Grain Oriented Electrical Steel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

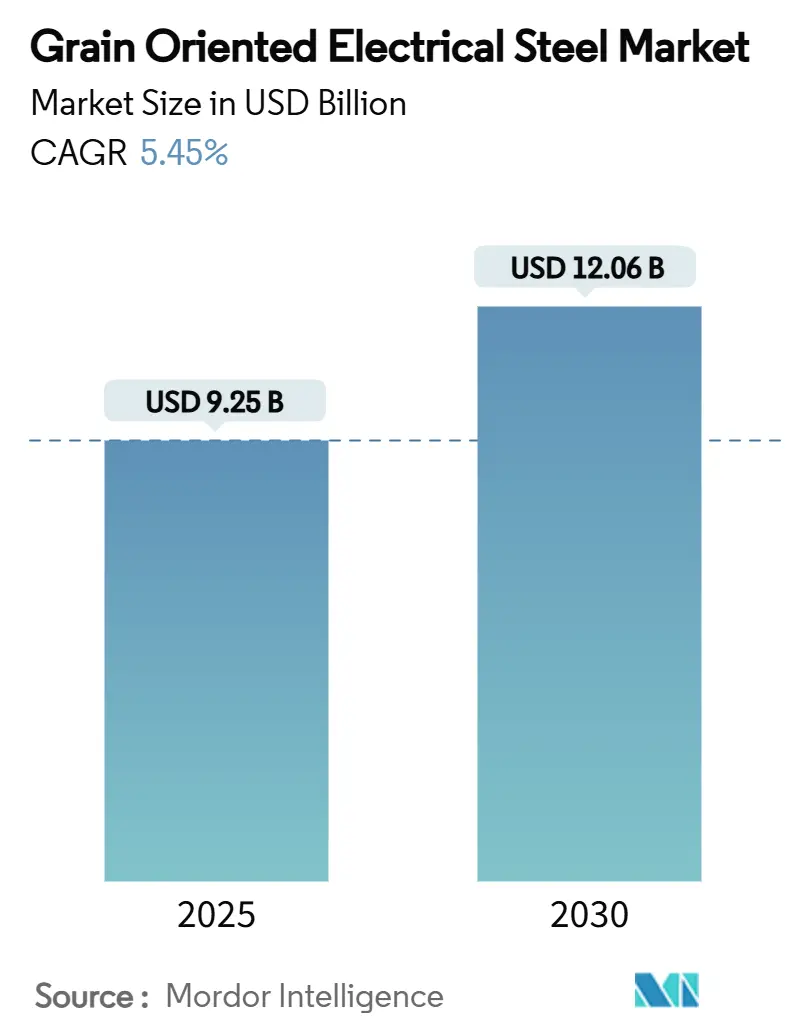

| Market Size (2025) | USD 9.25 Billion |

| Market Size (2030) | USD 12.06 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

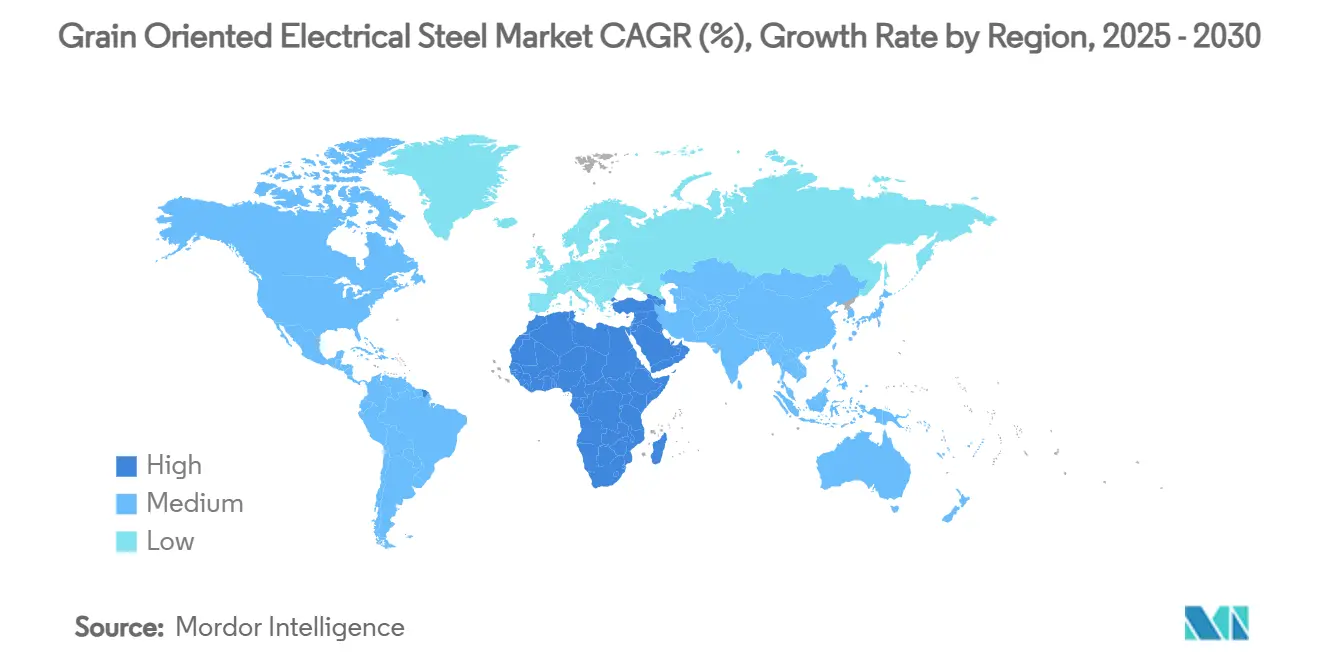

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

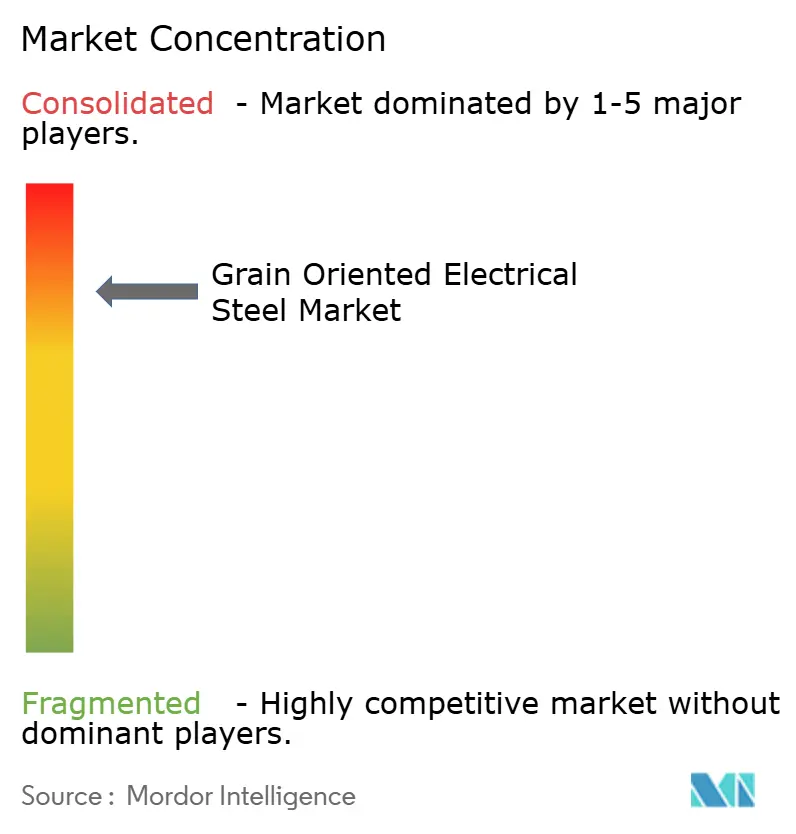

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain Oriented Electrical Steel Market Analysis by Mordor Intelligence

The Grain Oriented Electrical Steel Market size is estimated at USD 9.25 billion in 2025, and is expected to reach USD 12.06 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030). Near-term growth rests on transformer efficiency mandates in the United States and Europe, while aging grid assets in China and India stoke replacement demand. Long-term momentum originates from hyperscale data-center construction and solid-state electric-vehicle charger rollouts, both of which require ultra-low-loss magnetic cores. Supply–demand tightness persists because only a handful of integrated mills can produce premium grades at scale, creating pricing power for vertically integrated manufacturers. Producers with dependable selenium and aluminum feedstock now enjoy margin resilience, whereas standalone lamination suppliers face cost pass-through risk.

Key Report Takeaways

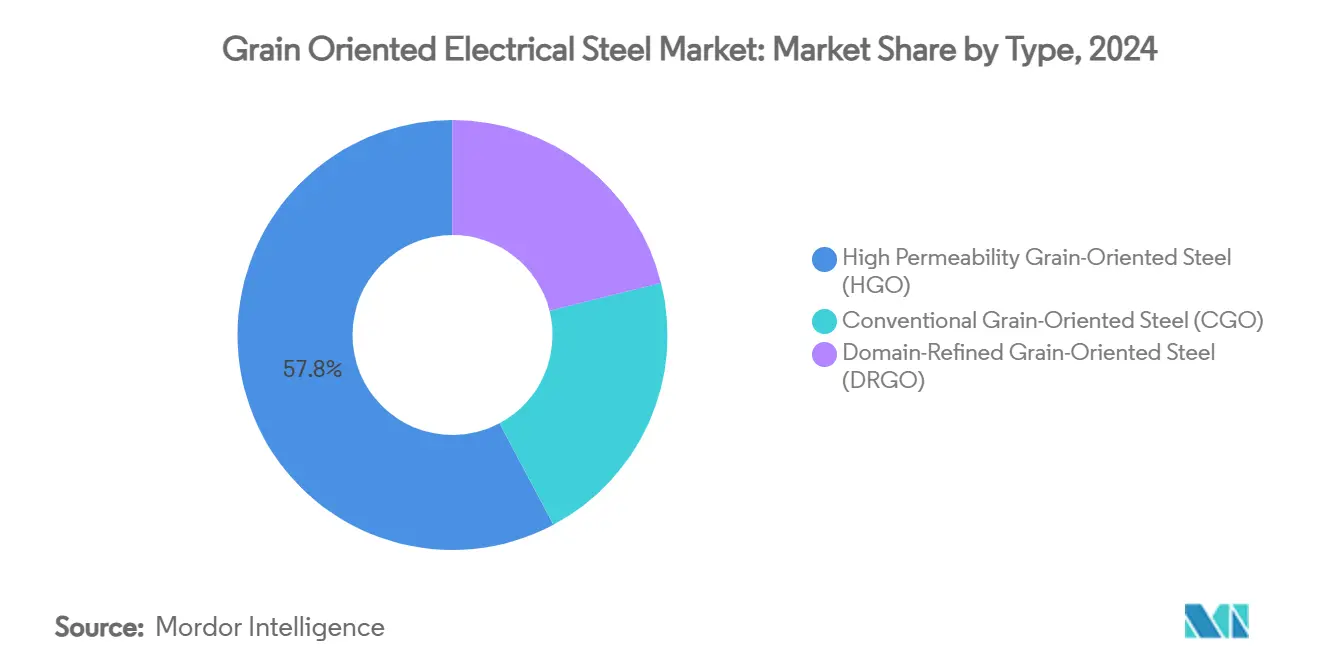

- By type, High Permeability Grain-Oriented Steel held 57.78% of the grain oriented electrical steel market share in 2024, while Domain-Refined Grain-Oriented Steel is projected to expand at a 6.10% CAGR through 2030.

- By application, power transformers commanded 54.23% of the grain oriented electrical steel market size in 2024; distribution transformers are advancing at a 5.83% CAGR to 2030.

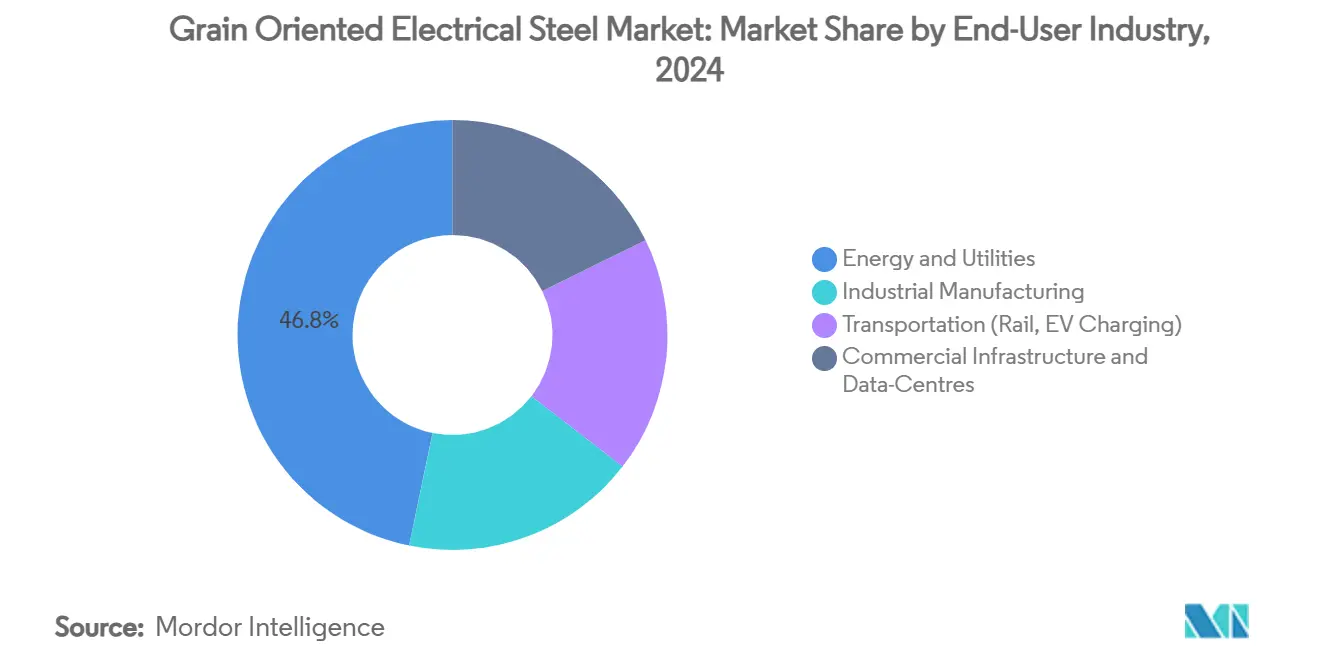

- By end-user industry, energy and utilities led with 46.78% revenue share in 2024, yet commercial infrastructure and data centers are forecast to rise at 6.43% CAGR through 2030.

- By geography, Asia-Pacific controlled 40.25% of 2024 volume, whereas the Middle East & Africa region is set to grow at 5.95% CAGR to 2030.

Global Grain Oriented Electrical Steel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for energy-efficient transformers | +1.0% | Global | Medium term (2–4 years) |

| Rising investments in global power infrastructure | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Increasing grid expansion and modernisation programmes | +1.2% | North America & EU | Medium term (2–4 years) |

| Surging transformer demand from hyperscale data centers | +0.7% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Development of high-frequency GOES for solid-state EV chargers | +0.8% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for energy-efficient transformers

Global minimum-energy-performance rules pivot toward reduction of transformer core loss, allowing 75% of U.S. distribution units to remain GOES-based under the Department of Energy’s 2029 standard while cutting no-load losses by 10–30%[1]U.S. Department of Energy, “Distribution Transformer Efficiency Standards,” energy.gov. The European Union’s Ecodesign regime has already pushed average transformer losses down to 23 MWh per unit, a 17% drop from 2020 levels[2]European Commission, “Ecodesign Requirements for Power Transformers,” europa.eu . These policies elevate lifecycle-cost thinking, enabling utilities to justify premium grades even when initial prices exceed those of conventional laminations. Producers have responded with laser-scribing and stress-annealing techniques that trim core loss without impairing tensile strength. Because the compliance horizon extends four years, mills have a window to debottleneck annealing lines and train operators, safeguarding domestic jobs in Pennsylvania and Ohio.

Rising investments in global power infrastructure

Electric-grid outlays hit USD 331 billion in 2023, with Europe supplying one-fifth as wind and solar additions compel large-scale transformer replacements. Utilisation lags demand by roughly 2% for power transformers, granting GOES mills stronger price discipline. China’s Special Action Plan shifts blast-furnace capacity toward lower-carbon electric-arc units, trimming 53 million t of CO₂ by 2030 and indirectly supporting specialty grades. MENA sovereign funds now channel petrodollar surpluses into 400-kV transmission corridors, lifting regional demand by 7.3% annually. Parallel spending lifts integrated producers that can supply both cores and finished transformer tanks.

Increasing grid expansion and modernisation programmes

U.S. transformer shortages lengthened lead times to 70 weeks in 2024 and sent prices up 60–70% from early 2020, prompting industry to lobby Congress for USD 1.2 billion in relief funding. Only one-fifth of domestic demand is met at home, providing headroom for new capacity announcements in Alabama and Ohio. European operators adopt ester-filled, digitally monitored units that need lower core losses, a specification met by high-permeability GOES. Renewable intermittency elevates harmonic distortion, nudging buyers toward domain-refined grades. Smart-grid rollouts value thermal stability and noise reduction, criteria where premium GOES shows demonstrable advantage.

Surging transformer demand from hyperscale data centers

Annual U.S. data-center capex topped USD 27 billion in 2024, up 69% year over year, and now absorbs 4% of national electricity use; this share could climb to 9.1% by 2030. To avert downtime losses that can reach millions per hour, operators insist on ultra-reliable, low-loss cores. High-density AI racks require step-down transformers able to dissipate heat effectively at 20–100 MW site loads, and premium grain oriented electrical steel market grades deliver the needed magnetic stability. Because campus construction clusters in Northern Virginia, Oregon, and Singapore, localized demand spikes expose regional supply deficits, reinforcing forward-contracting with integrated mills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus non-oriented electrical steel | –0.9% | Global | Medium term (2–4 years) |

| Availability of substitutes such as amorphous steel | –0.6% | North America & EU | Long term (≥ 4 years) |

| Volatile prices of specialty alloying elements | –0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production cost versus non-oriented electrical steel

Precision cold-rolling, repeated anneals, and tension coatings lift GOES production expenses 40–60% above non-oriented equivalents. Capital-intensive bell-anneal furnaces raise barriers to entry, and tight process windows heighten scrap risk. In economies where power tariffs remain subsidized, utilities often select cheaper non-oriented cores. Nevertheless, as policymakers align procurement with total-cost-of-ownership metrics, the pendulum swings back toward GOES. Vertical integration helps mills absorb energy shocks, but independent processors may struggle to pass costs through during stainless and selenium volatility spikes.

Availability of substitutes such as amorphous steel

Amorphous ribbons deliver 60–70% lower no-load losses, attracting EU regulators debating Tier-3 standards that could privilege the technology. Yet brittleness and limited stacking height make amorphous cores challenging for large-MVA units. Production is concentrated among a few ribbon casters, constraining supply. GOES producers counter by adopting laser domain-refinement to narrow the loss gap. Competitiveness will hinge on whether amorphous vendors can scale thin-gauge, wide-width stock without sacrificing mechanical integrity, a hurdle not expected to be fully cleared before 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: HGO Dominance Faces DRGO Innovation

High Permeability GOES held 57.78% share of the grain oriented electrical steel market in 2024, underpinned by mature process know-how and cost-effective scale economics. Producers ship large slit coils to transformer OEMs that value predictable magnetostriction and stacking factors. The grain oriented electrical steel market size for this segment is projected to increase in lockstep with grid-renewal programs, but incremental growth slows as utilities seek even lower loss levels. In response, mills deploy laser scribing to create domain-refined variants which capture premium margins. Domain-Refined GOES, expanding at 6.10% CAGR, appeals to data-center and offshore wind converters where each watt saved translates directly into OPEX relief. However, capacity remains constrained because stress-annealing chambers require upgraded atmosphere controls and longer dwell times.

Innovations such as Thyssenkrupp’s bluemint powercore tout up to 50% CO₂ reductions, aligning material choice with Scope-3 targets. The grain oriented electrical steel industry also banks on high-frequency grades that maintain ≤0.9 W/kg loss at 400 Hz, a prerequisite for solid-state chargers. Conventional GOES retains a foothold in budget-sensitive emerging markets where CAPEX trumps lifecycle economics. Over the forecast horizon, blended-grade strategies let OEMs mix HGO and DRGO to balance performance and cost inside the same core stack, optimizing total transformer efficiency.

By Application: Power Transformers Lead Distribution Growth

Power transformers consumed 54.23% o f total volume in 2024 because network operators replaced aging 220–765 kV units to accommodate renewable in-feed. With every 1 MVA of rating demanding roughly 1.4 t of laminations, the grain oriented electrical steel market continues to track high-voltage buildouts. The grain oriented electrical steel market size allocated to power transformers should expand steadily as interregional DC lines proliferate. Distribution transformers, advancing at 5.83% CAGR, receive regulatory tailwinds such as the DOE’s 2029 rule which guides 75% of new poles-top units toward GOES cores. Rising rooftop solar and vehicle-to-grid systems intensify low-voltage back-feed, another factor that elevates domain-refined grades.

Reactors and instrument transformers show modest but stable demand tied to power-quality installations. Data-center step-down units form a fast-emerging niche; hyperscale builders insist on ≤0.85 W/kg core loss to curb cooling loads. As AI clusters multiply, their aggregate load profiles resemble small utility districts, reinforcing the grain oriented electrical steel market narrative that computing projects will rival traditional grid capex. For all applications, higher frequency and harmonic content oblige OEMs to source tighter tolerance, lower-thickness laminations, nudging mills to widen 0.18 mm product lines.

By End-user Industry: Data Centers Disrupt Utility Dominance

Utilities still represented 46.78% of consumption in 2024 because they purchase bulk high-MVA transformers, yet their share is set to decline marginally as commercial infrastructure accelerates. AI-enabled data centers are clocking 6.43% CAGR thanks to an explosion of 20–100 MW campuses that each require dozens of low-loss step-down units. The grain oriented electrical steel market thus pivots from a single-buyer utility model toward multipolar demand. Industrial manufacturing remains a reliable base as process electrification spreads through chemicals and steel mini-mills adopting electric-arc furnaces. Transportation, encompassing rail traction and 800 V EV chargers, will likely outpace general GDP growth, fostering specialty high-frequency GOES adoption.

Data-center developers increasingly bundle long-term service agreements that penalize energy wastage, motivating transformer OEMs to specify DRGO cores. Utilities, by contrast, balance CAPEX and tariff constraints, leading many to favour hybrid core designs that blend HGO and amorphous ribbons. Consequently, sales teams must segment customer value propositions more finely than before, signalling a structural diversification of the grain oriented electrical steel market customer base.

Geography Analysis

Asia-Pacific captured 40.25% of 2024 shipments, buoyed by China’s 1.16 million t production capacity and India’s USD 660 million JSW–JFE joint venture slated for 2027 output. Regional demand expands as South Korea’s POSCO revamps its Gwangyang line to lift premium grades by 30%. Japan’s Nippon Steel is raising Hirohata capacity 40% to serve offshore wind converters. Southeast Asian grids add 52 GW of renewable capacity between 2025 and 2030, requiring higher-grade core steel for variable-load balancing. Collectively, these factors fortify APAC’s role as both production hub and consumption epicenter for the grain oriented electrical steel market.

North America benefits from the Infrastructure Investment and Jobs Act, yet transformer shortages extend lead times to 70 weeks. Cleveland-Cliffs injects USD 150 million into its Weirton GOES line while ArcelorMittal erects a USD 1.2 billion Alabama mill slated for 2027 commissioning. Canadian utilities align with U.S. efficiency rules, ensuring a unified North American specification set that favours premium grades. Mexico’s near-shoring boom spurs industrial load, adding incremental core demand. The grain oriented electrical steel market share in the region could rise 1–2 percentage points if announced capacities materialize on schedule.

The Middle East & Africa emerges as the fastest-growing territory at 5.95% CAGR, propelled by USD 250 billion of grid expansion plans across Saudi Arabia, the UAE, and Egypt. Abundant solar irradiance couples with green-hydrogen ambitions, necessitating HVDC lines that soak up premium laminations. Africa’s electrification goals, targeting 80% access by 2030, open a pipeline of distribution-level projects where weight and loss constraints guide buyers toward HGO. Government incentives for local electrical-steel coating lines are under study in Saudi Arabia, aiming to capture value-added downstream.

Europe’s decarbonisation strategy tightens transformer loss budgets under Ecodesign, already slicing 17% off average EU no-load figures. Germany, France, and the UK account for 40% of continental volume. Voestalpine secured EUR 300 million EIB financing to trial hydrogen-based strip annealing, a potential blueprint for greener laminations. While macro growth is moderate, specification upgrades drive higher average selling prices, cushioning mills against demand plateaus. South America posts stable expansion led by Brazil’s grid rebuilds, though currency volatility tempers import appetite.

Competitive Landscape

The grain oriented electrical steel market is highly consolidated. Baowu Group, Nippon Steel, POSCO, Cleveland-Cliffs, and Thyssenkrupp leverage proprietary secondary-recrystallisation know-how and large melt shops. Barriers to entry include USD 500–700 million capital outlay for bell-anneal lines and the scarcity of process engineers. Nippon Steel’s purchase of U.S. Steel in late 2024 broadened its U.S. footprint and secured low-carbon slab feedstock, signalling an era of trans-Pacific consolidation.

Technology differentiation now centres on laser domain-refinement, CO₂-curbed metallurgy, and high-frequency product variants. Thyssenkrupp’s bluemint powercore, Baowu’s Baosteel-Z oriented line, and POSCO’s Hyper NO electrical steel all target specific loss ranges. Data-center OEMs are forming trilateral alliances with mills and transformer winders to lock in multi-year coil supply at fixed loss grades. This vertical linking simultaneously assures feedstock and transfers R&D risk upstream. Smaller regional lamination houses pivot toward niche thicknesses or tap foreign toll-coating partnerships to stay afloat.

Raw-material volatility, especially selenium prices, injects balance-sheet risk for non-integrated processors. Mills owning captive roasting capacity or offtake contracts from copper refineries hold an edge. ESG pressures accelerate the retirement of high-emission blast furnaces, and producers advertising ≥30% Scope-1 emission cuts already win procurement preference among European utilities. Overcapacity in mid-tier Chinese mills could push spot prices lower, but premium DRGO coils remain supply-constrained, underpinning a bifurcated pricing structure that benefits innovation leaders.

Grain Oriented Electrical Steel Industry Leaders

Baosteel Co.,Ltd.

JFE Steel Corporation

POSCO

NIPPON STEEL CORPORATION

Thyssenkrupp AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ArcelorMittal announced its plans to establish an advanced manufacturing facility for non-grain-oriented electrical steel (NOES) in Alabama. This facility, entirely owned by ArcelorMittal, aims to produce up to 150,000 metric tons of NOES annually. The production will cater to a diverse range of applications, including automotive, renewable energy, electric motors, generators, and other specialized industrial and commercial uses.

- June 2024: JFE Steel Corporation revealed that its environmentally-friendly JGreeX green steel, a grain-oriented electrical steel, has been chosen by a leading U.S. manufacturer of IT data center transformers. Marking its debut in the U.S. market, the order is set to be delivered to Eaton Corporation, a prominent U.S. transformer maker, via Toyota Tsusho Corporation.

Global Grain Oriented Electrical Steel Market Report Scope

| Conventional Grain-Oriented Steel (CGO) |

| High Permeability Grain-Oriented Steel (HGO) |

| Domain-Refined Grain-Oriented Steel (DRGO) |

| Power Transformers |

| Distribution Transformers |

| Reactors and Instrument Transformers |

| Energy and Utilities |

| Industrial Manufacturing |

| Transportation (Rail, EV Charging) |

| Commercial Infrastructure and Data-Centres |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Conventional Grain-Oriented Steel (CGO) | |

| High Permeability Grain-Oriented Steel (HGO) | ||

| Domain-Refined Grain-Oriented Steel (DRGO) | ||

| By Application | Power Transformers | |

| Distribution Transformers | ||

| Reactors and Instrument Transformers | ||

| By End-user Industry | Energy and Utilities | |

| Industrial Manufacturing | ||

| Transportation (Rail, EV Charging) | ||

| Commercial Infrastructure and Data-Centres | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the grain oriented electrical steel market?

It is valued at USD 9.25 billion in 2025 and is forecast to reach USD 12.06 billion by 2030.

Which product type dominates sales?

High Permeability GOES leads with 57.78% share, though Domain-Refined grades are growing fastest.

Why are data centers important to demand?

Hyperscale facilities need ultra-low-loss transformers to cut energy costs, driving a 6.43% CAGR in commercial and data-center demand.

Which region grows quickest through 2030?

The Middle East & Africa region is projected to expand at 5.95% CAGR due to grid and renewable investments.

Page last updated on: