Mobile Crushers And Screeners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

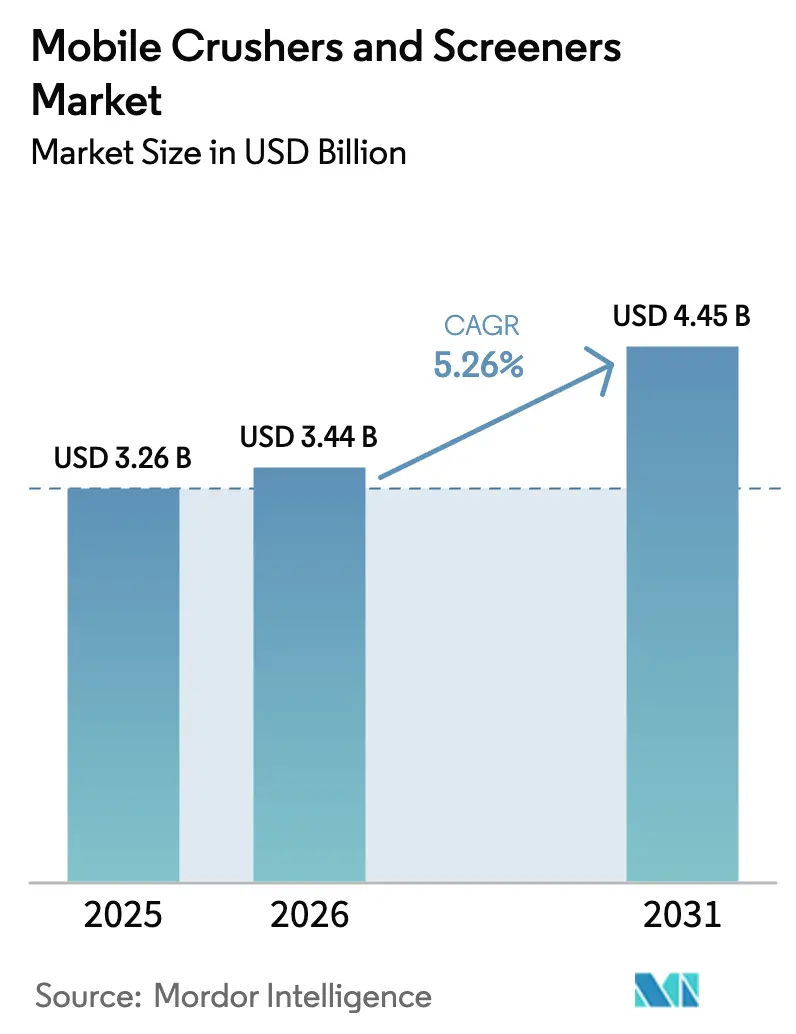

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

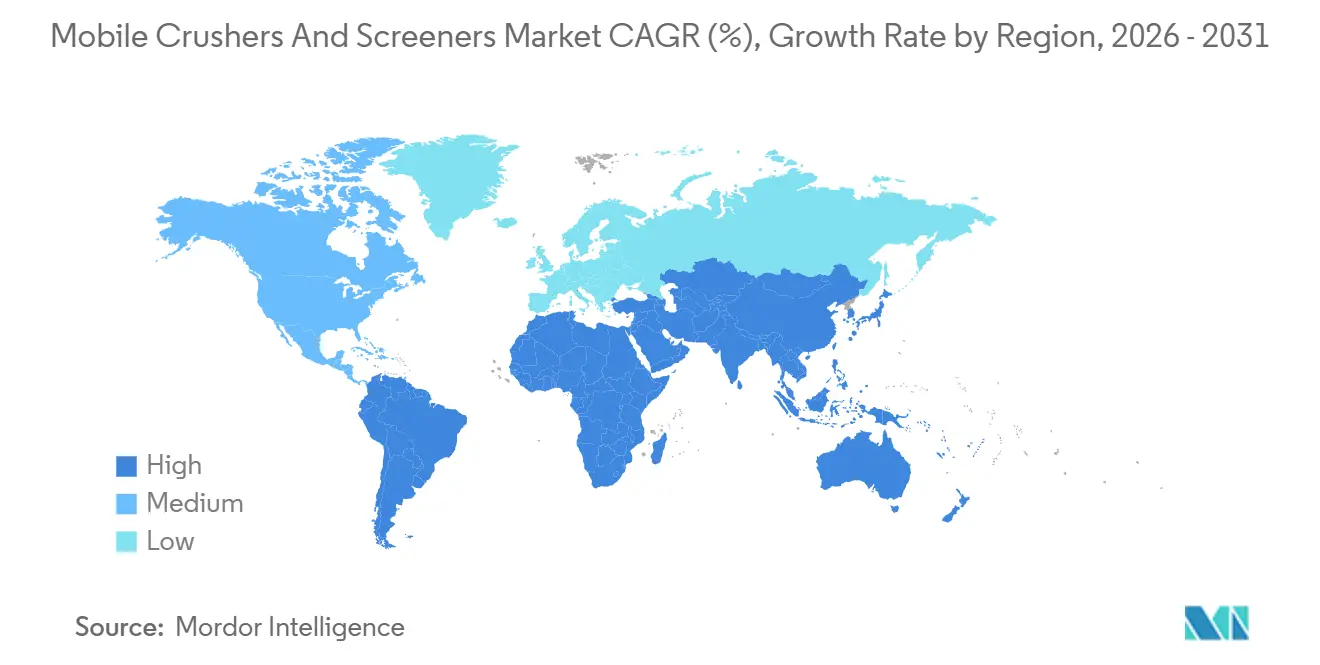

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

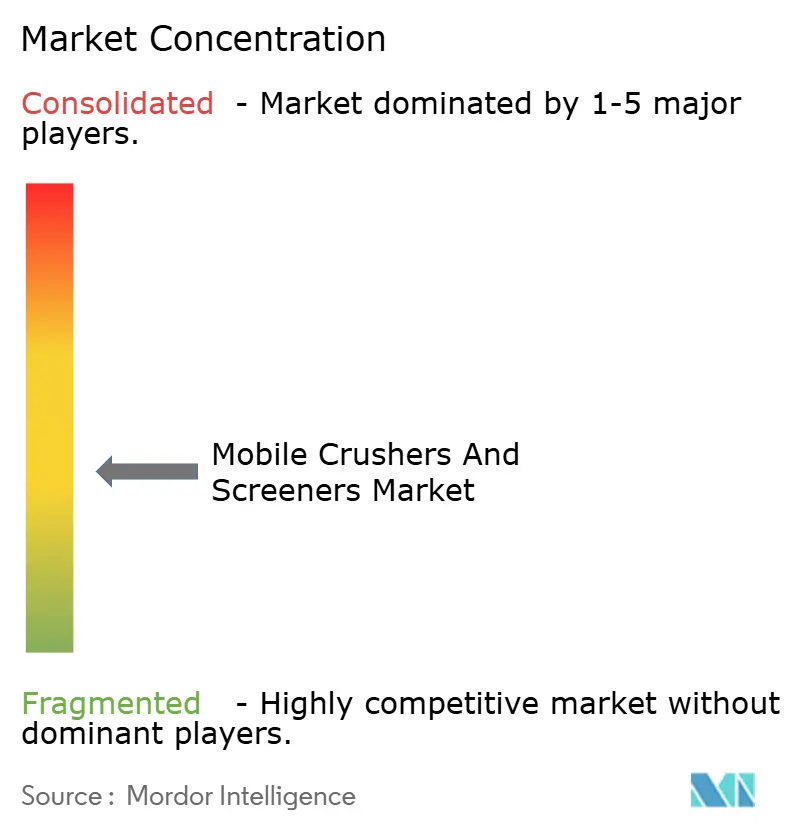

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Crushers And Screeners Market Analysis by Mordor Intelligence

The Mobile Crushers And Screeners Market size is expected to increase from USD 3.26 billion in 2025 to USD 3.44 billion in 2026 and reach USD 4.45 billion by 2031, growing at a CAGR of 5.26% over 2026-2031.

Steady adoption stems from contractors relocating crushing and screening to project sites, thereby eliminating multi-stage haulage, and from rental operators that absorb up-front capital expenditure and provide short-term contracts that preserve buyer liquidity. Rising demand for fully electric models, stricter non-road emission limits, and expanding quarry and recycling activity across Asia Pacific, North America, and Europe are reinforcing equipment replacement cycles. Middle East and Africa is gaining momentum as lithium and cobalt extraction accelerates, while mature markets are shifting toward hybrid and electric fleets to comply with urban noise and air-quality rules. Competitive rivalry remains elevated, yet OEMs able to combine modular platforms, telematics, and electrified drivetrains are widening their lead on lifecycle cost and regulatory compliance.

Key Report Takeaways

- By machinery type, mobile crushers led with 55.14% of the mobile crushers and screeners market share in 2025, while mobile screeners are set to expand at a 5.81% CAGR through 2031.

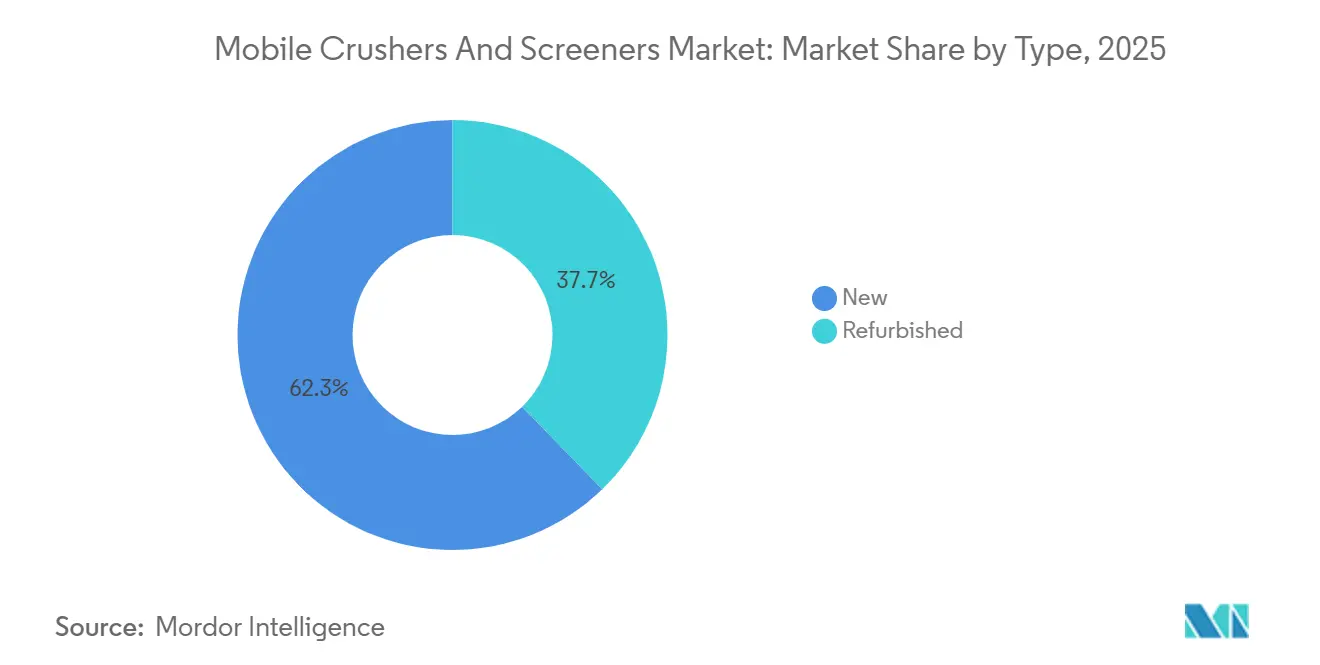

- By type, new units dominated with 62.27% revenue in 2025; refurbished equipment is forecast to climb at a 6.90% CAGR to 2031.

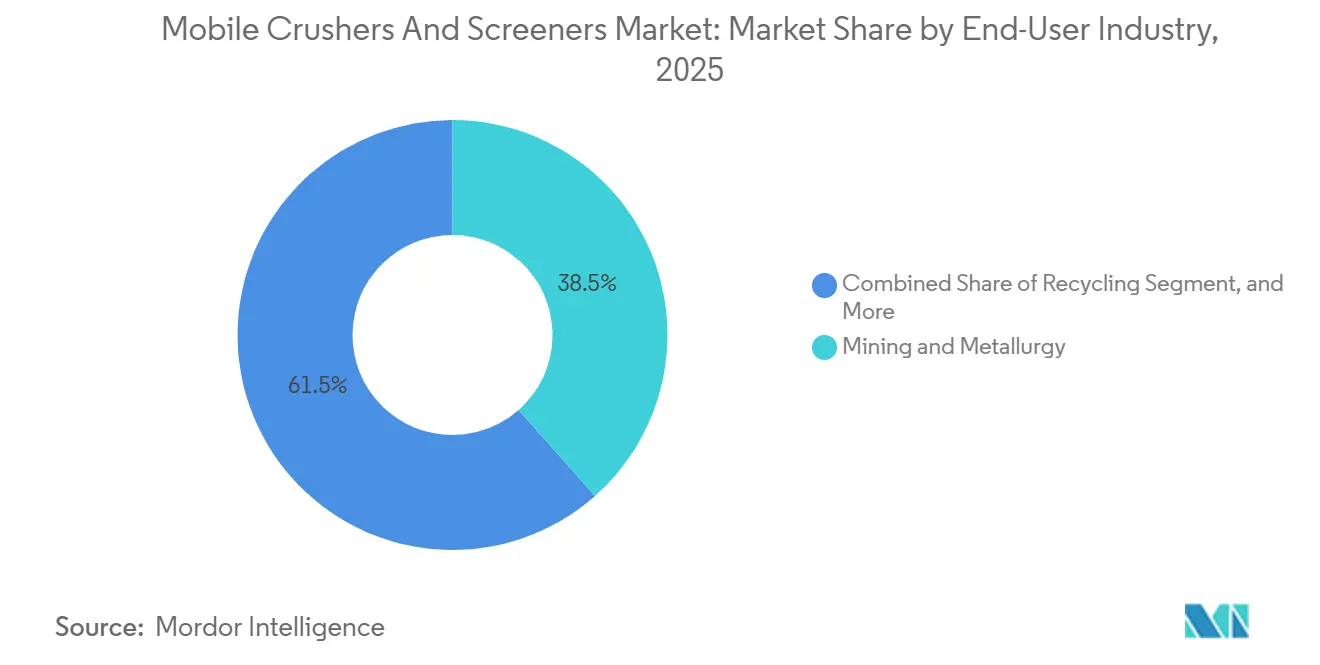

- By end-user industry, mining and metallurgy controlled 38.47% of 2025 demand, yet recycling is projected to register the highest 6.29% CAGR over the outlook period.

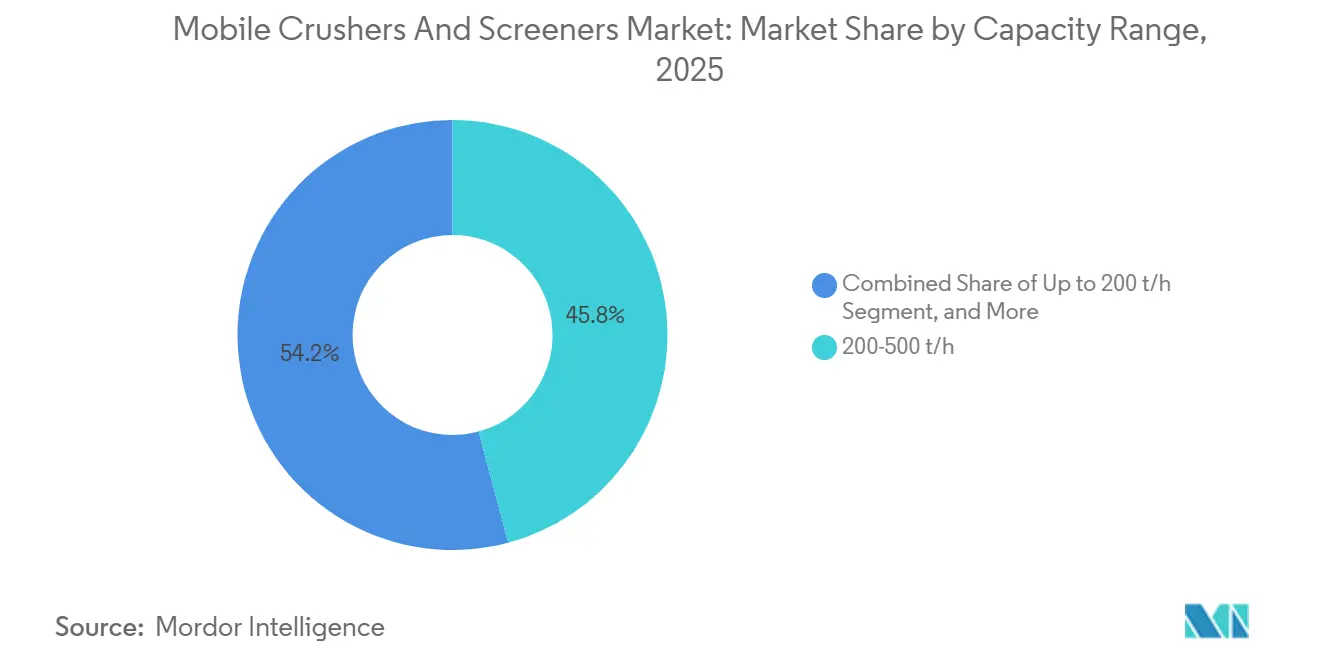

- By capacity, the 200-500 t/h band captured 45.83% of 2025 shipments, whereas sub-200 t/h units are poised for a 6.55% CAGR on micro-mobility projects.

- By power source, diesel-hydraulic models retained 71.20% of 2025 sales; fully electric machines are on track for a 6.18% CAGR.

- By geography, Asia Pacific generated 42.11% of 2025 revenue, but Middle East and Africa is anticipated to record the fastest 5.98% CAGR thanks to critical-mineral projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Crushers And Screeners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for on-site crushing to cut hauling costs | +0.70% | Global, with concentration in North America, Europe, and Asia Pacific | Medium term (2–4 years) |

| Expansion of construction sector amid urbanization | +1.10% | Asia Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rising mineral extraction in emerging economies | +0.90% | Africa, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Adoption of hybrid-electric mobile crushers for emission compliance | +0.60% | Europe, North America, select Asia Pacific cities | Short term (≤ 2 years) |

| Rental fleet expansion driven by asset-light strategies | +0.50% | North America and Europe, emerging in Asia Pacific | Medium term (2–4 years) |

| Integration of telematics enabling predictive maintenance | +0.40% | Global, led by North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for On-Site Crushing to Cut Hauling Costs

Mobile jaw and cone crushers are increasingly stationed within meters of excavation faces, trimming diesel consumption for haul trucks and shortening project schedules by up to one quarter. Rental companies are scaling mixed fleets that can be dispatched on 30-day contracts, converting what was a USD 500,000-USD 1.5 million capital outlay into a predictable operating expense. Sunbelt Rentals generated GBP 8.98 billion (USD 11.4 billion) in the fiscal year ended April 2024, underscoring robust fleet utilization.[1]Sunbelt Rentals, “Annual Report 2024,” ashtead-group.com Persistent construction-equipment operator growth projected by the U.S. Bureau of Labor Statistics further supports long-term equipment demand.[2]U.S. Bureau of Labor Statistics, “Construction Equipment Operators,” bls.gov

Expansion of Construction Sector Amid Urbanization

Metro rail, expressway, and brownfield redevelopment projects across India, Indonesia, and the Gulf states increasingly favour track-mounted crushers that can be relocated weekly as building phases advance. India’s National Infrastructure Pipeline earmarked USD 1.4 trillion for projects through 2025. Mobile screeners also free 2,000-3,000 square meters of scarce city land otherwise occupied by stationary plants, a decisive advantage where zoning restricts heavy industrial footprints.

Rising Mineral Extraction in Emerging Economies

Lithium, cobalt, and copper exploration is accelerating in the Democratic Republic of Congo, Zambia, and Zimbabwe, regions where grid power and paved roads remain limited. Self-contained mobile units allow miners to commence ore processing quickly and truck concentrates to distant smelters, side-stepping multi-year delays tied to fixed plant permitting. Financing for the Inga 3 hydropower project and the Lobito Atlantic Railway highlights the infrastructure wave underpinning equipment adoption.[3]World Bank, “Inga 3 Hydropower Project Financing,” worldbank.org

Adoption of Hybrid-Electric Mobile Crushers for Emission Compliance

The European Union’s Non-Road Mobile Machinery Regulation 2025/14 tightened particulate and NOx ceilings, driving demand for battery-electric and hybrid crushers that can operate in zero-emission zones. Sandvik’s QH443E electric cone crusher consumes 25% less energy than the diesel equivalent and lowers lubricant use by up to 91%, yielding USD 15,000-USD 25,000 annual savings for two-shift operations.[4]Sandvik AB, “Sandvik Launches 800i Cone Crusher Series,” sandvik.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital expenditure | -0.80% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Volatility in raw material prices impacting equipment cost | -0.60% | Global, with supply-chain concentration in Asia | Medium term (2–4 years) |

| Permitting hurdles for mobile plant deployment in urban zones | -0.30% | North America, Europe, select Asia Pacific cities | Short term (≤ 2 years) |

| Skilled operator shortage limiting utilization rates | -0.40% | North America, Europe, Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Mid-capacity mobile crushers cost USD 500,000-USD 1.5 million, a hurdle for buyers in regions where equipment-finance interest rates remain elevated. Rental penetration still sits below 15% of construction-equipment spending in many African and Southeast Asian nations, hampering access to modern low-emission fleets. Although OEMs such as Metso now market modular platforms that reduce investment per application, high borrowing costs identified in International Monetary Fund outlooks continue to defer outright purchases.

Volatility in Raw Material Prices Impacting Equipment Cost

Copper prices rose 8.1% in 2024 according to the International Monetary Fund, inflating hydraulic-component bills, while lithium and cobalt cost swings inject USD 30,000-USD 50,000 uncertainty into battery packs for fully electric models. OEMs face limited hedging horizons and must either absorb volatility or raise list prices, both scenarios that can delay procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refurbished Units Gain Momentum

Refurbished equipment accounted for a growing slice of the mobile crushers and screeners market in 2025 and is projected to climb at a 6.90% CAGR through 2031. The segment benefits from certified rebuild programs that deliver up to 90% of new-unit performance at 40-60% lower cost. Caterpillar’s remanufacturing division processed 147 million pounds of returned material in 2023, achieving an 88% core-return rate and underscoring a closed-loop supply chain that resonates with emission-reporting mandates.

Rental fleets exploit the price gap by reserving refurbished units for short-term contracts and deploying new machines on long-duration leases, thereby optimizing asset utilization across customer segments. Although new machines still hold the majority of revenue, lifecycle economics, landfill-disposal fees, and circular-economy legislation in the European Union suggest sustained momentum for rebuilds. Overall, the mobile crushers and screeners market size tied to refurbished sales is likely to rise faster than headline demand.

By Machinery Type: Screeners Narrow the Gap

Mobile screeners logged a 5.81% CAGR outlook, eclipsing crushers’ 5.26% trajectory. Vibratory models dominate thanks to low power draw, but high-tonnage gyratory screeners are gaining share in iron-ore and coal circuits where deck blinding limits linear-screen throughput. EU Directive 2018/851 mandates 70% recovery of construction and demolition waste, driving onsite separation workflows that hinge on versatile screening plants.

OEMs are integrating wind sifters and magnetic separators into screen chassis, converting single-purpose machines into multi-fraction processors. Kleemann’s 10.5 m² triple-deck MOBISCREEN MSS 1102 PRO exemplifies the trend, enabling contractors to create recycled concrete aggregate that meets road-base specifications without trans-shipping material. Such innovations underpin the mobile crushers and screeners market’s pivot toward value-adding separation rather than pure size reduction.

By End-User Industry: Recycling Accelerates

Recycling is set to outpace mining, aggregates, and infrastructure, expanding at a 6.29% CAGR. Landfill-diversion mandates in Europe and California have transformed demolition debris into an input commodity, and municipal contracts increasingly specify recycled content thresholds. The mobile crushers and screeners market size tied to recycling therefore grows in tandem with circular-economy policies.

Mining and metallurgy, while still the largest vertical, faces a flatter trajectory as many majors already operate modern fleets. Nonetheless, planned copper and lithium projects across Africa and Latin America will sustain baseline demand. Aggregate processing remains a key application on expressway and rail developments, yet recycled concrete and asphalt are capturing mix share, further lifting screener adoption.

By Capacity Range: Sub-200 t/h Units Surge

Compact track-mounted models below 200 t/h throughput are projected to advance at a 6.55% CAGR. These machines support wind-farm access roads, transmission-line corridors, and pipeline rights-of-way where haul distances and space constraints rule out stationary plants. Rubble Master’s 29-tonne RM J110X fits into a 40-foot container and mobilizes in under four hours, demonstrating the engineering focus on logistics-friendly footprints.

The larger 200-500 t/h band remains the revenue mainstay, aligned with mid-tier quarry output and urban demolition. Models above 500 t/h are largely confined to iron-ore, coal, and copper mines where economies of scale and continuous operations justify high-capex installations.

By Power Source: Electric Adoption Quickens

Contractors, aiming for zero-tailpipe credentials in municipal bids, are driving a forecasted 6.18% CAGR for fully electric models, trailing only behind refurbished growth. Fully electric models are gaining traction due to their ability to meet stringent environmental regulations and reduce operational emissions, making them a preferred choice for urban and municipal projects. By combining diesel generators with batteries, hybrid units are filling off-grid gaps, allowing nighttime operations in noise-sensitive areas.

These hybrid systems offer flexibility and efficiency, particularly in regions where grid access is limited or unreliable. While diesel-hydraulic equipment remains prevalent in off-grid applications, rising fuel prices and savings on lubricants are bolstering the appeal of electric alternatives. Additionally, advancements in battery technology and the growing availability of charging infrastructure are further enhancing the adoption of electric solutions, reinforcing momentum within the mobile crushers and screeners market.

Geography Analysis

Asia Pacific anchored 42.11% of 2025 revenue, with China, India, and Indonesia investing heavily in rail, road, and affordable housing. The region benefits from both large-scale quarrying and urban redevelopment, ensuring steady equipment turnover. Australia continues to procure above-500 t/h crushers for iron-ore expansions, while Southeast Asian nations prefer mid-capacity units that can navigate tighter job sites.

Middle East and Africa is expected to post the fastest 5.98% CAGR as lithium and cobalt extraction scales in the Democratic Republic of Congo, Zambia, and Zimbabwe. Mobile plants permit early cash-flow generation ahead of permanent infrastructure completion, and recent upgrades to the Lobito Atlantic Railway further enhance export economics. Funding for hydropower and logistics corridors supports sustained demand for off-grid diesel-hydraulic and hybrid machines.

North America represents the second-largest revenue pool thanks to high rental penetration and an aging interstate network currently under rehabilitation via Infrastructure Investment and Jobs Act allocations. Europe’s mature construction sector shows slower aggregate growth, but stringent emission standards accelerate fleet renewal toward hybrid and electric models, underpinning replacement demand within the mobile crushers and screeners market. South America and the Middle East round out global sales, driven by Brazilian mining expansions and Saudi megaprojects respectively.

Regulatory Landscape

Emissions and compliance requirements for mobile crushing and screening fleets increasingly track non-road engine and machinery rules across major regions. In the European Union, Regulation (EU) 2016/1628 (Stage V) continues to anchor non-road mobile machinery (NRMM) engine-emissions compliance, and Regulation (EU) 2025/14 strengthens approval and market-surveillance obligations for machinery circulating on public roads. This is pushing OEMs and fleet owners toward tighter documentation, conformity procedures, and traceability.

In the United States, mobile and portable operations intersect both air-permitting and engine-emissions compliance, including federal standards for nonmetallic mineral processing plants (40 CFR 60 Subpart OOO) and requirements commonly applicable to stationary compression ignition engines (40 CFR 60 Subpart IIII) used on-site. In 2026, the US Environmental Protection Agency (EPA) issued guidance reaffirming right-to-repair for nonroad diesel equipment owners. In July 2026, the EPA also proposed amendments affecting Model Year 2027 and later heavy-duty engines, including changes around DEF-related engine derates and alerts, which shapes how equipment owners plan uptime, diagnostics access, and aftertreatment management practices.

Competitive Landscape

Market concentration is Moderate: Metso, Sandvik, Terex, Kleemann, and Komatsu together hold roughly 40-45% revenue, leaving space for specialists such as Rubble Master, McCloskey, and Keestrack. Leading OEMs focus on modular platforms that share chassis, powertrains, and control software, lowering per-unit R&D cost. Sandvik’s ACS-c 5 automation, bundled with the 800i cone series, enables predictive maintenance and remote parameter adjustments, trimming unplanned downtime by up to one third.

Terex’s MAGNA brand, unveiled in 2024, packages crushers, screeners, and conveyors with bundled service contracts aimed at rental fleets, signifying a strategic push to lock in annuity revenue. Smaller challengers exploit white-space niches: Rubble Master targets sub-200 t/h micro-mobility work, while Keestrack pioneers battery-swap solutions that slash charger downtime.

Equipment digitization, autonomous drilling integration, and telematics-driven usage pricing remain the battlegrounds shaping long-term competitive positioning in the mobile crushers and screeners market.

Mobile Crushers And Screeners Industry Leaders

Terex Corporation

Metso Oyj

Komatsu Ltd.

McCloskey International Limited

CDE Global Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrification and diesel-electric architectures create openings for contractors and rental operators seeking compliant machines for urban, noise-sensitive, or emission-controlled work zones, without sacrificing mobility. The 2026 evidence base includes the commissioning of a fully electric Sandvik UJ443E mobile crushing plant in Africa, and Pilot Crushtec highlighting EU Stage V-aligned offerings at Hillhead 2026. Together, these developments broaden the reference base for electric and low-emission mobile circuits beyond early adopter regions. Dual-power and fully electric configurations also suit sites with partial grid access, since operators can cut reliance on onboard engines while keeping deployment flexibility.

A second opportunity cluster is connected operations and automation, where multi-site fleets can reduce labor intensity and improve utilization through tighter monitoring and control. During 2026, Terex showcased the MAGNA range alongside its INNEX digital platform at Hillhead 2026, while Metso rolled out a renewed digital services portfolio for aggregates with AI-driven predictive maintenance and performance monitoring. In parallel, an Austrian Research Promotion Agency (FFG)-funded project reported by SBM Mineral Processing focused on autonomous mobile crushing using digital-twin and camera-based particle-size detection, linking telematics use cases to higher autonomy in crushing and screening workflows.

Recent Industry Developments

- June 2026: Metso authorized a EUR 60 million second-phase investment in its Lokomotion technology center in Lahdesjaervi, Tampere, Finland, adding capacity including a new crusher factory. The program strengthens vertical integration and throughput for modern diesel-electric and digitally enabled mobile crushing portfolios, improving delivery resilience for OEM-built units and key modules.

- May 2026: Metso and Pilot Crushtec conducted the South African market launch of the diesel-electric Lokotrack LT400J jaw crusher. The launch expands access to diesel-electric mobile crushing in a region where mines and contractors often balance off-grid constraints with tightening emissions and operating-cost requirements.

- May 2024: Metso launched the first diesel-electric Lokotrack EC range units. The product move accelerates the shift from purely diesel-hydraulic drivetrains toward electrified architectures that support lower fuel consumption, reduced site emissions, and easier integration with connected monitoring tools.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from mobile crushing and mobile screening equipment that is used at job sites to process aggregates, mining materials, construction debris, and recyclable materials, including both new and refurbished units.

Scope exclusions: stationary crushers and screeners, and purely service-only revenues such as long-term plant operations without equipment sales are excluded.

Segmentation Overview

- By Type

- New

- Refurbished

- By Machinery Type

- Mobile Crushers

- Jaw Crushers

- Cone Crushers

- Impact Crushers

- Other Mobile Crushers

- Mobile Screeners

- Vibratory Screeners

- Gyratory Screeners

- Other Mobile Screeners

- Mobile Crushers

- By End-User Industry

- Mining and Metallurgy

- Aggregate Processing

- Recycling

- Construction and Infrastructure

- Other End-User Industries

- By Capacity Range

- Up to 200 t/h

- 200-500 t/h

- Above 500 t/h

- By Power Source

- Diesel-Hydraulic

- Hybrid-Electric

- Fully Electric

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, especially around construction activity, mining output signals, and cross-border equipment flows that influence demand for mobile units. We relied on public sources such as the USGS for minerals and aggregates context, the World Bank and IMF for macro construction and infrastructure indicators, UN Comtrade for machinery trade patterns, and IEA or similar energy-transition trackers for electrification signals in off-highway equipment.

On the supply side, annual reports, investor decks, and product catalogs were reviewed to understand typical capacity ranges and powertrain offerings (diesel-hydraulic, hybrid-electric, and fully electric), and how new versus refurbished units are positioned. Limited paid database subscriptions for company financials, news, and patent lookups were also used to cross-check timelines and technology direction, and then the assumptions were taken forward into interviews. The sources listed above are illustrative and not exhaustive, and other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the demand pool and pricing logic through interviews and structured surveys with equipment OEM-side experts, dealers, rental firms, quarry and mining operators, and recycling contractors across major consuming regions. These discussions were used to confirm adoption of tracked and wheeled units, the role of refurbishment, typical replacement cycles, and how capacity and power source choices shift by application and regulation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 43% |

| Mid tier: 53% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 20% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where off-highway machinery spend signals, construction and mining activity indicators, and machinery trade flows are used to reconstruct a realistic demand pool for mobile crushing and screening. To keep the totals grounded, the outputs are then checked with selective bottom-up approximations, such as sampled unit shipments by region, dealer channel checks, and average selling price bands applied to typical mixes of crushers versus screeners.

Key inputs that shape the model include infrastructure spending direction, quarrying and mining production volumes, recycled aggregate throughput trends, fleet replacement timing, and the shift in power sources from diesel-hydraulic toward hybrid-electric and fully electric units in specific markets. Capacity mix (up to 200 t/h, 200-500 t/h, and above 500 t/h) is treated as a practical fingerprint because it links to end-use intensity and also affects price levels. Forecasting uses scenario analysis supported by simple regression-style relationships between equipment demand and the strongest activity indicators, and then those forward assumptions are adjusted using expert consensus from primary discussions. When country or application data is thin, gaps are handled through proxy indicators (such as construction output and mining capex signals) and normalized back to regional totals to avoid overstating smaller markets.

Data Validation & Update Cycle

Outputs are triangulated across multiple independent checks, including comparisons against construction and mining equipment cycles, trade movement direction, and observed pricing movements for key capacity bands. Variances are flagged, then reviewed in a second analyst pass, and respondents are re-contacted when a driver changes materially or a region shows an outlier jump that cannot be explained by activity indicators.

The model and narrative go through multi-step internal reviews before sign-off, including consistency checks between type, end-user, capacity, and power source splits. Reports are refreshed annually, and interim updates are made when major events occur, such as sharp currency moves, regulation changes impacting diesel equipment, or sudden shifts in construction and mining activity. Right before delivery, a final update pass is performed so clients receive the most current view tied to the same repeatable logic.

Mordor Intelligence's Mobile Crushers and Screeners Market Size Compared Against Other Published Estimates

Different published market sizes for mobile crushers and screeners can vary because the study periods are not aligned, the included equipment condition differs, and the pricing logic is not always built from the same capacity and power-source mix. In practice, even a one-year base shift can change totals because construction cycles and mining capex move unevenly by region.

Some external estimates emphasize a broader calendar-year base with revenue totals that can mix in adjacent equipment groupings and a different treatment of used units. In Mordor Intelligence's view, the counted scope is limited to mobile crushers and mobile screeners (including new and refurbished) and is structured with explicit checks by capacity band, power source, and end-user demand signals before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.44 B (2026) | |

| Global Consultancy A | USD 3.99 B (2024) | Uses a 2024 base-year revenue view and a shorter horizon, and it can differ from this study due to calendar timing, currency conversion timing, and a different weighting of region mix and application splits. |

| Industry Publisher B | USD 3.30 B (2025) | Uses a 2025 base year and a longer forecast window, and the gap can be driven by how used equipment and end-use categories are grouped, plus more conservative price progression assumptions over the forecast period. |

The comparison mainly shows that base-year selection and scope handling around equipment condition and pricing mix can move the total by a noticeable amount. By keeping capacity, power source, and end-user drivers visible in the model, the estimate stays traceable to real demand signals and can be repeated consistently during future refreshes.

Key Questions Answered in the Report

How large is the mobile crushers and screeners market today?

The mobile crushers and screeners market size stood at USD 3.44 billion in 2026 and is forecast to reach USD 4.45 billion by 2031.

Which application segment is growing the fastest?

Recycling is projected to post the highest 6.29% CAGR through 2031 as landfill-diversion mandates lift demand for on-site processing equipment.

What region is expected to record the quickest growth?

Middle East and Africa is set to expand at a 5.98% CAGR, propelled by lithium and cobalt mining that relies on mobile crushers in off-grid locations.

How are emission regulations influencing equipment design?

The European Union’s tightened non-road limits are accelerating adoption of fully electric and hybrid crushers, such as Sandvik’s QH443E, which lowers energy use by 25%.

What is the outlook for refurbished equipment?

Refurbished units are forecast to rise at a 6.90% CAGR as certified rebuild programs deliver near-new performance at roughly half the capital cost.

Page last updated on: