Size and Share of Sensor Fusion Market in Autonomous Vehicles

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

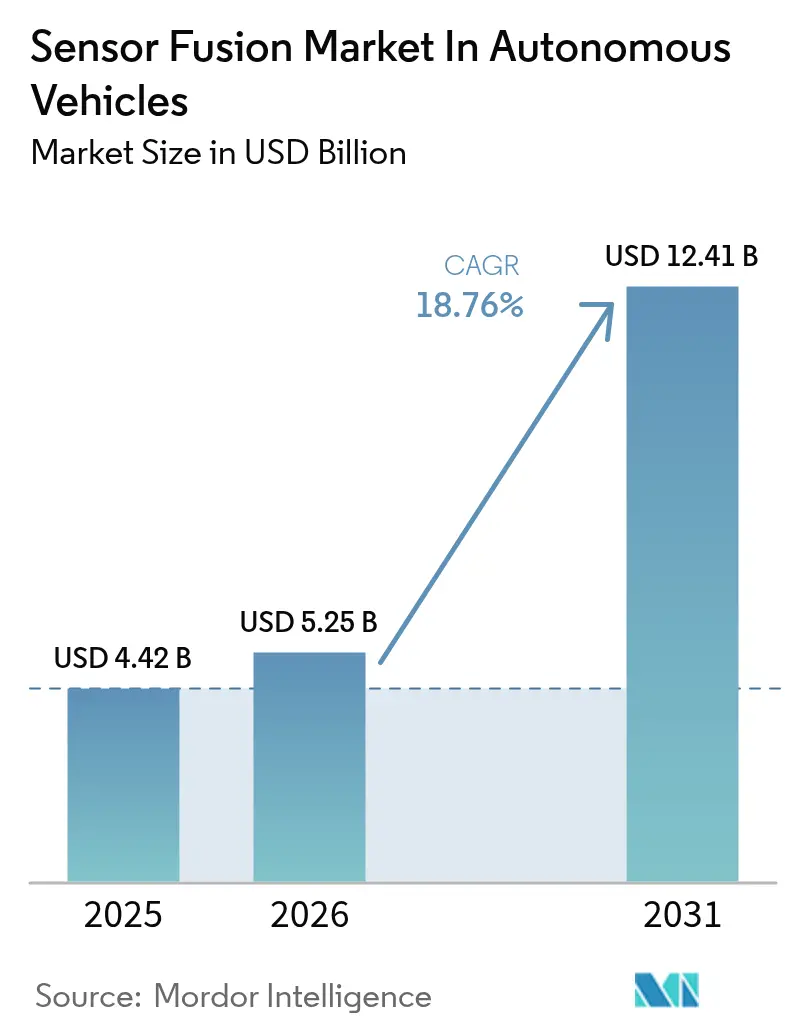

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 18.76% CAGR |

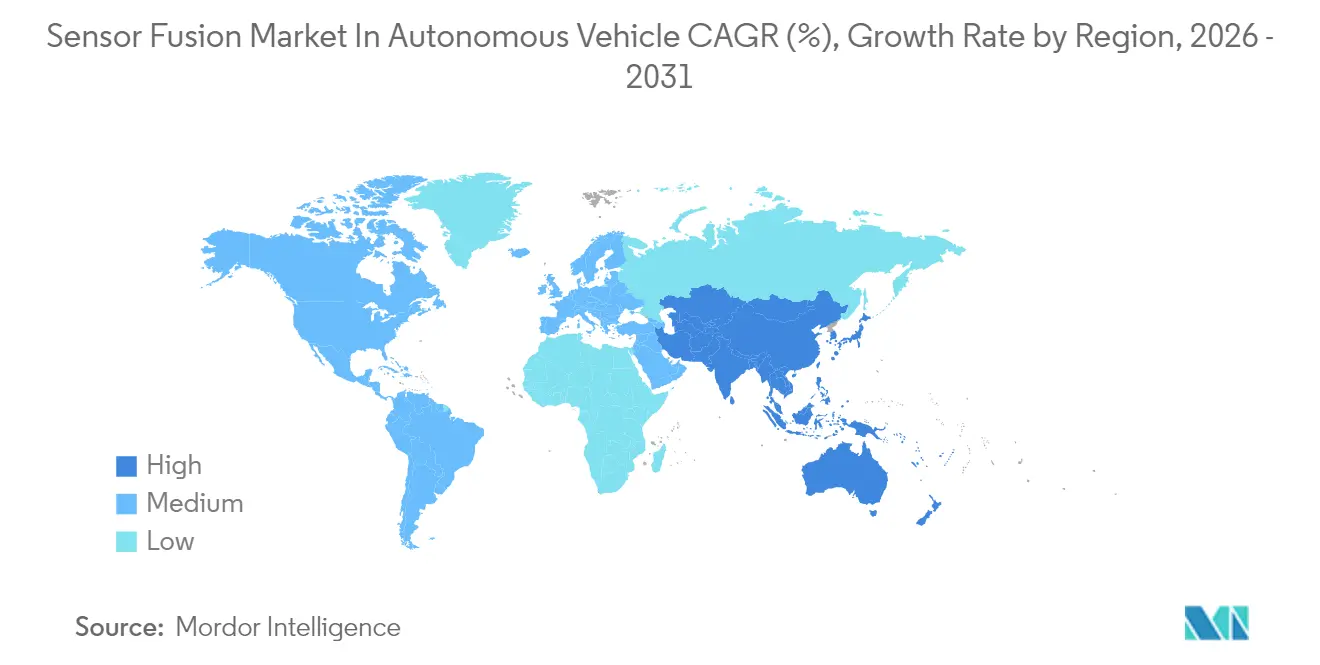

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

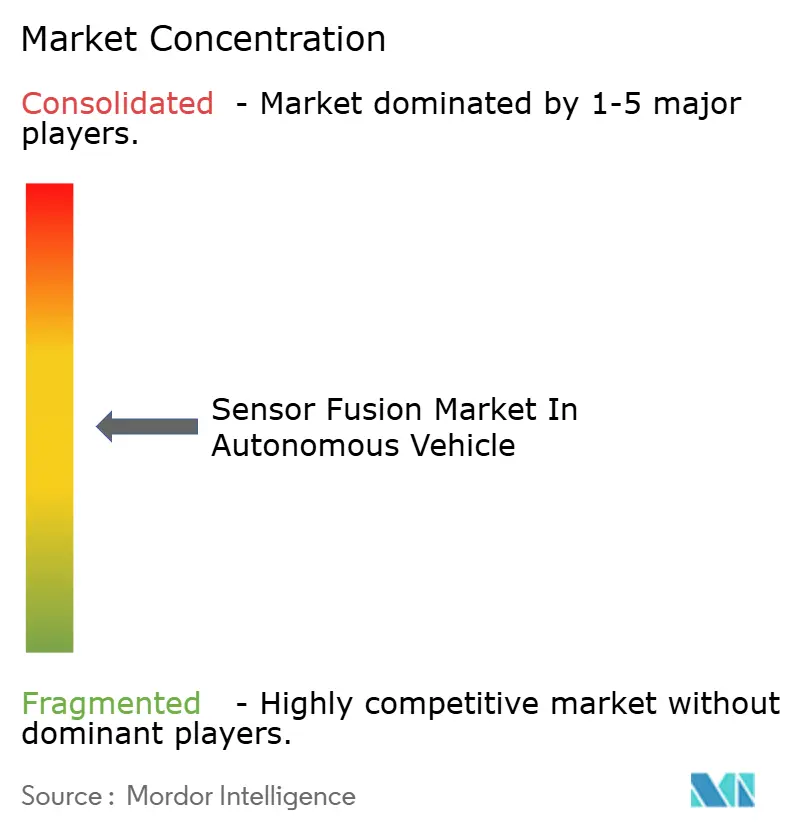

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of Sensor Fusion Market in Autonomous Vehicles by Mordor Intelligence

The sensor fusion market size in autonomous vehicles is expected to grow from USD 4.42 billion in 2025 to USD 5.25 billion in 2026 and is forecast to reach USD 12.41 billion by 2031 at 18.76% CAGR over 2026-2031. Regulatory deadlines for advanced driver-assistance systems, solid-state LiDAR prices that dipped below USD 400 per unit, and edge-AI chipsets that cut fusion latency to under 10 milliseconds collectively support this steep trajectory. Automakers are racing to certify perception stacks that comply with Euro NCAP 2025 five-star protocols while balancing processor power budgets in battery-electric vehicles, a trade-off that favors centralized computing and high-bandwidth data buses. Suppliers able to deliver ISO 26262 and ISO/SAE 21434-compliant hardware–software combos gain an edge, yet headline risks from Section 301 tariffs and UNECE WP.29 validation delays inflate bills of material and lengthen release cycles. The Asia Pacific commands the largest regional revenue and maintains the fastest growth, driven by China’s Level 2 mandate and Japan’s Society 5.0 smart city investments.

Key Report Takeaways

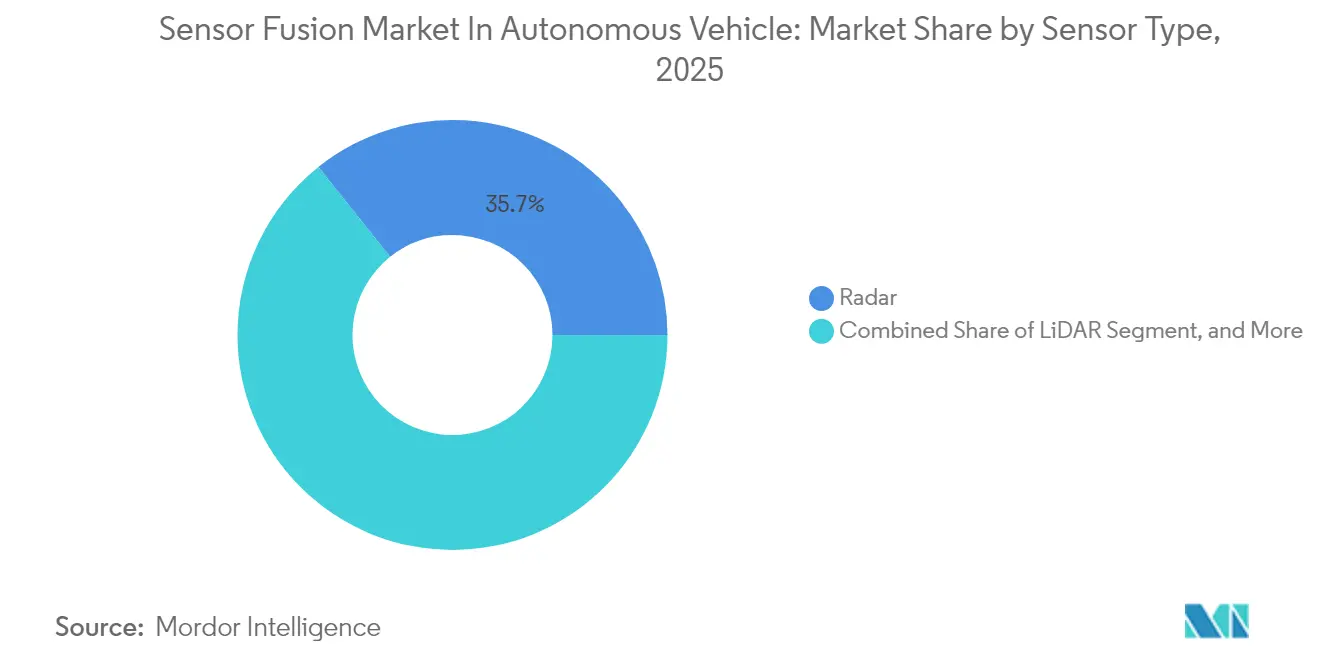

- By sensor type, radar led with a 35.72% share of the sensor fusion market in autonomous vehicles in 2025, whereas LiDAR is forecast to expand at a 21.63% CAGR through 2031.

- By component, hardware accounted for a 60.12% share of the sensor fusion market size in autonomous vehicles in 2025, while software is advancing at a 21.34% CAGR.

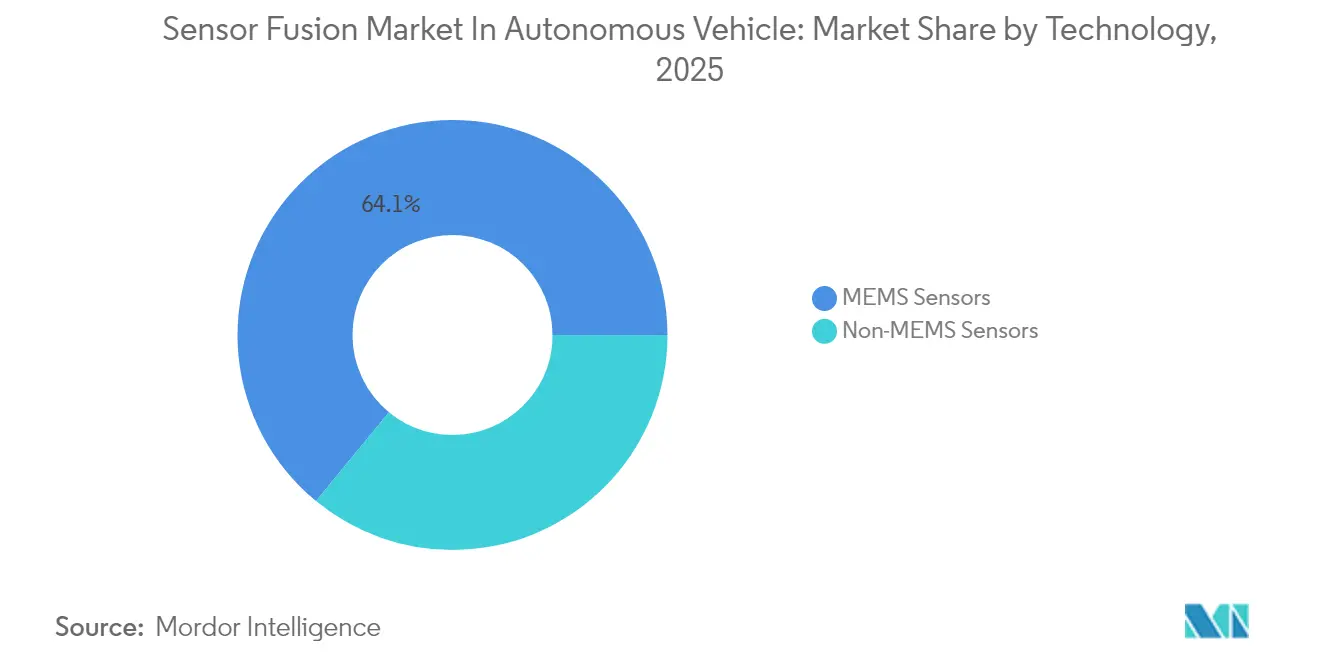

- By technology, MEMS sensors commanded 64.05% share of the sensor fusion market size in autonomous vehicles in 2025 and are growing at a 20.76% CAGR.

- By level of automation, Level 2 captured a 41.35% share of the sensor fusion market size in autonomous vehicles in 2025, whereas Level 4 systems are projected to record the highest CAGR of 22.98% from 2025 to 2031.

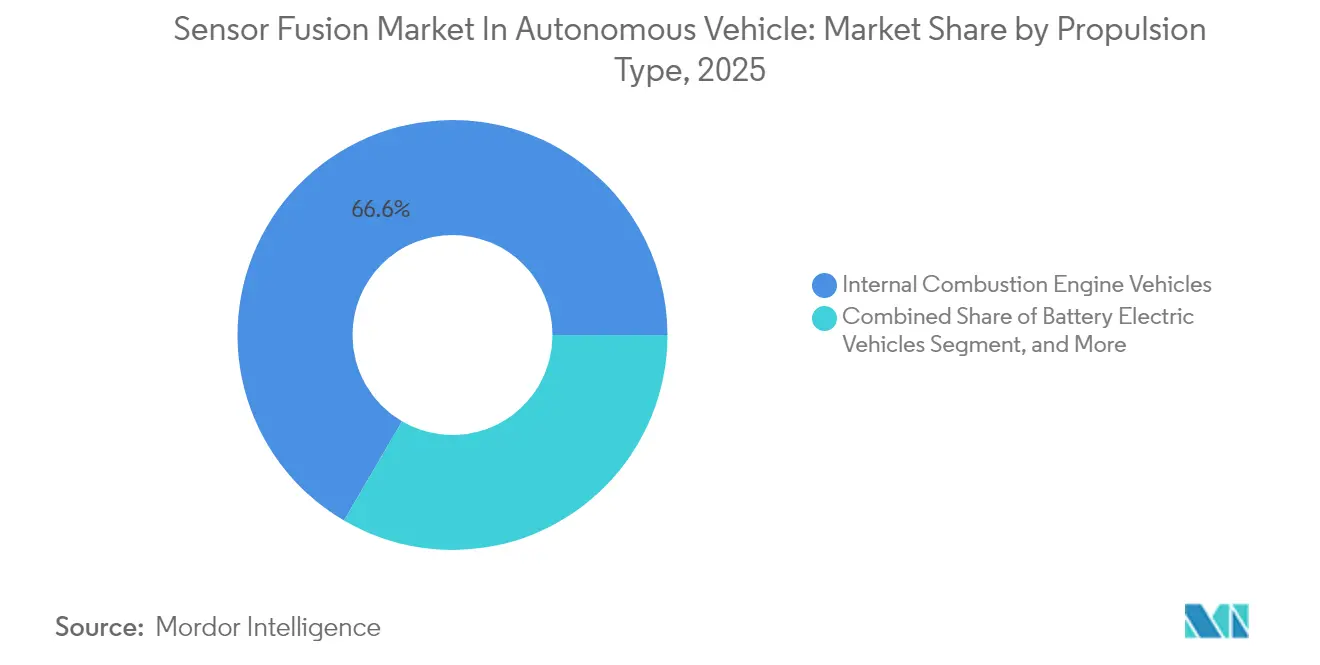

- By propulsion type, internal combustion engine vehicles held a 66.58% share of the sensor fusion market size in autonomous vehicles in 2025; however, battery electric vehicles are progressing at a 21.74% CAGR.

- By vehicle type, passenger cars led with 68.95% revenue share of the sensor fusion market size in autonomous vehicles in 2025; heavy commercial vehicles are forecast to advance at a 22.34% CAGR to 2031.

- By geography, the Asia Pacific region represented a 41.88% share of the sensor fusion market size in autonomous vehicles in 2025 and is expected to grow at a 21.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Sensor Fusion Market in Autonomous Vehicles

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream ADAS mandates accelerating multi-sensor adoption | +4.2% | Global, early EU and China | Short term (≤ 2 years) |

| Declining solid-state LiDAR costs below USD 400 per unit | +3.8% | North America and EU; spillover Asia Pacific | Medium term (2-4 years) |

| In-vehicle edge-AI chipsets enabling <10 ms fusion latency | +3.5% | Global, led by North America and Asia Pacific | Medium term (2-4 years) |

| Over-the-air regulation requiring continuous perception updates | +2.6% | EU and North America, expanding China | Long term (≥ 4 years) |

| Smart-city V2X pilots demanding high-fidelity environmental models | +2.1% | Core Asia Pacific, spillover MEA | Long term (≥ 4 years) |

| Insurance telematics incentives for fused safety-score APIs | +1.9% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream ADAS Mandates Accelerating Multi-Sensor Adoption

Euro NCAP’s 2025 rules make forward-collision mitigation and lane-keeping mandatory for a five-star rating, pushing every major automaker in Europe to adopt multi-sensor stacks.[1]Euro NCAP, “2025 Roadmap: A Safer Future for All,” euroncap.com The U.S. FMVSS 127 final rule requires the implementation of pedestrian automatic emergency braking by 2029, combining camera classification with radar range-rate to reduce urban false positives.[2]National Highway Traffic Safety Administration, “FMVSS 127: Pedestrian Automatic Emergency Braking,” nhtsa.gov China’s C-NCAP 2024 scoring upgrade rewards nighttime pedestrian detection, prompting BYD and Geely to integrate 905-nanometer LiDAR with millimeter-wave radar. Tighter timelines compress validation cycles, favoring suppliers that provide simulation libraries and annotated edge-case data. As mandates converge, the sensor fusion market in autonomous vehicles gains a self-reinforcing demand loop among mainstream brands.

Declining Solid-State LiDAR Costs Below USD 400 per Unit

Hesai’s 2024 roadmap aims to achieve a sub-USD 200 bill-of-material cost by 2026 through ASIC integration and automated optical alignment. Innoviz secured a USD 350 supply deal for 500,000 units with a European premium OEM, signaling that LiDAR is fast approaching radar price parity. Removing mechanical mirrors reduces failure rates and meets AEC-Q100 Grade 2 thermal cycles, enabling deployment in Level 2+ cars that require improved cut-in detection. As cost curves bend, the sensor fusion market in autonomous vehicles shifts from radar-camera dominance toward LiDAR-inclusive perception, especially in premium sedans and crossovers where consumers pay a safety premium.

In-Vehicle Edge-AI Chipsets Enabling less than and equal to 10 ms Fusion Latency

NVIDIA’s DRIVE Thor samples at 2,000 TOPS and fuses 20 cameras, 12 radars, and 3 LiDARs in under 8 ms end-to-end. Qualcomm’s Snapdragon Ride Elite triples the prior-generation AI compute and embeds ASIL-D lock-step cores, allowing OEMs to consolidate domain ECUs into a single zonal board. Mobileye EyeQ Ultra ships in production EVs in 2024 at 176 TOPS while drawing <100 W, preserving battery range. These chips support transformer-based fusion, which reweights sensor inputs in real-time, enhancing perception robustness in harsh lighting conditions or radar clutter. As latency decreases, the sensor fusion market in autonomous vehicles converts advanced safety features into a differentiated user experience, boosting adoption among mid-volume brands.

Over-the-Air Regulation Requiring Continuous Perception Updates

UNECE R156 compels automakers to install auditable update management that covers any change affecting emergency braking logic. The pending EU Cyber Resilience Act could require 15 years of security support, prompting suppliers to maintain neural-network pipelines throughout a vehicle’s lifespan. OEMs, therefore, pivot to subscription models, spreading the lifetime cost of software across monthly revenue. Tesla’s shadow-mode data logging proves the concept, and legacy brands now replicate massive datasets to retrain models offline. These shifts enlarge software revenue within the sensor fusion market in autonomous vehicles and increase barriers to entry for hardware-only vendors.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of global sensor-data standards across OEMs | -2.8% | Global | Medium term (2-4 years) |

| Double-digit tariffs on LiDAR and IMU imports in 2025 | -2.3% | North America and EU | Short term (≤ 2 years) |

| Real-time cybersecurity certification bottlenecks | -1.9% | EU and North America | Short term (≤ 2 years) |

| Processor power-budget limits in BEVs below 20 W | -1.6% | Global, acute in compact BEVs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Absence of Global Sensor-Data Standards Across OEMs

ISO 23150 remains in draft, leaving vendors to custom-code radar, LiDAR, and camera middleware per customer.[3]ISO, “ISO 23150 Draft Standard,” iso.org SAE J2735 omits fusion schemas, and AUTOSAR Adaptive 24-11 lacks binding cross-sensor timestamp specs. Tier-1 suppliers, therefore, maintain parallel code branches, which inflates engineering spend by 20–30% and delays launches. Smaller firms struggle to recoup validation costs, thinning competition in the sensor fusion market for autonomous vehicles. A breakthrough may arrive only when regulators codify a canonical interface, but consensus across the U.S., EU, and China looks two model cycles away.

Double-Digit Tariffs on LiDAR and IMU Imports in 2025

Section 301 keeps 25% U.S. tariffs on Chinese LiDAR and IMU, lifting the landed cost of a LiDAR from USD 400 to USD 500. EU duties range from 4.5% to 14%, with heavier rates applied to modules with integrated processors. Domestic capacity is nascent, with 12–18-month line-build lead times, forcing OEMs to dual-source or delay advanced sensor packs. Premium vehicle margins absorb the hit, but cost-sensitive segments push fusion upgrades to full redesigns, trimming near-term volume for the sensor fusion market in autonomous vehicles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: LiDAR Outpaces Radar in Premium Deployments

Radar retained 35.72% of the sensor fusion market share in autonomous vehicles in 2025, thanks to its low cost and all-weather reliability. The sensor fusion market size in autonomous vehicles for LiDAR, however, is projected to rise at a 21.63% CAGR through 2031, as Euro-NCAP-compliant Level 3 offerings, such as Mercedes-Benz Drive Pilot, rely on centimeter-level depth. Greater object-classification confidence in adverse light conditions makes LiDAR a de-risking investment for premium OEMs. Camera sensors deliver rich color and pixel density, but they falter in diffuse glare. Therefore, automakers fuse them with radar Doppler to stabilize pedestrian trajectories. Ultrasonic and IMU units fill specific niches, yet their limited range means they augment, not replace, core perception.

Demand for LiDAR remains skewed toward upper-trim crossovers and robotaxis, where customers are willing to tolerate higher costs for hands-free operation. Radar’s incremental generational cost drops cement its dominance in mass-market ADAS. Still, as solid-state LiDAR units approach USD 300, mid-segment EVs plan to adopt them in the 2027 refresh. Suppliers compete on angular resolution and eye-safe wavelengths, while regulatory clarity on 1,550-nanometer lasers could broaden design windows. Consequently, LiDAR’s dollar growth outstrips that of radar, reshaping supplier shares within the sensor fusion market in autonomous vehicles.

By Component: Software Gains as Fusion Algorithms Migrate to Cloud-Trained Models

Hardware accounted for 60.12% of revenue in 2025, encompassing transceivers, optics, and microcontrollers. Yet, the software CAGR of 21.34% outpaces hardware as automakers pivot to neural-network fusion that requires constant fleet-scale retraining. The sensor fusion market size in autonomous vehicles for software services covers calibration, mapping, and cybersecurity updates, forming recurring revenue streams. Continental’s Advanced Radar Sensor 540 compresses raw data to reduce Ethernet traffic by 70%, demonstrating a co-design ethos where edge preprocessing and cloud inference split workloads.

Services such as Mobileye’s Road Experience Management turn anonymized drive data into high-definition maps, monetizing usage beyond initial equipment sales. Over-the-air management platforms expand attach rates, especially in subscription-oriented EV brands. Hardware margins compress under price pressure, while certified middleware commands a premium. The shift alters bargaining power: suppliers offering full-stack solutions capture a bigger share of the sensor fusion market in the autonomous vehicle profit pool than pure-play component vendors.

By Technology: MEMS Sensors Dominate Through Power Efficiency and Scalability

MEMS devices held a 64.05% share and grew 20.76% as their batch semiconductor processes yield cost economies unavailable to discrete radar or mechanical LiDAR. MEMS gyros and accelerometers consume microwatts, enabling always-on stabilization during autonomous maneuvers. This energy frugality aligns with BEV power budgets.

Non-MEMS sensors stay relevant in long-range adaptive cruise, yet face replacement by 4D imaging radar on SiGe RF-CMOS rails. TDK’s piezoelectric MEMS ultrasonics add high sensitivity at half the footprint, facilitating seamless bumper integration. As fabs shift to 200-mm MEMS lines, unit costs continue to fall, sustaining volume leadership for MEMS within the sensor fusion market in autonomous vehicles.

By Level of Automation: Level 4 Surges as Robotaxi Deployments Scale

Level 2 retains a 41.35% share today, but Level 4 achieves a 22.98% CAGR as Waymo and Baidu expand their robotaxi routes. The sensor fusion market in autonomous vehicles benefits as geofenced services demonstrate safety parity with human drivers. Level 3 remains constrained by liability laws, while Level 5 remains aspirational pending a general AI breakthrough.

Urban geofences reduce scenario entropy, enabling sensor suite downsizing and improving economic viability. Fleet operators value uptime over cost, buying redundant sensors plus remote operations links. As 5G standalone networks mature, remote supervision density climbs, further lifting Level 4 penetrations through 2031.

By Propulsion Type: Battery Electric Vehicles Lead Through Architectural Synergies

Internal combustion engine cars still comprise 66.58% of installations, yet battery electric vehicles are growing at a 21.74% CAGR because high-voltage backbones and centralized E/E layouts facilitate multi-gigabit sensor buses. The sensor fusion market size in autonomous vehicles for BEVs is accelerating as OEMs pitch software-defined performance updates that leverage unused battery capacity.

Hybrids hedge power needs with regenerative boosts, but pack-space constraints crimp sensor placement above wheel arches. Fuel-cell vehicles remain niche. As the EV boom aligns with autonomy hype, component bins standardize around 48-volt auxiliaries, simplifying supply chains and shortening learning curves for new entrants.

By Vehicle Type: Heavy Commercial Vehicles Accelerate Through Fleet Economics

Passenger cars remain 68.95% of 2025 revenue, but heavy commercial vehicles rise at 22.34% CAGR on platooning’s 10-15% fuel savings. Fleets amortize sensor capex across 500,000 km annual duty cycles, a math that validates triple-LiDAR roof pods on Class-8 trucks.

Light commercial vans follow as e-commerce booms. Niche autonomous shuttles and mining rigs prioritize sensor counts aggressively, as customer comfort is secondary. Regulatory exemptions for off-highway operations speed testing, pushing edge-case learning back into on-road stacks, and indirectly enriching the broader sensor fusion market in autonomous vehicles.

Geography Analysis

Asia Pacific captured 41.88% share and will hold a 21.57% CAGR, buoyed by China’s Level 2 mandate in 2025 and Japan’s USD 670 million Society 5.0 V2X budget. The region’s manufacturing clusters compress iteration loops between sensor fabs and vehicle assembly lines.

North America remains a technology testbed, with the FCC allocating 30 MHz C-V2X spectrum and California green-lighting driverless robotaxis in Los Angeles and San Francisco. Europe enforces UNECE regulations and stimulus for zero-fatality targets, sustaining premium OEM spending despite softer unit demand.

South America, the Middle East, and Africa lag, but they operate lighthouse pilots in Brazil’s São Paulo and the UAE’s Dubai logistics corridors. Currency volatility and infrastructure gaps defer mass rollouts, but falling LiDAR costs could unlock price-sensitive applications by 2028. Overall, geographic diversification cushions cyclical shocks, stabilizing revenue visibility for the sensor fusion market in autonomous vehicles.

Competitive Landscape

Tier-1 suppliers, such as Bosch, Continental, Denso, and Aptiv, compete with semiconductor specialists NVIDIA, Mobileye, Qualcomm, and Infineon in a moderately fragmented market. Bosch’s 2024 tie-up with Microsoft layers Azure analytics on top of its motion-sensor portfolio, allowing OEMs to push perception updates over the air. Mobileye’s SuperVision bundles cameras, compute, and software across seven OEMs, shrinking integration headaches but concentrating supplier power.

Cost disruptors Hesai and Innoviz drop solid-state LiDAR below USD 350, winning Chinese and European design slots formerly held by mechanical incumbents. NVIDIA’s Omniverse simulation suite sells millions of virtual miles, differentiating its DRIVE Thor chip beyond raw TOPS. Qualcomm and Continental launched a JV to embed on-sensor fusion in a single module, reducing network load by 80%.

White-space persists in heavy-truck trailer sensors and aftermarket retrofit kits. Patent filings indicate a shift toward transformer-based multimodal fusion, yet compute draw increases 20-fold, favoring vendors with bleeding-edge silicon. ISO 26262 and ISO/SAE 21434 certification remain a gating factor; incumbents leverage decades-old process lattices to defend their share, while startups focus on subsystems to bypass capital-intensive full-stack offerings. Collectively, the top five suppliers control approximately 40% of the 2025 revenue, indicating moderate concentration.

Leaders of Sensor Fusion Market in Autonomous Vehicles

-

Robert Bosch GmbH

-

Continental AG

-

ZF Friedrichshafen AG

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Qualcomm and Mercedes-Benz signed a multi-year deal to roll Snapdragon Ride Elite across upcoming EVs, covering 40 sensors per car.

- September 2025: NVIDIA won BYD’s premium EV compute contract with DRIVE Thor chips, including Omniverse validation.

- August 2025: Hesai completed a 100,000-unit annual LiDAR plant, cutting unit build time to 45 minutes.

- July 2025: Continental and Qualcomm created a JV to deliver integrated radar-camera modules satisfying ASIL-D.

- June 2025: Mobileye EyeQ Ultra entered production with Zeekr, enabling Level 3 conditional automation on Chinese highways.

- May 2025: Bosch Sensortec launched the BHI360 IMU with on-board fusion firmware outputting 1,000 Hz orientation quaternions.

- April 2025: Waymo expanded its autonomous ride-hailing service to Los Angeles International Airport with 150 Jaguar I-PACE vehicles.

- March 2025: Infineon introduced the AURIX TC4D microcontroller with 600 MHz triple-core lock-step processing and hardware radar acceleration.

Scope of Report on Sensor Fusion Market in Autonomous Vehicles

The report on the Sensor Fusion Market in Autonomous Vehicles segments the market by various criteria. Sensor types include LiDAR, Radar, Camera, Ultrasonic, and Inertial Measurement Units (IMU). Components are categorized into Hardware, Software, and Services. Technology encompasses both MEMS and non-MEMS sensors. Levels of Automation span from Level 1 to Level 5. Propulsion Types encompass Internal Combustion Engine Vehicles, Battery Electric Vehicles, Hybrid Electric Vehicles, and Fuel Cell Electric Vehicles. Vehicle Types include Passenger Cars, Light and Heavy Commercial Vehicles, and other Autonomous Vehicles. Geographically, the report encompasses North America, South America, Europe, the Asia-Pacific region, and the Middle East and Africa. Market forecasts are presented in USD value terms.

| LiDAR |

| Radar |

| Camera |

| Ultrasonic |

| Inertial Measurement Units (IMU) |

| Hardware |

| Software |

| Services |

| MEMS Sensors |

| Non-MEMS Sensors |

| Level 1 |

| Level 2 |

| Level 3 |

| Level 4 |

| Level 5 |

| Internal Combustion Engine Vehicles |

| Battery Electric Vehicles |

| Hybrid Electric Vehicles |

| Fuel Cell Electric Vehicles |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Other Autonomous Vehicles |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Sensor Type | LiDAR | ||

| Radar | |||

| Camera | |||

| Ultrasonic | |||

| Inertial Measurement Units (IMU) | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Technology | MEMS Sensors | ||

| Non-MEMS Sensors | |||

| By Level of Automation | Level 1 | ||

| Level 2 | |||

| Level 3 | |||

| Level 4 | |||

| Level 5 | |||

| By Propulsion Type | Internal Combustion Engine Vehicles | ||

| Battery Electric Vehicles | |||

| Hybrid Electric Vehicles | |||

| Fuel Cell Electric Vehicles | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Other Autonomous Vehicles | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Sensor Fusion Market In Autonomous Vehicle today?

It reached a market size of USD 5.25 billion in 2026 and is set to reach USD 12.41 billion by 2031.

What is the projected CAGR for sensor fusion solutions in autonomous vehicles?

The Sensor Fusion Market In Autonomous Vehicle is forecast to expand at a strong 18.76% CAGR from 2026 to 2031.

Which sensor type is growing the fastest in upcoming autonomous vehicles?

LiDAR shows the highest growth, projected at a 21.63% CAGR through 2031, owing to falling prices and Level 3-plus automation needs.

Why are battery electric vehicles important for sensor fusion adoption?

BEVs offer centralized electrical architectures and ample power budgets that simplify high-bandwidth sensor data buses, pushing a 21.74% CAGR in fusion installations.

Which region leads the adoption of multi-sensor perception stacks?

Asia Pacific holds the largest share at 41.88% and is projected to grow at 21.57% CAGR, fueled by China’s Level 2 mandate and smart-city programs.

What are the major challenges restraining market growth?

Lack of unified sensor-data standards, tariffs on key components, cybersecurity certification delays, and BEV power-budget limits weigh on near-term adoption.

Page last updated on: