Collagen Peptides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

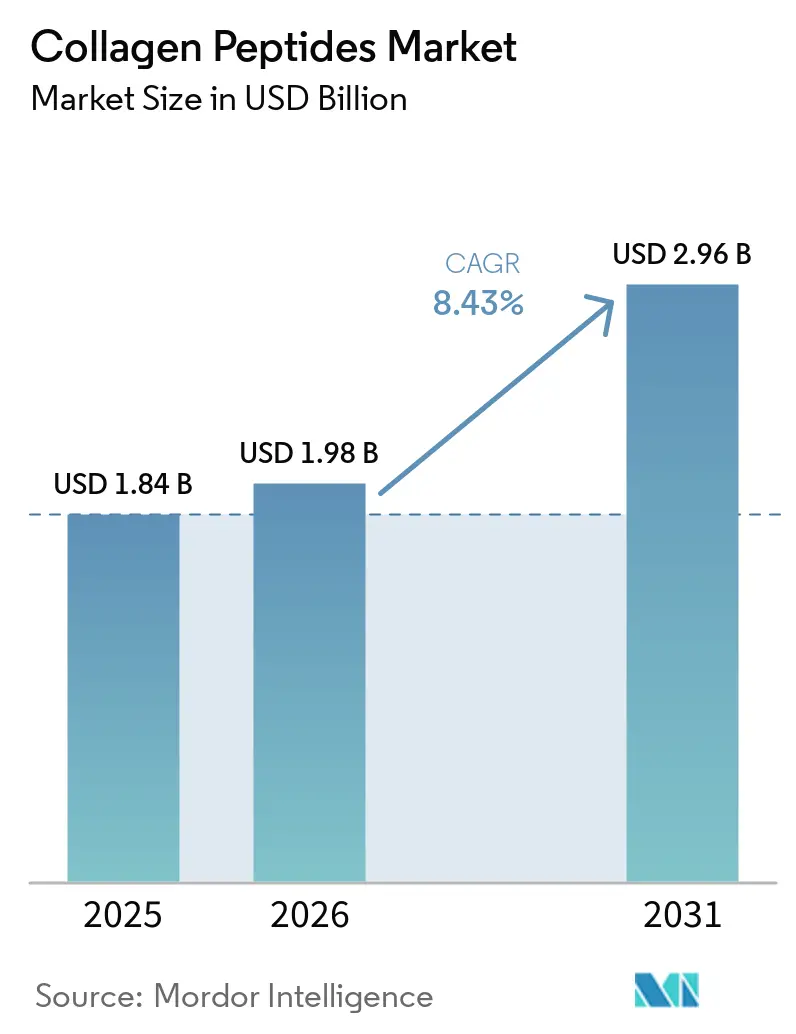

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.96 Billion |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Collagen Peptides Market Analysis by Mordor Intelligence

The global collagen peptides market size was valued at USD 1.84 billion in 2025 and estimated to grow from USD 1.98 billion in 2026 to reach USD 2.96 billion by 2031, at a CAGR of 8.43% during the forecast period (2026-2031). Aging populations, a heightened emphasis on preventive healthcare, and a growing consumer interest in beauty-enhancing supplements drive this growth. The market demonstrates its strength through diverse applications, expanding beyond traditional pharmaceutical uses into sports nutrition and cosmeceuticals, both of which command higher price points. Older consumers increasingly seek products for joint health, skin elasticity, and bone strength, making the aging demographic trend a key driver of market growth. Health-conscious consumers have incorporated collagen supplements into their daily wellness routines, propelled by the preventive healthcare movement. Additionally, the rising "beauty-from-within" trend has fueled demand for collagen-infused products across various categories, including beverages, supplements, and functional foods.

Key Report Takeaways

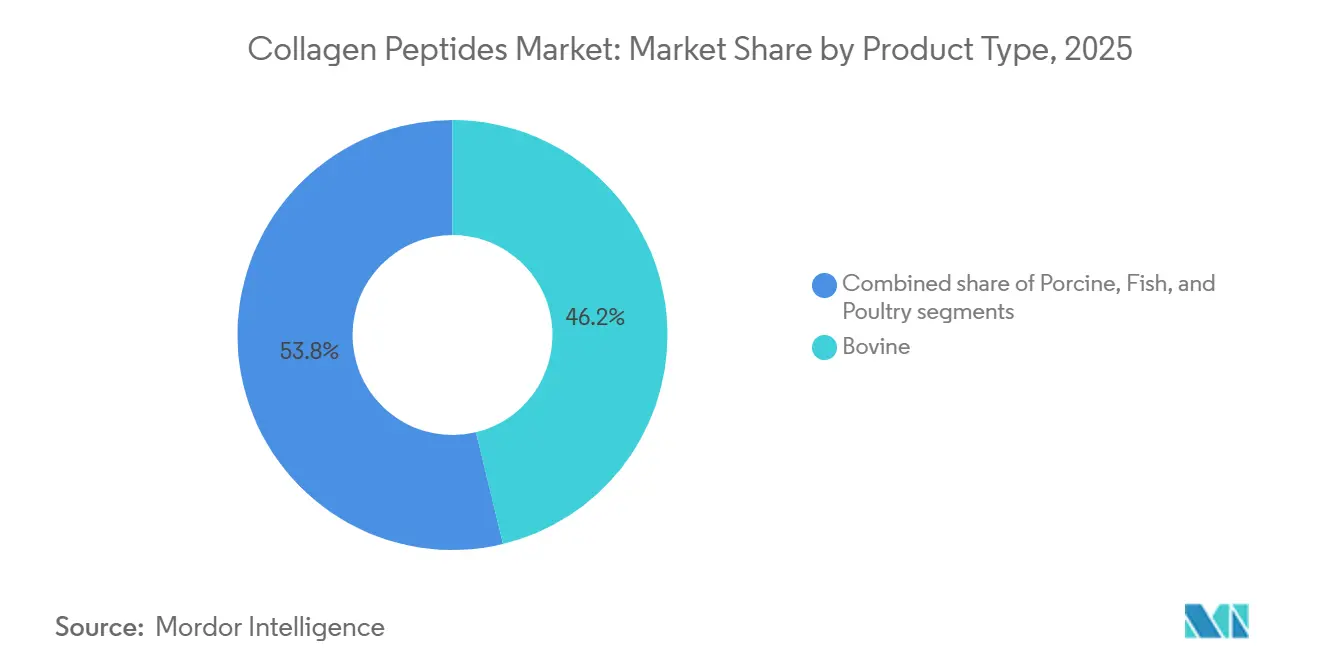

- By product type, bovine collagen held 46.23% of the collagen peptides market share in 2025, whereas fish collagen is projected to post the highest CAGR of 11.79% through 2031.

- By source, hides and skins accounted for 71.68% of the collagen peptides market in 2025, whereas bones are advancing fastest at a 9.64% CAGR through 2031.

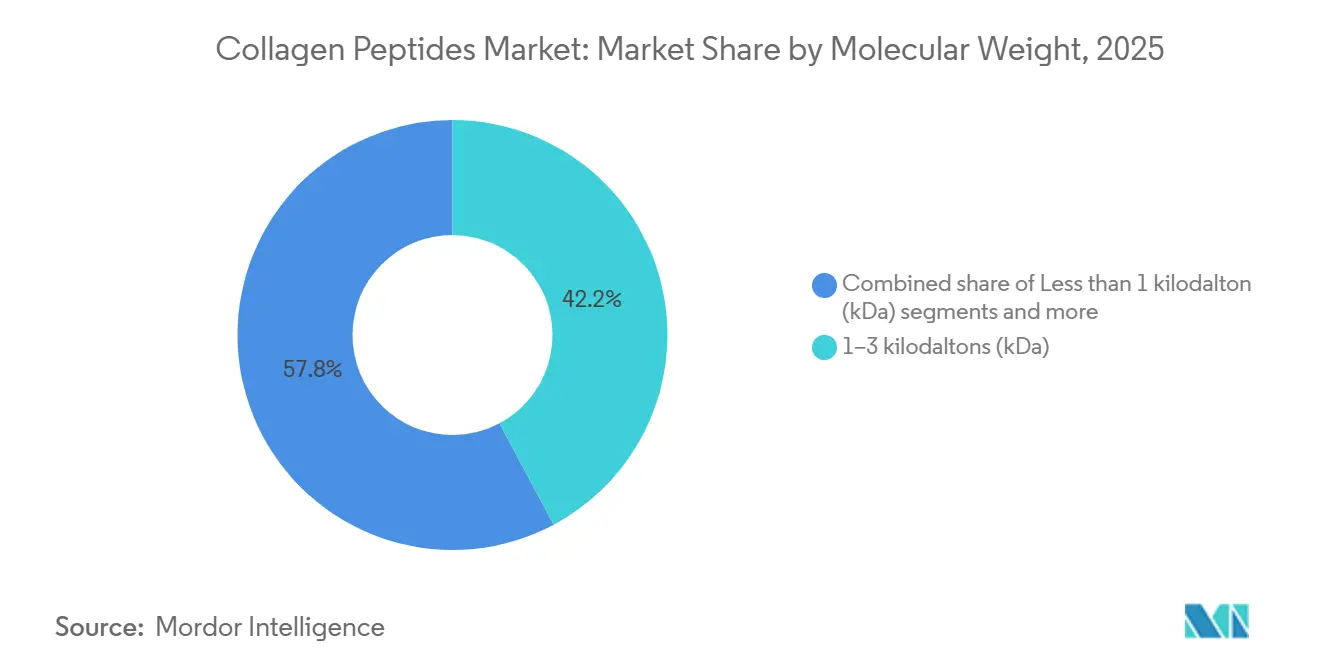

- By molecular weight, 1–3 kilodaltons (kDa) held 42.20% of the collagen peptides market share in 2025, whereas less than 1 kilodalton (kDa) is projected to post the highest CAGR of 10.48% through 2031.

- By application, dietary supplements accounted for 40.34% of the collagen peptides market in 2025 and are advancing fastest, with a 9.95% CAGR to 2031.

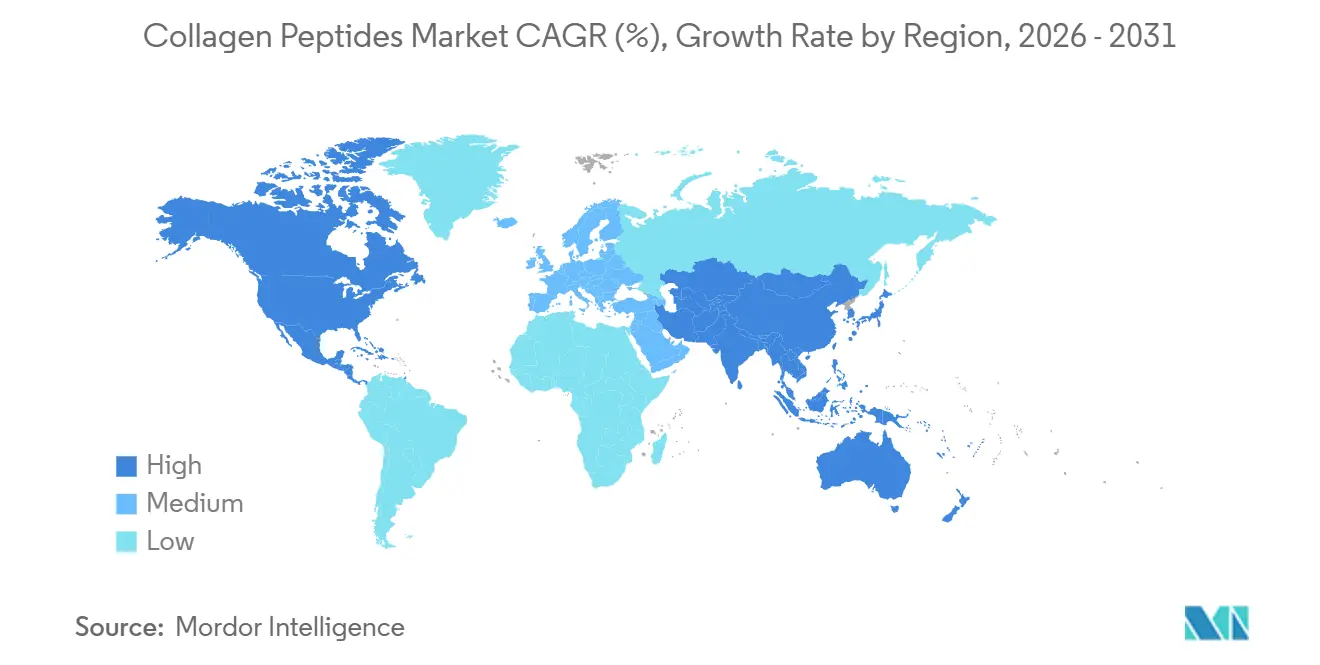

- By geography, North America led with 34.14% of the collagen peptides market share in 2025, whereas Asia-Pacific is set to deliver the quickest 10.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Collagen Peptides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of personalized nutrition and targeted collagen supplementation | +1.6% | Global, early concentration in North America and Europe | Medium term (2–4 years) |

| Growing commercialization of collagen peptides in sports nutrition products | +1.3% | North America, Europe, Asia-Pacific (Japan, South Korea, Australia) | Short to medium term (≤4 years) |

| Increasing popularity of beauty-from-within and nutricosmetics | +1.9% | Asia-Pacific core (China, Japan, South Korea); spill-over to Europe | Short term (≤2 years) |

| Rising consumer focus on preventive healthcare and healthy aging | +1.5% | Global, accelerated impact in North America and Asia-Pacific | Long term (≥4 years) |

| Mainstreaming of "food as medicine" philosophy and functional food culture | +0.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Increasing adoption in the pharmaceutical and medical nutrition applications | +1.1% | North America, Europe, Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rise of personalized nutrition and targeted collagen supplementation

The global dietary supplement market is shifting from generic, broad-spectrum formulations to precision-engineered nutritional solutions designed to deliver clinically validated results for specific physiological functions, with collagen peptides playing a pivotal role in this evolution. Rousselot's launch of the Nextida platform at Vitafoods Europe 2024 exemplifies the growing emphasis on personalized nutrition, transforming collagen peptides from a basic protein commodity into a portfolio of bioactive compositions targeting specific biological needs. This platform, described as a "GPS for the body," uses rigorous cellular model testing to identify optimal peptide compositions that act as precise biological signals, guiding the body toward balance restoration. At Vitafoods Europe 2025, Rousselot showcased its science-backed innovation, Nextida GC, to support post-meal glucose management. Meanwhile, advancements in artificial intelligence and bioengineering are accelerating the development of precision collagen peptide compositions, enabling the creation of human-identical, mechanism-specific collagen fragments.

Growing commercialization of collagen peptides in sports nutrition products

The sports nutrition category, a key commercial channel for collagen peptides targeting athletic and active consumers, is witnessing robust global growth. According to Mordor Intelligence, the global sports nutrition market was valued at USD 35,800.7 million in 2025, offering a significant opportunity for collagen peptide inclusion. Supplement brands are increasingly incorporating collagen peptides into recovery-specific SKUs, joint-support formulations, and multi-benefit active nutrition products to cater to the evolving needs of this expanding consumer base. The demand for sports recovery supplementation is accelerating, driven by a surge in participation in physical activity. According to the Sports and Fitness Industry Association's (SFIA) 2025 Topline Participation Report, 80% of Americans were actively engaged in physical activities in 2024, representing 247.1 million individuals, an increase of 25.4 million active participants since 2019[1]Source: Sports and Fitness Industry Association, "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024", sfia.org. This growing pool of fitness enthusiasts and athletes represents a substantial market for recovery nutrition solutions, where collagen peptides are becoming a key ingredient.

Rising consumer focus on preventive healthcare and healthy aging

The global collagen peptides market is witnessing significant growth as consumers increasingly prioritize proactive wellness over reactive treatments. This shift is driving demand for nutritional solutions that enhance mobility, joint health, bone strength, skin vitality, and overall well-being, particularly to combat age-related disorders. The rising prevalence of musculoskeletal conditions, such as osteoarthritis (OA), further underscores the importance of collagen peptides. According to the Centers for Disease Control and Prevention (CDC), by 2025, over 100 types of arthritis will be recognized, with OA affecting 32.5 million adults in the United States. Among these, 43% are aged 65 or older, 88% are 45 or older, and women constitute 62% of the affected population[2]Source: Centers for Disease Control and Prevention, "OA Prevalence and Burden", oaaction.unc.edu. The financial burden is also significant, with an average annual direct cost of USD 11,000 per person for OA. Factors such as aging, sedentary lifestyles, and obesity exacerbate joint degeneration, cartilage deterioration, and mobility issues, prompting consumers to adopt collagen peptides as a preventive measure to support connective tissue health and mitigate physical decline.

Mainstreaming of "food as medicine" philosophy and functional food culture

The global collagen peptides market is witnessing significant growth, driven by the increasing adoption of the "Food as Medicine" approach, in which consumers are turning to food and beverages as proactive solutions for managing health concerns such as mobility, aging, metabolic wellness, skin health, and muscle recovery. This shift has driven the functional food segment to evolve from basic nutritional fortification to advanced, condition-specific solutions that cater to modern consumer demands for convenience, indulgence, clean-label attributes, and clinically validated benefits. Manufacturers are responding by developing innovative collagen peptide applications across categories such as high-protein snacks, fortified beverages, sports nutrition, and healthy-aging products. For instance, GELITA AG launched Optibar in May 2024, a collagen peptide blend tailored for protein and cereal bars, enabling the production of high-protein bars with superior texture and mouthfeel, even at protein levels of up to 60%, while also supporting low-sugar claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations related to animal-derived ingredients, traceability, and labeling | -1.5% | Europe, Japan, South Korea, Canada | Medium term (2–4 years) |

| High production and hydrolysis costs associated with manufacturing specialized collagen peptides | -0.9% | Global, concentrated impact in Europe and North America | Short to medium term (≤4 years) |

| Adoption of alternative functional ingredients for joint health, bone support, and beauty applications | -0.7% | Global, with notable pressure in North America and Asia-Pacific | Medium to long term (2–5 years) |

| Fluctuations in the availability and pricing of bovine, porcine, and marine raw materials | -0.8% | Global, concentrated in Europe (bovine imports) and Asia-Pacific (marine) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent regulations related to animal-derived ingredients, traceability, and labeling

The growth of the collagen peptide market is being hindered by stringent regulations surrounding animal-based ingredients, traceability, and labeling requirements. Collagen peptides, derived from sources such as bovine hides, porcine skin, poultry cartilage, fish scales, bones, and tendons, are subject to rigorous food safety, veterinary, and hygiene standards, particularly in key markets like Europe, the United States, and the United Kingdom. These regulations, aimed at ensuring ethical sourcing and consumer safety, have led to higher certification costs, longer approval timelines, and increased trade barriers. Manufacturers face significant challenges navigating complex import and traceability rules, as evidenced by the European Commission’s strict health certification requirements for animal-based products entering Europe. The situation intensified in April 2026 when the European Union expanded the list of products requiring mandatory border checks, compelling collagen peptide exporters to maintain detailed sourcing records to avoid shipment delays.

Adoption of alternative functional ingredients for joint health, bone support, and beauty applications

Collagen peptides are increasingly facing competition from a variety of alternative ingredients that are gaining traction in the joint health, bone support, and beauty markets. While collagen peptides remain a significant presence in nutraceuticals and wellness products, alternatives such as hyaluronic acid, glucosamine, chondroitin, ceramides, calcium, vitamin D, and plant-based peptides are emerging as strong contenders. These alternatives offer diverse benefits, including enhanced skin hydration, cartilage support, improved mobility, and overall healthy aging, thereby reducing the need for collagen peptides as a primary ingredient. Furthermore, the rise of vegan and biotech-based collagen substitutes is intensifying this competition. A 2025 Veganuary survey found that 47% of participants globally chose vegan products primarily due to animal welfare concerns, followed by personal health (20%) and environmental considerations (14%). Moreover, advancements in plant-based peptides and next-generation collagen substitutes are further reshaping the market. For example, UK-based startup LeafyColl developed what it claims to be the first true vegan collagen using plant-based molecular farming technology, as reported by Vitafoods Insights in October 2025. Collagen peptides face competition in joint health and bone support from established ingredients like glucosamine, chondroitin, hyaluronic acid, calcium, and vitamin D. For instance, hyaluronic acid, as noted by the Cleveland Clinic, aids in skin hydration, joint lubrication, wound healing, and eye health, and is also used in gel injections to alleviate knee pain in osteoarthritis patients[3]Source: Cleveland Clinic, "Hyaluronic Acid", my.clevelandclinic.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Marine Collagen Gains Share on Bovine Dominance

Bovine collagen peptides are expected to maintain their dominance in the global collagen peptides market, accounting for 46.23% of total market revenue by 2025. This strong position is attributed to their widespread availability, cost-effectiveness, and versatile applications across industries such as food and beverage, nutraceuticals, and personal care. Additionally, bovine-derived collagen is favored for its rich amino acid profile and high functionality, appealing to both manufacturers and consumers. Its adaptability in various formulations further strengthens its market presence. These factors collectively make bovine collagen peptides a preferred choice in the industry.

Fish collagen peptides are anticipated to be the fastest-growing product segment, with a projected CAGR of 11.79% over the forecast period of 2026-2031. The growing consumer demand for marine-sourced ingredients is a key driver of this growth. Furthermore, the rising demand for clean-label and sustainably sourced products aligns with the growing popularity of fish collagen. Known for its superior bioavailability, fish collagen is increasingly utilized in beauty-from-within supplements, functional foods, and skincare products. This trend highlights the expanding role of fish collagen in meeting consumer preferences for health and sustainability.

By Source: Hides Dominate Supply, Bones Offer a High-Growth Cost Pathway

Hides and skins remain the largest raw material segment in the global collagen peptides market, accounting for 71.68% of total market revenue in 2025. This leadership is primarily due to their widespread availability from the meat processing industry, which ensures a steady and cost-effective supply. Hides and skins offer a high collagen yield, making them a preferred choice for large-scale production. Their established supply chains further enhance their suitability for use in various applications, including food, nutraceuticals, and cosmetics. The consistent demand for these raw materials underscores their critical role in meeting the growing demand for collagen peptides.

Bones are expected to be one of the fastest-growing raw material categories, with a CAGR of 9.64% through 2031. This growth is driven by increasing efforts to utilize by-products effectively, thereby promoting sustainability across the value chain. The focus on reducing raw material waste has further encouraged the adoption of bone-derived collagen peptides. Technological advancements in extraction processes have also made it easier to harness collagen from bones, enhancing their appeal as an alternative source. Moreover, the rising demand for sustainable, eco-friendly collagen sources is expected to drive the use of bone-based collagen peptides across diverse end-use industries.

By Molecular Weight: Sub-Kilodalton Fractions Redefine Bioavailability Standards

Collagen peptides with a molecular weight of 1-3 kDa dominated the global collagen peptides market in 2025, accounting for 42.20% of the market. This dominance is attributed to their ideal combination of bioavailability, functionality, and adaptability across a range of applications, including dietary supplements, functional foods, beverages, and personal care products. These peptides are highly favored for their efficient absorption, ensuring maximum health benefits. Their proven efficacy in promoting skin elasticity, joint mobility, and bone strength has further solidified their market position. Manufacturers continue to leverage these attributes to meet the growing global demand for health and wellness products.

Collagen peptide fractions with a molecular weight below 1 kDa are projected to grow the fastest, with a CAGR of 10.48% during the forecast period of 2026 to 2031. This growth is primarily driven by the growing preference for highly bioavailable ingredients that offer faster absorption and greater effectiveness. The rising popularity of premium health and beauty supplements, particularly those targeting anti-aging and skin health, is further driving demand for these ultra-low-molecular-weight peptides. Technological advancements in collagen extraction and processing are enabling manufacturers to produce more refined and efficient peptide formulations. As consumer awareness of the benefits of collagen peptides continues to grow, this segment is expected to gain significant traction in the coming years.

By Application: Dietary Supplements Drive Volume, Pharmaceuticals Attract Investment

Dietary supplements remain the leading application segment in the global collagen peptides market, accounting for 40.34% of total revenue in 2025. This dominance is attributed to the growing consumer focus on collagen's health benefits, including improved skin elasticity, enhanced joint mobility, stronger bones, and support for healthy aging. The segment is expected to grow at a CAGR of 9.95% during the forecast period, driven by the increasing popularity of easy-to-consume formats such as powders, capsules, tablets, and gummies. Additionally, the rising trend of incorporating collagen into daily diets is further fueling demand. Manufacturers are also leveraging advancements in product formulations to cater to evolving consumer preferences, boosting the segment's growth.

The shift toward preventive healthcare and personalized nutrition is significantly influencing the adoption of collagen supplements. Consumers are increasingly integrating these products into their wellness routines to address specific health concerns and maintain overall well-being. The segment's growth is further supported by innovations in product development, such as clean-label and multifunctional supplements. Expanding retail channels, including e-commerce platforms, are making these products more accessible to a broader audience. Furthermore, the rising demand for beauty-from-within solutions and active lifestyle products is expected to sustain the segment's upward trajectory throughout the forecast period.

Geography Analysis

North America continues to dominate the global collagen peptides market, accounting for 34.14% of total revenue in 2025. The region's leadership is attributed to its well-established dietary supplement industry, high consumer expenditure on wellness products, and the increasing use of collagen to improve joint, bone, and overall health. The United States, Canada, and Mexico are key contributors, driven by growing awareness among healthcare professionals and consumers about collagen's health benefits. Additionally, the availability of advanced manufacturing facilities and a strong distribution network further supports market growth in the region. The rising trend of preventive healthcare and personalized nutrition also plays a pivotal role in sustaining demand for collagen peptides.

The Asia-Pacific region is anticipated to be the fastest-growing market for collagen peptides, with a projected CAGR of 10.94% through 2031. This growth is fueled by increasing health consciousness, a surge in demand for beauty-from-within products, and the rising consumption of functional foods and dietary supplements. Major markets such as China, Japan, and India are driving regional expansion, supported by a large and growing consumer base, rising disposable incomes, and significant investments in collagen peptide production. Furthermore, the region's focus on innovative product development and the incorporation of collagen in traditional diets are boosting its market potential. The increasing popularity of marine-sourced collagen, particularly in Japan and South Korea, is also contributing to this growth.

Europe holds a substantial share of the global collagen peptides market, driven by strong demand for clean-label, functional, and fortified food products. Consumers in the region are increasingly prioritizing ingredient transparency, sustainability, and premium-quality nutrition, which has led to higher adoption of collagen-based products. Countries like Germany, France, and the United Kingdom are key markets, supported by robust research and development activities and a growing focus on health and wellness. Meanwhile, South America and the Middle East and Africa are emerging as promising markets, benefiting from increasing awareness of collagen's health benefits, expanding supplement consumption, and the availability of bovine raw materials. The introduction of halal-certified collagen products is further enhancing market opportunities in these regions.

Competitive Landscape

The collagen peptides market is highly consolidated, with a few key players accounting for a significant share of overall revenue. Prominent market leaders such as GELITA AG, Darling Ingredients, Nitta Gelatin Inc., Tessenderlo Group NV, and Shandong Hengxin Biotech Co., Ltd. leverage their strong raw material sourcing capabilities and extensive manufacturing networks. These companies offer diverse product portfolios catering to various applications, including food, beverages, nutraceuticals, pharmaceuticals, and personal care. Their global presence and ability to meet the growing demand for collagen peptides across multiple industries have solidified their market positions. Additionally, their focus on maintaining high-quality standards and ensuring consistent supply chains further strengthens their competitive edge.

Market competition is increasingly shaped by factors such as product quality, scientific validation, and innovation tailored to specific applications. Leading players are prioritizing research and development to create advanced collagen peptide solutions that address key consumer needs, such as healthy aging, beauty-from-within, sports nutrition, joint health, and medical nutrition. These companies are also emphasizing technical support and formulation expertise to build long-term partnerships with clients. By focusing on innovation and customer-centric solutions, they aim to differentiate themselves in a competitive landscape. Furthermore, the ability to provide scientifically backed products enhances their credibility and appeal among end-users.

While global leaders dominate the market, regional and niche suppliers are steadily expanding their presence by offering competitive pricing, sustainable sourcing practices, and specialized products. The rising demand for marine-derived, halal-certified, and premium collagen peptides has encouraged these players to diversify their offerings and enhance their production capabilities. Innovation, traceability, and the development of value-added products are becoming critical factors for success in this market. Regional players are also capitalizing on local consumer preferences and regulatory requirements to strengthen their foothold. As a result, the competitive dynamics of the collagen peptides market continue to evolve, driven by a combination of global and regional strategies.

Collagen Peptides Industry Leaders

-

Gelita AG

-

Darling Ingredients Inc.

-

Tessenderlo Group nv

-

Shandong Hengxin Biotech Co., Ltd

-

Nitta Gelatin Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GELITA launched CURADERM, a new bioactive collagen peptide specifically developed to support skin barrier health and outer body barrier repair. This ingredient is the first collagen peptide with scientifically substantiated results for evidence-based positioning in innovative skin and gum care concepts.

- June 2025: Thai Union launched its first marine collagen derived from tuna skin and has invested USD 30 million into building a processing factory specially dedicated to producing marine collagen ingredients.

- May 2025: Thai Union Ingredients expanded its product line with the launch of its new-generation marine collagen peptides, ThalaCol, at Vitafoods Europe. According to the brand, it is derived from the skin of wild and responsibly sourced tuna and is naturally pure and fully traceable.

- March 2025: Weishardt launched Naticol x3Peptide, capturing headlines as the first marine collagen tripeptide available in the European market. Developed through an exclusive, highly precise enzymatic hydrolysis process, this next-generation bioactive ingredient guarantees a minimum tripeptide concentration of 25%.

Global Collagen Peptides Market Report Scope

Collagen peptides are short chains of amino acids derived from collagen, a structural protein naturally found in the skin, bones, tendons, and connective tissues of animals and humans. The collagen peptides market is segmented by product type, source, molecular weight, application, and geography. By product type, the market is segmented into bovine, porcine, marine, fish, and poultry. Based on the source, the market is segmented by bones, hides, and skin. Based on molecular weight, the market is segmented by less than 1 kilodalton (kDa), 1–3 kilodaltons (kDa), 3–5 kilodaltons (kDa), and greater than 5 kilodaltons (kDa). Based on application, the market is segmented into food and beverages, dietary supplements, pharmaceuticals, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million) and volume (Tons).

| Bovine |

| Porcine |

| Fish |

| Poultry |

| Bones |

| Hides and Skins |

| Less than 1 kilodalton (kDa) |

| 1–3 kilodaltons (kDa) |

| 3–5 kilodaltons (kDa) |

| Greater than 5 kilodaltons (kDa) |

| Pharmaceuticals |

| Dietary Supplements |

| Food and Beverages |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Bovine | |

| Porcine | ||

| Fish | ||

| Poultry | ||

| By Source | Bones | |

| Hides and Skins | ||

| By Molecular Weight | Less than 1 kilodalton (kDa) | |

| 1–3 kilodaltons (kDa) | ||

| 3–5 kilodaltons (kDa) | ||

| Greater than 5 kilodaltons (kDa) | ||

| By Application | Pharmaceuticals | |

| Dietary Supplements | ||

| Food and Beverages | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for collagen peptides through 2031?

The collagen peptides market size is projected at USD 1.98 billion in 2026 and is forecast to reach USD 2.96 billion by 2031, projected to grow at 8.43% CAGR. Growth is being supported by beauty supplements, preventive health use, sports nutrition, and emerging clinical applications.

Which product category leads global demand for collagen peptides?

Bovine collagen peptides led product demand with 46.23% share in 2025 because they benefit from mature supply chains, strong familiarity, and the widest evidence base among animal derived sources.

Which collagen source is growing fastest and why?

Bone sourced material is projected to grow at 9.64% CAGR, while fish collagen peptides as a product type are set to grow at 11.79% CAGR. Growth is tied to better cost recovery options in alternative feedstocks and stronger bioavailability and lifestyle fit in marine formats.

Why are low molecular weight collagen peptides gaining attention?

Fractions below 1 kDa are forecast to grow at 10.48% CAGR because brands and consumers increasingly associate smaller peptide sizes with faster absorption and more advanced formulation science.

Page last updated on: