Cold Cuts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

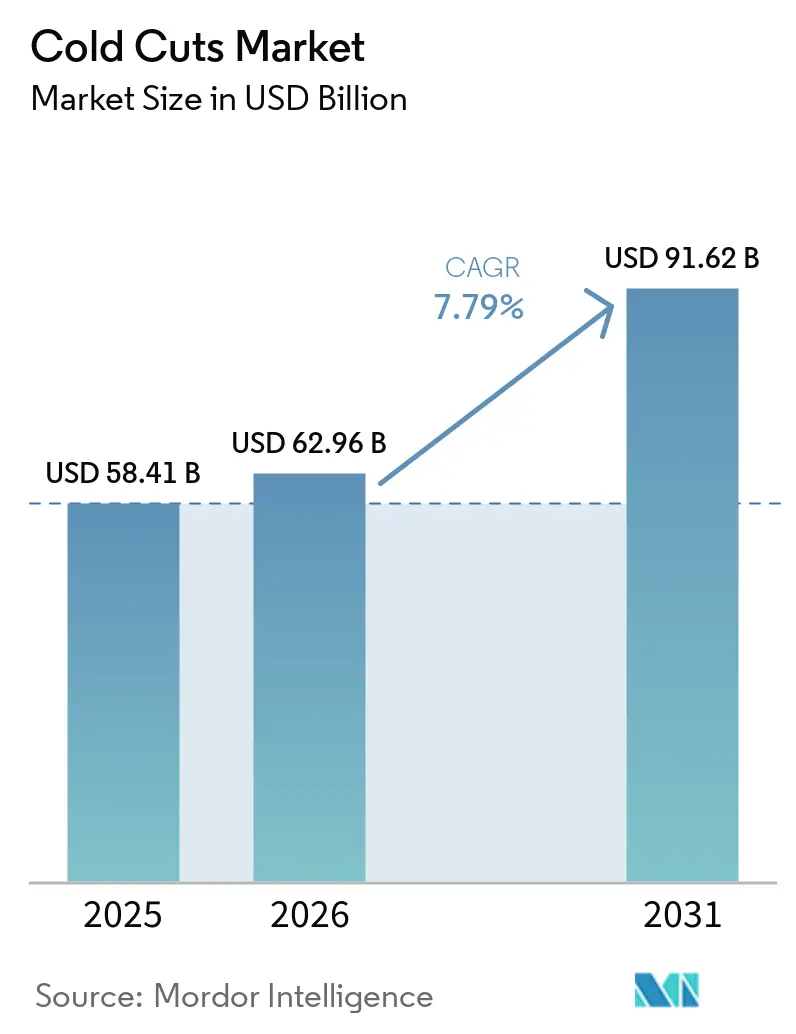

| Market Size (2026) | USD 62.96 Billion |

| Market Size (2031) | USD 91.62 Billion |

| Growth Rate (2026 - 2031) | 7.79% CAGR |

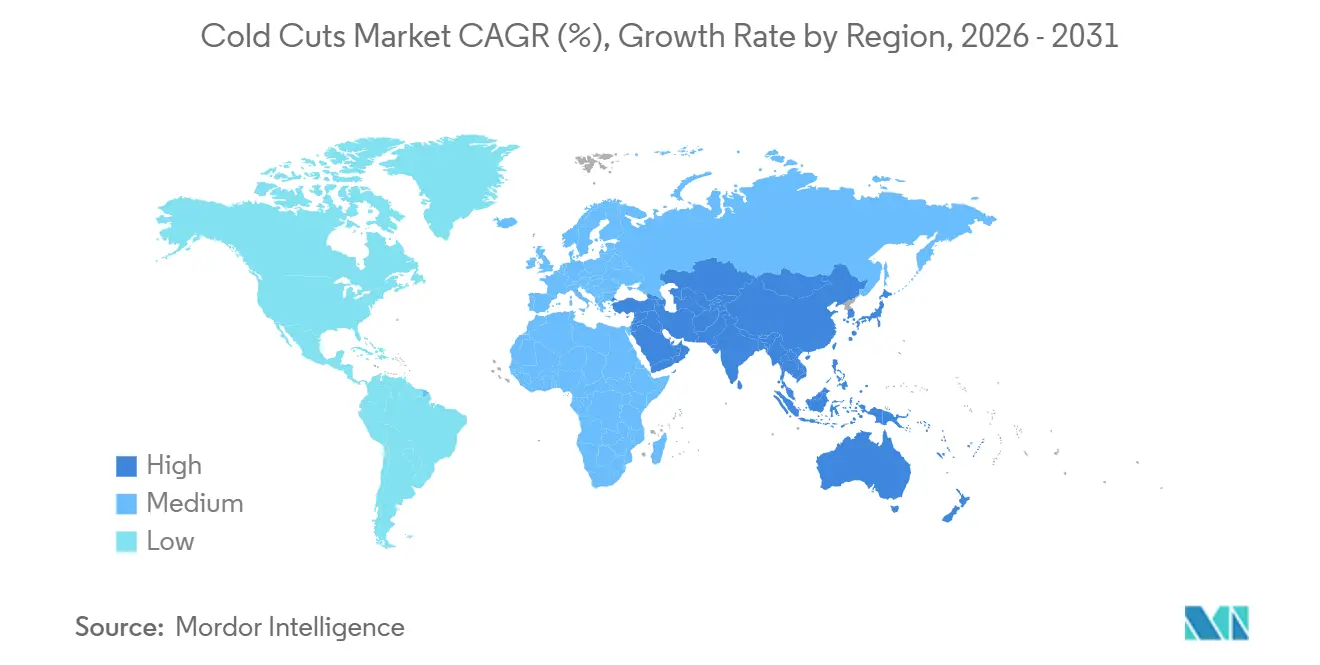

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cold Cuts Market Analysis by Mordor Intelligence

The cold cuts market size in 2026 is estimated at USD 62.96 billion, up from 2025's USD 58.41 billion, with 2031 projections showing USD 91.62 billion, growing at a 7.79% CAGR over 2026-2031. Rising consumer demand for convenient, protein-rich foods is driving market growth, while stricter nitrite limits, recyclable-packaging mandates, and inflationary input costs are pushing processors to prioritize clean-label reformulation and packaging innovation. Poultry continues to dominate as the primary revenue contributor, with turkey emerging as the fastest-growing segment due to its lean profile, which aligns with high-protein dietary preferences among younger consumers. Modified-atmosphere packaging (MAP) currently holds the largest market share; however, vacuum skin and mono-material films are rapidly gaining traction, driven by extended producer responsibility (EPR) regulations in Europe and several U.S. states. Regionally, North America is a mature, margin-sensitive market, while Asia-Pacific is witnessing significant growth as urban households increasingly shift from traditional wet-market meat to branded chilled deli formats.

Key Report Takeaways

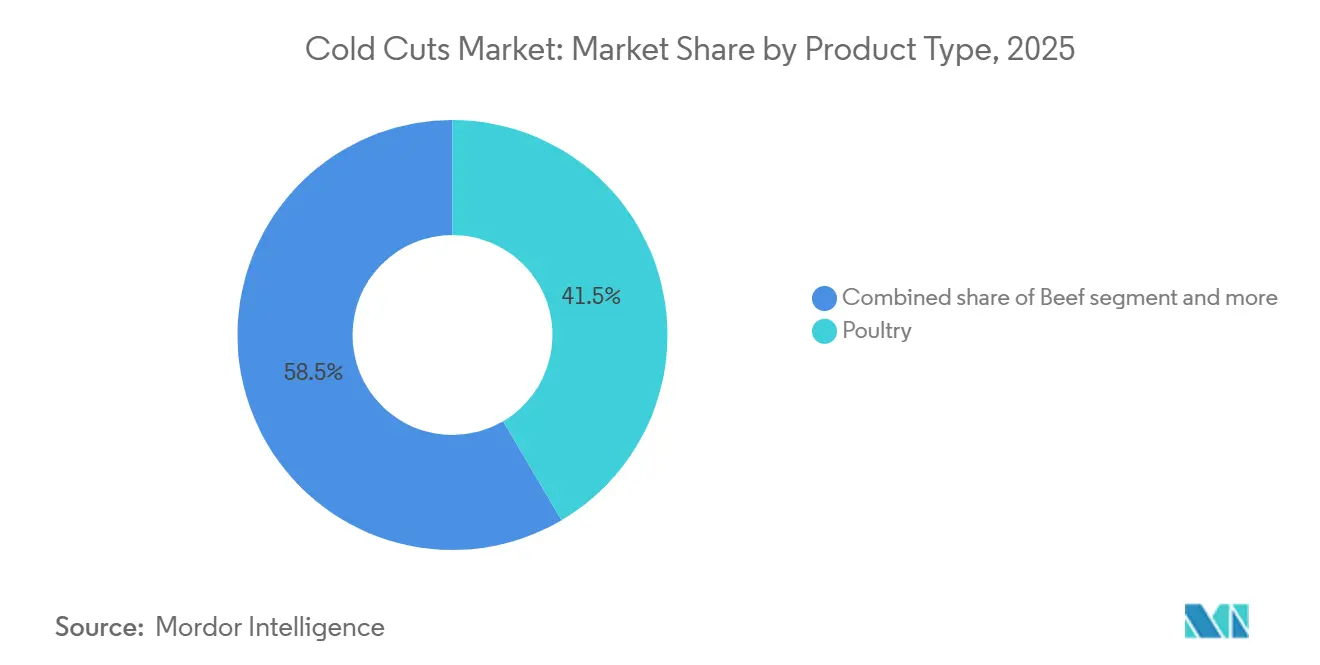

- By product type, poultry led with 41.54% of cold cuts market share in 2025, while beef is projected to advance at a 9.12% CAGR through 2031.

- By form, sliced cold cuts accounted for 43.82% of revenue in 2025; whole cuts are set to expand at a 9.46% CAGR over 2026-2031.

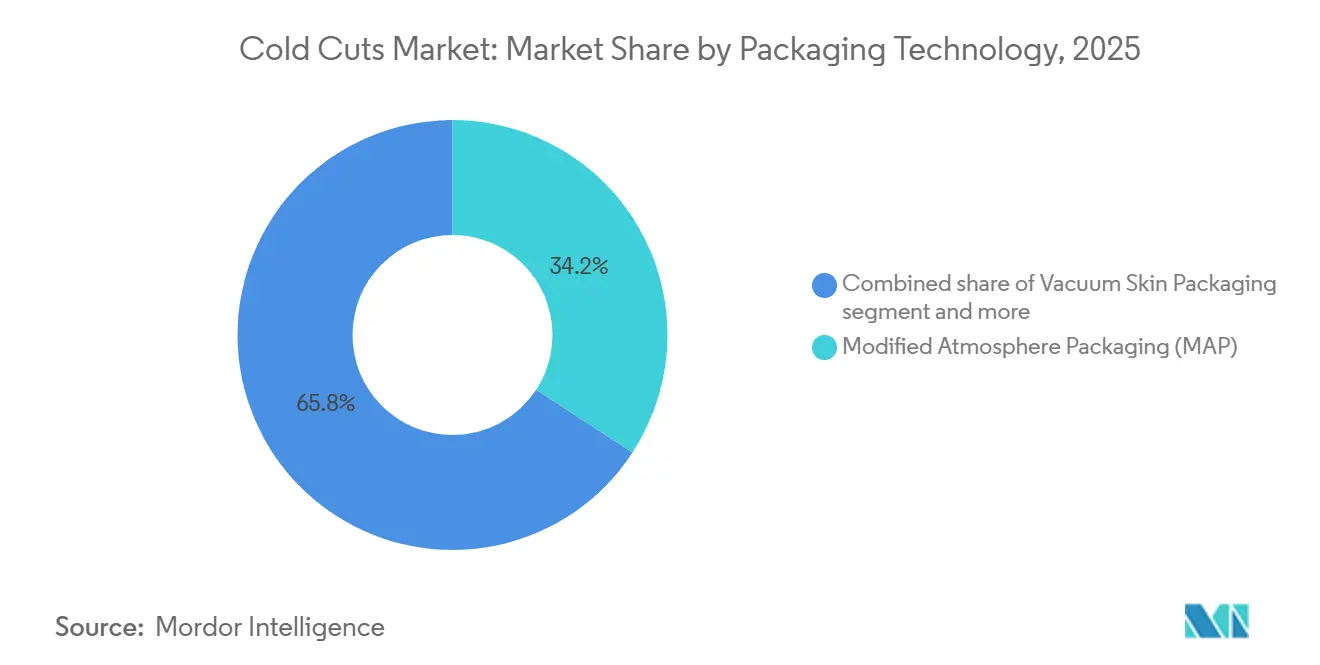

- By packaging technology, MAP captured 34.13% share in 2025, whereas recyclable and mono-material formats are forecast to grow at 10.85% CAGR through 2031.

- By distribution channel, retail commanded 59.16% of revenue in 2025; foodservice and HoReCa are poised for an 8.59% CAGR through 2031.

- By geography, North America accounted for 34.11% of global revenue in 2025, yet Asia-Pacific is expected to register a 11.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cold Cuts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient ready-to-eat protein foods | +1.8% | Global, with strongest uptake in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Clean-label and health-oriented reformulations | +1.5% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Advancements in packaging technologies | +1.2% | Global, led by Europe, North America, emerging in Latin America | Medium term (2-4 years) |

| Product innovation and flavor diversification | +1.0% | North America, Europe, Asia-Pacific premium segments | Short term (≤ 2 years) |

| Expansion of foodservice and catering industries | +0.9% | Global, with acceleration in North America, Europe, Middle East | Medium term (2-4 years) |

| Growing popularity of high-protein diets | +1.4% | North America, Western Europe, urban centers in China and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient ready-to-eat protein foods

The rising global interest in high-protein diets is significantly reshaping the cold cuts market, driving innovation, premiumization, and policy convergence around cleaner, more nutritious meat offerings. This trajectory is closely tied to consumer trends, particularly in urban centers, favoring convenient, ready-to-eat protein sources. This demand is bifurcating the market: value-conscious buyers gravitate toward private-label sliced turkey and chicken, while premium segments favor artisanal charcuterie and nitrite-free options. According to Cargill's 2024 consumer survey, 61% of Americans increased their protein intake, with convenience cited as the primary purchase driver. The ready-to-eat segment also benefits from declining household cooking frequency. Retailers are responding by expanding refrigerated deli sections and introducing meal kits that bundle cold cuts with complementary sides, effectively converting occasional buyers into habitual purchasers.

Clean-label and health-oriented reformulations

Consumers are increasingly demanding transparency and healthier ingredient profiles. Processors are responding by eliminating artificial preservatives, reducing sodium content, and incorporating natural antimicrobials such as rosemary extract and green tea polyphenols. These reformulations not only align with evolving regulatory standards but also cater to health-conscious consumers who are willing to pay a premium for products perceived as safer and more natural. Regulatory tightening and consumer skepticism toward synthetic additives are forcing processors to reformulate legacy recipes, a transition that carries both compliance risk and margin opportunity. The European Commission's Regulation (EU) 2023/2108, effective October 2025, reduced permissible nitrite levels to 80 mg/kg for most cold cuts and 55 mg/kg for sterilized products, with residual limits capped at 25-50 mg/kg [1]Source: European Commission, “Commission Regulation (EU) 2023/2108,” ec.europa.eu. In the United States, the USDA Food Safety and Inspection Service clarified in 2024 that "uncured" claims require disclosure of nitrite or nitrate sources, even when derived from celery powder or sea salt. These regulatory changes are pushing manufacturers to adopt clean-label practices.

Advancements in packaging technologies

Shelf-life extension and sustainability mandates are converging to drive adoption of modified atmosphere packaging, vacuum skin packaging, and recyclable mono-material films. ULMA Packaging introduced its Fast Skin system in 2025, combining vacuum skin technology with paperboard trays that reduce plastic content by 60% while extending refrigerated shelf life to 21 days. Vacuum skin packaging, which molds a transparent film directly onto the product surface, is gaining traction in premium segments because it eliminates air pockets, reduces drip loss, and enhances visual appeal on retail shelves. Advancements in modified atmosphere packaging (MAP) are enabling processors to maintain product freshness and quality for longer durations. Companies are also exploring bio-based, compostable films to meet growing consumer demand for environmentally friendly packaging solutions. Smart packaging technologies, including temperature-sensitive labels and freshness indicators, are emerging as value-added features, providing consumers with real-time information about product quality and safety.

Expansion of foodservice and catering industries

Institutional foodservice and hospitality channels are recovering from pandemic-era disruptions, with operators prioritizing labor-saving ingredients that deliver consistent portion control and food-safety compliance. North American catering operators are expanding cold-cut offerings in boxed lunches, sandwich bars, and charcuterie platters, driven by corporate return-to-office mandates and event resumption. Sysco Corporation, the largest foodservice distributor in the United States, reported a 7% increase in deli-meat case volume during fiscal 2025, with pre-sliced, portion-controlled formats accounting for 68% of unit sales. Additionally, the growing trend of convenience-focused dining has driven increased demand for ready-to-serve cold cuts in institutional settings, including schools, hospitals, and corporate cafeterias. Foodservice growth is also evident in quick-service restaurants (QSRs), where limited-time sandwich promotions featuring premium cold cuts generate traffic spikes and trial among younger demographics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over processed meats | -1.3% | Global, with heightened sensitivity in Western Europe, North America, urban Asia-Pacific | Long term (≥ 4 years) |

| Rise of plant-based protein alternatives | -1.1% | North America, Western Europe, early adoption in urban China and India | Medium term (2-4 years) |

| EPR packaging laws raise compliance costs | -0.7% | Europe, North America, spillover to Latin America | Short term (≤ 2 years) |

| Livestock disease-driven input volatility | -0.9% | Global, with acute impact in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over processed meats

Persistent associations between processed-meat consumption and chronic disease risk are constraining volume growth in mature markets, despite industry efforts to reformulate and reposition products. Nitrite and nitrate additives remain focal points of scrutiny, even as regulators acknowledge their role in preventing botulism and extending shelf life. The European Commission's 2025 nitrite reduction mandate reflects a precautionary approach, yet it imposes reformulation costs estimated at EUR 0.08-0.15 per kilogram for affected products, squeezing margins in price-sensitive categories. Sodium content is another pressure point; the U.S. Food and Drug Administration issued voluntary sodium-reduction targets in 2024, recommending that processed meats lower sodium levels by 20% over three years, a threshold that requires balancing flavor, microbial safety, and water-holding capacity [2]Source: U.S. Food and Drug Administration, "Sodium Reduction in the Food Supply," fda.gov. Processors are exploring potassium chloride and sea salt blends as partial sodium replacements. The health-concern headwind is most pronounced among affluent, educated demographics who have access to fresh, minimally processed alternatives.

EPR packaging laws raise compliance costs

Extended producer responsibility regulations are shifting packaging-waste management costs from municipalities to brand owners, compressing margins and forcing capital reallocation toward recyclable materials and lightweighting initiatives. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024 and phased in through 2030, requires all packaging to be recyclable or reusable, sets minimum recycled-content thresholds, and mandates deposit-return schemes for certain formats. Germany's VerpackG (Packaging Act) obligates producers to register with a dual-system operator and pay fees based on material type and weight, adding an estimated EUR 0.02-0.05 per kilogram for multi-layer films commonly used in modified atmosphere packaging [3]Source: German Federal Environment Agency, "VerpackG Compliance Guidance," umweltbundesamt.de. Processors are responding by consolidating suppliers, investing in mono-material films that simplify recycling, and redesigning secondary packaging to reduce plastic content. Processors are exploring advanced packaging technologies, such as bio-based and compostable films, to align with sustainability goals while maintaining product quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Poultry Dominates, Beef Accelerates

Poultry captured 41.54% of the market in 2025, driven by chicken's cost advantage, versatility, and broad culinary acceptance. Chicken remains ubiquitous in Latin America and Southeast Asia due to its affordability and adaptability to local cuisines. Additionally, the rising preference for lean protein sources among health-conscious consumers has further bolstered the demand for poultry cold cuts. Innovations in poultry processing, such as reduced-sodium formulations and clean-label offerings, are also contributing to the segment's expansion.

Beef registered a 9.12% CAGR through 2031, supported by its premium positioning and strong demand in foodservice channels. Beef cold cuts, including pastrami, corned beef, and roast beef, generate higher per-kilogram margins, particularly in artisanal sandwiches and charcuterie boards, which are gaining popularity in urban markets. The segment benefits from the growing trend of gourmet and specialty meat products, with consumers willing to pay a premium for high-quality, sustainably sourced beef. Additionally, advancements in preservation techniques, such as vacuum-sealed packaging, have extended shelf life and enhanced the appeal of beef cold cuts in retail and foodservice sectors.

By Form: Whole Cuts Gain Foodservice Traction

Sliced cold cuts held 43.82% of form-based share in 2025, driven by retail convenience and single-serve snack packs, yet the segment faces margin pressure from private-label competition and consumer preference for freshly sliced deli-counter offerings. Sliced cold cuts benefit from modified atmosphere packaging, which flushes the trays with nitrogen or carbon dioxide to inhibit oxidation and microbial growth, but the format's higher surface area accelerates moisture loss, limiting shelf life. Additionally, the rising demand for pre-packaged sliced cold cuts in urban areas is driven by their ease of use in ready-to-eat meals and sandwiches, catering to consumers' fast-paced lifestyles.

Whole cold cuts are projected to grow at 9.46% CAGR through 2031, outpacing sliced formats as foodservice operators seek portion control, labor savings, and visual differentiation in open-kitchen environments. Whole cold cuts, which include boneless hams, turkey breasts, and roast beef rounds, allow foodservice operators to slice to order, reducing waste and enabling customization for sandwiches, salads, and protein bowls. Packaging innovation is critical to whole-cut growth, as vacuum skin and shrink-bag formats extend refrigerated shelf life to 60-90 days, enabling centralized production and long-haul distribution. Ground or processed cold cuts, including luncheon meat, bologna, and liverwurst, are stable in value-oriented retail channels but are declining in premium segments, where consumers associate grinding with lower quality and higher processing intensity.

By Packaging Technology: Sustainability Mandates Accelerate Recyclable Adoption

Modified atmosphere packaging captured 34.13% of the packaging-technology share in 2025, leveraging nitrogen and carbon dioxide gas flushes to extend shelf life and maintain color stability; however, the format's reliance on multi-layer barrier films complicates recycling and attracts higher EPR fees under the European Union's Packaging and Packaging Waste Regulation. This technology is particularly effective at preserving the freshness of sliced cold cuts, minimizing oxidation and microbial growth, and ensuring product quality throughout extended distribution cycles. The growing demand for convenience foods and ready-to-eat products has also driven the adoption of modified atmosphere packaging, especially in urban markets where consumers prioritize freshness and extended shelf life.

Vacuum Skin Packaging is expanding at 10.85% CAGR through 2031, driven by extended producer responsibility mandates in Europe and North America that penalize non-recyclable multi-layer films and incentivize mono-material alternatives. Vacuum skin packaging, which molds a transparent film directly onto the product surface, eliminates air pockets and reduces drip loss, making it the preferred format for premium whole cuts and portion-controlled foodservice items. Sealed Air reported a 22% increase in vacuum skin film sales for meat applications in 2025, with growth concentrated in Europe and North America, where retailers prioritize visual appeal and extended shelf life. Processors are also exploring active packaging technologies that incorporate antimicrobial agents, oxygen scavengers, or moisture regulators into the film matrix, extending shelf life without additional preservatives and supporting clean-label positioning.

By Distribution Channel: Foodservice Recovery Outpaces Retail Maturity

Retail channels held 59.16% of distribution share in 2025, anchored by supermarkets and hypermarkets that offer broad assortments, promotional pricing, and private-label options, yet the segment faces saturation in North America and Western Europe, where per-capita cold-cuts consumption has plateaued. Within retail, supermarkets and hypermarkets benefit from economies of scale in procurement, refrigerated logistics, and promotional support, yet they are losing incremental share to online retail and specialty stores. Online retail is expanding as e-commerce platforms invest in cold-chain infrastructure and same-day delivery.

Foodservice and HoReCa channels are projected to grow at 8.59% CAGR through 2031, outpacing retail's mature trajectory as corporate return-to-office mandates, event resumption, and institutional catering demand drive volume recovery. Foodservice operators, by contrast, are expanding cold-cut offerings in boxed lunches, sandwich bars, and charcuterie platters, with Sysco Corporation reporting a 7% increase in deli-meat case volume during fiscal 2025. Quick-service restaurants are leveraging limited-time sandwich promotions featuring premium cold cuts to generate traffic spikes and trial among younger demographics.

Geography Analysis

North America accounted for 34.11% of global cold cuts revenue in 2025, reflecting mature per-capita consumption, extensive retail infrastructure, and a competitive landscape dominated by Tyson Foods, Hormel Foods, and Smithfield Foods. The region's cold cuts market is supported by strong foodservice recovery, increasing adoption of high-protein diets, and the growing popularity of convenient, ready-to-eat meat products. Retailers are also focusing on premiumization, offering organic and nitrate-free options to cater to health-conscious consumers. Mexico's cold cuts market is expanding rapidly, driven by urbanization, rising disposable incomes, and a growing preference for Western-style diets. In Canada, the pork sector is benefiting from robust export demand, with production shipped to international markets.

Asia-Pacific is projected to grow at 11.24% CAGR through 2031, the fastest rate among all regions, propelled by urbanization, Western-style protein adoption, and premiumization in China, India, Japan, and Southeast Asia. India's cold cuts market remains nascent due to vegetarian dietary traditions and limited cold-chain infrastructure, yet urban centers such as Mumbai, Delhi, and Bangalore are witnessing growth in Western-style deli meats as expatriate populations and affluent millennials drive trial. Southeast Asia, including Thailand, Indonesia, and Singapore, is benefiting from foodservice expansion and tourism recovery, with hotel, restaurant, and catering operators increasing cold-cut procurement for breakfast buffets, sandwich bars, and catering events.

Europe holds a significant share of global revenue in 2025, anchored by traditional charcuterie cultures in Germany, Italy, France, Spain, and Poland, where protected designation of origin certifications support premium pricing and differentiate regional specialties. Germany's processed-meat sector is consolidating, with large companies acquiring smaller producers to achieve scale in reformulation and EPR compliance. For instance, Goldschmaus acquired Hein and Wolf, underscoring the strategic imperative to spread fixed costs across higher volumes. The United Kingdom's post-Brexit regulatory divergence creates compliance complexity, as processors serving both EU and UK markets must navigate dual labeling, nitrite, and packaging standards.

Competitive Landscape

The cold cuts market is moderately fragmented, with global incumbents such as Tyson Foods, JBS, and Hormel Foods competing alongside regional specialists, private-label programs, and clean-label insurgents. This structure creates strategic opportunities for processors capable of navigating tightening nitrite limits, extended producer responsibility packaging mandates, and livestock disease volatility without compromising shelf life, sensory appeal, or margins. JBS reported consolidated net revenue of USD 84.1 billion for 2024, with North American operations accounting for 55% of total sales, underscoring the region's mature yet competitive nature.

Strategic trends in the market are converging on three key areas: clean-label reformulation to address health concerns and regulatory requirements; packaging innovation to comply with EPR laws and extend shelf life; and geographic expansion into high-growth Asia-Pacific markets, where the adoption of Western-style protein is accelerating. Emerging disruptors include plant-based meat startups capturing incremental share in deli slices and sausages, hybrid-protein innovators blending animal and plant ingredients, and direct-to-consumer brands leveraging e-commerce to bypass traditional retail intermediaries. Smaller players such as Applegate Farms, Dietz & Watson, and Boar's Head are challenging incumbents by emphasizing transparency, artisanal production, and no-antibiotic-ever sourcing, appealing to affluent consumers willing to pay premiums for perceived quality and ethical production.

Technology deployment is becoming a critical differentiator, with processors investing in high-pressure processing, pulsed electric fields, and natural antimicrobials to extend shelf life without additional preservatives. These advancements support clean-label claims and help reduce waste. The U.S. Patent and Trademark Office granted 47 patents related to meat-packaging technologies in 2025, including active films incorporating nisin, rosemary extract, and green tea polyphenols, signaling intensifying innovation in shelf-life extension. Regulatory compliance is emerging as a competitive advantage; processors with in-house R&D capabilities and reformulation expertise are better positioned to adapt to nitrite reduction and EPR packaging mandates compared to smaller rivals reliant on co-packers and third-party suppliers.

Cold Cuts Industry Leaders

-

Tyson Foods Inc.

-

WH Group (Smithfield Foods)

-

Hormel Foods Corp.

-

BRF S.A.

-

JBS S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Marfrig Global Foods and BRF S.A. completed a merger, creating MBRF Global Foods Company S.A., a new global meat-processing giant. The deal creates a major competitor to JBS and Tyson Foods, combining Marfrig's strength in beef (including National Beef in the US) with BRF's dominant poultry, pork, and processed food operations.

- July 2025: Columbus Craft Meats, a Hormel Foods brand, expanded its deli meat portfolio by introducing its first standalone uncured pepperoni product. This launch responded directly to consumer demand for premium, versatile deli options and reinforces Hormel’s competitive positioning in the premium deli sector with a clean-label, additive-free offering.

- April 2025: BRF inaugurated a new plant in Jeddah, Saudi Arabia, slated to begin operations with a capacity of 40,000 tons per year, potentially increasing to 80,000 tons based on demand. This new plant represents the company's seventh unit in the Middle East, strengthening its local presence and supply chain.

- January 2025: Brooklyn Cured launched new Cocktail-Inspired Salami flavors, Dirty Martini Salami and pork-free Tuscan Red Wine Beef Salami, while expanding national store placements for its Snack Packs and refreshing its online presence. This demonstrated the company’s focus on flavor innovation, dietary inclusivity (pork-free), and strengthening brand visibility both in retail and digital channels.

Global Cold Cuts Market Report Scope

Cold cuts, also known as deli meats, lunch meats, or sliced meats, are pre-cooked or cured meat products, such as ham, poultry, beef, turkey, salami, and bologna, that are sliced and served cold or at room temperature. The cold cuts market is segmented by product type, form, packaging technology, distribution channel, and geography. Based on product type, the market is segmented into pork, beef, poultry, and other meats. By form, the market is segmented into sliced, whole, and ground or processed cold cuts. By packaging technology, the market has been segmented into modified atmosphere packaging (MAP), vacuum skin packaging, and others. By distribution channels, the market has been segmented into foodservice/HoReCa and retail. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (units).

| Pork |

| Beef |

| Poultry |

| Other Meats |

| Sliced Cold Cuts |

| Whole Cold Cuts |

| Ground or Processed Cold Cuts |

| Modified Atmosphere Packaging (MAP) |

| Vacuum Skin Packaging |

| Others |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores |

| Other Distribution Channels | |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Pork | |

| Beef | ||

| Poultry | ||

| Other Meats | ||

| By Form | Sliced Cold Cuts | |

| Whole Cold Cuts | ||

| Ground or Processed Cold Cuts | ||

| By Packaging Technology | Modified Atmosphere Packaging (MAP) | |

| Vacuum Skin Packaging | ||

| Others | ||

| By Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| By Geography | Other Distribution Channels | |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cold cuts market by 2031?

The cold cuts market is forecast to reach USD 91.62 billion by 2031, advancing at a 7.79% CAGR from 2026-2031.

Which protein segment is expected to grow the fastest through 2031?

Beef leads growth with a projected 9.12% CAGR because consumers view it as a lean, clean-label-friendly option.

Which region offers the highest growth opportunity for cold cuts?

Asia-Pacific holds the strongest outlook with an expected 11.24% CAGR driven by urbanization and Western-style protein adoption.

Why are whole cold cuts gaining share in foodservice?

Foodservice operators prefer whole muscles they can slice on demand, reducing waste and signaling freshness, which underpins a 9.46% CAGR to 2031.

Page last updated on: