Green Coffee Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 32.86 Billion |

| Market Size (2030) | USD 44.39 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

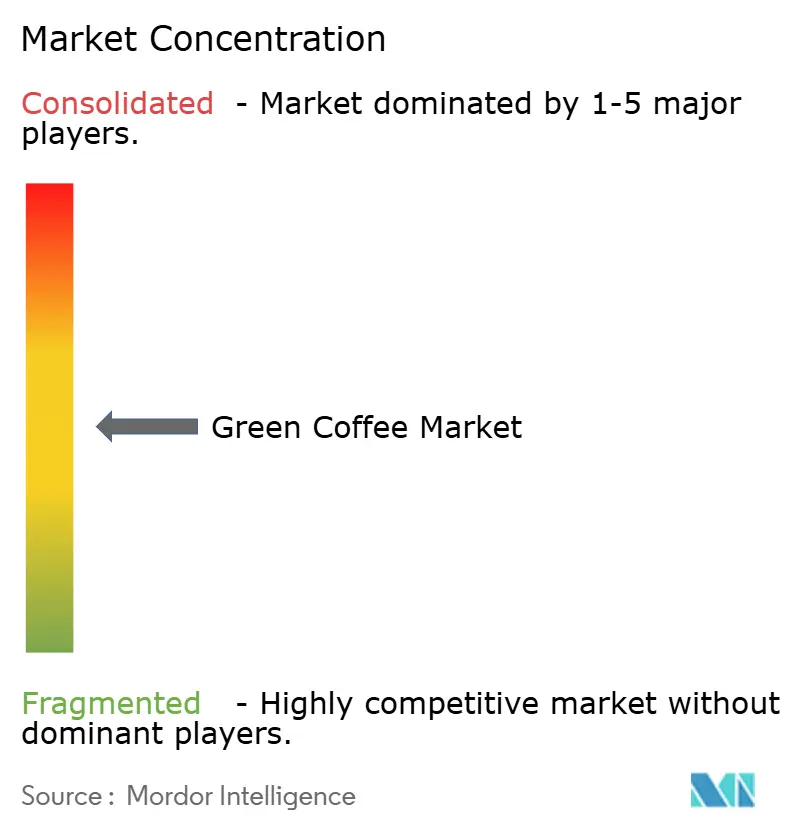

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Green Coffee Market Analysis by Mordor Intelligence

In 2025, the global green coffee market size was valued at USD 32.86 billion. Projections indicate an ascent to USD 44.39 billion by 2030, marking a CAGR of 6.20% from 2025 to 2030. This is bolstered by a steady demand for certified beans, a surge in health applications for green coffee extract, and a swift embrace of premium products in the Asia-Pacific region. Major roasters are pivoting to direct-trade models, streamlining supply chains, and boosting farmer incomes. Concurrently, producers are channeling investments into climate-resilient varietals to safeguard future yields. Innovative practices like controlled-environment farming and hydroponic trials are emerging in unconventional regions, broadening production horizons. However, the landscape is not without challenges: regulatory shifts, notably the EU Deforestation Regulation and fresh U.S. tariffs, are recalibrating trade dynamics and heightening competition for compliant supplies. This growth narrative underscores the sector's adaptability in the face of climate adversities and a shifting consumer tilt towards premium, sustainable coffee offerings. The market's upward momentum is fueled by a burgeoning appetite for specialty coffee, heightened health awareness propelling green coffee extract consumption, and a rapidly expanding coffee-loving middle class in the Asia-Pacific.

Key Report Takeaways

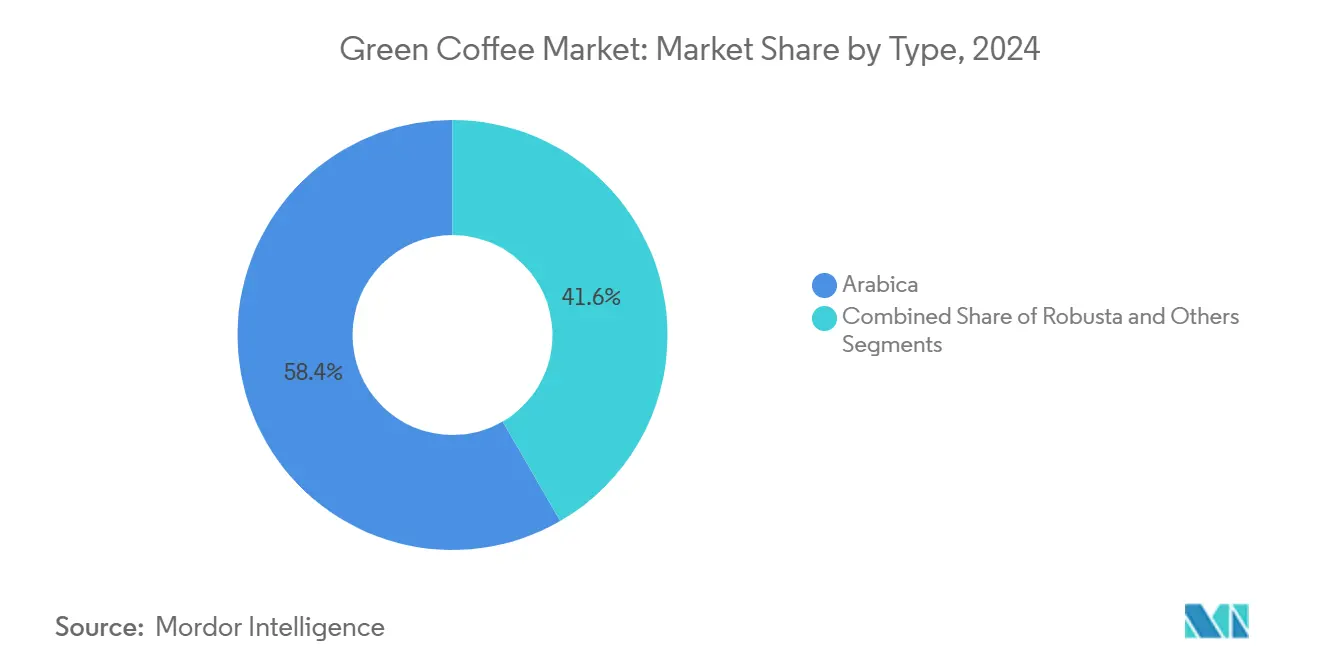

- By type, Arabica retained 58.36% of the green coffee market share in 2024, while Robusta is projected to grow at 5.40% CAGR to 2030.

- By form, green coffee beans accounted for 82.63% share of the green coffee market size in 2024; green coffee extract is advancing at 6.10% CAGR through 2030.

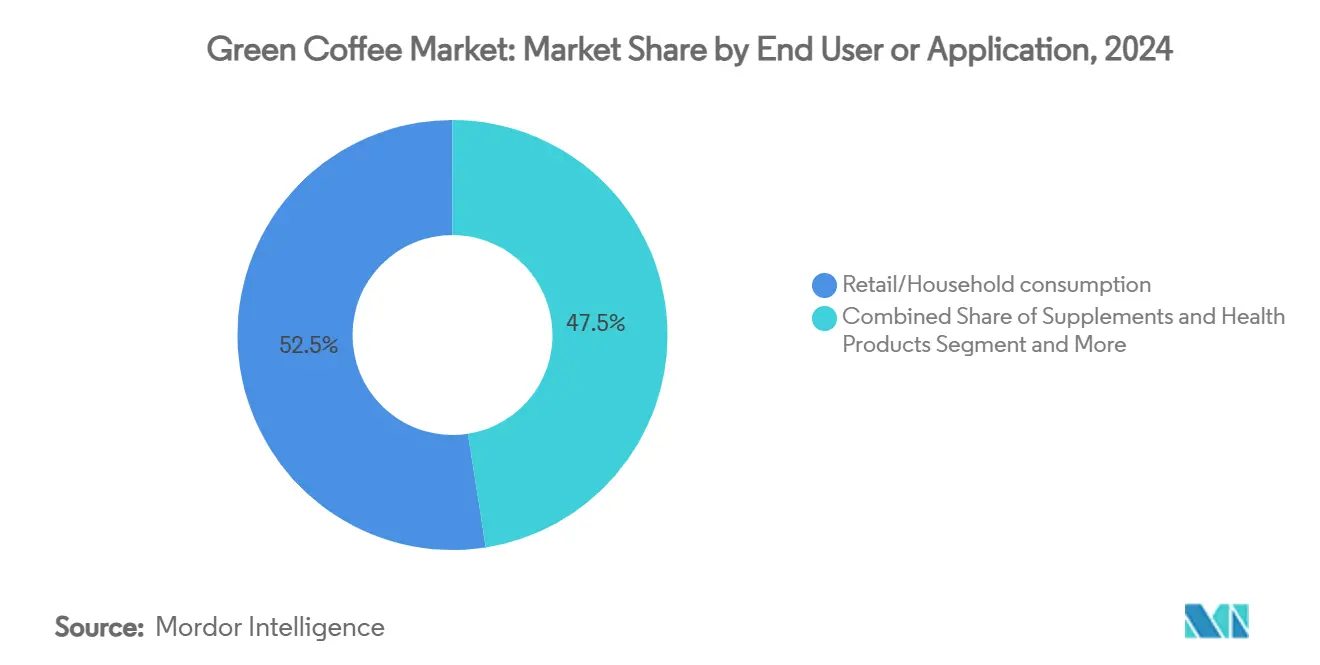

- By end user/application, retail and household consumption led with 52.47% revenue share in 2024, whereas supplements and health products are set to expand at 7.20% CAGR to 2030.

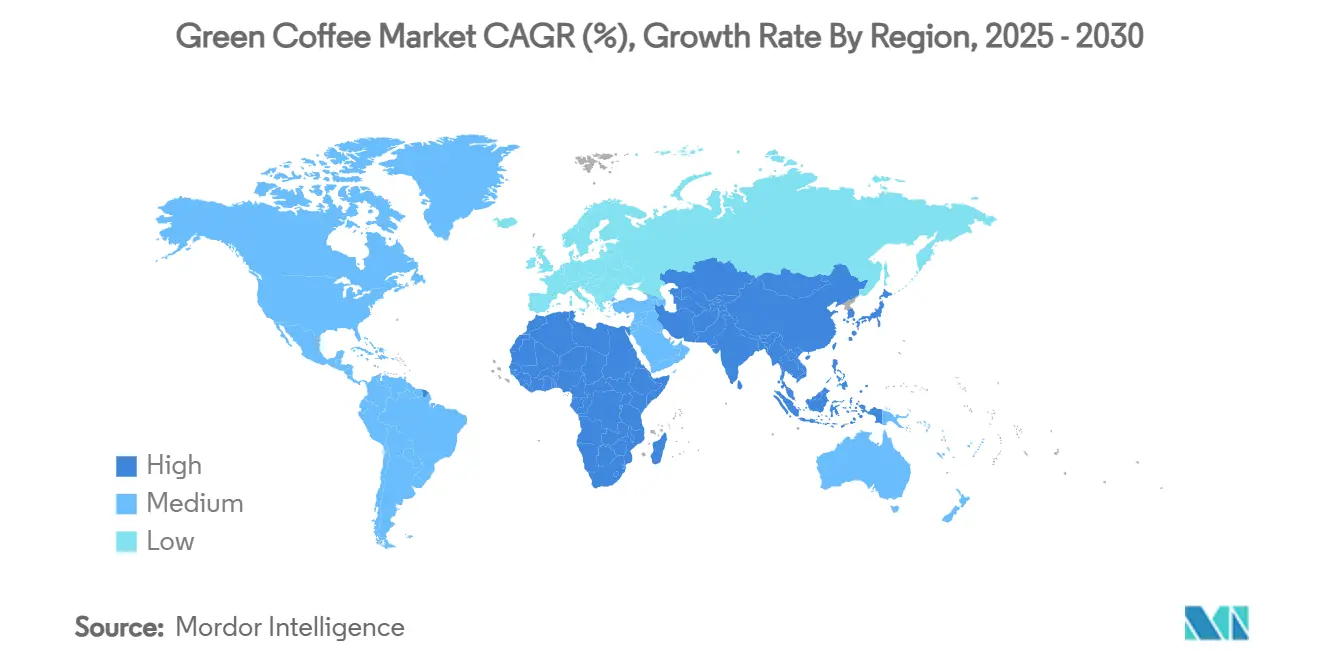

- By region, Europe dominated with 36.29% of the green coffee market in 2024; Asia-Pacific is the fastest-growing region at 5.70% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Green Coffee Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for specialty & premium coffee | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising consumer focus on sustainable & certified coffee | +1.2% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| Expansion of coffee-consuming middle class in Asia-Pacific | +1.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Controlled-environment coffee cultivation | +0.8% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Digitally enabled direct-trade platforms | +0.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Health and wellness trends shaping green coffee consumption | +0.9% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Specialty & Premium Coffee

As consumers increasingly prioritize quality over price, premium coffee consumption is reshaping market dynamics, leading to substantial value-chain premiums for differentiated products. The Specialty Coffee Association's 2024 National Coffee Data Trends report[1]Speciality Coffee Association, "2024 National Coffee Data Trends Specialty Coffee Breakout Report Now Available", June 2024, sca.coffee revealed that over 80% of millennials recognize sustainable coffee and are willing to pay a premium for sustainably sourced products. Millennials and Gen Z consumers are showing a growing preference for single-origin, micro-lot, and certified beans, leading to a heightened willingness to pay premiums. This trend is spurring investments in quality control and traceability systems. Highlighted at the 2025 World of Coffee Jakarta trade show, Indonesian growers are seizing this opportunity by marketing distinct flavor profiles and establishing direct-trade partnerships, thereby amplifying their value capture at the origin. In response, roasters are entering long-term contracts to secure consistent cup profiles, simultaneously rewarding sustainable practices. This quality emphasis is driving experimentation with controlled fermentation, anaerobic processing, and precision agriculture to enhance sensory attributes. Furthermore, the rising specialty demand is broadening revenue streams for origin countries, prompting a diversification beyond traditional commodity grades.

Rising Consumer Focus on Sustainable & Certified Coffee

In the green coffee market, especially in Europe and North America, sustainability certifications have transitioned from being niche differentiators to becoming baseline expectations. Importers now increasingly demand credentials like Rainforest Alliance, Fairtrade, or Organic, viewing them as essential proof of environmental stewardship and social compliance. With the EU's upcoming Deforestation Regulation, there's a heightened emphasis on ensuring coffee is sourced without contributing to deforestation. This has led exporters to invest in satellite monitoring and digital traceability tools. Certified suppliers enjoy preferential access and pricing, while those who fall short face potential exclusion. To streamline processes, industry alliances are harmonizing code requirements, reducing audit redundancies, and offering guidance to smallholders grappling with increasing administrative demands. The Global Coffee Platform has noted a rise in sustainability schemes aligning with the Coffee Sustainability Reference Code, underscoring the industry's commitment to standardized sustainable practices. European markets are at the forefront of this shift. In 2023, the EU imported 133,000 tonnes of organic green coffee, marking a notable uptick even amidst broader market challenges.[2]Government of the Netherlands, "European market potential for organic coffee", April 2025, www.cbi.eu

Expansion of Coffee-Consuming Middle Class in Asia-Pacific

As incomes rise and lifestyles shift in Asia-Pacific, the region's burgeoning middle class is fueling a growing appetite for premium and specialty green coffee products. The World Bank and the Asian Development Bank report that, while economic growth in the region is moderating, it continues to uplift millions from poverty annually. Projections suggest that by 2030, Asia will be home to two-thirds of the global middle class. This expanding demographic isn't just confined to major urban hubs; it's making its mark in smaller cities and towns, amplifying the reach of coffee culture. With rising incomes and a tilt towards western lifestyles, consumers are increasingly gravitating towards higher-quality, health-centric beverages, including green coffee. This trend is evident in both retail and foodservice sectors. As this middle class gains prominence, they're not just consumers but trendsetters, prompting both international brands and local producers to innovate and adapt. Given this backdrop of economic growth and an insatiable appetite for premium products, the Asia-Pacific region is poised to be a significant player in the green coffee market's expansion in the coming years.

Controlled-Environment Coffee Cultivation

In response to climate change pressures, there's a growing interest in greenhouse, shade-housing, and hydroponic systems for coffee cultivation, adept at regulating temperature and moisture. Pilot projects in California and North Carolina highlight the commercial viability of producing high-quality beans outside their traditional tropical zones. These innovative systems can cut water usage by up to 90%, reduce pest occurrences, and facilitate year-round harvesting, though they come with elevated capital costs. However, advancements in energy-efficient lighting and automated climate controls promise to reduce operating costs. This positions controlled environments as a long-term complement to open-field production in the green coffee market. As climate change poses increasing threats, technological advancements in controlled-environment agriculture emerge as strategic solutions, paving the way for sustainable coffee production in unconventional regions. Research from the University of California, published in the International Journal of Climatology, indicates that with appropriate thermal management strategies, such as agroforestry shade trees, over 230 km² of coastal southern and central California land could be primed for coffee cultivation.

Restraints Impact Analysis of Green Coffee Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change-driven yield & quality volatility | -2.1% | Global, especially Brazil, Vietnam, Central America | Short term (≤2 years) |

| Trade barriers restrict access to developed markets | -1.3% | Global, impacting developing-country exporters | Medium term (2-4 years) |

| Competition from traditional coffee products | -0.8% | Global, particularly in price-sensitive markets | Medium term (2-4 years) |

| Labor shortages due to rural-urban migration | -0.9% | Origin countries in Central America and Southeast Asia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Climate-Change-Driven Yield & Quality Volatility

Climate change is wreaking havoc on the green coffee market, with rising temperatures, erratic rainfall, and extreme weather events disrupting production in major growing regions. The Intergovernmental Panel on Climate Change (IPCC) warns that by 2050, nearly half of the land now suitable for coffee cultivation could be rendered unusable. Global yields are set to plummet due to shifting temperature and precipitation patterns. This isn't just a future concern: Vietnam's coffee production plummeted by 20% in the 2023/24 season due to a prolonged drought[3]International Comunicaffe, "Climate change: challenges for the coffee industry in 2025", International Comunicaffe, February 2025, www.comunicaffe.com. Meanwhile, Brazil's 2024 harvest faced setbacks from both drought and extreme heat. Such climatic challenges not only diminish yields but also compromise bean quality. Elevated temperatures and erratic rainfall heighten susceptibility to pests, diseases, and disorders, impacting both the quantity and flavor of green coffee. These challenges jeopardize farmer livelihoods and threaten the stability of global coffee supply chains, a concern echoed by the International Coffee Organization (ICO) and various government studies. As climate change's grip tightens, the green coffee market grapples with heightened uncertainty, soaring production costs, and supply instability, highlighting an urgent call for adaptive strategies across the sector.

Trade Barriers Restrict Access to Developed Markets

In April 2025, the U.S. imposed tariffs ranging from 10% to a steep 46% on imports from major producing nations. This move not only jacked up domestic prices but also nudged roasters to scout for alternative sources. Meanwhile, the EU's Deforestation Regulation has thrown compliance challenges, especially for smallholders who lack the digital traceability tools. If these producers falter in meeting the new documentation standards, they risk losing out on volumes from Ethiopia and other regions that heavily depend on EU demand. Although trade agreements like the EVFTA offer some relief by softening duties, they come with an added layer of administrative burdens and potential penalties, casting a shadow of uncertainty over exporters and dampening short-term growth prospects. Recent government interventions and tightening tariff regimes have erected significant trade barriers for the green coffee market, limiting access to major markets, especially in the U.S. and EU. The U.S., as highlighted by the U.S. Department of Agriculture, stands as a titan in the green coffee import arena, drawing over 20% of its supply from Colombia, alongside notable quantities from Brazil, Vietnam, and Mexico. However, the landscape shifted in 2025 when the U.S. introduced new tariffs: a hefty 50% on Brazilian coffee and escalated rates on imports from both Indonesia and Vietnam. Such trade barriers have sent ripples through the global supply chain, inducing price volatility and availability issues, and often triggering retaliatory actions that further unsettle the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Green Coffee Market Segment Analysis

By Type:

Robusta Resilience Challenges Arabica DominanceIn 2024, Arabica commanded a 58.36% share of the green coffee market, buoyed by a deep-rooted consumer preference for its sweeter, more nuanced flavor profile. Yet, with Robusta projected to grow at a 5.40% CAGR through 2030, growers are strategically pivoting towards this hardier variety, known for its resilience to heat, pests, and unpredictable rainfall. Specialty roasters are increasingly experimenting with fine Robusta lots, bridging the historical perception divide and expanding their portfolios to mitigate climate risks. Ongoing breeding initiatives focus on reducing bitterness and enhancing flavor complexity, solidifying Robusta's position as a premium contender. As climate challenges mount in traditional Arabica regions, the quality perception gap between the two is closing, with U.S. and European specialty roasters actively seeking high-quality Robusta.

Robusta's upward trajectory underscores its positioning as a climate-resilient alternative, with research institutions, like the University of Florida, pioneering improved varieties to cater to future demands. Their climate-smart coffee research highlights Robusta's adaptability and its potential for higher yields with reduced resource input, indicating its ability to flourish in varied environments without compromising quality. Robusta’s ascent is further bolstered by supply-chain shifts, a response to Arabica's susceptibility to extreme temperatures. Early 2025 witnessed Vietnamese Robusta prices surge to a 50-year peak, driven by crop shortfalls, underscoring the market's volatility. Producers are harnessing fermentation techniques and selective drying to boost cup scores, while researchers delve into grafting and genome editing for enhanced disease resistance. While Arabica may continue to reign supreme among connoisseurs, the green coffee market is increasingly acknowledging Robusta's pivotal role in ensuring volume and affordability.

By Form:

Extract Innovation Disrupts Traditional Bean MarketsIn 2024, green coffee beans commanded a significant 82.63% share of the revenue, anchoring the global supply chains for roasting, soluble products, and ready-to-drink (RTD) offerings, catering to both household and foodservice channels. Illustrating the trend, multinational traders are bolstering their storage and processing capabilities. For instance, in 2025, the Louis Dreyfus Company is set to double its capacity in Varginha, Brazil, in response to the surging throughput demands. This green coffee dominance is further underscored by a growing consumer appetite for premium, single-origin, and micro-lot beans. Major producing nations like Brazil, Colombia, and Ethiopia, capitalizing on their favorable climates and continuous investments, are fortifying their supply chains to satiate the world's expanding thirst for green coffee.

Yet health-centric demand is propelling green coffee extract, which is forecast to grow at 6.10% CAGR to 2030 as research links chlorogenic acids to weight management and metabolic benefits. Supplement brands integrate standardized extracts into capsules, beverages, and functional snacks, broadening consumer reach beyond traditional brews. Clinical studies demonstrating reductions in BMI, waist circumference, and lipid profiles after six-month supplementation underpin credibility, even as regulatory agencies such as the FDA and Health Canada maintain cautious guidance on dosage. This scientific momentum spurs product innovation, from sugar-free cold brews fortified with green coffee extract to skincare serums leveraging antioxidant properties. As marketing emphasises clean labels and plant-based actives, extract-led formats will continue to chip away at bean-centric dominance in the green coffee market.

By End User/Application:

Health Products Surge Past Traditional ConsumptionIn 2024, retail and household channels dominated the green coffee market, claiming 52.47% of the share. This underscores the beverage's entrenched status as a daily staple in both mature and emerging economies. Supermarkets and e-commerce platforms are enhancing access to certified single-origin beans, driving the trend of specialty brewing at home. The segment enjoys the advantage of established distribution networks and ingrained consumer habits. Major retailers and coffee chains are further amplifying their presence through both physical stores and digital platforms. According to Deloitte's 2024 coffee study, which surveyed 7,000 consumers across 13 countries, the rising prices are nudging consumers towards home brewing. Notably, these consumers are showing a readiness to pay a premium for coffee that's sustainably produced.

Meanwhile, the supplements and health products sector is poised to register a 7.20% CAGR through 2030, signaling a pronounced shift towards functional nutrition. Brands are touting green coffee extract shots for their energy-boosting and weight management properties. Furthermore, formulators are enhancing these extracts by blending them with collagen, adaptogens, and probiotics, resulting in multi-benefit products. The foodservice sector, especially in the rapidly urbanizing centers of Asia-Pacific, is witnessing a surge in demand. The burgeoning café culture is propelling the appetite for high-margin espresso-based drinks. While cosmetics remain a niche, they're witnessing rapid growth. Formulators are tapping into caffeine's antioxidant properties and its benefits for skin micro-circulation. Collectively, these trends highlight the expanding revenue avenues within the green coffee market.

Geography Analysis

Europe Green Coffee Market

Europe stands as the dominant player in the global green coffee arena, commanding a 36.29% share in 2024. This stronghold is bolstered by a rich coffee culture and a pronounced demand for premium and sustainable offerings. Germany, Italy, and France lead the charge, with consumers gravitating towards high-quality, organic, and specialty green coffee. There's also a burgeoning interest in the health benefits of unroasted beans. Sustainability and traceability are paramount in European markets, with many consumers prioritizing beans that are both organic and ethically sourced. The continent's vibrant café culture, combined with the rise of home brewing and specialty coffee shops, ensures a consistent demand, solidifying Europe's status as a pivotal hub for green coffee imports and innovations.

APAC Green Coffee Market

Asia-Pacific is set to lead the global green coffee market, with projections indicating a CAGR of 5.70% through 2030. This growth is fueled by rising incomes, swift urbanization, and the embrace of Western coffee culture in nations like China, India, and Vietnam. As the region's middle class seeks out premium and specialty coffee experiences, demand surges for high-quality green beans and innovative coffee products. Vietnam, historically recognized for its robusta, is now channeling investments into specialty arabica production. Concurrently, global chains, notably Starbucks, are swiftly broadening their footprint in major cities across China and Southeast Asia. This underscores the region's appetite for both traditional and specialty green coffee. Adding to this momentum, a shift towards e-commerce and online retail channels is making green coffee more accessible to a wider audience.

The Americas and MEA Green Coffee Market

Regions such as North America, Latin America, the Middle East, and Africa also hold significant stakes in the global green coffee market, each with its unique growth trajectories and dynamics. North America, spearheaded by the U.S. and Canada, witnesses steady demand, bolstered by a robust specialty coffee segment and heightened awareness of green coffee's health perks. Latin America, with Brazil and Colombia at the helm, not only dominates as a leading producer in the global supply chain but also witnesses a surge in domestic consumption. Meanwhile, in the Middle East and Africa, urbanization and a surge in coffee shops are amplifying demand, with Saudi Arabia and South Africa standing out as burgeoning markets. Across these diverse regions, trends like premiumization, product innovation, and the rise of digital retail channels are reshaping the green coffee landscape.

Competitive Landscape

With a concentration score of 5 out of 10, the green coffee market showcases moderate fragmentation. While Neumann Kaffee Gruppe, Olam Group, and Louis Dreyfus Company leverage scale advantages to dominate trading volumes, niche roasters and origin-based exporters carve out their share through a focus on quality and sustainability. Illustrating the trend of ongoing consolidation, JAB Holding bolstered its downstream roasting presence by acquiring a 17.6% stake in JDE Peet’s from Mondelez for a hefty USD 2.3 billion. In a bid for vertical integration, Starbucks and Nestlé are making strategic moves: Starbucks has inaugurated two innovation farms in Central America to experiment with climate-resilient coffee varietals, and Nestlé is banking on its “Star 4” Arabica variety, touted for its higher yields and rust resistance.

As specialty coffee shops proliferate, especially in Europe and the Asia-Pacific region, competition is heating up. This surge is compelling both established and nascent firms to carve out distinctions through unique sourcing, direct trade ties, and innovative products. Key players in the market, such as Neumann Kaffee Gruppe, Louis Dreyfus Company BV, Sucafina, Volcafe Ltd., and Merchants of Green Coffee, are not just trading and processing specialists. They are instrumental in sourcing, ensuring quality, and managing the supply chain, with a pronounced emphasis on sustainability and traceability to align with shifting consumer and regulatory expectations. The market landscape is further shaped by strategic maneuvers, like Neumann Kaffee Gruppe’s 2023 acquisition of Nordic Approach Group to bolster its specialty coffee offerings, and Sucafina’s takeover of Sustainable Harvest, broadening its North American and specialty trading footprint.

Digital platforms are revolutionizing the industry. TYPICA, for instance, links farmers across 36 countries with roasters in 40, slashing intermediary fees and more than doubling farm-gate earnings. Westrock Coffee’s state-of-the-art automated facility in Arkansas underscores the industry's pivot towards manufacturing efficiency, catering to the rising demand for ready-to-drink products. On the frontier of innovation, startups delving into hydroponic and cultured-cell coffee production are challenging the status quo, aiming to localize supply in temperate regions and diminishing the traditional advantages of coffee origins. Thus, in the green coffee market, competitive dynamics are influenced not just by land and export capabilities, but also by research and development strength, digital integration, and readiness for compliance.

Green Coffee Industry Leaders

-

Neumann Kaffee Gruppe

-

Olam Group

-

ECOM Agroindustrial

-

Louis Dreyfus Company Coffee

-

Sucafina S.A

- *Disclaimer: Major Players sorted in no particular order

Green Coffee Market Companies Covered in this Report

- Neumann Gruppe GmbH

- Olam Group Limited

- ECOM Agroindustrial Corp. Limited.

- Louis Dreyfus Holding B.V.

- Sucafina SA

- ED&F Man Commodities (Volcafe)

- Royal Coffee

- Grupo Tristao

- Intercontinental Coffee Trading (ICT)

- Coffee Bean Corral

- Westrock Coffee Company

- Forest Coffee

- StoneX Specialty Coffee

- Ally Coffee

- Burman Coffee Traders, LLC

- Tata Consumer Products Limited

- Paragon Coffee Trading Company

- Taiyo Kagaku Corporation

- Colombian Direct Coffee

- Caravela Limited

Recent Industry Developments in Green Coffee Market

- July 2025: Louis Dreyfus Company doubled coffee storage and processing capacity at its Varginha, Brazil hub to meet rising global demand.

- October 2024: JAB Holding bought Mondelez’s 17.6% stake in JDE Peet’s for USD 2.3 billion, raising its ownership to 68% .

- June 2024: Westrock Coffee Company has inaugurated North America's largest roast-to-ready-to-drink manufacturing facility. Spanning 570,000 square feet in Conway, Arkansas, this state-of-the-art facility, boasting a USD 315 million investment, features an extensive beverage development laboratory. With this facility, Westrock Coffee solidifies its leadership in coffee and Ready-To-Drink beverage innovation and production.

Global Green Coffee Market Report Scope

Segmentation Overview

| Arabica |

| Robusta |

| Others |

| Instant Green Coffee Premix |

| Green Coffee Beans |

| Green Coffee Powder |

| Green Coffee Extract |

| Retail/Household Consumption |

| FoodService/HoReCa |

| Supplements and Health Products |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Columbia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Arabica | |

| Robusta | ||

| Others | ||

| By Form | Instant Green Coffee Premix | |

| Green Coffee Beans | ||

| Green Coffee Powder | ||

| Green Coffee Extract | ||

| By End User/Application | Retail/Household Consumption | |

| FoodService/HoReCa | ||

| Supplements and Health Products | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Columbia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the green coffee market?

The green coffee market size stood at USD 32.86 billion in 2025 and is projected to reach USD 44.39 billion by 2030.

Why is Robusta coffee gaining momentum?

Robusta offers higher tolerance to heat and pests, enabling cost-effective cultivation in a warming climate, and is expected to grow at 5.40% CAGR to 2030.

What drives demand for green coffee extract?

Clinical studies linking chlorogenic acids to weight management and metabolic health are pushing extract formats to a 6.10% CAGR through 2030.

How fragmented is the green coffee market?

With a concentration score of 5, the market is moderately fragmented; the top five players handle just over half of global trade, leaving scope for specialist competitors.

How does the EU Deforestation Regulation affect coffee suppliers?

From 2025, exporters must prove beans are deforestation-free, favouring producers with robust traceability and excluding non-compliant supply.

Page last updated on: