Insulated Shipper Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

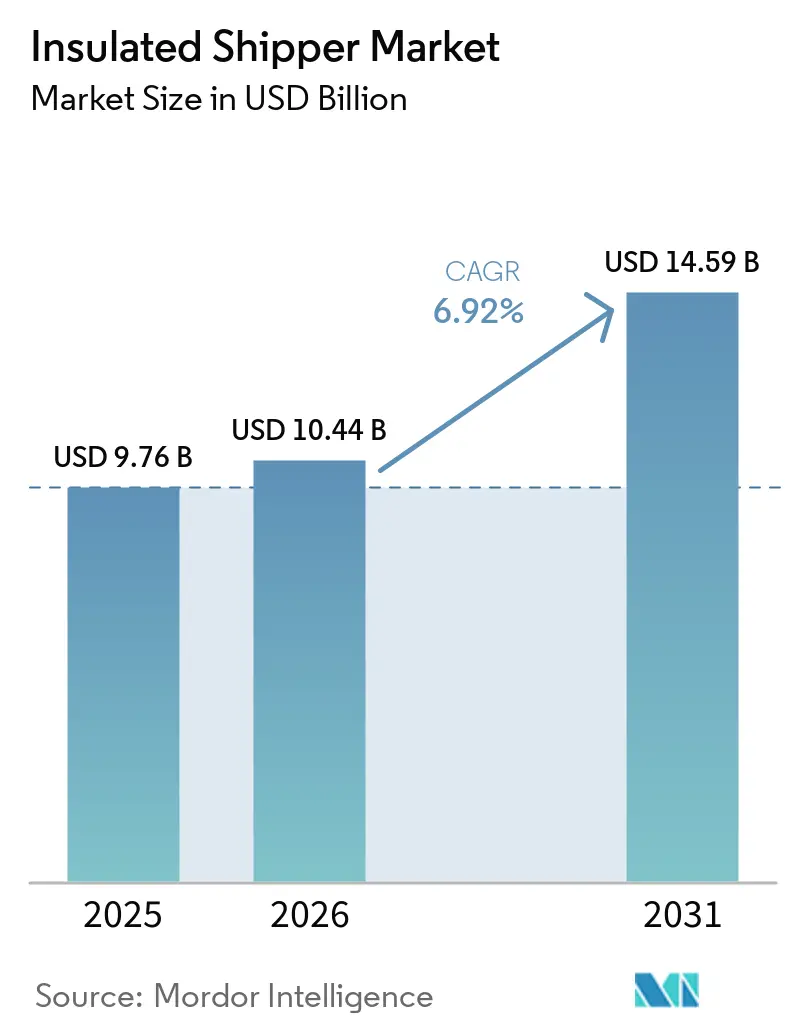

| Market Size (2026) | USD 10.44 Billion |

| Market Size (2031) | USD 14.59 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulated Shipper Market Analysis by Mordor Intelligence

The Insulated Shipper Market size was valued at USD 9.76 billion in 2025 and is estimated to grow from USD 10.44 billion in 2026 to reach USD 14.59 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Specialty medicines that cannot tolerate the conventional 2 °C-8 °C range, e-grocery’s ongoing efforts to achieve profitable last-mile cold-chain logistics, and stricter global regulations requiring enhanced passive-packaging validation are collectively driving structural demand growth. Pharmaceutical shippers are emphasizing narrower temperature ranges and extended hold times, leading to material innovations from expanded polystyrene (EPS) to vacuum-insulated panels (VIP) and bio-based alternatives. Logistics providers such as DHL, FedEx, and UPS are vertically integrating rental fleets to secure high-margin biologics shipments, while emerging markets are rapidly increasing cold-storage capacity. Cost pressures, supply constraints in fumed-silica powders, and the phase-out of single-use foam remain challenges, but the higher value of products continues to justify the premium costs of advanced packaging solutions.

Key Report Takeaways

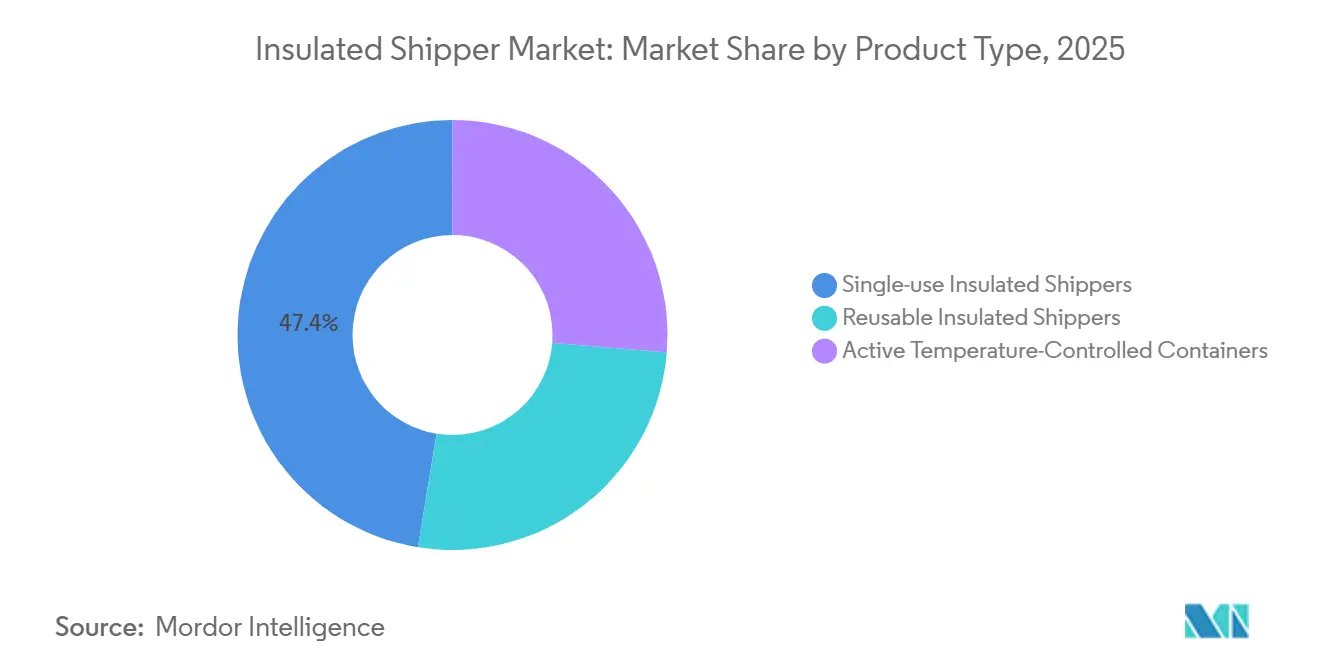

- By product type, single-use insulated shippers led with 47.44% of the insulated shipper market share in 2025 and are expected to advance at a 7.31% CAGR through 2031.

- By material, expanded polystyrene (EPS) captured 39.88% of the insulated shipper market share in 2025, while vacuum-insulated panels (VIP) are forecast to post the fastest 7.43% CAGR through 2031.

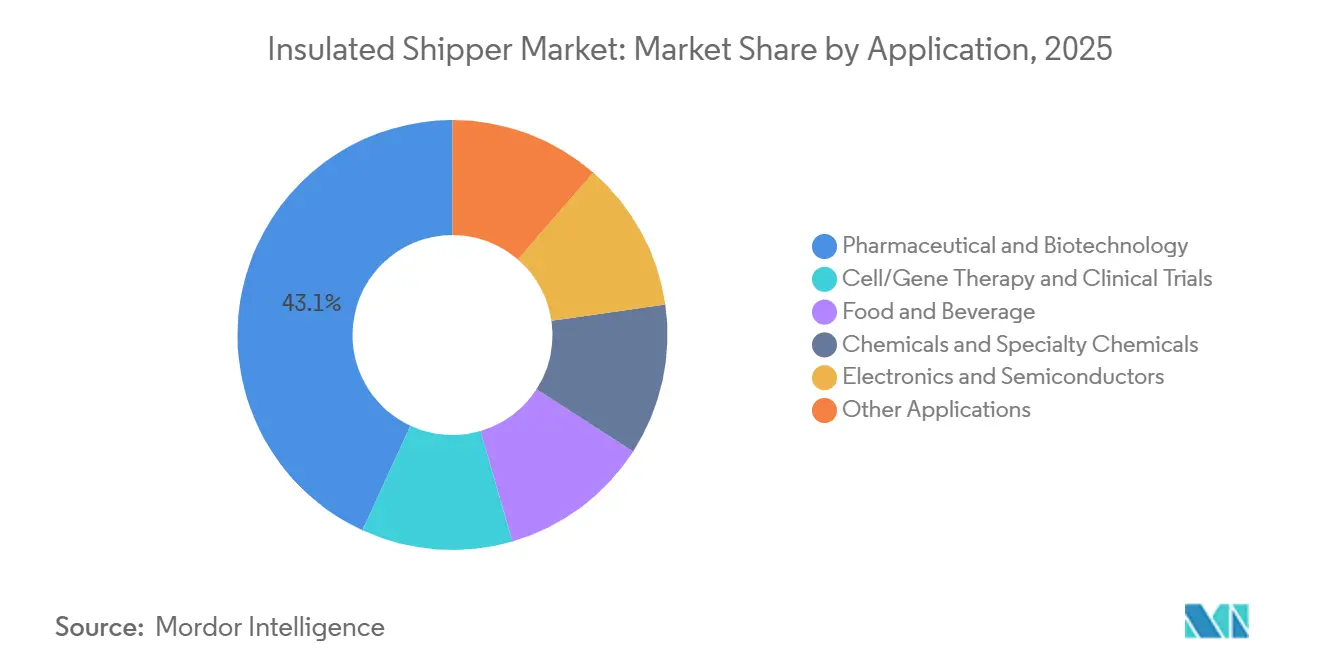

- By application, pharmaceutical and biotechnology represented 43.12% of the insulated shipper market share in 2025, while food and beverage is expected to be the fastest-growing segment at a 7.54% CAGR through 2031.

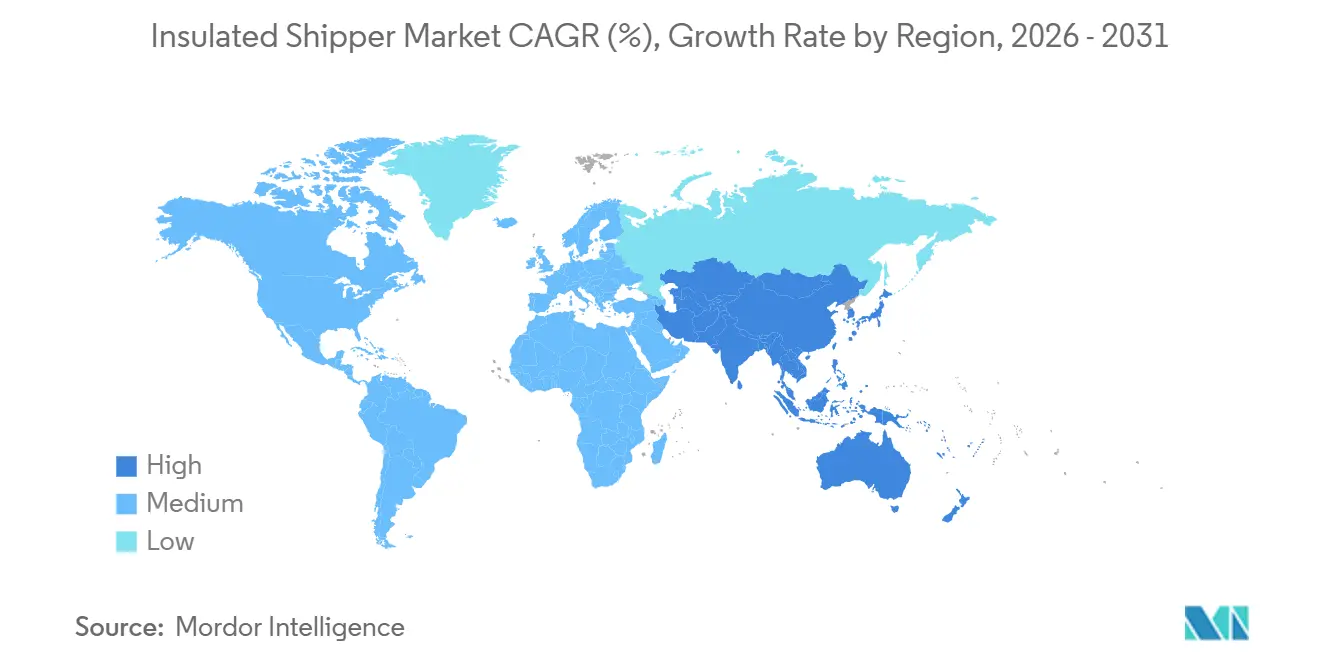

- By geography, North America commanded 46.44% of the insulated shipper market share in 2025; Asia-Pacific is projected to register a 7.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insulated Shipper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Temperature-sensitive pharma and biologics volume surge | +2.1% | Global, with concentration in North America, Europe, and emerging APAC markets (India, China, Vietnam) | Medium term (2-4 years) |

| E-grocery and meal-kit last-mile deliveries expand | +1.3% | North America and Europe core, with spillover to urban APAC and Latin America | Short term (≤ 2 years) |

| Cold-chain infrastructure modernization in emerging markets | +1.8% | APAC (India, Vietnam, ASEAN), Latin America (Brazil, Argentina), Middle-East and Africa (Saudi Arabia, South Africa) | Long term (≥ 4 years) |

| Regulatory mandates for validated passive packaging | +1.2% | Europe (EU GDP, PPWR), North America (FDA 21 CFR Part 11, FSMA Section 204), WHO PQS globally | Medium term (2-4 years) |

| AI-driven lane-specific predictive pack-out design adoption | +0.5% | North America and Europe early adopters, scaling to APAC by 2028-2030 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Temperature-Sensitive Pharma and Biologics Volume Surge

GLP-1 drugs, mRNA vaccines, and CAR-T therapies are driving the need for shippers to validate performance for extreme conditions, including temperatures as low as -196 °C for cell-and-gene therapy transportation. Nordic Cold Chain Solutions introduced the Nordic Express Pack in late 2025, the first ISTA-tested passive box designed for GLP-1 molecules. Latin American pharmaceutical sales reached USD 136.5 billion in 2024 and are growing at an annual rate of 9.7%, increasing the demand for GDP-compliant lanes with continuous monitoring. Growth in cold-chain logistics is increasingly tied to the rising share of high-value biologics, which require premium cold-chain services, rather than overall medicine volumes.

E-Grocery and Meal-Kit Last-Mile Deliveries Expand

Meal-kit companies and premium seafood exporters rely on overnight delivery services utilizing phase-change materials capable of withstanding weekend delays. Pelican BioThermal’s Crēdo Cargo, launched through Polar Group Brazil in March 2026, offers 120-168 hours of protection while reducing dry ice usage by 75%, thereby lowering freight weight and carbon emissions. However, reverse logistics remains a challenge, as returning reusable boxes can increase delivery costs by 15%-25%. IoT-enabled lease models are mitigating this issue by automating return labels and improving asset utilization rates to over 80%.

Cold-Chain Infrastructure Modernization in Emerging Markets

India has initiated 404 cold-chain projects, projected to grow its market from USD 13 billion in 2025 to USD 20 billion by 2030. Vietnam’s USD 34 million Dong Nai hub, set to open in 2026, will distribute biologics across ASEAN under stricter WHO and PIC-S standards. In Africa, solar-powered cold rooms are reducing energy consumption by 40%, highlighting how grid limitations are influencing insulated shipper specifications.

Regulatory Mandates for Validated Passive Packaging

Regulations such as FDA 21 CFR Part 11 now mandate electronic records and signatures for temperature logs, while the EU’s Packaging and Packaging Waste Regulation requires reusable or recyclable formats by 2030. Additionally, FSMA Section 204 imposes 24-hour digital traceability for high-risk foods, driving the adoption of IoT loggers, which increase per-shipment costs by USD 15-50. Validation expenses for new box designs have risen to as much as USD 100,000, creating significant entry barriers while reinforcing the competitive position of established players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of VIP/PCM configurations | -0.8% | Global, with acute impact in price-sensitive emerging markets (APAC, Latin America, Africa) | Medium term (2-4 years) |

| Single-use polymer foam phase-outs (EU, selected U.S. states) | -0.6% | Europe (EU Single-Use Plastics Directive), North America (California, Maryland, Maine bans) | Short term (≤ 2 years) |

| Supply bottlenecks in high-barrier films and fumed-silica powders | -0.4% | Global, with concentration in VIP-dependent pharmaceutical and biotech segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of VIP/PCM Configurations

VIPs provide 10 times the insulation of EPS but increase ownership costs by 125%-180%, restricting their use to high-value pharmaceuticals[1]Cold Chain SA, “VIP Cost Benchmarking 2025,” coldchainsa.com. Even with reuse, reverse-logistics costs can negate savings unless shipment volumes exceed 500 per week. Solutions like EcoFlex 3’s prepaid return labels demonstrate how process improvements can reduce costs, but the food industry is likely to continue using foams until regulatory changes mandate alternatives.

Single-Use Foam Phase-Outs (EU, selected U.S. states)

EU bans on EPS and U.S. state regulations are accelerating timelines for compliance, but bio-based alternatives are still in the scaling phase. In 2025, fumed-silica spot prices increased by over 18%, and custom VIP lead times extended to 20 weeks. Without rapid advancements in material innovation, operators may face margin pressures as compliance deadlines approach faster than substitute materials can be produced at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-use Insulated Shipper Leads the Market

Single-use insulated shippers held 47.44% of the insulated shipper market share in 2025 and are expected to grow at a 7.31% CAGR through 2031. Active temperature-controlled containers, designed for cargo requiring -70 °C to -196 °C, add USD 200-500 per trip. Developments like EcoFlex 3 and Crēdo on Demand are encouraging pharmaceutical shippers to consider reusable options, provided reverse-logistics costs drop below a 10% threshold.

Reusable programs perform well in areas with efficient return loops, such as metro corridors or closed pharmaceutical distribution systems. Europe’s 2030 reuse mandate is already influencing purchasing trends, while North America and Asia-Pacific lag due to less stringent policy frameworks.

By Material: Vacuum-Insulated Panels (VIP) Ascend Despite Price Premiums

Expanded polystyrene (EPS) accounted for 39.88% of 2025 revenue, but vacuum-insulated panels (VIP) are the fastest-growing segment, with a projected 7.43% CAGR through 2031. Shortages of silica and barrier films limit VIP adoption, but its low thermal conductivity of 0.0043 W/(m·K) makes it a preferred choice for pharmaceutical applications. Phase-change-material composites are also gaining momentum, supported by AI-driven lane matching that reduces dry-ice consumption. Polyurethane avoids many single-use bans but increases freight weights, partially offsetting its benefits. Bio-based fibers and wool show potential for strong thermal performance but require ISTA certification at scale.

Material preferences are diverging: high-margin biologics are likely to absorb VIP costs, while food shippers continue to rely on foams until regulations mandate alternatives. The long-term cost curve will be influenced more by the supply stability of fumed silica than by incremental process improvements.

By Application: Food and Beverage Becomes the Growth Engine

The pharmaceutical and biotechnology application represented 43.12% of 2025 demand, driven by premium pricing and strict validation requirements. However, the food and beverage segment is growing at a 7.54% CAGR through 2031, driven by increasing demand for seafood, specialty coffee, and meal kits beyond early-adopter metropolitan areas. Electronics and specialty chemicals also contribute steady revenue, requiring temperature stability of 20-25 °C and low humidity.

Premium food shipments often rely on EPS due to the high cost of VIP. Regulatory foam bans and IoT-enabled reuse models could change this dynamic by 2028-2029, enabling hybrid lease models to gain traction in perishables, similar to their adoption in pharmaceuticals.

Geography Analysis

North America’s 46.44% of the 2025 revenue share stems from mature pharma supply chains and early IoT adoption. FedEx Surround and UPS Premier provide sub-five-minute telemetry, and DHL’s USD 1.1 billion regional spend deepens network density. Canada and Mexico contribute cross-border flows that reinforce demand for ISTA-graded packaging.

Asia-Pacific is the fastest region at a 7.27% CAGR through 2031. India’s cold-chain outlays, and Vietnam’s Dong Nai hub underpin growth, while China invests in mRNA capacity that triggers demand for -70 °C lanes. However, uneven rural infrastructure means that boxes must perform beyond the standard ISTA hot-lane baselines.

Europe remains regulation-led: GDP, PPWR, and CEIV Pharma certifications accelerate reusable uptake and single-use foam withdrawals. DHL’s Florstadt expansion and va-Q-tec’s merged platform with Envirotainer underscore that integrated service plus validated hardware is the new competitive norm.

South America’s pharma spend is rising nearly 10% per year, but gaps in reverse logistics hamper reuse. Pelican’s Crēdo Cargo launch with Polar Group Brazil is an early test of rental economics under less-developed retrieval networks.

Middle-East and Africa show infrastructure growth yet live with 40% post-harvest spoilage. Solar-assisted cold rooms and Tower Cold Chain’s -80 °C boxes leased by Saudia Cargo illustrate solutions tuned for grid interruptions and vast desert transits.

Competitive Landscape

The insulated shipper market exhibits moderate concentration. va-Q-tec, Pelican BioThermal, Cold Chain Technologies, and Softbox own global validation labs and rental fleets, while DHL, FedEx, and UPS integrate boxes into premium healthcare lanes. va-Q-tec’s 2024 merger with Envirotainer combined active and passive portfolios, broadening one-stop offerings[2]Nordic Cold Chain Solutions, “va-Q-tec and Envirotainer Merger Close,” nordiccoldchain.com. DHL’s USD 2.3 billion cold-chain bet and UPS’s USD 1.6 billion Andlauer buyout highlight vertical integration that converts packaging from commodity spend to a loyalty lever.

Growth strategies revolve around AI-enabled pack-out design, IoT telemetry, and circular models that cut landfill waste. EcoFlex 3 has logged 5 million cycles, and Nordic Express Pack targets GLP-1 specialists with right-sized payload cavities. Supply-chain vulnerabilities in fumed silica remain a systemic risk; players with captive material channels hold cost advantages. New entrants will likely focus on ultra-low-temperature or bio-based niches where incumbents have yet to prove economics.

Insulated Shipper Industry Leaders

Cold Chain Technologies

ThermoSafe

Peli BioThermal LLC

SOFTBOX SYSTEMS (I) PVT. LIMITED

va-Q-tec Thermal Solutions GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cold Chain Technologies acquired Global Cold Chain Solutions to expand its product portfolio and global service network. The acquisition highlighted the company's focus on enhancing its position in the insulated shipper market.

- January 2025: United Parcel Service of America, Inc. enhanced its European operations by acquiring healthcare cold-chain logistics providers Frigo-Trans and BPL. The combined operations were designed to address the pharmaceutical industry's growing need for integrated cold and frozen supply chains, aligning with the rising demand in the insulated shipper market.

Global Insulated Shipper Market Report Scope

Insulated shippers are specialized containers used to maintain the stability of temperature-sensitive goods, including pharmaceuticals, food, and chemicals, during transit. These containers typically utilize EPS or polyurethane foam, reflective liners, and cooling agents such as gel packs or dry ice. They are designed to preserve product integrity for 24 to over 72 hours.

The Insulated Shipper Market is segmented into product type, material, application, and geography. By product type, the market is segmented into single-use insulated shippers, reusable insulated shippers, and active temperature-controlled containers. By material, the market is segmented into expanded polystyrene (EPS), polyurethane (PUR), vacuum-insulated panels (VIP), phase-change-material (PCM) composites, bio-based fiber and wool, and other materials. By application, the market is segmented into pharmaceutical and biotechnology, cell/gene therapy and clinical trials, food and beverage, chemicals and specialty chemicals, electronics and semiconductors, and other applications. The report also covers the market size and forecasts for the insulated shipper in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Single-use Insulated Shippers |

| Reusable Insulated Shippers |

| Active Temperature-Controlled Containers |

| Expanded Polystyrene (EPS) |

| Polyurethane (PUR) |

| Vacuum-Insulated Panels (VIP) |

| Phase-Change-Material (PCM) Composites |

| Bio-based Fiber and Wool |

| Other Materials |

| Pharmaceutical and Biotechnology |

| Cell/Gene Therapy and Clinical Trials |

| Food and Beverage |

| Chemicals and Specialty Chemicals |

| Electronics and Semiconductors |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Single-use Insulated Shippers | |

| Reusable Insulated Shippers | ||

| Active Temperature-Controlled Containers | ||

| By Material | Expanded Polystyrene (EPS) | |

| Polyurethane (PUR) | ||

| Vacuum-Insulated Panels (VIP) | ||

| Phase-Change-Material (PCM) Composites | ||

| Bio-based Fiber and Wool | ||

| Other Materials | ||

| By Application | Pharmaceutical and Biotechnology | |

| Cell/Gene Therapy and Clinical Trials | ||

| Food and Beverage | ||

| Chemicals and Specialty Chemicals | ||

| Electronics and Semiconductors | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the insulated shipper market?

The insulated shipper market stands at USD 10.44 billion in 2026 and is expected to reach USD 14.59 billion by 2031.

Which product type leads revenue in 2025?

Single-use insulated shippers hold 47.44% of 2025 revenue.

Why are VIP-based shippers gaining traction in pharmaceuticals?

VIPs offer 10× better thermal performance than EPS, enabling hold times beyond 120 hours for biologics that cannot tolerate even brief excursions.

What region is projected to grow fastest through 2031?

Asia-Pacific is projected to post a 7.27% CAGR through 2031, fueled by Indian and ASEAN cold-storage buildouts and expanding biologics manufacturing.

Page last updated on: