Steel Tire Cord Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

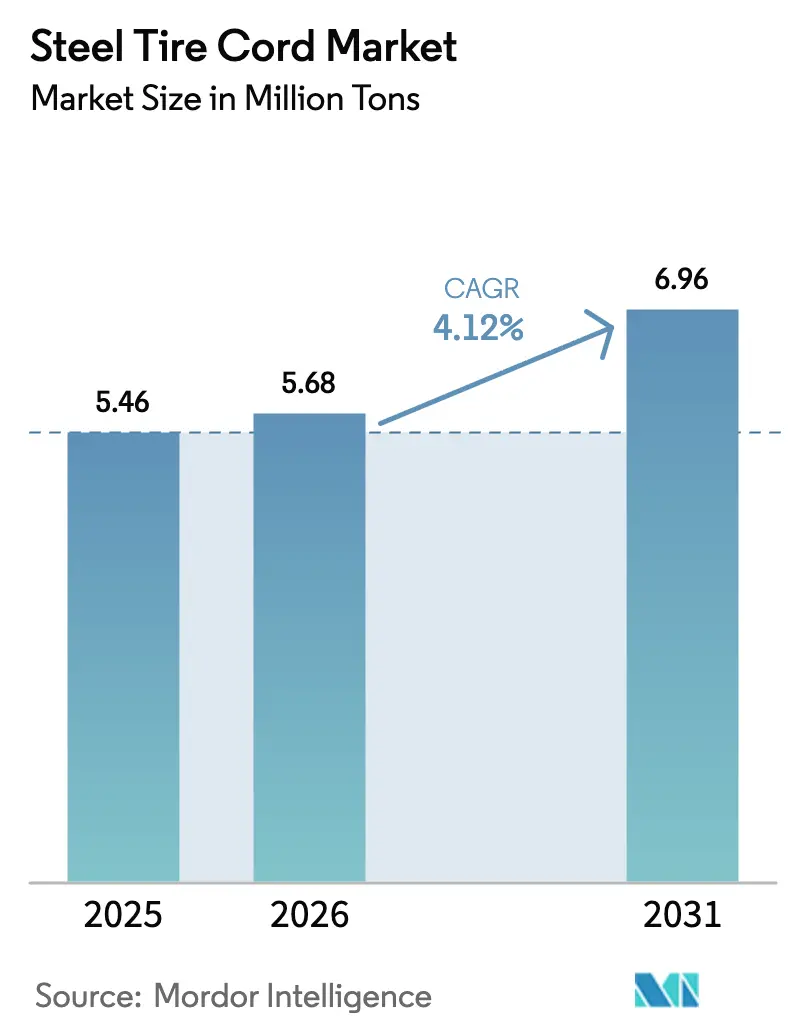

| Market Volume (2026) | 5.68 Million tons |

| Market Volume (2031) | 6.96 Million tons |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

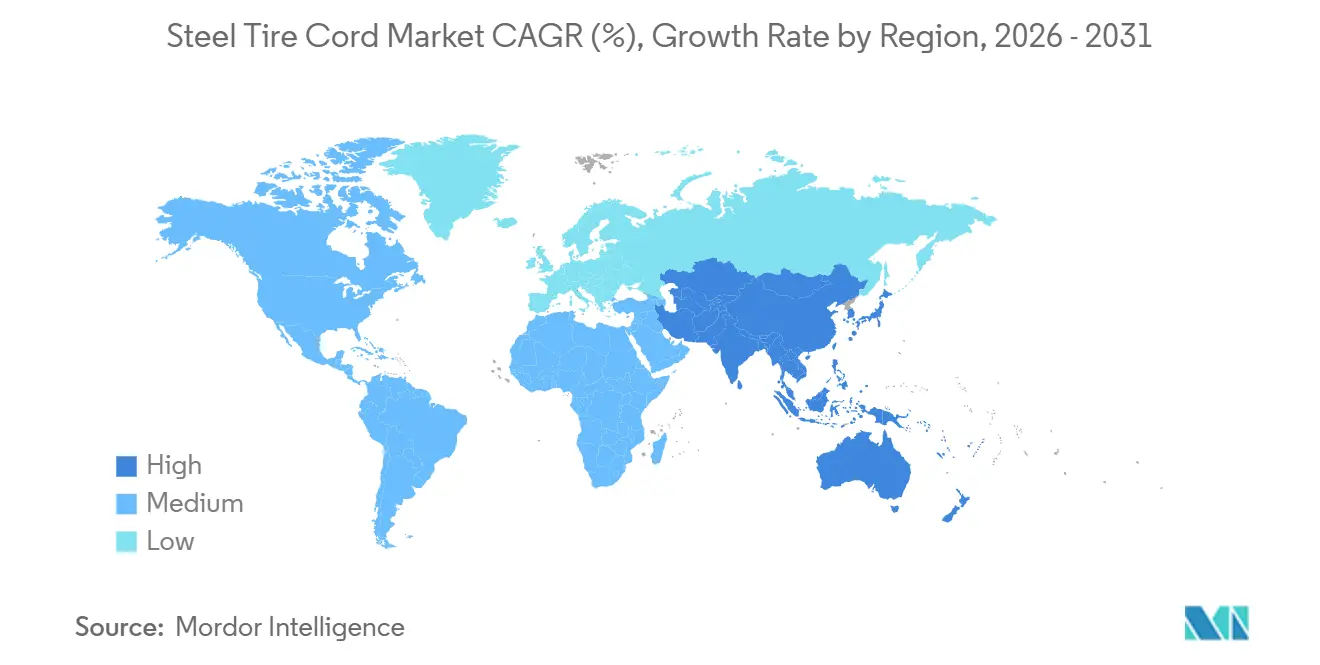

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Steel Tire Cord Market Analysis by Mordor Intelligence

The Steel Tire Cord Market size is expected to grow from 5.46 million tons in 2025 to 5.68 million tons in 2026 and is forecast to reach 6.96 million tons by 2031 at a 4.12% CAGR over 2026-2031. A tightening focus on electric-vehicle (EV) lightweighting, Asia’s accelerating radialization of truck tires, and regulatory pressure for low-rolling-resistance designs are reshaping demand patterns. OEMs now specify ultra-thin, high-tensile cords that pare 200-300 grams from each EV tire, while Asian truck fleets convert from bias-ply to radial designs to capture 8-12% fuel savings. Cost competition is intensifying as Chinese producers leverage wire-rod integration to undercut Western incumbents by 12-18% on standard grades. At the same time, premium opportunities have opened in sensor-embedded cords and cobalt-free coatings that meet tightening EU chemical restrictions.

Key Report Takeaways

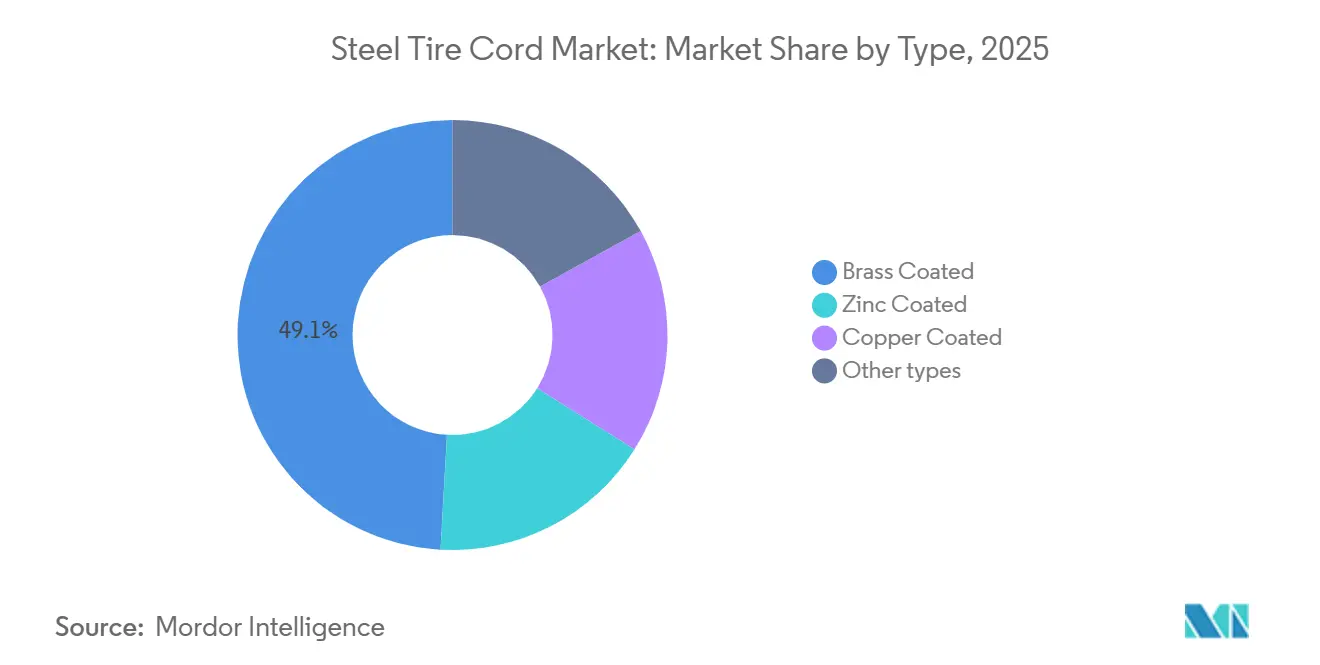

- By type, brass-coated cord captured 49.12% of the steel tire cord market share in 2025, and its 4.83% CAGR through 2031 positions it as both the largest and fastest-growing coating category.

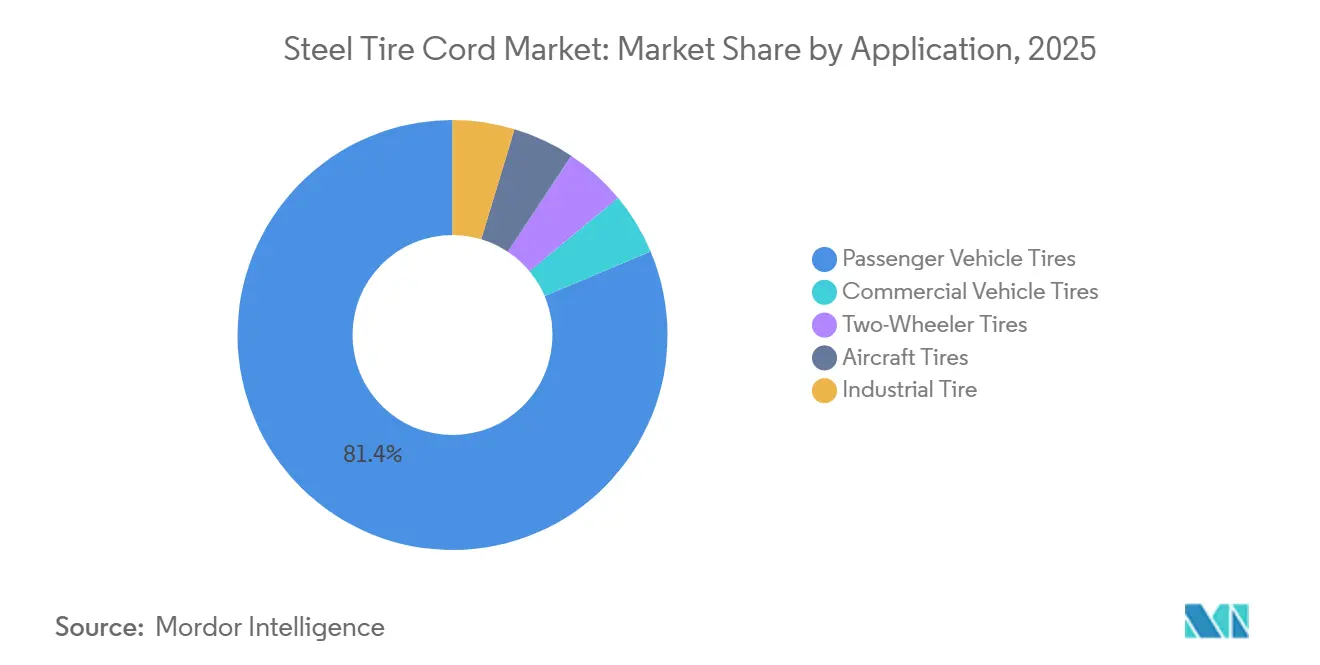

- By application, passenger vehicle tires commanded an 81.35% share of the steel tire cord market size in 2025; this application is advancing at a 4.22% CAGR to 2031.

- By geography, Asia-Pacific accounted for 50.22% of the steel tire cord market share in 2025, and the region is projected to expand at a 5.12% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Steel Tire Cord Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid radialization of commercial-vehicle tires | +1.2% | Asia-Pacific, spillover to MEA and South America | Medium term (2-4 years) |

| Sustainability push for low-rolling-resistance tires | +0.9% | Europe, North America, APAC premiums | Long term (≥4 years) |

| EV-specific ultra-flex fatigue-resistant cord demand | +1.5% | Global EV hubs | Short term (≤2 years) |

| OEM shift to ultra-thin high-tensile cords | +1.1% | Global OEM bases | Medium term (2-4 years) |

| Sensor-embedded smart cords | +0.6% | North America, Europe, APAC pilots | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Radialization of Commercial-Vehicle Tires

Asia’s truck-tire market is shifting from bias-ply to radial designs, because fleets gain 8-12% fuel savings and 40-60% longer tire life. China set a 96% radialization target for 2025, creating an incremental 1.2-1.5 million-ton steel tire cord market opportunity[1]Ministry of Industry and Information Technology, “14th Five-Year Plan for the Tire Industry,” miit.gov.cn. India is following suit as OEMs expand radial capacity for margin premiums of 15-20% over bias equivalents. ASEAN governments support radial export growth, exemplified by Thailand’s approval of Xingda’s USD 400 million, 260,000-ton plant that will start up in 2027. The result is a two-tier steel tire cord market: high-tensile grades for premium radials and standard grades for cost-sensitive fleets. Chinese integration into upstream wire rod sustains price advantages that accelerate adoption.

Sustainability Push for Low-Rolling-Resistance Tires

EU Regulation 2020/740 scores rolling resistance from A to E, prompting tire makers to redesign belt packages around thinner, more flexible cords that cut hysteresis losses by 8-10% and improve fuel economy by 0.3-0.5 liters per 100 km. Bekaert responded with cords containing ≥50% recycled steel, certified under ISO 14021, giving tire firms a ready sustainability lever[2]Bekaert, “TAWI® Technical Data Sheet,” bekaert.com. Michelin’s 100% sustainable-material roadmap signals a closed-loop future where recycled cord feedstock differentiates suppliers. China is tightening domestic GB standards, and California’s clean-truck rules amplify the shift. Coating advances, notably zinc-cobalt and Cu-Sn layers, now deliver ISO 3801 fatigue compliance while reducing copper and zinc use by 10-15%, further lowering the carbon footprint.

EV-Specific Ultra-Flex Fatigue-Resistant Cord Demand

Instant torque and regenerative braking lift tangential forces by 20-30%, demanding cords with 1.5-2.0× the fatigue life of conventional grades. Continental’s 2024 patent on 3,080-4,190 N/mm² monofilaments trims each EV tire by 200-300 grams and recovers up to 0.5% vehicle range. Bridgestone’s 2026 divestment of commodity cord assets to Bekaert reflects a strategy to focus R&D on proprietary EV designs. Chinese producers are scaling similar high-tensile lines to secure contracts from BYD and NIO. As EV sales accelerate toward a 34% CAGR to 2030, these purpose-built cords emerge as the premium growth pocket within the steel tire cord market.

OEM Shift to Ultra-Thin High-Tensile Cords for Lightweighting

Automakers target 100-150 kg vehicle mass reduction, and every kilogram shaved from tires boosts EV range by 0.3-0.5%. Ultra-thin cords at 0.33-0.37 mm diameter now achieve >3,000 N/mm² tensile strength, replacing 0.40 mm cords without compromising puncture resistance. Premium OEMs pay 15-20% price uplifts for these cords, while volume brands blend high-tensile and standard grades. Brass plating struggles to coat such small wires uniformly, so Bekaert’s Cu/Zn/Fe ternary alloy secures consistent adhesion at 0.8-1.0 µm thickness and shows 15% better aged pull-out than traditional brass. The technology leap effectively splits supply between commodity producers and R&D-intensive leaders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer or aramid fiber substitution threat | -0.8% | Global premium passenger segments | Long term (≥4 years) |

| Tier-1 tire makers’ dual-sourcing diluting contracts | -0.5% | North America and Europe | Medium term (2-4 years) |

| Airless non-pneumatic tire pilots | -0.3% | North America and Europe logistics fleets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Polymer or Aramid Fiber Substitution Threat

Aramid and PET cords weigh 10-15% less than steel and cut rolling resistance by up to 8%, appealing to high-end passenger tires. Michelin’s glass-fiber reinforced UPTIS concept, protected by 19 patents, extended pilot life to 200,000 km on DHL fleets, foreshadowing broader deployment. Hyosung ran near 100% PET-cord utilization during 2024 capacity tightness, signaling pricing power. Yet these fibers fall short on tensile strength for heavy-duty or aircraft tires that face 200-320 psi pressures, keeping steel irreplaceable in those niches. Cord suppliers counter by offering hybrid steel-polymer belts that balance strength with weight reduction, blunting wholesale substitution risk.

Tier-1 Tire Makers’ Dual-Sourcing Diluting Contracts

Consolidated tire groups are splitting volumes among multiple cord vendors to reduce dependency and wring out price concessions. Hyosung’s exploration of a USD 1 billion cord divestiture in 2025 highlights margin pressure even on a 40% profit-contributing business. Bridgestone’s EUR 60 million sale of its Chinese and Thai cord assets to Bekaert points to similar cost-of-capital reprioritization. The US ITC’s 2024 investigation showed Thai truck-tire dumping margins up to 48.39% and revealed cord and bead wire form 12.4% of US tire raw-material costs, underlining buyer leverage. Producers respond through vertical integration and value-added services like custom coating design that raise switching costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Brass Coating Dominates Through Proven Adhesion Chemistry

Brass-coated cord captured 49.12% steel tire cord market share in 2025 as its Cu-Zn alloy forms durable CuₓS bonds during vulcanization, delivering 150-200 N initial pull-out and 70-80% retention after 1,000 hours at 80°C. The segment is tracking a 4.83% CAGR to 2031, supported by commercial-vehicle demand where reliability trumps cost. Zinc-cobalt variants are gaining in corrosive environments because 1.5 wt% Co raises salt-spray durability by 15-20%. Copper-only coatings, once niche, re-emerge as recyclability priorities rise. Ternary Cu/Zn/Fe alloys, exemplified by Bekaert’s TAWI, already show 15% better aged adhesion than brass and meet EU REACH cobalt-phase-out trajectories. Over the outlook period, cobalt-free and thinner coatings will widen premium-grade profit pools, while standard brass holds steady in cost-driven segments of the steel tire cord market.

Innovations accelerate differentiation. Bridgestone patented non-twisted cords with ternary coatings that allow thinner rubber skim, removing 100-150 grams per tire and helping EVs meet range targets. Michelin’s polybenzoxazine resin eliminates cobalt entirely and secures comparable adhesion, appealing to EU chemical-safety agendas. Chinese mills, flush with wire-rod overcapacity, discount zinc-coated grades by 8-12%, enabling budget-focused tire makers to switch without tooling changes. Consequently, brass retains dominance yet faces gradual dilution from specialty coatings within the broader steel tire cord market.

By Application: Passenger Vehicles Lead, Commercial Segments Accelerate

Passenger tires absorbed 81.35% of the 2025 volume and will grow at a 4.22% CAGR through 2031 as global vehicle parc expansion and EV replacements shorten duty cycles. Commercial-vehicle tires show the highest incremental steel tire cord market size gains because radialization in China and India increases cord content from 1 kg to around 3 kg per tire. Two-wheelers add a steady but low-intensity demand of 0.3-0.5 kg per tire, while aircraft tires remain technologically critical despite minimal volume. Industrial segments benefit from construction and mining booms in Brazil, Saudi Arabia, and India’s USD 1.4 trillion infrastructure pipeline.

Application mix is fragmenting. EV passenger tires require cords with double life-cycle fatigue limits, and premium OEMs are prepared to pay 20-30% premiums, lifting margins for R&D-driven suppliers. Long-haul trucking seeks high-tensile cords for durability, whereas urban logistics fleets opt for low-rolling-resistance grades. Two-wheeler radialization in ASEAN introduces steel cord to models that previously used nylon, a nascent but rising pocket inside the steel tire cord market. Technology spillovers from aircraft, such as 3,500-4,000 MPa cords, feed future automotive innovations, preserving a cross-segment knowledge flywheel.

Geography Analysis

Asia-Pacific anchored 50.22% of 2025 volume, driven by China’s 704 million-tire output target and 96% truck radialization push that together add 1.2-1.5 million tons cord demand. Regional CAGR sits at 5.12% as tire makers migrate to lower-cost ASEAN clusters. Xingda’s plant underscores this realignment and will lift the regional steel tire cord market capacity by 260,000 tons in 2027. India’s Production Linked Incentive scheme earmarked INR 6,322 crore (USD 725.7 million) to stimulate domestic specialty-steel investment, but Chinese wire-rod imports that surged 30% in 2024-2025 slashed local mill margins by up to 91%, slowing high-tensile upgrades. Japan and South Korea prune commodity capacity to fund EV materials, typified by Hyosung’s contemplated USD 1 billion exit.

In North America, the USMCA nudges some reshoring through Mexican expansions, yet 2024 USITC findings of up to 48.39% dumping margins on Thai truck tires highlight cost pressure. EV sales reached 1.4 million units in 2025, nudging demand for ultra-thin cords, but the installed-base effect keeps total tonnage moderate. Europe’s market share, as Regulation 2020/740 and looming Euro 7 abrasion limits, channels demand toward advanced coatings. Bekaert’s acquisition of Bridgestone’s Asian plants provides a footprint to serve European OEMs from cost-effective hubs.

South America and the Middle East Africa together grow in lockstep with resource investment. Brazil’s road-building surge lifted truck-tire output, and Continental invested USD 26.5 million in a conveyor-belt cord facility to tap mining demand. Saudi Arabia’s Vision 2030 infrastructure pipeline boosts OTR tire consumption, yet political and currency volatility keeps most cord imports Asia-sourced. Technology leapfrogging appears where new plants adopt EV-grade cords from inception, bypassing incremental traditional upgrades, thereby widening the geographic spread of premium products in the global steel tire cord market.

Competitive Landscape

The Steel Tire Cord market is consolidated. Chinese firms capitalize on vertical integration to deliver 12-18% cheaper standard grades, forcing Western incumbents to defend the premium end with proprietary coatings and co-development services. Bekaert’s February 2026 purchase of Bridgestone’s Chinese and Thai plants adds USD 86 million in revenue and secures cost-aligned capacity for European customers. Regulatory headwinds, notably EU REACH cobalt restrictions and tighter ISO fatigue standards for EV tires, reward producers with metallurgical and R&D depth, reinforcing entry barriers across the evolving steel tire cord market.

Steel Tire Cord Industry Leaders

Bekaert

Daye Co., Ltd.

HS HYOSUNG ADVANCED MATERIALS

Jiangsu Xingda Steel Tyre Cord Co., Ltd.

Tokusen Kogyo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bekaert inked a deal with Bridgestone, setting its sights on Bridgestone's tire reinforcement operations in China and Thailand. The agreement not only includes a long-term supply pact but also the handover of two tire cord manufacturing sites. The deal is on track to be finalized in the first half of 2026.

- July 2025: Bain Capital, a US private investment firm, revealed its intention to purchase the tire steel cord division of HS Hyosung Advanced Materials Corp. The deal is valued at approximately USD 1.1 billion.

Global Steel Tire Cord Market Report Scope

The steel tire cord is a combination of numerous thin wires that help tires absorb shock while improving passengers' comfort. It is made of a high-carbon steel surface with brass or a special purpose of fine steel wire or rope. Steel tire cord reduces a tire’s weight and rolling resistance, helping to create sustainable tires. It also offers longer tire life and improved adhesion at a lower cost. Steel tire cords can be medium, high, or super-strength and exhibit open, closed, extensible, or shock-resistant properties.

The steel tire cord market is segmented by material type, application, and geography. By material type, the market is segmented into brass-coated, zinc-coated, copper-coated, and other types (bronze-coated steel tire cords, nickel-coated steel tire cords, and polymer-coated steel tire cords). By application, the market is segmented into passenger vehicle tires, commercial vehicle tires, two-wheeler tires, aircraft tires, and industrial tires. The report also covers the market size and forecasts for the steel tire cord market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Brass Coated |

| Zinc Coated |

| Copper Coated |

| Other types |

| Passenger Vehicle Tires |

| Commercial Vehicle Tires |

| Two-Wheeler Tires |

| Aircraft Tires |

| Industrial Tire |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Brass Coated | |

| Zinc Coated | ||

| Copper Coated | ||

| Other types | ||

| By Application | Passenger Vehicle Tires | |

| Commercial Vehicle Tires | ||

| Two-Wheeler Tires | ||

| Aircraft Tires | ||

| Industrial Tire | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the steel tire cord market be by 2031?

It is projected to reach 6.96 million tons by 2031 at a 4.12% CAGR from 2026.

Which coating type leads global demand?

Brass-coated cord remains dominant with 49.12% share in 2025 and a 4.83% CAGR outlook.

Why is Asia-Pacific pivotal for suppliers?

The region already holds 50.22% of volume and benefits from China’s radialization policy plus ASEAN export growth, driving the fastest 5.12% CAGR.

What is the biggest growth driver through 2031?

EV-specific ultra-flex, high-tensile cords that address instant-torque fatigue loads add the largest 1.5% uplift to forecast CAGR.

How are companies defending margins?

Leaders invest in ultra-thin cords, cobalt-free coatings, and sensor-embedded designs while vertically integrating wire-rod to reduce input costs.

Page last updated on: