cloud platforms score higher in request-for-proposal evaluations that increasingly weigh cyber-resilience and open APIs.

Traffic Sensors Industry Leaders

Kapsch TrafficCom AG

Siemens AG (Mobility ITS)

Teledyne FLIR (Traffic)

Iteris Inc.

SWARCO AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Siemens Mobility secured EUR 2.8 billion in contracts with Deutsche Bahn for modern control and safety technology as part of a EUR 6.3 billion framework agreement Siemens Mobility.

- February 2025: Siemens Mobility won a 40-month maintenance contract for the Klang Valley MRT Line in Kuala Lumpur from SMH Rail Siemens Mobility.

- January 2025: Siemens Mobility obtained four contracts worth EUR 670 million with HS2 Ltd for Britain’s high-speed rail infrastructure and maintenance Siemens Mobility.

- December 2024: China’s Central Committee issued guidelines on new urban infrastructure stressing intelligent municipal networks Central Committee of the Communist Party of China.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the traffic sensors market covers revenues generated from dedicated in-road, over-road, roadside, and portable sensing devices, such as inductive loops, piezoelectric strips, magnetometers, radar, infrared, and LiDAR units, that detect, count, weigh, or classify vehicles to feed traffic control and analytics systems.

Scope Exclusions: Cameras embedded exclusively in automatic number-plate recognition or enforcement kiosks, as well as broader smart-city software platforms without a discrete hardware sensor, fall outside this study.

Segmentation Overview

- By Sensor Type

- Inductive Loop

- Piezoelectric

- Bending Plate

- Magnetometer

- Image / Video

- Radar-Based

- Infrared

- LiDAR

- By Installation Method

- Intrusive (In-Road)

- Non-Intrusive (Over-Road / Roadside)

- Portable / Temporary

- By Application

- Traffic Monitoring and Flow Optimisation

- Weigh-In-Motion

- Vehicle Classification and Profiling

- Automated and Dynamic Tolling

- Incident Detection and Safety Analytics

- By Deployment Location

- Urban Intersections

- Highways and Expressways

- Bridges and Tunnels

- Parking Facilities

- By End-Use Sector

- Government and Road Agencies

- Toll Operators / PPP Concessions

- Smart-City Solution Integrators

- Logistics and Fleet Operators

- By Connectivity Technology

- Wired (CAN, Ethernet)

- Wireless (DSRC / C-V2X)

- Cellular-IoT (NB-IoT / LTE-M / 5G)

- LPWAN (LoRa / Sigfox)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- APAC

- China

- Japan

- India

- Australia

- Rest of APAC

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed traffic engineers at road agencies, toll-road concessionaires, and system integrators across North America, Europe, India, and the GCC. Follow-up surveys with sensor OEM product managers helped refine ASP differentials for intrusive versus non-intrusive deployments and confirm regional installation rates, bridging gaps left by desk research.

Desk Research

Our analysts first assembled a fact base from publicly available tier-1 sources such as the US Federal Highway Administration, Eurostat road freight statistics, Japan's MLIT traffic census, and UN Comtrade shipment codes for HS-class sensors. Industry associations, including ITS America and ERTICO, and peer-reviewed journals on weigh-in-motion accuracy provided adoption ratios by sensor type. Company 10-Ks, investor decks, and reputable press added average selling price (ASP) trends, while vehicle-kilometer data from national transport ministries anchored demand growth. To validate corporate revenues and installed base disclosures, we accessed D&B Hoovers, a paid database within Mordor's toolkit. This list is illustrative; many additional references informed data collection, cross-checks, and clarifications.

Market-Sizing & Forecasting

A top-down build starts with lane-kilometer stock and new-road additions, multiplied by sensor penetration factors by roadway class. Results are corroborated with selective bottom-up rolls of sampled supplier shipments and channel checks. Key variables like average sensors per signalized intersection, Weigh-In-Motion roll-out mandates, connected-vehicle penetration, and urban congestion index shifts drive the model. Forecasts to 2030 rely on multivariate regression that links those drivers to GDP per capita and public infrastructure outlays, with scenario analysis adjusting for smart-city funding volatility. When bottom-up inputs are patchy, volume gaps are back-filled using three-year moving ASP medians and regional project pipelines.

Data Validation & Update Cycle

Outputs pass anomaly screens against import data, OEM earnings, and installation tenders before senior analyst sign-off. Reports refresh annually; interim updates occur when material policy, pricing, or capacity shocks emerge, ensuring clients receive the latest vetted view.

Why Mordor's Traffic Sensors Baseline Commands Reliability

Published estimates diverge because firms vary sensor inclusion, currency timing, and refresh cadence.

Key gap drivers include: some studies merge cameras and cloud platforms with sensors, others freeze exchange rates, and several extrapolate historic counts without field validation, whereas Mordor continually revisits assumptions through live interviews and yearly model reruns.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| US $0.72 B (2025) | Mordor Intelligence | - |

| US $24.30 B (2024) | Regional Consultancy A | Bundles networked traffic management platforms and services; revenue roll-up only; no demand-side checks |

| US $0.566 B (2021) | Global Consultancy B | Omits LiDAR and cellular-IoT sensors; uses dated base year, fixed 2020 FX rates, limited geography |

In short, our disciplined scope, blended top-down-bottom-up model, and continuous primary validation give decision-makers a balanced baseline they can trace to transparent variables and repeat with confidence.

Key Questions Answered in the Report

What is the current size of the traffic sensors market?

The market stands at USD 0.78 billion in 2026 and is projected to climb to USD 1.17 billion by 2031 on an 8.38% CAGR.

Which segment grows fastest within the traffic sensors market?

LiDAR-based sensors register the highest 12.02% CAGR as operators migrate to non-intrusive, high-resolution detection.

Why are cellular-IoT links gaining traction?

National V2X plans and 5G roll-outs favor cellular’s low-latency, high-bandwidth profile, pushing the connectivity segment toward a 13.16% CAGR.

Which region leads adoption?

Asia-Pacific holds 34.70% revenue and delivers the quickest 11.93% CAGR, underpinned by China’s and Japan’s smart-city programs.

How does high capital expenditure restrain growth?

Full intersection V2X upgrades can cost billions, and pavement disruption during intrusive installs drives agencies toward portable, wireless alternatives.

Page last updated on: