Non Grain Electric Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.29 Billion |

| Market Size (2031) | USD 25.08 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

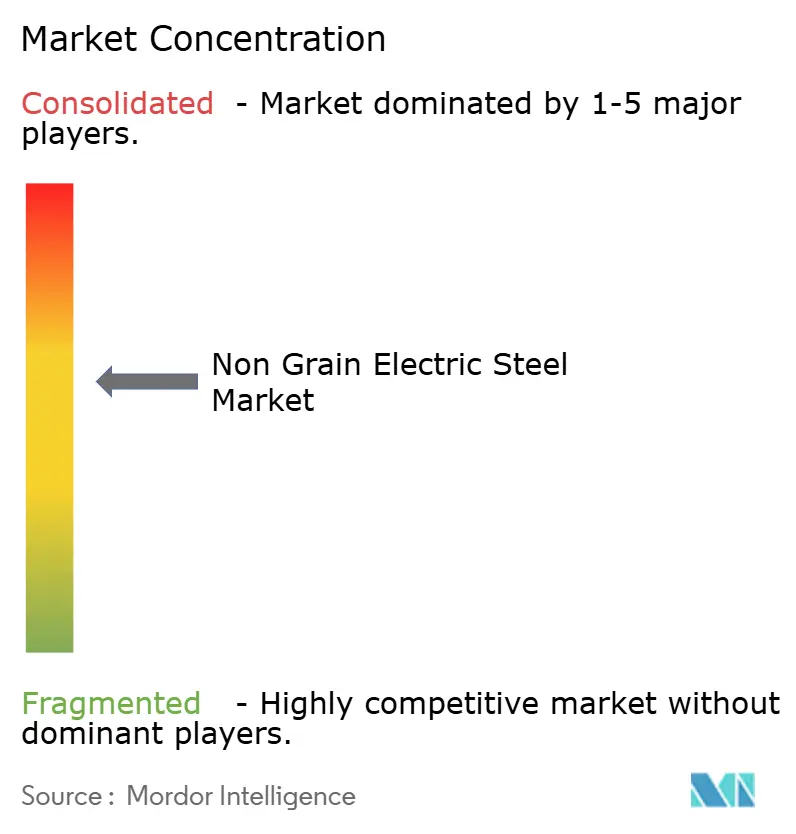

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non Grain Electric Steel Market Analysis by Mordor Intelligence

The Non Grain Electric Steel Market size is projected to expand from USD 19.45 billion in 2025 and USD 20.29 billion in 2026 to USD 25.08 billion by 2031, registering a CAGR of 4.33% between 2026 to 2031. This growth reflects a structural shift in rotating machinery that must deliver higher efficiency, lighter weight, and lower lifecycle carbon intensity. Automakers, renewable-energy developers, and grid-equipment makers continue to prioritize thin-gauge, fully processed laminations that cut iron loss, shorten supply chains, and help meet aggressive decarbonization targets. Domestic-content rules in the United States and Europe steer transformer and motor-core procurement toward regional mills, while Asia-Pacific investments boost capacity for traction-motor grades with gauges down to 0.10 millimeter. Thin-gauge innovation compresses the performance gap between silicon steel and cobalt-iron alloys, allowing OEMs to satisfy 800-volt platform requirements without resorting to exotic materials. Meanwhile, substitution threats from amorphous and nano-crystalline ribbons remain confined to wound-core transformers because mechanical robustness and high flux density are non-negotiable in rotating machines.

Key Report Takeaways

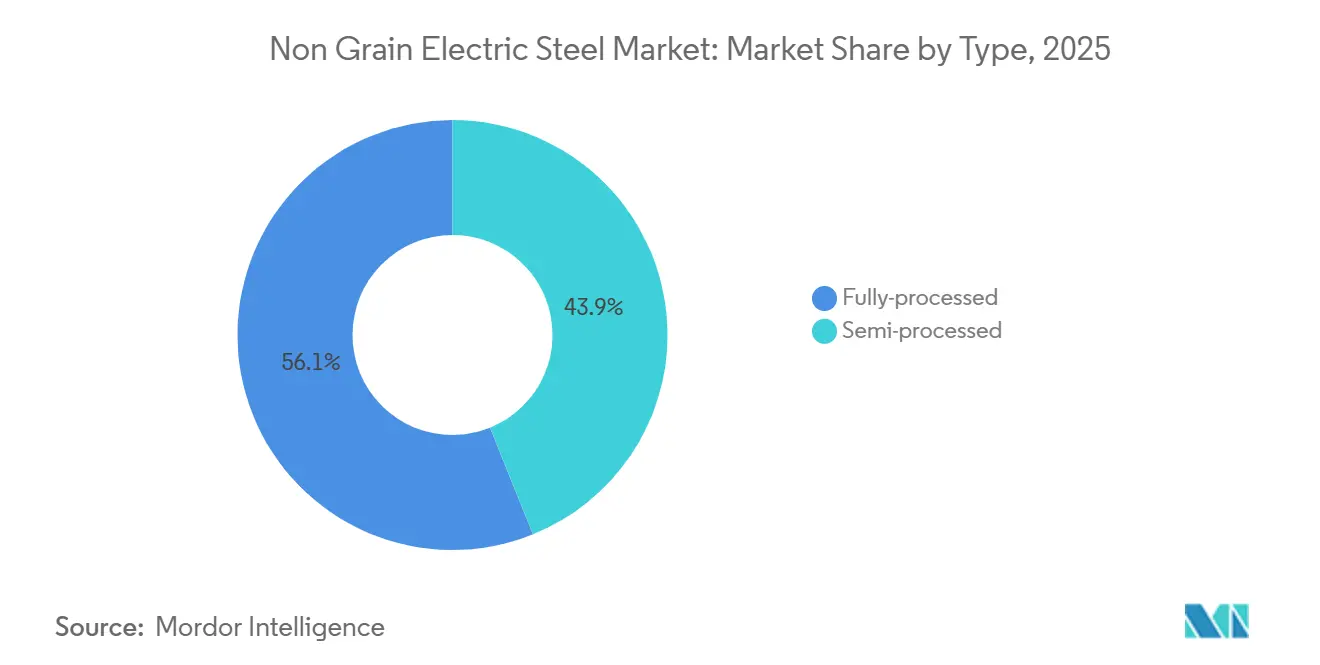

- By type, fully-processed grades led with 56.11% of the non grain electric steel market share in 2025 and are advancing at a 5.36% CAGR through 2031.

- By application, motors captured 46.78% of the non grain electric steel market size in 2025 and are projected to expand at a 4.91% CAGR through 2031.

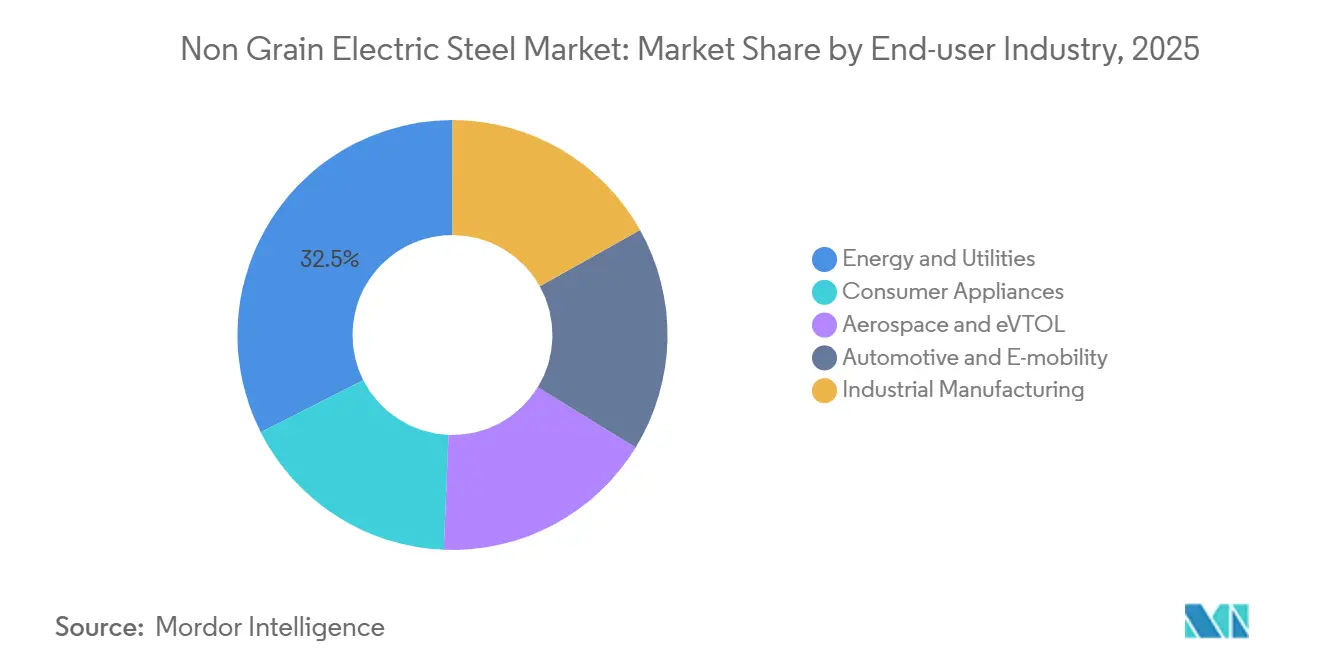

- By end-user industry, energy and utilities retained 32.46% of the non grain electric steel market size in 2025, while automotive and e-mobility will register the fastest 5.78% CAGR through 2031.

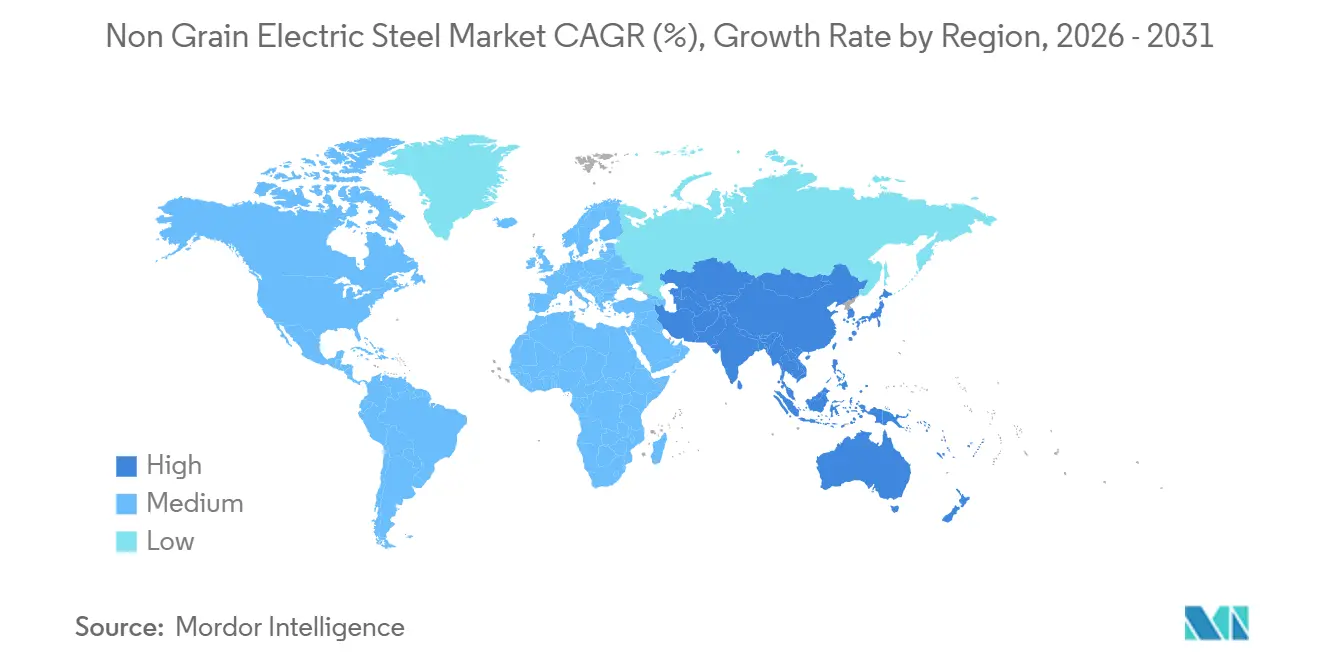

- By geography, Asia-Pacific commanded 47.11% of the non grain electric steel market size in 2025 and is forecast to deliver a 5.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non Grain Electric Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric Vehicle Production Expansion | + 1.8% | APAC core, spill-over to North America and EU | Medium term (2–4 years) |

| Renewable and Wind-Turbine Build-Out | + 1.2% | Global, with offshore concentration in EU and APAC | Long term (≥ 4 years) |

| Thin-Gauge NGOES for High-Speed Motors | + 0.9% | APAC manufacturing hubs, EU automotive clusters | Short term (≤ 2 years) |

| Domestic-Content Rules for Transformer Cores | + 0.7% | North America (IRA), EU (REPowerEU) | Medium term (2–4 years) |

| Digital-Twin-Driven Grade Upgrades | + 0.5% | Global, early adoption in APAC and EU integrated mills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle Production Expansion

Battery-electric and plug-in hybrid sales surpassed 2.146 million units at BYD in the first half of 2025, illustrating how rapidly traction-motor demand is compounding. India’s 2.08 million EV sales in 2024 and a 30% penetration goal by 2030 will require large numbers of charging stations, substations, and distribution transformers, all of which use NGOES cores. China’s April 2025 export controls on rare-earth minerals restrict neodymium supplies and push automakers toward electrically excited synchronous motors that replace permanent magnets with extra electrical-steel laminations. POSCO’s target of 7.5 million motor cores a year by 2030 showcases vertical integration as OEMs safeguard coil supply. High-speed 800-volt traction motors operate above 1,000 hertz, where core loss scales with frequency squared, making 0.20-0.27 millimeter gauges a necessity rather than an option.

Renewable and Wind-Turbine Build-Out

Global wind additions reached 114.3 gigawatts in 2024, driven by China’s 79.4 gigawatt build that alone accounted for 69.4% of the total[1]International Energy Agency, “Wind Market Report 2024,” iea.org . Offshore turbine ratings climbed toward 10 megawatts on average in 2024, with 16-26 megawatt platforms entering commercial tenders, each using multi-ton generator cores and transformer banks. Electrical-steel shortages lifted transformer prices 75% over 2018 levels as mill capacity lags renewable interconnection queues that now top 1,650 gigawatts worldwide. Electrically excited generators that sidestep rare-earth magnets boost NGOES content per turbine by up to 20%, cushioning the loss of share to amorphous cores in small transformers. Policy support in the EU and APAC continues to funnel capital toward offshore wind clusters that are, by necessity, hungry for premium NGOES grades.

Thin-Gauge NGOES for High-Speed Motors

Baosteel unveiled 0.10 millimeter B10AHV900M in May 2025 for EV traction motors, humanoid robots, and low-altitude electric aircraft operating above 15,000 rpm. IEEE research shows 0.08 millimeter laminations cut iron loss by 53% versus conventional 0.35 millimeter sheet at 10,000 rpm, translating into 2-3% whole-motor efficiency gains. thyssenkrupp started series production of powercore NGO 025-125Y420 at 0.25 millimeter and 12.5 W/kg core loss in January 2025, aimed at inverter-fed drives and on-board chargers. China Steel and Tata Steel likewise offer less than 0.25 millimeter portfolios for industrial servo drives, railway traction, and HVAC compressors. Rapid adoption of variable-frequency drives accelerates demand for these thin gauges across every major economy.

Domestic-Content Rules for Transformer Cores

The U.S. Department of Energy’s FAL 2025-08 Buy America waiver requires that melting, casting, rolling, annealing, and coating occur domestically for federally funded grid projects, closing a loophole that once allowed imported semi-processed coils to be merely slit onshore. A USD 6 billion round of Section 48C tax credits further incentivizes Cleveland-Cliffs and Nucor to add electrical-steel line. Europe’s REPowerEU plan imposes similar sourcing rules, benefiting integrated mills in Belgium, Germany, and Austria. These policies fragment global trade yet secure offtake for producers that can issue full domestic value-add certificates, elevating barriers for traders of semi-processed NGOES.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Amorphous and Nano-Crystalline Alloys | -0.6% | North America and APAC distribution-transformer retrofits | Medium term (2–4 years) |

| ESG-Driven Shift to "Green" Steel Alternatives | -0.4% | EU automotive and wind OEMs, expanding to North America | Long term (≥ 4 years) |

| Hydrogen-Embrittlement Risk in Next-Gen Drives | -0.2% | Global, concentrated in hydrogen-based steelmaking regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Amorphous and Nano-Crystalline Alloys

Hitachi Metals started commercial output of 2605HB1M amorphous ribbons at Conway, South Carolina in June 2026, delivering no-load transformer losses barely one-third of grain-oriented silicon steel. The HB1M-LL grade pushes loss down to 0.19 W/kg at 1.42 Tesla and 60 Hz, a 20-40% improvement on earlier amorphous products. Hitachi already controlled 57% of the amorphous-core segment worth USD 865 million in 2024 and aims for 6.9% CAGR through 2032. Although brittleness and low saturation flux limit ribbons to wound cores under 5 MVA, utilities chasing tighter DOE efficiency standards are shifting distribution-transformer specifications accordingly. For NGOES producers this erodes share in small-power units even as rotating-machine demand stays intact.

ESG-Driven Shift to “Green” Steel Alternatives

Nissan adopted Nippon Steel’s NSCarbolex Neutral in February 2025, targeting 30% lifecycle CO₂ cuts versus the 2018 baseline. thyssenkrupp supplies bluemint recycled steel with up to 64% lower CO₂ intensity to BMW’s iX3 platform, while Siemens Energy reserved bluemint powercore for 700 offshore-wind transformers. Procurement teams now embed carbon price signals in RFQs, letting low-carbon NGOES fetch 5-10% price premiums. Europe's upcoming Carbon Border Adjustment Mechanism and Japan’s GX League reinforce this preference, nudging mills worldwide to invest in hydrogen DRI or high-scrap EAF routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fully Processed Grades Capture Automaker Demand

Fully processed grades held 56.11% of non grain electric steel market share in 2025 and are projected to grow at 5.36% CAGR to 2031 as OEMs favor coils that arrive ready for punching without extra annealing. The non-grain electric steel market size for fully processed, reflecting automaker vertical-integration moves such as BYD’s in-house lamination stamping and POSCO Mobility Solution’s 7.5 million-core goal.

Automotive traction motors, IE4/IE5 industrial drives, and on-board chargers increasingly demand ultra-thin gauges down to 0.10 mm with certified core loss. Investments totaling JPY 213 billion brought Nippon Steel’s Hirohata and Setouchi lines online and will add Hanshin and Yawata by 2027, showing the capex race needed to stay relevant. Semi-processed grades remain common in large synchronous generators that undergo site-specific stress relief.

By Application: Traction and IE4/IE5 Motors Drive Volume

Motors controlled 46.78% of the non grain electric steel market size in 2025, and is slated to climb at a 4.91% CAGR through 2031. This expansion is split between 800-volt EV traction motors and industrial IE4/IE5 machines mandated under IEC 60034-30-1.

Transformer demand is throttled by 4-year lead times and 75% price escalation since 2018. Electrically excited wind-turbine generators bolster NGOES tonnage because each 16-26 MW machine uses several tons of laminations. Inductors, reactors, and sensors collectively remain a niche but strategically important as power-factor correction and harmonic filtering spread in renewables and data centers.

By End-user Industry: Automotive E-Mobility Accelerates Fastest

Energy and utilities commanded 32.46% of 2025 revenue as coal retirements offset grid reinforcement. In contrast, automotive and e-mobility will post the quickest 5.78% CAGR through 2031, aided by BYD’s 2.146 million NEVs in H1 2025 and India’s 30% target for 2030.

Industrial manufacturing is benefiting from HVAC and robotics shifts to variable-frequency drives. Consumer appliances and eVTOL deliver moderate growth as brushless DC motors and high-speed flight platforms require ultra-thin NGOES laminations.

Geography Analysis

Asia-Pacific dominated the non grain electric steel market with 47.11% revenue in 2025 and will log a 5.49% CAGR to 2031. China’s 79.4 GW of new wind in 2024 and India’s expanding EV ecosystem underpin the region’s appetite. Capacity additions at Hirohata, Setouchi, and POSCO’s Pohang mobility line ensure local supply for Toyota, Hyundai, and BYD programs.

In North America, Section 48C credits and Buy America clauses redirect demand to Cleveland-Cliffs, Nucor, and ArcelorMittal mills, while Hitachi Metals’ Conway ribbon plant positions the region as an amorphous-core hub.

Europe’s demand is by Ecodesign IE4 mandates and REPowerEU sourcing rules[2]European Commission, “REPowerEU Plan,” europa.eu . Thyssenkrupp’s Bluemint and Voestalpine’s Greentec steel reinforce the bloc’s push toward low-carbon metallurgy, while Gent and Ringwood supply Volkswagen and Stellantis traction programs.

South America, and Middle-East and Africa are hampered by scarce domestic rolling lines, currency swings, and import dependence. Nevertheless, Brazil’s industrial electrification and Saudi Arabia’s NEOM megaproject offer selective upside for exporters able to certify ESG credentials.

Competitive Landscape

Global capacity remains moderately concentrated: the top five players, including Nippon Steel, POSCO, Baosteel, ArcelorMittal, and JFE Steel, collectively held roughly 61% output in 2025. Nippon Steel’s JPY 213 billion capex spree expanded fully processed output for Toyota and Nissan programs, whereas POSCO Mobility Solution integrates stamping to secure Hyundai and Kia demand.

Baosteel, thyssenkrupp, and Tata Steel battle in the thin-gauge arena, racing to push losses below 12.5 W/kg at 400 Hz in gauges under 0.25 mm. Low-carbon claims emerge as a new moat: bluemint and NSCarbolex record double-digit price premiums and multi-year offtake with BMW and Siemens Energy.

Digital-twin deployments from ASE Steel and ProcTwin pilots give early adopters a cost edge by trimming scrap and stabilizing magnetic properties across green-steel feeds. Still, brittleness and limited flux density confine ribbons to wound-core transformers, suggesting coexistence rather than wholesale substitution in motors and generators.

Non Grain Electric Steel Industry Leaders

ArcelorMittal

JFE Steel Corporation

NIPPON STEEL CORPORATION

POSCO

Baoshan Iron & Steel Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: For the first time, Bokaro Steel Plant (BSL) of Steel Authority of India Limited (SAIL) developed a special grade steel, marking a significant stride in broadening its range of high-value products. The plant successfully produced approximately 1,100 tons of 0.5 mm thick IS 18316 LS Grade Non-Grain Oriented (NGO) Electrical Steel.

- May 2025: Baoshan Iron & Steel Co. Ltd. introduced a 0.10 mm thick non grain-oriented electrical steel (NGOES) grade, B10AHV900M, specifically developed for high-speed, high-efficiency motors used in electric vehicle (EV) traction systems and high-precision robotics. This ultra-thin material, thinner than a sheet of A4 paper, is designed to address the need for higher torque and efficiency in compact motor designs.

Global Non Grain Electric Steel Market Report Scope

Non-Grain Oriented (NGO) Electrical Steel is a soft magnetic material characterized by isotropic magnetic properties, providing uniform magnetic performance in all directions. It is mainly utilized in high-efficiency electric motors, generators, and compressors due to its low core losses and high permeability.

The Non Grain Electric Steel Market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into fully-processed and semi-processed. By application, the market is segmented into motors, traction (EV/rail), industrial (IE4/IE5, HVAC), transformers (power, distribution, and EV on-board), generators, inductors and reactors, and sensors and miscellaneous. By end-user industry, the market is segmented into energy and utilities, automotive and e-mobility, industrial manufacturing, consumer appliances, and aerospace and eVTOL. The report also covers the market size and forecasts for non grain electric steel in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Fully-processed |

| Semi-processed |

| Motors | Traction (EV/rail) |

| Industrial (IE4/IE5, HVAC) | |

| Transformers | Power |

| Distribution and EV on-board | |

| Generators | |

| Inductors and Reactors | |

| Sensors and Miscellaneous |

| Energy and Utilities |

| Automotive and E-mobility |

| Industrial Manufacturing |

| Consumer Appliances |

| Aerospace and eVTOL |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Fully-processed | |

| Semi-processed | ||

| By Application | Motors | Traction (EV/rail) |

| Industrial (IE4/IE5, HVAC) | ||

| Transformers | Power | |

| Distribution and EV on-board | ||

| Generators | ||

| Inductors and Reactors | ||

| Sensors and Miscellaneous | ||

| By End-user Industry | Energy and Utilities | |

| Automotive and E-mobility | ||

| Industrial Manufacturing | ||

| Consumer Appliances | ||

| Aerospace and eVTOL | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the non grain electric steel market?

The non grain electric steel market stands at USD 20.29 billion in 2026 and is projected to reach USD 25.08 billion by 2031.

Which segment leads demand in 2025?

Motors account for 46.78% of 2025 demand, led by EV traction and IE4/IE5 industrial drives.

Why are fully processed grades growing faster through 2031 than semi-processed grades?

They let automakers bypass annealing, trim lead times, and guarantee magnetic properties, driving a 5.36% CAGR through 2031.

How do domestic-content rules in the United States affect suppliers?

Buy America clauses shift transformer-core sourcing to Cleveland-Cliffs, Nucor, and ArcelorMittal mills that can certify full onshore value-add.

Page last updated on: