Cognitive AI Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

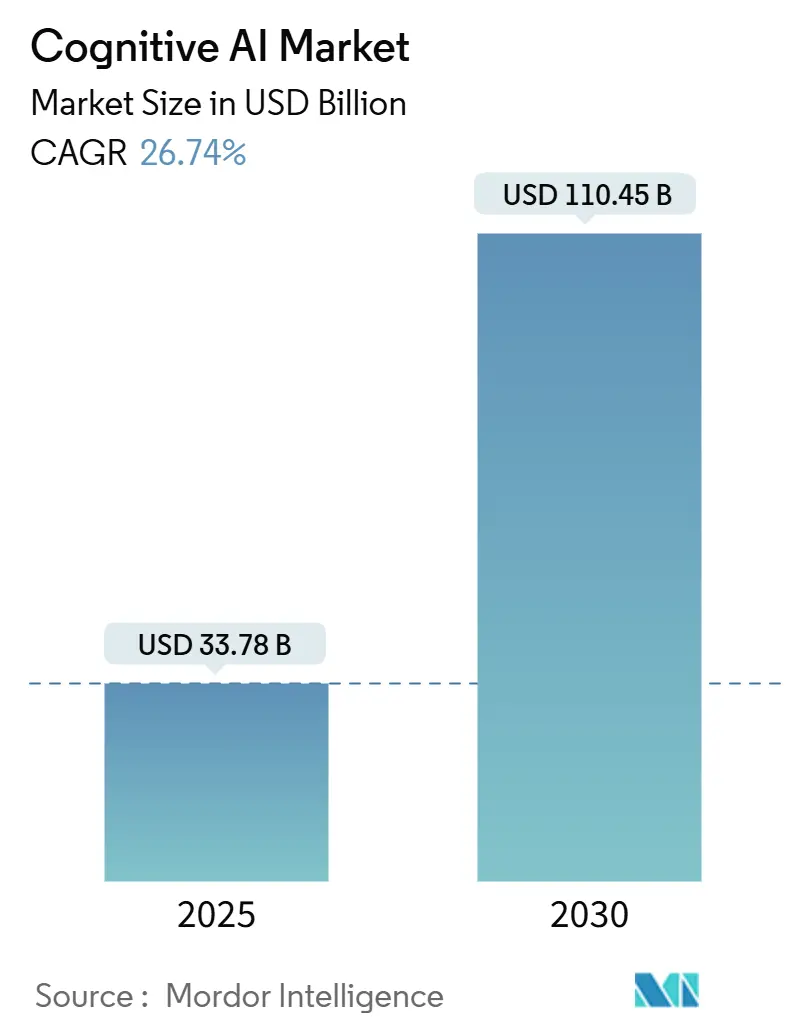

| Market Size (2025) | USD 33.78 Billion |

| Market Size (2030) | USD 110.45 Billion |

| Growth Rate (2025 - 2030) | 26.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive AI Market Analysis by Mordor Intelligence

The cognitive AI market size climbed to USD 33.78 billion in 2025 and is forecast to reach USD 110.45 billion by 2030, translating into a 26.74% CAGR. Momentum stems from sovereign AI mandates that require on-device inference, the Pentagon’s USD 15 billion procurement signal, and the fusion of generative algorithms with established business-intelligence stacks [1]Government Accountability Office, “Defense AI Procurement,” defense.gov. Rising data-localization rules accelerate hybrid cloud-edge deployments, while platform vendors differentiate through explainable-AI toolkits that satisfy the EU AI Act [2]European Union, “Regulation (EU) 2024/… on Artificial Intelligence,” eur-lex.europa.eu . Hardware shortages and talent gaps temper adoption but also boost demand for managed services and small-language-model innovation. Competitive intensity grows as Chinese patent holders widen their intellectual-property lead, pressuring Western incumbents to deepen vertical specialization.

Key Report Takeaways

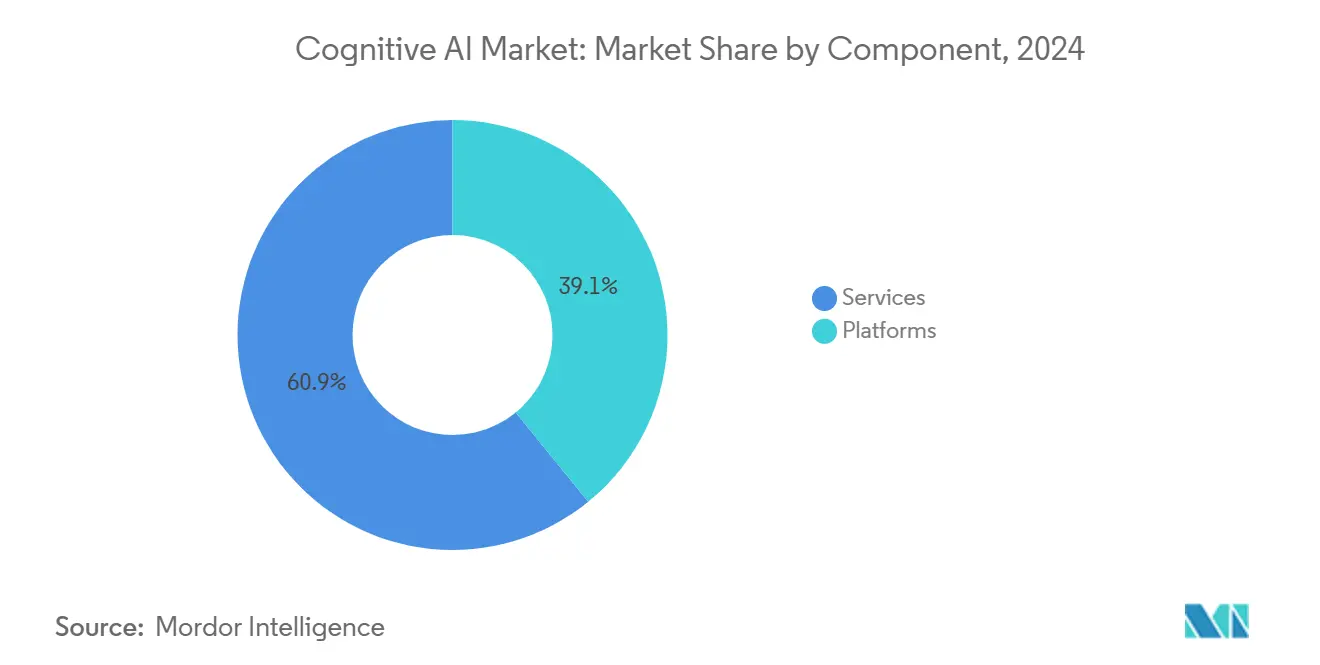

- By component, platforms led with 39.12% revenue share in 2024, while services are set to grow at a 27.02% CAGR through 2030.

- By technology, natural-language processing held 42.24% of the cognitive AI market share in 2024, whereas machine learning and deep learning are projected to expand at a 27.56% CAGR to 2030.

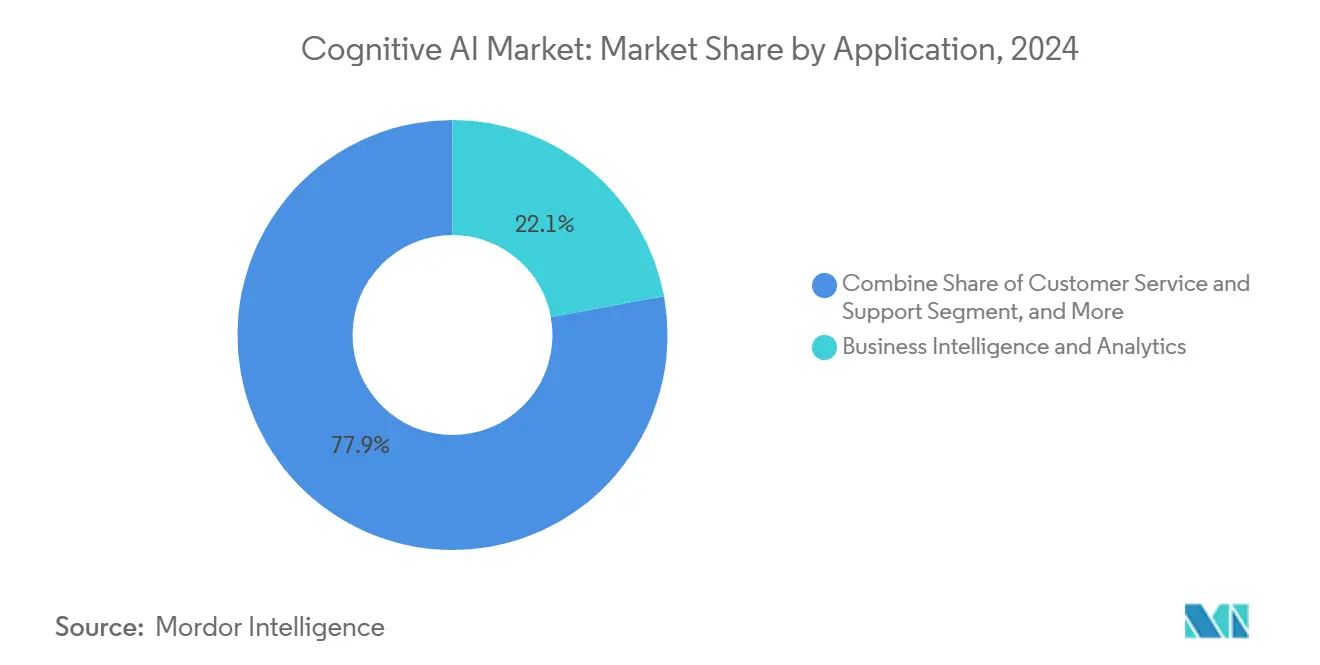

- By application, business intelligence and analytics commanded 22.11% of the cognitive AI market size in 2024, and customer service and support are advancing at a 26.96% CAGR through 2030.

- By end-user industry, BFSI captured 24.85% share of the cognitive AI market in 2024, while retail and e-commerce registered the highest forecast CAGR at 28.71% to 2030.

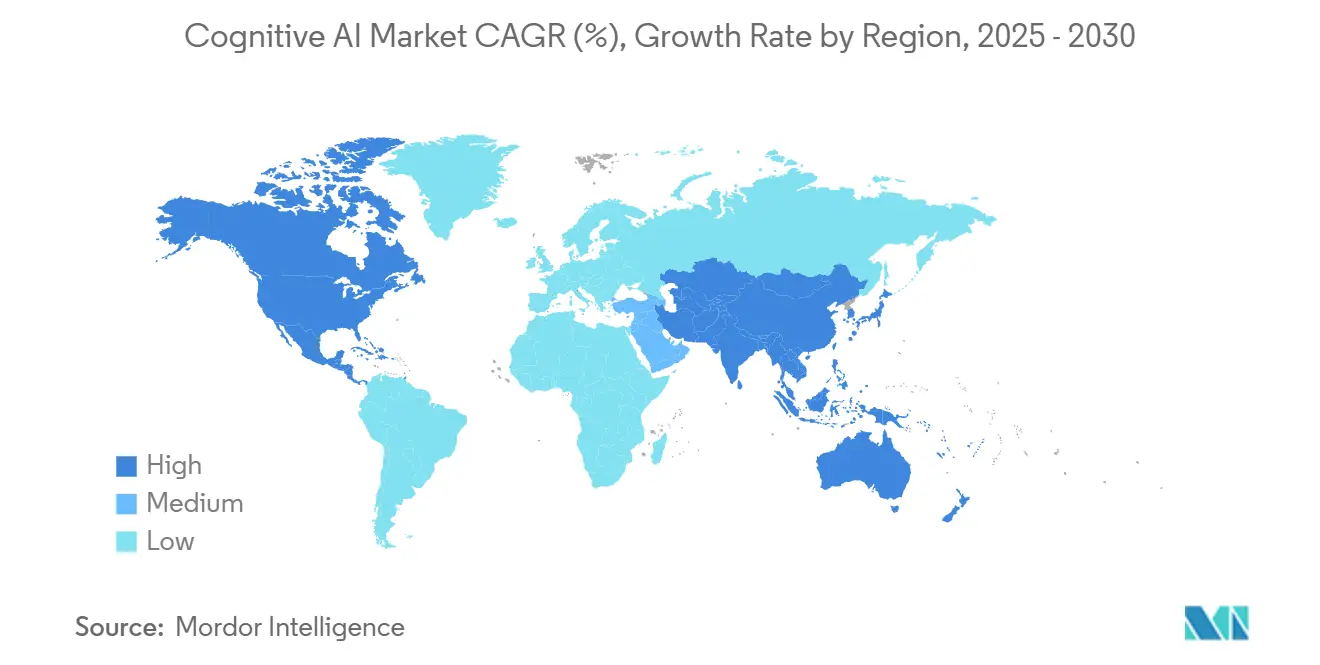

- By geography, North America accounted for a 37.45% share in 2024, and the Asia Pacific is on track for a 27.12% CAGR through 2030.

Global Cognitive AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of enterprise and edge data lakes | +4.2% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Shift to Gen-AI copilots inside SaaS suites | +2.8% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Rise of low-code cognitive service marketplaces | +3.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Regulatory mandates for explainability in high-risk AI | +2.5% | EU, North America, with adoption in APAC | Long term (≥ 4 years) |

| Quantum-ready cognitive pipelines for Monte-Carlo workloads | +1.9% | North America, EU, Japan | Long term (≥ 4 years) |

| Small-language-model distillation for on-device cognition | +1.7% | Global, with early gains in mobile-first markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosion of Enterprise and Edge Data Lakes

Enterprises deploy cognitive AI systems at edge locations to cut latency and meet data-localization rules under GDPR. Real-time inference across distributed data lakes demands hybrid cloud-edge architectures that legacy AI stacks cannot match. Vendors that enable multimodal ingestion across on-premises and cloud assets win larger deals. Supply-chain leaders already cite USD 500 billion in potential efficiency gains from faster decisions.

Shift to Gen-AI Copilots Inside SaaS Suites

SaaS leaders bake cognitive copilots directly into workflows, moving from optional add-ons to default features [3]Oracle Corp., “Generative AI in Fusion Cloud Applications,” oracle.com . The model lifts per-seat pricing yet cuts adoption friction because users tap AI inside familiar interfaces. Professional-services teams leverage copilots for document review and strategic planning, improving billable-hour productivity. Compliance frameworks under ISO 27001 and SOC 2 push demand for copilots that log each suggestion for audit.

Rise of Low-Code Cognitive Service Marketplaces

Low-code marketplaces let business users assemble cognitive AI workflows through drag-and-drop tools, closing talent gaps in the Asia Pacific. Network effects emerge as enterprises share pre-built modules, cutting deployment times. Vendors integrate privacy-by-design principles to satisfy data-protection authorities. Citizen-developer momentum broadens the cognitive AI market beyond technical teams, especially in mobile-first economies.

Regulatory Mandates for Explainability in High-Risk AI

The EU AI Act compels transparent decision-making in healthcare, finance, and autonomous systems. Enterprises shift from black-box models to interpretable cognitive platforms that surface reasoning steps. FDA guidance on AI-enabled medical devices amplifies demand for explainable algorithms in diagnostics. ASEAN adopts similar principles, giving vendors global scale for compliant solutions.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of AI/ML ops talent | -2.1% | Global, acute in North America and EU | Medium term (2-4 years) |

| Escalating cost of GPU/ASIC supply cycles | -1.8% | Global, with supply chain dependencies on APAC | Short term (≤ 2 years) |

| Enterprise audit failure on synthetic-data provenance | -1.4% | EU, North America, with regulatory spill-over to APAC | Medium term (2-4 years) |

| Export-control frictions on advanced foundation models | -1.2% | Global, with acute impact on US-China technology transfer | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of AI/ML Operations Talent

Eighty percent of AI projects stall during deployment because operational expertise lags behind model development. Mid-market firms lose bidding wars for scarce engineers, slowing cognitive AI implementation. Managed-service contracts grow as enterprises outsource monitoring and model retraining. The talent gap narrows only as universities revamp curricula and vendors automate DevOps workflows.

Escalating Cost of GPU/ASIC Supply Cycles

Advanced chips are concentrated in a few Asia Pacific foundries, exposing global buyers to supply shocks and price spikes [4]Nikkei Asia, “Chip Supply Bottlenecks Threaten AI Growth,” asia.nikkei.com . Capital-intensive workloads become unaffordable for smaller enterprises, delaying large-scale cognitive AI rollouts. Vendors respond with optimized small language models that run on commodity hardware. Edge-focused architectures also reduce reliance on centralized compute.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Amid Platform Maturity

Services topped the growth leaderboard with a 27.02% CAGR outlook, even though platforms retained 39.12% of 2024 revenue. The cognitive AI market benefits as enterprises seek integration know-how rather than raw software licenses. Professional-service units guide data-migration, model validation, and regulatory alignment, offsetting the shortage of in-house AI talent. Managed-service contracts add recurring revenue that smooths vendor cash flow. Vendors with consulting depth secure larger wallet share and cross-sell platform modules.

Hybrid service models now bundle software subscriptions with outcome-based guarantees. Clients pay for uptime, accuracy, or cost savings, aligning incentives on measurable results. This shift blurs lines between software and services, a pattern evident in IBM’s USD 6 billion AI revenue where consulting uplifted platform usage. As clients renew, vendors harvest telemetry that feeds product roadmaps, reinforcing competitive moats.

By Technology: Machine Learning Accelerates Beyond NLP Dominance

Natural-language processing held 42.24% cognitive AI market share in 2024; however, machine and deep learning are growing at 27.56% CAGR through 2030. Enterprises shift from conversational use cases toward autonomous decision frameworks that predict, recommend, and act. Computer-vision workloads gain traction in quality control and shopper analytics pilots. Automated reasoning systems address scenarios with incomplete data, critical for financial-risk modeling, where regulations demand traceable logic.

Integrated platforms that blend NLP, vision, and reasoning reduce vendor sprawl. Microsoft Azure AI serves 53,000 customers who prefer unified toolchains across domains. As models converge, vendors emphasize explainability dashboards to satisfy regulators. Technological convergence favors providers with research pipelines that span multiple AI paradigms and hardware optimizations.

By Application: Customer Service Transforms Business-Intelligence Leadership

Business-intelligence stacks led with 22.11% share of the cognitive AI market size in 2024, yet customer-service bots are tracking a 26.96% CAGR to 2030. Voice and chat agents shorten response times and lift Net Promoter Scores across retail and telecom. Cognitive fraud-detection engines scan real-time transactions, reducing false positives that burden compliance teams. Marketing automation suites personalize campaigns using behavioral predictions, driving revenue per user.

Supply-chain orchestration platforms adopt cognitive AI to flag disruption risks and scout optimal shipping lanes. End-users prefer applications that surface plain-language explanations alongside predictions, easing stakeholder trust. Vendors capitalize by offering modular APIs that plug into existing CRM and ERP systems, minimizing integration overhead.

By End-User Industry: Retail Disrupts BFSI Incumbency

BFSI retained a 24.85% share in 2024, anchored by risk analytics and robo-advisory services. Retail and e-commerce, however, are racing ahead at a 28.71% CAGR, powered by hyper-personalization mandates. Virtual stylists and dynamic-pricing engines showcase real-time inference benefits. Healthcare and life sciences deployments expand through FDA-aligned diagnostic aids that promise quicker time-to-diagnosis. Manufacturing plants leverage predictive maintenance to reduce downtime.

Government and defense orders soared after the Pentagon earmarked USD 15 billion for agentic AI, rewarding vendors with security clearances. Vertical specialization becomes pivotal; vendors embed regulatory logic into pre-trained models, lowering client compliance costs. Cross-industry learnings accelerate product cycles as use cases converge on explainability, cost control, and edge deployment.

Geography Analysis

North America commanded 37.45% cognitive AI market share in 2024 and remains a revenue anchor, yet talent shortages and hardware costs erode its lead. Government contracts and mature enterprise ecosystems sustain demand, but export-control rules limit global monetization of U.S. models. Edge-optimized offerings gain popularity as companies manage rising cloud bills.

Asia Pacific is rising at a 27.12% CAGR and could eclipse North America before 2030. China’s goal of publishing 50 national AI standards by 2026 ensures regulatory certainty that accelerates deployments. Japan favors voluntary guidelines, supporting agile experimentation. India’s national AI strategy cultivates talent pipelines, making the region a development and cost-optimization hub.

Europe grows steadily on the back of the EU AI Act, which prioritizes explainable cognitive systems. Organizations view transparency as a competitive differentiator. The Middle East and Africa explore leapfrog strategies that bypass legacy IT with AI-native services, particularly in telecom. Latin America adopts cognitive AI for customer-service improvements but still battles infrastructure gaps. The geographic mosaic underscores a multipolar trajectory for the cognitive AI market.

Competitive Landscape

The cognitive AI industry features moderate fragmentation, with incumbents such as IBM, Microsoft, and Google competing against agile startups. Patent analysis shows Tencent holding 2,074 generative-AI patents, while IBM leads in overall AI filings, revealing East-West asymmetry. Vendors move toward vertical integration: platform giants acquire niche players, and consulting firms develop proprietary stacks. Edge-first challengers exploit small-language models that run on off-the-shelf chips, appealing to privacy-sensitive sectors.

Explainability tools now serve as table stakes because regulators require traceable logic in high-risk applications. Service-heavy go-to-market models gain favor as enterprises outsource complex operations. Competitive intensity sharpens around hybrid deployments that span cloud and edge to meet data-sovereignty rules. Market entrants that show domain expertise and compliance readiness secure premium pricing despite price wars in commoditized compute.

Cognitive AI Industry Leaders

IBM Corporation

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Pentagon awarded USD 200 million in agentic-AI contracts to Anthropic, Google, xAI, and OpenAI under a broader USD 15 billion program.

- May 2025: OpenAI raised USD 40 billion in capital to fund cognitive AI research and projected USD 100 billion ARR by 2027.

- February 2025: ASEAN issued expanded AI governance guidelines that streamline cross-border deployments for vendors.

- September 2024: Oracle embedded more than 50 AI agents into Fusion Cloud, making cognitive functionality native to its SaaS suite.

- July 2024: China’s Ministry of Industry and Information Technology published guidelines to create 50 national AI standards by 2026, clarifying cognitive AI compliance pathways.

Global Cognitive AI Market Report Scope

| Platforms | |

| Services | Professional Services |

| Managed Services |

| Natural Language Processing |

| Machine and Deep Learning |

| Computer Vision |

| Automated Reasoning and Planning |

| Others |

| Business Intelligence and Analytics |

| Customer Service and Support |

| Risk and Fraud Detection |

| Sales and Marketing |

| Supply-Chain Management |

| Other Applications |

| BFSI |

| IT and Telecommunication |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Defense |

| Other End User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Platforms | ||

| Services | Professional Services | ||

| Managed Services | |||

| By Technology | Natural Language Processing | ||

| Machine and Deep Learning | |||

| Computer Vision | |||

| Automated Reasoning and Planning | |||

| Others | |||

| By Application | Business Intelligence and Analytics | ||

| Customer Service and Support | |||

| Risk and Fraud Detection | |||

| Sales and Marketing | |||

| Supply-Chain Management | |||

| Other Applications | |||

| By End-User Industry | BFSI | ||

| IT and Telecommunication | |||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Government and Defense | |||

| Other End User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is cognitive AI projected to grow between 2025 and 2030?

The segment shows a 26.74% CAGR, rising from USD 33.78 billion in 2025 to USD 110.45 billion by 2030.

Which region is expected to post the strongest expansion in cognitive AI deployments?

Asia Pacific carries a 27.12% CAGR outlook as China, Japan, and ASEAN markets standardize regulations and scale infrastructure.

What is driving enterprises to adopt edge-ready cognitive AI solutions?

Data-localization mandates and lower latency requirements push organizations toward hybrid cloud-edge architectures running small language models.

Why are services outpacing platforms in revenue growth?

Firms need integration, monitoring, and compliance expertise, making services the fastest-growing component at a 27.02% CAGR.

Which end-use sector is advancing the quickest?

Retail and e-commerce applications lead with a 28.71% CAGR as brands invest in hyper-personalized customer-engagement engines.

What supply-side hurdle could slow near-term adoption?

Limited GPU/ASIC capacity and rising chip prices constrain large-scale deployments, especially for mid-sized enterprises.

Page last updated on: