Cold Spray Technology Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

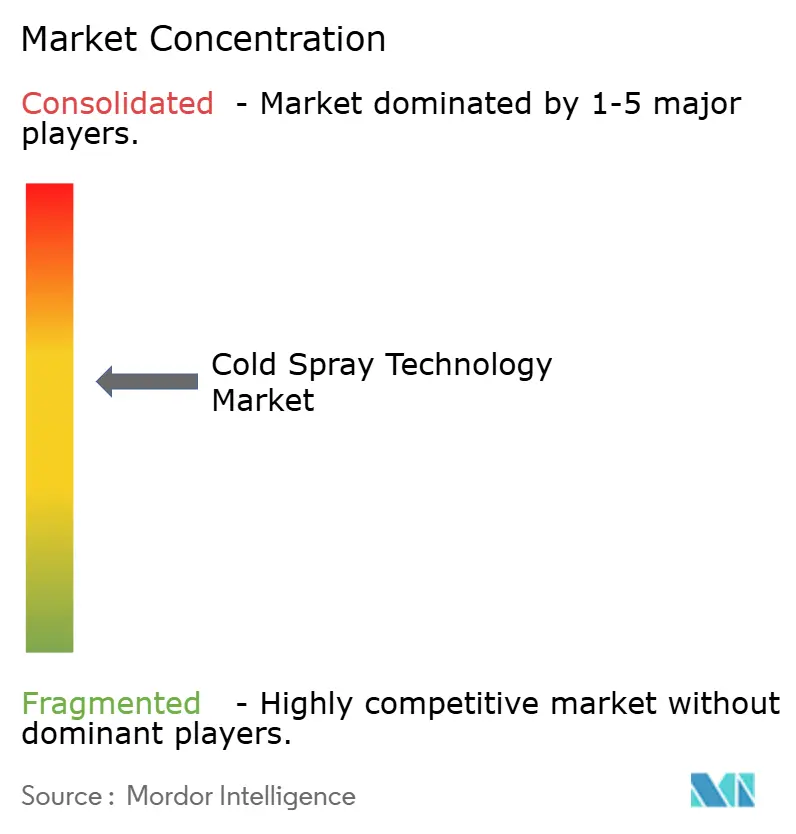

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Spray Technology Market Analysis by Mordor Intelligence

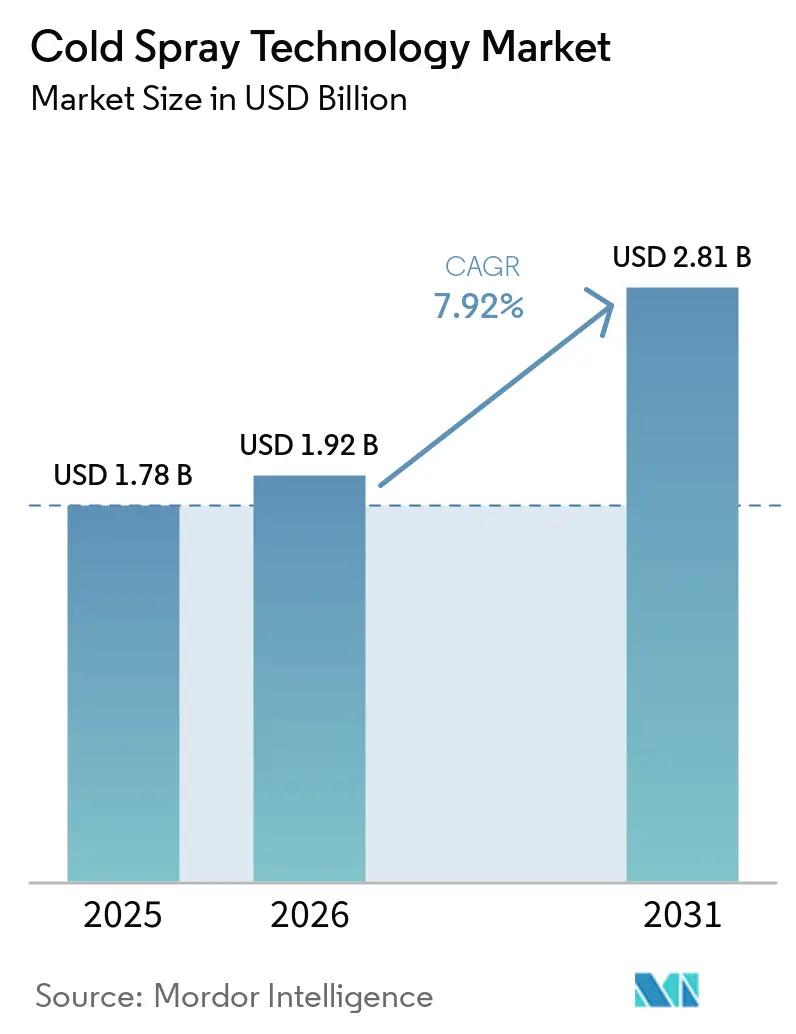

The Cold Spray Technology Market size is expected to grow from USD 1.78 billion in 2025 to USD 1.92 billion in 2026 and is forecast to reach USD 2.81 billion by 2031 at 7.92% CAGR over 2026-2031. In defense maintenance, qualification frameworks such as Military Standard (MIL-STD)-3021 are expediting approval cycles, resulting in a sharp adoption curve. Meanwhile, the commercial aerospace sector is addressing a growing Maintenance, Repair, and Overhaul (MRO) backlog, creating a multi-year growth opportunity. Portable, supersonic units are expanding the customer base beyond large depots. Materials suppliers are increasing atomized-powder production lines to meet the precise particle-size requirements of additive manufacturing. The ongoing alignment of International Organization for Standardization (ISO) 21452, American Society for Testing and Materials (ASTM) B3302, and naval standards is reducing compliance costs, encouraging capital investments even from mid-sized repair shops. Additionally, helium-recovery systems and high-temperature nitrogen propellant loops are lowering operating expenses by up to 35%, enhancing the cost-efficiency of high-pressure systems.

Key Report Takeaways

- By substrate, metals commanded 67.88% of the cold spray technology market share in 2025, while composite and hybrid substrates are projected to advance at an 8.02% CAGR through 2031.

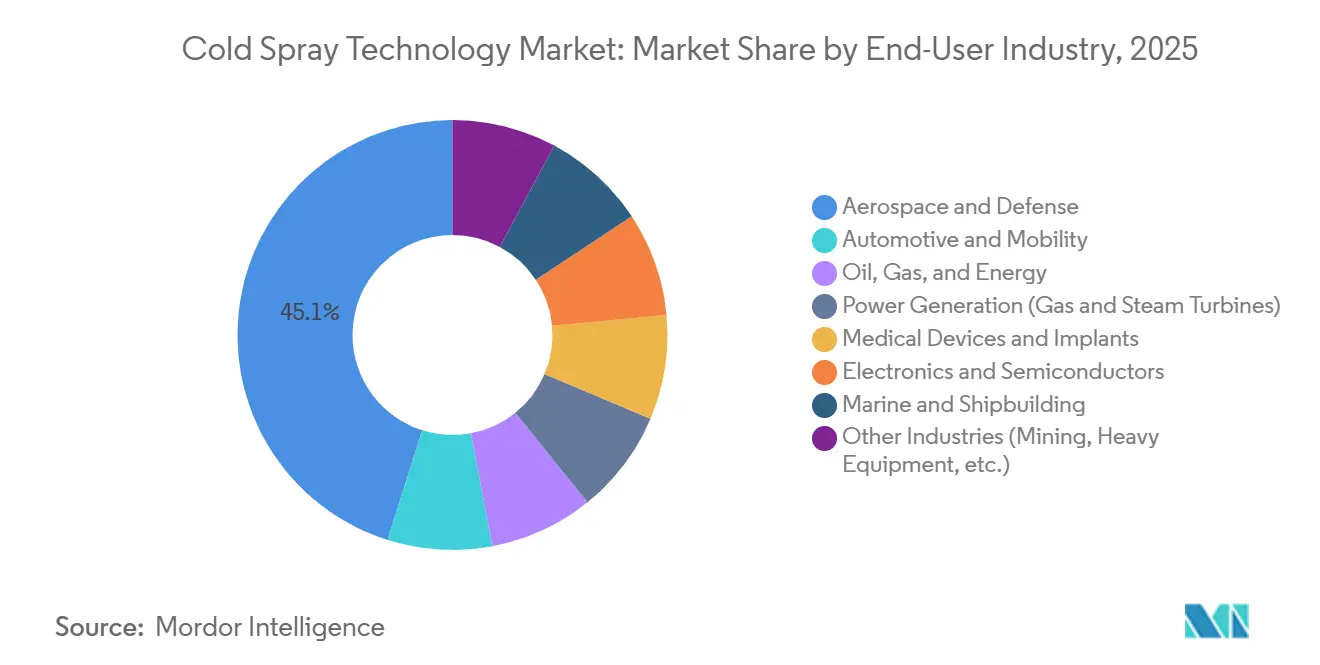

- By end-user industry, aerospace and defense led with 45.11% revenue share in 2025; electronics and semiconductors are the fastest-expanding segment at an 8.33% CAGR to 2031.

- By process/system type, high-pressure equipment captured 69.89% of 2025 revenue, whereas micro-cold spray is forecast to grow at 8.51% CAGR through 2031.

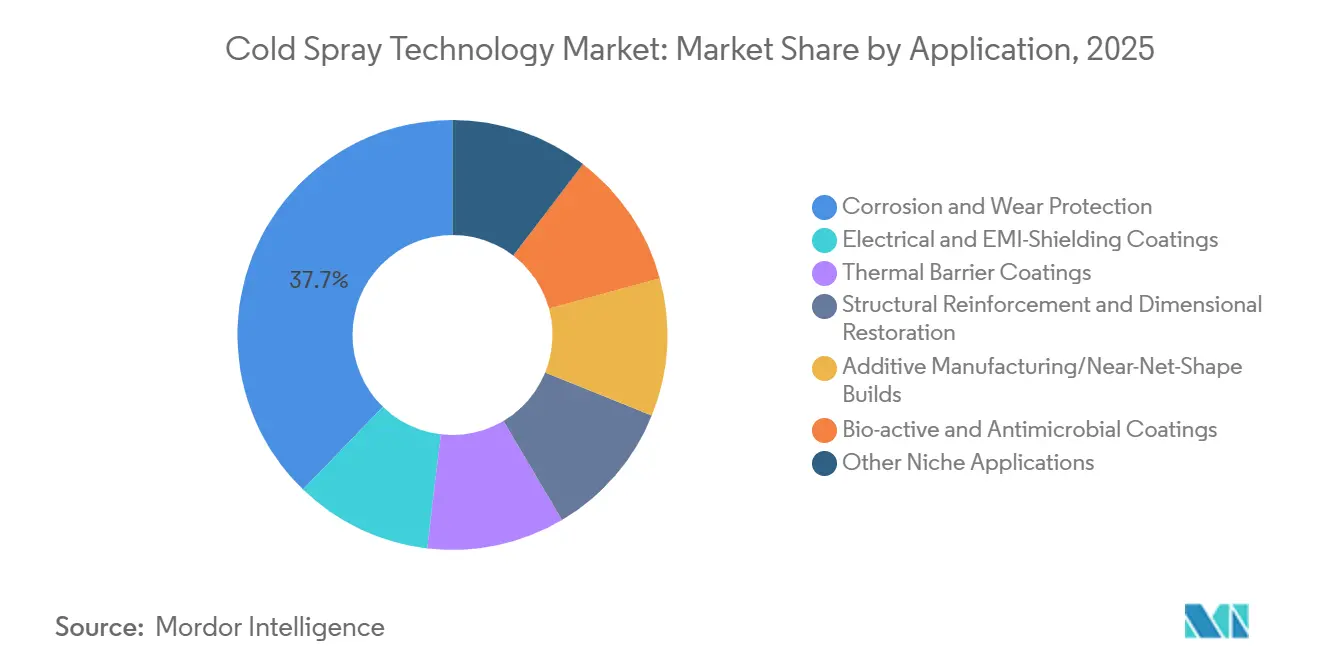

- By application, corrosion and wear protection held a 37.75% share in 2025, while additive manufacturing and near-net-shape builds are positioned for an 8.02% CAGR over 2026-2031.

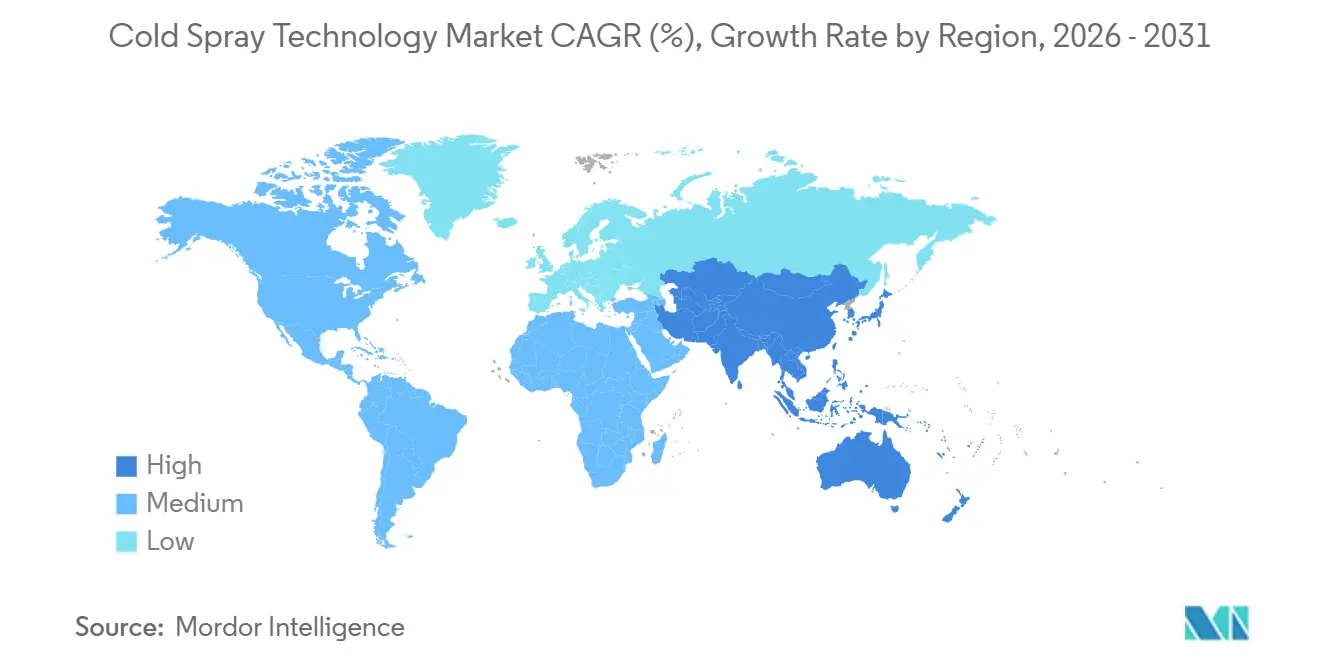

- By geography, North America led with 38.88% revenue in 2025; Asia-Pacific is set to post the fastest regional CAGR of 8.57% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cold Spray Technology Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for advanced surface-coating technologies in aerospace and defense | +2.1% | Global, with concentration in North America, Europe, and Asia-Pacific defense hubs | Medium term (2-4 years) |

| Increasing adoption for component repair and life-extension of critical assets | +1.8% | North America and Europe (mature MRO infrastructure), expanding to the Middle East and Asia-Pacific offshore energy | Long term (≥ 4 years) |

| Rising investment in additive manufacturing of lightweight metals and alloys | +1.5% | North America, Europe, and Asia-Pacific (China, Japan, South Korea) | Medium term (2-4 years) |

| Rapid emergence of supersonic portable cold-spray units for naval and offshore repairs | +1.2% | Global, with early adoption in North America, Europe, and Australia, expanding to the Middle East and the Asia-Pacific maritime sectors | Short term (≤ 2 years) |

| Low-cost air-based systems broadening SME access in developing economies | +0.9% | Asia-Pacific (India, ASEAN), South America, and Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Advanced Surface-Coating Technologies in Aerospace and Defense

High-value turbine, compressor, and structural parts require bond coats that resist oxidation without causing thermal distortion. By September 2025, original equipment manufacturers (OEMs) and depots globally installed over 100 EvoCSII systems, replacing plasma spraying on critical rotating components. Royal NLR’s 2025 procurement highlighted European public-sector support for solid-state deposition research and development (R&D). A shaft repair on the USS North Dakota, conducted by the U.S. Navy, achieved a 98.5% cost reduction, demonstrating significant life-cycle savings for budget-constrained defense agencies. Laboratory studies confirm that bond coats form slower oxides at 1,100°C compared to air-plasma-sprayed counterparts, indicating superior high-temperature durability. With cold spray aligning with MIL-STD-3021, qualification timelines have reduced from 18 months to under a year, enabling faster fleet deployment.

Increasing Adoption for Component Repair and Life-Extension of Critical Assets

Cold spray’s solid-state deposition restores dimensional tolerances without heat-affected zones, allowing multiple life-cycle resets for shafts, blades, and landing-gear lugs. VRC field teams restore propulsion hardware on-site, avoiding the logistics costs associated with depot shipments. India’s International Advanced Research Center for Powder Metallurgy and New Materials (ARCI) validated the mechanical integrity of 6061 and 7075 aluminum repairs for Boeing airframe parts, expanding the range of qualified materials[1]“Indigenously Developed Cold Spray Technology Can Reduce Costs of Repair of Engineering Components,” Department of Science & Technology, dst.gov.in. The U.S. Department of Energy included cold spray in its 2025 roadmap for power-sector turbine refurbishment, reflecting growing cross-industry confidence. ATL Turbine Services’ acquisition of dual Oerlikon Surface Two cells in December 2025 demonstrates the method’s return on investment for commercial maintenance, repair, and overhaul (MRO) contracts. Documented fatigue-life improvements from compressive residual stress support extended inspection intervals for critical rotating parts.

Rising Investment in Additive Manufacturing of Lightweight Metals and Alloys

Deposition rates exceeding 10 tons per hour enable near-net builds of titanium, aluminum, and copper alloys, achieving part sizes not feasible with powder-bed fusion. SPEE3D’s TitanSPEE3D is producing Ti-6Al-4V hull inserts for naval programs, with Austal reporting shorter lead times compared to castings. Linde is optimizing copper-nickel (Cu-Ni) builds for the United States Navy seawater systems by integrating gas-supply analytics with closed-loop process control. Cold spray mitigates oxidation risks common in laser melting, making it a viable option for oxygen-reactive metals. Research into nozzle miniaturization is reducing exit diameters below 4 millimeters, a critical requirement for achieving finer wall thicknesses in aerospace brackets and satellite panels.

Rapid Emergence of Supersonic Portable Cold-Spray Units for Naval and Offshore Repairs

Raptor and TitanSPEE3D systems achieve supersonic particle velocities with controlled gas flows, enabling deployment on flight decks and remote offshore rigs. The Australian Army fabricates spare parts at forward bases, reducing resupply lead times from weeks to hours. Université de Limoges adopted Titomic’s D523 mobile platform for aerospace trials in the field. Woodside Energy reported reduced vessel downtime after using VRC’s portable cartridge feeders to rebuild hull valve seats at the quayside. While portable devices may have lower deposition efficiency, their ability to return multi-million-dollar assets to service within a single shift provides significant value in maritime operations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and limited awareness among small manufacturers | -0.8% | Global, with acute impact in South America, the Middle East & Africa, and developing Asia-Pacific economies | Medium term (2-4 years) |

| Coating-adhesion challenges on complex multi-material geometries | -0.5% | Global, particularly in the automotive and electronics sectors with hybrid substrate assemblies | Long term (≥ 4 years) |

| Absence of standardized qualification protocols for Cold Spray Additive Manufacturing in regulated industries | -0.4% | Global, with regulatory fragmentation most pronounced across North America, Europe, and the Asia-Pacific jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Limited Awareness Among Small Manufacturers

Base-build systems, including helium management and powder feeders, often exceed USD 500,000, a cost that many small and medium enterprises (SMEs) find challenging to afford. To address this, the International Advanced Research Center for Powder Metallurgy and New Materials (ARCI) has developed air-based prototypes that use compressed air to reduce equipment costs. However, these systems still require skilled operators and a dependable supply chain for quality feedstock. Leasing models and shared-service bureaus are being introduced to mitigate upfront costs, though adoption remains limited. Vendor training academies in India, Brazil, and South Africa are working to enhance the technician talent pool, but accreditation pathways are not yet standardized. Until operating expenses decrease or financial incentives expand, adoption outside Tier 1 aerospace and defense sectors is expected to grow gradually.

Coating-Adhesion Challenges on Complex Multi-Material Geometries

Bond strength decreases in hybrid assemblies when impact angles deviate from normal incidence. Research on carbon-fiber-reinforced polymer metallization demonstrates that achieving bond strengths above 30 megapascals (MPa) requires precise control of particle velocity windows, which is difficult to maintain on curved surfaces. Finite-element modeling indicates that silicon carbide (SiC) particles must embed deeper than half their diameter to prevent cyclic delamination, a threshold that is challenging to achieve on recessed features. For example, automotive battery casings that combine aluminum frames and polymer separators face micro-cracking after thermal cycles due to mismatched thermal expansion. Techniques such as robotic multi-axis heads, in-situ laser pre-heating, and hybrid ultrasonic consolidation are being tested to expand the process window, but comprehensive field data is still limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Metals Dominate, Yet Composites Gain Traction

In 2025, metals accounted for 67.88% of the revenue, with aluminum, copper, titanium, and nickel alloys being the primary choices for aerospace and energy refurbishments. This positions metals at the forefront of the cold spray technology market. Composite and hybrid substrates currently hold a smaller share but are witnessing an 8.02% compound annual growth rate (CAGR). Original equipment manufacturers (OEMs) are using metalized carbon-fiber panels for purposes like electromagnetic shielding and protection against lightning strikes[2]“Powders for Cold Spray Deposition,” Fukuda Metal Foil & Powder, fukuda-kyoto.co.jp. Ceramics maintain a specialized role in thermal barrier stacks, and polymer substrates, particularly polyether ether ketone (PEEK), are gaining traction in orthopedic implants.

The adoption of composites is driven by cold spray's capability to coat temperature-sensitive fibers without degrading the matrix. Japanese researchers have optimized copper-chromium-zirconium (CuCrZr) powders, enhancing deposition efficiency on carbon fiber-reinforced polymer (CFRP) housings for 5G antennas. Lunar regolith-aluminum composites have been demonstrated for potential use in extraterrestrial construction, indicating future space applications as launch costs become more viable. This diversification in substrates is broadening the cold spray technology market and enabling innovative design approaches in aerospace, automotive, and electronics.

By End-User Industry: Defense Anchors, Electronics Accelerates

Aerospace and defense captured 45.11% of the end-user revenue in 2025, reflecting their reliance on cold spray for turbine blade repairs, structural fittings, and abradable seals. Electronics and semiconductors are the fastest-growing sector, with an 8.33% CAGR through 2031. This growth is driven by the performance of dense copper vias over traditional solder pastes in high-power modules. Automotive OEMs are adopting cold spray for thermal channels in battery packs, and oil and gas operators are utilizing it for subsea anti-corrosion overlays, moving away from thermally sprayed Inconel.

While defense maintains a stronghold with significant entry barriers, adjacent sectors are broadening the overall cold spray technology market. The 5G infrastructure's reliance on cold-sprayed copper for electromagnetic interference (EMI) shielding over polymer composites is driving electronics revenue, bringing it closer to traditional aerospace earnings. Medical devices are benefiting from antimicrobial silver-copper surfaces, which are durable enough to endure sterilization. Marine users value the swift repairs available at docking sites, aligning with the trend of portability.

By Process/System Type: High-Pressure Leads, Micro-Cold Spray Surges

High-pressure systems accounted for 69.89% of the 2025 revenue, as they utilize helium or high-temperature nitrogen flows to achieve the density essential for flight-critical components. This grants high-pressure systems the largest market share in the cold spray technology market. Micro-cold spray is set to experience an 8.51% CAGR, especially as feature resolutions drop below 100 micrometers (µm), making it suitable for applications like semiconductor packaging and dental stents.

Air-based and medium-pressure systems are broadening access in cost-sensitive markets, though they compromise on deposit density. For instance, Plasma Giken’s PCS-1000v2 achieved 0.1% porosity on aluminum alloy 6061 (A6061) using optimized helium parameters. The International Advanced Research Center for Powder Metallurgy and New Materials (ARCI)’s air-propelled prototype reduced consumable costs by 40% for small and medium enterprises (SMEs) in repair. Portable rigs, like the Raptor, offer on-deck mobility, albeit with reduced throughput. However, their utility in defense and offshore scenarios keeps demand steady.

By Application: Corrosion Protection Prevails, Additive Manufacturing Ascends

Corrosion and wear overlays made up 37.75% of the 2025 revenue, highlighting cold spray's role in extending the life of assets in marine, mining, and oilfield sectors. Additive manufacturing and near-net-shape builds are forecast to grow at an 8.02% CAGR until 2031, as deposition rates exceed 10 tons per hour, making large titanium structures financially viable. Telecommunications are driving demand for electrical shielding coatings, while cold-sprayed metal-chromium-aluminum-yttrium bond coats in thermal barrier stacks are slowing oxide growth at temperatures of 1,100°C.

Dimensional restoration maintains a consistent revenue share, as the induced compressive residual stresses enhance fatigue performance in rotating machinery. In orthopedics, bioactive layers on titanium and PEEK implants, utilizing materials like hydroxyapatite or tantalum-silver, are gaining traction. In specialized fields, regolith-based composites are being explored for lunar infrastructure and sacrificial mold forming, showcasing the design possibilities that solid-state deposition offers.

Geography Analysis

In 2025, North America accounted for 38.88% of the revenue, supported by the U.S. Department of Defense's procurement activities and the Federal Aviation Administration's (FAA) expedited repair approvals. The region's cold spray technology market benefits from a well-established ecosystem comprising equipment manufacturers, powder suppliers, and university testing centers. Initiatives like America Makes are funding essential nozzle research, while state tax incentives are encouraging private Maintenance, Repair, and Overhaul (MRO) shops to invest.

Asia-Pacific, while smaller in size currently, is projected to be the fastest-growing region with an 8.57% Compound Annual Growth Rate (CAGR) through 2031. China's focus on turbine-blade refurbishments for aero-engines and gas turbines is driving this growth. India's International Advanced Research Center for Powder Metallurgy and New Materials (ARCI) is commercializing a domestic air-based system, reflecting policy support for local manufacturing. Japan's Fukuda Metal Foil & Powder and Plasma Giken are improving feedstock sphericity and automated lay-ups, positioning themselves to serve automotive and consumer-electronics Original Equipment Manufacturers (OEMs).

Europe is balancing sustainability mandates with its established aerospace clusters. Titomic Europe, with Dutch 3D Printing Knowledge (3D PK) funding, is scaling additive builds for defense and energy applications, reflecting the region's focus on near-net-shape production. Germany’s Oerlikon is integrating cold spray with laser cladding to provide hybrid repairs for Lufthansa Technik. France’s Safran, in collaboration with the French Alternative Energies and Atomic Energy Commission (CEA), is conducting bond-coat trials. South America and the Middle East & Africa are in the early stages of development but show potential in mining equipment repairs and subsea oil infrastructure. Demonstrations on offshore platforms in the Gulf are expected to drive future regional investments, pending the finalization of the NORSOK M-501 qualification.

Competitive Landscape

The cold spray technology market is moderately concentrated. The five largest Original Equipment Manufacturers (OEMs) continue to dominate high-pressure equipment sales, although portable entrants are contributing to a fragmented market share. Impact Innovations utilizes its presence in 30 countries to cross-sell EvoCSII upgrades. Oerlikon integrates helium recovery with its powder supply to enhance its offerings. Plasma Giken differentiates itself with a nozzle design that achieves less than 0.2% porosity on aluminum, meeting specifications valued by aerospace industry leaders.

SPEE3D and VRC Metal Systems focus on expeditionary logistics. SPEE3D’s containerized Electro Magnetic Unit (EMU) can be redeployed within 3 hours, making it suitable for disaster-relief operations. VRC’s Raptor includes a 20-ft hose set that connects directly to shipboard compressed-air lines, eliminating the need for external gas cylinders. Linde’s LINSPRAY Connect platform combines gas analytics with deposition monitoring, generating recurring revenue from consumables and cloud-based diagnostics.

Vertical integration through acquisitions is transforming the service segment. Bodycote’s acquisition of Spectrum Thermal Processing in January 2026 added two cold-spray bays in Ohio and Texas, expanding its turbine-component service capabilities. Machine-tool OEMs and cold-spray specialists are jointly developing hybrid machining cells that integrate CNC finishing cuts with in-situ deposition, offering comprehensive repair solutions. These advancements address the current limitations of cold spray technology and extend its application to medium-complexity geometries.

Cold Spray Technology Industry Leaders

Titomic Limited

Bodycote

CenterLine (Windsor) Limited

Curtiss-Wright Corporation

OC Oerlikon Management AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bodycote acquired Spectrum Thermal Processing, expanding North America's capacity for aerospace and defense component refurbishment. This acquisition aligns with the growing adoption of cold spray technology, which is increasingly used for repairing and enhancing components in these industries.

- November 2025: ATL Turbine Services has installed two Oerlikon Surface Two cells, leveraging cold spray technology to enhance the durability of gas-turbine blades used in aviation and power generation. This installation aims to reduce maintenance costs and improve operational efficiency for operators in these industries.

Global Cold Spray Technology Market Report Scope

Cold spray technology accelerates metallic powder particles using a supersonic gas jet, enabling high-velocity deposition. This solid-state process is used to form coatings or repair parts. When these particles strike the substrate, they deform significantly, creating a metallurgical bond without melting. This process prevents oxidation, phase changes, and heat-affected zones.

The cold spray technology market is segmented by substrate, end-user industry, process/system type, application, and geography. By substrate, the market is segmented into metals, ceramics, polymers and plastics, and composite and hybrid substrates. By end-user industry, the market is segmented into aerospace and defense, automotive and mobility, oil, gas, and energy, power generation (gas and steam turbines), medical devices and implants, electronics and semiconductors, marine and shipbuilding, and other industries (mining, heavy equipment, etc.). By process/system type, the market is segmented into high-pressure cold spray (HPCS), low/medium-pressure cold spray (L/MPCS), air-based cold spray (ABCs), and micro-cold spray. By application, the market is segmented into corrosion and wear protection, electrical and EMI-shielding coatings, thermal barrier coatings, structural reinforcement and dimensional restoration, additive manufacturing/near-net-shape builds, bio-active and antimicrobial coatings, and other niche applications. The report also covers the market size and forecasts for cold spray technology in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Metals |

| Ceramics |

| Polymers and Plastics |

| Composite and Hybrid Substrates |

| Aerospace and Defense |

| Automotive and Mobility |

| Oil, Gas, and Energy |

| Power Generation (Gas and Steam Turbines) |

| Medical Devices and Implants |

| Electronics and Semiconductors |

| Marine and Shipbuilding |

| Other Industries (Mining, Heavy Equipment, etc.) |

| High-Pressure Cold Spray (HPCS) |

| Low/Medium-Pressure Cold Spray (L/MPCS) |

| Air-Based Cold Spray (ABCS) |

| Micro-Cold Spray |

| Corrosion and Wear Protection |

| Electrical and EMI-Shielding Coatings |

| Thermal Barrier Coatings |

| Structural Reinforcement and Dimensional Restoration |

| Additive Manufacturing/Near-Net-Shape Builds |

| Bio-active and Antimicrobial Coatings |

| Other Niche Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Substrate | Metals | |

| Ceramics | ||

| Polymers and Plastics | ||

| Composite and Hybrid Substrates | ||

| By End-User Industry | Aerospace and Defense | |

| Automotive and Mobility | ||

| Oil, Gas, and Energy | ||

| Power Generation (Gas and Steam Turbines) | ||

| Medical Devices and Implants | ||

| Electronics and Semiconductors | ||

| Marine and Shipbuilding | ||

| Other Industries (Mining, Heavy Equipment, etc.) | ||

| By Process/System Type | High-Pressure Cold Spray (HPCS) | |

| Low/Medium-Pressure Cold Spray (L/MPCS) | ||

| Air-Based Cold Spray (ABCS) | ||

| Micro-Cold Spray | ||

| By Application | Corrosion and Wear Protection | |

| Electrical and EMI-Shielding Coatings | ||

| Thermal Barrier Coatings | ||

| Structural Reinforcement and Dimensional Restoration | ||

| Additive Manufacturing/Near-Net-Shape Builds | ||

| Bio-active and Antimicrobial Coatings | ||

| Other Niche Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the cold spray technology market in 2031?

The Cold Spray Technology Market size is expected to grow from USD 1.78 billion in 2025 to USD 1.92 billion in 2026 and is forecast to reach USD 2.81 billion by 2031 at 7.92% CAGR over 2026-2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to advance at an 8.57% CAGR due to turbine-blade refurbishment programs and expanding electronics demand.

Which end-user segment is expanding most rapidly?

Electronics and semiconductors, driven by dense copper interfaces and EMI shielding, are growing at an 8.33% CAGR to 2031.

How do portable cold spray units impact adoption?

Supersonic portable systems enable on-site repairs for naval, aerospace, and offshore assets, reducing downtime and cutting logistics costs.

Page last updated on: